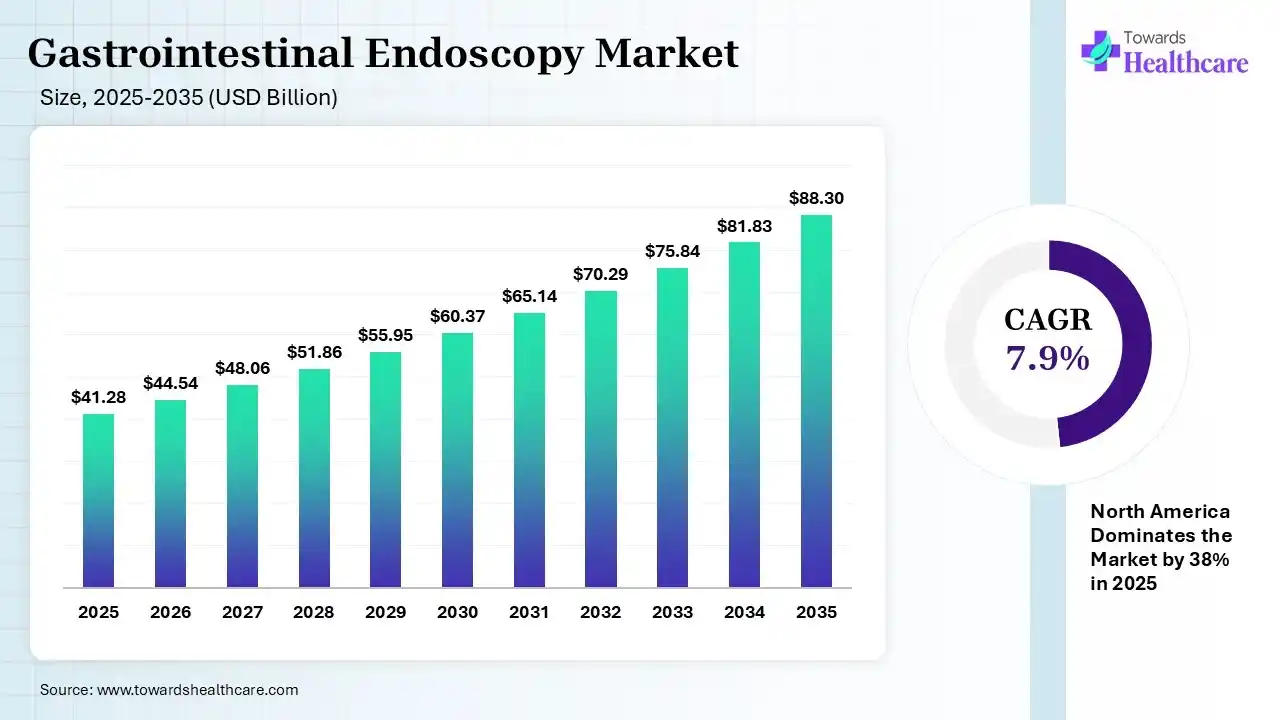

The global gastrointestinal endoscopy market size was estimated at USD 41.28 billion in 2025 and is predicted to increase from USD 44.54 billion in 2026 to approximately USD 88.3 billion by 2035, expanding at a CAGR of 7.9% from 2026 to 2035. The growing cancer burden globally is increasing the demand for gastrointestinal endoscopy. Increasing demand for minimally invasive approaches, health awareness, technological innovations, and new product launches are also enhancing the market growth.

")

The gastrointestinal endoscopy market is driven by rising gastrointestinal disorders and technological innovations. The gastrointestinal endoscopy refers to the medical procedure utilizing an endoscope with an attached camera and light for the diagnosis of the gastrointestinal tract. They are used for the diagnosis of digestive system diseases, cancer screening, removal of polyps, and monitoring chronic diseases such as inflammatory bowel disease (IBD).

AI offers a wide range of applications in gastrointestinal endoscopy by providing real-time image analysis and better diagnostic accuracy. It also helps with computer-aided diagnosis, disease severity assessments, and predicting disease progression. AI also helps in offering smart endoscopes, reducing human errors, and enhancing workflow efficiency.

Rise of Minimally Invasive Procedures

Increasing health awareness is driving the demand for minimally invasive procedures, which promotes the use of gastrointestinal endoscopy. Their less pain, fewer complications, and faster recovery periods are increasing their use.

Expanding Innovations

The companies are developing various types of gastrointestinal endoscopy, creating new opportunities. Capsule endoscopy, robotic endoscopy, and single-use endoscopes are being developed.

Advancing Imaging Technologies

To offer enhanced viability and accurate detection of small lesions or other diseases, the imaging technologies are being improved. This is driving the development of high definition, ultra-high-resolution, and 3D imaging solutions.

| Table | Scope |

| Market Size in 2026 | USD 44.54 Billion |

| Projected Market Size in 2035 | USD 88.3 Billion |

| CAGR (2026 - 2035) | 7.9% |

| Leading Region | North America by 38% |

| Key Applications | Gastrointestinal cancer screening, colorectal disease diagnosis, GERD evaluation, inflammatory bowel disease monitoring, bleeding management, polyp removal, bariatric procedures, therapeutic interventions, and advanced GI imaging. |

| Primary End Users | Hospitals, ambulatory surgical centers, specialty gastroenterology clinics, diagnostic centers, academic and research institutions. |

| Key Challenges | High equipment costs, infection control requirements, regulatory compliance, need for skilled specialists, and maintenance complexity of advanced systems. |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Procedure Type, By Application, By End User, By Technology, By Usability, By Age Group, By Region |

| Top Key Players | Olympus Corporation, Ambu A/S, Fujifilm Holding Corporation, Cook Medical LLC, Boston Scientific Corporation, Micro-Tech Co., Ltd., PENTAX Medical (Hoya Corporation), STERIS plc, Medtronic plc, Karl Storz SE & Co. KG |

")

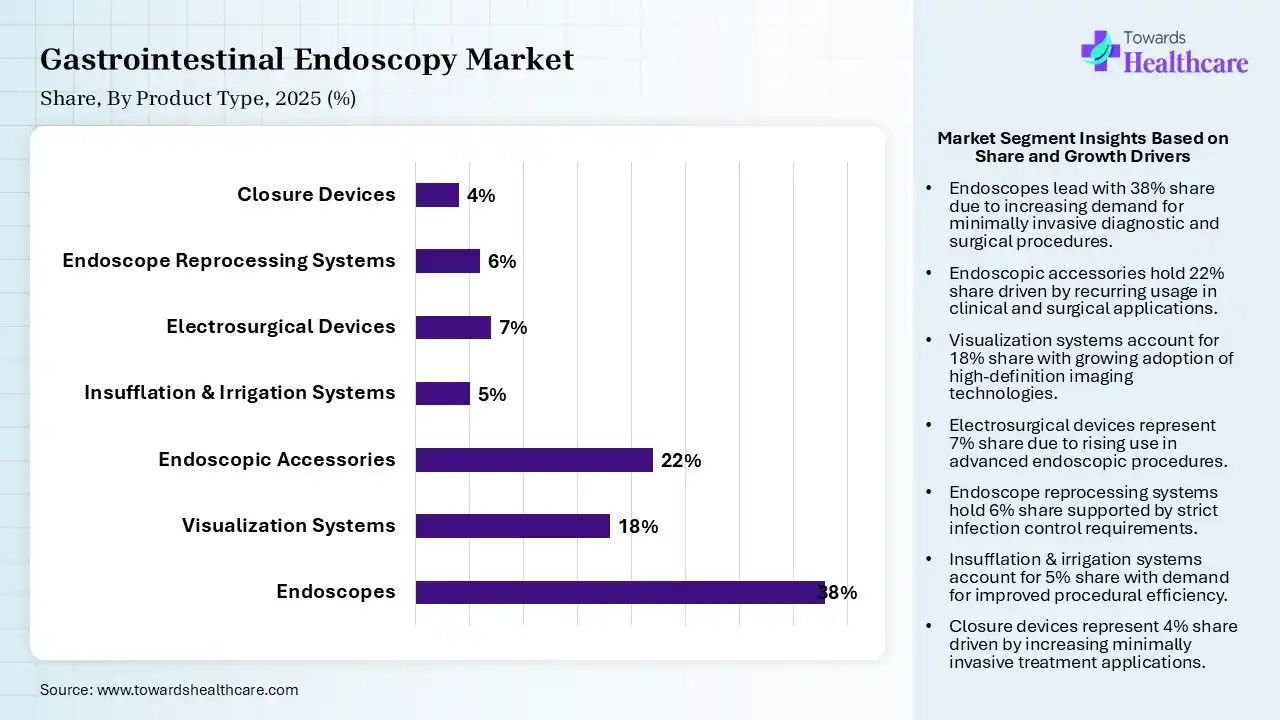

| Segment | Share 2025 (%) |

| Endoscopes | 38% |

| Visualization Systems | 18% |

| Endoscopic Accessories | 22% |

| Insufflation & Irrigation Systems | 5% |

| Electrosurgical Devices | 7% |

| Endoscope Reprocessing Systems | 6% |

| Closure Devices | 4% |

The Endoscopes Segment Dominated the Market With 38% in 2025

The endoscopes segment led the gastrointestinal endoscopy market with 38% share in 2025, due to growth in colorectal cancer screening programs, which increased the demand for advanced GI scopes. Hospitals continued upgrading flexible and high-definition endoscopy platforms, which increased their use. High procedural volumes also supported their recurring procurement across healthcare systems.

The endoscopic accessories segment held the second-largest share of 22% of the market in 2025, driven by high procedural frequency, which drives strong utilization of disposable accessories globally. Therapeutic interventions also require advanced snares, forceps, and retrieval devices. Increasing minimally invasive procedures also sustain accessory replacement demand.

The visualization systems segment held 18% of the gastrointestinal endoscopy market share in 2025 and is expected to witness the fastest growth with a CAGR of 9.1% during the forecast period, due to increasing use of AI-enabled imaging, which improves lesion detection and procedural accuracy in gastroenterology. Healthcare facilities are also adopting 4K and 3D visualization for enhanced diagnostics. Integration with digital workflow systems also accelerates market penetration.

The electrosurgical devices segment held 7% of the market share in 2025, due to therapeutic GI procedures increasingly relying on electrosurgical precision technologies. Growing use of polypectomy and mucosal resections also boosts device demand. Improved safety profiles also support the replacement of conventional instruments.

")

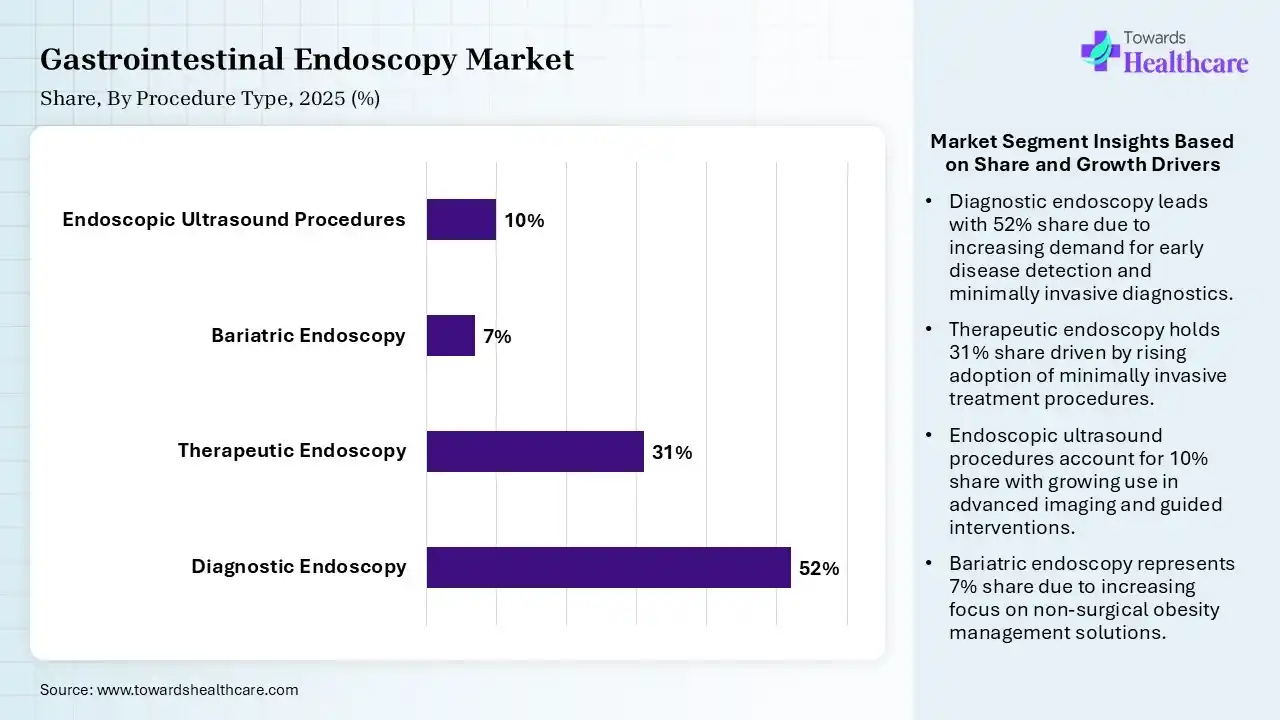

| Segment | Share 2025 (%) |

| Diagnostic Endoscopy | 52% |

| Therapeutic Endoscopy | 31% |

| Bariatric Endoscopy | 7% |

| Endoscopic Ultrasound Procedures | 10% |

The Diagnostic Endoscopy Segment Dominated the Market With 52% in 2025

The diagnostic endoscopy segment accounted for the highest revenue share of 52% of the gastrointestinal endoscopy market in 2025, driven by large-scale colorectal cancer screening programs. Growth in the early disease detection initiatives also increased routine GI diagnostic procedures. Aging populations contributed to higher gastrointestinal disorder prevalence.

The therapeutic endoscopy segment held the second-largest share of 31% of the market in 2025 and is expected to show the highest growth with a CAGR of 8.9% during the forecast period, due to minimally invasive therapeutic procedures, which reduce hospitalization and recovery time. Increasing adoption of EMR, ESD, and ERCP also enhances procedure volumes. Physicians are also preferring endoscopic intervention over open surgical alternatives.

The endoscopic ultrasound procedures segment held 10% of the gastrointestinal endoscopy market share in 2025, driven by increasing pancreatic and biliary disorder diagnoses, which supports EUS procedure growth. Combined imaging and biopsy capabilities also improve clinical efficiency. Advanced oncology applications also expand their adoption in tertiary care facilities.

The bariatric endoscopy segment held 7% of the market share in 2025, due to the rising obesity prevalence, which drives demand for non-surgical weight management solutions. Patients increasingly prefer minimally invasive bariatric interventions. Their technological advancements are also improving the procedural safety and effectiveness.

")

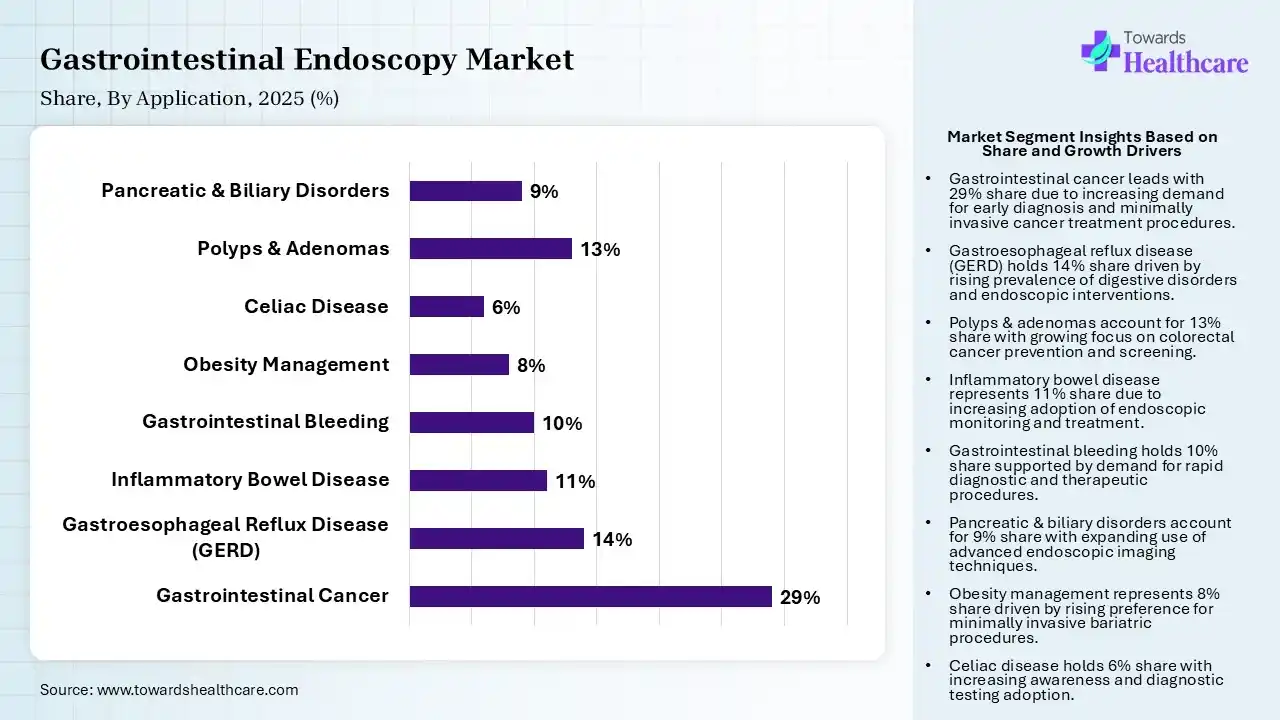

| Segment | Share 2025 (%) |

| Gastrointestinal Cancer | 29% |

| Gastroesophageal Reflux Disease (GERD) | 14% |

| Inflammatory Bowel Disease | 11% |

| Gastrointestinal Bleeding | 10% |

| Obesity Management | 8% |

| Celiac Disease | 6% |

| Polyps & Adenomas | 13% |

| Pancreatic & Biliary Disorders | 9% |

The Gastrointestinal Cancer Segment Dominated the Market With 29% in 2025

The gastrointestinal cancer segment held a major revenue share of 29% of the gastrointestinal endoscopy market in 2025, due to the rising global incidence of colorectal and gastric cancers, which drives screenings. Governments are also promoting early detection programs using advanced endoscopic procedures. Therapeutic endoscopy is also increasingly supporting cancer management pathways.

The gastroesophageal reflux disease (GERD) segment held the second-largest share of 14% of the market in 2025, as sedentary lifestyles and dietary changes increase GERD prevalence worldwide. Growing awareness encourages patients to undergo diagnostic endoscopy procedures. Improved reimbursement policies also support procedural accessibility.

The polyps & adenomas segment held 13% of the gastrointestinal endoscopy market share in 2025, as colonoscopy-based polyp detection programs continue to expand worldwide. Preventive screening initiatives also reduce colorectal cancer progression risks significantly. Their advanced imaging also improves adenoma detection accuracy during procedures.

The obesity management segment held 8% of the market share in 2025 and is expected to expand rapidly with a CAGR of 9.3% during the forecast period, as endoscopic bariatric procedures gain traction as less invasive obesity treatments. Increasing the obesity burden also expands patient eligibility for interventions. Technological advancements also improve safety and long-term efficacy outcomes.

")

| Segment | Share 2025 (%) |

| Hospitals | 54% |

| Ambulatory Surgical Centers | 18% |

| Specialty Gastroenterology Clinics | 15% |

| Diagnostic Centers | 8% |

| Academic & Research Institutes | 5% |

The Hospitals Segment Dominated the Market With 54% in 2025

The hospitals segment contributed the biggest revenue share of 54% of the gastrointestinal endoscopy market in 2025, driven by large patient inflow and advanced infrastructure supporting procedural dominance. Growth in investments in AI-enabled and therapeutic endoscopy technologies also contributed to their expansion. Multidisciplinary gastroenterology services also increased procedure volumes consistently.

The ambulatory surgical centers segment held the second-largest share of 18% of the market in 2025 and is expected to gain the highest share with a CAGR of 8.7% during the forecast period, due to increasing outpatient procedures, reducing treatment costs, and hospital stay durations. Favorable reimbursement policies also support ambulatory endoscopy expansion. Patients are increasingly preferring convenient same-day discharge facilities.

The specialty gastroenterology clinics segment held 15% of the gastrointestinal endoscopy market share in 2025, due to expanding specialized GI care centers with advanced diagnostic capabilities globally. Increasing chronic gastrointestinal disease burden also supports repeat visits. Clinics are also adopting compact and cost-efficient endoscopy systems rapidly.

The diagnostic centers segment held 8% of the market share in 2025, due to increasing preventive screening demand, which strengthens standalone diagnostic center growth globally. Improved imaging technologies also enhance procedural efficiency and accuracy. Urban healthcare expansion also increases diagnostic infrastructure investments.

")

| Segment | Share 2025 (%) |

| Conventional Endoscopy | 20% |

| Flexible Endoscopy | 36% |

| Robot-assisted Endoscopy | 8% |

| Capsule Endoscopy | 14% |

| AI-powered Endoscopy | 15% |

| Disposable Endoscopy | 7% |

The Flexible Endoscopy Segment Dominated the Market With 36% in 2025

The flexible endoscopy segment held the largest revenue share of 36% of the gastrointestinal endoscopy market in 2025, due to high procedural versatility, which supported widespread gastrointestinal diagnostic applications. Improved maneuverability also enhanced physician efficiency during complex interventions. Demand for minimally invasive procedures also sustained technology leadership.

The conventional endoscopy segment held the second-largest share of 20% of the market in 2025 due to established infrastructure and affordability, maintaining continued utilization globally. Smaller healthcare facilities also continue to rely on conventional platforms. Emerging economies also retain significant adoption due to lower capital costs.

The AI-powered endoscopy segment held 15% of the gastrointestinal endoscopy market share in 2025, due to AI-assisted lesion detection, which enhances adenoma identification accuracy substantially. Real-time analytics also improves physician decision-making during procedures. Hospitals are increasingly investing in digital gastroenterology ecosystems.

The robot-assisted endoscopy segment held 8% of the market share in 2025 and is expected to grow with the fastest CAGR of 10.1% during the forecast period, due to robotic precision, which improves navigation and therapeutic intervention capabilities significantly. Healthcare providers are adopting robotic systems for advanced GI procedures. Technological innovation also increases procedural accuracy and physician control.

")

North America dominated the gastrointestinal endoscopy market with 38% in 2025 due to an advanced healthcare infrastructure that supported widespread endoscopy adoption. Strong colorectal cancer screening programs also sustained procedural demand. Rapid AI integration also enhanced diagnostic accuracy and workflow efficiency, which contributed to the market growth.

U.S. Market Trends

High healthcare expenditure in the U.S. drives rapid technology adoption nationwide. Favorable reimbursement policies also support routine screening procedures. Strong presence of leading medical device manufacturers also boosts their innovations.

Asia Pacific held 24% share of the gastrointestinal endoscopy market in 2025 and is expected to grow at the fastest CAGR of 9.3% during the forecast period, due to expanding healthcare infrastructure, which drives procedural accessibility across emerging economies. Rising gastrointestinal cancer prevalence also supports screening initiatives. Medical tourism and private investments also accelerate advanced technology adoption, enhancing the market growth.

China Market Trends

Large patient population in China fuels high gastrointestinal procedure volumes annually. Government healthcare reforms also expand hospital diagnostic capabilities significantly. Domestic manufacturers also improve the affordability of endoscopy technologies, increasing their adoption.

| Category | Market Participants / Explanation |

| Technology Providers | Companies developing AI-assisted imaging, robotic navigation, high-definition visualization, capsule endoscopy, and advanced diagnostic technologies. Examples include Olympus Corporation, Fujifilm, Medtronic, and Boston Scientific. |

| Product Manufacturers | Medical device manufacturers producing endoscopes, visualization systems, accessories, electrosurgical devices, clips, stents, and reprocessing systems. |

| Service Providers | Companies providing maintenance, sterilization solutions, training programs, technical support, and procedural workflow solutions. |

| Platform Providers | Digital healthcare companies supporting AI-enabled diagnosis, imaging analytics, and connected endoscopy workflows. |

| CROs/CDMOs | Limited direct role; some medical device development partners support clinical validation, regulatory testing, and product commercialization. |

| Software Vendors | AI imaging companies and healthcare IT providers developing computer-aided detection and workflow optimization solutions. |

| Research Institutions | Universities, hospitals, and gastroenterology research centers involved in clinical studies, AI validation, and procedural innovation. |

| End-User Industries | Hospitals, outpatient surgical facilities, gastroenterology clinics, cancer screening programs, and diagnostic healthcare networks. |

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Tier 1 | Tie 2 | Tier 3 | |

| Typical Market Influence | 65% | 25% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Olympus Corporation | Tokyo, Japan | Japan | Global leader in gastrointestinal endoscopy with extensive installed base and strong GI procedure portfolio. | EVIS X1 Endoscopy System, GI scopes, imaging platforms, therapeutic accessories |

| Fujifilm Holdings Corporation | Tokyo, Japan | Japan | Major imaging technology provider with strong presence in diagnostic and therapeutic endoscopy. | ELUXEO System, CAD EYE AI detection, GI endoscopes |

| Boston Scientific Corporation | Marlborough, Massachusetts, USA | United States | Leading interventional GI device company with strong therapeutic endoscopy portfolio. | SpyGlass, AXIOS Stents, endoscopic accessories, therapeutic devices |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| PENTAX Medical (HOYA Corporation) | Tokyo, Japan | Japan | Established endoscopy manufacturer specializing in GI imaging systems and scopes. | INSPIRA Endoscopy System, i-scan imaging technology |

| Ambu A/S | Ballerup, Denmark | Denmark | Growing player focused on single-use endoscopy solutions. | aScope Gastro, disposable endoscopes |

| Cook Medical LLC | Bloomington, Indiana, USA | United States | Strong presence in therapeutic GI accessories and minimally invasive devices. | Hemostasis devices, stents, biopsy devices |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| EndoMed Systems GmbH | Voerde, Germany | Germany | Specialized provider of endoscopy systems and medical imaging solutions. | Endoscopy towers, visualization systems |

| SonoScape Medical Corp. | Shenzhen, China | China | Developing endoscopy and imaging technologies with growing international presence. | HD endoscopy systems, GI imaging solutions |

| CapsoVision | Saratoga, California, USA | United States | Innovative capsule endoscopy technology company. | CapsoCam capsule endoscopy system |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Procedure Type

By Application

By End User

By Technology

By Usability

By Age Group

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar