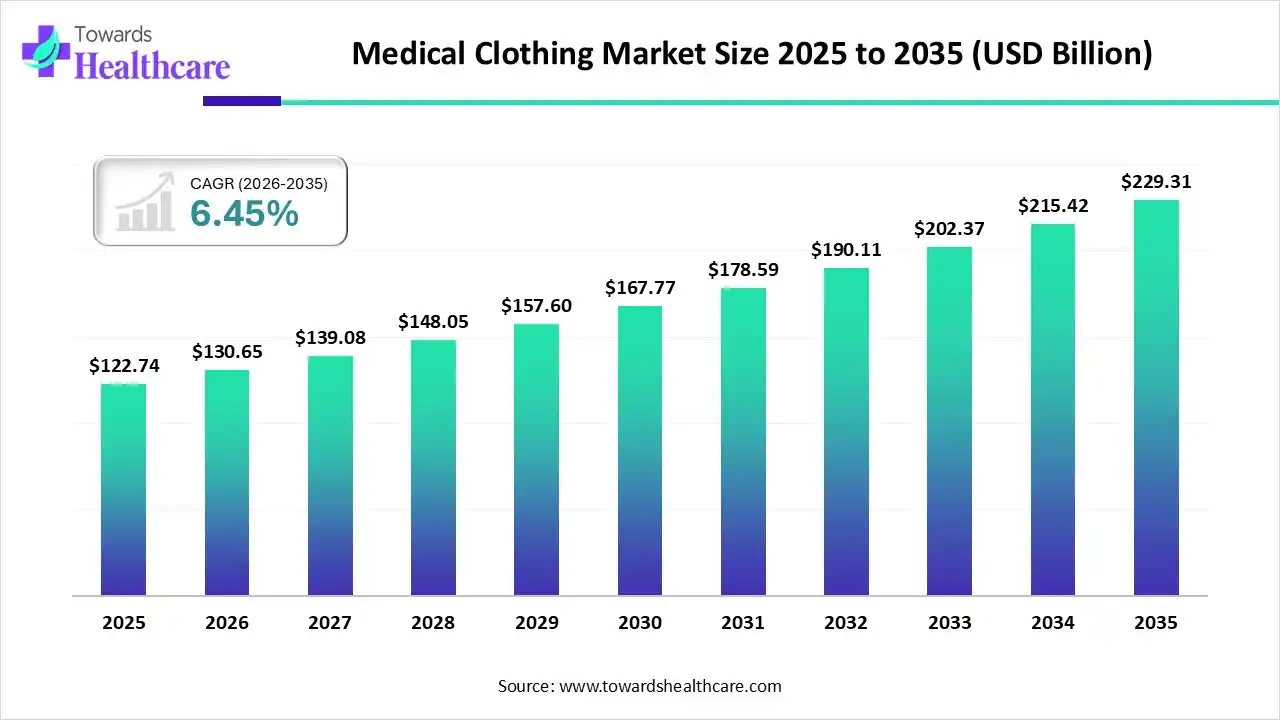

The global medical clothing market size was estimated at USD 122.74 billion in 2025 and is predicted to increase from USD 130.65 billion in 2026 to approximately USD 229.31 billion by 2035, expanding at a CAGR of 6.45% from 2026 to 2035.

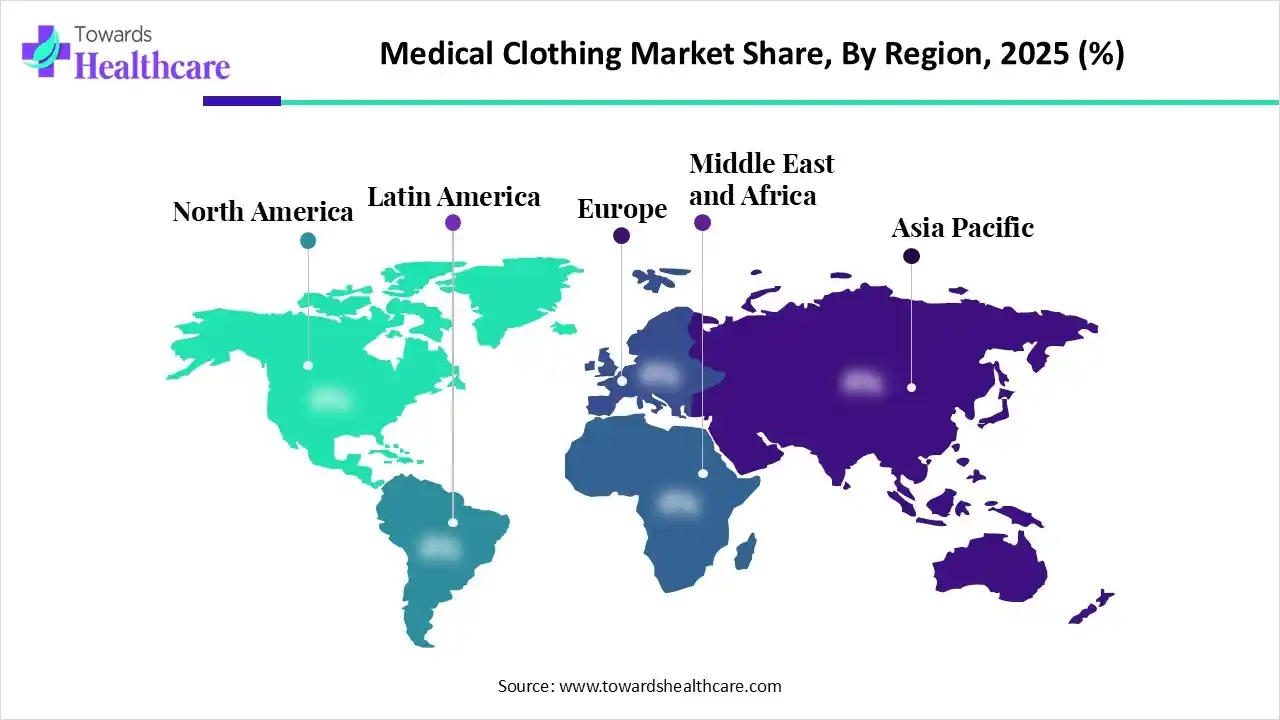

The global medical clothing market is experiencing steady growth, supported by increasing demand for infection-control apparel such as surgical gowns, scrubs, and protective wear. Expansion of healthcare facilities and stricter safety regulations are further supporting adoption. North America dominated the market, holding the largest share, supported by well-established healthcare infrastructure, high healthcare expenditure, and strong compliance with quality and safety standards.

The medical clothing market refers to the sector focused on the production, distribution, and sale of specialized garments used in healthcare settings, including hospitals, clinics, and outpatient facilities. These garments, such as scrubs, surgical gowns, lab coats, and patient apparel, are designed to ensure hygiene, safety, and comfort for both healthcare professionals and patients. The market is driven by increasing awareness of infection control, rising patient visits, stringent healthcare regulations, and the growing demand for sterile and durable medical apparel. Technological advancements in fabrics, such as antimicrobial, fluid-resistant, and breathable materials, further propel market adoption.

Growing healthcare infrastructure investments across emerging economies are creating new opportunities for manufacturers to expand their product portfolios and geographic presence. Demand is also increasing for reusable and sustainable medical garments as healthcare facilities seek to reduce waste and operational costs while maintaining compliance with safety standards. The integration of smart textiles, including sensor-enabled fabrics that can monitor temperature, movement, or physiological indicators, is gaining attention in advanced healthcare environments. In addition, rising employment of healthcare professionals and the expansion of ambulatory care centers contribute to consistent apparel consumption.

E-commerce platforms and direct procurement channels are improving product accessibility, enabling healthcare organizations to source customized, high-quality clothing solutions more efficiently across diverse clinical settings and evolving patient care requirements globally.

AI integration can significantly enhance the medical clothing market by improving design precision, manufacturing efficiency, and product performance. AI-driven fabric analytics enable the development of garments with optimized breathability, durability, and fluid resistance. In manufacturing, AI supports predictive maintenance, quality inspection, and demand forecasting, reducing defects and waste. AI-enabled supply chains improve inventory planning and responsiveness during healthcare surges. Additionally, AI helps analyze user feedback and clinical data to refine fit, comfort, and safety compliance. Overall, AI adoption supports faster innovation, cost optimization, and consistent quality across medical clothing products while meeting evolving healthcare standards.

Rise of Antimicrobial and Infection-Control Fabrics:

Medical clothing is increasingly made from antimicrobial and antibacterial fabrics that reduce the risk of infections. These fabrics help maintain hygiene in hospitals, clinics, and outpatient facilities, responding to rising awareness of workplace safety and patient protection.

Adoption of Ergonomic and Comfortable Designs:

Healthcare professionals prefer scrubs and uniforms designed for comfort, flexibility, and ease of movement. Ergonomic designs reduce fatigue during long shifts, improve productivity, and enhance the overall workplace experience, driving demand for modern, functional medical apparel.

Growth of Sustainable and Eco-Friendly Clothing:

Manufacturers are using recycled, biodegradable, and environmentally friendly materials to produce medical clothing. This trend reflects increasing focus on sustainability and corporate responsibility while meeting consumer demand for green and eco-conscious products.

Integration of Smart and Wearable Technology:

Medical garments are being embedded with sensors to monitor health parameters or track usage. Smart clothing enhances efficiency, supports patient care, and provides data-driven insights, representing the intersection of healthcare and technology in the apparel sector.

Expansion of Direct-to-Consumer (B2C) Channels:

Online platforms, e-commerce, and home delivery services are boosting B2C sales of medical clothing. Individual healthcare professionals and home-care providers increasingly purchase directly, seeking personalized, convenient, and quickly available products.

Focus on Customization and Personalization:

Hospitals and professionals demand clothing tailored to specific needs, including size, color, or functional features. Customization enhances branding, comfort, and identity, becoming a key differentiator in the competitive medical clothing market.

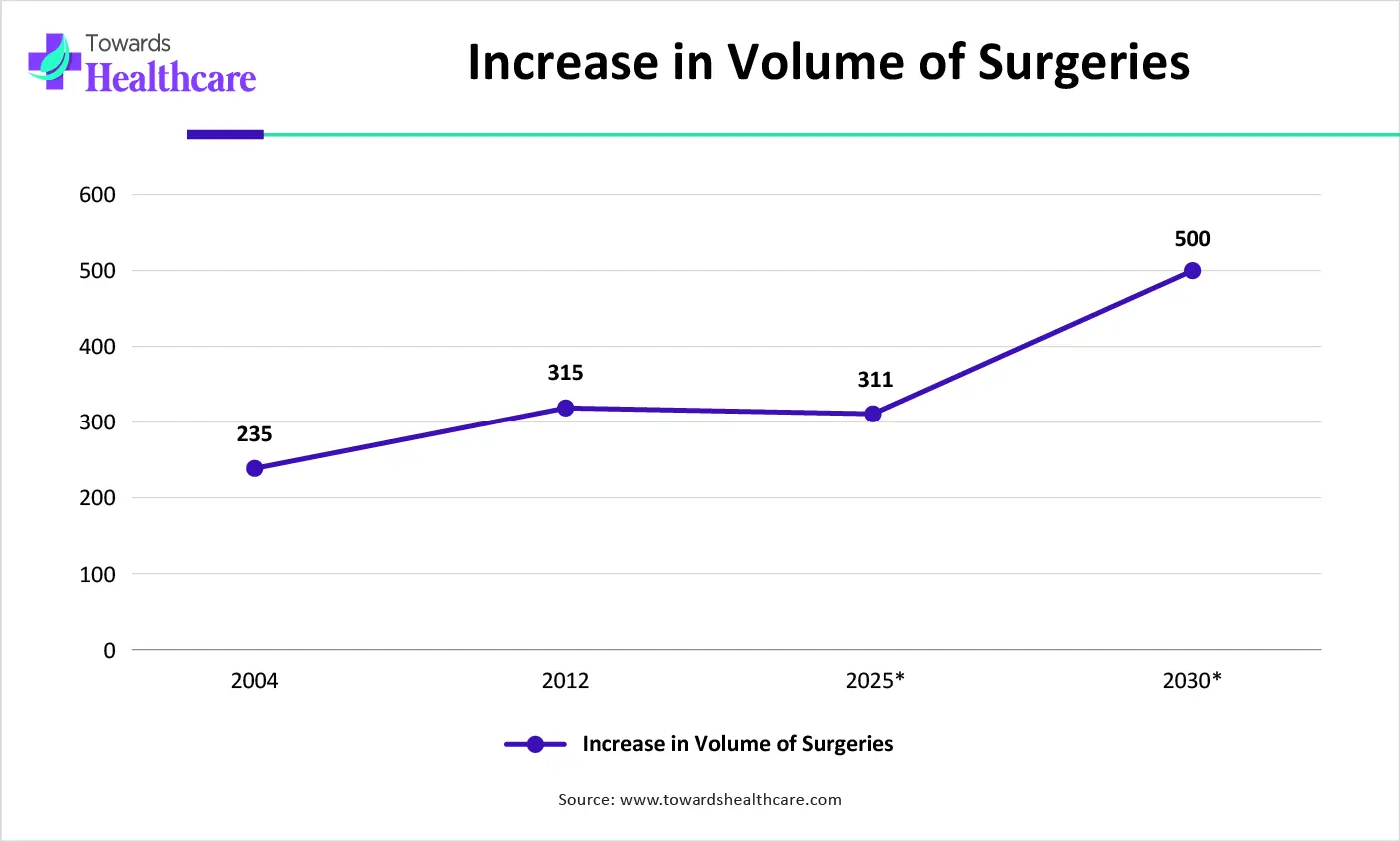

| Year | Estimated Surgeries (million) | Source |

| ~2004 | ~234 | WHO estimate-: https://iris.who.int/bitstream/handle/10665/42891/924156265X.pdf |

| ~2012 | ~313 (estimate) | PubMed analysis-: https://pmc.ncbi.nlm.nih.gov/articles/PMC8460445 |

| 2025 | ~300+ | Recent estimate-: https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(25)00985-7/abstract |

| 2030 (proj) | ~430–550 | WHO delivered projection-: https://pmc.ncbi.nlm.nih.gov/articles/PMC5321301/ https://www.cdc.gov/nchs/fastats/inpatient-surgery.htm |

| Key Elements | Scope |

| Market Size in 2026 | USD 130.65 Billion |

| Projected Market Size in 2035 | USD 229.31 Billion |

| CAGR (2026 - 2035) | 6.45% |

| Leading Region | North America by 40% |

| Key Applications | Surgery, Infection Control, Clinical Care, Laboratory Operations, Emergency Response, Patient Care |

| Primary End Users | Hospitals, Ambulatory Surgical Centers, Clinics, Laboratories, Long-Term Care Facilities, Healthcare Workers |

| Key Challenges | Pricing pressure, regulatory compliance, supply chain disruptions, counterfeit products, sustainability concerns |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By Type, By Usage, By End-user, By Sales Channel, By Region |

| Top Key Players | 3M Company, Cardinal Health, Inc., Medline Industries, LP, Mölnlycke Health Care AB, Ansell Limited, Halyard Health (Owens & Minor), Alpha Pro Tech, Ltd., Lohmann & Rauscher |

| Segments | Shares % |

| Surgical Drapes, Scrubs & Gowns | 30% |

| Gloves | 20% |

| Facial Protection | 15% |

| Sterilization Wraps | 10% |

| Protective Apparel | 10% |

| Others | 15% |

Which Product Segment Dominated the Medical Clothing Market?

The surgical drapes, scrubs & gowns segment dominates the market by 30% due to their routine and mandatory use across hospitals, operating rooms, and outpatient settings. High procedure volumes, strict infection-control protocols, and frequent replacement requirements drive consistent demand. Additionally, standardized guidelines for sterile environments and growing emphasis on healthcare worker and patient safety further reinforce the segment’s leading position.

Facial Protection

The facial protection segment is estimated to be the fastest-growing segment in the market due to increasing awareness of airborne infections and rising demand for masks, face shields, and respirators in hospitals and clinics. Frequent use during surgical procedures, pandemics, and routine healthcare operations, along with stringent safety regulations, drives adoption. Innovations in comfort, breathability, and antiviral materials further accelerate market growth.

| Segments | Shares % |

| For Healthcare Professional | 60% |

| For Patient | 40% |

Why Did the for Healthcare Professional Segment Dominate the Medical Clothing Market?

The for healthcare professional segment dominates the market by 60% share due to consistent and high demand from doctors, nurses, and hospital staff. Strict infection-control protocols, mandatory use of protective apparel, and frequent replacement of scrubs, gowns, and lab coats reinforce adoption. Additionally, growing awareness of workplace safety and standardized hospital dress codes further strengthens this segment’s leading position in the market.

For Patient

The for-patient segment is anticipated to be the fastest-growing in the market due to rising hospital admissions, increasing outpatient procedures, and growing awareness of patient hygiene and infection prevention. Demand for comfortable, disposable, and easy-to-wear patient gowns is rising, driven by hospitals’ focus on patient safety, convenience, and compliance with hygiene protocols, fueling rapid adoption of this segment.

| Segments | Shares % |

| Disposable | 70% |

| Reusable | 30% |

Why Did the Above Disposable Dominant Segment in the Medical Clothing Market?

The disposable segment dominates the market by 70% share due to its convenience, hygiene, and ability to prevent cross-contamination in healthcare settings. High usage in surgeries, clinics, and emergency care, coupled with strict infection-control protocols, drives consistent demand. Additionally, hospitals and medical facilities prefer cost-effective, single-use garments for staff and patients, reinforcing the disposable segment’s leading position.

Reusable

The reusable segment is estimated to be the fastest-growing in the market due to increasing focus on sustainability and environmental concerns. Hospitals and clinics are adopting washable, durable gowns, scrubs, and protective apparel to reduce medical waste. Advances in antimicrobial fabrics and sterilization technologies enhance safety and longevity, while cost-efficiency over repeated use drives rapid adoption in healthcare facilities.

| Segments | Shares % |

| Hospitals | 50% |

| Outpatient Facilities | 25% |

| Physicians’ Offices | 15% |

| Others | 10% |

Which End-User Segment Led the Medical Clothing Market?

The hospitals segment dominates the market by 50% share due to high patient volumes, diverse medical procedures, and strict infection-control protocols. Continuous demand for surgical gowns, scrubs, and protective apparel for healthcare professionals and patients reinforces adoption. Additionally, hospitals’ focus on safety, standardized dress codes, and frequent replacement of medical clothing solidify this segment’s leading position in the market.

Outpatient Facilities

The outpatient facilities segment is anticipated to be the fastest-growing segment in the medical clothing market due to increasing outpatient procedures, rising patient visits, and heightened awareness of hygiene and infection control. Demand for disposable and comfortable gowns, scrubs, and protective apparel is expanding rapidly. Additionally, smaller facilities prioritize cost-effective, easy-to-use medical clothing, fueling growth in this segment.

| Segments | Shares % |

| B2B (Business-to-Business) | 60% |

| B2C (Business-to-Consumer) | 30% |

| Online | 5% |

| Retail Stores | 5% |

Why Did B2B (business-to-business) sales channel Dominant Segment in the Medical Clothing Market?

The B2B (business-to-business) channel segment dominates the market by 60% share due to long-term contracts with hospitals, clinics, and healthcare institutions, ensuring consistent bulk orders. Strong relationships with distributors, suppliers, and institutional buyers facilitate large-scale procurement, while customized product offerings and compliance with healthcare regulations further strengthen B2B adoption. Additionally, centralized purchasing processes in healthcare organizations drive higher demand through this channel.

B2C channel

The B2C (business-to-consumer) channel segment is anticipated to be the fastest-growing segment in the medical clothing market due to increasing consumer awareness about hygiene, comfort, and professional appearance. Online platforms and e-commerce enable direct access to a wide range of products, while personalized options and convenient doorstep delivery attract individual buyers. Rising demand from self-employed healthcare professionals and home-care providers also fuels this growth.

")

North America dominates the market with share of 40% in 2025, due to strong emphasis on infection prevention, widespread use of certified protective apparel, and well-established healthcare infrastructure. High awareness of worker safety, strict regulatory compliance, and consistent demand from hospitals, clinics, and ambulatory centers further support adoption. Continuous product innovation and early acceptance of advanced medical textiles also reinforce the region’s leading position.

U.S Market Trends

The U.S. leads the North American market due to its extensive hospital network, high procedural volumes, and strong focus on healthcare worker safety. Stringent regulatory standards, rapid adoption of advanced and disposable medical apparel, and consistent procurement by public and private healthcare institutions further support demand. The presence of major manufacturers and continuous innovation also reinforces the country’s dominant position.

Canada Market Trends

Canada’s medical clothing market is expanding through strong healthcare spending, infection-control priorities, and modernization of hospital infrastructure. Provincial health systems continue investing in protective apparel and reusable surgical textiles to improve sustainability. Rising demand for antimicrobial fabrics and ergonomic scrubs is shaping procurement decisions. Canada’s aging population and growing outpatient care network are increasing apparel consumption, while domestic manufacturers are benefiting from government support for resilient healthcare supply chains and local production initiatives.

Mexico Market Trends

Mexico’s medical clothing market is growing due to healthcare infrastructure expansion, increased hospital admissions, and stronger infection-prevention standards. Government programs aimed at improving public healthcare access are boosting demand for affordable, high-quality medical apparel. The country’s large manufacturing base supports local production of scrubs, gowns, and protective clothing for both domestic use and export. Rising private healthcare investments and medical tourism are also contributing to sustained market growth nationwide.

Asia-Pacific is the fastest-growing region in the medical clothing market by 20% share due to the rapid expansion of healthcare infrastructure, rising hospital admissions, and increasing awareness of infection control. Growth in medical tourism, supportive government initiatives for local manufacturing, and rising investments in healthcare facilities further accelerate demand. Additionally, improving regulatory standards and growing adoption of disposable and protective medical apparel contribute to strong regional growth momentum.

India Market Trends

India’s medical clothing market is witnessing rapid growth driven by expanding healthcare infrastructure, rising hospitalization rates, and stricter hygiene standards after the pandemic. Government initiatives such as Ayushman Bharat and increased public health spending are improving healthcare access and boosting demand for medical apparel. India’s strong textile manufacturing ecosystem supports large-scale production of cost-effective scrubs, gowns, and PPE, while growing private hospitals and diagnostic centers further accelerate market expansion.

China Market Trends

China dominates the Asia-Pacific market due to its large healthcare system, strong domestic manufacturing base, and cost-efficient production capabilities. Widespread hospital expansion, high demand for protective medical apparel, and government support for medical textile manufacturing strengthen supply. Additionally, China’s ability to scale production rapidly and serve both domestic and export markets reinforces its leading regional position.

Japan Market Trends

Japan’s medical clothing market is advancing steadily due to its aging population, high healthcare utilization, and emphasis on patient safety and hygiene. Hospitals increasingly prefer high-performance, breathable, and antimicrobial fabrics to improve staff comfort and infection control. Government support for healthcare modernization and eldercare services is strengthening demand for specialized medical apparel. Japan’s focus on quality standards and technological innovation is encouraging adoption of premium, durable, and reusable medical clothing solutions.

Europe is a notably growing region in the market share 30% due to increasing focus on healthcare worker safety, stringent infection-control regulations, and rising adoption of certified protective apparel. Expansion of public healthcare systems, aging population-driven hospital demand, and growing preference for sustainable and reusable medical clothing further support regional growth. Continuous regulatory updates and emphasis on quality standards also encourage consistent market expansion.

UK Market Trends

The UK dominates the European medical clothing market due to its well-established public healthcare system and consistent procurement through the NHS. Strong emphasis on infection prevention, strict regulatory compliance, and high usage of standardized medical apparel across hospitals and clinics support demand. Additionally, the presence of experienced suppliers, focus on sustainable healthcare textiles, and continuous upgrades in healthcare infrastructure reinforce the country’s leading position.

How is the Market Growing in the South American Region?

Rapidly rising healthcare costs, increased awareness of infection prevention, and an increase in the prevalence of chronic illnesses that call for specialized, high-quality protective garments are the main factors driving South America's medical clothing market. The need for comfortable, fluid-resistant, and antimicrobial clothing has increased due to post-pandemic changes and an aging population. The demand for medical textiles is rising due to the region's increased investment in both public and commercial healthcare facilities. The introduction of sophisticated, high-performance surgical gowns and scrubs is driven by a significant focus on lowering healthcare-associated infections (HAIs). The necessity for protective clothing is being driven by strict sanitary regulations. Better protective clothes are required in long-term care facilities due to an aging population and an increase in patient admissions. The market is improved by the increased availability of antibacterial and technologically advanced fabrics.

Brazil Market Trends

Brazil plays a significant role in the market, particularly in advanced wound care and surgical products, driven by its expanding medical tourism industry, stringent care standards, and substantial textile sector backed by government initiatives. Contributing factors include competitive pricing compared to Asian markets, high-quality and sustainable production, and growing demand for reusable, specialized medical textiles. The country's global leadership in aesthetic and orthopedic surgeries further amplifies the demand for customized medical clothing and post-surgical garments, with organizations such as ApexBrasil and Abit providing substantial support to the textile industry. Brazilian manufacturers are placing greater emphasis on sustainable and reusable medical textiles, in line with global eco-conscious market trends, as noted by IndustryARC. Additionally, Brazil's comparatively lower production costs make it an appealing option for international companies seeking to source products, as observed by Chameleon Pharma Consulting and Global Health Intelligence.

The Middle East and Africa (MEA) region is emerging as an important player in the medical clothing market by 5% share, largely due to substantial investments in healthcare infrastructure, particularly in Saudi Arabia and the UAE. The region is experiencing swift growth in the disposable medical textiles segment, driven by stringent infection control measures and an increasing volume of surgical procedures. Initiatives like Saudi Arabia’s Vision 2030 are fostering the development of new hospitals and clinics, consequently increasing demand for healthcare apparel such as scrubs, gowns, and drapes. Additionally, countries like Turkey and the UAE are advancing as medical tourism hubs, contributing to a rise in the use of medical clothing to align with international hygiene and patient care standards. The increasing prevalence of diseases that require surgical intervention, such as diabetes and cardiovascular conditions, has resulted in a greater demand for surgical procedures, subsequently driving the need for surgical apparel. Additionally, post-pandemic measures in hospitals and clinics across the region have emphasized infection prevention, contributing to the widespread adoption of advanced surgical gowns and scrubs with antimicrobial and fluid-resistant properties.

UAE Market Trends

The UAE is a leading player in the medical clothing market due to the expansion of healthcare infrastructure, adherence to stringent infection control regulations, and significant investments in medical technologies. Factors such as population growth, rising surgical volumes, and heightened awareness of hygiene contribute to the increasing demand for protective apparel. The development of hospitals and healthcare centers further drives the need for medical uniforms and protective gear. A stronger emphasis on infection control and safety standards within medical facilities has led to the widespread adoption of high-quality scrubs, gowns, and protective equipment. Additionally, the UAE's efforts to establish itself as a global medical tourism hub have resulted in increased surgical volumes, which boost demand for surgical drapes, scrubs, and gowns. Substantial investments from both government and private entities in the healthcare sector, combined with collaborative efforts, promote local manufacturing and the use of innovative, environmentally sustainable medical apparel.

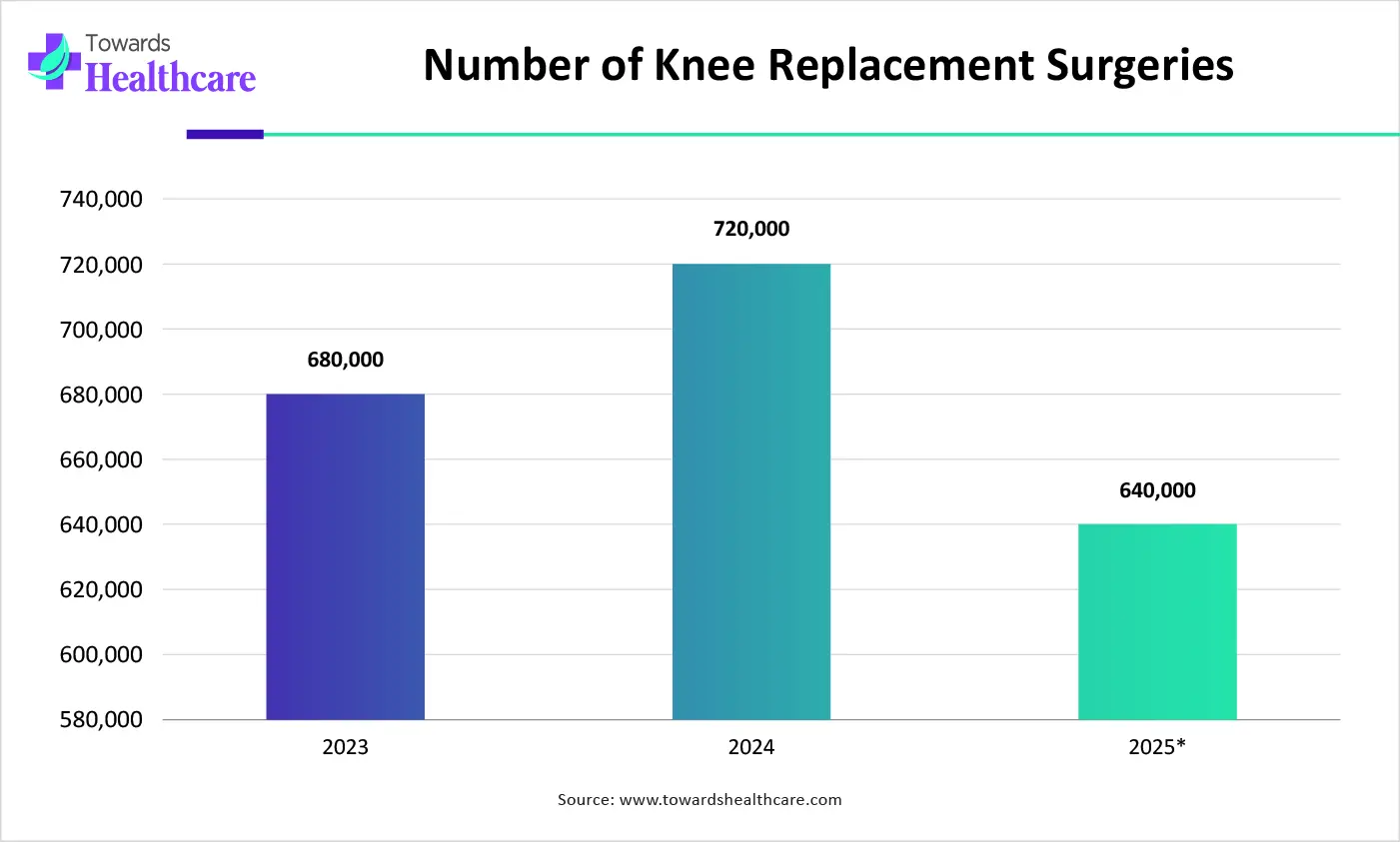

| Years | Number of Knee Replacement Surgeries |

| 2023 | 690,000 |

| 2024 | 718,000 |

| 2025* | 637,059 |

|

Category

|

Key Participants | Explanation |

| Technology Providers | DuPont, Kimberly-Clark, Berry Global, Freudenberg Performance Materials | Provide advanced fabrics, antimicrobial textiles, barrier protection technologies, and nonwoven materials. |

| Product Manufacturers | Medline Industries, Cardinal Health, Mölnlycke Health Care, Superior Group of Companies, Barco Uniforms | Manufacture medical apparel, scrubs, surgical gowns, lab coats, and patient garments. |

| Service Providers | Aramark Healthcare, Cintas Healthcare, ImageFIRST | Provide laundering, rental, inventory management, and apparel services for healthcare facilities. |

| Platform Providers | Medline, Cardinal Health, Owens & Minor | Distribution platforms supplying medical clothing and healthcare consumables. |

| CROs/CDMOs | Not a major segment participant | CRO/CDMO involvement is limited in medical clothing markets. |

| Software Vendors | Infor, SAP Healthcare, Oracle Health Supply Chain | Support inventory tracking, procurement, and apparel management systems. |

| Research Institutions | AAMI, ASTM International, NIOSH, CDC Research Programs | Develop standards and evaluate performance requirements for medical apparel. |

| End-User Industries | Hospitals, Clinics, Laboratories, Pharmaceutical Manufacturing, Biotechnology Facilities | Major consumers of medical clothing products. |

Research & Development:

Clinical Trials & Regulatory Approval:

Patient Support & Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Market Influence (%) | 68% | 22% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medline Industries | Northfield, Illinois | United States | One of the largest global suppliers of medical apparel and PPE | Scrubs, Isolation Gowns, Surgical Apparel, Patient Wear |

| Cardinal Health | Dublin, Ohio | United States | Major healthcare products supplier with extensive apparel offerings | Surgical Gowns, Protective Apparel, Scrubs |

| Mölnlycke Health Care | Gothenburg | Sweden | Global leader in surgical clothing and infection prevention products | Surgical Gowns, Procedure Packs, Protective Apparel |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Barco Uniforms | Gardena, California | United States | Leading healthcare uniform manufacturer | Scrubs, Lab Coats, Healthcare Uniforms |

| Superior Group of Companies | St. Petersburg, Florida | United States | Significant healthcare uniform supplier | Medical Uniforms, Scrubs, Healthcare Apparel |

| Angelica Corporation | Alpharetta, Georgia | United States | Healthcare apparel and linen solutions provider | Surgical Apparel Programs, Healthcare Garments |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| FIGS | Santa Monica, California | United States | Fast-growing premium medical apparel brand | Scrubs, Lab Coats, Medical Apparel |

| Jaanuu | San Diego, California | United States | Digital-first medical apparel innovator | Premium Scrubs, Antimicrobial Apparel |

Strengths

Weaknesses

Opportunities

Threats

In February 2026, commenting on the launch, Mr. Raghunath Mannil Balakrishnan, CEO, Mafatlal Industries Limited, said, “The launch of Mafatlal MedFits marks a crucial step in the expansion of our healthcare and technical textiles portfolio. It reflects our continued investment in manufacturing capability, quality systems, and process excellence. Through this digital platform, we are extending our strengths directly to healthcare professionals across India by offering medical scrubs and related essentials in internationally benchmarked styles and designs, engineered for comfort, functionality, and durability. This initiative reinforces our focus on operational efficiency, customer proximity, and sustainable growth in a high-potential segment.”

By Product

By Type

By Usage

By End-user

By Sales Channel

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar