")

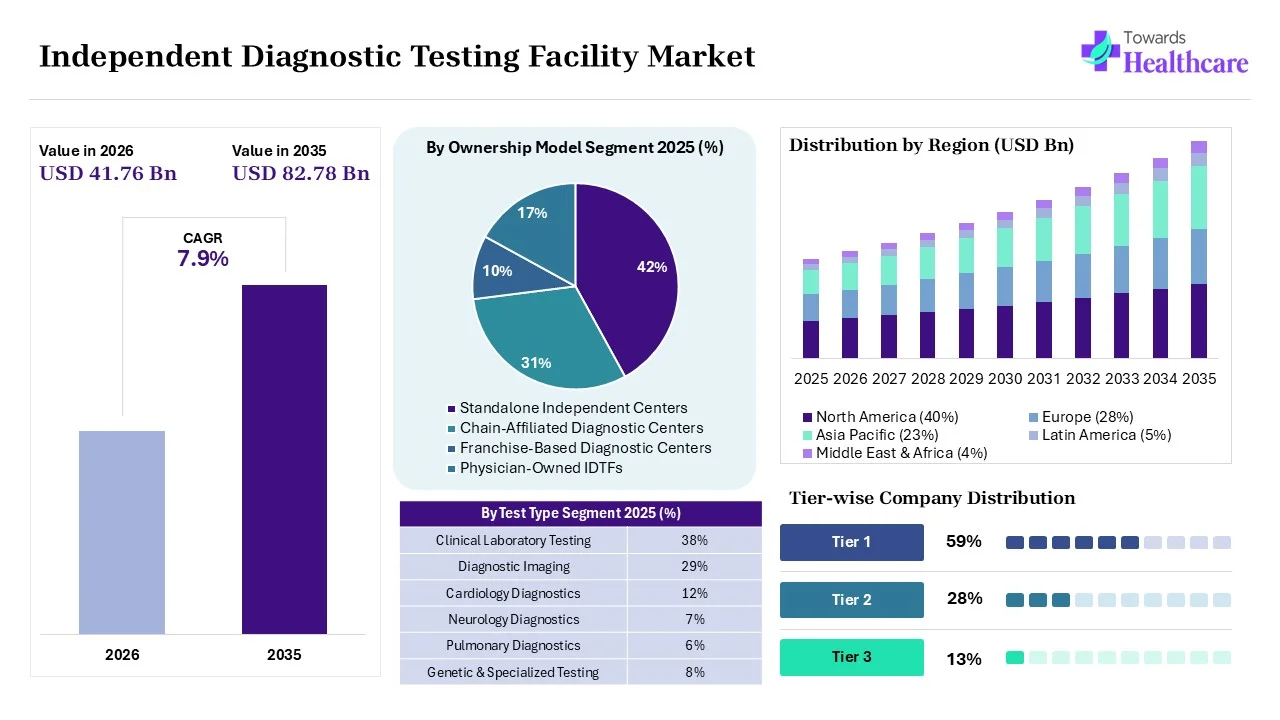

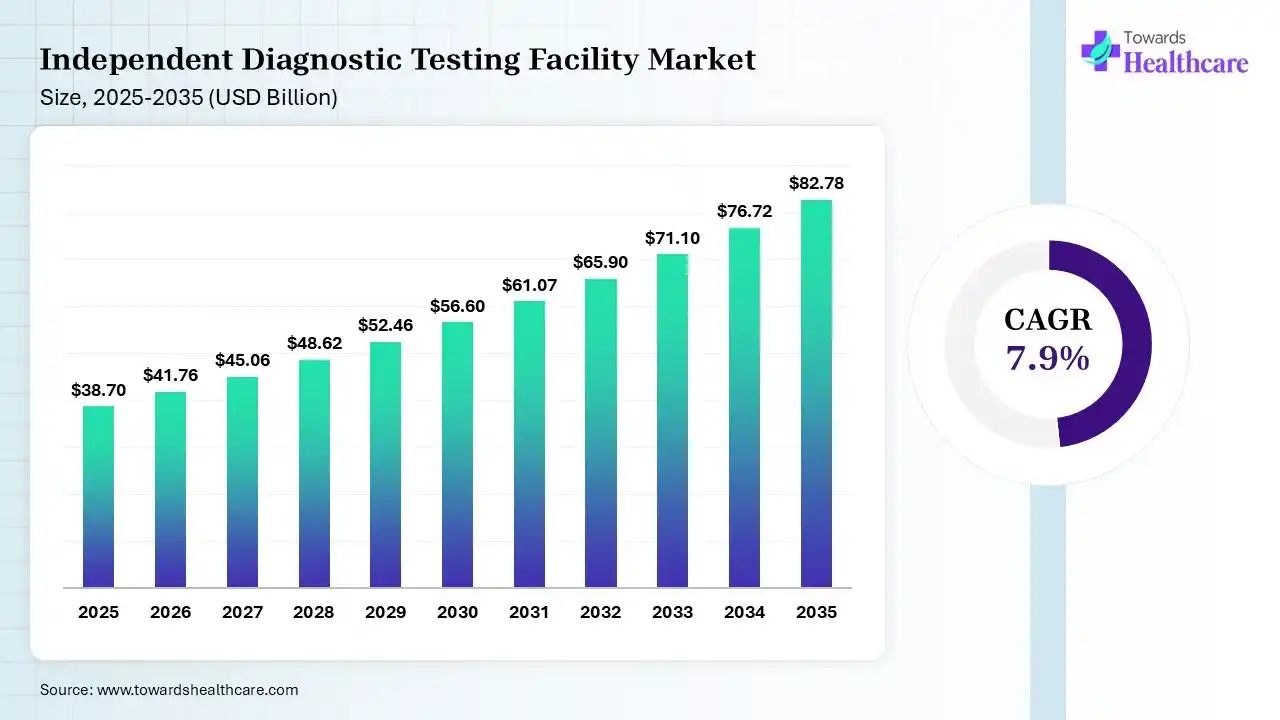

The independent diagnostic testing facility market size was estimated at USD 38.7 billion in 2025 and is predicted to increase from USD 41.76 billion in 2026 to approximately USD 82.78 billion by 2035, expanding at a CAGR of 7.9% from 2026 to 2035. The market grew in 2025 due to rising demand for diagnostic testing and early disease detection. In 2026, AI-powered diagnostics and preventive healthcare are driving market expansion. Future growth will be supported by decentralized testing and laboratory automation. North America led the market with 38% in 2025 because of advanced healthcare infrastructure and high testing volumes.

")

The independent diagnostic testing facility (DTF) market includes standalone centers that provide diagnostic services such as imaging and physiological testing outside hospital settings. Market growth is driven by the increasing demand for early disease detection, the rising prevalence of chronic diseases, and the growing preference for outpatient diagnostic services.

The market is being shaped by the adoption of AI-enabled diagnostics, digital imaging, and cloud-based healthcare solutions. Expanding prevention healthcare, mobile diagnostic services, and continuous advancements in diagnostic technologies are creating new growth opportunities and improving patient outcomes.

The independent diagnostic testing facility market is growing due to the increasing demand for early and accurate disease diagnosis, the rising prevalence of chronic diseases, and the growing demand for cost-effective outpatient care. Advancements in diagnostic imaging, artificial intelligence, and digital health technologies are improving testing efficiency and accuracy. Additionally, the expanding aging population, greater focus on preventive healthcare, and increasing access to specialized diagnostic services are further supporting market growth.

Technological advancements are transforming the Independent Diagnostic Testing Facility (IDTF) market by improving diagnostic accuracy, efficiency, and patient accessibility. The adoption of AI-powered image analysis, advanced imaging systems, cloud-based data management, and remote diagnostic solutions enables faster and more reliable test results. These innovations streamline clinical workflows, support early disease detection, reduce operational costs, and enhance the overall quality of outpatient diagnostic services.

Growing Adoption of AI-Enabled Diagnostics

Artificial intelligence is increasingly being integrated into diagnostic imaging and data analysis to improve accuracy, reduce reporting time, and support clinical decision-making. As AI technologies continue to evolve, Independent Diagnostic Testing Facilities (IDTFs) are expected to enhance operational efficiency while delivering faster and more reliable diagnostic services.

Expansion of Outpatient and Preventive Diagnostic Services

The growing emphasis on preventive healthcare and cost-effective outpatient care is driving demand for independent diagnostic facilities. IDTFs are expanding their service offerings and geographic reach to improve access to early disease detection, routine health screenings, and specialized diagnostic testing across diverse patient populations.

Integration of Digital Health and Remote Diagnostics

The adoption of cloud-based platforms, electronic health records, and remote diagnostic technologies is improving data sharing and care coordination. These digital advancements enable seamless communication between healthcare providers and diagnostic centers, supporting faster diagnoses, better patient management, and continued market growth.

| Table | Scope |

| Market Size in 2026 | USD 41.76 Billion |

| Projected Market Size in 2035 | USD 82.78 Billion |

| CAGR (2026 - 2035) | 7.9% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Test Type, By Facility Type, By Ownership Model, By Patient Type, By Technology, By Payer Type, By End User, By Region |

| Top Key Players | Quest Diagnostics Incorporated, Labcorp Holdings Inc., Sonic Healthcare Limited, Eurofins Scientific SE, Unilabs, SYNLAB AG, Fulgent Genetics, Inc. |

")

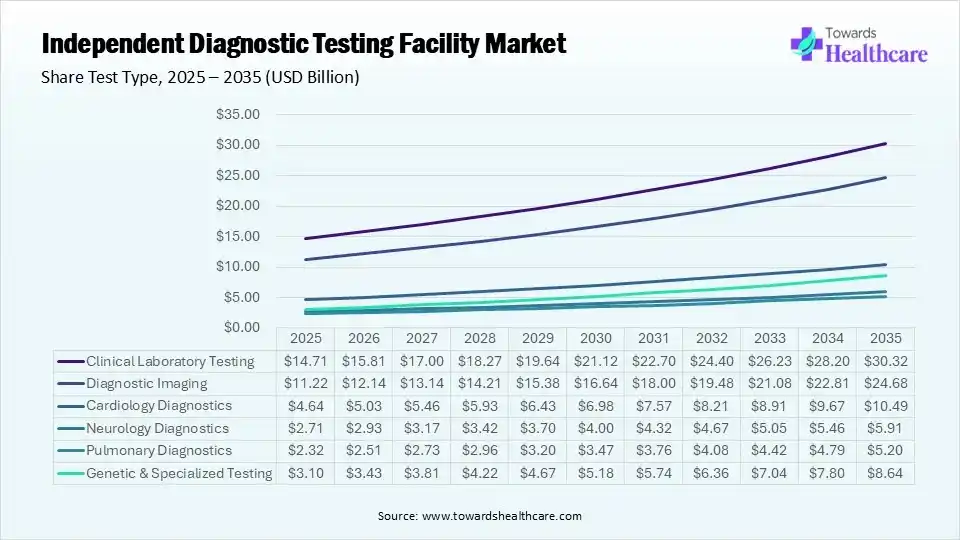

| Segment | Share 2025 (%) |

| Clinical Laboratory Testing | 38% |

| Diagnostic Imaging | 29% |

| Cardiology Diagnostics | 12% |

| Neurology Diagnostics | 7% |

| Pulmonary Diagnostics | 6% |

| Genetic & Specialized Testing | 8% |

The Clinical Laboratory Testing Segment Dominated the Independent Diagnostic Testing Facility Market in 2025

The clinical laboratory testing segment held a dominant share of 38% in 2025 due to its essential role in diagnostic, monitoring, and managing a wide range of acute and chronic diseases. Rising demand for routine blood tests, infectious disease screening, and preventive health checkups, coupled with increasing healthcare awareness and physician referrals, continues to drive high testing volumes and support the segment’s leading market share.

The diagnostic imaging segment held the second-largest share of 29% in 2025 due to the growing demand for early and accurate disease diagnosis. Increasing use of MRI, CT, X-ray, Ultrasound, and mammography for detecting chronic conditions, combined with advancements in imaging technologies and the preference for outpatient diagnostic services, continues to drive strong demand for this segment.

The cardiology diagnostics segment held a 12% of market share due to the increasing prevalence of cardiovascular diseases, the rising aging population, and the growing demand for early heart disease detection. Higher adoption of non-invasive diagnostic tests such as electrocardiograms (ECG), electrocardiography, stress testing, and Holter monitoring, along with advancements in cardiac diagnostic technologies and greater awareness of preventive cardiac care, are driving segment growth.

The genetic & specialized testing segment held 8% share in 2025 and is expected to grow at the fastest CAGR of 10.8% in the independent diagnostic testing facility market during the forecast period due to increasing demand for precision medicine, early disease detection, and personalized treatment approaches. Rising awareness of genetic disorders, expanding applications in oncology and rare disease diagnosis, and continuous advancements in molecular diagnostic and next-generation sequencing technologies are further accelerating the adoption of specialized testing services.

")

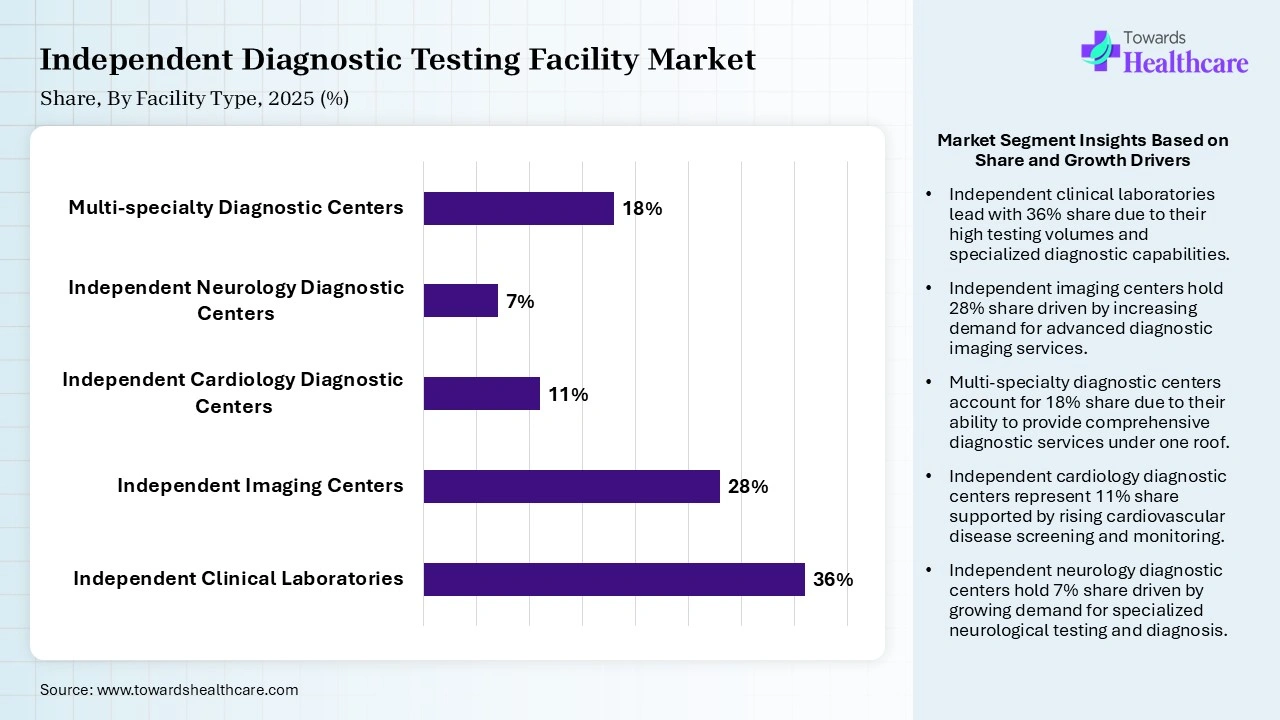

| Segment | Share 2025 (%) |

| Independent Clinical Laboratories | 36% |

| Independent Imaging Centers | 28% |

| Independent Cardiology Diagnostic Centers | 11% |

| Independent Neurology Diagnostic Centers | 7% |

| Multi-specialty Diagnostic Centers | 18% |

The Independent Clinical Laboratories Segment Led the Market in 2025 with the Largest Share

The independent clinical laboratories segment dominated the independent diagnostic testing facility market with a share of 36% in 2025 due to the high volume of routine and specialized laboratory tests performed for disease diagnosis, monitoring, and preventive healthcare. Increasing demand for blood tests, infectious disease screening, and chronic disease management, combined with cost-effective testing services, advanced laboratory automation, and blood physician referrals, continues to strengthen the segment’s leading market position.

The independent imaging centers segment held the second-largest share of 28% in 2025 due to the rising demand for advanced imaging procedures, including MRI, CT, X-ray, ultrasound, and mammography. These centers offer cost-effective, convenient, and faster diagnostic services compared to hospitals, while continuous advancements in imaging technologies and increasing outpatient visits further support their strong market position.

The multi-specialty diagnostic centers segment held 18% share in 2025 and is expected to grow at the fastest CAGR of 9.5% during 2026-2035 in the independent diagnostic testing facility market during the forecast period due to increasing demand for comprehensive diagnostic services under one roof. These centers offer greater convenience, faster diagnosis, and are integrated across multiple specialties. Rising healthcare awareness, expanding preventive screening programs, technological advancements, and the growing preference for outpatient healthcare services are further accelerating segment growth.

The independent cardiology diagnostic centers segment held a 11% of market share due to the rising prevalence of cardiovascular diseases and increasing demand for early cardiac risk assessment. Growing adoption of non-invasive diagnostic procedures, such as ECG, echocardiography, stress testing, and Holter monitoring, along with expanding outpatient cardiac care services and advancements in cardiac imaging technologies, is driving the rapid growth of this segment.

")

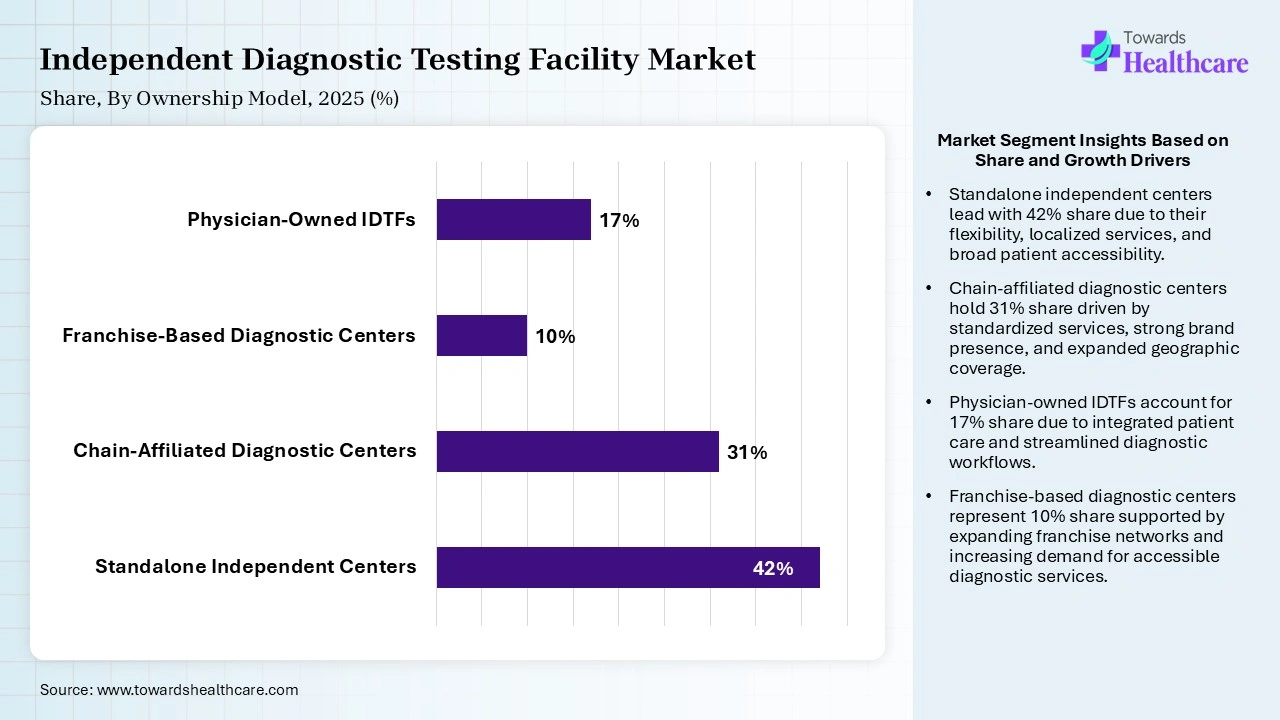

| Segment | Share 2025 (%) |

| Standalone Independent Centers | 42% |

| Chain-Affiliated Diagnostic Centers | 31% |

| Franchise-Based Diagnostic Centers | 10% |

| Physician-Owned IDTFs | 17% |

The Standalone Independent Centers Segment Led the Independent Diagnostic Testing Facility Market in 2025 with the Largest Share

The standalone independent centers segment led the market with a share of 42% in 2025 due to their widespread accessibility, cost-effective diagnostic services, and operational flexibility. These facilities offer faster appointment scheduling, shorter waiting times, and a broad range of diagnostic tests outside hospital settings. Growing patient preference for convenient outpatient care and increasing investments in independent healthcare infrastructure continue to support the segment market leadership.

The chain-affiliated diagnostic centers segment held the second-largest share of 31% in 2025 due to their standardized service quality, broad geographic presence, and strong brand recognition. These centers benefit from centralized operations, advanced diagnostic technologies, and efficient patient management systems. Increasing investments in network expansion and rising demand for reliable outpatient diagnostic services continue to strengthen their market position.

The physician-owned IDTFs segment held a 17% of market share due to increasing demand for integrated, patient-centered diagnostic services and improved care coordination. These facilities enable physicians to provide timely diagnostic testing, accelerating clinical decision-making, and enhancing patient convenience. Rising adoption of value-based healthcare, growing preference for outpatient services, and investments in advanced diagnostic technologies are further driving the growth of physician-owned IDTFs.

The franchise-based diagnostic centers segment held 10% share in 2025 and is expected to grow at the fastest CAGR of 9.8% in the independent diagnostic testing facility market during the forecast period due to its scalable business model, lower investment requirements, and rapid geographic expansion. Franchise networks enable standardized diagnostic services, strong brand recognition, and access to advanced technologies. Increasing demand for affordable outpatient diagnostics, particularly in underserved and emerging regions, is further accelerating the growth of this segment.

")

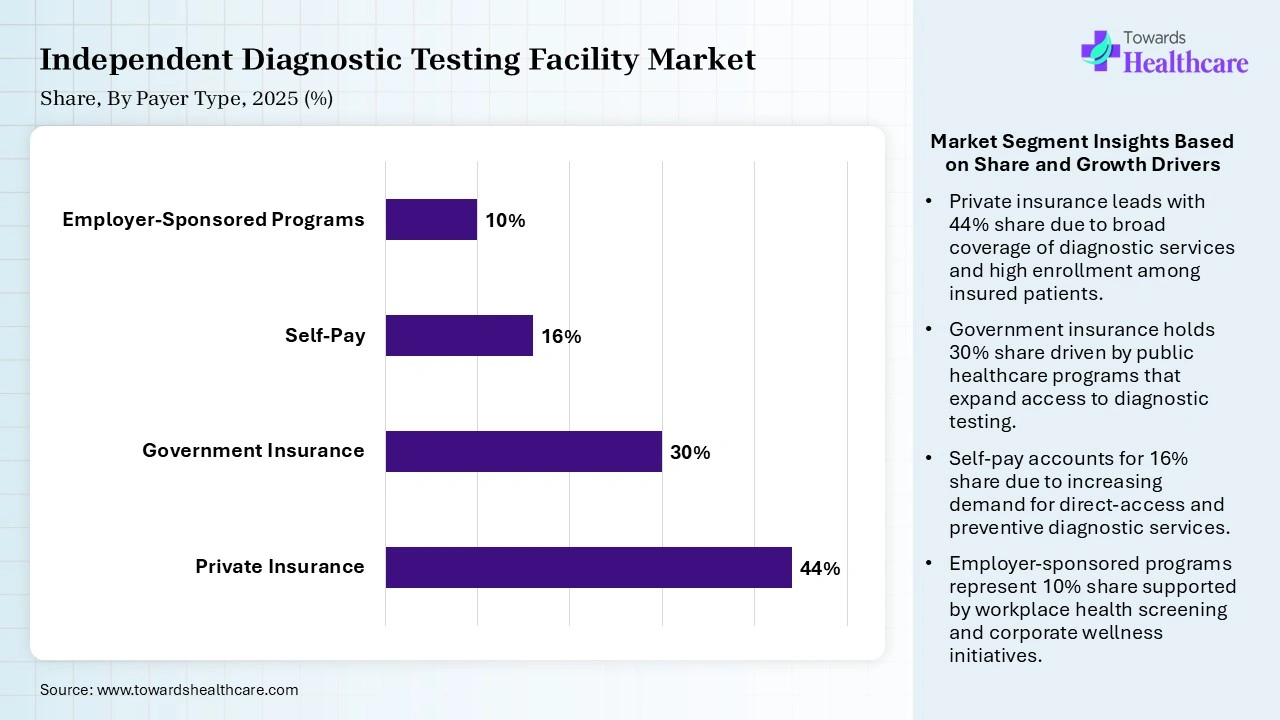

| Segment | Share 2025 (%) |

| Private Insurance | 44% |

| Government Insurance | 30% |

| Self-Pay | 16% |

| Employer-Sponsored Programs | 10% |

The Private Insurance Segment Led the Independent Diagnostic Testing Facility Market in 2025 with the Largest Share

The private insurance segment dominated the market with a share of 44% in 2025 due to broad insurance coverage for outpatient diagnostic services, faster reimbursement processes, and greater access to advanced diagnostic tests. High enrollment in employer-sponsored and commercial health insurance plans, along with increasing utilization of preventive healthcare and specialized diagnostic services, continues to drive patient volumes and strengthen the segment’s leading market position.

The government insurance segment held the second-largest share of 30% in 2025 due to extensive coverage provided through public healthcare programs for eligible populations, particularly older adults and low-income individuals. Rising prevalence of chronic diseases, increasing utilization of diagnostic services, and government initiatives promoting early disease detection and preventive healthcare continue to drive demand within this segment.

The self-pay segment held 16% share in 2025 and is expected to grow at the fastest CAGR of 8.8% in the independent diagnostic testing facility market during the forecast period due to rising demand for preventive health screenings, increasing availability of affordable diagnostic packages, and greater consumer preference for direct access to diagnostic services. Growing uninsured and underinsured populations, along with increasing healthcare awareness and faster outpatient testing options, are further accelerating the adoption of self-pay diagnostic services.

The employer-sponsored programs segment held a 10% of market share due to increasing corporate investments in employee wellness, preventive healthcare, and occupational health screening initiatives. Employers are encouraging routine diagnostic testing to improve workforce health, reduce healthcare costs, and enhance productivity. Rising adoption of workplace health programs. expanding health insurance benefits, and growing awareness of early disease detection are further driving the growth of this segment.

")

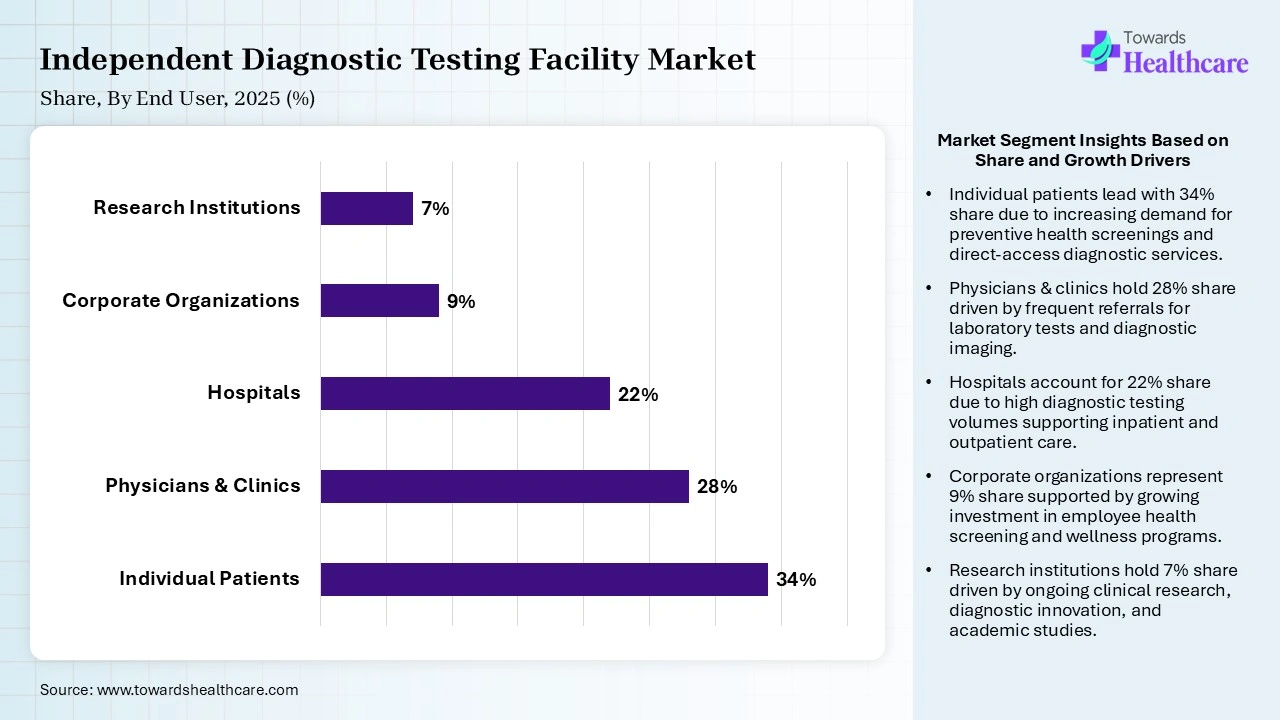

| Segment | Share 2025 (%) |

| Individual Patients | 34% |

| Physicians & Clinics | 28% |

| Hospitals | 22% |

| Corporate Organizations | 9% |

| Research Institutions | 7% |

The Individual Patients Segment Led the Market in 2025 with the Largest Share

The individual patients segment dominant share of the independent diagnostic testing facility market of 34% in 2025 due to the high demand for routine health checkups, chronic disease monitoring, and early disease diagnosis. Increasing healthcare awareness, growing preference for convenient outpatient diagnostic services, and rising prevalence of chronic and age-related conditions continue to drive patient visits. Improved accessibility and cost-effective testing services further strengthened the segment’s leading market position.

The physicians & clinics segment held the second-largest share of 28% in 2025 due to frequent referrals for laboratory and imaging tests to support diagnosis and treatment decisions. Increasing outpatient consultation, rising prevalence of chronic diseases, and growing emphasis on early disease detection continue to drive demand for independent diagnostic services, strengthening the segment’s significant market position.

The hospitals segment held a 22% of market share due to the increasing need for specialized diagnostic testing, advanced imaging, and laboratory services to support complex patient care. Hospitals are increasingly partnering with independent Diagnostic Testing Facilities (IDTFs) to improve diagnostic efficiency, reduce operational burden, and expand service capacity. Rising hospital admissions, chronic disease prevalence, and demand for accurate, timely diagnoses continue to drive segment growth.

The research institutions segment held 7% share in 2025 and is expected to grow at the fastest CAGR of 9.3% in the independent diagnostic testing facility market during the forecast period due to increasing investments in clinical research, biomarker discovery, and precision medicine. Rising collaborations between research organizations and diagnostic facilities, growing testing, and continuous advancements in diagnostic technologies are accelerating the adoption of independent diagnostic testing services in research applications.

North America dominated the market with a share of 38% in 2025 due to its mature outpatient diagnostic ecosystem and high integration of laboratory and imaging services. Strong collaboration between healthcare providers, insurers, and diagnostic networks has improved patient access to timely testing. The region also benefits from widespread adoption of digital pathology, laboratory automation, and AI-enabled imaging technologies. Increasing demand for precision diagnostics, routine health screening, and decentralized testing further reinforces North America's dominant market position.

U.S. Dominates the North American Independent Diagnostic Testing Facility Market

The U.S. dominated the market with a share of 30% in 2025 due to its extensive network of independent laboratories, imaging centers, and physician-referred diagnostic facilities. High utilization of advanced molecular testing, genetic diagnostics, and specialized laboratory services has increased testing volumes across outpatient settings. Continuous investments by leading diagnostic companies, strong private insurance coverage, and rapid commercialization of innovative diagnostic technologies continue to position the U.S. as the region's primary growth engine.

Canada Emerges as the Fastest-Growing Market for Independent Diagnostic Testing Facilities Market

Canada held the second-largest share of 5% in 2025 as healthcare systems increasingly expand community-based diagnostic services to reduce hospital burden. Investments in modern laboratory infrastructure, digital health integration, and advanced imaging capabilities are improving access to diagnostic care. The growing emphasis on preventive screening, shorter diagnostic turnaround times, and expansion of independent diagnostic centers across underserved regions are creating favorable conditions for sustained market growth.

The Asia Pacific held 24% share of the market in 2025 and is expected to grow at the fastest CAGR of 10.2% in the market during the forecast period due to the rapid expansion of private diagnostic chains and increasing accessibility of outpatient testing services. Rising disposable incomes, improving health insurance coverage, and growing demand for affordable diagnostics are encouraging patients to seek independent testing facilities. Technological advancements in molecular diagnostics, telepathology, and AI-assisted imaging, along with increasing investments from domestic and international healthcare providers, are further supporting regional market expansion.

China Leads the Asia Pacific Independent Diagnostic Testing Facility Market

China dominated the market with a share of 8% in 2025 by continuously expanding its diagnostic capacity through large-scale investments in laboratory infrastructure and advanced imaging facilities. The country's focus on strengthening disease surveillance, preventive health programs, and precision medicine has accelerated demand for specialized diagnostic testing. Growing collaboration between public healthcare institutions and private diagnostic providers, coupled with rapid adoption of automation technologies, continues to enhance China's leadership in the regional market.

India Sets the Pace for Future Growth in Independent Diagnostic Testing Facilities

India held 4% share in 2025 and is expected to grow at the fastest CAGR of 11.8% in the market during the forecast period due to the rapid expansion of organized diagnostic chains into Tier II and Tier III cities. Increasing consumer preference for preventive health packages, home-based sample collection, and digital diagnostic platforms is reshaping the market. Rising investments from private healthcare providers, greater availability of affordable diagnostic services, and expanding use of advanced laboratory technologies are expected to significantly accelerate the growth of independent diagnostic testing facilities across the country.

R&D

Clinical Trials

Patient Support and Services

| Companies | Headquarter | Offerings |

| Quest Diagnostics Incorporated | Secaucus, New Jersey, U.S. | Clinical laboratory testing, pathology services, genetic testing, esoteric diagnostics, and employer health screening |

| Labcorp Holdings Inc. | Burlington, North Carolina, U.S. | Clinical laboratory testing, specialty diagnostics, genetic testing, drug testing, and clinical trial laboratory services |

| Sonic Healthcare Limited | Sydney, Australia | Clinical laboratory services, pathology, radiology, genomic testing, and diagnostic imaging |

| Eurofins Scientific SE | Luxembourg City, Luxembourg | Clinical diagnostics, specialty laboratory testing, molecular diagnostics, genomics, biomarker testing |

| Unilabs | Geneva, Switzerland | Laboratory diagnostics, diagnostic imaging, pathology, radiology, and preventive health screening |

| SYNLAB AG | Munich, Germany | Clinical laboratory testing, molecular diagnostics, pathology, genetic testing, and medical imaging services |

| Fulgent Genetics, Inc. | El Monte, California, U.S. | Genetic testing, precision diagnostics, molecular diagnostics, oncology testing, infectious disease testing |

In June 2026, “At Thyrocare, we envision making trustworthy and state-of-the-art diagnostic services attainable for every Indian household. The rollout of our new facility indicates our persistent efforts to expand our presence while mitigating diagnostic gaps through a patient-focused and technology-led approach.” Rahul Guha, MD and CEO, Thyrocare, said.

By Test Type

By Facility Type

By Ownership Model

By Patient Type

By Technology

By Payer Type

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar