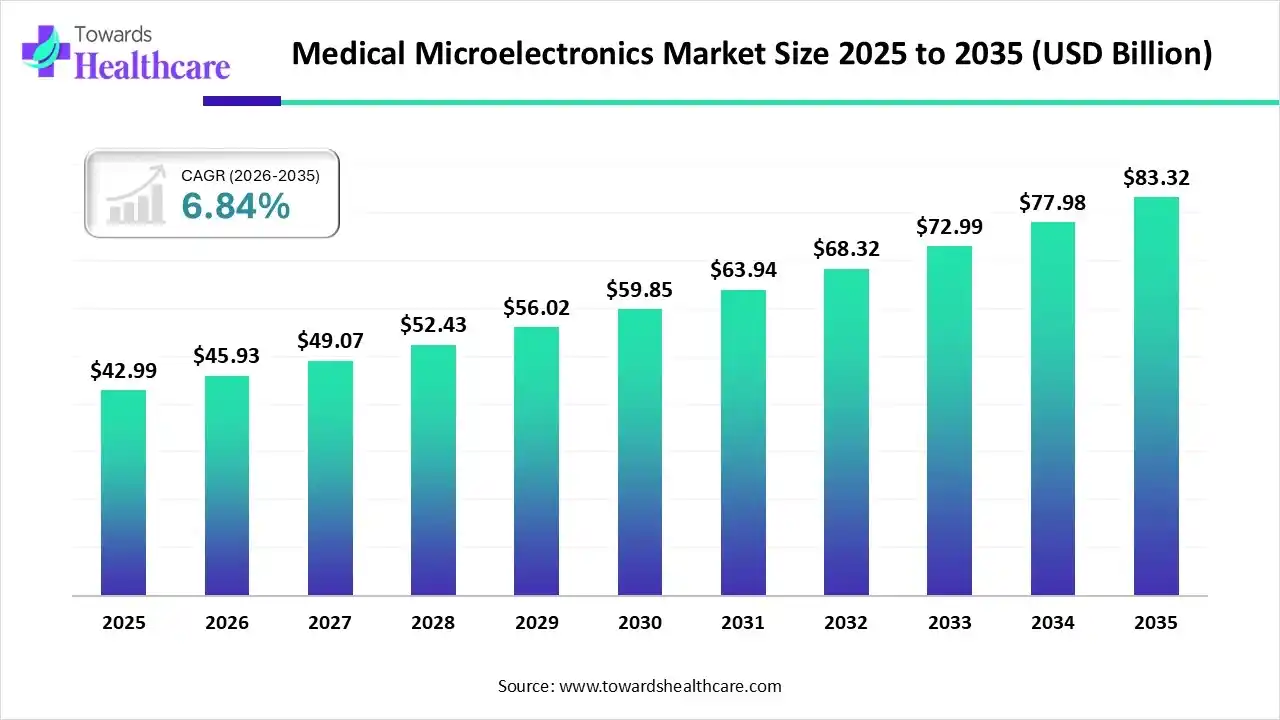

The global medical microelectronics market size was estimated at USD 42.99 billion in 2025 and is predicted to increase from USD 45.93 billion in 2026 to approximately USD 83.32 billion by 2035, expanding at a CAGR of 6.84% from 2026 to 2035.

")

The current era and coming years will face a huge rise in chronic disease cases, which demands advanced medical imaging and diagnostics solutions that leverage smart semiconductors. Besides this, several companies are executing AI algorithms in advanced sensors. Moreover, the market is stepping into bolstering biodegradable wireless sensors and flexible electronics to monitor health parameters.

Primarily, the medical microelectronics market encompasses miniaturized electronic components & circuits that are united into medical devices to track, diagnose, and treat diseases. The widespread adoption of these devices is fueled by the progress of wearable medical devices and portable diagnostic health monitoring. Moreover, the market is stepping towards innovations in biodegradable wireless sensors and flexible electronics to track gastrointestinal or tissue-level changes in real-time.

The medical microelectronics market is growing rapidly due to the increasing demand for compact, reliable, and energy-efficient electronic components used in modern healthcare devices. These technologies play a crucial role in medical imaging systems, implantable devices, wearable health monitors, diagnostic equipment, and patient monitoring solutions. The growing burden of chronic diseases and the rising adoption of remote patient monitoring are encouraging the development of miniaturized medical electronics with improved performance and longer battery life. Advances in semiconductor manufacturing, sensor technologies, and wireless connectivity are further enhancing device capabilities. Increasing healthcare digitalization and the integration of artificial intelligence into medical equipment are also creating new growth opportunities for the market.

Nowadays, AI has a prominent role in the development of immersive devices, while in the respective market, AI advances medical imaging devices, like CT, MRI, and ultrasound by enhancing image quality, lowering noise, and reducing radiation exposure time. Alongside this, the globe is leveraging AI-assisted robotics, such as the Hybrid Assistive Limb (HAL) exoskeleton, which uses surface sensors to interpret bioelectrical signals from the user and further provides tailored rehabilitation for stroke or spinal cord injury patients.

Spurring Modern Sensing & MEMS

The leading firms are promoting microelectromechanical systems (MEMS) & more sophisticated semiconductor materials, which allow increased precision, reliability, & robust performance in harsh biological conditions.

Shifting Towards Retinomorphic Devices

Researchers are exploring specialized optical sensors that act as biological retinas to process visual information at the point of detection, which is vital for prospective bio-electronic eyes & robotic surgery.

Fostering Electronic Skin (E-skin)

An important future breakthrough will include emerging soft, flexible, and self-healing systems, which mimic the sensory functions of human skin for prosthetics, wound healing, & health monitoring.

| Table | Scope |

| Market Size in 2026 | USD 45.93 Billion |

| Projected Market Size in 2035 | USD 83.32 Billion |

| CAGR (2026 - 2035) | 6.84% |

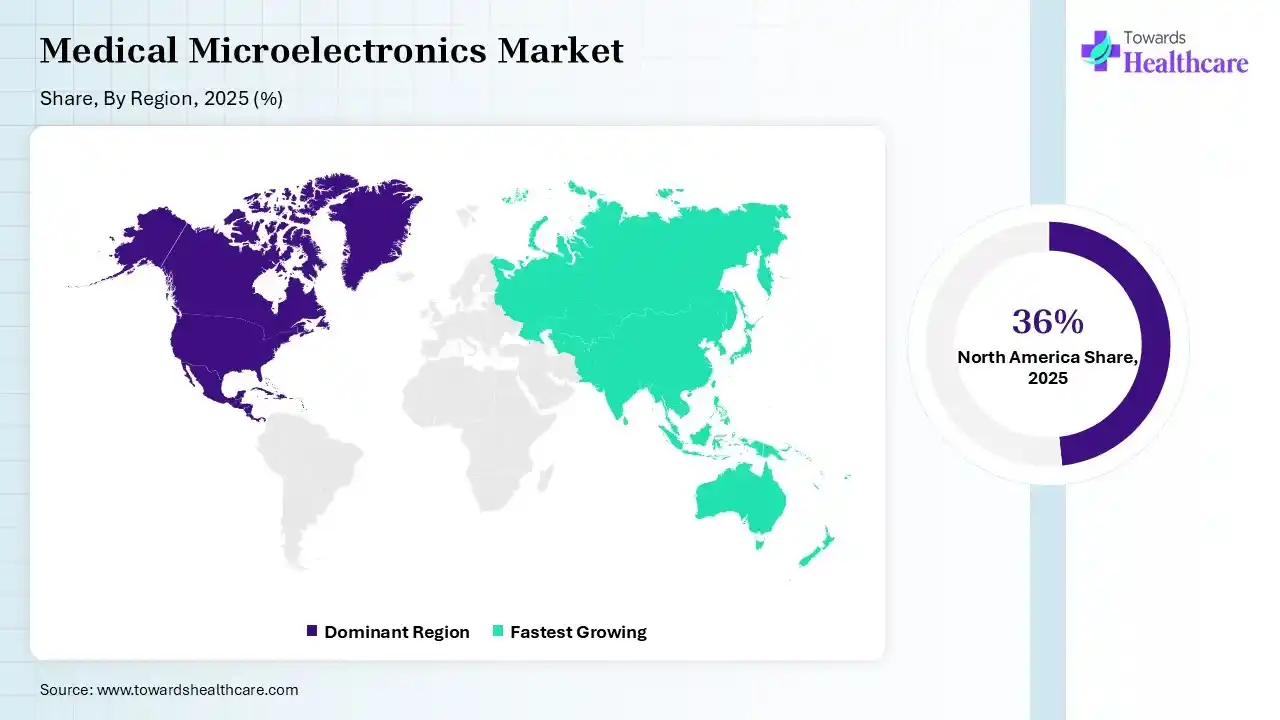

| Leading Region | North America by 36% |

| Key Applications | Implantable Cardiac Devices, Neurostimulation, Hearing Aids, Wearable Health Devices, Diagnostic Imaging Systems, Patient Monitoring, Smart Drug Delivery Systems, Biosensors, Surgical Devices |

| Primary End Users | Hospitals, Clinics, Ambulatory Care Centers, Medical Device OEMs, Diagnostic Laboratories, Research Institutes, Home Healthcare Providers |

| Key Growth Drivers | Miniaturization of medical devices, rising chronic diseases, growth in implantable devices, digital health adoption, wearable technologies, advances in MEMS and semiconductor technologies |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Component, By Application, By Device Classification, By Region |

| Top Key Players | Medtronic, Johnson & Johnson MedTech, Abbott Laboratories, Siemens Healthineers, GE HealthCare, Boston Scientific, Philips Healthcare, Stryker Corporation, Becton, Dickinson and Company (BD), Intuitive Surgical |

| Segments | Shares % |

| Integrated Circuits (ICs) | 46.8% |

| Sensors | 24.2% |

| Optoelectronics | 17% |

| Discrete Components | 12% |

Which Component Led the Medical Microelectronics Market in 2025?

In 2025, the integrated circuits (ICs) segment was dominant with approximately 46.8% share of the market. The globe is widely demanding wearable monitors & portable diagnostic tools, which are dependent on robust ICs for data collection. The emergence of radar-based sensors and remote photoplethysmography (rPPG) ICs is assisting in tracking signs without physical contact. Also, these solutions can combine into smart environments for fall detection and sleep analysis.

Sensors

The sensors segment is expected to expand at the highest CAGR during the forecast period. The broader adoption is driven by the use of miniaturization of sensors and integration with Internet of Things (IoT) technologies, which enable advanced, remote patient monitoring. Extensive breakthroughs are exploring sweat-based biochemical sensors, which monitor sweat for cortisol levels, facilitating non-invasive, real-time stress data. Whereas, ultrasound-based wearable monitors are substituting conventional cuffs for persistent, comfortable blood pressure tracking.

| Segments | Shares % |

| Medical Imaging | 31.9% |

| Patient Monitoring | 28.1% |

| Medical Implants | 22% |

| Wearables & Handhelds | 18% |

How did the Medical Imaging Segment Dominate the Market in 2025?

The medical imaging segment held nearly a 31.9% share of the medical microelectronics market in 2025. Along with a rise in cases of cancer, cardiovascular diseases, and neurological disorders, the segment is fueled by the growing demand for minimally invasive diagnostics & treatments. The era is moving towards innovative imaging microchips that process algorithms directly on the device, which lowers latency and boosts privacy.

Wearables & Handhelds

Moreover, the wearables & handhelds segment is predicted to expand fastest. The rising advances in decentralized care and telehealth are propelling demand for wearables that transmit real-time data, which supports early intervention. The upcoming developments are leveraging MXenes, graphene, and conductive hydrogels enables sensors to conform to the skin, & which raises signal fidelity and minimizes skin irritation.

| Segments | Shares % |

| Class II | 50% |

| Class I | 30% |

| Class III | 20% |

Why did the Class II Segment Lead the Market in 2025?

In 2025, the class II segment dominated with an approximate 50% share of the medical microelectronics market. This mainly covers devices that pose moderate-to-high risk, like powered wheelchairs, infusion pumps, surgical drapes, and catheters. Ongoing advancements are executing embedded artificial intelligence, shifts from passive data collection to active diagnostic assistance, including the detection of cardiac abnormalities in real-time.

Class III

In the future, the class III segment is estimated to show rapid growth. The segmental progress is impelled by the incorporation of the highest-risk, life-preserving, or permanently implantable electronic devices, like pacemakers, defibrillators, & cochlear implants. Many research activities are going towards implantable cardiac monitors that are more sensitive, with novel percutaneous right heart pumps to conduct without external drivelines, booming patient mobility & safety.

")

In 2025, North America held a nearly 36% revenue share of the medical microelectronics market. A prominent driver is ongoing substantial investment from both public & private sectors in R&D, with robust government funding for semiconductor research, which accelerates future novelty. Whereas, Health Canada has developed novel, definite guidelines for the pre-market evaluation of machine-learning-enabled medical devices, which focus on safety, transparency, & lifecycle monitoring.

U.S. Market Trends

Meanwhile, the U.S. was a huge contributor to the market, which has executed diverse packaging approaches, including System-in-Package technology (SiP), which lowers board areas by up to 60% & allows more advanced, smaller implantable devices.

For instance,

Canada Market Trends

Canada is seeing steady growth in the medical microelectronics market as healthcare providers continue adopting advanced medical technologies to improve patient care. The demand for compact and high-performance electronic components is increasing in medical imaging, diagnostic equipment, implantable devices, and remote monitoring systems. Strong investments in healthcare research, growing collaboration between technology companies and medical institutions, and rising focus on digital health solutions are supporting innovation. An aging population and increasing need for continuous patient monitoring are also driving market expansion across Canada.

During the prospective period, the Asia Pacific is anticipated to expand at the highest CAGR of approximately 11.5% in the medical microelectronics market, due to a rise in semiconductor manufacturing capacity in the region, especially China and Taiwan, with favourable government policies for domestic production & digital healthcare innovations. In certain cases, APAC is bolstering innovations in integrated AI, Internet of Medical Things (IoMT), & 5G into medical devices, which transforms patient monitoring & diagnostics.

China Market Trends

Moreover, China is emphasizing 70% self-sufficiency in core medical materials & high-end components by 2025, which highly supports local players in government procurement. China’s 2025 Innovation Task Notice is focused on AI-powered devices for smart diagnostics and remote monitoring, which comprises flexible sensors, nanoparticle-based cancer treatment, & advanced imaging

India Market Trends

India is witnessing rapid growth in the medical microelectronics market due to expanding healthcare infrastructure and increasing demand for affordable medical devices. Hospitals and diagnostic centers are adopting advanced electronic technologies to improve patient care and disease monitoring. Rising investments in domestic medical device manufacturing, supportive government initiatives, and growing healthcare awareness are encouraging innovation. The increasing use of wearable health devices, portable diagnostic equipment, and remote patient monitoring systems is also creating strong demand for medical microelectronics across the country's healthcare sector.

Europe is predicted to witness lucrative expansion in the medical microelectronics market. This will be mainly influenced by the promotion of a highly miniaturized, redox-measuring ingestible sensor, which is three times smaller than existing capsule endoscopies. Eventual regulatory changes by the European Commission on streamlining the Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR) are accelerating access to groundbreaking, digitally powered devices.

UK Market Trends

The UK market is fostering 4D medical device production, and the Annual IMAPS-UK Conference also emphasized "New Frontiers in Chip Packaging," primarily highlighting biocompatible encapsulation & fluxless bonding for medical chiplets.

Germany Market Trends

Germany is experiencing strong growth in the medical microelectronics market because of its advanced healthcare infrastructure and well-established medical device industry. Hospitals and manufacturers are increasingly using miniaturized electronic components in diagnostic equipment, implantable devices, and patient monitoring systems. Rising demand for precision healthcare and digital medical technologies is driving innovation. Strong investments in research, government support for healthcare innovation, and close collaboration between medical device companies and research institutions are helping develop advanced microelectronics solutions for a wide range of medical applications.

| Ecosystem Segment | Description | Key Participants |

| Technology Providers | Develop semiconductor technologies, MEMS, sensors, ICs, analog and mixed-signal electronics | Texas Instruments, Analog Devices, STMicroelectronics, NXP Semiconductors |

| Product Manufacturers | Develop finished medical devices utilizing microelectronics | Medtronic, Abbott, Boston Scientific, GE HealthCare |

| Service Providers | Design, engineering, testing and manufacturing services | Jabil Healthcare, Flex Health Solutions, Plexus Corp |

| Platform Providers | Connected healthcare and medical device platforms | Philips, Siemens Healthineers, GE HealthCare |

| CROs/CDMOs | Medical electronics development and manufacturing support | Integer Holdings, Cirtec Medical, TE Connectivity Medical |

| Software Vendors | Embedded software, device connectivity, analytics | Philips Healthcare IT, GE HealthCare, Siemens Healthineers |

| Research Institutions | Advanced bioelectronics and medical semiconductor research | MIT, Stanford University, Johns Hopkins University, Fraunhofer Institutes |

| End-User Industries | Healthcare delivery, diagnostics, medical device manufacturing, home healthcare | Hospitals, Clinics, Medical Device OEMs |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 65% | 25% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medtronic plc | Dublin | Ireland | World's largest medical device manufacturer with extensive implantable electronics portfolio | Pacemakers, Neurostimulators, Insulin Pumps, Implantable Monitoring Systems |

| Abbott Laboratories | Abbott Park, Illinois | USA | Major supplier of implantable and connected medical electronics | Cardiac Rhythm Management Devices, Continuous Glucose Monitors |

| Boston Scientific Corporation | Marlborough, Massachusetts | USA | Leading implantable microelectronic therapeutic devices provider | Neurostimulation Systems, Cardiac Devices, Electrophysiology Products |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Philips Healthcare | Amsterdam | Netherlands | Strong patient monitoring and connected care electronics portfolio | Monitoring Systems, Diagnostic Equipment, Wearables |

| Analog Devices Inc. | Wilmington, Massachusetts | USA | Major supplier of medical-grade analog and mixed-signal semiconductors | Biosensor ICs, Medical Signal Processing Chips |

| Texas Instruments Incorporated | Dallas, Texas | USA | Key supplier of medical electronics components and power management solutions | Medical ICs, Embedded Processors, Sensor Interfaces |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Cirtec Medical Corporation | Brooklyn Park, Minnesota | USA | Specialized implantable medical electronics development company | Implantable Device Electronics, Neurostimulation Components |

| Integer Holdings Corporation | Plano, Texas | USA | Leading outsourced manufacturer of implantable medical electronics | Implantable Device Components, Battery Systems |

| TE Connectivity Medical | Berwyn, Pennsylvania | USA | Specialized medical interconnect and microelectronic solutions provider | Medical Connectors, Implantable Device Components |

Strengths

Weaknesses

Opportunities

Threats

In June 2026, commenting on the development, Mr. Siva Ram A, on behalf of MICK Digital India Limited, said: “We are honoured to be empanelled as an authorised Channel Partner of AMTZ India’s premier medical devices manufacturing hub and a testament to what domestic ingenuity can achieve. This partnership marks a defining step in MICK Digital’s journey into the healthcare sector. Our vision is to ensure that the best of Indian-made medical technology reaches not just large hospitals in metros, but also district hospitals, community health centres, and healthcare institutions in Tier 2 and Tier 3 cities across the country. Together with AMTZ, we are committed to contributing meaningfully to a self-reliant, accessible, and world-class Indian healthcare ecosystem.”

By Component

By Application

By Device Classification

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar