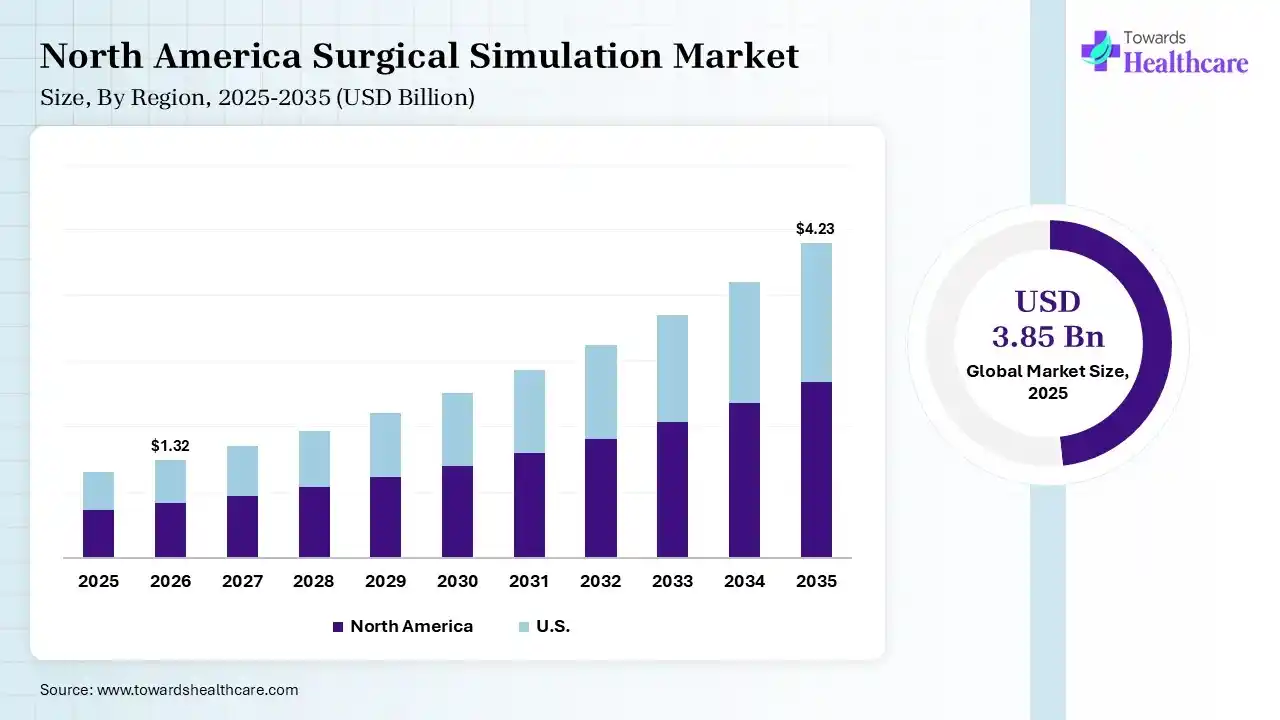

The global surgical simulation market size was estimated at USD 3.85 billion in 2025 and is predicted to increase from USD 4.42 billion in 2026 to approximately USD 15.31 billion by 2035, expanding at a CAGR of 14.8% from 2026 to 2035. The worldwide rising demand for minimally invasive procedures, an emphasis on reducing errors, & impelling advances in robotic surgeries propel the global market development. Many leading institutions and hospitals are promoting AR, VR, XR, and other AI-driven solutions in the different surgical domains.

")

Training technique, which replaces or raises real patient experiences with guided, immersive, & interactive scenarios, is considered the surgical simulation market. This further enables medical professionals to practice procedures, boost skills, & enhance patient safety in a risk-free circumstance. The global expansion is driven by rising focus on improving patient safety, with lowered errors, along with the progression of minimally invasive & robotic surgery.

To push the market expansion, AI approaches are widely using machine learning for real-time, automated performance evaluation, stepping towards facilitating tailored feedback & assessing technical proficiency. Moreover, hyperrealistic, patient-specific digital twins for preoperative rehearsal, AI-powered surgical robotics training, & VR-based team training are supporting improvements in nontechnical skills.

Spurring Patient-Specific Simulation

Surgeons are fostering the use of 3D printing & imaging data to enable them to rehearse specific prospective patient cases & elevate procedural planning.

Promoting Integration into Curricula

Rigorous regulatory bodies & institutions are exploring mandatory simulation-based training in residency programs to replace the traditional see one, do one apprenticeship model.

Focusing on Sustainability in Resource-Limited Areas

The market is actively searching for affordable, portable simulation models to utilize in Low- & Middle-Income Countries (LMICs).

| Table | Scope |

| Market Size in 2026 | USD 4.42 Billion |

| Projected Market Size in 2035 | USD 15.31 Billion |

| CAGR (2026 - 2035) | 14.8% |

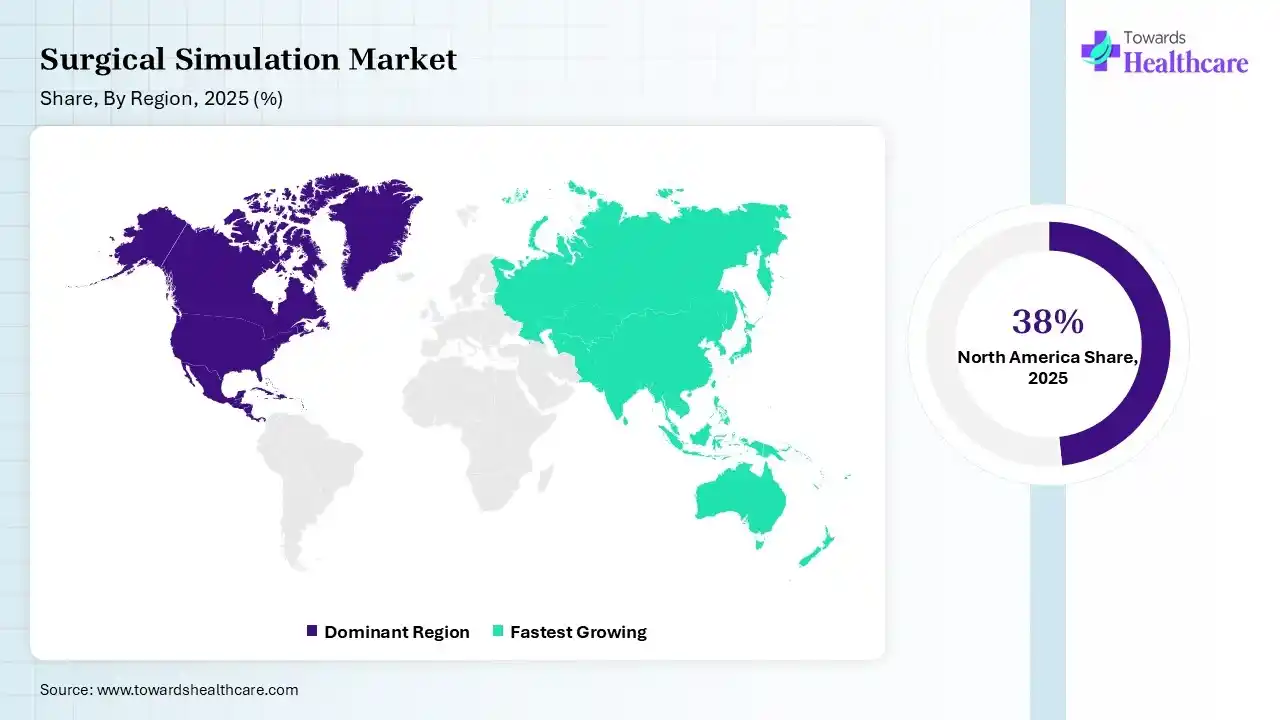

| Leading Region | North America by 38% |

| Key Applications | Surgical skills training, minimally invasive surgery training, robotic surgery simulation, laparoscopic simulation, orthopedic simulation, cardiovascular simulation, neurosurgery simulation, pre-operative planning, competency assessment |

| Primary End Users | Hospitals, medical universities, surgical training centers, residency programs, medical device companies, research institutions |

| Key Challenges | High equipment costs, limited reimbursement models, integration challenges, need for clinical validation, adoption barriers in developing regions |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Technology, By Application, By End User, By Surgical Specialty, By Region |

| Top Key Players | Materialise, Stratasys, CAE Inc., Surgical Science, Mentice, Gaumard Scientific, Simulab Corporation, VirtaMed AG,3-Dmed Learning Through Simulation, Laerdal Medical |

| Segment | Share 2025 (%) |

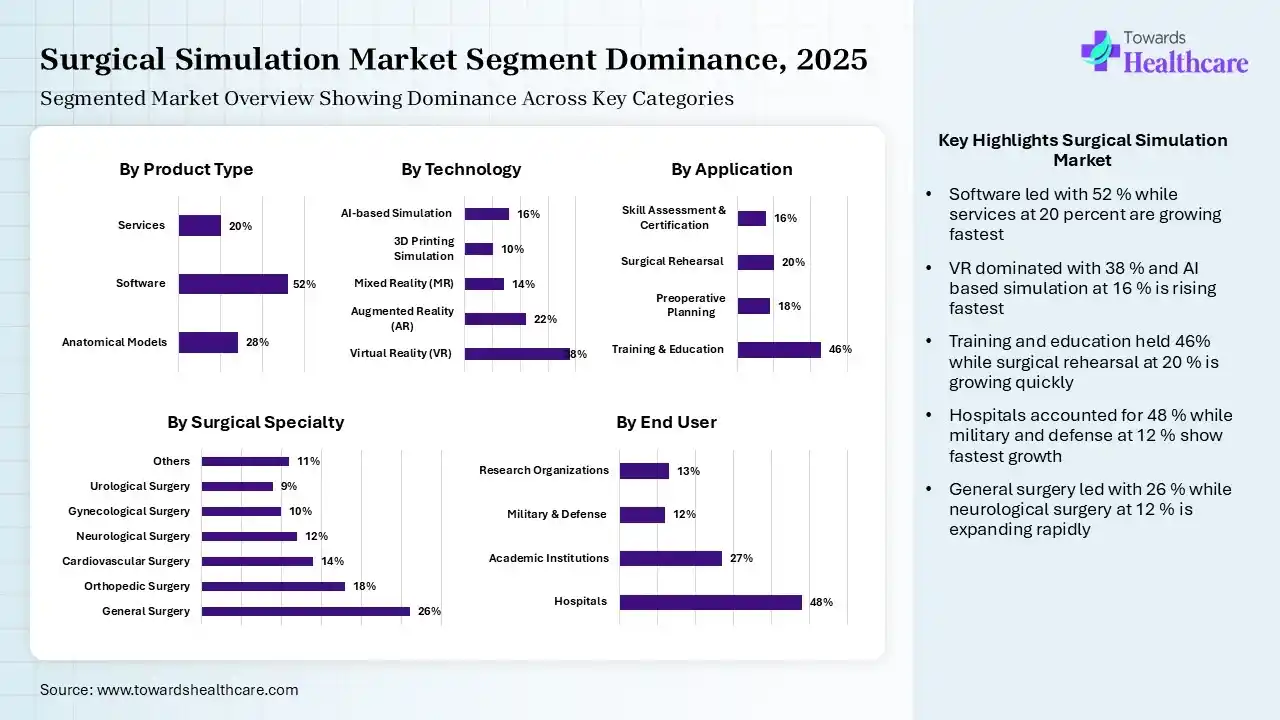

| Anatomical Models | 28% |

| Software | 52% |

| Services | 20% |

The Software Segment Dominated the Market in 2025

In 2025, the software segment held 52% share of the surgical simulation market. Major catalysts are the growing need to lower errors and the widespread adoption of 3D printing for anatomical modeling & cloud-based platforms for scalable training. The latest software offers objective, metrics-based evaluation of user skills, like kinematic analysis, time effectiveness, & tissue handling accuracy.

The anatomical models segment captured the second-largest share of 28% in 2025, due to the surging demand for high-fidelity, inexpensive, & standardized procedural training. The use of deep learning provides accurate, patient-specific 3D models from DICOM data, coupled with automated segmentation of organs, blood vessels, & tumors.

However, the services segment held 20% share in 2025 & is predicted to register rapid growth in the surgical simulation market. This mainly covers specialized training, curriculum integration, cloud-based platform access, & performance analytics. Alongside, the market is promoting designing, installing, & maintaining simulation labs, such as software updates & hardware maintenance.

| Segment | Share 2025 (%) |

| Virtual Reality (VR) | 38% |

| Augmented Reality (AR) | 22% |

| Mixed Reality (MR) | 14% |

| 3D Printing Simulation | 10% |

| AI-based Simulation | 16% |

The Virtual Reality (VR) Segment Led the Market in 2025

The virtual reality (VR) segment dominated with 38% share of the market in 2025. Dominance is fueled by their speeded skill acquisition, haptic feedback for realistic tissue simulation, & affordable, on-demand training. The Virtual Reality Surgery Simulator (VRSS) project has used off-the-shelf VR equipment to develop a cost-effective simulation, which makes high-quality surgical training available to several institutions.

The augmented reality (AR) segment accounted for 22% share of the surgical simulation market. AR solutions show optimized real-time visualization during procedures. Also, assists in the overlay of anatomical data, with a pivotal role in intraoperative guidance.

Whereas the AI-based simulation segment held 16% share in 2025 & is estimated to grow fastest during the forecast period. This technology allows adaptive learning & predictive analytics, & also customizes training pathways. However, IVAs offer real-time, automated monitoring of surgical trainees, finding errors in real-time, specifically in laparoscopic training.

The mixed reality (MR) segment captured 14% share in 2025, due to the emerging combination of VR and AR for hybrid simulation environments. Also, integrates MR visualization with physical, haptic-enabled mannequins to facilitate realistic tactile feedback during procedures.

The 3D printing simulation segment held 10% share in 2025, due to the development of patient-specific, anatomical models for pre-operative planning, simulation, and training. Surgeons are increasingly leveraging needle passage for cardiac patches, vascular repairs, or dental surgeries, which enables trainees to repeat procedures to achieve the goal.

| Segment | Share 2025 (%) |

| Training & Education | 46% |

| Preoperative Planning | 18% |

| Surgical Rehearsal | 20% |

| Skill Assessment & Certification | 16% |

The Training & Education Segment Was Dominant in the Market in 2025

The training & education segment led with 46% share of the surgical simulation market in 2025. This is driven by the expansion of specialized, complex procedures, which require training tools that enable surgeons to acquire proficiency outside the operating room. Interactive apps enable trainees to practice surgical steps in a step-by-step format on mobile devices.

The surgical rehearsal segment captured 20% share in 2025 & is anticipated to expand fastest. The market is allowing surgeons to practice patient-specific procedures with minimal complications & operation time. Surgeons are fostering hyper-realistic, patient-specific platforms leveraging AI, VR, & 3D-printed hydrogel models.

The preoperative planning segment held 18% share of the surgical simulation market, due to rising need for increased accuracy, lowered operative risks, & tailored, patient-specific treatment. Diverse 3D-printed physical models are enabling tactile rehearsal, with practice incisions, handling instruments, & detecting possible challenges.

The skill assessment & certification segment captured 16% share by facilitating objective evaluation metrics for surgeons & assisting credentialing processes. The market raises safety, includes objectivity to board certifications, & acts as a tool for remediation.

| Segment | Share 2025 (%) |

| Hospitals | 48% |

| Academic Institutions | 27% |

| Military & Defense | 12% |

| Research Organizations | 13% |

The Hospitals Segment Led the Market in 2025

In 2025, the hospitals segment held a major share of 48% of the market. A rise in surgical volumes, demand for less invasive procedures, & broader adoption of AR & VR, drives the segmental dominance. To overcome the lack of specialized surgeons & restricted resident hours, hospitals are executing advanced simulation programs.

The academic institutions segment captured the second-largest share of 27% of the surgical simulation market. Key growth factors are expanding adoption in medical education curricula, with enhanced hands-on training quality. Also, government funding is fostering deployment.

The research organizations segment held 13% share of the market in 2025. They emphasize validation of simulation models to optimize operative performance & minimize training errors, often joining with industry to bolster realism. They also help in clinical trials & experimentations.

The military & defense segment held 12% of the market share and is predicted to witness the fastest growth, due to the escalating need for sophisticated combat casualty care training, high-fidelity trauma simulation, & the need for risk-free, scalable training solutions in austere environments.

| Segment | Share 2025 (%) |

| General Surgery | 26% |

| Orthopedic Surgery | 18% |

| Cardiovascular Surgery | 14% |

| Neurological Surgery | 12% |

| Gynecological Surgery | 10% |

| Urological Surgery | 9% |

| Others | 11% |

The General Surgery Segment Dominated the Market in 2025

In 2025, the general surgery segment captured the largest share of 26% of the surgical simulation market. Globally surging need to raise patient safety, surge trainee learning curves, & promote complex, minimally invasive, or robotic techniques outside the operating room, impacts the adoption in these kinds of surgeries. Breakthroughs include enhancement in technical skills through SBT & fulfilling competency-based education requirements.

The orthopedic surgery segment held 18% share in 2025, due to the increasing prevalence of orthopaedic conditions. In these cases, simulation is employed for joint replacement procedures, which boosts precision in implants.

The cardiovascular surgery segment captured 14% share in 2025, as the globe is facing a massive burden of CVD instances. Advanced simulation is assisting in complex heart procedures training, which enhances outcomes in high-risk surgeries.

The neurological surgery segment captured 12% of the market share in 2025 and is estimated to expand at a rapid CAGR in the surgical simulation market. Simulation has a vital role in brain & spine procedures, coupled with the wider use of neuroendoscopy & robot-assisted surgery, which requires novel psychomotor skills.

")

North America led with 38% share of the surgical simulation market in 2025. The regional growth is propelled by the growing investment in medical training & robust healthcare infrastructure. Immersive clinical trials are demonstrating that AI–augmented tailored expert instruction majorly enhances surgical performance.

For instance,

U.S. Market Trends

The U.S. market, with 30% share, fosters innovation through leading players. Various U.S. universities & hospitals have highly adopted these simulation approaches, and also encouraged integration of simulation software into them to enable instant training, skill assessment, etc.

Asia Pacific held 22% of the market share and is estimated to show the fastest expansion in the surgical simulation market, due to the faster, continuous evolution in hospital infrastructure & rising number of medical universities across Southeast Asia & India, which raises demand.

For instance,

China Market Trends

However, China is a center for employing 5G to connect rural clinics to top-tier hospitals, with successful remote operations performed over 4,000 km away from the patient. They have also introduced a vast robotic telesurgery center to train young staff remotely.

| Ecosystem Category | Description | Key Participants |

| Technology Providers | Companies developing VR, AR, AI, haptic feedback, and simulation technologies | FundamentalVR, PrecisionOS, Osso VR, Surgical Science |

| Product Manufacturers | Developers of physical surgical trainers, anatomical models, laparoscopic simulators, robotic training platforms | 3D Systems, CAE Healthcare, Limbs & Things |

| Service Providers | Surgical education, simulation-based training programs, certification support | Simbionix, Surgical Science training solutions |

| Platform Providers | Digital surgical simulation platforms for hospitals and academic institutions | Osso VR, PrecisionOS, FundamentalVR |

| CROs/CDMOs | Limited direct involvement; mainly used for medical device training validation | Not a core segment |

| Software Vendors | VR surgical simulation software, AI assessment tools, cloud-based simulation platforms | Surgical Science, FundamentalVR |

| Research Institutions | Develop simulation methodologies and surgical competency frameworks | Academic medical centers, surgical societies |

| End User Industries | Healthcare providers, medical education, medical device companies | Hospitals, universities, surgical academies |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 58% | 30% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Surgical Science Sweden AB | Gothenburg, Sweden | Sweden | Global leader in surgical simulation software and virtual training solutions with strong hospital and medical device partnerships | LAP Mentor, VR simulation platforms, robotic surgery simulation |

| 3D Systems | Rock Hill, South Carolina, USA | USA | Major healthcare simulation provider through medical modeling and surgical training technologies | Simbionix surgical simulators, anatomical models |

| CAE Healthcare | Sarasota, Florida, USA | USA | Established global healthcare simulation provider used by hospitals and medical schools | Surgical simulation, patient simulation platforms |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| PrecisionOS | Vancouver, British Columbia, Canada | Canada | Specialized VR surgical education company focused on orthopedic procedures | VR surgical training platform |

| Limbs & Things | Bristol, England, UK | UK | Long-standing manufacturer of physical medical simulation models | Surgical trainers, procedural simulation models |

| Mentice AB | Gothenburg, Sweden | Sweden | Specialized in endovascular and vascular procedure simulation | VIST simulation systems |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| VISTAS Medical Education | USA | USA | Provides specialized simulation-based medical education solutions | Surgical education simulation |

| Touch Surgery | London, England, UK | UK | Digital surgery education platform used for procedure visualization and learning | Touch Surgery platform |

| EON Reality | Irvine, California, USA | USA | Develops immersive VR learning environments including healthcare applications | VR medical training solutions |

Strengths

Weaknesses

Opportunities

By Product Type

By Technology

By Application

By End User

By Surgical Specialty

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar