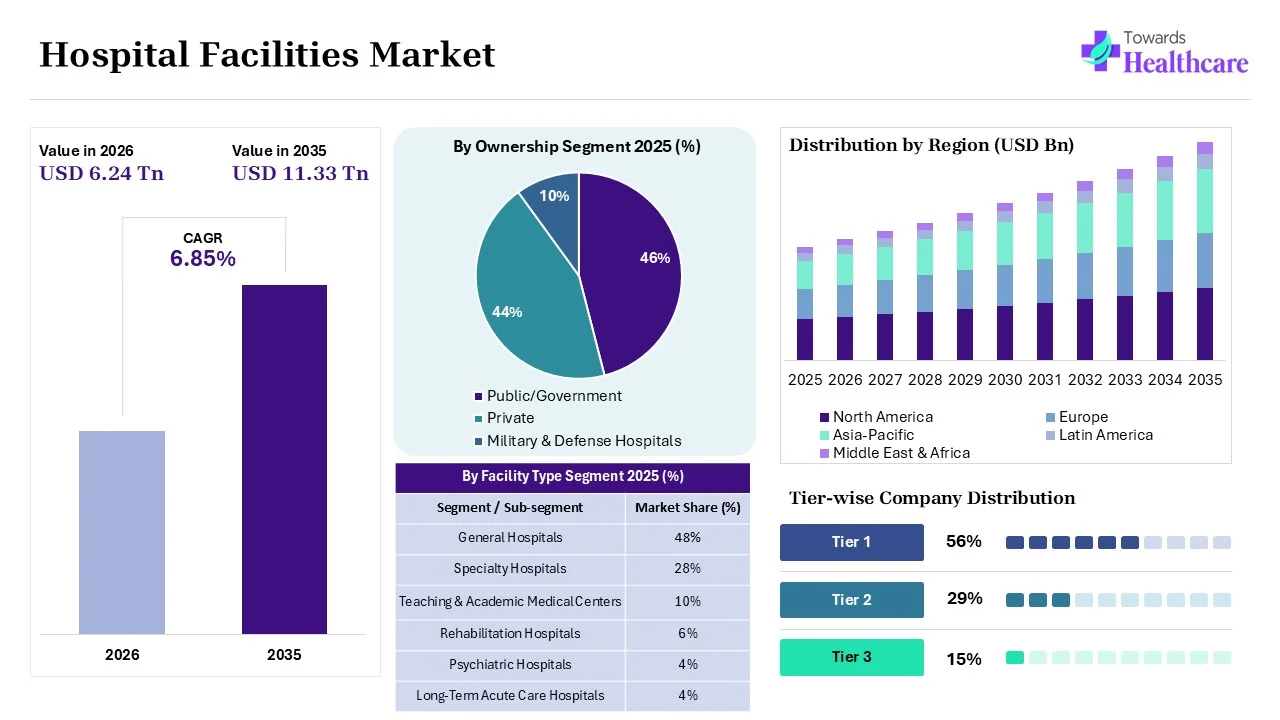

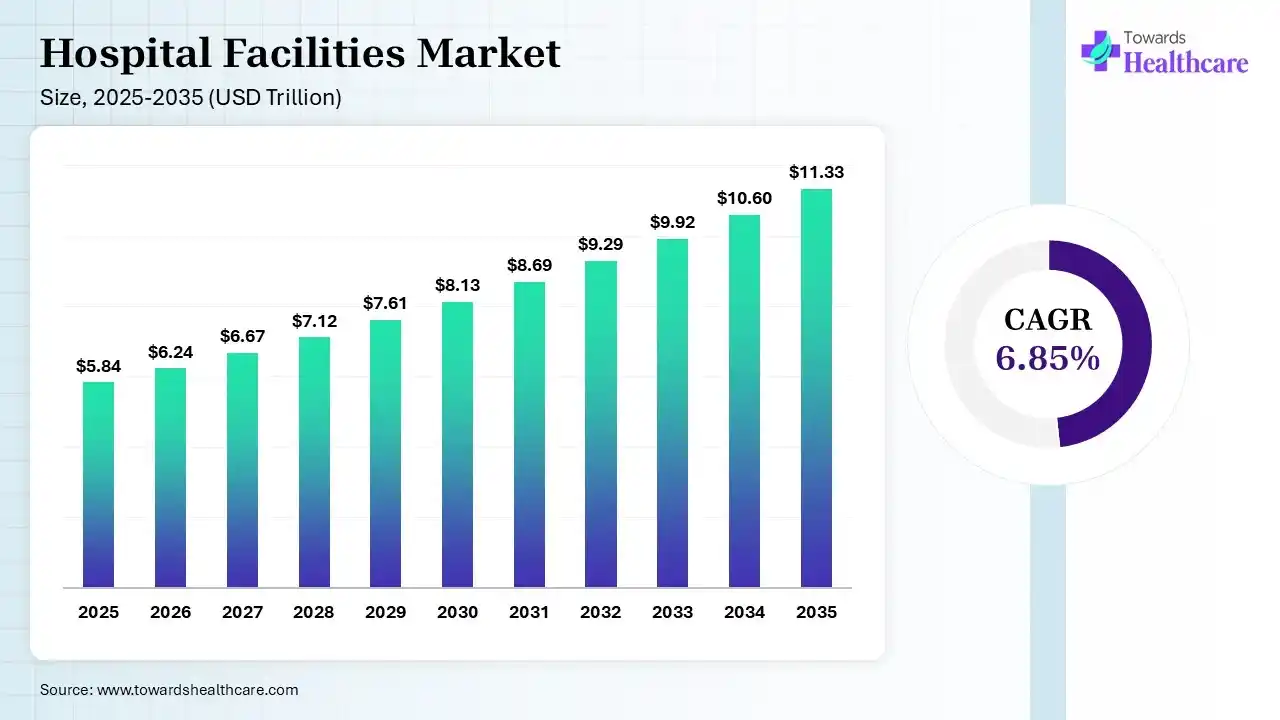

The global hospital facilities market size is calculated at USD 5.84 trillion in 2025, driven by a growth in the demand for advanced healthcare services. The market continues to grow USD 6.24 trillion in 2026 due to the rising healthcare investments, expanding smart infrastructure, and growing outpatient services. It is expected to reach USD 11.33 trillion by 2035, expanding at a CAGR of 6.85% from 2026 to 2035. As continued healthcare expansion, AI integration, and growing focus on patient-centric care accelerate market expansion. North America accounted for 36% of the market in 2025 due to its advanced healthcare infrastructure, high healthcare spending, and digital transformation.

")

")

The hospital facilities market is driven by rising investments, expanding smart infrastructure, and growing demand for advanced healthcare systems. Hospital facilities refer to the infrastructure offering medical, therapeutic, and surgical services to maintain and improve health outcomes. These facilities offer efficient hospital operation for disease diagnosis, management, treatment, and prevention, ensuring patient safety and comfort. These hospital facilities consist of patient wards, operating rooms, diagnostic laboratories, pharmacies, intensive care units, emergency departments, and ambulance services.

The growth in the chronic disease burden, driving patient volume, is increasing the demand for hospital facilities in order to leverage their services. Their availability of outpatient services, minimally invasive approaches, specialized diagnostic tools, maternity care, and rehabilitation services are also propelling their use. Additionally, based on the survey conducted by the research team, expanding healthcare infrastructure, rising demand for quality care, growing advanced medical technology integration, increasing government investments, and a rise in medical procedures are also contributing to the market expansion.

Expanding Healthcare Infrastructure

The rise in investments and funding from the private and government sectors is increasing the healthcare infrastructure. Additionally, growing healthcare modernization programs and rapid digital transformation are also expanding the hospital infrastructure globally.

Growing Burden of Chronic Diseases

Increasing prevalence of chronic illnesses is driving the demand for advanced healthcare services, promoting the use of hospital facilities. This is also driving the expansion and use of specialty departments and multidisciplinary care facilities.

Population Aging

The growing geriatric population impacts the market expansion by driving the demand for various hospital services. They increase hospital admissions, demand for geriatric care, as well as long-term healthcare infrastructure demand.

High Capital and Operating Costs

Financial barriers associated with hospital construction, equipment procurement, workforce management, and facility maintenance are responsible for high capital and operating costs, which reduce their use.

Workforce Shortages

Growing shortages of physicians and nurses are affecting hospital operations, while decreasing technicians and administrators are also impacting hospital expansion, which in turn limits their growth.

Smart Hospital Development

Investment opportunities in AI-enabled hospitals and intelligent infrastructure are promoting the development of smart hospitals. Increasing use of automation and connected healthcare ecosystems are also driving their expansion.

Medical Tourism Expansion

The growing demand for internationally accredited hospitals serving cross-border patients is expanding medical tourism and driving the demand for advanced hospital facilities.

Emerging Healthcare Markets

A rise in infrastructure investments is expanding healthcare markets across Asia-Pacific, Latin America, the Middle East, and Africa, where rapid digitalization is also creating new opportunities.

Regulatory Compliance

Rapidly evolving healthcare regulations governing infrastructure, patient safety, quality standards, and digital healthcare slow down market growth.

Cybersecurity Risks

Increasing cybersecurity threats associated with hospital digitalization and electronic health records limit the adoption of advanced technologies.

AI plays an important role in hospital facilities, where it helps in various hospitals' operations and management, enhancing administrative tasks and automated patient scheduling as well as reducing waiting times. It also supports medical imaging, diagnosis, clinical decision-making, and remote patient monitoring, promoting more efficient, data-driven, and patient-centric care. AI is also used for hospital room management, inventory optimization, and maintenance of medical tools.

Threat of New Entrants

Threat of new entrants focuses on rising barriers due to capital requirements, regulations, workforce availability, and healthcare accreditation.

Bargaining Power of Suppliers

Supplier influence over medical equipment, healthcare technologies, pharmaceuticals, and construction materials are included in the bargaining power of suppliers.

Bargaining Power of Buyers

Bargaining power of buyers highlights the negotiating power of governments, insurers, institutional buyers, and patients.

Threat of Substitutes

Alternative care settings such as outpatient centers, telemedicine, and home healthcare are the threat of substitutes.

Competitive Rivalry

Competitive Rivalry focuses on competitive strategies among hospital operators, healthcare systems, and specialty providers.

Growing Healthcare Investments

A rise in government and private investments are enhancing healthcare investments and driving the development of new hospitals and expanding hospital facilities. These investments are also supporting the modernization of healthcare infrastructure, leading to a rise in the development of smart hospitals and specialized care facilities. This capital also helps in the adoption of advanced medical equipment and integration of digital technologies, enhancing operational efficiency.

Strong Focus on Patient-Centric Care

In order to improve patient safety, comfort, and experience, the healthcare providers are increasingly focusing on enhancing patient-centric care. This, in turn, is leading to a rise in personalized care services, modernization of patient rooms, and strong focus on infection control, which is enhancing patient satisfaction. Additionally, expansion of navigation systems and improved healing environments are also enhancing treatment adherence and patient treatment outcomes.

Rise in Emergency Preparedness

Due to frequent disease outbreaks and mass casualty events, hospital facilities are strengthening their emergency preparedness. This rise in emergency services helps in enhancing healthcare systems' resilience and improving patient outcomes. Moreover, it is also expanding emergency departments, ICU beds, isolation rooms, emergency stockpiles, advanced monitoring systems, disaster recovery services, and emergency response systems.

| Table | Scope |

| Market Size in 2026 | USD 6.24 Trillion |

| Projected Market Size in 2035 | USD 11.33 Trillion |

| CAGR (2026 - 2035) | 6.85% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Facility Type, By Ownership, By Bed Capacity, By Service Type, By Technology Integration, By End User, By Infrastructure, By Region |

| Top Key Players | Mayo Clinic, The Johns Hopkins Hospital, Cleveland Clinic, Karolinska Universitetssjukhuset, Toronto General Hospital, University Hospital Heidelberg, Sheba Medical Center, West China Hospital, Charité, Singapore General Hospital |

")

| Segment | Share 2025 (%) |

| General Hospitals | 48% |

| Specialty Hospitals | 28% |

| Teaching & Academic Medical Centers | 10% |

| Teaching & Academic Medical Centers | 6% |

| Psychiatric Hospitals | 4% |

| Long-Term Acute Care Hospitals | 4% |

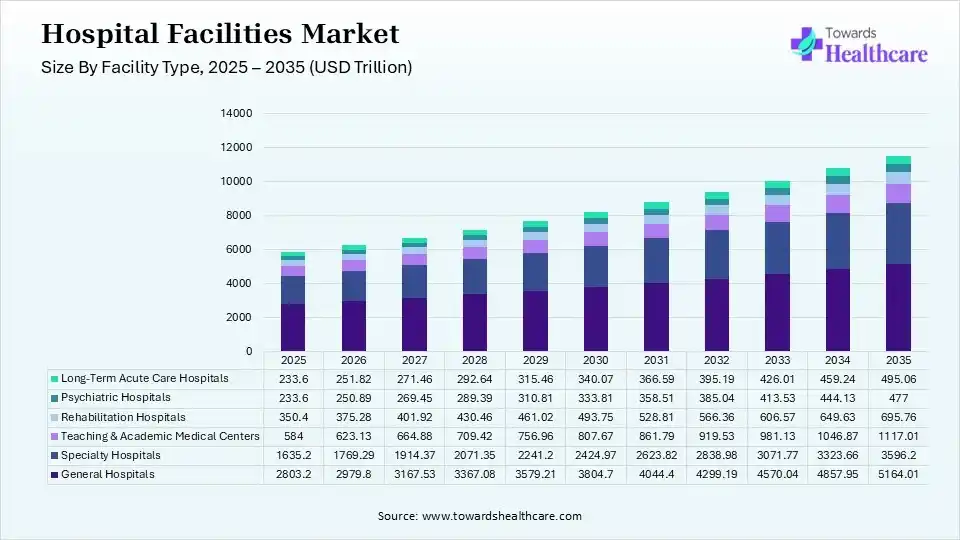

The General Hospitals Segment Dominated the Hospital Facilities Market With 48% in 2025

The general hospitals segment led the market with a 48% share in 2025, due to growth in patient admissions, which increased the demand for comprehensive treatment. Governments continue expanding multispecialty facilities, which attracted a large patient population. Private investments also strengthened hospital networks. 24/7 availability and large bed capacity also increased their use.

The specialty hospitals segment held the second-largest share of 28% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 8.20% during the forecast period, driven by rising chronic diseases accelerating specialty care demand. Precision medicine encourages specialized infrastructure investments, promoting their expansion. Higher reimbursement also drives their growth.

The teaching & academic medical centers segment held 10% of the hospital facilities market share in 2025, due to medical education expansion, which increases hospital capacity. Clinical research strengthens investments, which expands their reach. Academic partnerships enhance advanced care, which increases their use.

The rehabilitation hospitals segment held 6% of the market share in 2025, driven by growing aging populations, which increase rehabilitation demand. Stroke and trauma recovery services expansion also increases their use. Value-based care improves rehabilitation utilization. A strong focus on quality of life also increases their preference.

")

| Segment | Share 2025 (%) |

| Public/Government | 46% |

| Private | 44% |

| Military & Defense Hospitals | 10% |

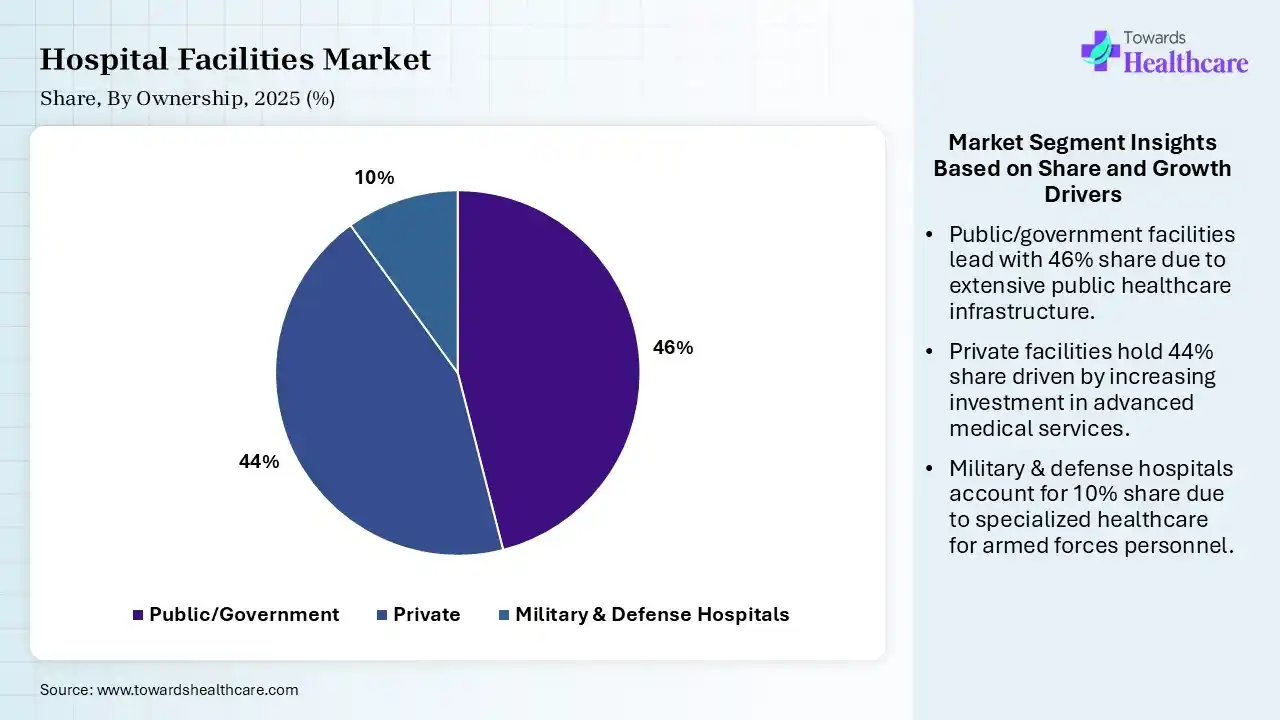

The Public/Government Segment Dominated the Hospital Facilities Market With 46% in 2025

The public/government segment accounted for the highest revenue share of 46% of the market in 2025, due to growth in public investments, which improved healthcare accessibility. Universal healthcare also supported infrastructure expansion. National hospital modernization also contributed to its continued growth. Affordable services and insurance coverage also increased their acceptance rate.

The private segment held the second-largest share of 44% of the market in 2025 and is expected to show the highest growth with a CAGR of 7.60% during the forecast period, driven by growing private investments, which accelerate hospital construction. Expanding medical tourism also boosts private healthcare demand. A rise in premium healthcare services also attracts patients.

The military & defense hospitals segment held 10% of the hospital facilities market share in 2025, due to defense healthcare modernization improving facilities. A rise in emergency preparedness is also increasing investments, leading to their expansion. Military personnel healthcare requirements also remain stable, contributing to their growth.

")

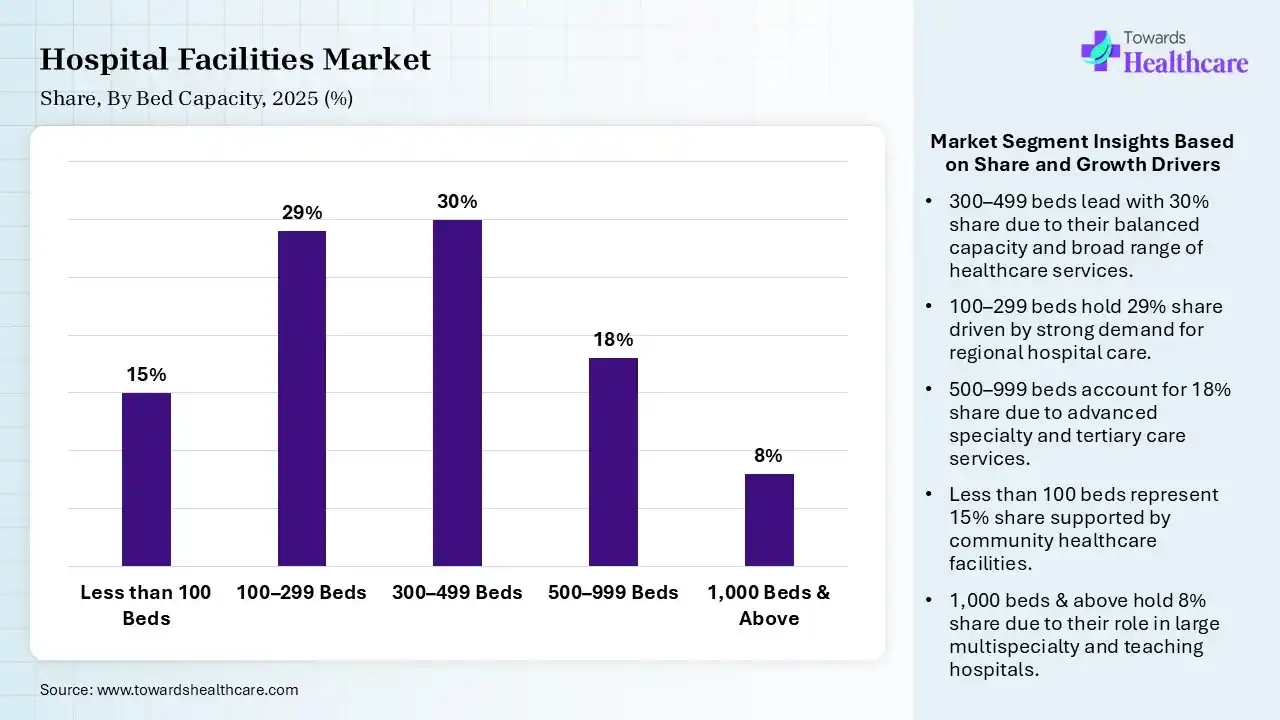

| Segment | Share 2025 (%) |

| Less than 100 Beds | 15% |

| 100–299 Beds | 29% |

| 300–499 Beds | 30% |

| 500–999 Beds | 18% |

| 1,000 Beds & Above | 8% |

The 300–499 Beds Segment Dominated the Hospital Facilities Market With 30% in 2025

The 300–499 beds segment held a major revenue share of 30% of the market in 2025, driven by growth in urban healthcare demand, which supported capacity expansion. Expansion of advanced specialty departments also increased their utilization. Efficient resource allocation strengthened operations. They also help deliver quality care and a wide range of medical services.

The 100–299 beds segment held the second-largest share of 29% of the market in 2025, due to regional healthcare expansion increasing mid-sized facilities. Balanced operating costs also attract investors, where a growing population also supports their utilization. Growing investment also drives their demand for community-based services.

The 500–999 beds segment held 18% of the hospital facilities market share in 2025 and is expected to expand rapidly with a CAGR of 7.60% during the forecast period, driven by large healthcare systems expanding tertiary care services. Complex procedures require greater bed availability. High-acuity patient volumes continue increasing.

The less than 100 beds segment held 15% of the market share in 2025, due to community healthcare expansion, which supports smaller hospitals. Increasing rural healthcare investments are also improving their access. Local patient demand remains consistent, promoting their use.

")

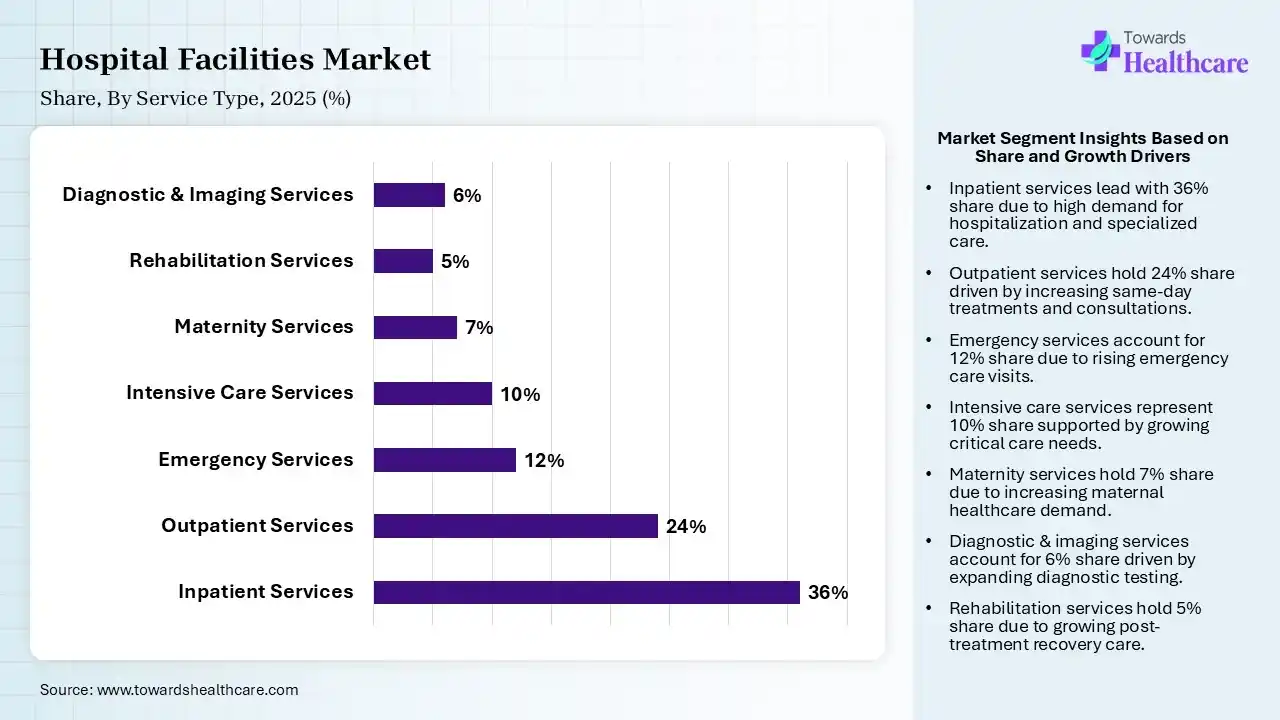

| Segment | Share 2025 (%) |

| Inpatient Services | 36% |

| Outpatient Services | 24% |

| Emergency Services | 12% |

| Intensive Care Services | 10% |

| Maternity Services | 7% |

| Rehabilitation Services | 5% |

| Diagnostic & Imaging Services | 6% |

The Inpatient Services Segment Dominated the Hospital Facilities Market With 36% in 2025

The inpatient services segment held the largest revenue share of 36% of the market in 2025, driven by growth in chronic disease treatment, which increased admissions. Surgical procedures require hospitalization, which increased the demand for these services. Aging populations also sustained inpatient demand.

The outpatient services segment held the second-largest share of 24% of the market in 2025 and is expected to grow with the fastest CAGR of 8.30% during the forecast period, due to minimally invasive procedures, which are reducing hospitalization. Rapid expansion of ambulatory care also increases their use. Healthcare systems improve operational efficiency.

The emergency services segment held 12% of the hospital facilities market share in 2025, driven by rising accident rates increasing emergency visits. Trauma centers expand nationwide, increasing their accessibility. Emergency preparedness also improves infrastructure.

The intensive care services segment held 10% of the market share in 2025, due to critical illness management driving ICU expansion. Advanced monitoring technologies improve outcomes, increasing their use. Pandemic preparedness also strengthens investments.

")

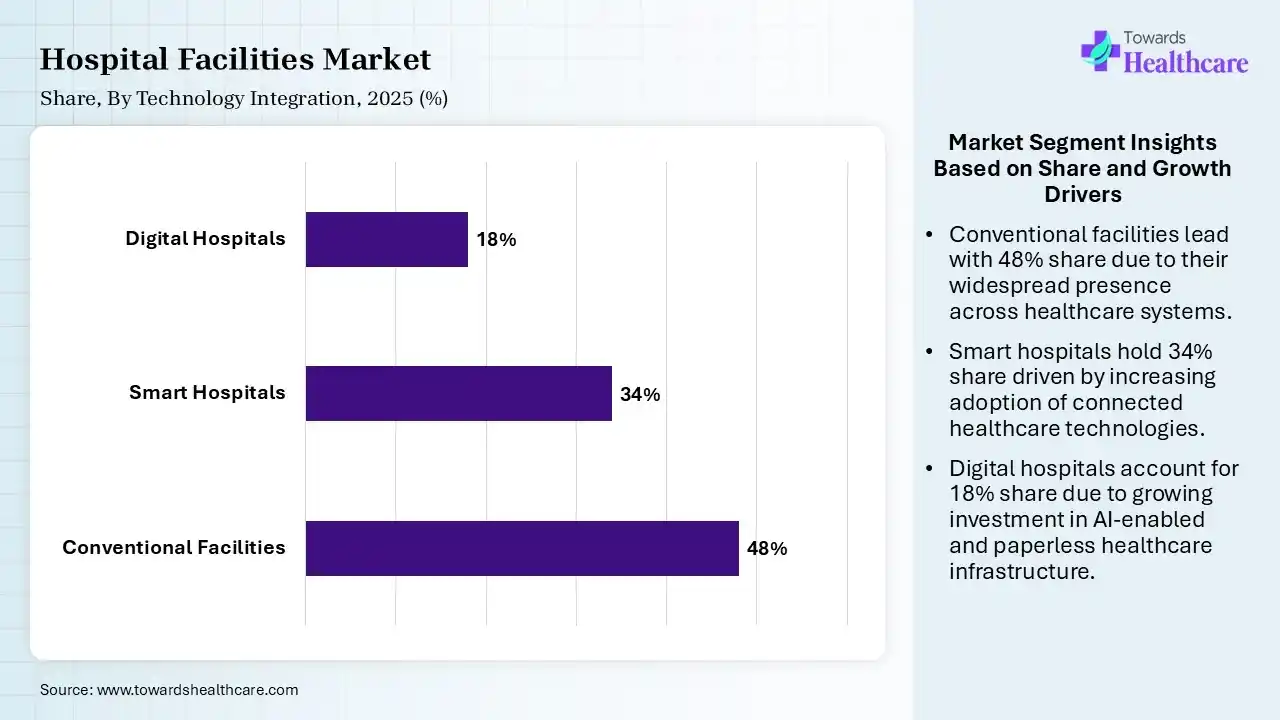

| Segment | Share 2025 (%) |

| Conventional Facilities | 48% |

| Smart Hospitals | 34% |

| Digital Hospitals | 18% |

The Conventional Facilities Segment Dominated the Hospital Facilities Market With 48% in 2025

The conventional facilities segment contributed the biggest revenue share of 48% of the market in 2025, due to legacy hospitals continued to serve major populations. Incremental upgrades improved operations, which increased their use. Existing infrastructure also remained widely utilized.

The smart hospitals segment held the second-largest share of 34% of the market in 2025 and is expected to gain the highest share with a CAGR of 9.10% during the forecast period, driven by AI, IoT, and robotics optimizing hospital workflows. Connected infrastructure enhances patient monitoring, increasing their preference. Automation improves clinical efficiency, promoting their use.

The digital hospitals segment held 18% of the hospital facilities market share in 2025, due to electronic health records improving care coordination. Digital platforms streamline operations, driving their adoption. Telehealth integration also strengthens patient engagement.

")

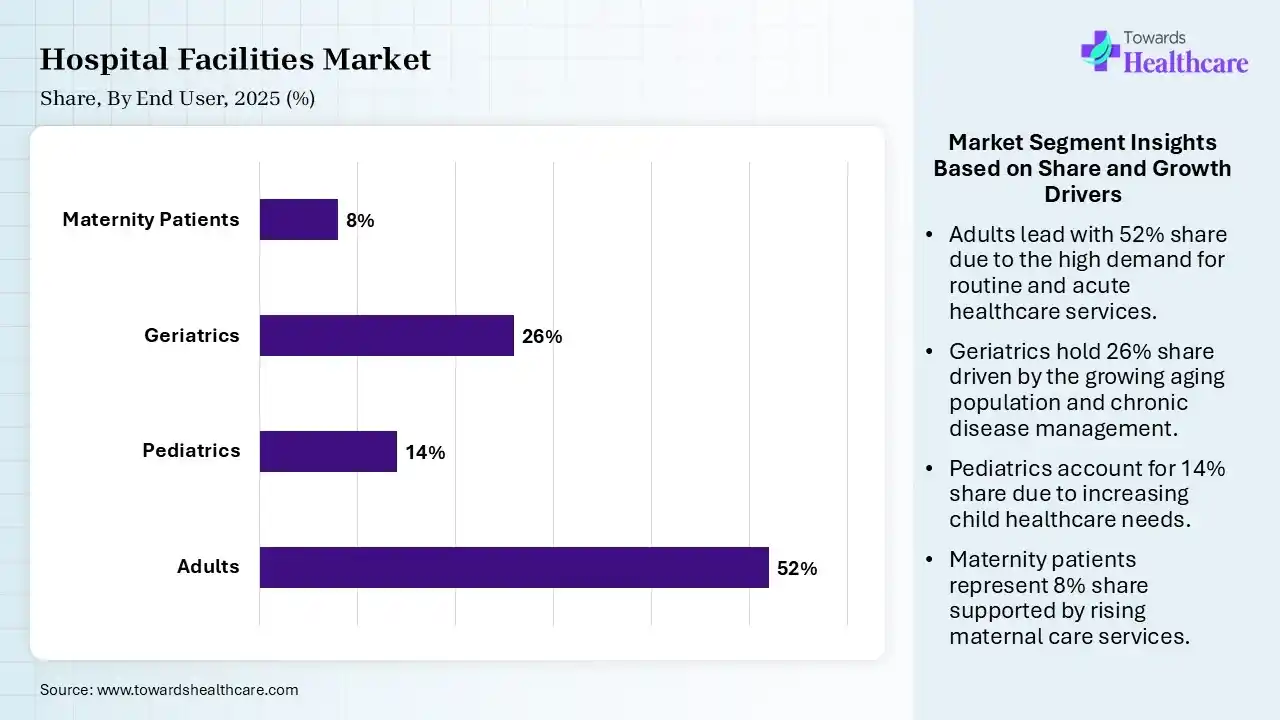

| Segment | Share 2025 (%) |

| Adults | 52% |

| Pediatrics | 14% |

| Geriatrics | 26% |

| Maternity Patients | 8% |

The Adults Segment Dominated the Hospital Facilities Market With 52% in 2025

The adults segment accounted for the highest revenue share of 52% of the market in 2025, due to growth in chronic disease prevalence, which increased hospital admissions. Working-age populations required comprehensive healthcare, which increased their use. Lifestyle disorders support the rise in their demand.

The geriatrics segment held the second-largest share of 26% of the market in 2025 and is expected to gain the highest share with a CAGR of 8.20% during the forecast period, driven by rapid aging populations, which increase hospital utilization. Multiple chronic conditions require complex care, also driving demand. Long-term treatment demand continues rising.

The pediatrics segment held 14% of the hospital facilities market share in 2025, due to pediatric specialty services continuing to expand. Childhood disease management improves care utilization. Government child health programs support investments, promoting their expansion.

The maternity patients segment held 8% of the market share in 2025, driven by maternal healthcare investments that improve accessibility. Specialized maternity centers expand, which is attracting patients. Preventive prenatal care also increases hospital visits.

North America dominated the market with 36% in 2025, due to the presence of advanced healthcare infrastructure, which supported market leadership. High healthcare spending also sustained investments, where a rise in digital transformation also accelerated modernization. A rise in chronic disease burden also increased the adoption of advanced technologies and critical care services. Growth in government and private investments also expanded the healthcare infrastructure, where a strong focus on patient safety and emergency preparedness also increased their use, which contributed to the market growth.

US Market Growth

U.S. held an 82% share of the hospital facilities market in 2025, driven by extensive hospital networks that supported patient demand. Continuous technology adoption also improved efficiency, where private investments remained strong and enhanced accessibility to hospital facilities. The presence of leading healthcare providers and growth in healthcare spending also increased the adoption of advanced technologies, leading to a rise in smart hospitals. Growth in the geriatric population and demand for patient-centric care also increased their use, while a focus on infection control also promoted their use.

Mexico Market Growth

Mexico held a 7% share in the hospital facilities market in 2025 and is expected to grow with the highest CAGR of 6.60% during the studied years, due to private healthcare expansion, which improves service availability. Expanding medical tourism is also strengthening investments, which is increasing the reliance on hospital facilities, where increasing urban hospital construction is also expanding their services. Rising focus on hospital modernization and increasing demand for quality care are also driving the upgradation of hospital facilities. High healthcare expenditure and robust emergency care services are also increasing their use.

Europe held a 27% share of the market and is expected to grow significantly during the forecast period, due to the presence of universal healthcare systems, which maintain hospital expansion. Sustainability initiatives are also modernizing facilities, where a rise in aging populations is supporting the growth in demand for hospital facilities. The growth in healthcare spending, investments, and government support are also fueling the digital transformation of healthcare facilities. Additionally, strong focus on emergency preparedness, expansion of specialty hospitals and rehabilitation centres are also enhancing the market growth.

Germany Market Growth

Germany held a 24% share in the hospital facilities market in 2025, driven by continued acceleration in hospital digitization. Strong reimbursement also supported growth in investments, where expansion of advanced specialty care facilities also encouraged their usage. High healthcare expenditures and large hospital networks also contributed to hospital facility modernization, as well as promoted the adoption of AI technology, new medical devices, and advanced equipment. Stringent focus on quality standards and patient safety also fueled their acceptance rate, while emergency preparedness also promoted their expansion.

The rest of Europe held a 15% share in the hospital facilities market in 2025 and is expected to witness the fastest growth with a CAGR of 6.60% over the forecast period, due to a rise in EU healthcare investments improving accessibility. Continued hospital upgrades and regional healthcare reforms are also supporting hospital facilities expansion. Increasing geriatric population and chronic disease burden are also increasing the dependence on these facilities, where growing adoption of advanced technologies, digital health solutions, and smart devices are also attracting patients. Growing government support and a shift towards sustainable hospital facilities are also promoting their advancements.

Asia Pacific held a 25% share of the market in 2025 and is expected to grow at the fastest CAGR of 8.40% during the forecast period, due to rapid urbanization, which is increasing healthcare demand. Growing government investments are expanding hospitals, where a rise in middle-class populations is also improving healthcare access. Increasing chronic disease burden is also driving the demand for advanced hospital services, where expanding health insurance coverage is also increasing their accessibility. Rising government initiatives are also supporting the development of specialty hospitals, digital health solutions, and smart hospitals, where expanding medical tourism is also promoting the market growth.

China Market Growth

China held a 34% share of the hospital facilities market in 2025, driven by continued large-scale hospital construction. Healthcare reforms also improved accessibility, where growth in smart hospital adoption also increased their use. Growth in chronic diseases and the geriatric population also increased the demand for hospital facilities. Rapid healthcare modernization supported by government investments also increased the adoption of various smart healthcare technologies and improved their accessibility. A focus on quality care, emergency preparedness, and infection control also enhanced their infrastructure.

India Market Growth

India held a 20% share in the hospital facilities market in 2025 and is expected to expand rapidly with a CAGR of 9.50% in the coming years, due to growing public and private investments, which are expanding hospital capacity. Rapid growth in medical tourism and healthcare infrastructure modernization are also increasing the demand and use of hospital facilities. The presence of a large population and a growing chronic disease burden are also increasing the use of these facilities for patient-centric care services, where expanding insurance coverage is also driving their demand. At the same time, growing government initiatives are increasing their accessibility as well as driving the adoption of new equipment and technologies.

Latin America held a 7% share in the market in 2025 and is expected to show lucrative growth during the forecast period, due to healthcare reforms increasing hospital investments. Private providers are expanding capacity, and a rise in chronic disease burden is also supporting growth in their demand. Growing population and chronic disease incidence are also increasing their use, while increasing adoption of digital health technologies is also attracting patients. A rise in government investments is also enhancing their accessibility, where strong regulatory preparedness and focus on patient safety are also increasing their use, which is fueling the market expansion.

Brazil Market Growth

Brazil held a 46% share in the hospital facilities market in 2025, driven by hospital modernization, which strengthens infrastructure. A rise in private healthcare investments and rapid urban expansion also supported capacity growth. The presence of extensive hospital networks and high healthcare expenditure also expanded accessibility to their services. The large patient population also increased their use, while growth in government support also promoted the adoption of advanced solutions. Furthermore, growing specialty hospitals and diagnostic facilities also increased their use.

The rest of Latin America held a 32% share in the hospital facilities market in 2025 and is expected to gain the highest market share with a CAGR of 7.20% during the forecast period, due to healthcare accessibility improving regionally. Increasing international investments are also driving their usage, where ongoing infrastructure development is also driving their expansion. Strong focus on patient safety and quality care is also increasing their use, while growing healthcare programs and government investments are also promoting their use and advancements. Rapid urbanization and emergency preparedness are also drveing their expansion.

MEA held a 5% share in the market in 2025 and is expected to show notable growth during the forecast period, due to government diversification strategies increasing healthcare investments. Smart hospitals are also gaining momentum, where growing medical tourism is also supporting their expansion. Growing patient population, demand for advanced medical solutions, and patient-centric care are also increasing the shift towards hospital facilities. Increasing focus on hospital modernization, infection control, and emergency preparedness are also encouraging their advancements, which is driving the market growth.

Saudi Arabia Market Growth

Saudi Arabia held a 35% share in the hospital facilities market in 2025, driven by national healthcare transformation, which accelerated hospital construction. Vision-driven investments also improved infrastructure, and expansion of private participation also increased the dependence on hospital facilities. Increased hospital modernization initiatives and medical tourism also increased their advancements and use, where growing specialty and outpatient services also enhanced their accessibility. Growth in advanced technology adoption and quality care services also increased their use, where a rise in healthcare investments also expanded the launch of specialty hospitals.

UAE Market Growth

United Arab Emirates (UAE) held a 28% share in the hospital facilities market in 2025 and is expected to show the fastest growth with a CAGR of 8.40% over the forecast period, due to a rise in medical tourism attracting premium investments. Smart hospital adoption is growing rapidly, where expanding digital healthcare is also leading to a rise in the adoption of various medical technologies. Growing demand for premium health services is also supporting the development of smart hospitals and specialty clinics, where growth in chronic disease burden is increasing their use. Furthermore, a strong focus on patient-centric care services is also increasing their usage, where government initiatives are driving their rapid expansion.

Strategic Planning

Hospital Design and Construction

Medical Equipment Integration

Clinical Operations

Facility Management

Continuous Modernization

Greenfield Projects

The greenfield projects focus on the development of new hospital construction with the latest medical technologies, supporting healthcare expansion.

Brownfield Expansion

Renovation and modernization of existing hospital facilities to expand their capacities and services are included in brownfield expansion.

Public-Private Partnerships

Increasing public-private partnerships are expanding collaborative financing models, accelerating healthcare infrastructure development.

Healthcare Real Estate Investments

Investment activity by infrastructure funds, REITs, sovereign wealth funds, and institutional investors for expanding hospital facilities are involved in healthcare real estate investments.

| Hospitals | Headquarters | Core Services |

| Mayo Clinic | Rochester, U.S. | Oncology, cardiology, neurology, diabetes, orthopedics, gastroenterology, and endocrinology |

| The Johns Hopkins Hospital | Baltimore, U.S. | Oncology, urological, psychiatric, behavioral, and children's services |

| Cleveland Clinic | Cleveland, U.S. | Cardiovascular, neurology, digestive diseases, urology, and kidney |

| Karolinska Universitetssjukhuset | Solna, Sweden | Oncology, pathology, cardiovascular, neurology, rare metabolic disease, transplantation, pediatrics, and cellular therapies |

| Toronto General Hospital | Toronto, Canada | Cardiac, multi-organ transplant, surgeries, and respiratory care |

| University Hospital Heidelberg | Württemberg, Germany | Oncology, neurology, cardiovascular, urology, and transplantation |

| Sheba Medical Center | Tel HaShomer, Israel | Oncology, heart, gastroenterology, hepatology, obstetrics, reproductive endocrinology, and rehabilitation services |

| West China Hospital | Chengdu, China | Neurology, anesthesiology, gastroenterology, pulmonary, hepatobiliary, and trauma care services |

| Charité | Berlin, Germany | Oncology, cardiac, and immunology |

| Singapore General Hospital | Outram, Singapore | Heart, cancer, bone marrow, dermatology, and hematology |

In September 2025, after the announcement by Medanta, highlighting the commencement of operations at its new 550-bedded hospital in Noida, its Chairman and Managing Director, Dr. Naresh Trehan, expressed, “Our new hospital in Noida marks another milestone in Medanta’s journey of bringing world-class healthcare to the people of India. With advanced infrastructure, cutting-edge technology, and a strong team of clinicians, this facility is designed to deliver comprehensive tertiary and quaternary care. Strategically located to serve patients across Delhi-NCR and Western Uttar Pradesh, it reinforces our commitment to expanding access to high-quality, patient-centric healthcare across the country.”

By Facility Type

By Ownership

By Bed Capacity

By Service Type

By Technology Integration

By End User

By Infrastructure

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar