")

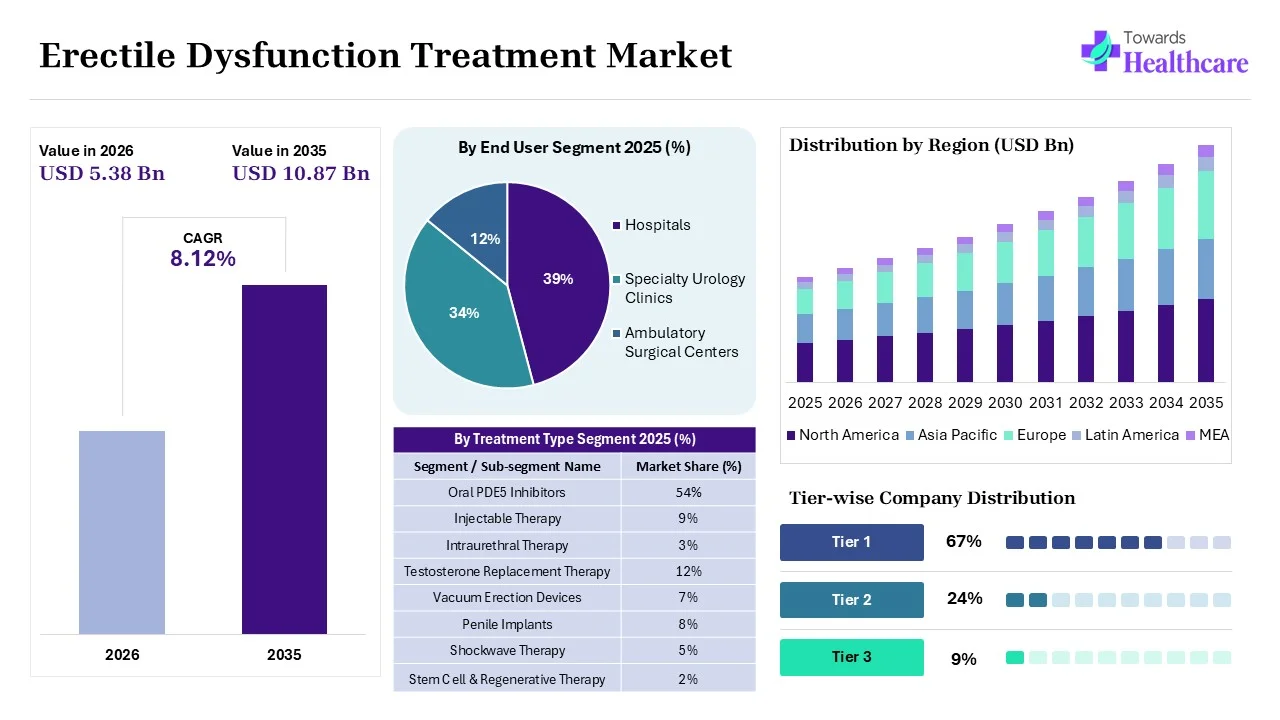

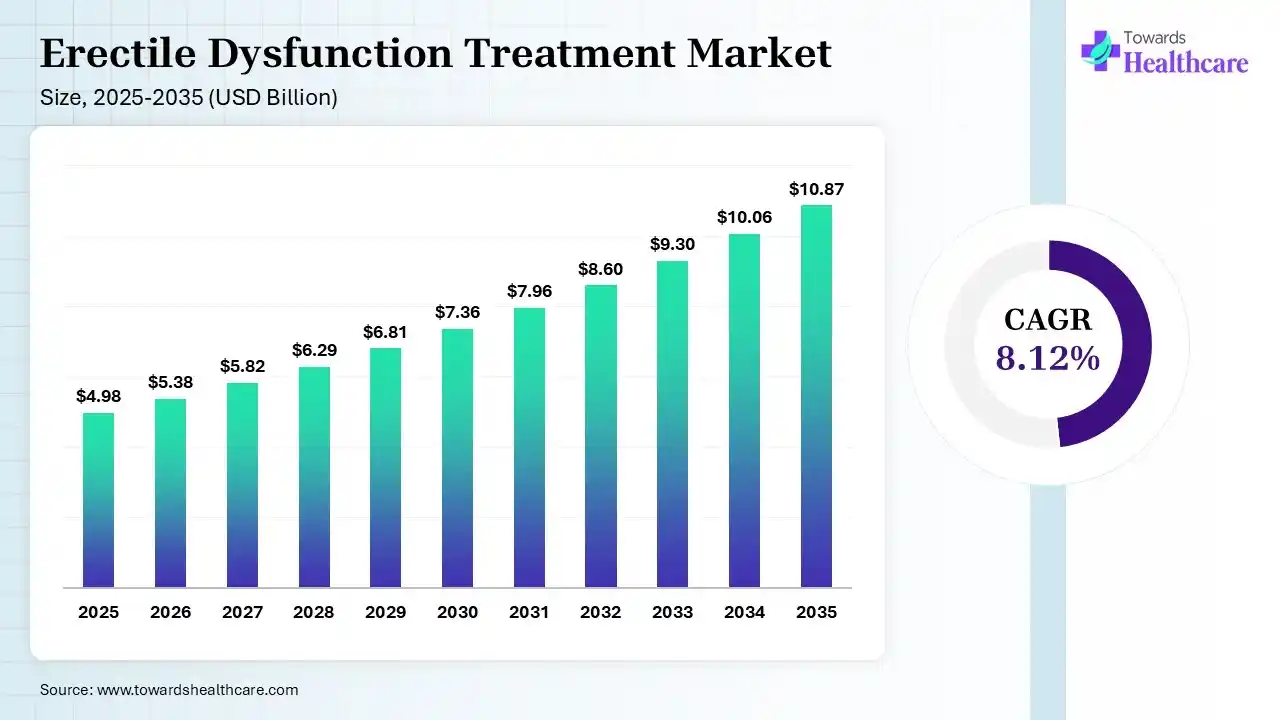

The global erectile dysfunction treatment market size is calculated at USD 4.98 billion in 2025, driven by growth in the geriatric population and a rise in chronic disease burden. The market continues to grow in 2026 at USD 5.38 billion due to the rising use of AI-enabled healthcare, accelerated drug development, and a rise in the focus on men's healthcare. It is expected to reach USD 10.87 billion by 2035, achieving a CAGR of 8.12% between 2026 and 2035, due to growing interest in regenerative medicines, rising minimally invasive solutions, and technological advancements. North America accounted for 38% of the market in 2025 due to its high ED diagnostic rates, growth in health awareness and rise in healthcare spending.

")

The erectile dysfunction treatment market is driven by an increasing geriatric population, growing prevalence of vascular co-morbidities, and rising advanced treatment adoption. The erectile dysfunction treatment encompasses medications, procedures, medical therapies, and devices utilized by men to maintain an erection sufficient for sexual activity. Erectile dysfunction (ED) refers to a medical condition where men are unable to achieve or maintain an erection sufficient for satisfactory sexual activity. Difficulty in getting or maintaining an erection and reduced sexual desire are some of the common symptoms of ED, and various physical or psychological health conditions, such as diabetes, high blood pressure, obesity, heart disease, stress, depression, and hormonal imbalances, are responsible for this condition.

The rise in occasional and persistent erectile dysfunction cases globally is increasing the demand for treatment options. The treatment options help in restoring erectile function, addressing the underlying causes of erectile dysfunction, improving sexual performance, and enhancing quality of life. The oral medications, psychological counselling, penile injections, vacuum erection devices, hormone therapy, penile implants, and lifestyle modifications are commonly available ED treatment options. Increasing health awareness, growing mental health issues, increasing healthcare expenditure, and expanding telemedicine platforms are also propelling the market growth.

AI offers a wide range of applications, where it helps in the early identification of erectile dysfunction and in the detection of its risk factors. It is also used for the assessment of treatment effectiveness, to offer personalized treatment recommendations, and to monitor patient adherence to the treatment. AI supports clinical decision-making, helps in patient data analysis, and accelerates drug discovery and development. The AI-powered health platforms and chatbots also help in remote screening and consultation.

Rising Drug Development

The growing incidence of erectile dysfunction is creating new opportunities for the development of new drug products with enhanced safety, efficacy, efficiency, and duration of action. This, in turn, is driving R&D activities to develop next-generation ED drugs, where the growing focus on personalized medicine is also supporting the development of targeted treatments. These products are being developed to address the underlying causes and offer enhanced patient compliance.

Blooming Regenerative Medicine

The growing interest in regenerative medicine is driving the development of regenerative therapies to restore erectile function. Therefore, the companies are developing new stem cell therapies and platelet-rich plasma therapies to repair damaged blood vessels and promote tissue regeneration. At the same time, their long-term benefits and ability to overcome underlying causes of erectile dysfunction are also increasing their demand and innovations.

Flourishing Medical Devices

The growing shift towards minimally invasive treatment solutions and non-pharmacological treatment solutions is increasing the demand for medical devices. This, in turn, is driving the adoption of penile implants and vacuum erection devices, where they are also being preferred by patients unresponsive to drug therapy. Additionally, expanding technological advancements are also driving the development of devices with improved effectiveness, safety, and comfort.

| Table | Scope |

| Market Size in 2026 | USD 5.38 Billion |

| Projected Market Size in 2035 | USD 10.87 Billion |

| CAGR (2026 - 2035) | 8.12% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Treatment Type, By Etiology, By Route of Administration, By Distribution Channel, By End User, By Region |

| Top Key Players | Pfizer Inc., Vivus LLC, Eli Lilly And Company, Petros Pharmaceuticals, Inc., Bayer AG, Viatris Inc., Futura Medical plc |

")

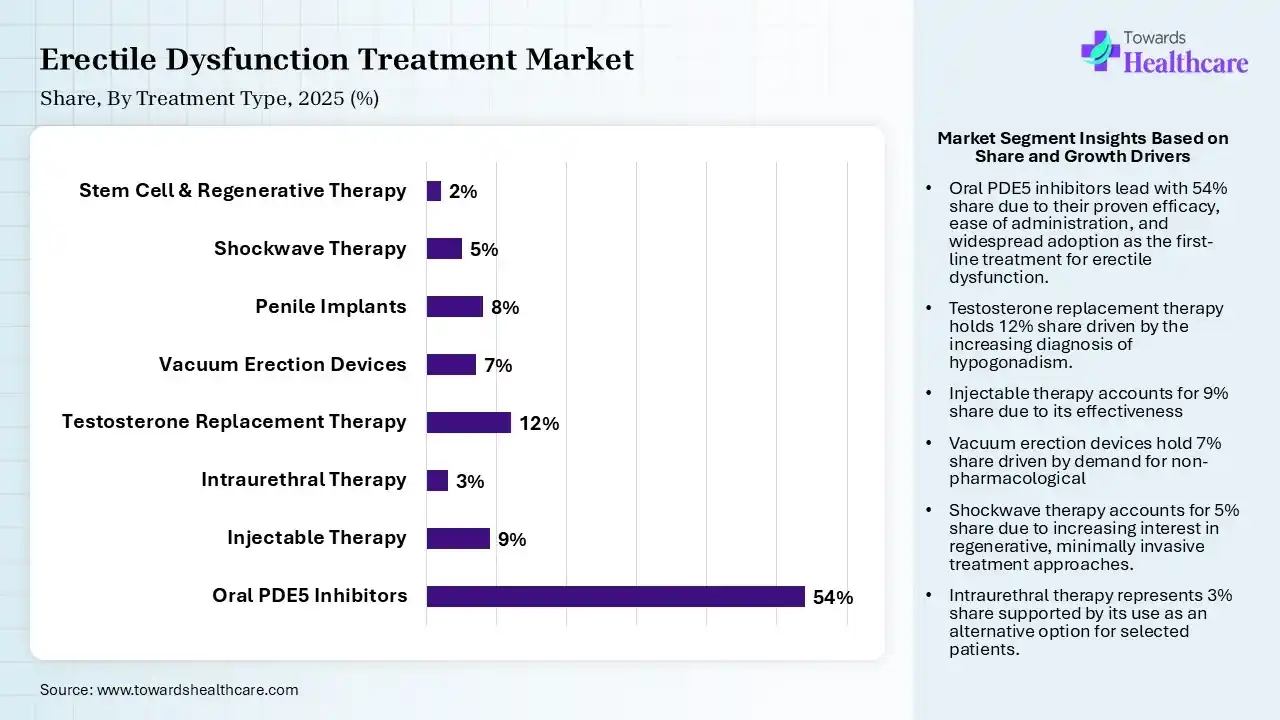

| Segment | Share 2025 (%) |

| Oral PDE5 Inhibitors | 54% |

| Injectable Therapy | 9% |

| Intraurethral Therapy | 3% |

| Testosterone Replacement Therapy | 12% |

| Vacuum Erection Devices | 7% |

| Penile Implants | 8% |

| Shockwave Therapy | 5% |

| Stem Cell & Regenerative Therapy | 2% |

The Oral PDE5 Inhibitors Segment Dominated the Market With 54% in 2025

The oral PDE5 inhibitors segment led the erectile dysfunction treatment market with a 54% share in 2025. As a first-line therapy, it remained widely prescribed. Its generic availability also improved its affordability, which increased its adoption. High physician and patient acceptance also supported their sustained demand, as their high effectiveness also increased their use.

The testosterone replacement therapy segment held the second-largest share of 12% of the market in 2025, driven by rising diagnoses of hypogonadism, which drives prescriptions. Improved hormone testing is also supporting the adoption of these treatment options. The growing aging male population also increases its demand.

The injectable therapy segment held 9% of the erectile dysfunction treatment market share in 2025, driven by a rise in its use due to the failures of oral therapies. Better clinical outcomes in severe cases also encourage their adoption. At the same time, growing specialist adoption is also increasing their utilization.

The shockwave therapy segment held 5% of the market share in 2025 and is expected to witness the fastest growth with a CAGR of 12.50% during the forecast period, due to non-invasive regenerative treatment gaining clinical interest. Private clinics increasingly offer these therapies. Expanding clinical evidence also drives their adoption.

")

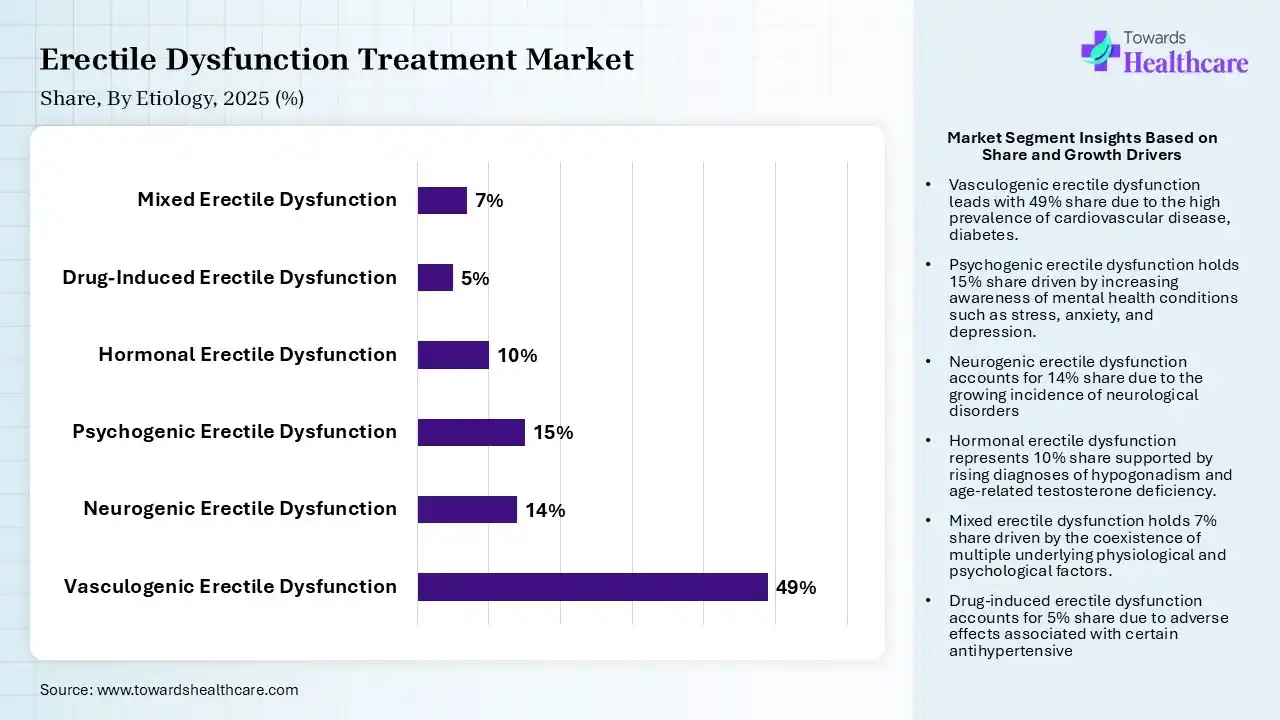

| Segment | Share 2025 (%) |

| Vasculogenic Erectile Dysfunction | 49% |

| Neurogenic Erectile Dysfunction | 14% |

| Psychogenic Erectile Dysfunction | 15% |

| Hormonal Erectile Dysfunction | 10% |

| Drug-Induced Erectile Dysfunction | 5% |

| Mixed Erectile Dysfunction | 7% |

The Vasculogenic Erectile Dysfunction Segment Dominated the Market With 49% in 2025

The vasculogenic erectile dysfunction segment accounted for the highest revenue share of 49% of the erectile dysfunction treatment market in 2025, driven by an increased prevalence of cardiovascular diseases and diabetes. Lifestyle disorders also expanded the patient population. A rise in health awareness promoted earlier diagnosis, which improved treatment rates.

The psychogenic erectile dysfunction segment held the second-largest share of 15% of the market in 2025 and is expected to show the highest growth with a CAGR of 9.20% during the forecast period, due to increasing mental health awareness and encouraging diagnosis. Telehealth is also expanding psychological consultation access. Younger patients increasingly seek treatment.

The neurogenic erectile dysfunction segment held 14% of the erectile dysfunction treatment market share in 2025, due to neurological disorders continuing to increase globally. Improved rehabilitation programs identify more patients, driving the demand for their treatment options. Better treatment accessibility also supports their demand.

The hormonal erectile dysfunction segment held 10% of the market share in 2025, driven by testosterone testing becoming routine. At the same time, an aging population leads to hormone deficiencies, encouraging their treatment. Personalized endocrine treatment also expands adoption.

")

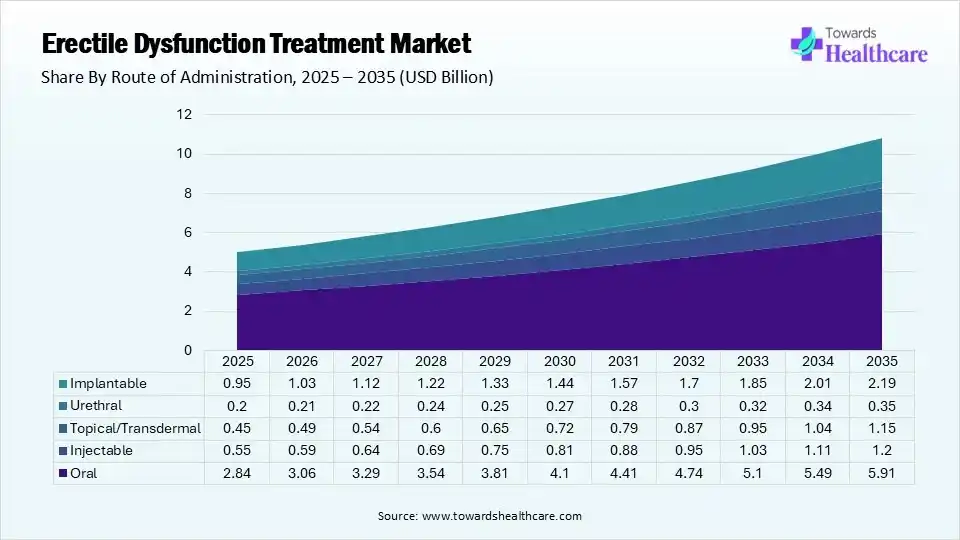

| Segment | Share 2025 (%) |

| Oral | 57% |

| Injectable | 11% |

| Topical/Transdermal | 9% |

| Urethral | 4% |

| Implantable | 19% |

The Oral Segment Dominated the Market With 57% in 2025

The oral segment held a major revenue share of 57% of the erectile dysfunction treatment market in 2025, due to convenient administration, which drives patient preference. Additionally, the presence of strong generic competition also improved its affordability. Physicians recommend oral drugs as first-line therapy, which has increased their adoption rates.

The implantable segment held the second-largest share of 19% of the market in 2025, driven by technological improvements increasing surgical success. Higher patient satisfaction supports referrals. Expanding reimbursement benefits also drive the adoption of the treatment for severe or treatment-resistant erectile dysfunction.

The injectable segment held 11% of the erectile dysfunction treatment market share in 2025, driven by effectiveness for severe dysfunction. Improved injection devices enhance compliance, where their rapid onset of action also increases their use. Specialist recommendations also increase their usage.

The topical/transdermal segment held 9% of the market share in 2025 and is expected to expand rapidly with a CAGR of 9.80% during the forecast period, due to a steady rise in hormonal gel adoption. Improved formulations enhance convenience. Rising hypogonadism treatment also supports a rise in demand.

")

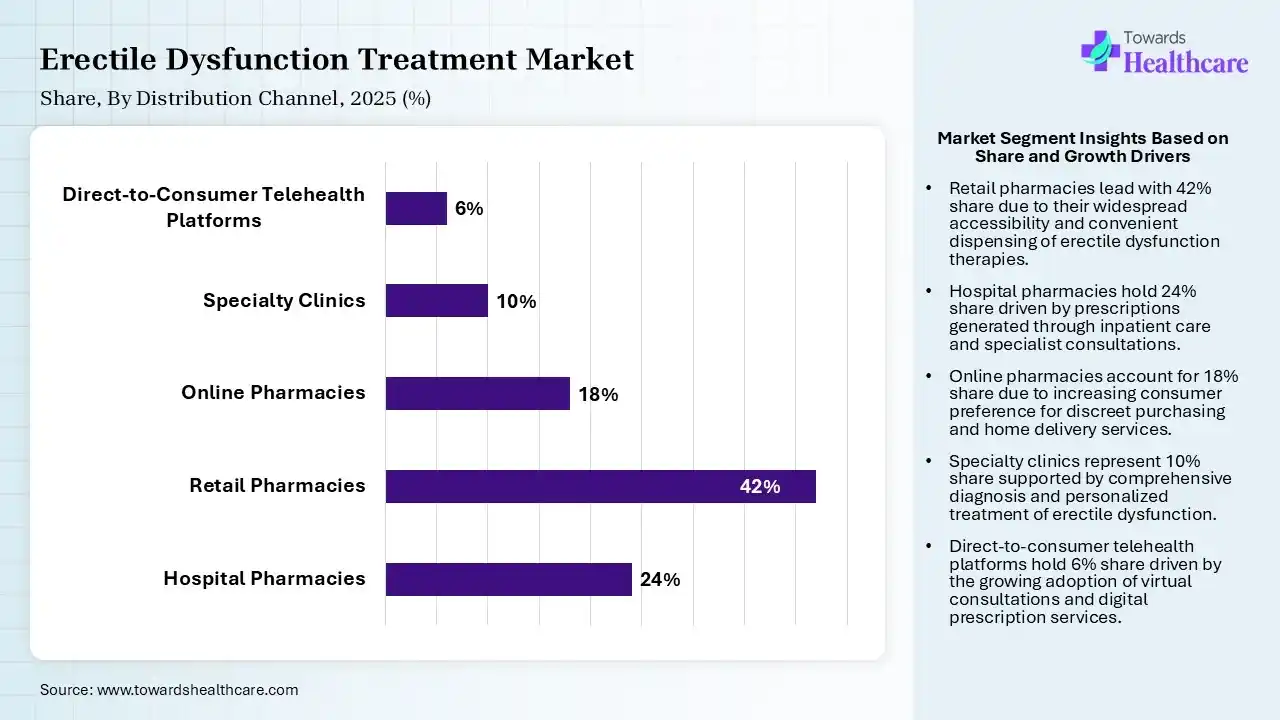

| Segment | Share 2025 (%) |

| Hospital Pharmacies | 24% |

| Retail Pharmacies | 42% |

| Online Pharmacies | 18% |

| Specialty Clinics | 10% |

| Direct-to-Consumer Telehealth Platforms | 6% |

The Retail Pharmacies Segment Dominated the Market With 42% in 2025

The retail pharmacies segment contributed the biggest revenue share of 42% of the erectile dysfunction treatment market in 2025, driven by their broad availability, which improved accessibility to a wide range of erectile dysfunction treatment options. Generic products also increased prescription volume. Consumer convenience also sustained their leadership.

The hospital pharmacies segment held the second-largest share of 24% of the market in 2025, due to hospitals managing complex patients. Strong physician prescribing is also supporting high dispensing volume. Surgical therapies increase institutional demand. Availability of advanced ED therapies and patient counselling services also attracts patients.

The online pharmacies segment held 18% of the erectile dysfunction treatment market share in 2025 and is expected to gain the highest share with a CAGR of 11.40% during the forecast period, due to expanding digital healthcare driving prescription fulfillment. Their enhanced privacy encourages patient purchases. Home deliveries also improve adherence.

The specialty clinics segment held 10% of the market share in 2025, driven by rising specialized urology services and increasing patient referrals. Personalized treatment plans improve outcomes, where the availability of a wide range of erectile dysfunction devices also increases their use. Advanced therapies also boost demand.

")

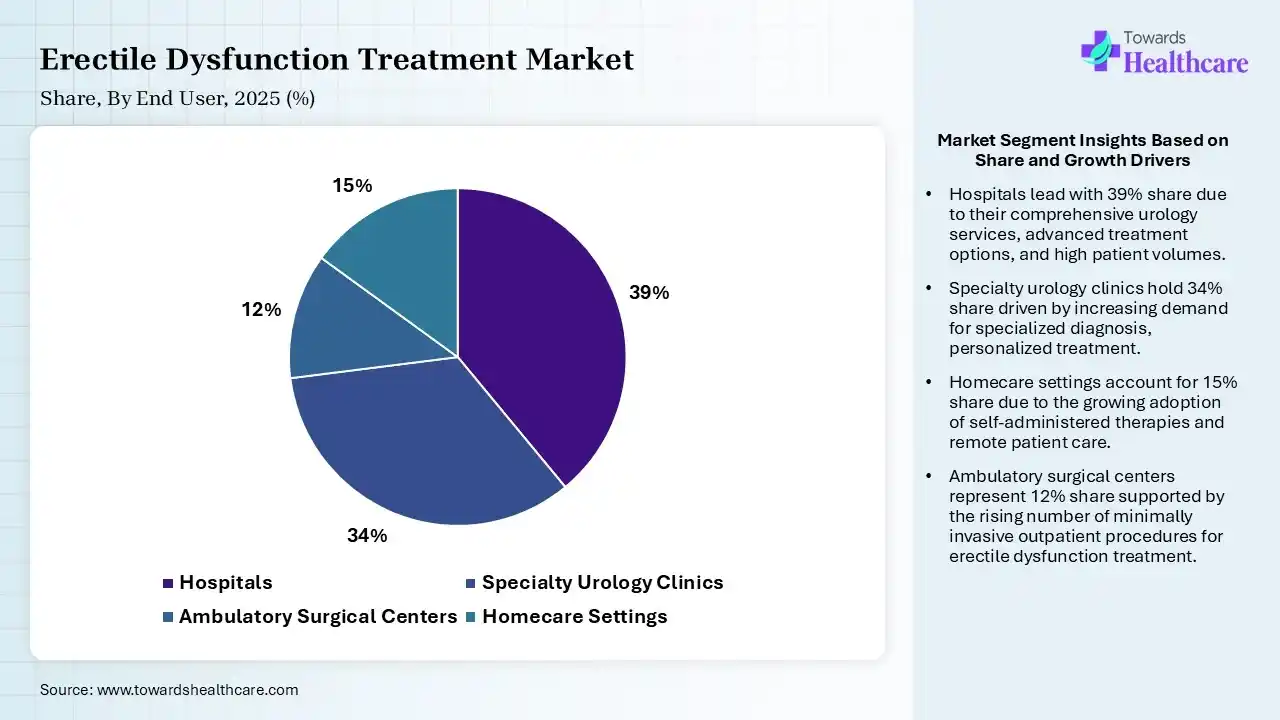

| Segment | Share 2025 (%) |

| Hospitals | 39% |

| Specialty Urology Clinics | 34% |

| Ambulatory Surgical Centers | 12% |

| Homecare Settings | 15% |

The Hospitals Segment Dominated the Market With 39% in 2025

The hospitals segment held the largest revenue share of 39% of the erectile dysfunction treatment market in 2025, due to the presence of comprehensive treatment options, which attracted patients. Surgical procedures remain concentrated in hospitals, which has increased their preference. Integrated diagnostics improve care, which increases their acceptance rate.

The specialty urology clinics segment held the second-largest share of 34% of the market in 2025 and is expected to grow with the fastest CAGR of 9.50% during the forecast period, driven by specialized expertise improving treatment outcomes. Increasing referrals expands patient volume, driving their demand. Advanced regenerative therapies also support their growth.

The homecare settings segment held 15% of the erectile dysfunction treatment market share in 2025, driven by rising self-administered therapies and increasing convenience. Telemedicine supports remote monitoring, driving adoption rates. An aging population expands home treatment demand, which increases the use of home-based care solutions.

The ambulatory surgical centers segment held 12% of the market share in 2025, due to outpatient procedures reducing costs. Faster recovery improves patient preference, where minimally invasive procedures also increase their use. At the same time, the healthcare systems are also shifting toward ambulatory care.

")

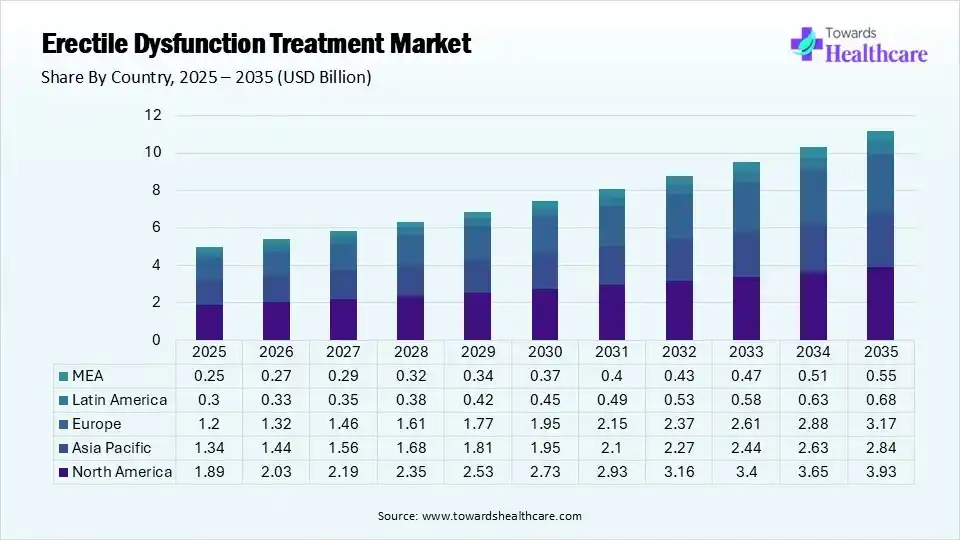

North America dominated the erectile dysfunction treatment market with 38% in 2025, due to high diagnosis rates, which supported treatment demand. Strong reimbursement also improved access to the treatment, while continuous product innovation also strengthened its market leadership. Growth in health awareness also increased demand, and the availability of advanced pharmaceutical products also increased their innovations. A rise in healthcare spending and the adoption of advanced treatment services also increased their use and adoption rates. The expansion of telehealth platforms and R&D activities has also increased their use, which contributed to the market growth.

US Market Growth

The U.S. held an 82% share of the erectile dysfunction treatment market in 2025, due to a large patient pool, which drives prescriptions. A strong pharmaceutical industry also supported innovation, where high healthcare expenditure also sustained their demand. A rise in the cases of obesity and diabetes also increased their incidence, which contributed to the growth of new therapies and devices. Widespread availability of advanced treatment options along with prescription medications also increased their adoption, where the collaborations among pharma and medical devices companies also accelerated their innovations. Expansion of telemedicine platforms also increased their accessibility.

Canada Market Growth

Canada held a share of 12% of the market and is expected to grow at the fastest CAGR of 8.10% during the forecast period, due to improved men's health awareness, which expands treatment. Universal healthcare also improves access to various erectile dysfunction treatments, where a rise in the aging population is also supporting their growth. High healthcare expenditure and increasing government support are also increasing their adoption and innovations. At the same time, expanding patient willingness and online consultation services are also increasing accessibility to various erectile dysfunction treatments and devices.

Asia Pacific held a 24% share of the erectile dysfunction treatment market in 2025 and is expected to grow at the fastest CAGR of 10.20% during the forecast period, due to rising healthcare spending, which expands access. A large, untreated population and telehealth adoption accelerate diagnosis and treatment, as well as create new opportunities. Increasing awareness and disposable income are also increasing their adoption rates, while growing investments are also driving the development of new erectile dysfunction medications and therapies. A rise in the incidence of obesity, cardiovascular disease, and diabetes is also increasing their incidence, where rapid healthcare expansion is also enhancing the market growth.

China Market Growth

China held a 34% share in the erectile dysfunction treatment market in 2025, due to a large patient base, which drives market expansion. Healthcare reforms also improved access to erectile dysfunction treatment options, and a rise in income also supported advanced treatment adoption. Growth in diabetes and obesity cases also increased the risk of erectile dysfunction, and a rise in awareness also increased the adoption of various products. A rise in government health initiatives, rapid healthcare expansion, and growth in telemedicine services also increased their use and created new opportunities for their innovations.

India Market Growth

India held a share of 18% of the market and is expected to grow at the fastest CAGR of 11.80% during the forecast period, due to the expanding healthcare infrastructure, which improves accessibility. Rising diabetes prevalence is also increasing erectile dysfunction cases, and expanding telehealth platforms are also accelerating treatment adoption. At the same time, increasing health awareness is also driving their early diagnosis, where increasing investments and funding are driving the development of new products, urology services, and telemedicine platforms.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Erectile Dysfunction Treatments |

| Pfizer Inc. | New York City, U.S. | Viagra |

| Vivus LLC | Campbell, U.S. | Stendra/Spedra |

| Eli Lilly And Company | Indianapolis, U.S | Cialis |

| Petros Pharmaceuticals, Inc. | New York City, U.S. | Stendra |

| Bayer AG | Leverkusen, Germany | Levitra and Staxyn |

| Viatris Inc. | Pittsburgh, U.S. | Tadalafil and Sildenafil Citrate |

| Futura Medical plc | Guildford, UK | Eroxon |

In June 2026, after the launch of the erectile dysfunction (ED) category consisting of prescription-only, personalized chewables by MedExpress Canada, its Medical Lead, Dr. Ashley White, highlighted that "Erectile dysfunction is far more common than most men realise, and it's still one of the conditions people are most reluctant to raise. What we see clinically is that there's no single right answer. The best treatment depends on someone's health, their lifestyle, and what matters most to them, whether that's spontaneity or predictability. The point of a properly assessed, personalized approach is that we match the treatment to the individual rather than asking the individual to fit the treatment. Our job is to make that assessment straightforward and make it an easy conversation to start."

By Treatment Type

By Etiology

By Route of Administration

By Distribution Channel

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar