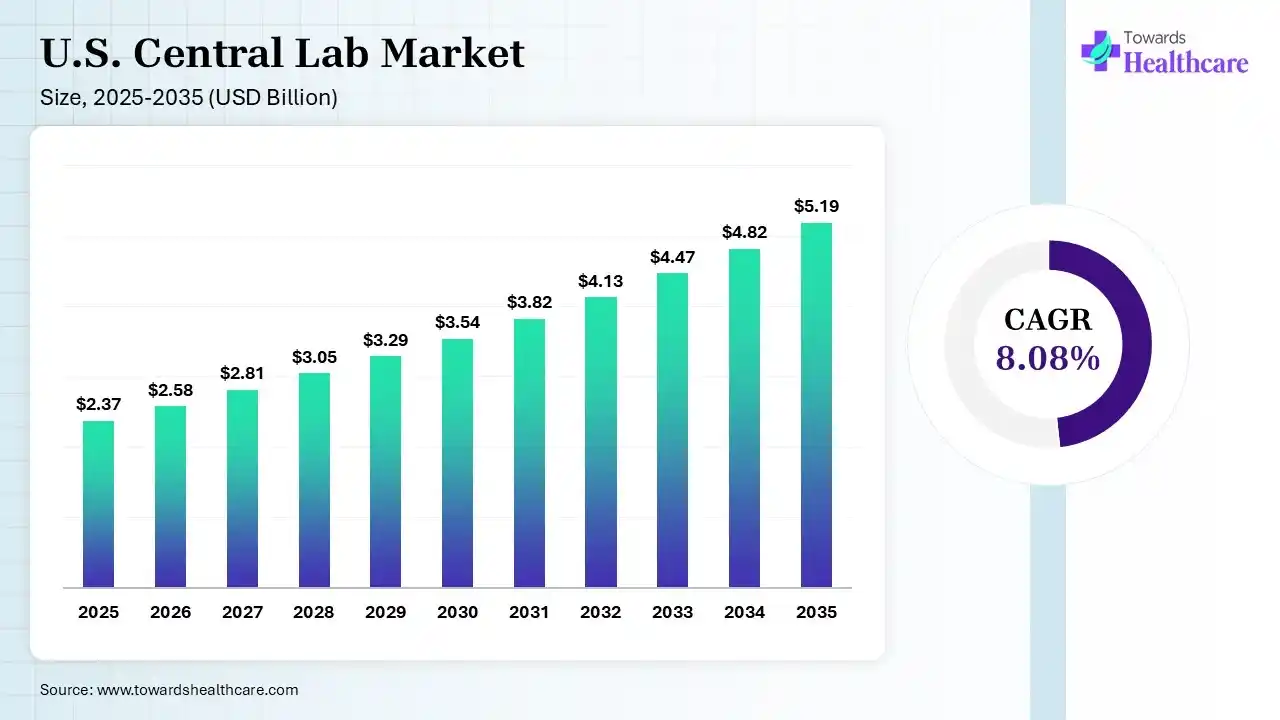

The U.S. central lab market size was estimated at USD 2.37 billion in 2025 and is predicted to increase from USD 2.58 billion in 2026 to approximately USD 5.19 billion by 2035, expanding at a CAGR of 8.08% from 2026 to 2035. The market is expanding steadily due to increasing clinical research activities, growing demand for standardized laboratory testing, and rising adoption of precision medicine in drug development. Strong investments from pharmaceutical and biotechnology companies, along with advancements in diagnostic technologies, continue to support market growth across the country.

")

A U.S. Central is a specialized laboratory facility that performs standardized testing, sample analysis, and data management services for clinical trials and healthcare research across multiple study locations in the United States. The U.S. central lab market is growing due to increasing clinical trial activities, rising demand for accurate and standardized laboratory testing, and expanding adoption of precision medicine. Pharmaceutical and biotechnology companies are increasingly relying on central labs for efficient sample management, biomarker testing, and faster data reporting. In addition, advancements in molecular diagnostics and growth in drug development are further supporting market expansion across the country.

Artificial intelligence is enhancing the market by improving data analysis, automating sample processing, and reducing diagnostic errors. AI-powered tools help laboratories manage large clinical trial datasets more efficiently, accelerate result interpretation, and support faster decision-making in drug development. Additionally, predictive analytics and machine learning are strengthening workflow optimization, improving testing accuracy, and enabling more personalized and precise healthcare research outcomes.

Rising Demand for Precision Medicine Testing

The growing focus on precision medicine is increasing the need for biomarker analysis, genetic testing, and specialized diagnostic services. Central laboratories are expanding advanced testing capabilities to support targeted therapies and personalized treatment approaches in clinical research and healthcare applications.

Increasing Clinical Trial Activities

The expansion of pharmaceutical and biotechnology research is driving higher demand for centralized laboratory services. Central labs play a crucial role in maintaining standardized testing, sample management, and consistent data reporting across multi-site clinical trials in the United States.

Growth of Decentralized Clinical Trials

The adoption of decentralized and hybrid clinical trial models is creating new opportunities for central laboratories. Companies are strengthening logistics networks, remote sample collection systems, and digital coordination platforms to improve patient participation and streamline nationwide clinical research operations.

| Table | Scope |

| Market Size in 2026 | USD 2.58 Billion |

| Projected Market Size in 2035 | USD 5.19 Billion |

| CAGR (2026 - 2035) | 8.08% |

| Key Applications | Clinical trials, biomarker testing, companion diagnostics, pharmacokinetics (PK), pharmacodynamics (PD), genomic analysis, infectious disease testing, oncology trials, biospecimen management |

| Primary End Users | Pharmaceutical companies, biotechnology companies, CROs, medical device manufacturers, academic research organizations |

| Key Growth Drivers | Growth in clinical trials, precision medicine adoption, biomarker-driven studies, decentralized trials, cell & gene therapy development, increasing outsourcing by sponsors |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By Phase, By End User, By Test Type, By Technology |

| Top Key Players | LabCorp, Quest Diagnostics, IQVIA, Thermo Fisher Scientific, Eurofins Scientific , Medpace |

The Safety Testing Segment Led the Market in 2025

In 2025, the safety testing segment held a major share of 23.50% of the U.S. central lab market. Dominance is driven by its vital role in clinical trials, which provides standardized hematology, biochemistry, & urinalysis testing. Also, this service offers regulatory compliance, worldwide harmonized data integrity, & lowered analytical expenditures. Bolstering oncology & rare-disease drugs fuels demand for highly specific safety, genetic & biomarker monitoring.

The genomic & molecular testing segment captured a 22.23% share in 2025 & is predicted to expand at a 9.42% CAGR. Increasing demand for precision medicine, growth in biomarker-driven clinical trials, & declining costs of next-generation sequencing (NGS) are propelling the progression of respective services. By leveraging extensive genomic profiling, these central labs are assessing numerous biomarkers simultaneously, matching patients with targeted therapies & clinical trials.

However, the specialty testing & biomarkers segment held a 21.46% share of the U.S. central lab market in 2025. Specifically, the surge in movement towards targeted therapies has escalated the demand for specialized biomarker services, like genetic, proteomic, & molecular tests to stratify patient populations & monitor drug efficacy. The recognition of an individual’s genetic makeup & their response to drugs propels the need for specialty testing services.

The pathology & histology services segment accounted for a 14.36% share in 2025. Booming biological drugs, cell therapies, & immunotherapies necessitate extensive, standardized tissue analysis to estimate efficacy. In the U.S, higher adoption of digital scanners is enabling central labs to digitize histology slides for instant, remote review by sub-specialty pathologists regardless of location.

The Oncology Segment Dominated the Market in 2025

In 2025, the oncology segment was dominant with a 34.68% share of the U.S. central lab market, due to the high incidence of cancer & the continued rise in oncology-focused clinical trials. Cancer research heavily depends on advanced biomarker testing & heavily depends on advanced biomarker testing, genetic profiling, & companion diagnostics to support targeted & customized therapies. Whereas strong pharmaceutical investment, rapid drug development pipelines, & growing adoption of precision oncology approaches further drive demand for centralized laboratory services in this therapeutic area.

The infectious diseases segment captured the second-largest share of 19.62% of the market in 2025. This is mainly driven by the continuous need for monitoring, diagnosis, & clinical research on viral, bacterial, & emerging pathogens. Alongside, frequent outbreaks & global health concerns are fueling large-scale clinical trials & surveillance studies. Moreover, robust government funding, vaccine development programs, & accelerating demand for rapid diagnostic testing further support the progression of central lab services in these cases.

On the other hand, the cardiovascular & metabolic diseases (CVMD) segment accounted for a 17.56% share of the U.S. central lab market. Major catalysts are a massive rise in instances of obesity, Type 2 diabetes, insulin resistance, & hypertension, which are developing a cascading clinical cycle (Cardiovascular-Kidney-Metabolic syndrome). This is significantly targeted by pharmaceutical R&D & specialized diagnostic testing. The U.S. labs are emphasizing novel multi-organ guidelines that focus on an assessment of liver, kidney, & heart markers simultaneously.

The rare diseases & genetic disorders segment captured a 5.67% share in 2025 & is estimated to expand at an 11.84% CAGR. Major advances in Next-Generation Sequencing (NGS), raising FDA approvals for targeted therapies, & a countrywide focus to shorten the 5-to-7-year diagnostic odyssey drive the respective segmental expansion. Particularly, state-level mandates have widened to test for more congenital genetic issues, resulting in rising early laboratory screening volumes.

The Phase III (Late Phase) Segment Was Dominant in the Market in 2025

The Phase III (late phase) segment held a 45.18% share of the U.S. central lab market in 2025. A key driver is the high volume & complexity of late-stage clinical trials required for regulatory approvals. These studies involve large patient populations, multiple sites, & comprehensive laboratory testing to ensure drug safety & efficacy. Central labs are essential for maintaining standardized data, ensuring regulatory compliance, & conveying reliable results, making them crucial in phase III clinical research activities.

The Phase I & II (early phase) segment captured the second-largest share of 42.82% in 2025 & is predicted to expand rapidly at an 8.56% CAGR. The segmental expansion is driven by rising early-stage drug development activities & increasing investment in novel therapies. These trials require detailed safety investment in novel therapies. Meanwhile, pharmaceutical & biotech leaders are heavily investing in phase II studies to find robust candidates before large-scale testing.

Moreover, the Phase IV (post-marketing surveillance) segment held a 12.00% share of the U.S. central lab market in 2025, due to the growing focus on post-marketing surveillance & real-world evidence generation. Phase IV studies are providing monitoring of long-term drug safety, effectiveness, & rare adverse effects after regulatory approvals. Besides this, increasing regulatory requirements, rising chronic disease burden, & the need for ongoing patient monitoring are driving demand for centralized laboratory testing & data management in phase IV clinical research.

The Small Molecules Segment Led the Market in 2025

The small molecules segment dominated with a 35.26% share of the market in 2025. Elevating demand for small molecule inhibitors targeting cancer pathways & neurological diseases is majorly spurring central lab sample volumes. Besides this, many pharma & biotech companies prefer small molecules for their economic scalability, structural stability, & superior oral dosing profiles as compared to large molecules.

In 2025, the biologics (large molecules) segment accounted for a 32.00% share of the U.S. central lab market. The U.S. is mainly demanding monoclonal antibodies (mAbs) & antibody-drug conjugates (ADCs), which inherently risk triggering an immune response. Although central labs are dependent upon running highly specialized immunoassays to determine anti-drug antibodies (ADAs) & neutralizing antibodies (NAbs).

On the other hand, the advanced therapies (ATMP) segment held a 20.56% share in 2025 & is anticipated to expand at a 11.82% CAGR in the coming era. This mainly covers diverse cell therapies, gene therapies, & tissue engineering. Respective higher demand is fueled by expanding clinical trial pipelines, escalating diagnostic complexity, & stringent FDA regulatory requirements for centralized, standardized data & safety surveillance.

The vaccines segment captured a notable share of 12.18% of the U.S. central lab market in 2025. Central lab services are fostering vaccines due to scalability, platform speed, storage stability, & the ability to induce targeted humoral or cellular immune responses. Many U.S. leaders are widely boosting the development of recombinant proteins & viral-vectored vaccines that have a long history of safe clinical use & stable immunogenicity.

The Pharmaceutical & Biotechnology Companies Segment Was Dominant in the Market in 2025

In 2025, the pharmaceutical & biotechnology companies segment registered dominance with a 62.83% share of the market. Dominance is driven by their large-scale involvement in drug discovery, development, & clinical trials, coupled with innovations in therapies, including biologics, gene therapies, & tailored medicine. In addition, surging R&D investments, expedited pipeline expansion, & reliance on centralized data further assist their significant market presence.

The contract research organizations (CROs) segment accounted for the second-largest share of 17.09% in 2025 & is predicted to witness rapid growth at a 9.62% CAGR. Upcoming progression is prominently driven by the rising outsourcing of clinical trial activities by pharmaceutical & biotechnology companies. Also, CROs are affordable, versatile, & efficient in managing complex studies, such as sample handling, data trials, demand for faster drug development timelines, & advanced trial management capabilities, which are further impelling their strong market growth.

The academic & government research institutes segment held an 11.01% share of the U.S. central lab market. These institutes are widely participating in clinical studies, translation research, & experiencing higher government-funded projects. Alongside, they are increasingly promoting disease understanding, biomarker discovery, & early-stage drug research, which necessitate advanced laboratory support.

The clinical diagnostic laboratories segment accounted for a 9.07% share in 2025, due to the rising geriatric population, growing burden of chronic diseases, & advancing clinical trial pipeline. Another driver is the surge in breakthroughs in precision medicine, & the rise in outsourcing of testing services is fueling continuous market progression. Growing cases of chronic illnesses are demanding that labs utilise robotic automation & digital pathology to maintain turnaround times low.

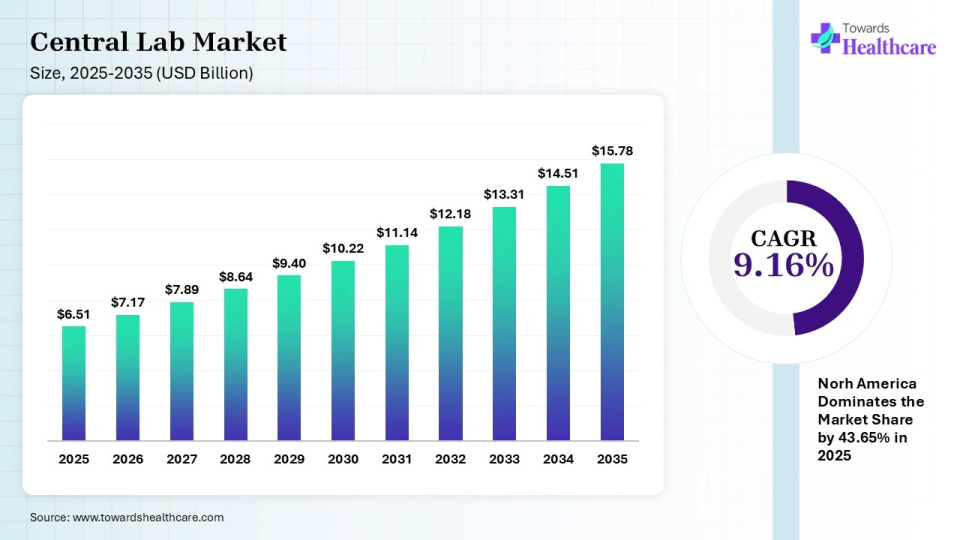

The global central lab market size is calculated at USD 6.51 billion in 2025 and is expected to be worth USD 15.78 billion by 2035, expanding at a CAGR of 9.16% from 2026 to 2035, as a result of rising investment in R&D and rising demand for clinical trials.

")

The Northeast remains a major hub for the U.S. central lab market, supported by dense pharmaceutical, biotechnology, and academic research clusters. States such as Massachusetts, New York, and Pennsylvania benefit from extensive clinical trial activity, advanced laboratory infrastructure, and strong collaborations between research institutions and life sciences companies, driving demand for centralized testing services.

The West region is witnessing significant expansion due to growing biotechnology innovation in California and neighboring states. Meanwhile, the South benefits from increasing clinical research investments, diverse patient populations, and expanding healthcare networks. The Midwest contributes through established healthcare systems, medical research centers, and rising participation in multicenter clinical trials requiring standardized laboratory support nationwide.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Thermo Fisher Scientific, Danaher (Beckman Coulter), Agilent Technologies | Supply laboratory instrumentation, analytical platforms, and diagnostic technologies used by central labs |

| Product Manufacturers | Thermo Fisher Scientific, Bio-Rad Laboratories, Agilent Technologies | Provide reagents, assay kits, consumables, and testing platforms |

| Central Lab Service Providers | Labcorp Central Laboratories, IQVIA Laboratories, ICON Central Laboratories, Medpace Reference Laboratories, Q² Solutions | Deliver clinical trial testing and sample analysis services |

| Platform Providers | IQVIA, Labcorp, Medidata Solutions | Clinical data integration, laboratory informatics, trial analytics platforms |

| CROs | IQVIA, ICON plc, Medpace Holdings, Parexel, Syneos Health | Integrate central laboratory services into broader clinical trial operations |

| Software Vendors | Medidata, Oracle Health Sciences, Veeva Systems | Laboratory information management, clinical data management, and trial workflow systems |

| Research Institutions | Mayo Clinic Laboratories, Cleveland Clinic Laboratories, Johns Hopkins Research Centers | Specialized testing, translational research, biomarker development |

| End-User Industries | Pharmaceuticals, Biotechnology, Medical Devices, Cell & Gene Therapy, Academic Research | Primary consumers of central laboratory services |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 68% | 22% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Labcorp Central Laboratories | Burlington, North Carolina, USA | USA | Largest dedicated central laboratory network supporting global clinical trials | Central lab testing, biomarker services, genomics, companion diagnostics |

| IQVIA Laboratories | Durham, North Carolina, USA | USA | Global clinical trial and laboratory leader with extensive sponsor relationships | Central lab services, biomarker testing, specialty assays |

| Q² Solutions | Morrisville, North Carolina, USA | USA | Major central laboratory provider focused on biomarker and translational medicine | Biomarker testing, genomics, esoteric testing |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Parexel International | Durham, North Carolina, USA | USA | Clinical trial leader offering integrated laboratory partnerships and services | Clinical trial laboratory solutions |

| Syneos Health | Morrisville, North Carolina, USA | USA | Provides laboratory-enabled clinical development solutions | Biomarker and laboratory-supported trials |

| Frontage Laboratories | Exton, Pennsylvania, USA | USA | Specialized laboratory and bioanalytical service provider | Central lab testing, bioanalysis |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Precision for Medicine | Bethesda, Maryland, USA | USA | Strong growth in precision medicine and biomarker-driven trials | Biomarker testing, translational medicine |

| Celerion | Lincoln, Nebraska, USA | USA | Specialized early-phase clinical research laboratory provider | Bioanalytical and central laboratory services |

| BioAgilytix | Durham, North Carolina, USA | USA | Leading bioanalytical and immunogenicity testing specialist | Biomarker and bioanalytical services |

Strengths

Weaknesses

Opportunities

Threats

By Service Type

By Therapeutic Area

By Phase

By End User

By Test Type

By Technology

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar