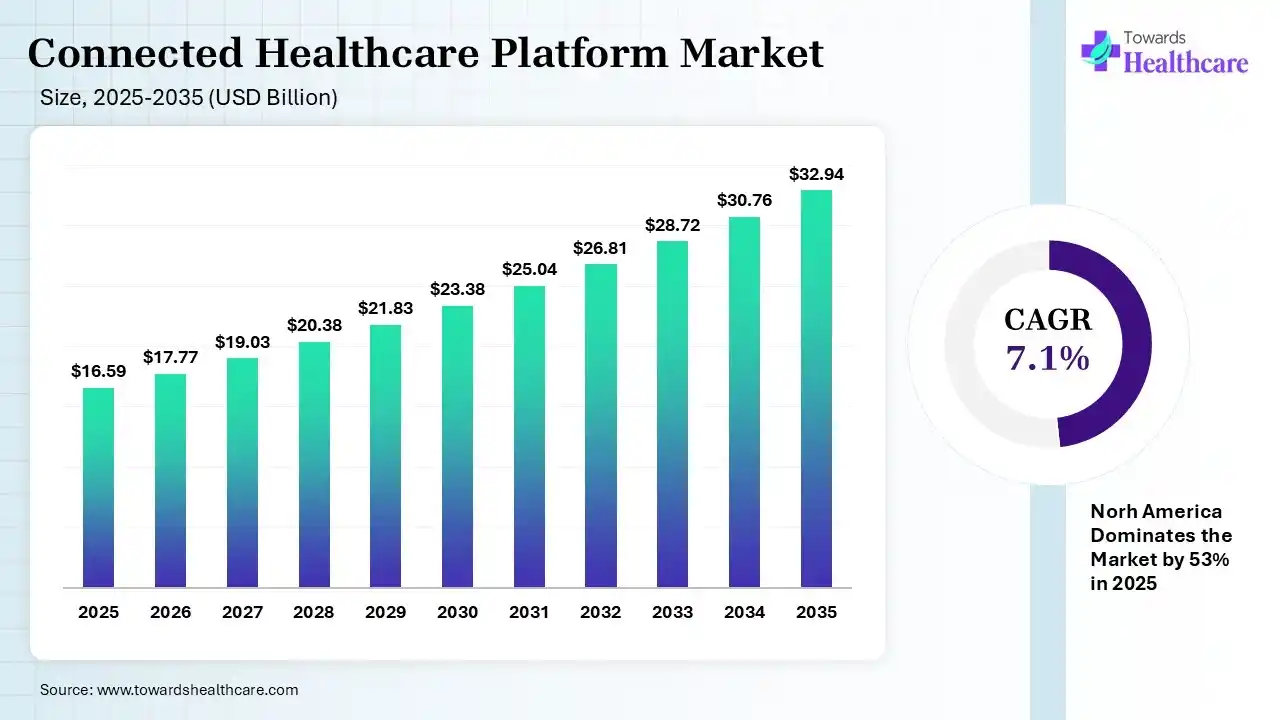

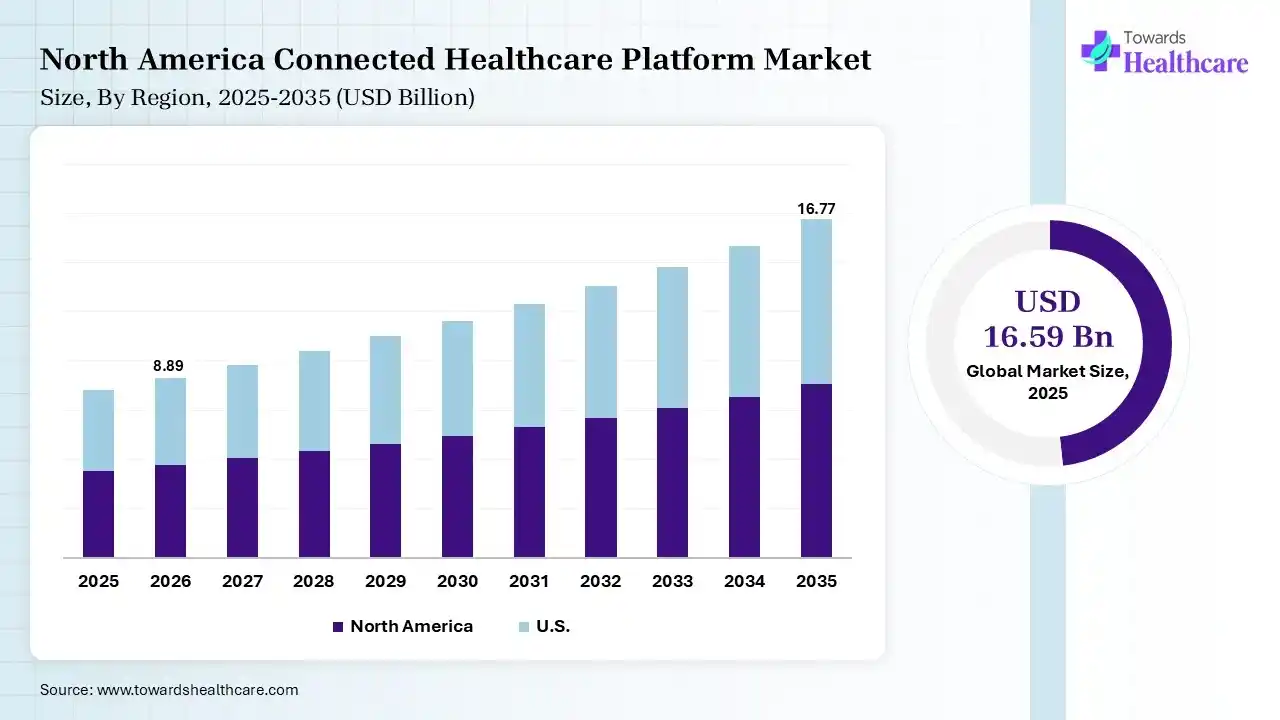

The global connected healthcare platform market size was estimated at USD 16.59 billion in 2025 and is predicted to increase from USD 17.77 billion in 2026 to approximately USD 32.94 billion by 2035, expanding at a CAGR of 7.1% from 2026 to 2035.

")

The market is witnessing steady growth, driven by increasing digitization, rising chronic disease burden, and demand for real-time patient monitoring. Integration of IoT, AI, and cloud technologies is enhancing care delivery, improving efficiency, and supporting data-driven clinical decisions.

A connected healthcare platform is a digital system that integrates medical devices, patient data, and healthcare services in real-time, enabling seamless communication between patients, doctors, and providers for better monitoring, diagnosis, and care delivery. The connected healthcare platform market is growing rapidly due to increasing demand for remote patient monitoring and the rising prevalence of chronic diseases. Technological advancements in IoT and cloud computing enable real-time data exchange and improved decision-making. Additionally, the shift toward patient-centric care, expanding telehealth adoption, and supportive government initiatives are driving adoption. Healthcare providers are increasingly investing in digital solutions to enhance efficiency, reduce costs, and improve overall patient outcomes.

| Year | % of Global deaths from Chronic Diseases |

| 2023 | 74% |

| 2024 | 75% |

AI can revolutionize connected healthcare platforms by enabling predictive analytics, early disease detection, and personalized treatment plans. It enhances real-time patient monitoring through smart algorithms that analyze continuous health data. AI-driven automation improves clinical workflows, reduces human errors, and speeds up decision-making. Additionally, virtual assistants and chatbots enhance patient engagement, while data insights help healthcare providers deliver more efficient, proactive, and outcome-focused care.

Growth of Remote Patient Monitoring (RPM)

The demand for remote patient monitoring is rising due to increasing chronic diseases and a preference for home-based care. Connected devices enable continuous tracking, reduce hospital visits, and support timely medical interventions, improving overall patient outcomes.

Rising Adoption of Telehealth Services

Telehealth is becoming a core component of connected healthcare platforms, enabling virtual consultations and improved access to care. It reduces geographical barriers, lowers healthcare costs, and enhances convenience for both patients and providers.

Focus on Interoperability and Data Security

Healthcare systems are prioritizing seamless data integration across platforms to improve coordination and efficiency. At the same time, strong data security measures are being implemented to protect sensitive patient information and ensure compliance with regulatory standards.

| Table | Scope |

| Market Size in 2026 | USD 17.77 Billion |

| Projected Market Size in 2035 | USD 32.94 Billion |

| CAGR (2026 - 2035) | 7.1% |

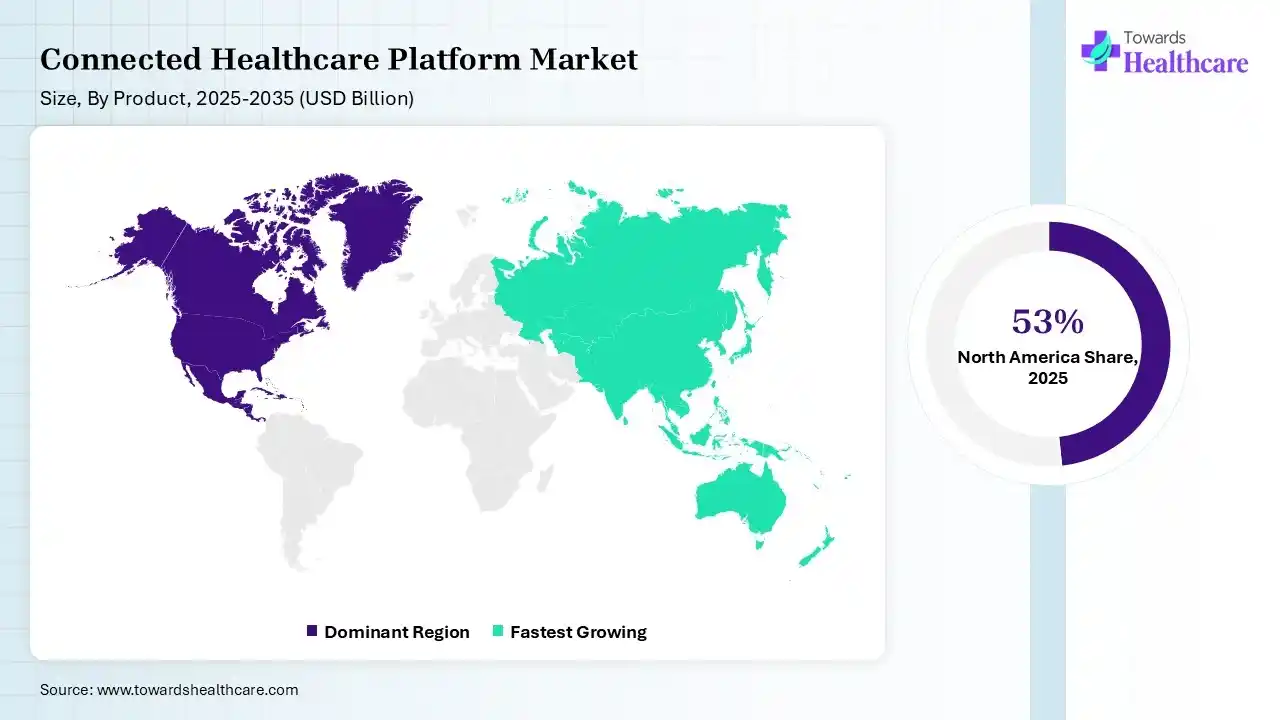

| Leading Region | North America by 53% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Solution Type, By Deployment Mode, By End-use, By Region |

| Top Key Players | ZS, Cognizant, IQVIA, GlobalLogic Inc, NTT DATA Group, Epic Systems Corporation, Cerner, Athenahealth |

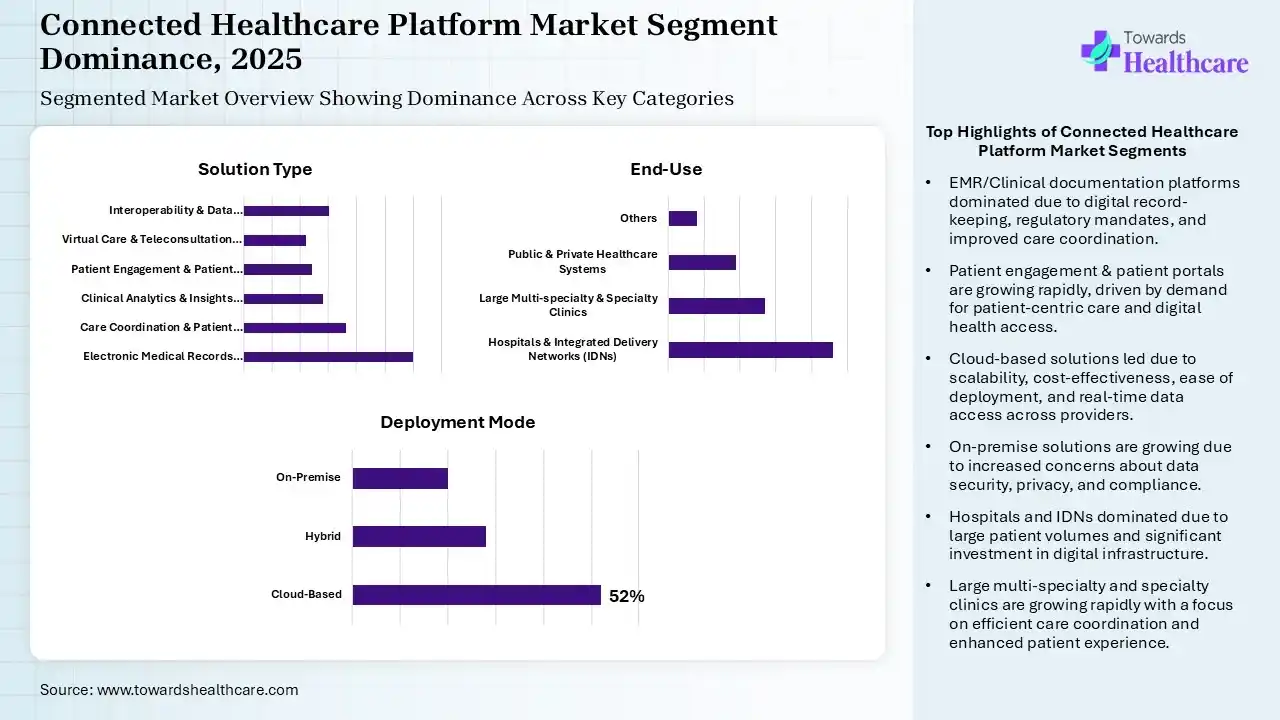

Why Did the Electronic Medical Records (EMR)/Clinical Documentation Platforms Segment Dominate in the Connected Healthcare Platform Market in 2025?

| Segment | Share 2025 (%) |

| Electronic Medical Records (EMR) / Clinical Documentation Platforms | 30% |

| Care Coordination & Patient Journey Management | 18% |

| Clinical Analytics & Insights Platforms | 14% |

| Patient Engagement & Patient Portals | 12% |

| Virtual Care & Teleconsultation Modules | 11% |

| Interoperability & Data Integration Layer | 15% |

Explanation

The electronic medical records (EMR)/clinical documentation platforms segment dominated the market by 30% in 2025 due to widespread adoption of digital record-keeping and regulatory mandates for health data management. These systems mandate health data management. These systems enable centralized patient information, improve clinical efficiency, and support seamless data sharing across providers. Their role in enhancing care coordination, reducing errors, and streamlining workflows has made them a core component of connected healthcare infrastructure.

Patient Engagement & Patient Portals

The patient engagement & patient portals segment is expected to grow at the fastest CAGR due to increasing demand for patient-centric care and digital health access. These platforms empower patients with easy access to medical records, appointment scheduling, and communication with providers. Rising smartphone usage, growing awareness of self-care, and the need for improved healthcare transparency and convenience are driving rapid adoption across healthcare systems.

What Made the Cloud-Based Segment Dominant in the Connected Healthcare Platform Market in 2025?

| Segment | Share 2025 (%) |

| Cloud-Based | 52% |

| Hybrid | 28% |

| On-Premise | 20% |

Explanation

The cloud-based segment dominated the market by 52% in 2025 and is expected to be the fastest-growing during 2026-2035 due to its scalability, cost-effectiveness, and ease of deployment. It enables seamless data access, real-time updates, and remote collaboration across healthcare providers. Cloud solutions reduce infrastructure costs and support interoperability, making them ideal for large-scale healthcare systems. Additionally, increasing adoption of digital health technologies and the need for secure data storage further accelerated their widespread use.

On-premise

The on-premise segment is expected to grow at a notable rate due to increasing concerns over data security, privacy, and regulatory compliance. Healthcare organizations prefer on-premise solutions for greater control over sensitive patient data and system customizations. Additionally, large hospitals and institutions with existing IT infrastructure continue to invest in on-premise platforms to ensure reliability, reduce dependency on external networks, and maintain strict data governance standards.

How Does the Hospitals and Integrated Delivery Networks (IDNs) Segment Dominate the Connected Healthcare Platform Market in 2025?

| Segment | Share 2025 (%) |

| Hospitals & Integrated Delivery Networks (IDNs) | 46% |

| Large Multi-specialty & Specialty Clinics | 27% |

| Public & Private Healthcare Systems | 19% |

| Others | 8% |

Explanation

The hospitals and integrated delivery networks (IDNs) segment dominated the connected healthcare platform market by 46% in 2025 due to their large patient volumes and strong investment capacity in digital infrastructure. These organizations require integrated systems for efficient data management, care coordination, and reduced operational costs, and adopting advanced healthcare technologies has significantly driven the adoption of connected healthcare platforms.

Large Multi-Specialty and Specialty Clinics

The large multi-specialty and specialty clinics segment is expected to grow at a significant rate due to increasing patient inflow and the need for efficient care coordination. These clinics are rapidly adopting connected healthcare platforms to streamline operations, manage diverse specialties, and enhance patient experience. Additionally, growing demand for specialized treatment, improved digital infrastructure, and focus on cost-effective outpatient care are driving accelerated adoption during the forecast period.

")

North America dominated the connected healthcare platform market 53% in 2025 due to advanced healthcare infrastructure, high adoption of digital technologies, and the strong presence of key market players. Supportive government initiatives, widespread use of electronic health records, and increasing demand for remote patient monitoring further fueled growth. Additionally, high healthcare spending and focus on improving patient outcomes accelerated the adoption.

U.S. Market Trends

The U.S. connected healthcare platform market is dominating due to its advanced digital infrastructure, high healthcare expenditure, and early adoption of innovative technologies. The strong presence of leading health tech companies, widespread use of electronic health records, and supportive regulatory framework drive growth. Additionally, increasing demand for remote care, chronic disease management, and patient-centric solutions continues to accelerate market expansion across the country.

Asia Pacific is anticipated to grow at the fastest CAGR in the connected healthcare platform market, due to rapid digitalization, expanding healthcare infrastructure, and rising adoption of telehealth solutions. Increasing population, growing chronic disease burden, and improving internet connectivity are driving demand. Additionally, supportive government initiatives and investments in healthcare IT, along with rising awareness of digital health, are accelerating the adoption of connected healthcare platforms across the region.

India Market Trends

India is expected to grow at the fastest CAGR in the connected healthcare platform market, due to a rapid digital transformation, increasing smartphone and internet penetration, and rising demand for accessible healthcare services. Government initiatives promoting digital health, along with expanding telemedicine adoption, are key drivers. Additionally, growing chronic disease burden and investments in healthcare IT infrastructure are accelerating the adoption of connected healthcare platforms across the country.

Europe is anticipated to grow at a notable rate in the connected healthcare platform market due to increasing adoption of digital health solutions and strong regulatory support for healthcare IT integration. A rising aging population and chronic disease burden are driving demand for efficient care delivery. Additionally, government initiatives promoting eHealth, improved healthcare infrastructure, and a focus on data security and interoperability are supporting the expansion of connected healthcare platforms across the region.

UK Market Trends

The UK is expected to grow at a notable rate in the connected healthcare platform market due to strong government support for digital health initiatives and widespread adoption of electronic health records. The presence of advanced healthcare infrastructure and increasing focus on improving patient care efficiency are key drivers. Additionally, rising demand for telehealth services, an aging population, and investments in healthcare IT are accelerating the adoption of connected healthcare platforms across the country.

R&D

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offering |

| ZS | Illinois, USA | Provides digital health solutions, analytics, and patient engagement platforms to improve care coordination and decision-making. |

| Cognizant | New Jersey, USA | Offers healthcare IT services, cloud-based platforms, and interoperability solutions for connected care ecosystems. |

| IQVIA | North Carolina, USA | Delivers advanced analytics, real-world data platforms, and patient-centric solutions for connected healthcare. |

| GlobalLogic Inc | California, USA | Provides digital engineering, IoT integration, and platform development for connected healthcare systems. |

| NTT DATA Group | Tokyo, Japan | Offers healthcare IT services, data integration, and digital transformation solutions for connected care delivery. |

| Epic Systems Corporation | Wisconsin, USA | Provides electronic health record (EHR) systems, patient portals, and integrated healthcare platforms. |

| Cerner | Missouri, USA | Offers cloud-based EHR, data analytics, and interoperability solutions for connected healthcare. |

| Athenahealth | Massachusetts, USA | Delivers cloud-based healthcare platforms, patient engagement tools, and revenue cycle management solutions. |

Strengths

Weaknesses

Opportunities

Threats

By Solution Type

By Deployment Mode

By End-use

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar