Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

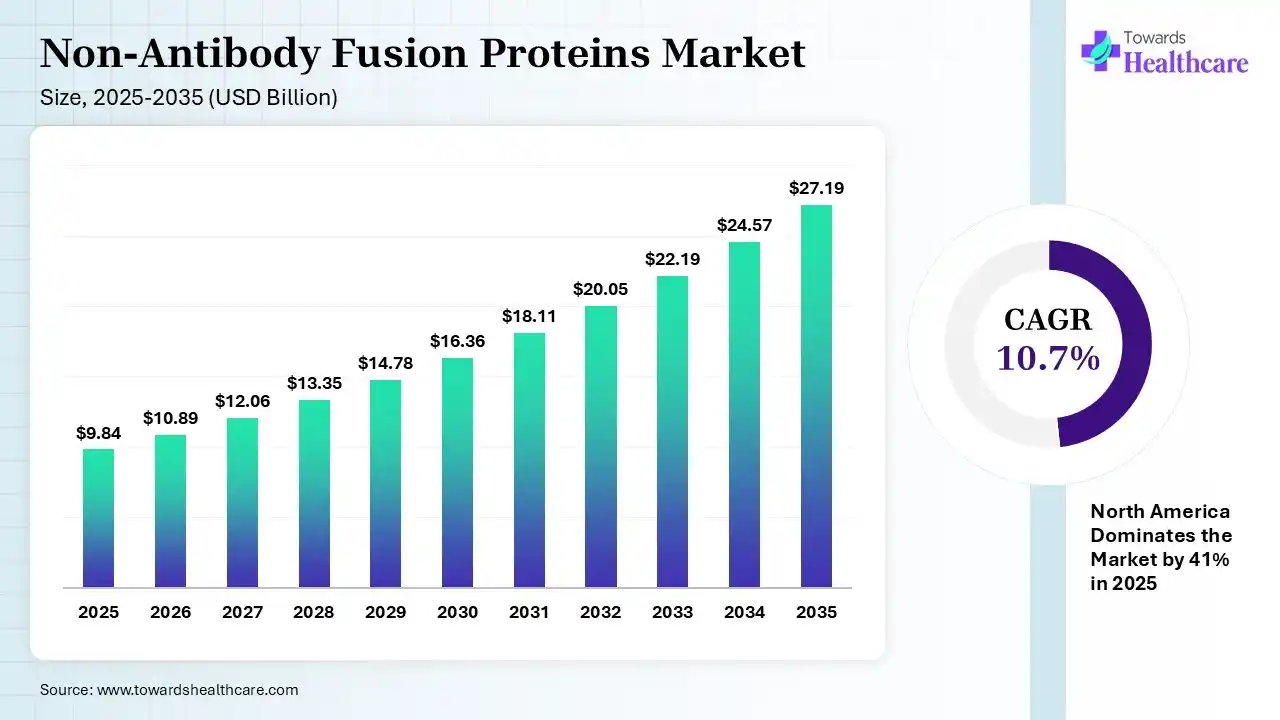

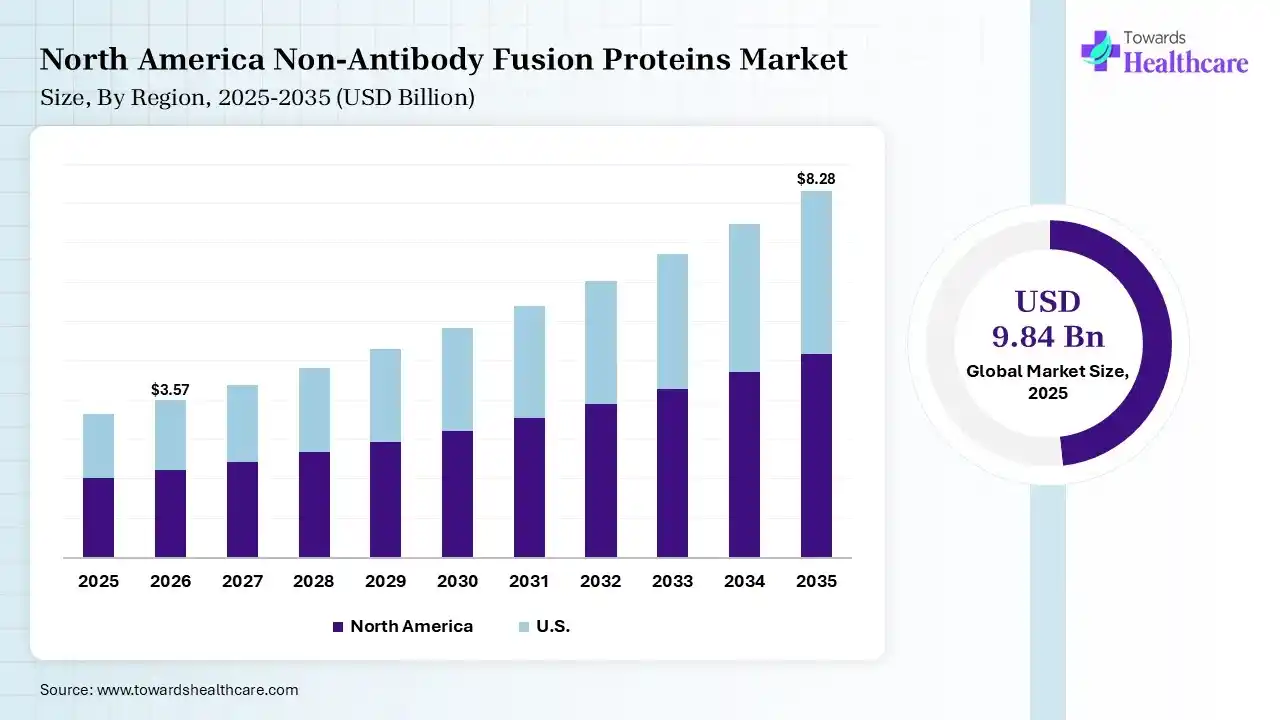

The global non-antibody fusion proteins market size was estimated at USD 9.84 billion in 2025 and is predicted to increase from USD 10.89 billion in 2026 to approximately USD 27.19 billion by 2035, expanding at a CAGR of 10.7% from 2026 to 2035. The market is expanding due to increasing demand for advanced biologics with improved stability, targeted action, and longer therapeutic efficacy in chronic and rare diseases. Growth is further driven by strong R&D activity and advances in protein engineering, supporting wider applications in oncology and autoimmune disorder treatment.

")

Non-antibody fusion proteins are engineered therapeutic proteins created by combining two or more functional protein domains to enhance stability, targeting, or biological activity. They are used in treatment and research to improve drug efficacy, half-life, and specific interaction with disease-related targets. The non-antibody fusion proteins market is witnessing robust growth due to rising demand for highly targeted, long-acting biologics that improve treatment outcomes and patient compliance. Breakthroughs in protein engineering and recombinant DNA technology are accelerating innovation, while strong R&D investments are expanding clinical pipelines. Increasing adoption of oncology, autoimmune, and rare disease therapies is further fueling global market expansion.

Non-antibody fusion proteins are engineered biologic molecules created by combining two or more protein domains to enhance therapeutic activity, targeting, ability, and pharmacokinetic performance without using an antibody-based structure. The non-antibody fusion proteins market is expanding due to the increasing demand for targeted biologics, rising prevalence of cancer, autoimmune disorders, and rare diseases, and growing investments in biopharmaceutical research. Technological advancements in recombinant DNA technology, protein engineering, AI-assisted protein design, and advanced bioprocessing are enabling the development of highly effective fusion protein therapies. A key market trend is the growing focus on long-acting and multifunctional fusion proteins that improve treatment efficacy and patient adherence. Future opportunities lie in precision medicine, next-generation fusion protein platforms, novel therapeutic targets, and scalable manufacturing technologies, supported by expanding clinical pipelines and continuous innovation in biologics development.

AI is transforming the market by accelerating protein design, optimizing molecular structures, and predicting therapeutic efficacy with greater accuracy. It reduces R&D time and costs while improving success rates in drug development. AI-driven insights also enable better target identification and personalized therapies, supporting faster clinical advancements and expanding applications across oncology, autoimmune, and rare disease treatments.

| Table | Scope |

| Market Size in 2026 | USD 10.89 Billion |

| Projected Market Size in 2035 | USD 27.19 Billion |

| CAGR (2026 - 2035) | 10.7% |

| Leading Region | North America by 41% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Therapeutic Application, By Expression System, By Route of Administration, By End User, By Region |

| Top Key Players | Amgen (Immunex legacy), Regeneron Pharmaceuticals + Bayer AG, Bristol Myers Squibb, Pfizer Inc., Eli Lilly and Company |

")

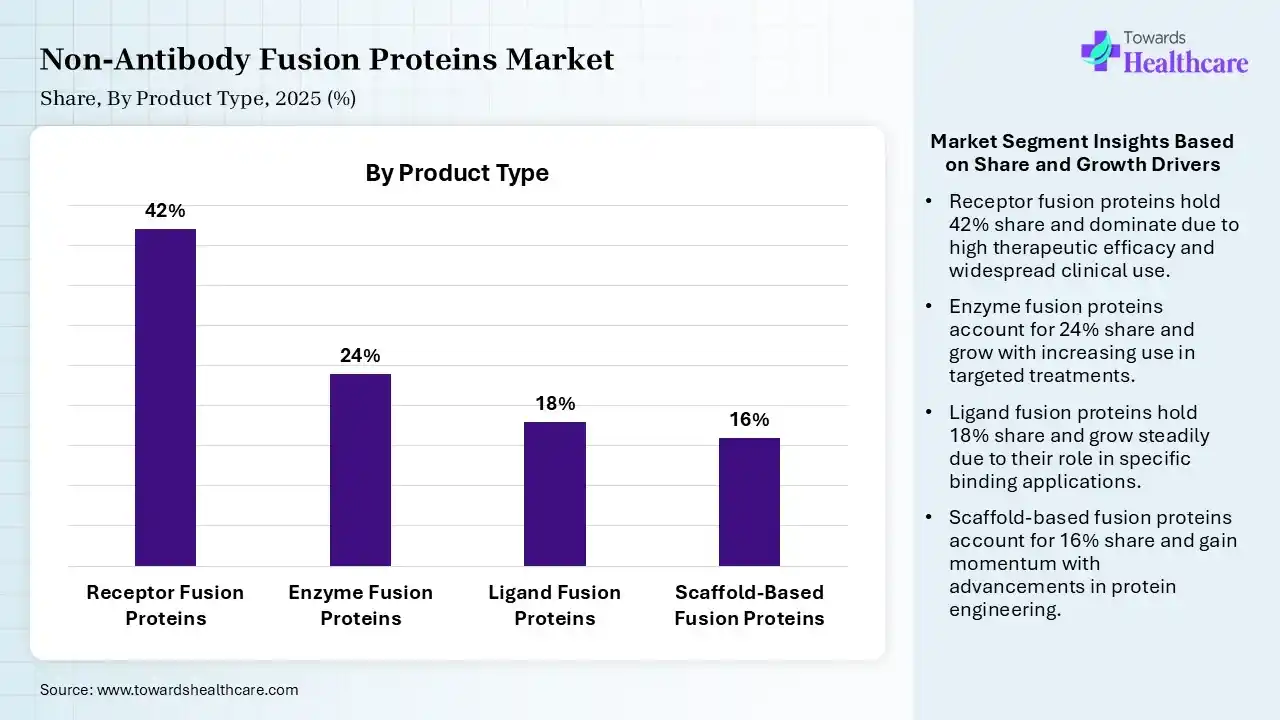

| Segment | Share 2025 (%) |

| Receptor Fusion Proteins | 42% |

| Enzyme Fusion Proteins | 24% |

| Ligand Fusion Proteins | 18% |

| Scaffold-Based Fusion Proteins | 16% |

The Receptor Fusion Proteins Segment Dominated the Market in 2025

The receptor fusion proteins segment dominated the non-antibody fusion proteins market with a revenue share of 42% in 2025 due to its strong ability to mimic natural receptor functions and effectively block disease pathways. These proteins offer high specificity, improved stability, and extended half-life, enhancing therapeutic outcomes. Their widespread use in treating autoimmune disease and inflammatory conditions, along with protein clinical success and regulatory approvals, has significantly driven their market leadership.

The enzyme fusion proteins segment held the second-largest share of 24% of the market in 2025 due to its effectiveness in enhancing enzyme stability, activity, and targeted delivery. These proteins are widely used in metabolic and rare disease treatments, including enzymes used in metabolic therapies. Growing demand for precision therapeutics, along with advancements in bioengineering and increasing clinical adoption, has supported a strong market presence and continued growth of this segment.

The ligand fusion proteins segment held 18% share in 2025 and is expected to grow at the fastest CAGR of 12.1% in the market during the forecast period due to its ability to precisely target specific receptors and modulate disease pathways with high efficiency. These proteins offer improved therapeutic specificity and reduced side effects. Increasing research focus, expanding applications in oncology and immunotherapy, and advancements in protein design technologies are accelerating their development and driving rapid market growth.

The scaffold-based fusion proteins segment held 16% of the non-antibody fusion proteins market share in 2025 due to their small size, high stability, and strong binding specificity, enabling efficient tissue penetration and targeted delivery. They offer advantages over traditional biologics, including lower immunogenicity and easier manufacturing. Increasing research interest, expanding applications in oncology and diagnostics, and advancements in protein engineering technologies are driving their adoption and supporting steady market growth.

")

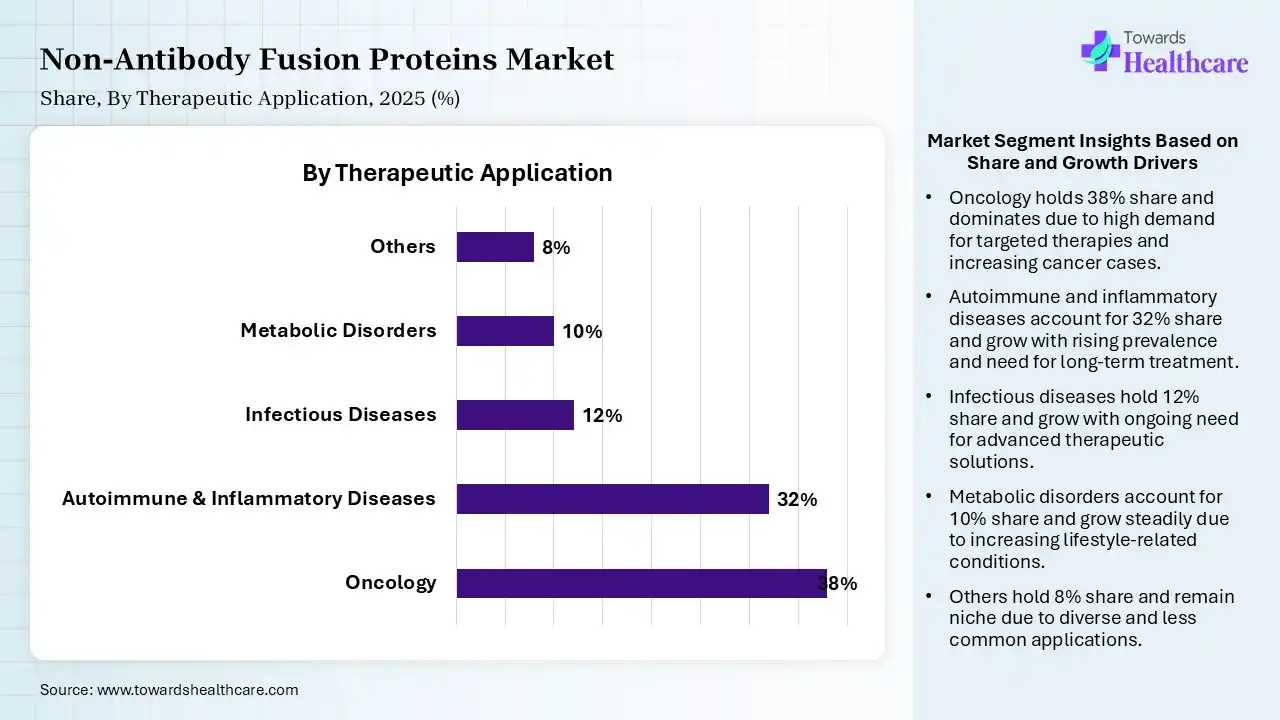

| Segment | Share 2025 (%) |

| Oncology | 38% |

| Autoimmune & Inflammatory Diseases | 32% |

| Infectious Diseases | 12% |

| Metabolic Disorders | 10% |

| Others | 8% |

The Oncology Segment Led the Market in 2025 with the Largest Share

The oncology segment led the non-antibody fusion proteins market with a share of 38% in 2025 and is expected to grow at the fastest CAGR of 11.8% in the market during the forecast period due to the rising global cancer burden and strong demand for targeted, effective therapies. These proteins enable precise tumor targeting, improved efficacy, and reduced systemic toxicity. Increasing clinical trials, approvals of innovative biologics, and growing adoption of advanced treatments such as immunotherapies have significantly driven their use in cancer management, supporting segment dominance.

The autoimmune & inflammatory diseases segment held the second-largest share of 32% of the market in 2025 due to the high global prevalence of conditions such as rheumatoid arthritis and psoriasis, driving demand for effective long-term therapies. Non-antibody fusion proteins offer targeted immune modulation, improved safety, and prolonged action. Increasing biologic adoption, stronger clinical outcomes, and continuous development of advanced therapies have supported significant growth in this segment.

The infectious diseases segment held 12% of the non-antibody fusion proteins market share in 2025 due to rising global incidence of viral and bacterial infections and the need for targeted, effective therapies. Non-antibody fusion proteins offer enhanced pathogen targeting. Improved immune response and longer half-life. Increasing research in antiviral and antimicrobial biologics, along with growing investments in novel treatment approaches and pandemic preparedness, is driving adoption and supporting steady market growth.

The metabolic disorders segment held 10% of the non-antibody fusion proteins market share in 2025 due to the increasing prevalence of conditions such as diabetes and rare metabolic diseases, driving demand for effective long-term treatments. Non-antibody fusion proteins enhance enzyme activity, stability, and targeted delivery in enzyme replacement therapies. Advancements in biotechnology, growing awareness, and expanding clinical research are further supporting the development and adoption of these therapies, fueling segment growth.

")

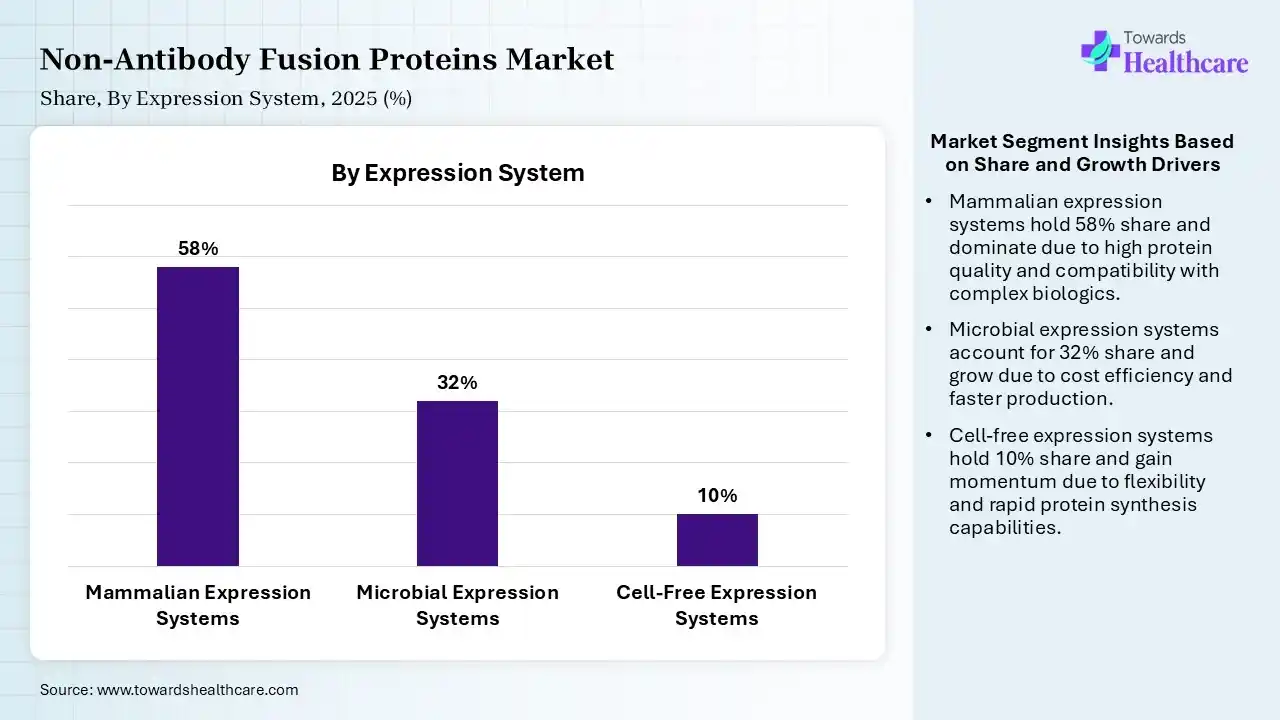

| Segment | Share 2025 (%) |

| Mammalian Expression Systems | 58% |

| Microbial Expression Systems | 32% |

| Cell-Free Expression Systems | 10% |

The Mammalian Expression Systems Segment Led the Market in 2025 with the Largest Share

The mammalian expression systems segment held a dominant share of 58% in 2025 due to its ability to produce complex fusion proteins with proper folding, post-translational modifications, and high biological activity. These systems ensure superior product quality, safety, and efficacy, making them ideal for therapeutic applications. Strong regulatory acceptance, widespread industry adoption, and increasing demand for high-quality biologics have further contributed to the non-antibody fusion proteins market dominance.

The microbial expression systems segment held the second-largest share of 32% of the market in 2025 and is expected to grow at the fastest CAGR of 11.2% in the market during the forecast period due to its cost-effectiveness, rapid production, and scalability for large-scale protein manufacturing. Systems such as bacteria and yeast enable efficient production of simpler fusion proteins with shorter development timelines. Increasing demand for affordable biologics, advancements in microbial engineering, and widespread use in early-stage research and commercial production have supported its strong market position.

The cell-free expression systems segment held 10% of the non-antibody fusion proteins market share in 2025 due to its rapid protein synthesis, flexibility, and ability to produce complex or toxic proteins without living cells. It enables faster screening and prototyping. and small-scale production, reducing development timelines. Increasing demand for high-throughput research, advancements in synthetic biology, and expanding applications in personalized medicine and on-demand biologics manufacturing are driving adoption and supporting strong market growth.

")

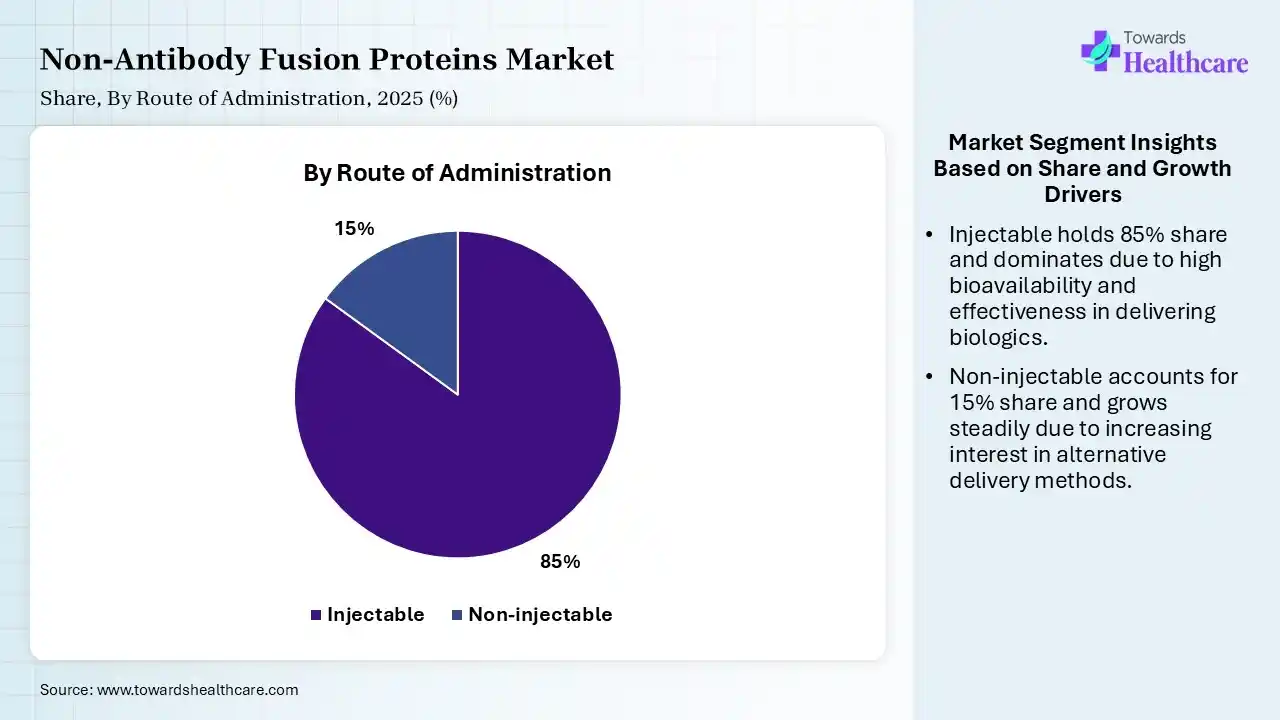

| Segment | Share 2025 (%) |

| Injectable | 85% |

| Non-injectable | 15% |

The Injectable Segment held a Dominant Position in the Market in 2025

The injectable segment led the non-antibody fusion proteins market with a share of 85% in 2025 due to the high bioavailability and rapid therapeutic action required for non-antibody fusion proteins. These biologics are often unstable in the gastrointestinal tract, making injections the most effective delivery method. Increasing use in chronic and complex diseases, rising demand for self-administration devices, and advancements in formulation technologies are further driving adoption and supporting segment growth.

The non-injectable segment held the second-largest share of 15% in 2025 and is expected to grow at the fastest CAGR of 12.6% in the market during the forecast period due to growing demand for more convenient and patient -friendly delivery options such as oral, nasal, and transdermal formulations. These routes improve patient compliance, especially for long-term treatments. Advancements in drug delivery technologies and formulation strategies are enabling better absorption and stability, supporting wider adoption alongside injectables in certain therapeutic applications.

")

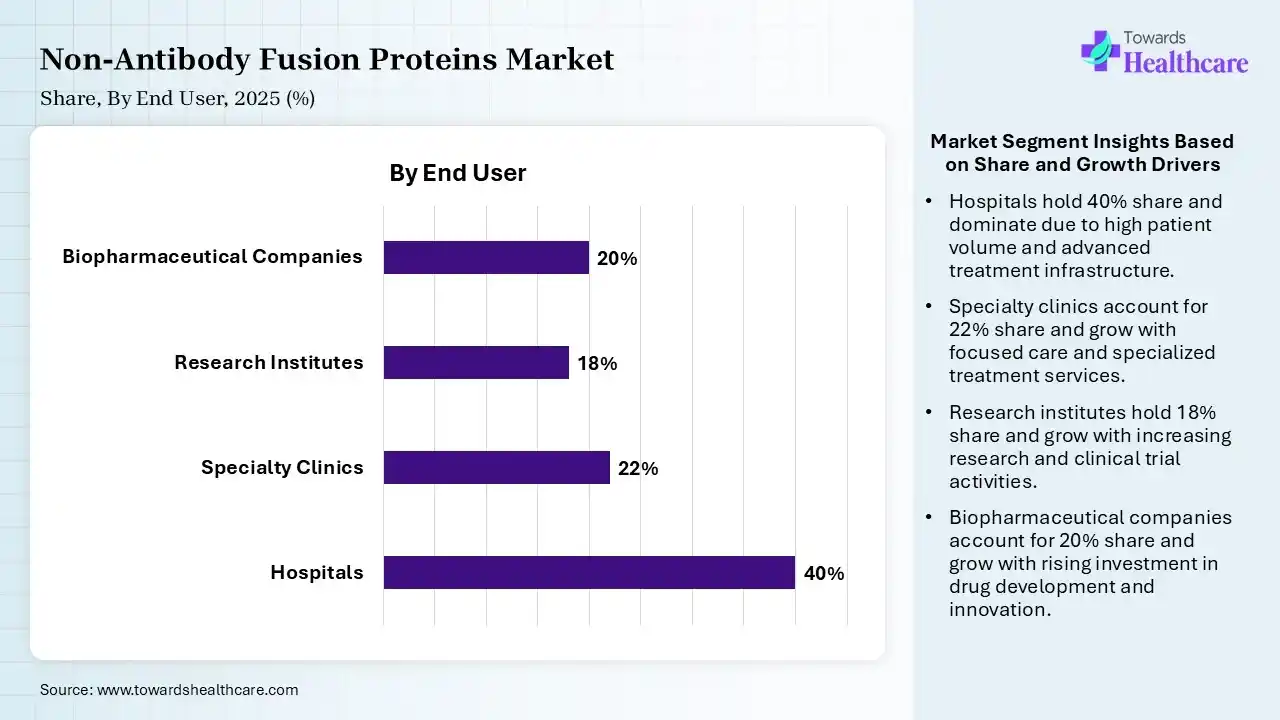

| Segment | Share 2025 (%) |

| Hospitals | 40% |

| Specialty Clinics | 22% |

| Research Institutes | 18% |

| Biopharmaceutical Companies | 20% |

The Hospitals Segment Dominated the Market in 2025

The hospitals segment held a dominant non-antibody fusion proteins market share of 40% in 2025 due to the availability of advanced healthcare infrastructure, skilled professionals, and specialized facilities required for administering complex biologic therapies. Hospitals manage a high volume of patients with chronic and severe conditions, ensuring consistent demand. Additionally, better reimbursement policies, access to innovative treatments, and strong clinical support systems have further strengthened their leading position in the market.

The specialty clinics segment held the second-largest share of 22% in 2025 due to focused expertise in treating specific conditions such as oncology, autoimmune, and metabolic disorders. These clinics offer personalized care, faster treatment access, and efficient patient management. Increasing preference for outpatient services, growing number of specialized centers, and rising adoption of advanced biologic therapies have supported their strong and expanding role in the market.

The research institutes segment held 18% share in 2025 and is expected to grow at the fastest CAGR of 11.7% in the non-antibody fusion proteins market during the forecast period due to increasing investments in biologics research, rising focus on novel protein therapeutics, and expanding academic industry collaborations. These institutes play a key role in early-stage discovery, protein engineering, and preclinical studies. Growing funding support, advancements in biotechnology tools, and increasing demand for innovative therapies are accelerating research activities and driving rapid segment growth.

")

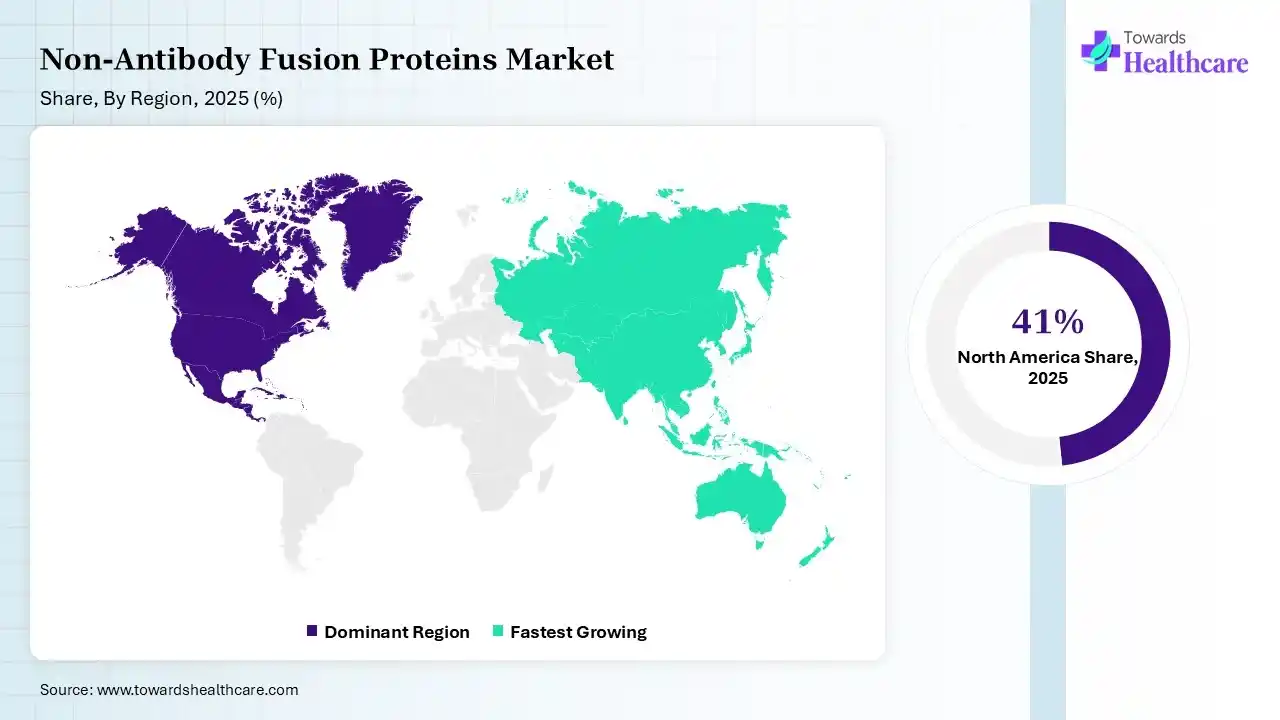

North America dominated the market with 41% of market share in 2025 due to the strong presence of leading biotech and pharmaceutical companies, advanced healthcare infrastructure, and high R&D investments. The region benefits from early adoption of innovative biologics, robust clinical trial activity, and a favorable regulatory framework. Additionally, the rising prevalence of chronic diseases and strong funding support for proteins-based therapeutic have further strengthened its market leadership.

U.S. Market Trends

The U.S. leads the market due to a strong biopharmaceutical ecosystem, high R&D spending, and the presence of major industry players. Advanced research infrastructure, rapid industry players. Advanced research infrastructure, rapid adoption of innovative biologics, and a robust clinical trials landscape support growth. Favorable regulatory support, increasing prevalence of chronic diseases, and continuous innovation in protein engineering further reinforced the country’s market dominance.

Canada Accelerates Innovation in Non-Antibody Fusion Proteins

Canada’s non-antibody fusion market is witnessing significant growth due to strong biopharmaceutical research capabilities, increasing investments in biologics development, and rising demand for targeted therapies for cancer and autoimmune diseases. Robust collaborations between academic institutions and biotechnology companies, expanding clinical research activities, and supportive government funding for life science are accelerating innovation, strengthening Canada’s position as a key hub for advanced fusion protein therapeutics.

Asia Pacific captured 21% of the total non-antibody fusion proteins market share in 2025 and is anticipated to grow at the fastest CAGR of 12.4% in the market during the forecast period due to expanding healthcare infrastructure, rising biopharmaceutical investment, and increasing demand for advanced biologics. Growing patient populations, improving access to innovative therapies, and supportive government initiatives are driving adoption. Additionally, the presence of emerging biotech companies, cost-effective manufacturing capabilities, and increasing clinical research activities are accelerating regional market growth.

India Market Trends

India is anticipated to grow at a significant CAGR due to rising healthcare investment, expanding biopharmaceutical sector, and increasing demand for advanced biologics. A large patient population, improving healthcare access, and supportive government initiatives are driving adoption. Additionally, growing clinical research activities, cost-effective manufacturing capabilities, and the presence of emerging biotech companies are accelerating market expansion across the country.

China Emerges as a Fast-Growing Biologics Innovation Hub

China’s non-antibody fusion protein market is growing significantly due to expanding biopharmaceutical manufacturing, increasing investments in biologics research, and rising demand for targeted therapies for cancer and autoimmune diseases. Strong government support for biotechnology, rapid growth of domestic biopharma companies, and expanding clinical trials activities are accelerating innovation. Additionally, advancements in protein engineering and large-scale biomanufacturing are strengthening China’s global competitiveness in fusion protein development.

R&D

Clinical Trials

Patient Support and Services

| Companies | Headquarters | Offerings |

| Amgen (Immunex legacy) | California, USA | Fc-fusion proteins, such as etanercept (Enbrel), focus on autoimmune and inflammatory diseases. |

| Regeneron Pharmaceuticals + Bayer AG | New York, USA | Fusion protein-based biologics like aflibercept (VEGF-trap) for ophthalmology and oncology applications. |

| Bristol Myers Squibb | New York City, USA | Fusion protein therapeutics such as abatacept (CTLA-4 Ig) for autoimmune diseases. |

| Pfizer Inc. | New York City, USA | Development of protein-based biologics and fusion protein candidates targeting inflammation and rare diseases. |

| Eli Lilly and Company | Indiana, USA | Biologic therapies, including engineered protein constructs and fusion-based therapeutics for metabolic and autoimmune disorders. |

In October 2025, “Patients with advanced solid tumors may have limited options with existing treatments, facing challenging disease control rates and low long-term survival,” “The MDX2004 multispecific antibody aims to rejuvenate T cells and sustain an expanded immune response in a broad range of tumors. We look forward to exploring further via this clinical trial”, said Giovanni Abbadessa, M.D., Ph.D., Chief Medical Officer of ModeX.

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Therapeutic Application

By Expression System

By Route of Administration

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar