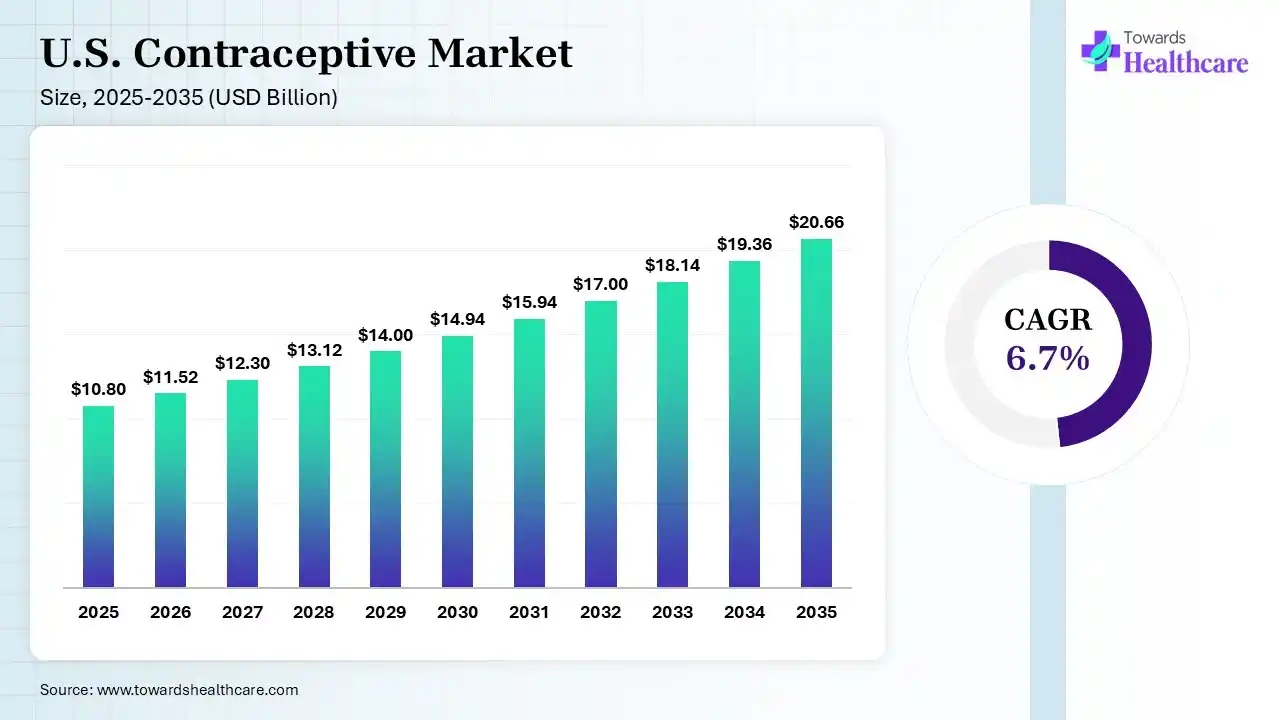

The U.S. contraceptive market size was estimated at USD 10.8 billion in 2025 and is predicted to increase from USD 11.52 billion in 2026 to approximately USD 20.66 billion by 2035, expanding at a CAGR of 6.7% from 2026 to 2035. The U.S. contraceptive market is growing due to its support for individuals to avoid unwanted pregnancies and plan births, which lowers pregnancy-related health challenges, specifically for adolescent girls.

")

The U.S. contraceptive market is growing, as efficient contraception advantages both mothers and children through lessening morbidity and mortality, enhancing the social and economic status of women, and improving the relationship of the mother with her offspring. The United States has rates of unintentional pregnancy and abortion more approaching those of an emerging country than those of other industrialized nations. In the U.S., couples, 40% select male or female sterilization as their technique of contraception. Novel contraceptive methods probably to become available in the US soon will increase the number of efficient, reversible contraceptive choices for US couples. Increasing access to a wide variety of methods will increase contraceptive applications.

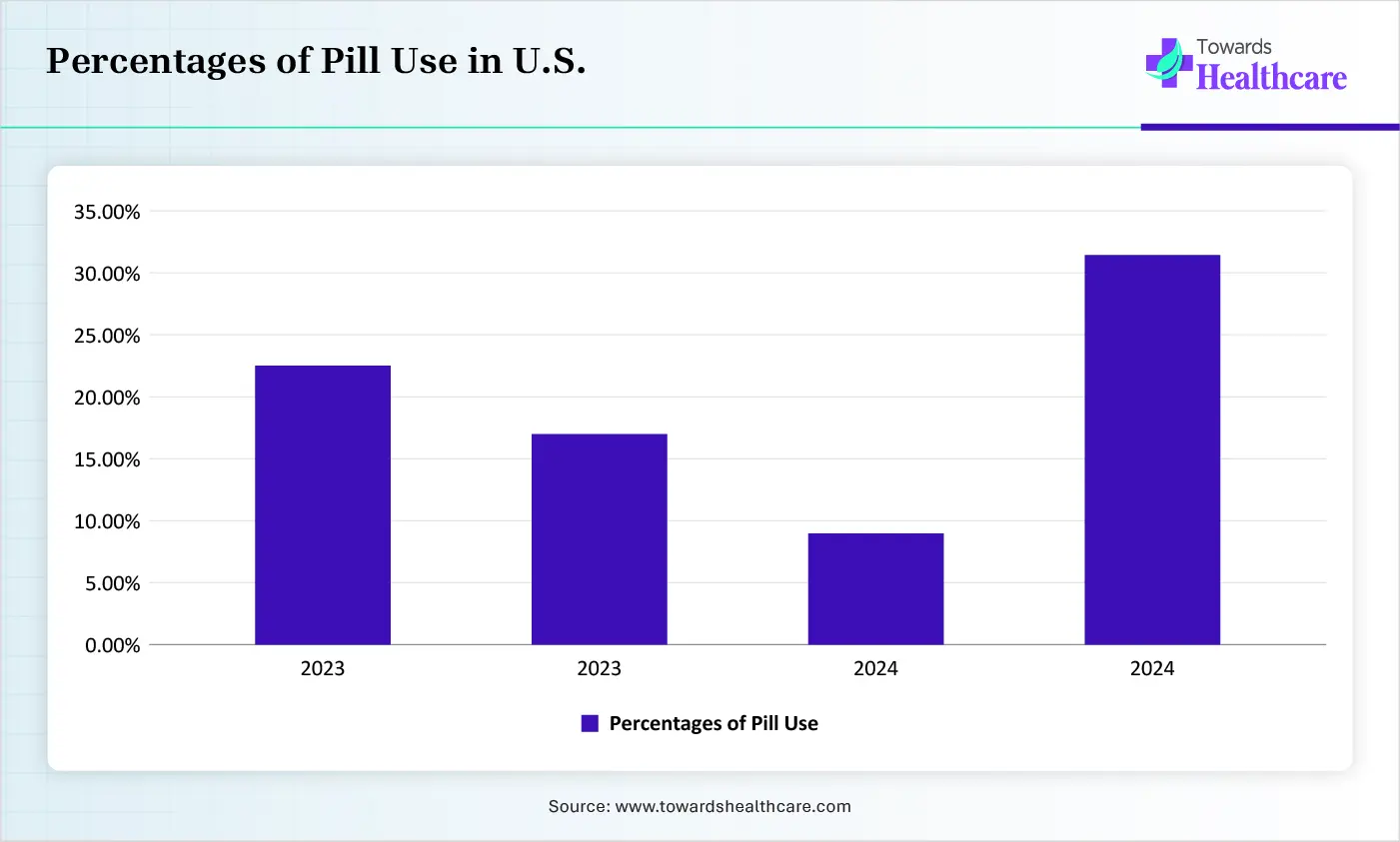

| Age Group | Percentages of Pill Use |

| 15-24 | 22.4% |

| 25 -34 | 16.9% |

| 35-44 | 8.7% |

| Older | 31% |

AI-based technology integrated into sexual reproductive health, involving enhancing care, offering high-quality contraception and infertility solutions, removing unsafe abortions, and allowing the prevention and treatment of sexually transmitted infections. AI-based technology analyzes to understand trends in sexual behavior, contraceptive use, and attitudes toward reproductive health. Government spending in AI-based initiatives, through collaboration of public-private organizations and intended funding streams, improves sustainability and encourages broad adoption.

Growth of Non-Hormonal Options:

Non-hormonal contraceptives are technologies that prevent pregnancy without intervening in the body’s hormonal cycle. Because they do not contain synthetic hormones like progestin or estrogen, they are used in women who cannot use hormonal contraceptives due to health reasons.

Rise in Male Contraception R&D:

The advancement of male contraception has been massively researched over the past few years. Different hormonal and non-hormonal technologies are being developed to offer better contraception with negligible or no disadvantages.

Dual-Protection Focus on Contraception:

A dual contraceptive technology is the utilization of any modern contraceptive technology along with male or female condoms, which decreases sexually transmitted diseases (STDs) and unwanted pregnancy.

| Table | Scope |

| Market Size in 2026 | USD 11.52 Billion |

| Projected Market Size in 2035 | USD 20.66 Billion |

| CAGR (2026 - 2035) | 6.7% |

| Key Applications | Family planning, birth control, reproductive health management, hormone regulation, long-acting reversible contraception (LARC) |

| Primary End Users | Women of reproductive age, healthcare providers, hospitals, gynecology clinics, retail pharmacies, online pharmacies, public health programs |

| Key Growth Drivers | Increased contraceptive awareness, OTC product availability, growth of LARC adoption, expanded insurance coverage, telehealth expansion |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Gender, By Age Group, By Distribution Channel |

| Top Key Players | Agile Therapeutics, Inc., Piramal Healthcare & Sun Pharma, HRA Pharma, Bayer AG, Pfizer Inc. |

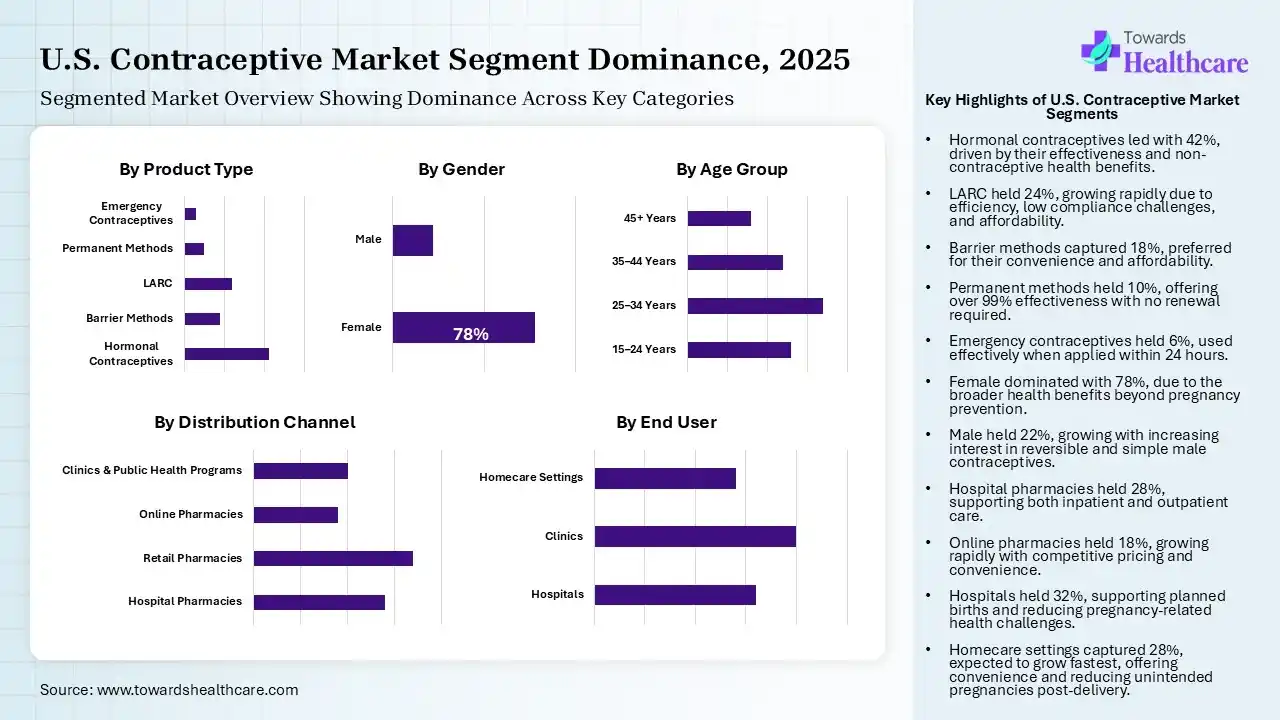

Hormonal Contraceptives Segment Led the U.S. Contraceptive Market in 2025

| Segment | Share 2025 (%) |

| Hormonal Contraceptives | 42% |

| Barrier Methods | 18% |

| LARC | 24% |

| Permanent Methods | 10% |

| Emergency Contraceptives | 6% |

The hormonal contraceptives segment contributed the largest market share of 42% in 2025, as hormonal contraceptives are efficient in preventing pregnancy; they contain a progestin, which inhibits ovulation. Hormonal contraceptives have been shown to offer different noncontraceptive advantages. Hormonal contraceptives reduce the risks of endometrial cancer, colorectal cancer, ovarian cancer, and osteoporosis.

The LARC segment held the second-largest share of 24% of the market in 2025 and is expected to grow at the fastest CAGR of 8.40% during the forecast period, as LARC offers an efficient process of contraception with lower compliance challenges by the consumer and prevents unwanted pregnancies and their challenges. These technologies are the most active modern contraceptive processes for preventing unintended pregnancy. They are long-acting, reliable, safe, and affordable.

Whereas the barrier methods segment held a notable share of 18% in the U.S. contraceptive market in 2025, as barrier contraception stops pregnancy by stopping the male's sperm from coming into contact with the female's ovum. Barrier contraceptives are affordable and convenient. Many women use them to avoid health challenges related to hormonal contraceptives.

The permanent methods segment held a notable share of 10% of the market in 2025, as permanent processes are more than 99% efficient at preventing pregnancy. Unlike short-term or long-acting processes, they never need to be renewed or replaced. Permanent contraception includes a surgical procedure that reliably prevents future pregnancies.

The emergency contraceptives segment held a notable share of 6% of the market in 2025, as emergency contraception is efficient when applied early, with only 3% of women becoming pregnant if used within 24 hours of unprotected sexual intercourse. Emergency contraception (EC) prevents up to over 95% of pregnancies when taken within 5 days after intercourse.

Female Segment Led the U.S. Contraceptive Market in 2025

| Segment | Share 2025 (%) |

| Female | 78% |

| Male | 22% |

The female segment contributed the largest market share of 78% in 2025, as female contraceptives provide significant benefits beyond pregnancy prevention, including highly efficient family planning, regulation of menstrual cycles, lower menstrual pain (dysmenorrhea), and reduced symptoms of PMS/PMDD.

The male segment held the second largest share of 22% of the U.S. contraceptive market in 2025 and is estimated to achieve 7.50% CAGR during 2026-2035, as male contraceptives lower the number of ejaculated fertile sperm inflowing the vagina to levels that reliably prevent fertilization. They have the strength to be simple to apply and reversible. Testosterone functions as a male contraceptive by suppressing the secretion of LH and FSH from the pituitary through negative feedback.

The Retail Pharmacies Segment held the Largest Share in the Market in 2025

| Segment | Share 2025 (%) |

| Hospital Pharmacies | 28% |

| Retail Pharmacies | 34% |

| Online Pharmacies | 18% |

| Clinics & Public Health Programs | 20% |

The retail pharmacies segment contributed the largest market share of 34% in 2025, as retail pharmacies play an important role in medical providers by offering convenient access to medications, a broad range of products, and significant additional solutions. Retail pharmacies are a significant part of medical care systems and, in major countries, are responsible for dispensing a huge proportion of medical care products.

The hospital pharmacies segment held the second largest share of 28% of the U.S. contraceptive market in 2025, as hospital pharmacies supply drugs to other entities performing medical actions, inpatient facilities offering 24-hour medical services, or outpatient health solutions.

The clinics & public health programs segment held a notable share of 20% of the market in 2025, as the family planning (KB) program aims to enhance the welfare of a family by limiting the birth rate or number of children born. These programs not only avert unintended pregnancies, lowering maternal and infant mortality rates, but also offer significant, comprehensive care.

The online pharmacies segment held a notable share of 18% of the market in 2025 and is expected to be the fastest-growing segment with 9.10% CAGR, as online pharmacies often provide competitive pricing, discounts, and generic substitutes, leading to potential price savings for patients. This affordability is predominantly relevant for those with chronic conditions who need long-term medicine.

The Clinics Segment held the Largest Share of the Market in 2025

| Segment | Share 2025 (%) |

| Hospitals | 32% |

| Clinics | 40% |

| Homecare Settings | 28% |

The clinics segment contributed the largest market share of 40% in 2025, as enhanced contraceptive use, lowered unintended pregnancies, better birth spacing, increased prenatal care, lowered incidence of preterm and low-birthweight offspring, increased breastfeeding, increased HPV vaccinations, and cervical tumor screenings.

The hospitals segment held the second-largest share of 32% of the U.S. contraceptive market in 2025. It supports patients in avoiding unintended pregnancies and planned births, and it lowers pregnancy-related health challenges, specifically for adolescent girls. Efficient contraception advantages both mothers and children by lowering morbidity and mortality, enhancing the social and economic status of women.

Whereas the homecare settings segment held a notable share of 28% in the market in 2025 and is estimated to grow at the highest CAGR of 7.80% during the upcoming period, as this type of care increases the effectiveness of contraceptive use, which could lower the incidence of unintended pregnancies, and if provided after delivery, could decrease short-interval unintended pregnancy. Home visits remove the requirement for transport to clinics, decreasing both the expenses and time challenges.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Bayer, CooperSurgical, Organon | Development of hormonal and non-hormonal contraceptive technologies |

| Product Manufacturers | Bayer, Organon, Pfizer, Viatris, Teva, Mayne Pharma | Manufacturing contraceptive drugs and devices |

| Service Providers | Planned Parenthood, CVS Health, Walgreens | Product dispensing, counseling, family planning services |

| Platform Providers | Nurx, Pandia Health, Twentyeight Health | Telehealth-enabled contraceptive access |

| CROs/CDMOs | Catalent, Thermo Fisher Patheon, Recipharm | Development and manufacturing support |

| Software Vendors | Epic Systems, Oracle Health | Electronic health record integration for reproductive healthcare |

| Research Institutions | National Institutes of Health, Guttmacher Institute, Population Council | Clinical research and contraceptive innovation |

| End-User Industries | Hospitals, Clinics, Pharmacies, Public Health Agencies | Product utilization and distribution |

R&D:

Manufacturing Processes:

Patient Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 68% | 23% | 9% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Bayer AG | Leverkusen, North Rhine-Westphalia | Germany | Dominates U.S. IUD segment and hormonal contraception market | Mirena, Kyleena, Skyla |

| Organon & Co. | Jersey City, New Jersey | United States | Major women's health portfolio with strong contraceptive revenues | Nexplanon, NuvaRing |

| CooperSurgical | Trumbull, Connecticut | United States | Leading non-hormonal IUD supplier | Paragard IUD |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Pfizer Inc. | New York, New York | United States | Strong injectable contraceptive presence | Depo-Provera |

| Viatris Inc. | Canonsburg, Pennsylvania | United States | Major generic contraceptive supplier | Xulane patch, oral contraceptives |

| Teva Pharmaceutical Industries Ltd. | Tel Aviv | Israel | Extensive generic contraceptive portfolio | Generic oral contraceptives |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Evofem Biosciences | San Diego, California | United States | Innovative non-hormonal contraception developer | Phexxi |

| Agile Therapeutics | Princeton, New Jersey | United States | Specialized contraceptive patch innovator | Twirla |

| Afaxys, Inc. | Charleston, South Carolina | United States | Women's health and contraceptive distribution specialist | Oral contraceptive portfolio |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Gender

By Age Group

By Distribution Channel

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar