")

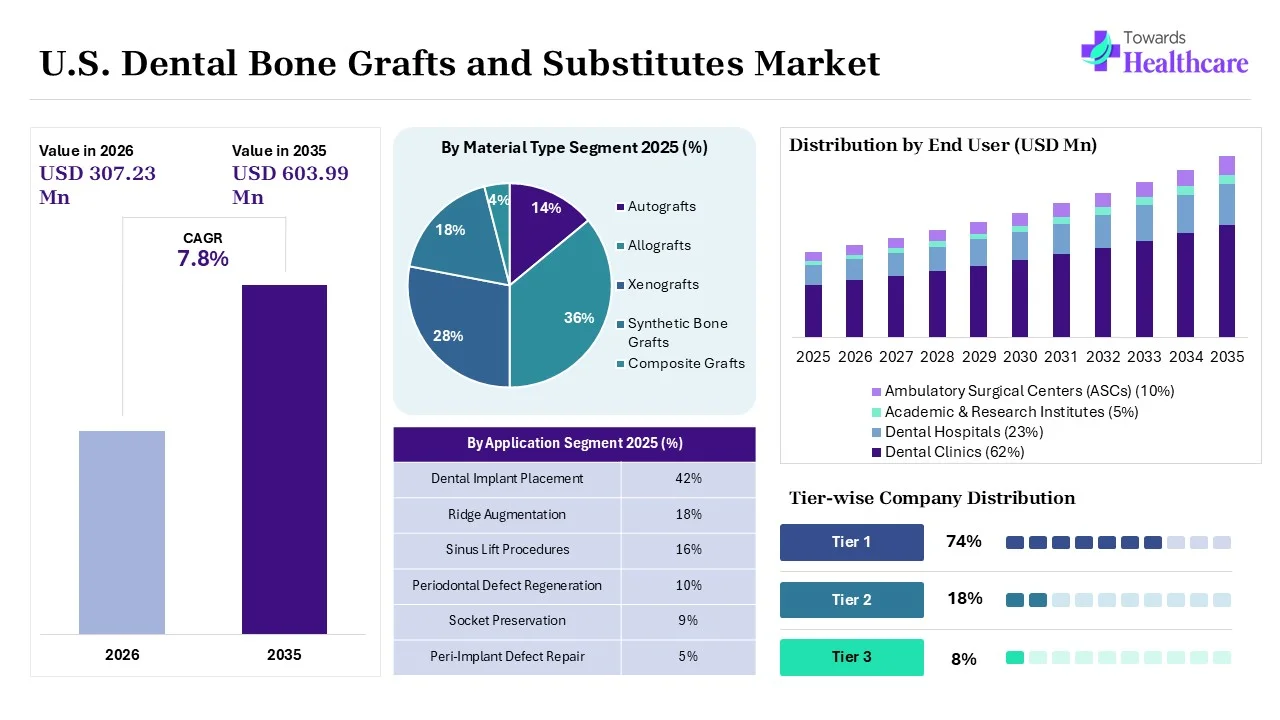

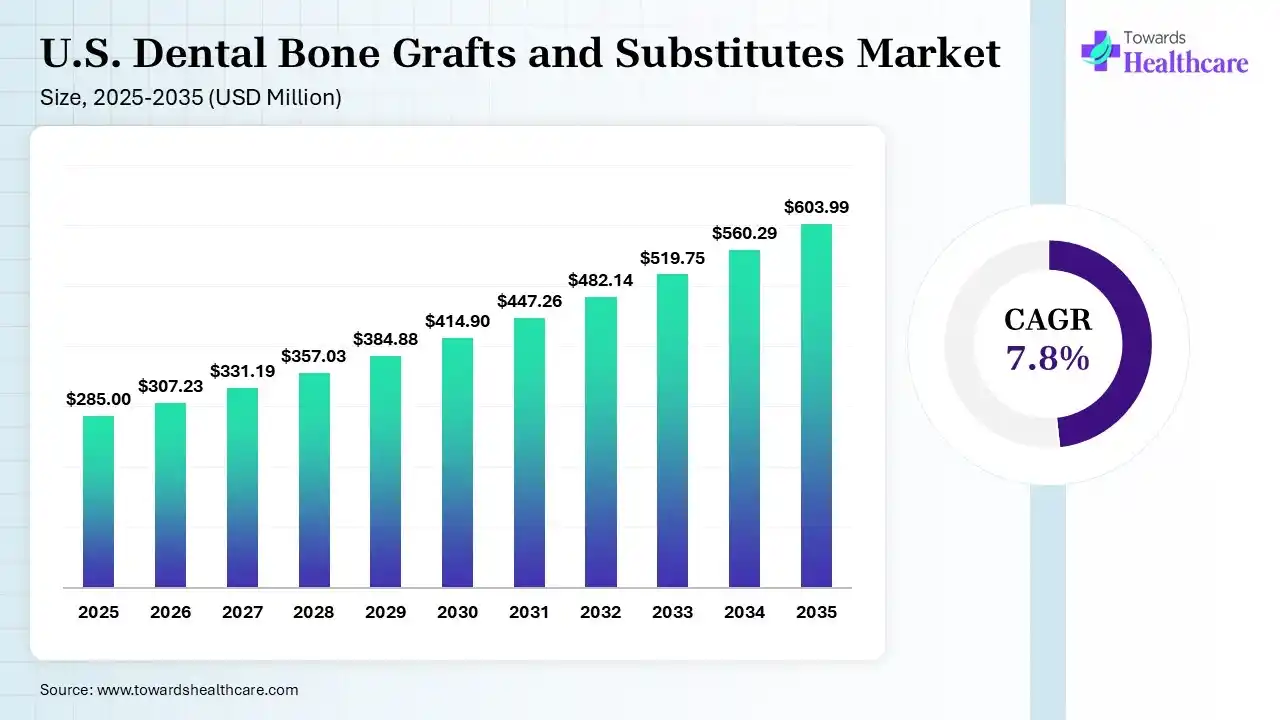

The U.S. dental bone grafts and substitutes market size was estimated at USD 285 million in 2025 and is predicted to increase from USD 307.23 million in 2026 to approximately USD 603.99 million by 2035, expanding at a CAGR of 7.8% from 2026 to 2035. A rise in dental problems across the U.S. is increasing the demand for dental bone grafts and substitutes. Additionally, increasing oral health awareness, expanding dental clinics, and technological advancements are also enhancing the market growth.

")

The U.S. dental bone grafts and substitutes market is driven by a surge in dental implant procedures and an increasing geriatric population. The U.S. dental bone grafts and substitutes encompass materials used to regenerate, increase, and restore bone volume in the jaw during oral surgery across the U.S. These are natural or synthetic materials promoting new bone formation, improving implant stability, reducing bone loss, and restoring jawbone structure and function. The U.S. is also experiencing a rise in geriatric population, jawbone deterioration, and tooth loss, due to the growing prevalence of dental caries and periodontal diseases.

This, in turn, is increasing the demand for dental bone grafts and substitutes across the U.S. The common types of bone grafts and substitutes used are calcium phosphate ceramics, bioactive glass, collagen-based matrices, calcium sulphate, demineralized bone matrix, and growth factor-enhanced grafts. This drives their use for dental implant site preparation, sinus lift procedures, ridge augmentation and reconstruction, socket preservation, and periodontal bone defect repair. At the same time, with the growing adoption of dental implants, a shift towards cosmetic dentistry, increasing oral health awareness, rising demand for minimally invasive techniques, increasing healthcare expenditure, and expanding medical tourism are also propelling the market growth.

The U.S. market features intense competition driven by a few dominant medical device giants and agile biotechnology firms. Major global players like Zimmer Biomet, Envista, and Geistlich lead the industry. These large corporations secure the highest market share by offering complete product lines, bundling bone grafts with dental implants, and maintaining massive sales networks across American clinics. Meanwhile, smaller companies compete by launching advanced synthetic materials and specialized tissue matrices. They win customers by offering lower prices or unique biological features that heal wounds faster. This combination of powerful corporate giants and innovative niche suppliers forces continuous product upgrades, keeping prices high but giving US oral surgeons a massive variety of tools.

AI offers a wide range of applications in the U.S. dental bone grafts and substitutes market, where it helps in the analysis of dental images and detection of bone defects, promoting appropriate treatment planning. It also helps in the identification of optimal graft volume and offers 3D and customized surgical guidance, where its predictive analytics help in predicting healing and success rates. AI is also used in personalized graft selection, post-operative monitoring, the generation of treatment simulations, and workflow automation.

Dental Implant Procedures on the Rise

Increasing cases of tooth loss in the U.S. are promoting the use of dental implants, which is driving the demand for dental bone grafts and substitutes to maintain adequate bone volume. Similarly, increasing periodontal disease is also increasing the use of proper implant placements. Additionally, growing awareness about the durability and functional benefits of dental implants is also driving their continued demand, which in turn is increasing the adoption of various dental bone grafts and substitutes.

Flourishing Regenerative Dentistry

The growing shift towards tissue regeneration and biological healing is increasing the shift towards regenerative therapies for new bone formation. This, in turn, is increasing the adoption of growth factors, stem cells, platelet-rich plasma, platelet-rich fibrin, and other tissue-engineered biomaterials to offer enhanced regenerative outcomes. Furthermore, their faster healing and improved implant success rates are also driving the development of next-generation bone grafts and substitutes with enhanced regenerative capabilities.

Expanding Customized and 3D Printed Bone Grafts

A rise in the health awareness rate is increasing the demand for customized bone grafts, where the advancements in 3D printing technologies are also driving the development of patient-specific grafts across the U.S. Additionally, the growing integration of 3D printing technologies with other imaging systems is also promoting the development of customized grafts with improved fit, stability, and healing outcomes. They are also preferred in complex oral procedures, where their accessibility and affordability also encourage their use.

| Table | Scope |

| Market Size in 2026 | USD 307.23 Million |

| Projected Market Size in 2035 | USD 603.99 Million |

| CAGR (2026 - 2035) | 7.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Material Type, By Product Form, By Application, By End User, By Distribution Channel |

| Top Key Players | ZimVie Inc., LifeNet Health, Dentsply Sirona Inc., Medtronic plc, BioHorizons, Collagen Matrix, Inc., Geistlich Pharma North America |

")

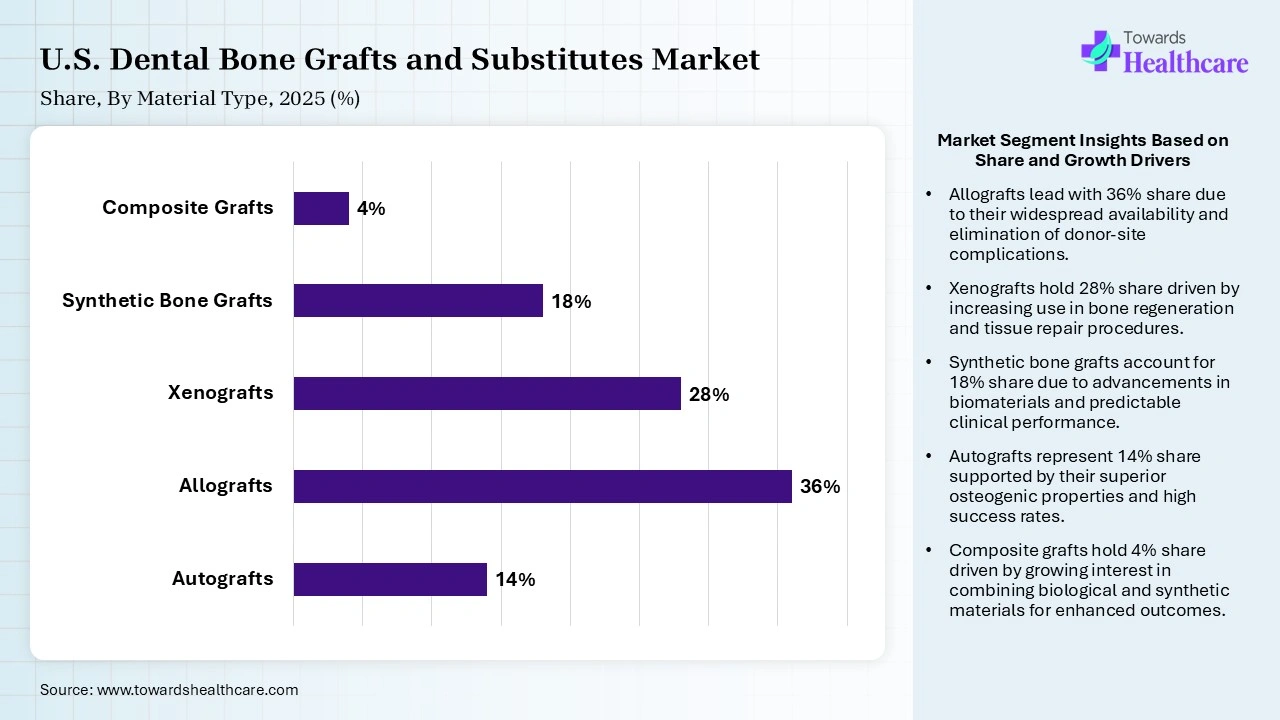

| Segment | Share 2025 (%) |

| Autografts | 14% |

| Allografts | 36% |

| Xenografts | 28% |

| Synthetic Bone Grafts | 18% |

| Composite Grafts | 4% |

The Allografts Segment Dominated the Market With 36% in 2025

The allografts segment led the U.S. dental bone grafts and substitutes market with a 36% share in 2025, driven by the widespread acceptance of implant procedures. They also helped in eliminating the second surgical site, which helped in reducing the patient's discomfort. Strong availability and consistent quality also supported their adoption rates.

The xenografts segment held the second-largest share of 28% of the market in 2025, as it provides long-term volume stability. Additionally, they are extensively used in sinus augmentation. Growing implant procedures also boost their demand. They also offer a natural bone-like structure and improved osteoconductive properties, which are increasing their acceptance rates.

The synthetic bone grafts segment held 18% of the U.S. dental bone grafts and substitutes market share in 2025 and is expected to witness the fastest growth with a CAGR of 9.8% during the forecast period, due to a rise in manufacturers launching advanced biomaterials. Their consistent quality also helps in improving clinician confidence. Their regulatory advantages also support a rise in their uptake.

The autografts segment held 14% of the market share in 2025, driven by its superior osteogenic properties. At the same time, their excellent biological compatibility is promoting their use in complex cases. Their high graft integration, no risk of immune rejection, and improved healing outcomes are also driving their use in large defect repairs and complex bone reconstruction.

")

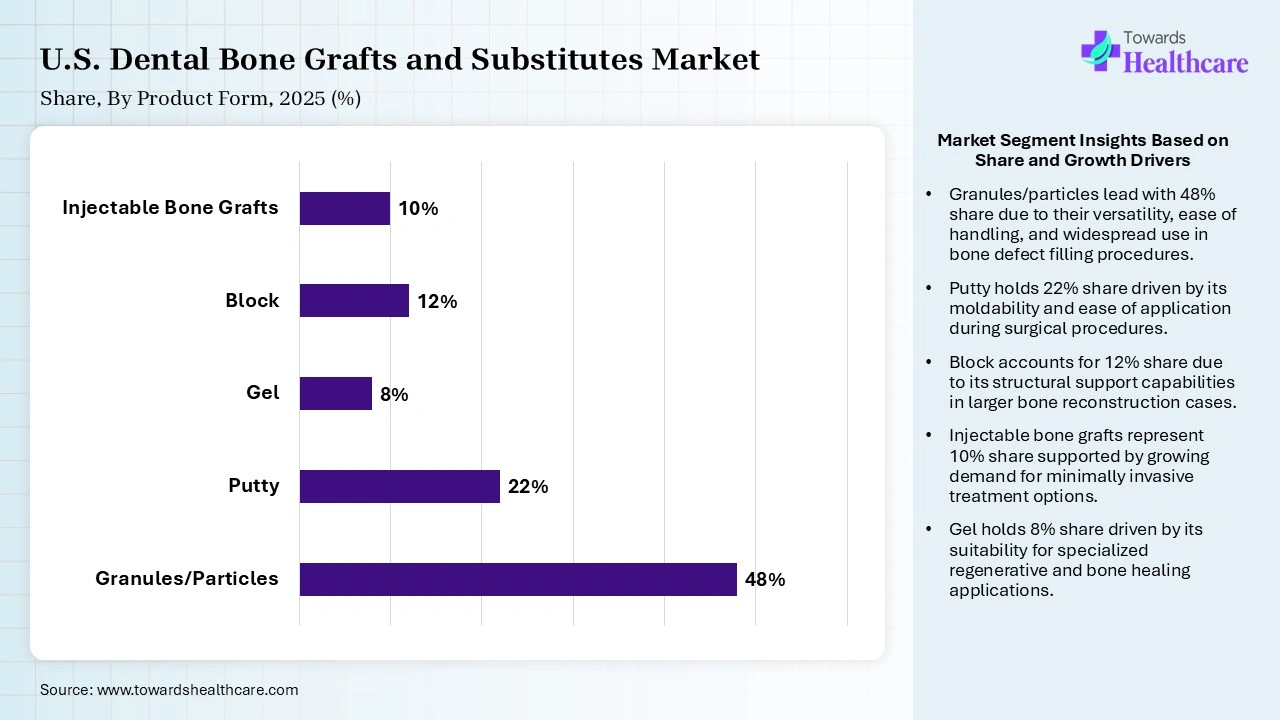

| Segment | Share 2025 (%) |

| Granules/Particles | 48% |

| Putty | 22% |

| Gel | 8% |

| Block | 12% |

| Injectable Bone Grafts | 10% |

The Granules/Particles Segment Dominated the Market With 48% in 2025

The granules/particles segment accounted for the highest revenue share of 48% of the U.S. dental bone grafts and substitutes market in 2025, driven by its excellent handling flexibility. Their enhanced compatibility with multiple surgical procedures also increased their use. Preferred by implant specialists due to their minimal preparation time, versatility, and proven clinical performance.

The putty segment held the second-largest share of 22% of the market in 2025, due to improved graft containment. Simplifies clinical application as well as supports minimally invasive approaches. At the same time, their enhanced versatility, ease of placement, and predictable bone regeneration also drive their demand.

The block segment held 12% of the U.S. dental bone grafts and substitutes market share in 2025, as it provides structural support in large defects. Common in ridge reconstruction, where their enhanced bone height and width restoration also drive their demand. Their enhanced compatibility with synthetic materials also increases their use in complex cases.

The injectable bone grafts segment held 10% of the market share in 2025 and is expected to show the highest growth with a CAGR of 10.5% during the forecast period, as it facilitates minimally invasive delivery. Their improved surgical efficiency is also supporting their widespread adoption. A rise in advanced regenerative dentistry is also fueling their demand.

")

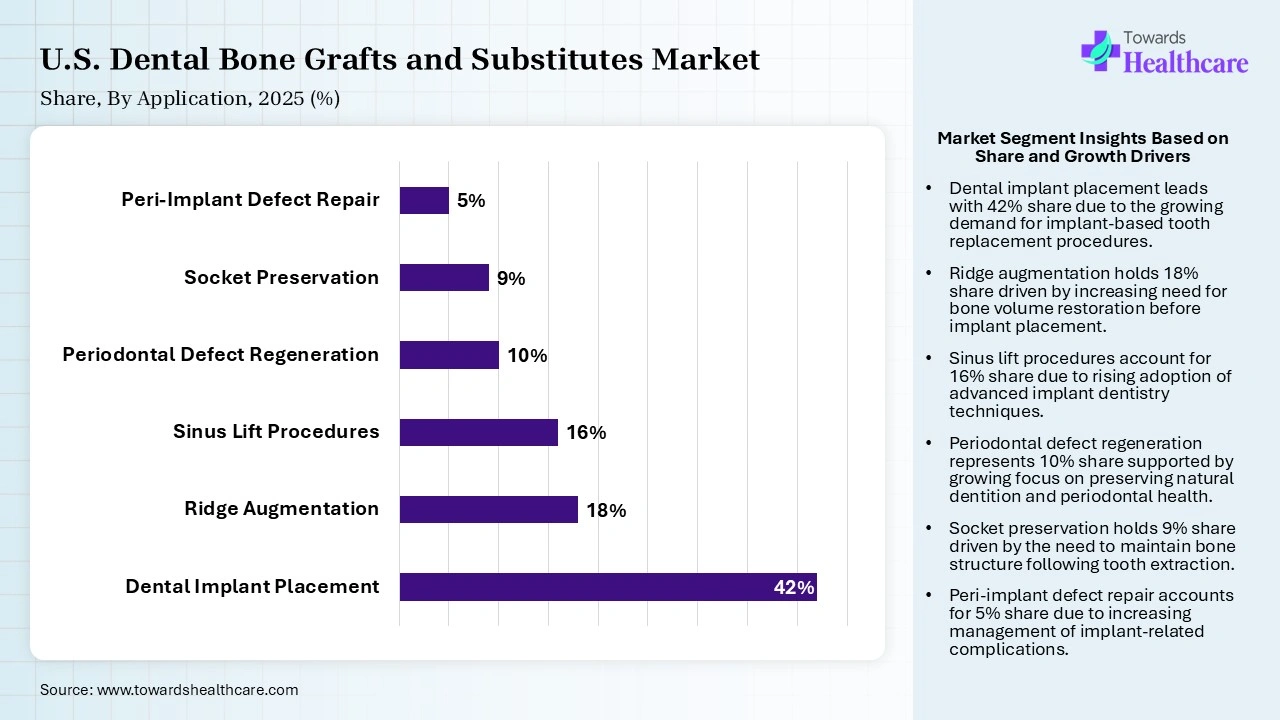

| Segment | Share 2025 (%) |

| Dental Implant Placement | 42% |

| Ridge Augmentation | 18% |

| Sinus Lift Procedures | 16% |

| Periodontal Defect Regeneration | 10% |

| Socket Preservation | 9% |

| Peri-Implant Defect Repair | 5% |

The Dental Implant Placement Segment Dominated the Market With 42% in 2025

The dental implant placement segment held a major revenue share of 42% of the U.S. dental bone grafts and substitutes market in 2025, due to growth in implant volumes, which increased graft demand. The aging population seeks tooth replacement, which has increased their use. Improved implant success rates also supported their growth.

The ridge augmentation segment held the second-largest share of 18% of the market in 2025, driven by expanding treatment eligibility for implants. They also support aesthetic outcomes, which increases their demand. Increasing specialist procedures are also driving their adoption rates. Their higher success rates are also increasing their use.

The sinus lift procedures segment held 16% of the U.S. dental bone grafts and substitutes market share in 2025, driven by the high prevalence of posterior maxillary bone loss. Their wide use before implants also contributes to their continuous usage. Advanced graft materials also improve outcomes, which supports their adoption rates.

The socket preservation segment held 9% of the market share in 2025 and is expected to expand rapidly with a CAGR of 9.4% during the forecast period, as dentists increasingly preserve alveolar bone after extraction. They also support future implant placement, which increases their demand. Patient awareness continues to rise, driving their demand.

")

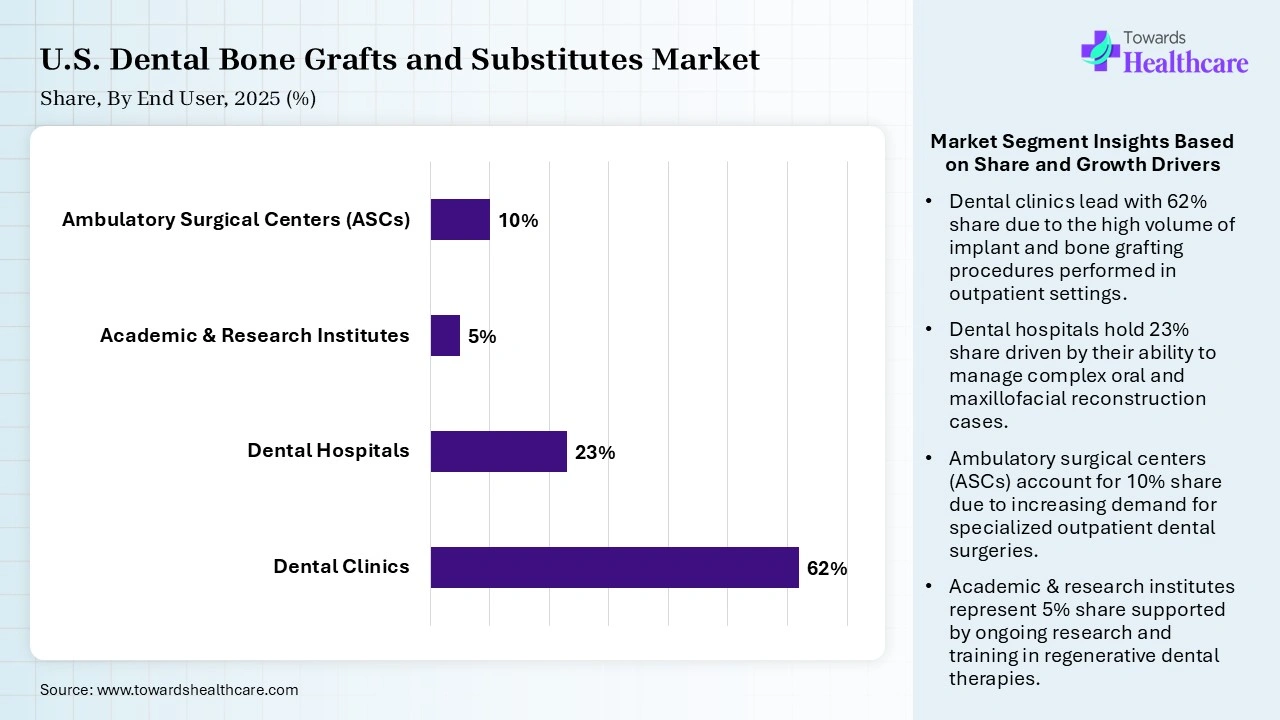

| Segment | Share 2025 (%) |

| Dental Clinics | 62% |

| Dental Hospitals | 23% |

| Academic & Research Institutes | 5% |

| Ambulatory Surgical Centers (ASCs) | 10% |

The Dental Clinics Segment Dominated the Market With 62% in 2025

The dental clinics segment contributed the biggest revenue share of 62% of the U.S. dental bone grafts and substitutes market in 2025, driven by the majority of implant and graft procedures occurring in clinics. Expansion of private practices also supported volume growth. Advanced technologies improved treatment capacity, which attracted the patients.

The dental hospitals segment held the second-largest share of 23% of the market in 2025, due to their increasing demand for handling complex oral reconstruction cases. Their benefit from multidisciplinary care is also increasing their demand. At the same time, growth supported by referral networks is also promoting their use.

The ambulatory surgical centers (ASCs) segment held 10% of the U.S. dental bone grafts and substitutes market share in 2025, due to growing outpatient procedures, which increase their utilization. These centres also offer lower procedural costs, which attract patients. Moreover, their growing efficiency advantages are also supporting their rapid expansion.

The academic & research institutes segment held 5% of the market share in 2025 and is expected to gain the highest share with a CAGR of 8.9% during the forecast period, driven by increasing biomaterial research, which drives their demand. Clinical trials expansion is also increasing their usage. Funding for regenerative dentistry also supports their growth.

")

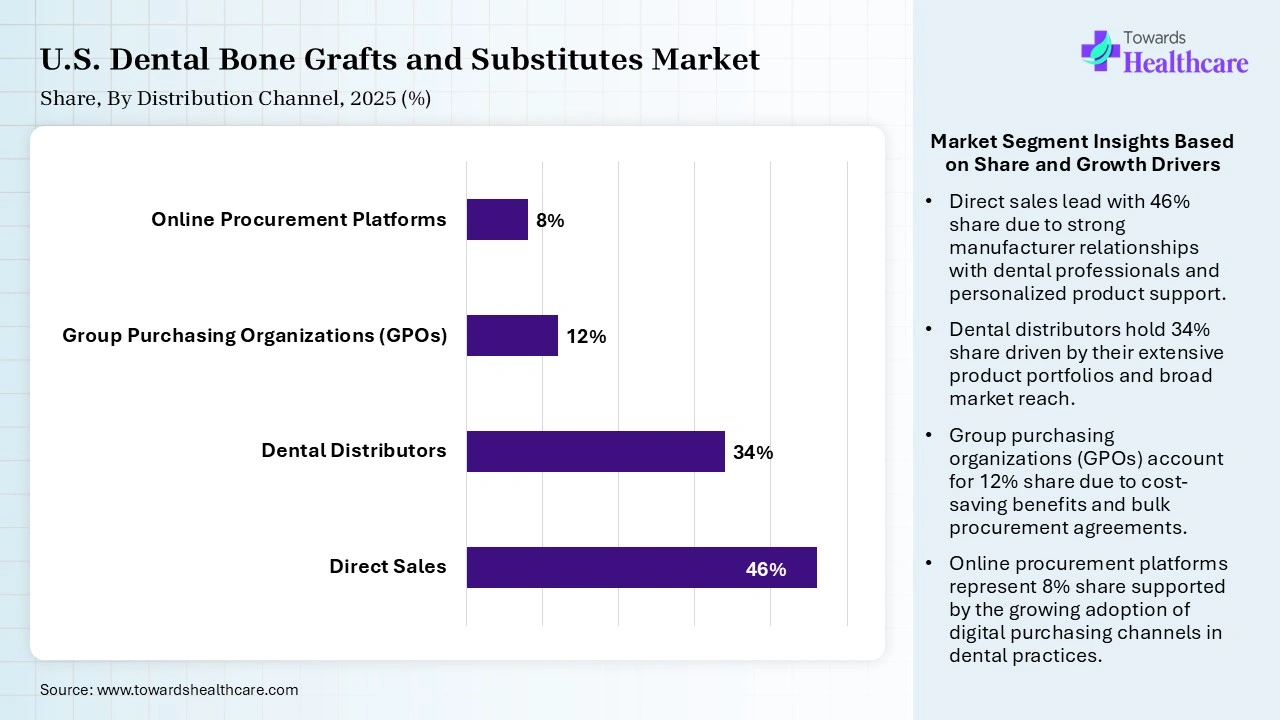

| Segment | Share 2025 (%) |

| Direct Sales | 46% |

| Dental Distributors | 34% |

| Group Purchasing Organizations (GPOs) | 12% |

| Online Procurement Platforms | 8% |

The Direct Sales Segment Dominated the Market With 46% in 2025

The direct sales segment held the largest revenue share of 46% of the U.S. dental bone grafts and substitutes market in 2025, driven by manufacturers maintaining strong clinical relationships. Their product training also improved their adoption rates. At the same time, their large accounts also preferred direct procurement, which increased their acceptance rates.

The dental distributors segment held the second-largest share of 34% of the market in 2025, due to broad product availability, which supports purchasing. Established distribution networks and improved inventory management also improve their accessibility and use. At the same time, clinics rely on distributor partnerships, which also increase their demand.

The group purchasing organizations (GPOs) segment held 12% of the U.S. dental bone grafts and substitutes market share in 2025, driven by their cost-saving contracts that attract providers. Consolidation increases purchasing power, promoting its use. Institutional buyers expand participation, which is driving new collaborations with GPOs.

The online procurement platforms segment held 8% of the market share in 2025 and is expected to grow with the fastest CAGR of 11.2% during the forecast period, due to digital procurement streamlining ordering. A rise in competitive pricing is also encouraging their adoption. E-commerce penetration continues to rise, which fuels its adoption.

The U.S. dental bone grafts and substitutes market held a significant share in 2025 and is expected to show lucrative growth during the forecast period, due to increasing incidences of periodontal disease and tooth loss. At the same time, a growing geriatric population is also increasing demand for regeneration procedures and restorative dental treatments, which is promoting the adoption of various dental bone grafts and substitutes. A rise in oral health, aesthetic, and cosmetic dentistry awareness is also increasing the use of these products, where expanding dental infrastructure and R&D activities supported by investments and funding are also increasing their use and innovations. Additionally, increasing demand for dental implants and bone augmentation procedures is also contributing to the market growth.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | U.S. Dental Bone Grafts and Substitutes |

| ZimVie Inc. | Palm Beach Gardens, U.S. | Puros Allograft, RegenerOss Xenograft, and RegenaVate DBM Putty |

| LifeNet Health | Virginia Beach, U.S. | Oracell, ReForm DBM Moldable Putty, and OraGRAFT |

| Dentsply Sirona Inc. | Charlotte, U.S. | Mineralized bone allograft, Symbios Allograft Particulate, and OSSIX Bone |

| Medtronic plc | Minneapolis, U.S. | Grafton DBM and Infuse Bone Graft |

| BioHorizons | Birmingham, U.S. | MinerOss Allograft, Memolok, and BioOss |

| Collagen Matrix, Inc. | Oakland, U.S. | Bone Graft Matrix, Mineralized Collagen Bone Graft Matrix, and Synthetic Anorganic Bone Mineral |

| Geistlich Pharma North America | Princeton, U.S. | Geistlich Bio-Oss and Geistlich Bio-Oss Collagen |

In December 2025, after the approval of U.S. FDA for the initiation of a pilot clinical trial to evaluate the safety and efficacy of TETRANITE®, Rahul Jadia, Ph.D., RevBio’s R&D Manager of Technology Development stated that “The ability for the product to adhere to the surrounding bony walls of a site that needs to be grafted is a fundamentally unique attribute of TETRANITE,” “Equally impressive is the fact that the material is substituted with bone in a clinically relevant timescale without significant loss of volume or adhesive and mechanical strength, which will ultimately help accelerate the course of complex dental procedures.”

By Material Type

By Product Form

By Application

By End User

By Distribution Channel

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar