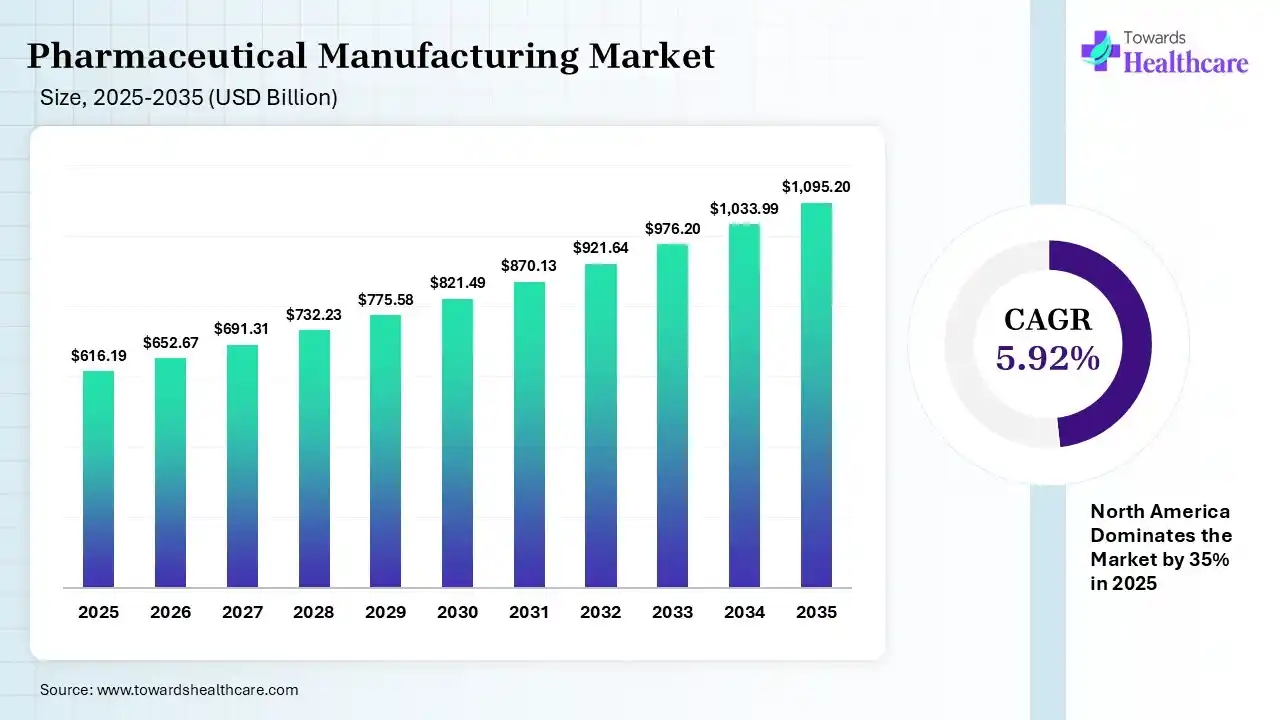

The global pharmaceutical manufacturing market size was estimated at USD 616.19 billion in 2025 and is predicted to increase from USD 652.67 billion in 2026 to approximately USD 1095.2 billion by 2035, expanding at a CAGR of 5.92% from 2026 to 2035.

A pivotal growth in chronic disease cases, demand for advanced therapies, biologics, and personalised medicines is driving the global market progression. Additionally, the leading firms are exploring the use of AI, machine learning, 3D printing & other advanced technologies in manufacturing processes.

")

The global pharmaceutical manufacturing market refers to the robust industrial-scale production of medicinal drugs, which follows the formulation, processing, & packaging of active pharmaceutical ingredients (APIs) into finished dosage forms, including tablets or injections. This covers ensuring drug safety, efficacy, & quality compliance with Good Manufacturing Practices (GMP). The entire growth of the market is propelled by the surging chronic disease instances, raised R&D, outsourcing to CMOs/CDMOs, & investments in AI & continuous manufacturing.

Primarily, AI algorithms are playing a vital role in the process improvement & control by analyzing process data to find optimal parameters for the prospective drug production, lowering waste & development time. Moreover, the use of deep learning supports image recognition, detection of flaws, & maintain persistent quality in real-time. However, AI also projects market demands, handles inventory, and enhances logistics to eliminate the lack of raw materials.

Encouraging Digitalization & AI

Numerous manufacturers are employing AI for predictive maintenance, quality control, & optimization, whereas digital twins are highly used to simulate production lines and minimise risks.

Raising Outsourcing to CDMOs

Gradually, firms are fostering Contract Development and Manufacturing Organizations (CDMOs) for specialized technology, with boosted capacity and minimal expenditure.

Looking for 3D Printing Approach

An eventual research will pose 3D printing technology, which allows tailored medicine with patient-specific dosage forms, ideal release profiles, & point-of-care manufacturing.

| Table | Scope |

| Market Size in 2026 | USD 652.67 Million |

| Projected Market Size in 2035 | USD 1095.2 Million |

| CAGR (2026 - 2035) | 5.92% |

| Leading Region | North America by 35% |

| Key Applications | Prescription drugs, OTC medicines, biologics, vaccines, specialty pharmaceuticals, cell & gene therapies |

| Primary End Users | Pharmaceutical companies, biotechnology firms, hospitals, government healthcare agencies, distributors |

| Key Growth Drivers | Rising global drug demand, biologics expansion, outsourcing to CDMOs, aging populations, chronic disease prevalence, advanced manufacturing technologies |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Manufacturing Type, By Formulation, By Therapeutic Area, By Scale of Operation, By End User, By Region |

| Top Key Players | Pfizer, Johnson & Johnson, AbbVie, Merck & Co., Roche, AstraZeneca, Novartis, Bristol Myers Squibb, GSK, Sanofi |

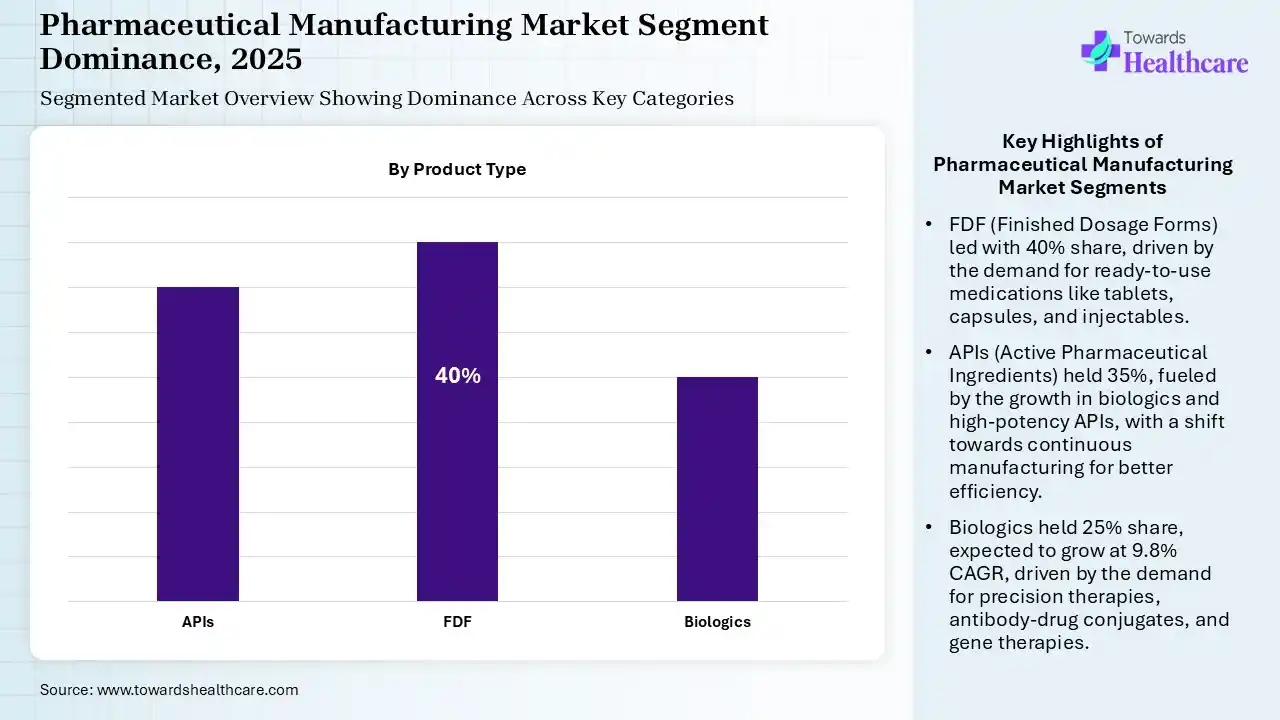

The FDF Segment Led the Market in 2025

| Segment | Share 2025 (%) |

| APIs | 35% |

| FDF | 40% |

| Biologics | 25% |

In 2025, the FDF segment dominated with 40% share of the pharmaceutical manufacturing market. This covers the production of ready-to-use medications, i.e., tablets, capsules, and injectables, to meet accelerating chronic disease cases & generic drug demand. Also, the globe is stepping towards the development of pre-designed, modular pharmaceutical FDF plants and the broader adoption of single-use disposable systems in biologics filling.

However, the APIs segment held the second-largest share of 35% of the market in 2025. Globally rising growth in biologics and high-potency APIs, investments in CDMOs for supply chain resilience, drive the demand for APIs. For this, companies are implementing continuous manufacturing as a mainstream, with superior efficiency, minimal waste, & constant quality.

Whereas the biologics segment held 25% share in 2025 & it is predicted to expand at a 9.8% CAGR. A huge burden of cancer, autoimmune disorders, and rare disease cases is fueling the demand for specialized, targeted biologics, especially precision therapies. The market is moving its focus towards the production of antibody-drug conjugates (ADCs), bispecific antibodies, & cell/gene therapies.

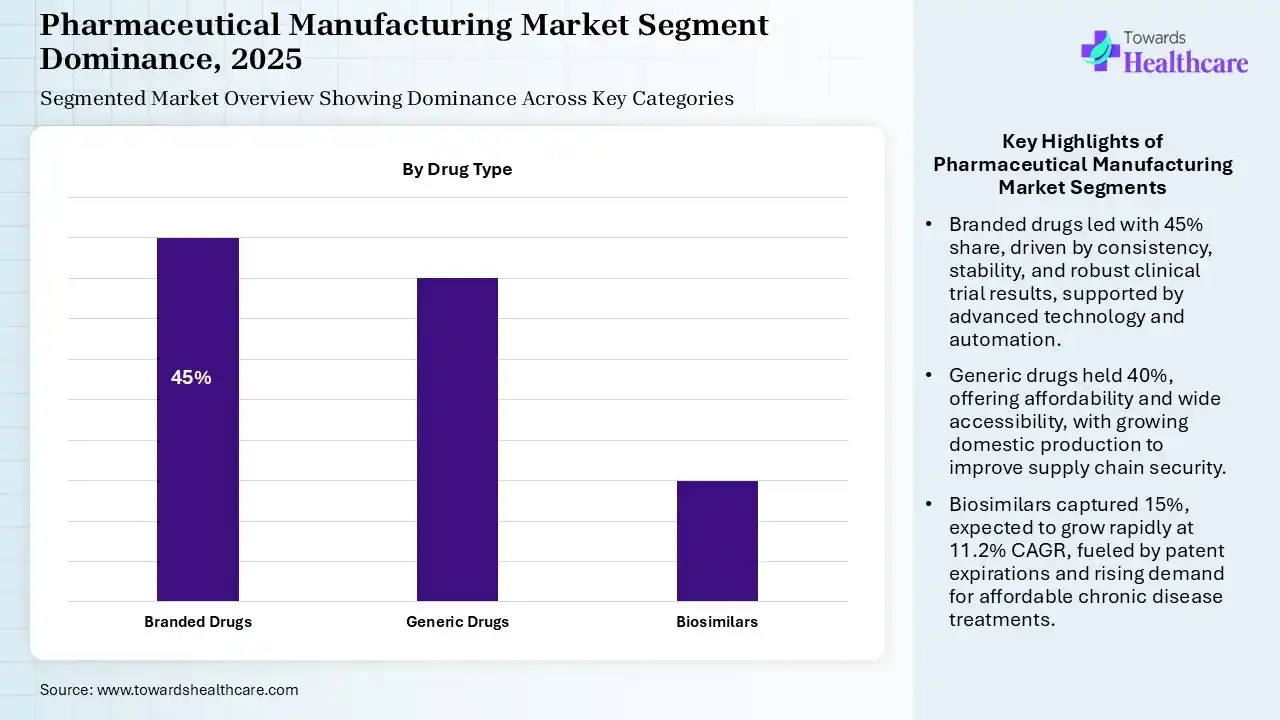

The Branded Drugs Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Branded Drugs | 45% |

| Generic Drugs | 40% |

| Biosimilars | 15% |

The branded drugs segment captured a 45% share of the pharmaceutical manufacturing market in 2025. The adoption of these drugs is driven by their consistency in appearance, stability for narrow therapeutic index (NTI) drugs, avoidance of specific allergens, and robust clinical trial results. Players strengthen the use of advanced technology & automated processes to perceive identical, high-quality batches.

The generic drugs segment held 40% share of the market, due to its affordability and wider accessibility. Nowadays, governments are fostering domestic production, like India's Bulk Drug Parks, to lower reliance on imported ingredients & improve supply chain security. A little step is moving towards complex formulations, advanced drug delivery systems, like nano-carriers, inhalers.

On the other hand, the biosimilars segment captured 15% & is estimated to expand rapidly at 11.2% CAGR in the coming era. Catalysts are patent expirations of key biologics, surging demand for inexpensive chronic disease treatments, & favourable regulatory roadmaps. A focus on bolstering production efficiency through high-density perfusion systems is impacting the overall growth.

The In-House Manufacturing Segment was dominant in the Market in 2025

| Segment | Share 2025 (%) |

| In-house Manufacturing | 55% |

| Contract Manufacturing | 45% |

In 2025, the in-house manufacturing segment held a major share of 55% of the pharmaceutical manufacturing market. Its dominance is driven by robust protection of proprietary manufacturing processes and confidential formulas, especially for complex molecules, novel drug launches, & blockbusters. Also, broadening investments in in-house, specialized capabilities, like the addition of formulation development services at CDMOs.

The contract manufacturing segment held 45% share in 2025 & is anticipated to witness the fastest expansion at 8.9% CAGR. The growing demand for biologics, gene therapies, and sterile injectables is fueling the need for the use of specialized staff of CDMOs. Many pharma companies of this era are widely exploring long-term partnerships with CDMOs to facilitate comprehensive services, like development, packaging, & regulatory support.

The Oncology Segment Led the Market in 2025

| Segment | Share 2025 (%) |

| Oncology | 30% |

| Cardiovascular | 20% |

| Infectious Diseases | 15% |

| Neurology | 12% |

| Immunology | 13% |

| Others | 10% |

The oncology segment captured 30% share of the pharmaceutical manufacturing market in 2025 & is estimated to expand at 10.5% CAGR during the forecast period. The notable growth in the geriatric population & changes in lifestyle lead to the massive cases of cancers, which are driving the need for advanced therapies. Firms are aiming at specialised isolators & Restricted Access Barrier Systems (RABS) to manage toxic compounds safely & lower worker exposure.

The cardiovascular segment held the second-largest share of 20% in 2025. Accelerating cases of heart attacks, strokes, and hypertension, demanding drugs like anticoagulants and lipid-lowering drugs. Companies are working on RNA therapies, like siRNA & antisense mRNA, to treat cardiac diseases.

The infectious diseases segment captured 15% share of the pharmaceutical manufacturing market. Drivers are escalating instances of HIV, hepatitis, tuberculosis, and influenza, with transformations in mRNA-LNP formulations, which enable faster adaptation to newer variants & other infectious diseases.

The neurology segment held 12% revenue share of the market in 2025. The globe is gradually experiencing a major rise in neurodegenerative and seizure-related disorders, like Alzheimer's, Parkinson’s, multiple sclerosis (MS), & epilepsy. The trend, focusing on LNP vehicles & ultrasound technologies, is to boost drug delivery efficacy into the brain.

The immunology segment captured 13% share of the market, due to the substantial growth in the prevalence of rheumatoid arthritis, psoriasis, & Crohn's disease. Diverse pharma firms are emphasizing multi-specific antibodies, i.e., bispecifics/trispecifics that bind to multiple targets, & raises efficiency for refractory patients.

The Pharmaceutical Companies Segment Dominated the Market in 2025.

| Segment | Share 2025 (%) |

| Pharmaceutical Companies | 60% |

| Biotechnology Companies | 30% |

| Research Institutes | 10% |

The pharmaceutical companies segment held the largest share of 60% of the market in 2025. Globally surging demand for advanced medications, precision treatments, and progressing outsourcing to CDMOs are fueling the growth of these companies. They are actively fostering continuous manufacturing, modular systems, & 3D printing for drug products.

The biotechnology companies segment captured 30% share of the pharmaceutical manufacturing market in 2025 & is predicted to expand at 9.2% CAGR. They are increasingly putting efforts into the development of novel monoclonal antibodies and vaccines for the oncology area. Moreover, specialized, small-scale, & automated manufacturing setups are bolstered by highlighting the complexities of tailored medicine.

The research institutes segment held 10% revenue share in 2025. Robust public institutions, including CSIR-IICT and NCL, with specialized Contract Research and Manufacturing Services (CRAMS), are fostering novelty in the pharma industry. These institutions are highly using AI & machine learning to improve molecular design, estimate drug-excipient interactions, & lower the time from lab to market.

")

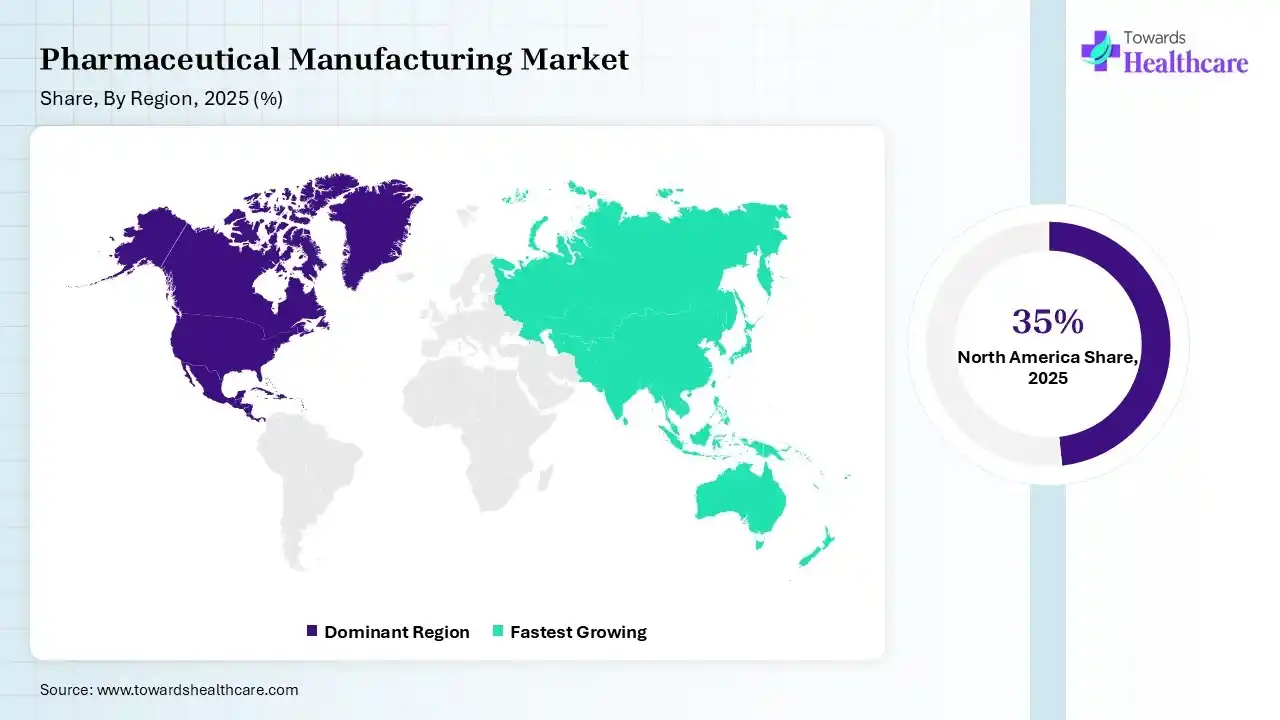

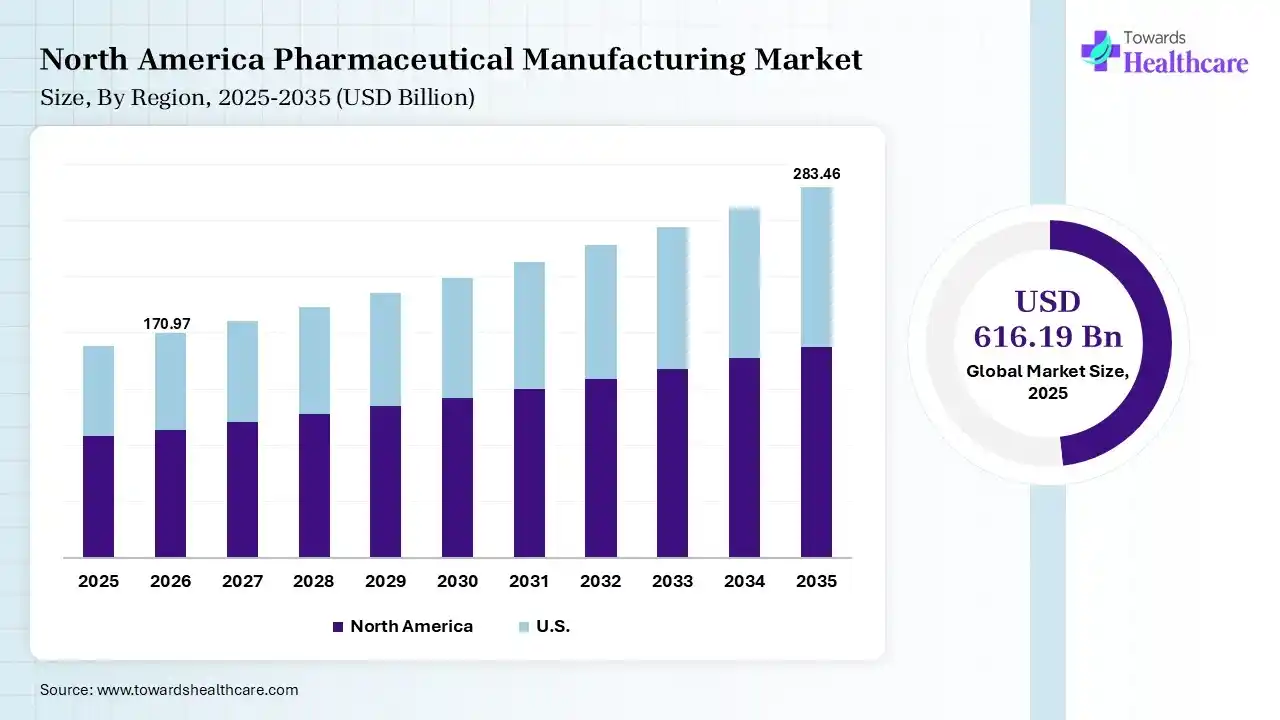

North America led with 35% share of the pharmaceutical manufacturing market, due to the presence of well-developed infrastructure and R&D investment. Also, the FDA is speeding up approvals for new drugs, which ultimately enhances the need for manufacturing capacity.

For instance,

U.S. Market Trends

Whereas, the U.S. market was a major contributor, as it focused on integration of AI-driven predictive modeling for quality management & autonomous robotics. Alongside, the FDA initiated the PreCheck program to accelerate the construction of production locations & lower regulatory obstacles for local manufacturing.

Asia Pacific held 25% of the market share in 2025 and is predicted to witness rapid expansion at 9.3% CAGR in the pharmaceutical manufacturing market. The region is highly promoting outsourcing production to India & China, with minimal spending, improved supply chain & the use of sophisticated manufacturing facilities. APAC is a center for generic drugs, which is fueled by the rising approvals of abbreviated new drug applications (ANDAs) & raised demand for affordable drugs.

China Market Trends

Many Chinese Laboratories are key firms in Antibody Drug Conjugates (ADCs), primarily in oncology. Subsequently, they are extensively focusing on synthetic drug manufacturing & traditional Chinese medicine, coupled with biotech-related medical products & sophisticated equipment.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Siemens, Emerson Electric, Rockwell Automation | Manufacturing automation, process control, digitalization |

| Product Manufacturers | Pfizer, Roche, Novartis | Drug development and commercial manufacturing |

| Service Providers | Thermo Fisher Scientific, Catalent | Manufacturing, packaging, analytical testing |

| Platform Providers | SAP, Dassault Systèmes | ERP, digital manufacturing, quality systems |

| CROs/CDMOs | Lonza, WuXi AppTec, Samsung Biologics | Contract development and manufacturing |

| Software Vendors | Veeva Systems, MasterControl | Quality, compliance, manufacturing execution |

| Research Institutions | National Institutes of Health, Fraunhofer Society | Manufacturing innovation and translational research |

| End-User Industries | Pharma, Biotechnology, Vaccines, Generics, Specialty Medicines | Commercial utilization of manufacturing capabilities |

R&D

Formulation and Final Dosage Preparation

Patient Support & Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 58% | 27% | 15% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Pfizer Inc. | New York, New York | USA | One of the world's largest pharmaceutical manufacturing networks | Branded pharmaceuticals, vaccines, sterile manufacturing |

| Roche Holding AG | Basel | Switzerland | Global leader in biologics and specialty pharmaceutical production | Oncology drugs, biologics, diagnostics manufacturing |

| Novartis AG | Basel | Switzerland | Large-scale innovative drug manufacturing operations | Innovative medicines, biologics, radiopharmaceuticals |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| AstraZeneca PLC | Cambridge, England | United Kingdom | Significant global manufacturing footprint | Oncology, respiratory, cardiovascular medicines |

| Eli Lilly and Company | Indianapolis, Indiana | USA | Major investment in pharmaceutical production expansion | Diabetes, obesity, oncology therapies |

| Sanofi S.A. | Paris | France | Large vaccine and pharmaceutical manufacturing network | Vaccines, specialty care medicines |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Samsung Biologics | Incheon | South Korea | World's leading biologics manufacturing specialist | Biologics contract manufacturing |

| Lonza Group AG | Basel | Switzerland | Premier CDMO serving global pharma companies | Drug substance and biologics manufacturing |

| Catalent, Inc. | Somerset, New Jersey | USA | Leading outsourced pharmaceutical manufacturing provider | Drug delivery and manufacturing services |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Drug Type

By Manufacturing Type

By Formulation

By Therapeutic Area

By Scale of Operation

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar