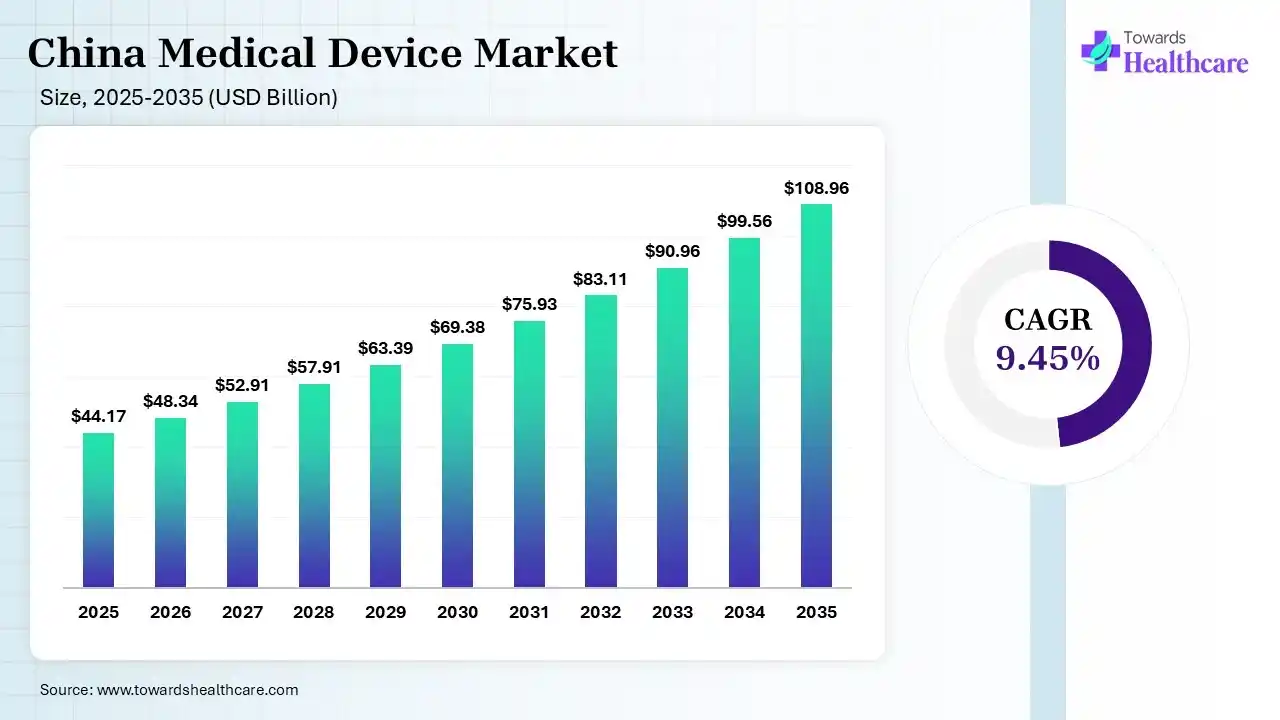

The China medical device market size was estimated at USD 44.17 billion in 2025 and is predicted to increase from USD 48.34 billion in 2026 to approximately USD 108.96 billion by 2035, expanding at a CAGR of 9.45% from 2026 to 2035. The Chinese medical device market is growing because of a rising aging population, increasing chronic diseases such as diabetes and cardiovascular diseases, and a shift toward home medical care.

")

The China medical device market is growing, as a medical device is any device designed to be applied for healthcare purposes. Noteworthy potential for hazards is inherent when using tools for medical purposes, and thus, medical devices are proven safe and operative. Medical devices vary in both their envisioned use and indications for use. Healthcare devices are used for the precise purposes of diagnosis and treatment of disease. A healthcare device is an apparatus, instrument, appliance, material, or other devices which is used for prevention, diagnosis, monitoring, treatment, or alleviation of a health condition. A medical device is any instrument used to diagnose a health condition, prevent illness, help healing, prevent conception, alleviate incapacity, substitute anatomy, or physiological technology. In China, 126,139 registered medical device products and 163,489 filing certificates were issued across the country.

AI-driven technology in medical devices is transforming worldwide healthcare systems in the regulation, reimbursement, and manufacturing development, becoming a significant driver of structural revolution. AI-based technology shows up most prominently in healthcare imaging, where it helps improve diagnostic accuracy. AI-based technologies have the potential to transform health care by deriving novel and significant insights from the massive amount of data generated through the delivery of health care. The incorporation of AI-based technology in healthcare devices brings transformative potential to healthcare, enhancing patient outcomes and creating novel possibilities for treatment and diagnostics. AI-based technology integration in medical devices is increasing advanced innovation in diagnostics, modified medicine, and operational accuracy.

The medical devices industry is transforming from import reliance to a worldwide hub, driven by novelty, digital incorporation, and government initiatives. The recent development in medical care device technology has created the opportunity to produce more convenient, less invasive, and more targeted medical devices that are mass-produced while maintaining affordable efficiency. Advancements in 3D printing technology enable producers to overcome traditional challenges during fabrication and create a recent wave of wearable medical devices.

Wearables Devices Monitoring:

Wearable devices equipped with safety features like GPS tracking, proximity sensors, and alert systems significantly improve workplace safety. Wearable sensors are redefining health and wellness, performance nursing by allowing continuous, non-invasive measurement of biochemical

Internet of Medical Things:

The Internet of Things in medical care is the use of internet-connected tools to gather and share patient data automatically. This technological integration is driving real-time health monitoring and holds significant potential for improving healthcare delivery.

Robotic Surgery Expansion:

Next-generation robotic surgery offers enhanced accuracy and control it offer. The robotic instrument’s ability to translate the surgeon's movements with a high degree of precision, integrating with enhanced visualization through three-dimensional imaging.

Remote Patient Monitoring (RPM):

Recent advancements in RPM, access to care, and changes in health status have been addressed rapidly to avoid crisis and expensive hospital admissions and readmissions.

| Table | Scope |

| Market Size in 2026 | USD 48.34 Billion |

| Projected Market Size in 2035 | USD 108.96 Billion |

| CAGR (2026 - 2035) | 9.45% |

| Key Applications | Diagnostic Imaging, In-Vitro Diagnostics (IVD), Cardiovascular Care, Orthopedics, Diabetes Management, Robotic Surgery, Remote Patient Monitoring, Home Healthcare |

| Primary End Users | Hospitals, Ambulatory Surgery Centers (ASCs), Clinics, Diagnostic Laboratories, Home Healthcare Providers |

| Key Growth Drivers | Aging population, rising chronic diseases, healthcare infrastructure expansion, AI integration, domestic manufacturing support, digital health adoption |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By Nutritional Content |

| Top Key Players | Shinva Medical Instrument, Neusoft Medical, Wego Group |

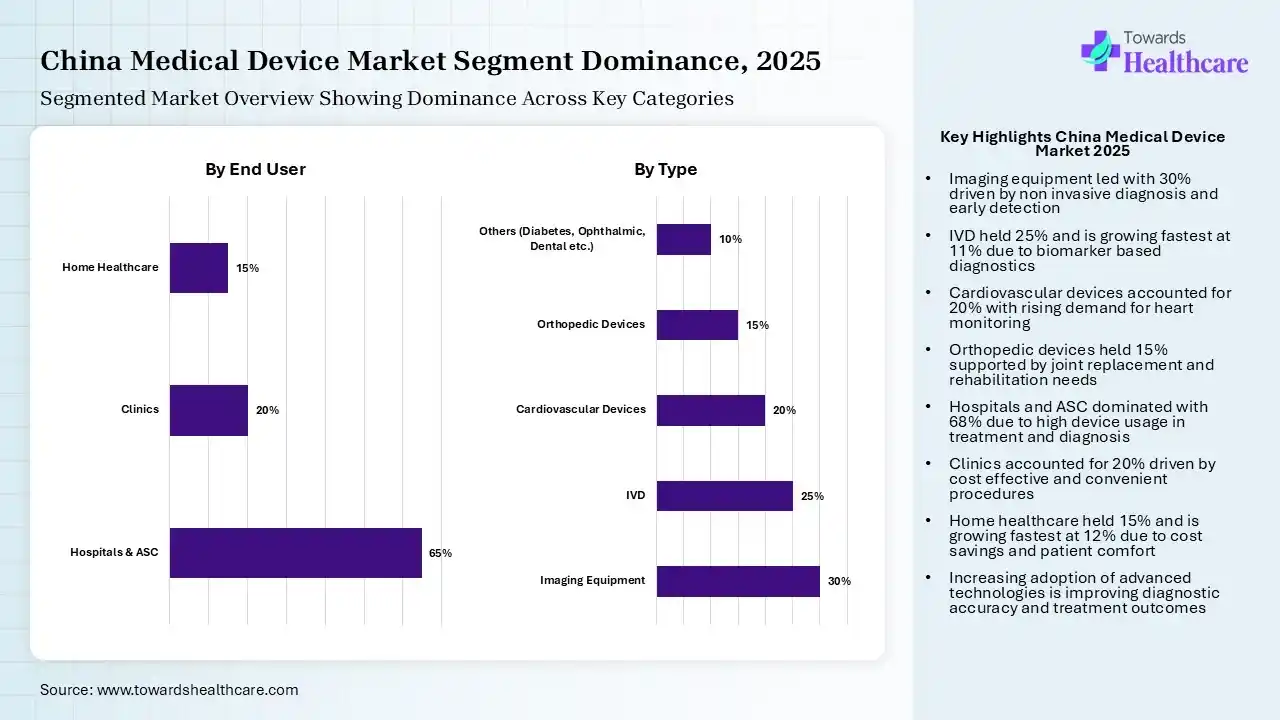

| Segment | Share 2025 (%) |

| Imaging Equipment | 30% |

| IVD | 25% |

| Cardiovascular Devices | 20% |

| Orthopedic Devices | 15% |

| Others (Diabetes, Ophthalmic, Dental etc.) | 10% |

The Imaging Equipment Segment Led the China Medical Device Market in 2025

The imaging equipment segment contributed the largest market share of 30% in 2025, as medical device imaging apparatus involves painless, non-invasive technology, early and precise diagnoses, helps in surgical planning, and more cost-effective health care via early diagnosis. Medical imaging apparatus involves the application of a machine to take images of the inside of an individual's body without invasive surgery.

The IVD segment held the second-largest share of 25% of the China medical device market, and is expected to grow at the fastest CAGR of 11% during the forecast period, as with IVD technologies, patients enhanced their understanding of their condition and made more informed healthcare decisions. It offers precise medical data that directly influences clinical decisions. IVDs identify biomarkers related to a broad array of diseases earlier symptoms.

The cardiovascular devices segment held a significant share of 20% of the market, as cardiac monitors enable patients to visit hospitals at their convenience, reducing their exposure to infectious surroundings. These devices have evolved as game-changers, providing a convenient and efficient means to monitor heart health.

The orthopedic devices segment held a significant share of 15% of the market in 2025, as advanced-quality orthopedic devices are intended to be durable and long-lasting, offering reliable help and function. They support or replace cartilage, muscles, joints, or bones, as well as the rehabilitation process post-surgery.

| Segment | Share 2025 (%) |

| Hospitals & ASC | 65% |

| Clinics | 20% |

| Home Healthcare | 15% |

Hospitals & ASC Segment Led the China Medical Device Market in 2025

The hospitals & ASC segment contributed the largest market share of 68% in 2025, as standardized healthcare devices reduce the challenges of human error in hospitals. Medical devices are considered an important component of health systems. It offers continue to increase as they're significant to prevent, diagnose, manage, and rehabilitate illnesses and diseases safely and effectively.

The home healthcare segment held a significant share of 15% the market, expected to grow at the fastest rate of 12% during the forecast period. As home health care allows consumers to recuperate in the ease and privacy of their own home, at an expense to savings of 36-50 % over hospitalization or nursing home confinement. Continuing at home means being near family and friends, people who provide loving care and support.

The clinics segment held a significant share of 20% of the China medical device market in 2025, as the convenience of actions done in a clinic treatment room over an operating room is a great time saver and significantly less costly. An orthopaedic clinic involves access to specialized devices and technology used in diagnosing and managing conditions.

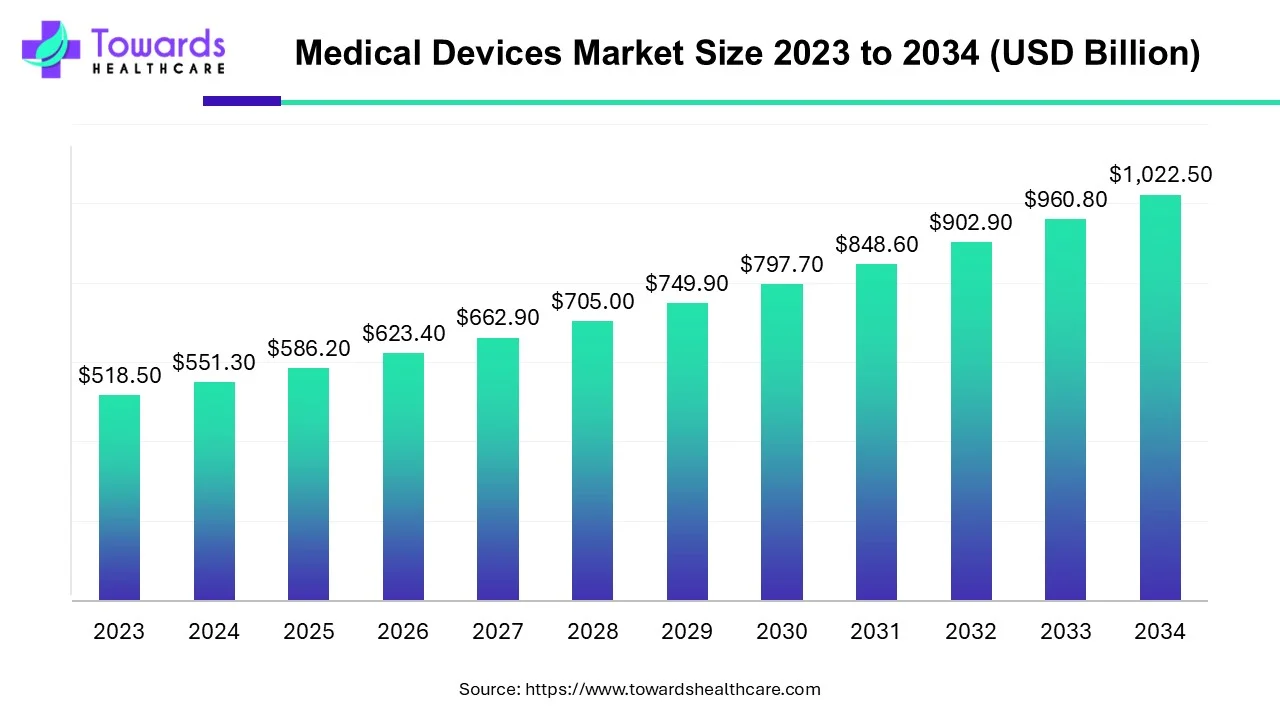

The global medical devices market size is calculated at USD 586.20 billion in 2025, grew to USD 623.37 billion in 2026, and is projected to reach around USD 1083.96 billion by 2035. The market is expanding at a CAGR of 6.34% between 2026 and 2035. Technological advancements and favorable government policies drive the market.

Key regions in China are driving medical device market growth through specialized industrial clusters and favorable local policies. The Bohai Rim, particularly Beijing, focuses on high-end R&D and innovative Class III devices, while the Yangtze River Delta (Shanghai/Jiangsu) operates as a major manufacturing hub for advanced consumables and imaging equipment. These areas provide infrastructure like the Suzhou Industrial Park to attract top firms.

The Pearl River Delta (Guangdong) excels in medical electronics, capitalizing on Shenzhen’s technology sector to develop AI and wearable devices. Meanwhile, Central China (Wuhan/Chengdu) supports expansion into regional markets, strengthening supply chain localization. Furthermore, Hainan’s Boao Lecheng pilot zone accelerates registration by allowing foreign devices, boosting regional innovation.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Mindray, United Imaging, Neusoft Medical | Develop imaging, monitoring, AI-enabled diagnostic technologies |

| Product Manufacturers | Mindray, WEGO, Lepu Medical, MicroPort, Shinva | Manufacture medical devices and healthcare equipment |

| Service Providers | Sinopharm Medical Devices, Shanghai Pharma Medical Devices | Distribution, maintenance, installation, support services |

| Platform Providers | Neusoft Medical, United Imaging Intelligence | AI-powered imaging and healthcare data platforms |

| CROs/CDMOs | WuXi AppTec, Pharmaron | Device testing, validation, regulatory support |

| Software Vendors | Neusoft Medical, United Imaging Intelligence | Medical imaging software and AI diagnostic solutions |

| Research Institutions | Chinese Academy of Medical Sciences, Peking Union Medical College, Tsinghua University | Device innovation, clinical research, validation |

| End-User Industries | Hospitals, ASCs, Clinics, Laboratories, Home Healthcare | Device deployment and utilization |

R&D:

Manufacturing Processes:

Patient Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 62% | 28% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Mindray Medical International | Shenzhen, Guangdong, China | China | China's largest medical device company with strong domestic and global presence | Patient Monitoring, Ultrasound, IVD Systems, Anesthesia Devices |

| GE HealthCare | Chicago, Illinois, USA | USA | Major supplier of imaging and diagnostic equipment across China | MRI, CT, Ultrasound, Molecular Imaging |

| Siemens Healthineers | Erlangen, Bavaria, Germany | Germany | Leading provider of imaging and laboratory diagnostics in China | MRI, CT, X-Ray, IVD Platforms |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lepu Medical Technology | Beijing, China | China | Major cardiovascular and interventional device manufacturer | Stents, Structural Heart Devices, Monitoring Systems |

| MicroPort Scientific | Shanghai, China | China | Strong position in cardiovascular and orthopedic devices | Coronary Stents, Orthopedic Implants, Surgical Robotics |

| WEGO Group | Weihai, Shandong, China | China | Large domestic medical consumables and equipment supplier | Consumables, Orthopedic Devices, Dialysis Products |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Shinva Medical Instrument | Zibo, Shandong, China | China | Growing domestic player in hospital equipment and sterilization | Surgical Equipment, Sterilization Systems |

| Edan Instruments | Shenzhen, Guangdong, China | China | Expanding global diagnostics and monitoring company | Ultrasound, ECG, Patient Monitoring |

| Yuwell Medical | Danyang, Jiangsu, China | China | Fast-growing home healthcare device provider | Oxygen Concentrators, Respiratory Care Devices |

Strengths

Weakness

Opportunities

Threat

By Type

By Nutritional Content

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar