")

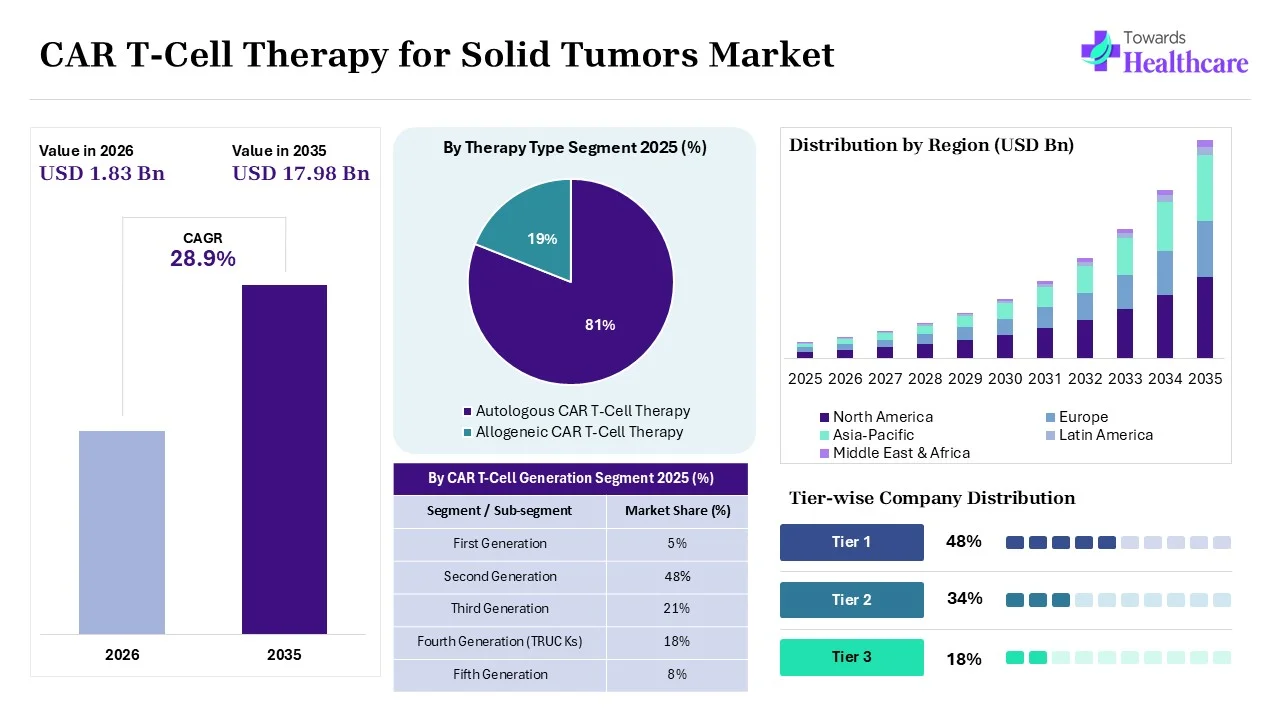

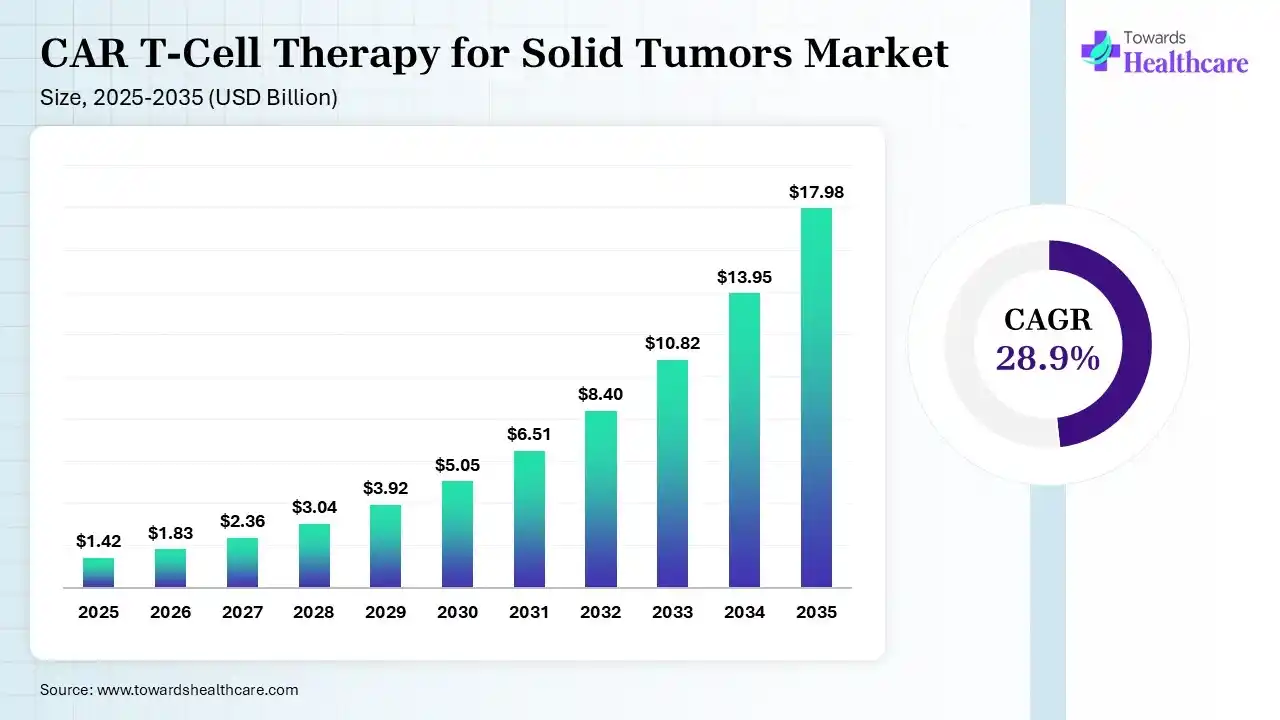

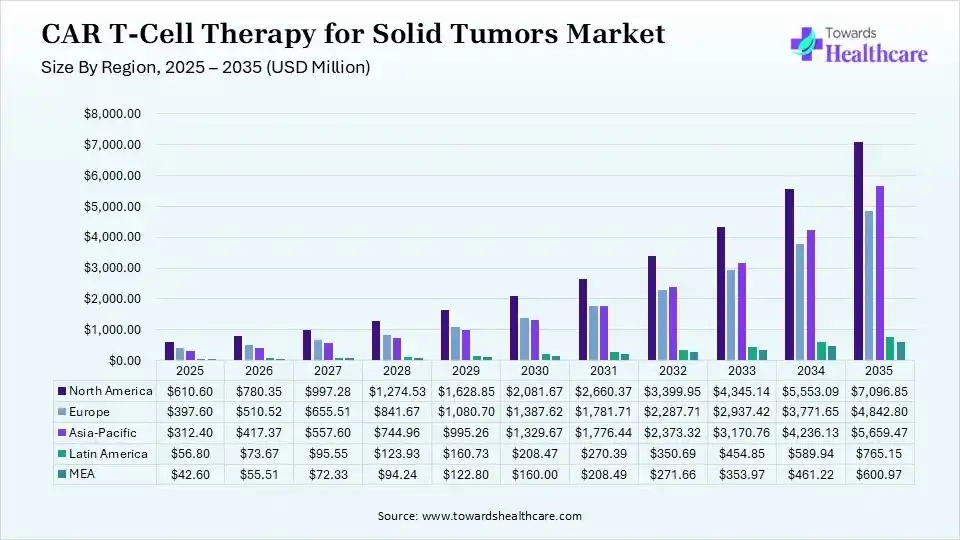

The global CAR T-cell therapy for solid tumors market size is calculated at USD 1.42 billion in 2025, driven by ideal R&D funding, advancements in tumor antigen targeting, & next-generation gene editing platforms. The market continues to grow USD 1.83 billion in 2026 due to technological innovation focused on bypassing the immunosuppressive tumor microenvironment & tackling antigen heterogeneity. It is expected to reach USD 17.98 billion by 2035, expanding at a CAGR of 28.9% as continued ‘armored’ CAR designs, off-the-shelf therapies, & combination treatments. North America held a 43% share of the market in 2025 due to the largest clinical trial ecosystem & robust biotech investment.

Generally, these kinds of therapies are highly customised immunotherapies, in which researchers engineer patients’ T-cells genetically in a lab to target specific proteins on their cancer cells. The CAR T-cell therapy for solid tumors market has been broadening across the globe, due to the increased demand for curative or durable alternatives for cancers, such as glioblastoma, pancreatic, & breast cancers. Gradual developments are covering significant private & public funding to unveil new targets, like HER2, EGFR, GD2, & mesothelin, into modern clinical assessment.

With a focus on resolving obstacles of tumors, researchers are developing novel therapies that can administer cells directly to the tumor site, i.e., either by intracavitary or intratumoral injections. For this, they have employed armored T-cells that enable the degradation of immunosuppressive stromal tissue. Day by day, many studies are transitioning towards in vivo CAR-T technologies, like leveraging antibody-drug conjugates to speed up CAR-T generation directly inside the patient, which substantially lowers waiting times & the reliance on complex hospital infrastructure.

The era has been increasingly pushing AI algorithms across the diversity of pharmaceuticals, including CAR-T cell therapy. Whereas leading researchers are widely employing Large Language Models (LLMs) & unified single-cell sequencing datasets to assess thousands of antigens. AI assists in nominating & prioritising highly specific targets that are active in solid tumors but spared in healthy tissues. On the other hand, the adoption of machine learning algorithms & deep learning models is exploring computational engineering & optimization of the chimeric receptors themselves. This leads to ultra-sensitive receptors capable of determining antigens at 10 to 50 times lower concentrations than conventional constructs.

Inclining towards Dual-Targeting & Logic Gates

The market has been emphasising the elimination of antigen heterogeneity, while novel CAR-T designs use dual targets. This pushes cancer cells to express multiple mutations to evade the immune system.

Promoting Combination Therapies

The trend is becoming a combination of CAR-T infusions with radiotherapy, targeted therapies, or immune checkpoint blockades to enhance tumor destruction.

Exploration of Next-Gen Cell Platforms

In this era, researchers are seeking beyond conventional T-cells by engineering CAR-NK (i.e., Natural Killer cells), CAR-Macrophages (CAR-Ms), & virus-specific T-cells to circumvent a dense tumor environment.

| Table | Scope |

| Market Size in 2026 | USD 1.42 Billion |

| Projected Market Size in 2035 | USD 17.98 Billion |

| CAGR (2026 - 2035) | 28.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Target Antigen, By Tumor Type, By CAR T-Cell Generation, By Therapy Type, By Delivery Route, By End User, By Development Stage, By Region |

| Top Key Players | CARsgen Therapeutics, BioNTech, Autolus Therapeutics, Gilead Sciences (Kite Pharma), Novartis, Legend Biotech, Bristol Myers Squibb (BMS), Atara Biotherapeutics, Noile-Immune Biotech, Immatics |

")

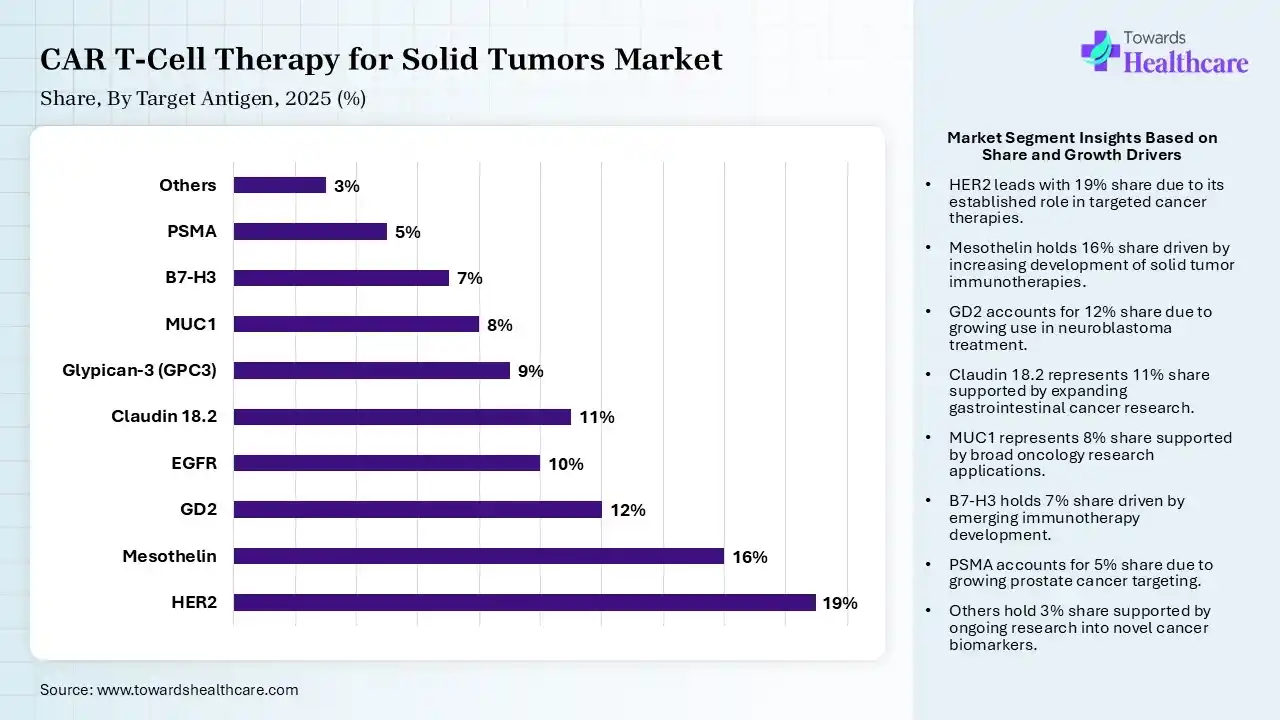

| Segment | Share 2025 (%) |

| HER2 | 19% |

| Mesothelin | 16% |

| GD2 | 12% |

| EGFR | 10% |

| Claudin 18.2 | 11% |

| Glypican-3 (GPC3) | 9% |

| MUC1 | 8% |

| B7-H3 | 7% |

| PSMA | 5% |

| Others | 3% |

The HER2 Segment Led the Market in 2025

In 2025, the HER2 segment held the largest share of 19% of the CAR T-cell therapy for solid tumors market. Primarily, this acts as a tumor-associated antigen target rather than just a traditional biological growth factor. Further dominance is propelled by a rise in cases of HER2-expressing cancers, such as breast, gastric, and ovarian, with the need to overcome tumor microenvironment (TME) immunosuppression. Expanding aims at boosting precision targeting to enhance effectiveness and drive the segmental growth.

The mesothelin segment captured the second-largest share of 16% of the market in 2025, due to the broader application in pancreatic & mesothelioma therapies. Also, its better tumor specificity is assisting the overall adoption. Various clinical trials are often joining MSLN-targeted CAR T-cells with immune checkpoint inhibitors & lymphodepleting chemotherapy.

The Claudin 18.2 (CLDN18.2) segment accounted for a 11% share in 2025 & is predicted to witness rapid expansion in the CAR T-cell therapy for solid tumors market. Respective growth is fueled by faster progress in gastric cancer programs, coupled with robust investment in Asia. Ongoing early clinical trials of this target antigen, like the trials assessing candidates, including CT041, have delivered strong clinical efficacy, objective response rates, & manageable safety profiles in heavily pre-treated patients.

Whereas the GD2 segment held a notable share of 12% of the market. This has been widely used in neuroectodermal tumors. Alongside, enhancements in CAR engineering are boosting persistence, with massive growth in pediatric oncology research, which fuels the overall adoption. Recent studies demonstrated that GD2 is highly expressed in DMGs, like Diffuse Intrinsic Pontine Gliomas (DIPG).

")

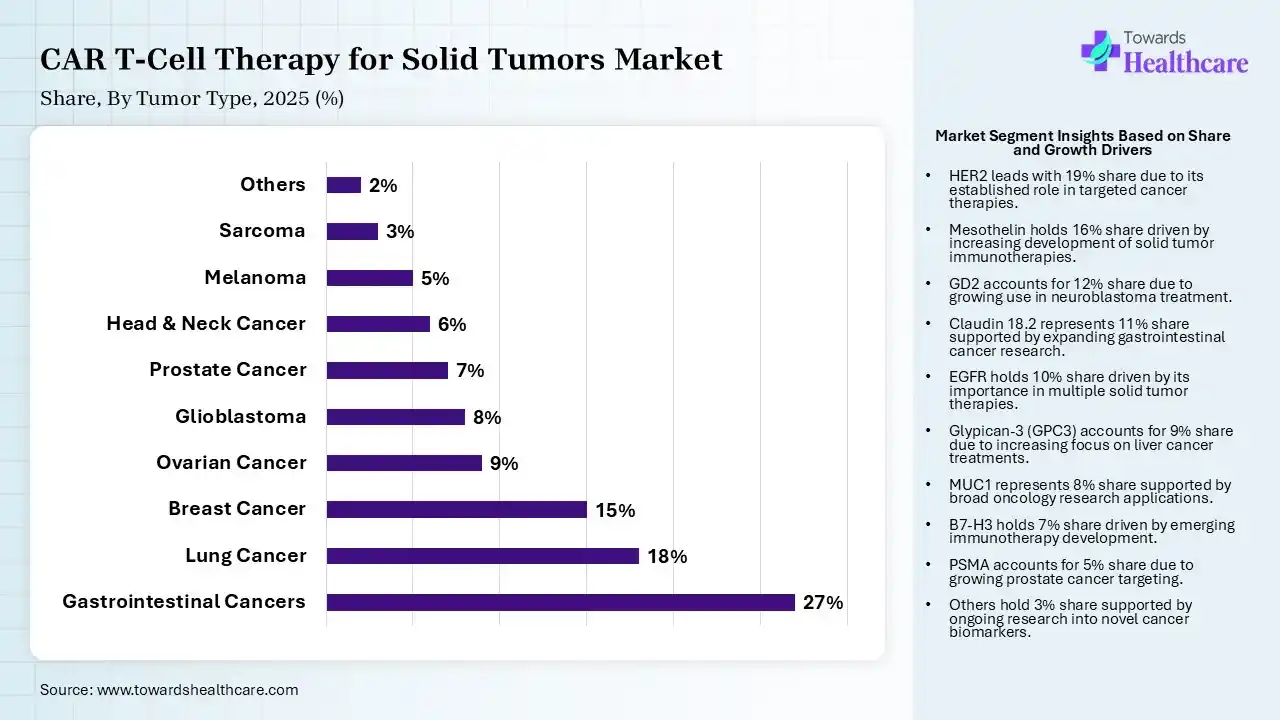

| Segment | Share 2025 (%) |

| Gastrointestinal Cancers | 27% |

| Lung Cancer | 18% |

| Breast Cancer | 15% |

| Ovarian Cancer | 9% |

| Glioblastoma | 8% |

| Prostate Cancer | 7% |

| Head & Neck Cancer | 6% |

| Melanoma | 5% |

| Sarcoma | 3% |

| Others | 2% |

The Gastrointestinal Cancers Segment Dominated the Market in 2025

In 2025, the gastrointestinal cancers segment led with a 27% share of the CAR T-cell therapy for solid tumors market. This mainly encompasses the esophagus, stomach, liver, pancreas, and colon/rectum that are propelled by an interplay of genetic mutations, chronic inflammation, & changing lifestyle factors. Prominent clinical trials are exploring GPC3 for hepatocellular carcinoma & CLDN18.2 for gastric cancer.

However, the lung cancer segment held the second-largest share of 18% in 2025, due to surging cases across the globe, driving trials. Alongside, innovative antigen discovery is further expanding the pipeline. A key catalyst also includes the urgent clinical need to treat advanced Non-Small Cell Lung Cancer (NSCLC) & Small Cell Lung Cancer (SCLC).

The breast cancer segment captured a 15% share of the market in 2025. A notable rise in instances of Triple-Negative Breast Cancer and vital R&D investments to overcome concerns are fueling the development of novel therapies for breast cancer. For these cases, the leading firms have been advancing HER2-targeted therapies expeditiously. Besides this, the world is highly demanding personalized medicine in these cases, which accelerates the greater adoption of CAR-T cell therapy.

The glioblastoma segment held an 8% share in 2025 & is estimated to expand fastest in the CAR T-cell therapy for solid tumors market. High mortality rate of brain cancers & the clinical need to overcome GBM-specific barriers, especially the blood-brain barrier (BBB), are fueling the demand for advanced therapies. Alongside, researchers are fostering the development of advanced local delivery that enhances the overall outcomes. Also, numerous global companies are encouraging brain tumor research with innovative CAR constructs.

")

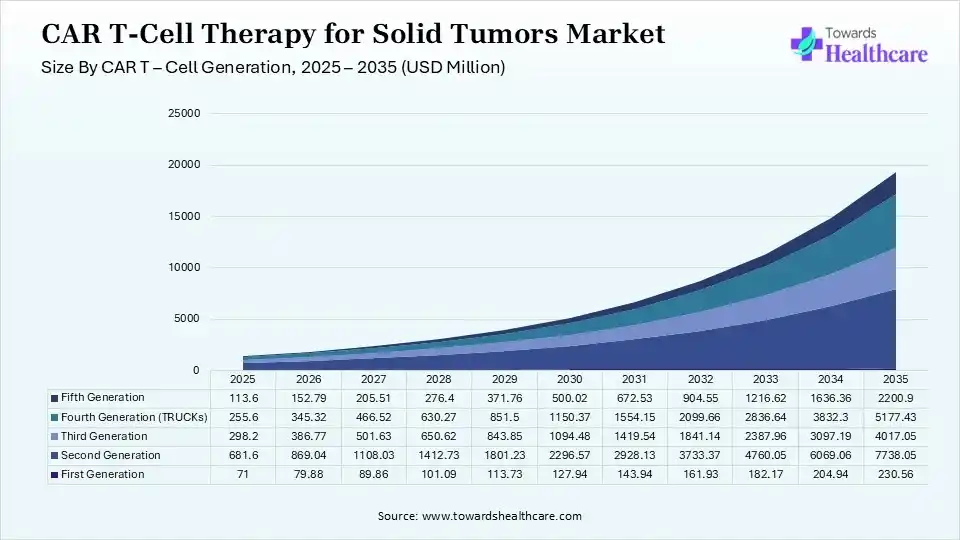

| Segment | Share 2025 (%) |

| First Generation | 5% |

| Second Generation | 48% |

| Third Generation | 21% |

| Fourth Generation (TRUCKs) | 18% |

| Fifth Generation | 8% |

The Second Generation Segment Was Dominant in the Market in 2025

The second generation segment dominated with a 48% share of the market in 2025. This generation is mainly serving as a foundational bedrock for next-generation constructs to fight against solid malignancies. Rising production expenditures & prolonged turnaround times for autologous second-generation therapies are forcing the market toward allogeneic, iPSC-derived CAR-T platforms.

The third-generation segment captured a 21% share of the CAR T-cell therapy for solid tumors market in 2025 due to its improved co-stimulation that enhances persistence. A surge in clinical validation & its better tumor killing properties are supporting the expansion. They highly leverage multiple signaling domains, like CD3ζ combined with CD28, 4-1BB, or OX40.

Moreover, the fourth generation (TRUCKs) segment held an 18% share in 2025 & is anticipated to expand fastest in the coming era. Specifically, cytokine release improves the tumour microenvironment. Additionally, cytokines generated by fourth-generation vectors act as a significant ‘third signal’ to mitigate T-cell exhaustion, massively increasing cell growth & persistence at the solid tumor site.

In 2025, the fifth-generation segment captured an 8% share of the market. This generation offers advanced signaling, which boost efficaciousness. Moreover, precision engineering across this generation is improving the comprehensive safety, & their progression has been bolstered by a rise in early-stage trials.

")

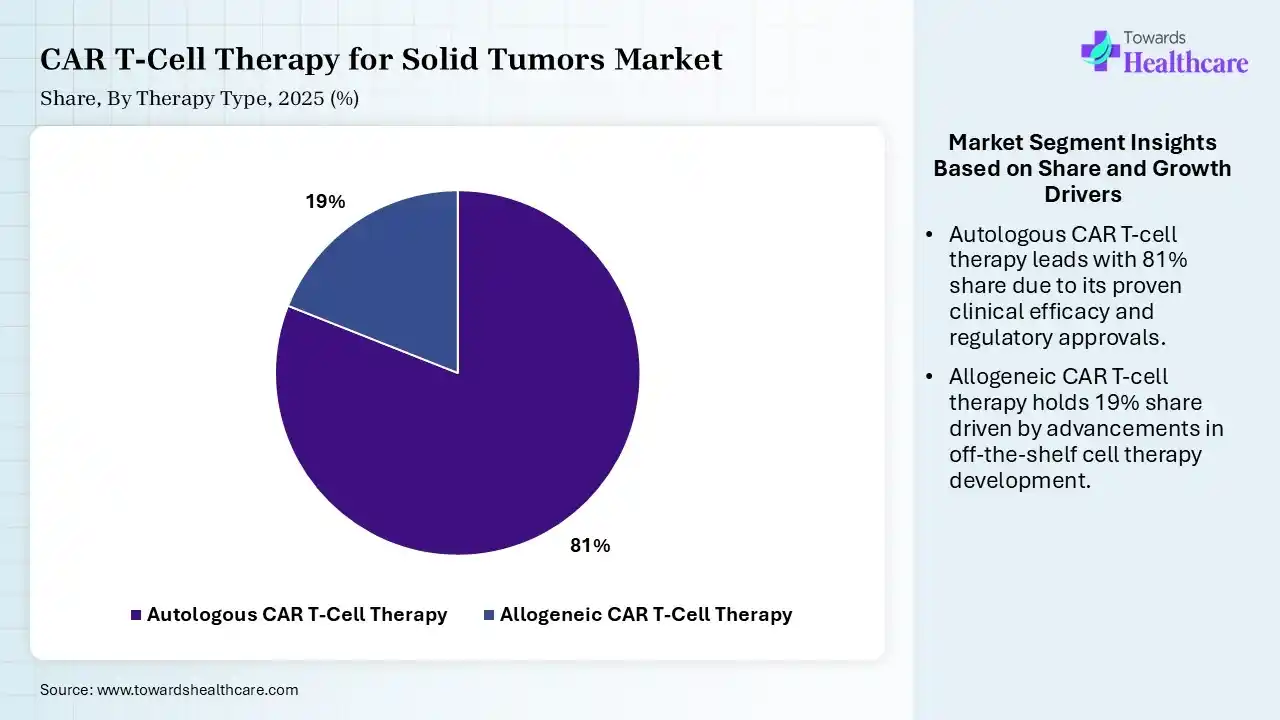

| Segment | Share 2025 (%) |

| Autologous CAR T-Cell Therapy | 81% |

| Allogeneic CAR T-Cell Therapy | 19% |

The Autologous CAR T-Cell Therapy Segment Held the Largest Share of the Market in 2025

The autologous CAR T-cell therapy segment led with an 81% share of the CAR T-cell therapy for solid tumors market in 2025. Growing clinical demand for precision oncology, with its ability to combat the risk of graft-versus-host disease (GvHD), is driving the adoption of this therapy. Continuous advances are promoting the pairing of these therapies synergistically with checkpoint inhibitors, chemotherapy, & oncolytic viruses to optimize cell trafficking & efficiency at the tumor site.

On the other hand, the allogeneic CAR T-cell therapy segment accounted for a 19% share in 2025 & is predicted to expand at a rapid CAGR. Especially, off-the-shelf production is reducing spending, and faster treatment availability is fueling their overall adoption. Consistent breakthroughs in gene editing, like deleting the T-cell receptor (TCR) to prevent GvHD and the CD52 gene to mitigate host rejection, are majorly propelling allogeneic therapeutics through clinical trials.

")

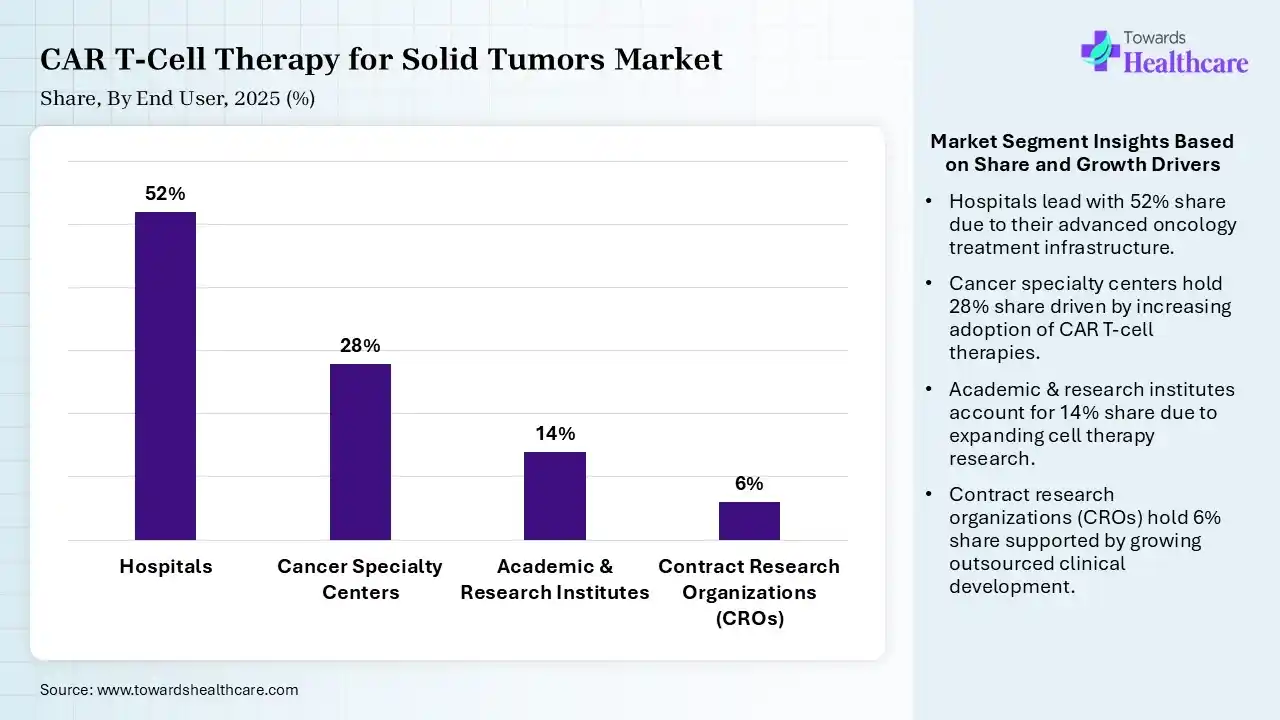

| Segment | Share 2025 (%) |

| Hospitals | 52% |

| Cancer Specialty Centers | 28% |

| Academic & Research Institutes | 14% |

| Contract Research Organizations (CROs) | 6% |

The Hospitals Segment Dominated the Market in 2025

In 2025, the hospitals segment held a dominant share of 52% of the CAR T-cell therapy for solid tumors market. Many hospitals are providing well-established oncology facilities, coupled with the expansion of clinical trials for armored CAR T-cells, logic-gated systems, and localized delivery. Day by day, the globe is demanding highly specialized facilities, including apheresis units, cryopreservation systems, and intensive care units, to manage acute toxicities like Cytokine Release Syndrome (CRS) that are extensively present in these hospital systems.

Whereas the cancer specialty centers segment captured a 28% share in 2025 & is estimated to register the fastest expansion in the coming years. These centers are highly offering specialized expertise that supports improvement in outcomes. Also, they are fostering diverse CAR T treatment programs, & also they have higher patient referrals. Also, centers are increasingly investing in the accommodation of advanced cellular products, like fifth-generation CARs, armored T-cells, and synthetic Notch receptors.

The academic & research institutes segment held a 14% share of the CAR T-cell therapy for solid tumors market in 2025. Respective growth is driven by their strong translation research, surging government funding, & continue pipeline innovation. Many major institutes are joining with biotech leaders to translate preclinical findings into commercial, multi-center trials.

The contract research organizations (CROs) segment captured a 6% share in 2025 due to increasing outsourcing, which accelerates the ongoing development. The worldwide clinical trials & partnerships among manufacturers are supporting the expansion of CROs. Also, they are highly using expertly guiding complex regulatory filings and ensuring compliance across changing international landscapes.

")

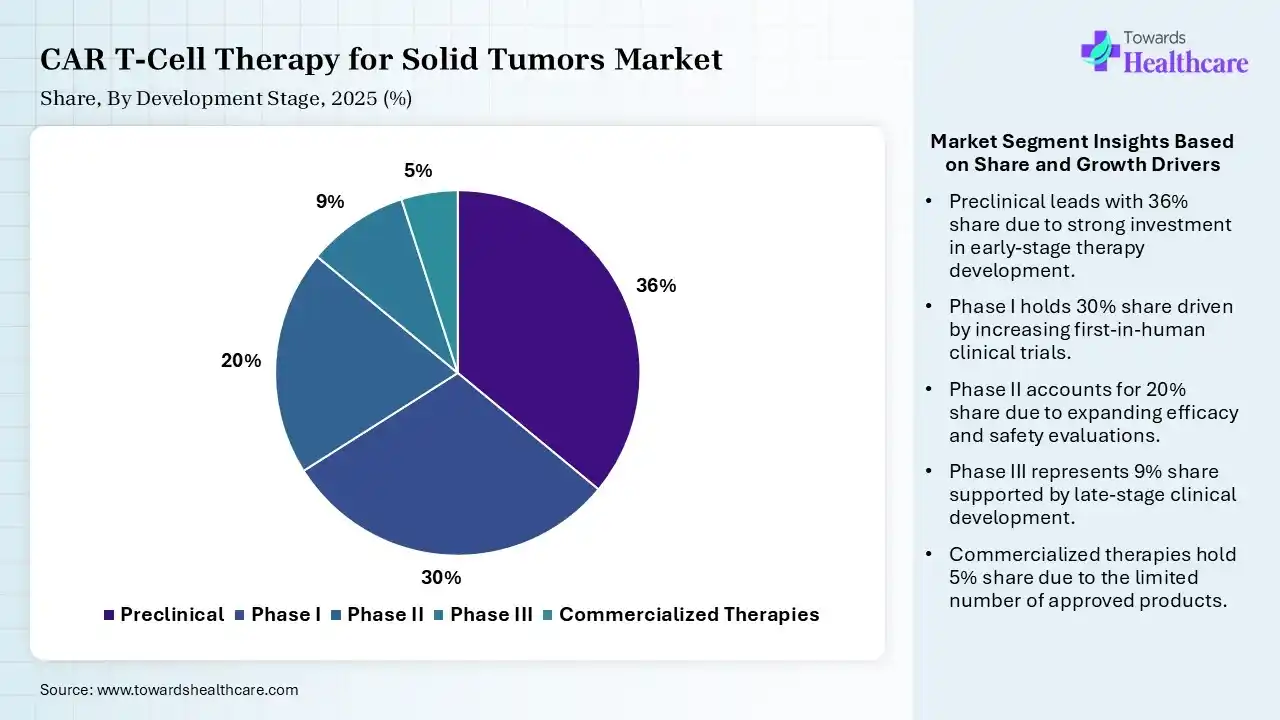

| Segment | Share 2025 (%) |

| Preclinical | 36% |

| Phase I | 30% |

| Phase II | 20% |

| Phase III | 9% |

| Commercialized Therapies | 5% |

The Preclinical Segment Was Dominant in the Market in 2025

In 2025, the preclinical segment registered dominance with a 36% share of the CAR T-cell therapy for solid tumors market. Several advanced preclinical models are ensuring the validation of receptors that are highly expressed in solid malignancies to skip ‘on-target, off-tumor’ toxicities. Key pharma & biotech firms are highly funding preclinical & early-stage pipeline assets to protect intellectual property.

Although the Phase I segment held the second-largest share of 30% in 2025, due to the growing number of first-in-human studies. Furthermore, the globally widening enrollment & positive early safety results are impacting the expansion of Phase I trials. Emerging funding is fostering this phase to find & target newer tumor-associated proteins, with non-protein targets like carbohydrate antigens.

The Phase II segment captured a 20% share of the CAR T-cell therapy for solid tumors market in 2025. Increasing efficacy validation & regulatory engagement are strengthening the development of this phase. With a focus on the fifth generation, the market is implementing platforms to recognize historical challenges, such as antigen escape, tumor-specific antigen scarcity, & T-cell exhaustion.

The Phase III segment held a 9% share in 2025 & is anticipated to expand rapidly in the market. Surging industrial investments, regulatory acceleration, & late-stage products approaching commercialization. The worldwide innovators in this phase are highly using localized delivery, like hepatic artery infusion (HAI), to bypass physiological barriers that earlier restricted T-cell infiltration.

")

North America captured a major share of 43% of the CAR T-cell therapy for solid tumors market in 2025. Rising oncology R&D investments, strong clinical trials pipelines, & rigorous regulatory frameworks are driving the regional dominance. Ongoing studies emphasise that in vivo approaches are highly leveraging lipid nanoparticles to modify T-cells directly inside the patient’s body, which significantly lowers treatment time & manufacturing expenses. Beyond solid tumors, detailed research activities are progressing CAR-T to treat severe autoimmune conditions, with clinical trials demonstrating potential for drug-free remission after a single infusion.

U.S. CAR T-Cell Therapy for Solid Tumors Market Trends

The U.S. market contributed to a major share of 37% in 2025, due to the largest biotech ecosystem & robust FDA support. A recent milestone effort covers a novel transatlantic trial funded by Cancer Grand Challenges that was unveiled across four US and UK sites to treat children and young adults with solid tumors. Also, it targets two markers simultaneously to enhance tumor entry & cytotoxicity.

Canada CAR T-Cell Therapy for Solid Tumors Market Trends

Canada held a 4% share of the CAR T-cell therapy for solid tumors market in 2025. Key drivers are the involvement of institutions, including the Tom Baker Cancer Centre in Alberta are developing the country's early-stage clinical trials targeting solid tumors. Health Canada is simplifying approval processes & pushing progressive provincial reimbursement models, making Canada an appealing hub for global biotech firms to test and launch new solid tumor therapies.

Asia Pacific held a 22% share in 2025 & is estimated to witness the fastest growth in the upcoming years. Day by day, APAC is fostering expedited biotechnology investments in the rapidly rising number of cancer cases. Also, many nations are promoting strong government assistance to accelerate commercialization. Pioneers, including Melbourne-headquartered Cartherics, are raising their position in the Asia Pacific region for their universal allogeneic stem cell therapies, with major patents received in China & Japan.

China CAR T-Cell Therapy for Solid Tumors Market Trends

China’s CAR T-cell therapy for solid tumors market accounted for an 11% share in 2025. China is expanding as a prominent of the global market by preserving regulatory approvals, like the landmark decision by the National Medical Products Administration (NMPA) that granted CARsgen Therapeutics approval for satricabtagene autoleucel (satri-cel) to treat gastric cancer. China has been delivering commercial CAR-T therapies, generally ranging from $120,000 to $220,000, a major reduction compared to Western markets.

India CAR T-Cell Therapy for Solid Tumors Market Trends

In 2025, India accounted for a 2% share of the market due to a massive rise in diverse cancer cases. Along with this, India’s local institutes, like the Tata Memorial Centre in Mumbai, are actively participating in global and domestic trial networks targeting solid tumors. Moreover, the strong Central Drugs Standard Control Organisation (CDSCO) & Indian regulatory bodies are simplifying the approval processes for gene and cell therapies.

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Company | Description |

| CARsgen Therapeutics | Their key product is satri-cel (zevorcabtagene autoleucel) for CLDN18.2-positive solid tumors, like gastric & pancreatic cancers. |

| BioNTech | A leading firm focuses on BNT211, an autologous CAR-T that targets the Claudin-6 (CLDN6) antigen in advanced solid tumors. |

| Autolus Therapeutics | Their offerings cover autologous CAR T-cell therapies for solid tumors, particularly for pediatric neuroblastoma. |

| Gilead Sciences (Kite Pharma) | This company is exploring the production of cellular therapy, with research in glioblastoma & identification of new tumor-associated targets. |

| Novartis | It is a developer of approved CAR T-cell treatments, with an emphasis on finding tumor-specific antigens & also allied with Legend Biotech to strengthen solid-tumor cell therapies. |

| Legend Biotech | Their major products are focusing on LB2102, targeting small-cell lung cancer & other difficult-to-treat solid malignancies. |

| Bristol Myers Squibb (BMS) | A leader is promoting investments in R&D for next-generation dual-targeting & allogeneic approaches for solid tumors. |

| Atara Biotherapeutics | This firm is unveiling the expansion of off-the-shelf, allogeneic CAR T-cell solutions & T-cell immunotherapies. |

| Noile-Immune Biotech | They are stepping into innovating next-generation CAR-T cells engineered with their proprietary PRIME technology. |

| Immatics | It is a clinical-stage biopharmaceutical company developing T-cell receptors (TCRs) & related engineered immunotherapies for various solid tumors. |

By Target Antigen

By Tumor Type

By CAR T-Cell Generation

By Therapy Type

By Delivery Route

By End User

By Development Stage

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar