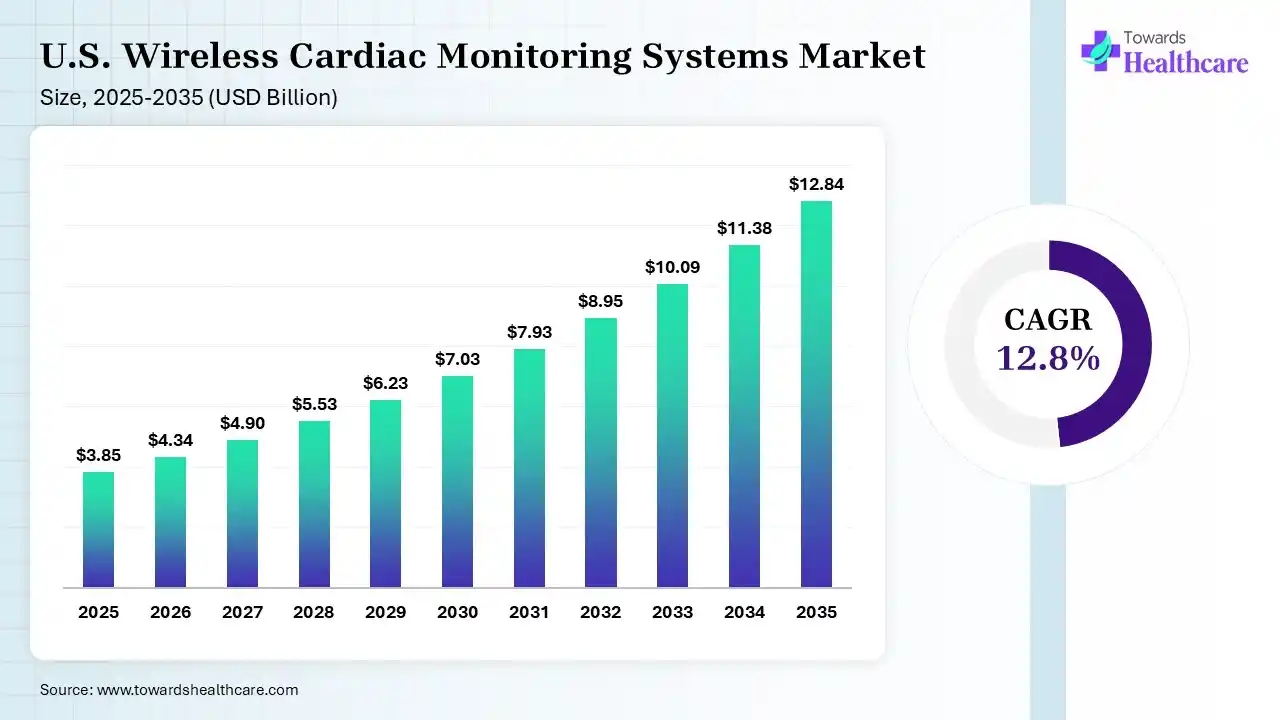

The U.S. wireless cardiac monitoring systems market size was estimated at USD 3.85 billion in 2025 and is predicted to increase from USD 4.34 billion in 2026 to approximately USD 12.84 billion by 2035, expanding at a CAGR of 12.8% from 2026 to 2035. A notable effort is fostering developments in wearables, RPM solutions, & integrated systems. Also, the market is highly pushing AI-powered solutions & advanced patch-based devices.

")

The U.S. wireless cardiac monitoring systems market encompasses a range of wearable or implantable devices that continuously track heart activity (ECG), heart rate, & other vitals without wires, & further share data via Bluetooth or cellular networks to healthcare providers. The overall adoption is driven by a growing geriatric population, modifying lifestyles in the U.S., which results in a higher rate of arrhythmia, heart failure, and hypertension, & demands for continuous monitoring, coupled with AI-powered devices & RPM approaches.

Primarily, the U.S. healthcare system is highly fostering AI applications in filtering out false positives from long-term monitoring, like insertable cardiac monitors (ICMs), where AI-powered ICMs have demonstrated a nearly 58.5% reduction in non-actionable alerts. Gradual breakthroughs involve smaller, patient-friendly wearable sensors & patch-based devices, along with the use of predictive analytics for early treatment.

Inclining Towards Multimodal Sensor Integration

Eventual developments are spurring novelty in the devices by integrating ECG with other metrics, including photoplethysmography (PPG) & seismocardiogram (SCG) for a detailed understanding of cardiac mechanics.

Innovations in Soft & Conformal Electronics

The trend is following a progression in flexible, breathable electronic skin to offer long-term monitoring comfort without skin irritation.

Extensive ‘Hospital-at-Home’ Integration

Research activities are shifting towards the combination of wireless monitors with home telehealth programs to control chronic conditions, like heart failure, with emphasis on lowering 30-day readmissions.

| Table | Scope |

| Market Size in 2026 | USD 1.55 Billion |

| Projected Market Size in 2035 | USD 2.83 Billion |

| CAGR (2026 - 2035) | 6.9% |

| Leading Region | North America by 34% |

| Key Applications | Arrhythmia detection, atrial fibrillation monitoring, heart failure management, post-discharge monitoring, stroke risk assessment, remote patient monitoring, preventive cardiac care |

| Primary End Users | Hospitals, cardiology clinics, ambulatory diagnostic centers, electrophysiology centers, home healthcare providers, patients |

| Key Growth Drivers | Rising cardiovascular disease burden, increasing adoption of remote patient monitoring, AI-based ECG analysis, reimbursement support, aging population, shift toward outpatient cardiac care |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Technology, By Application, By End User, By Distribution Channel |

| Top Key Players | iRhythm Technologies, Inc., Medtronic plc, Philips, Abbott Laboratories, Boston Scientific Corporation, Biotronik, GE Healthcare, Baxter International, Inc., AliveCor, Inc., Medicomp, Inc. |

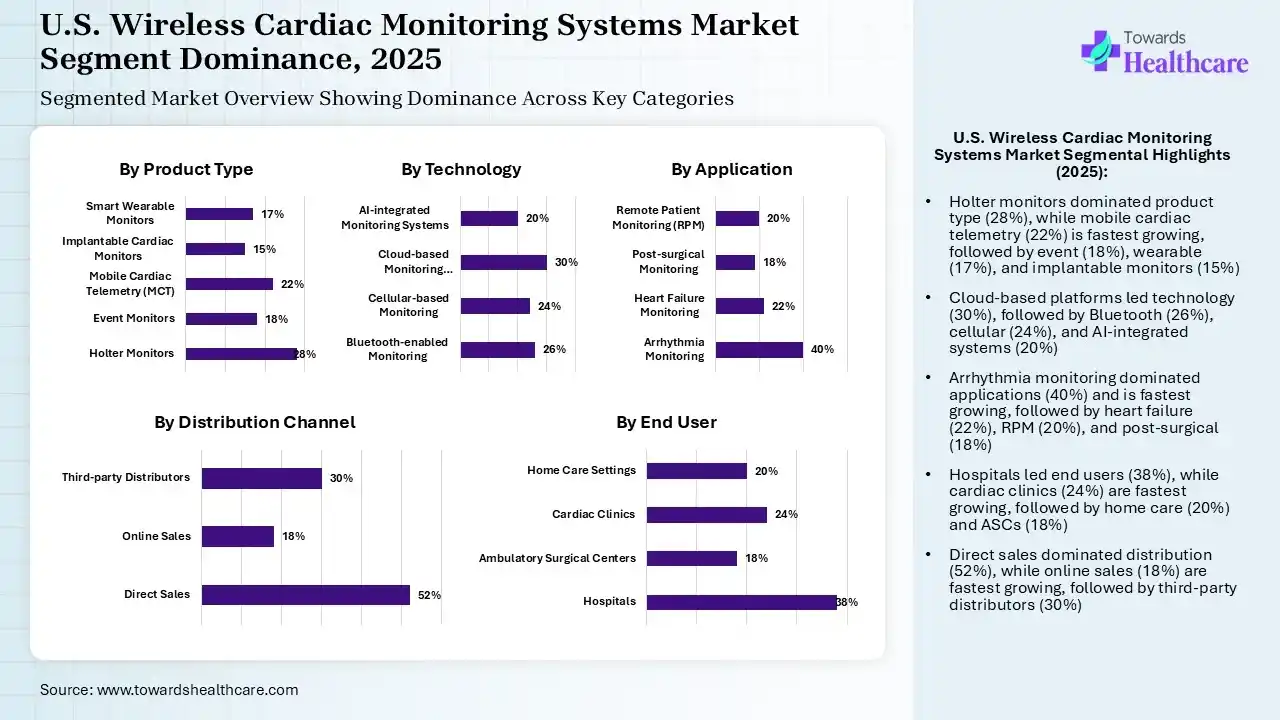

| Segment | Share 2025 (%) |

| Holter Monitors | 28% |

| Event Monitors | 18% |

| Mobile Cardiac Telemetry (MCT) | 22% |

| Implantable Cardiac Monitors | 15% |

| Smart Wearable Monitors | 17% |

The Holter Monitors Segment Dominated the Market in 2025

In 2025, the Holter monitors segment captured a major share of 28% of the U.S. wireless cardiac monitoring systems market. As per a study, the U.S. is experiencing nearly 121.5 million CVD cases per year, which demands consistent monitoring. Dominance is fueled by the use of portable, noninvasive devices that enable patients to maintain daily routines & also record heart activity.

However, the mobile cardiac telemetry (MCT) segment accounted for 22% share in 2025 & is predicted to expand fastest. A specific driver is its offering, which gives superior real-time analysis as compared to traditional Holter monitors, resulting in increased adoption by clinicians for eliciting arrhythmia detection. Ongoing advances are promoting smaller, fully disposable, & water-resistant patches to boost patient compliance.

The event monitors segment held 18% share of the U.S. wireless cardiac monitoring systems market. They have broader applications, such as the detection of atrial fibrillation (AF) after stroke, evaluation of drug effectiveness, & monitoring for arrhythmias following cardiac ablation. Numerous physicians widely use it for intermittent symptom tracking.

The smart wearable monitors segment captured 17% share in 2025, due to the surging health awareness in the U.S. Along with robust patient preference for non-invasive & user-friendly devices, the market is actively developing AI tools to assess single-lead ECGs from consumer smartwatches to find structural heart disease with greater accuracy.

The implantable cardiac monitors segment accounted for 15% share in 2025. A notable rise in arrhythmia instances and remote care demand requires ICMs to provide continuous, multi-year monitoring. Emerging innovations are encouraging to establish smaller, with enhanced battery life & improved memory to enable long-term recording.

| Segment | Share 2025 (%) |

| Bluetooth-enabled Monitoring | 26% |

| Cellular-based Monitoring | 24% |

| Cloud-based Monitoring Platforms | 30% |

| AI-integrated Monitoring Systems | 20% |

The Cloud-Based Monitoring Platforms Segment Led the Market in 2025

The cloud-based monitoring platforms segment captured a dominant share of 30% of the U.S. wireless cardiac monitoring systems market in 2025 & is anticipated to expand rapidly. The segmental growth is fueled by its constant, real-time remote patient monitoring, lowering hospital readmissions, & the use of AI for early detection of cardiac events. Specifically, cloud-based ABPM platforms are providing remote management of hypertension, & also allowing clinicians to view guideline-concordant reports remotely.

The Bluetooth-enabled monitoring segment held the second-largest share of 26% in 2025. This approach enables devices to transmit data directly to patient smartphones for instantaneous, real-time transmission to healthcare providers, which offers immediate detection of complexities. A key development comprises Bluetooth-enabled blood pressure cuffs for automatic syncing with medical records.

The cellular-based monitoring segment captured 24% share of the U.S. wireless cardiac monitoring systems market in 2025. The widespread adoption of implantable hemodynamic monitors & wearable sensors is allowing transmission of daily data on pulmonary artery pressure, thoracic impedance, & heart rate to determine fluid overload early. Major trends are showcasing the development of self-powered, piezoelectric ‘CardioHarvest-Net’ systems.

The AI-integrated monitoring systems segment accounted for 20% share of the market in 2025, due to the extensive analysis of massive datasets, & rapid FDA approvals for AI-assisted devices. The market has explored new AI-driven filters, like AccuRhythm AI for insertable cardiac monitors (ICMs), which finally reduces workload on clinic staff.

| Segment | Share 2025 (%) |

| Arrhythmia Monitoring | 40% |

| Heart Failure Monitoring | 22% |

| Post-surgical Monitoring | 18% |

| Remote Patient Monitoring (RPM) | 20% |

The Arrhythmia Monitoring Segment Was Dominant in the Market in 2025

In 2025, the arrhythmia monitoring segment led with 40% share of the U.S. wireless cardiac monitoring systems market & is predicted to register rapid growth in the coming era. In this year, there were approximately 10.5 million U.S. adults who had atrial fibrillation, which has raised arrhythmia concerns, coupled with substantial lifestyle changes. The U.S. has expanded AI-powered ECG signal & FDA clearances for devices to record multiple vital signs simultaneously.

The heart failure monitoring segment held 22% share in 2025, due to the accelerating prevalence of heart failures, especially among the geriatric & elder population of the U.S. Leading firms are focusing on diversity in pulmonary artery sensors, which detect fluid build-up weeks before symptoms occur, & also enable proactive medication adjustments to omit expansive hospital stays.

The remote patient monitoring (RPM) segment accounted for 20% share of the U.S. wireless cardiac monitoring systems market, due to the rigorous expansion of telehealth approaches. To bolster affordability, the U.S. is actively innovating wearable sensors, AI-assisted analytics, & mobile health apps, which allow accurate, real-time data collection.

The post-surgical monitoring segment captured 18% share in 2025, as hospitals are leveraging post-operative systems to enable early detection of complications, like arrhythmia or bleeding, before they require emergency re-hospitalization. Ongoing studies are spurring Smartcardia (SC) & similar adhesive patch devices for consistent recording of single-lead ECG, temperature, & pulse oximetry.

| Segment | Share 2025 (%) |

| Hospitals | 38% |

| Ambulatory Surgical Centers | 18% |

| Cardiac Clinics | 24% |

| Home Care Settings | 20% |

The Hospitals Segment Dominated the Market in 2025

In 2025, the hospitals segment registered dominance with 38% share of the U.S. wireless cardiac monitoring systems market. Along with a huge burden of an ageing population, the U.S. has been surging, with Medicare & insurance coverage for remote patient monitoring (RPM) & extended ECG services. Emerging telemetry is moving towards mobile, app-based platforms to view telemetry data from anywhere in the hospital.

The cardiac clinics segment held the second-largest share of 24% in 2025 & is estimated to expand rapidly. They are highly emphasizing proactive management to lower readmission rates & expenditures, also preferring continuous wireless monitoring. Also, using LifeSignals' app-enabled data uploading enables expedited data analysis & triage, often minimizing the burden on clinicians.

The home care settings segment captured 20% share of the U.S. wireless cardiac monitoring systems market, due to the rising demand for remote care. Particularly, CMS & private payers are broadening coverage for RPM services, enabling providers to bill for 30-day bundles & remote care management, & greater improvement in smartwatches for their role in screening for arrhythmias in asymptomatic populations.

The ambulatory surgical centers segment accounted for a notable share of 18% in 2025. The escalating need for in-center & post-operative wireless monitoring, coupled with ASCs’ higher efficiency, cost-effectiveness & faster recovery times, drives the segmental growth. The FDA is increasingly clearing wireless, wearable monitors for continuous blood pressure & cardiac output, specifically for ASC.

| Segment | Share 2025 (%) |

| Direct Sales | 52% |

| Online Sales | 18% |

| Third-party Distributors | 30% |

The Direct Sales Segment Led the Market in 2025

The direct sales segment was dominant with a 52% of the U.S. wireless cardiac monitoring systems market in 2025. Dominance is driven by a key step towards closer, direct-to-hospital and direct-to-patient models, and also assists in educating cardiologists & Electrophysiologists (EPs) on sophisticated, proprietary technology to ensure patient compliance. Many AI-driven patch-based technologies & cloud analytics are enabling direct-to-hospital sales of software-as-a-service models.

The third-party distributors segment accounted for the second-largest share of 30% in 2025, as they resolve the gap among device manufacturers and healthcare providers, handling distribution, data monitoring, & technical assistance. This significantly covers Independent Diagnostic Testing Facilities (IDTFs) & specialized logistics partners in reaching hospitals, clinics, & home care settings.

However, the online sales segment held 18% share in 2025 & is predicted to show the fastest expansion. To meet the increasing patient demand for RPM, companies are selling devices either directly to consumers or through healthcare providers, coupled with data syncing via Bluetooth to apps. These players are also pushing broader accessibility for immediate online purchase & facilitating medical-grade ECG data.

| Ecosystem Category | Description | Key Participants |

| Technology Providers | Sensor technology, wireless connectivity, AI algorithms, cloud infrastructure | iRhythm, AliveCor, Philips, Medtronic |

| Product Manufacturers | Wearable ECG patches, implantable monitors, telemetry systems | Abbott, Boston Scientific, iRhythm, GE HealthCare |

| Service Providers | Remote monitoring services, ECG analysis, clinical reporting | Philips, BioTelemetry legacy platforms, Preventice Solutions |

| Platform Providers | Cloud-based cardiac data platforms and physician dashboards | Philips, Medtronic, Vector Remote Care |

| CROs/CDMOs | Limited direct relevance; involved in medical device development and clinical validation | Specialized medical device CROs |

| Software Vendors | AI interpretation, workflow integration, remote monitoring software | AliveCor, Philips, Medtronic |

| Research Institutions | Clinical studies, electrophysiology research, AI validation | Universities, hospitals, cardiology research centers |

| End-User Industries | Healthcare delivery organizations adopting monitoring technologies | Hospitals, clinics, home healthcare networks |

R&D

Distribution to Hospitals & Clinics

Patient Support & Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 65% | 30% | 5% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| iRhythm Technologies, Inc. | San Francisco, California, USA | USA | One of the strongest pure-play wireless cardiac monitoring companies with major focus on ambulatory ECG monitoring | Zio XT, Zio AT, Zio monitor platform, AI-based ECG analysis |

| Medtronic plc | Minneapolis, Minnesota, USA | USA | Global cardiac technology leader with implantable monitoring and remote cardiac management ecosystem | LINQ II Insertable Cardiac Monitor, CareLink remote monitoring |

| Abbott Laboratories | Abbott Park, Illinois, USA | USA | Major cardiac device company with implantable cardiac monitoring technologies | Confirm Rx Insertable Cardiac Monitor, Merlin.net remote monitoring |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| GE HealthCare Technologies Inc. | Chicago, Illinois, USA | USA | Strong hospital monitoring presence and connected cardiac care systems | CARESCAPE monitoring, wireless telemetry solutions |

| AliveCor, Inc. | Mountain View, California, USA | USA | Pioneer in consumer and clinical ECG wearables with AI interpretation | KardiaMobile ECG devices, AI ECG analysis |

| VitalConnect, Inc. | Campbell, California, USA | USA | Specialized wearable biosensor company focused on remote cardiac monitoring | VitalPatch wearable biosensor, remote monitoring platform |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Vivalink, Inc. | Campbell, California, USA | USA | Emerging wearable biosensor company focused on remote patient monitoring | Medical-grade ECG wearable sensors |

| InfoBionic, Inc. | Lowell, Massachusetts, USA | USA | Specialized remote cardiac monitoring technology provider | MoMe ARC mobile cardiac telemetry platform |

| SmartCardia Inc. | Palo Alto, California, USA | USA | Developing AI-enabled multi-lead wearable ECG monitoring solutions | SmartCardia 7L ECG patch platform |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Technology

By Application

By End User

By Distribution Channel

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar