")

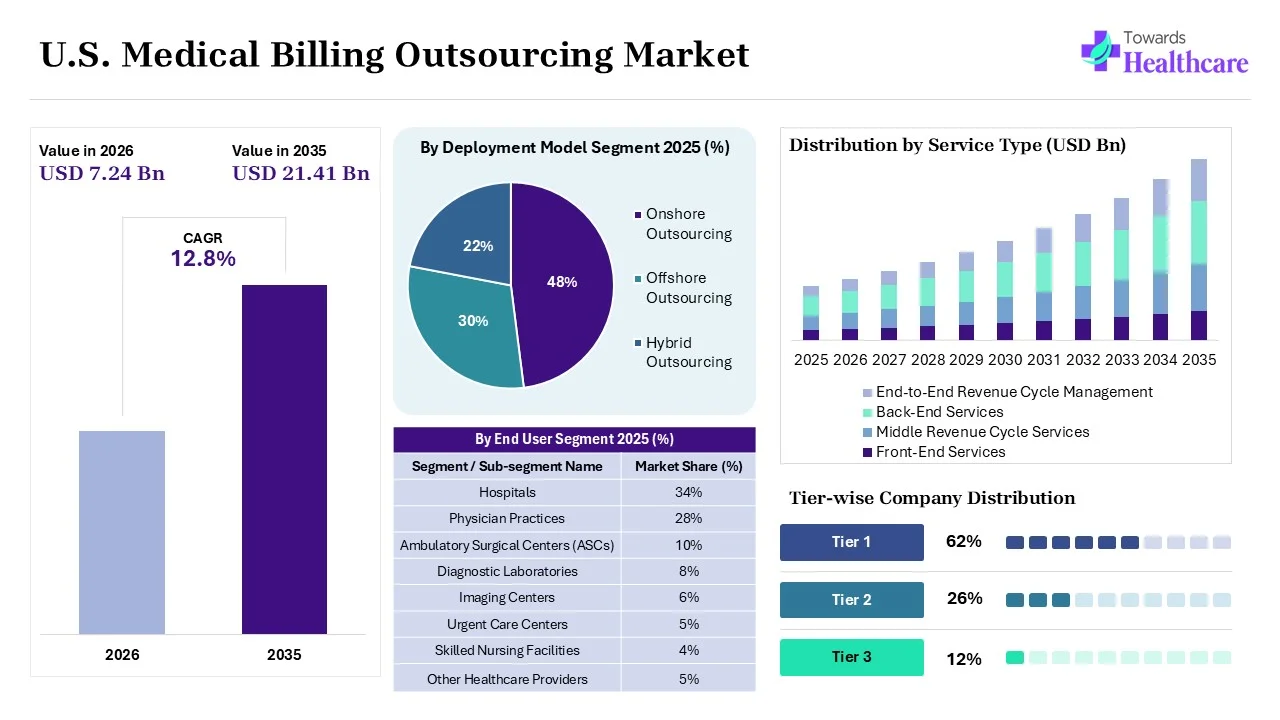

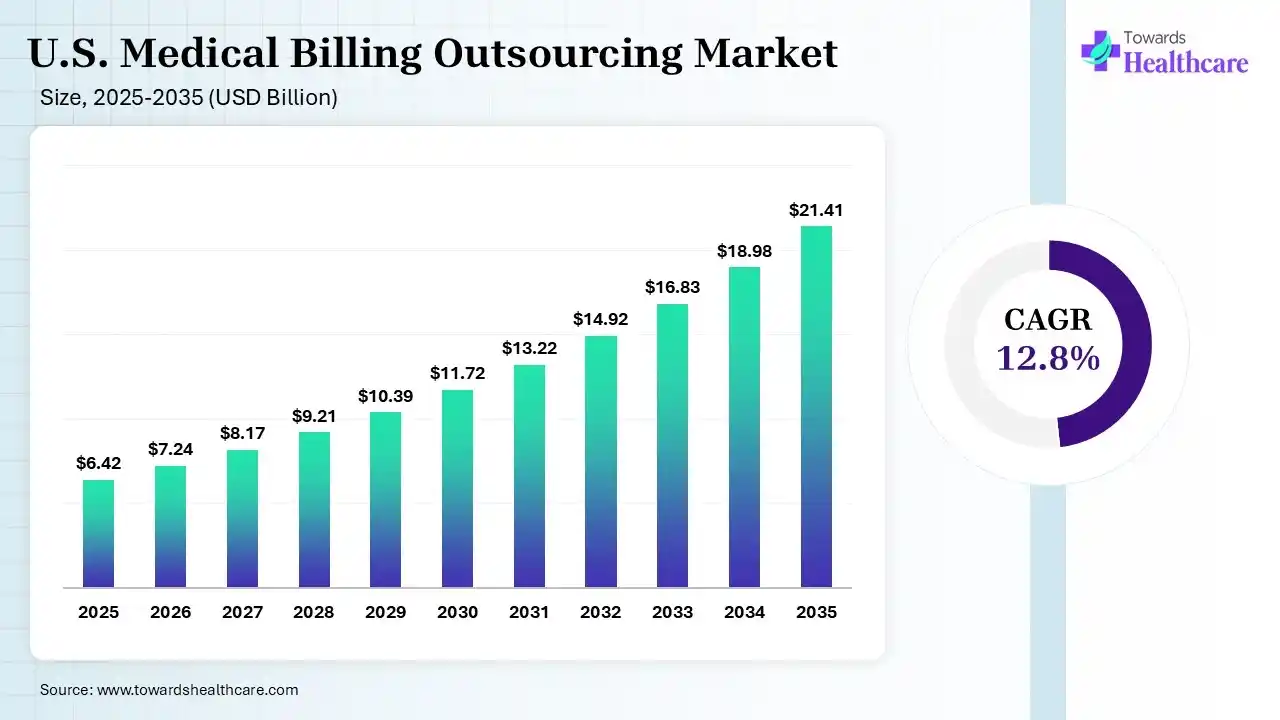

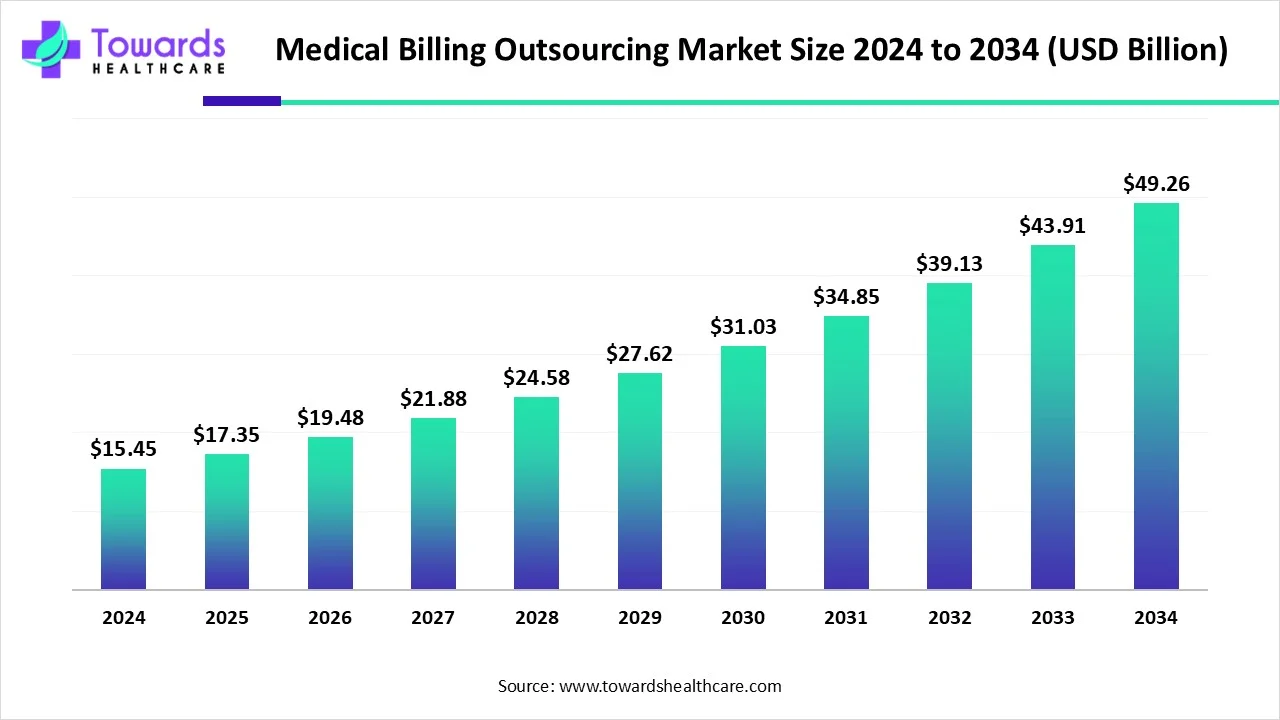

The U.S. medical billing outsourcing market is estimated at USD 6.42 billion in 2025, supported by increasing regulatory complexity, persistent staffing shortages, and the need to streamline administrative operations. The market is expected to witness steady growth in 2026 at USD 7.24 billion as providers focus on improving financial performance and compliance through specialized outsourcing partners. It is projected to reach USD 21.41 billion by 2035, CAGR of 12.8% over the forecast period driven by expanding cloud-based billing platforms, data analytics integration, and the growing shift toward scalable, technology-enabled revenue cycle solutions.

Medical billing outsourcing specializes in providing outsourced medical billing, coding, claims processing, and revenue cycle management (RCM) services to healthcare providers. It helps hospitals, physician practices, and other healthcare organizations improve reimbursement efficiency, reduce administrative burden, lower operational costs, and maintain compliance with evolving healthcare regulations.

Growth is driven by the increasing adoption of AI-powered revenue cycle management, automation, and cloud-based billing platforms. Key trends include the expanding use of digital billing solutions and data analytics, while opportunities are emerging from rising outsourcing demand among small and mid-sized healthcare providers. Technological advancements such as artificial intelligence (AI), robotic process automation (RPA), and predictive analytics are improving billing accuracy, reducing claim denials, and optimizing revenue cycle performance.

The U.S. medical billing outsourcing market is growing due to increasing demand for efficient revenue cycle management, rising healthcare services volumes, and complex reimbursement regulations. Healthcare providers are outsourcing billing operations to improve claims accuracy, reduce administrative workload, and accelerate reimbursement. Additionally, the adoption of AI-powered automation, cloud-based billing platforms, and advanced analytics is enhancing operational efficiency and supporting continued market growth.

Technological advancements are driving the U.S. medical billing outsourcing market by improving billing accuracy, streamlining claims processing, and enhancing revenue cycle efficiency. Cloud-based platforms, predictive analytics, robotic process automation (RPA), and advanced interoperability solutions help reduce administrative workload, minimize claim denials, ensure regulatory compliance, and accelerate reimbursement cycles, enabling outsourcing providers to deliver more efficient and scalable billing services.

Increasing Adoption of Cloud-Based Billing Platforms

Healthcare providers are increasingly adopting cloud-based billing platforms to improve data accessibility, streamline claims management, and support seamless integration with healthcare systems. These platforms enhance operational flexibility, strengthen data security, and enable faster reimbursement processes while ensuring regulatory compliance.

Growing Outsourcing by Small and Mid-Sized Healthcare Providers

Small and mid-sized healthcare providers are increasingly relying on outsourcing partners to manage billing operations efficiently while reducing operational costs. Future market growth will be driven by the need for scalable, compliant, and cost-effective billing solutions that support expanding healthcare services.

| Table | Scope |

| Market Size in 2026 | USD 7.24 Billion |

| Projected Market Size in 2035 | USD 21.41 Billion |

| CAGR (2026 - 2035) | 12.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By End User, By Specialty, By Deployment Model, By Organization Size, By Technology Integration, By Contract Model |

| Top Key Players | R1 RCM Inc., GeBBS Healthcare Solutions, CorroHealth, Ventra Health, ImagineSoftware, CareCloud, eClinicalWorks |

")

| Segment | Share 2025 (%) |

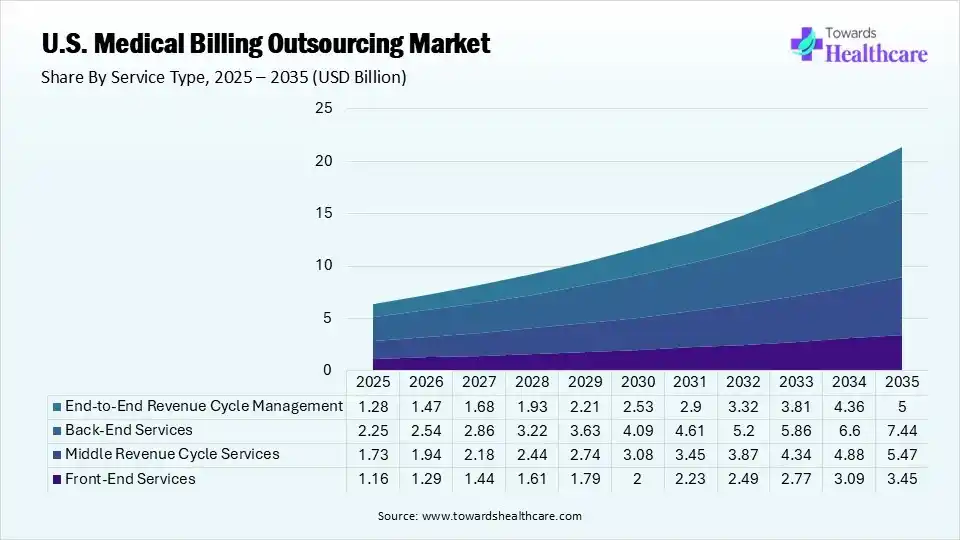

| Front-End Services | 18% |

| Middle Revenue Cycle Services | 27% |

| Back-End Services | 35% |

| End-to-End Revenue Cycle Management | 20% |

The Back-End Services Segment Dominated the U.S. Medical Billing Outsourcing Market in 2025

The back-end services segment held a dominant share of 35% in 2025 due to its critical role in claims submission, payment posting, and denial management, accounts receivable follow-up, and reimbursement optimization. Healthcare providers increasingly outsource these complex admission functions to improve cash flow, reduce billing errors, ensure regulatory compliance, and enhance overall revenue cycle performance while lowering operational costs.

The middle revenue cycle services segment held the second-largest share of 27% in 2025 due to its vital role in middle coding, charge capture, documentation review, and claim preparation. Healthcare providers increasingly outsource this preparation. Healthcare providers increasingly outsource these services to improve coding accuracy, reduce claim rejection, ensure regulatory compliance, and streamline reimbursement processes, ultimately enhancing operational efficiency and overall financial performance.

The end-to-end revenue cycle management segment held 20% share in 2025 and is expected to grow at the fastest CAGR in the U.S. medical billing outsourcing market during the forecast period due to rising demand for comprehensive billing solutions that streamline the entire reimbursement process. Healthcare providers are increasingly adopting integrated outsourcing services to improve financial performance, reduce administrative complexity, enhance claims efficiency, ensure regulatory compliance, and achieve long-term cost savings through a single service provider.

The front-end services segment held a 18% of market share in 2025 due to increasing emphasis on accurate patient registration, insurance eligibility verification, prior authorization, and appointment scheduling. Healthcare providers are outsourcing these functions to reduce claim denials, improve patient experience, minimize registration errors, and strengthen revenue cycle efficiency. Growing patient volumes and evolving payer requirements are further supporting segment growth.

")

| Segment | Share 2025 (%) |

| Hospitals | 34% |

| Physician Practices | 28% |

| Ambulatory Surgical Centers (ASCs) | 10% |

| Diagnostic Laboratories | 8% |

| Imaging Centers | 6% |

| Urgent Care Centers | 5% |

| Skilled Nursing Facilities | 4% |

| Other Healthcare Providers | 5% |

The Hospitals Segment Led the Market in 2025 with the Largest Share

The hospitals segment dominated the U.S. medical billing outsourcing market with a share of 34% in 2025 due to high patient volumes, complex billing requirements, and extensive reimbursement processes. Hospitals increasingly outsource billing services to improve claims accuracy and reduce administrative burden, accelerate reimbursement, and maintain compliance with evolving healthcare regulations. The need to optimize revenue cycle performance while managing rising operational costs continues to strengthen the segment’s market leadership.

The physician practices segment held the second-largest share of 28% in 2025 due to the increasing number of office-based surgical and minimally invasive procedures requiring effective blood management. These practices are adopting advanced medical technologies to improve procedural safety, enhance patient outcomes, and reduce referrals to hospitals. Growing demand for specialized care, expanding outpatient services, and improved access to surgical expertise have further supported the segment’s strong market position.

The diagnostic laboratories segment held a 8% of market share due to the increasing demand for rapid and accurate diagnostic testing to support timely clinical decision-making. Rising prevalence of infectious and chronic diseases, expanding preventive health screening programs, and greater adoption of automated laboratory technologies are driving growth. Continuous improvements in laboratory infrastructure, higher testing volumes, and stronger collaboration with healthcare providers are further supporting the segment expansion.

The urgent care centers segment held 5% share in 2025 and is expected to grow at the fastest CAGR in the U.S. medical billing outsourcing market during the forecast period due to rising demand for convenient, same-day medical services and shorter wait times compared to hospitals. Increasing cases of minor injuries and acute illness, expanding urgent care networks, and growing adoption of diagnostic technologies are driving patient visits. Greater affordability and extended operating hours are further accelerating the segment’s growth.

")

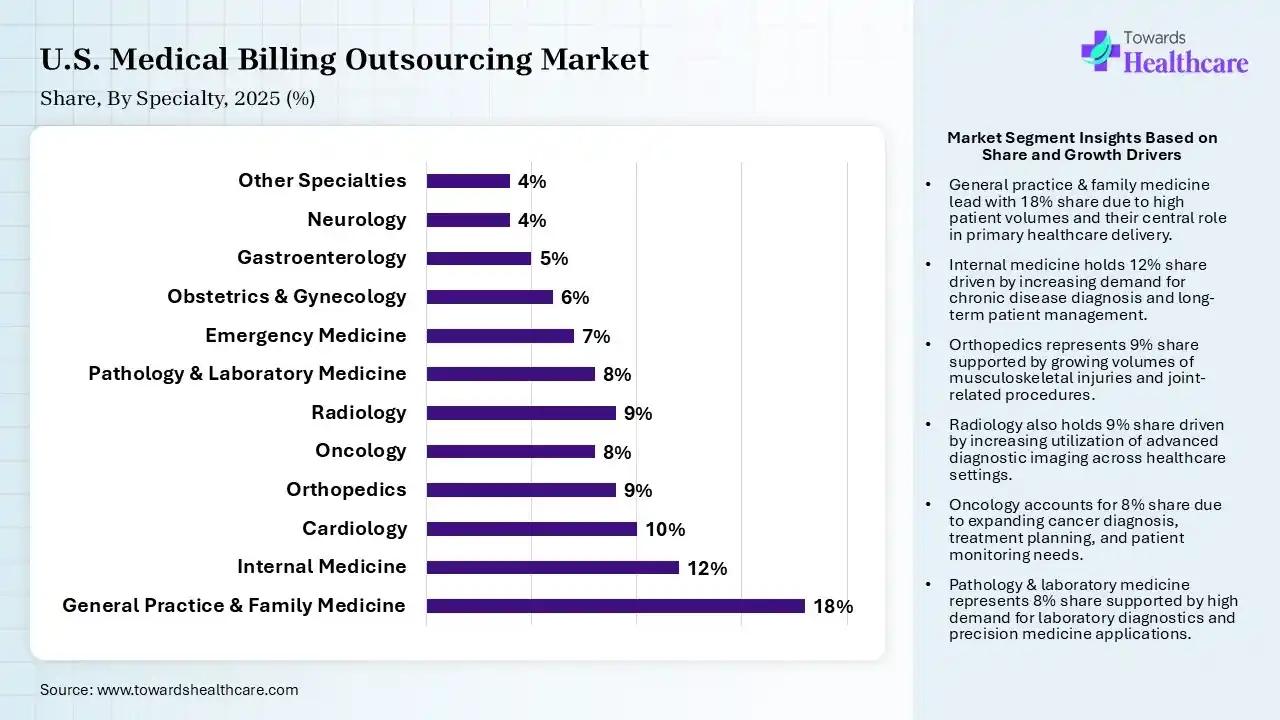

| Segment | Share 2025 (%) |

| General Practice & Family Medicine | 18% |

| Internal Medicine | 12% |

| Cardiology | 10% |

| Orthopedics | 9% |

| Oncology | 8% |

| Radiology | 9% |

| Pathology & Laboratory Medicine | 8% |

| Emergency Medicine | 7% |

| Obstetrics & Gynecology | 6% |

| Gastroenterology | 5% |

| Neurology | 4% |

| Other Specialties | 4% |

The General Practice & Family Medicine Segment Dominated the U.S. Medical Billing Outsourcing Market in 2025

The general practice & family medicine segment led the market with a share of 18% in 2025 due to its high patient volumes and frequent insurance claims, creating a greater need for efficient billing and coding services. Outsourcing helps these practices reduce administrative burden, improve claim accuracy, accelerate reimbursements, and maintain regulatory compliance. The growing focus on operational efficiency and allowing physicians to spend more time on patient care further strengthened the segment’s leading position.

The internal medicine segment held the second-largest share of 12% in 2025 due to the high volume of patients requiring ongoing management of chronic and complex medical conditions. Frequent consultation, diagnostic tests, and follow-up visits generate substantial billing activity, encouraging outsourcing for accurate coding and faster reimbursements. Increasing documentation requirements, insurance complexities, and the need to improve administrative efficiency further supported the segment’s strong position.

The orthopedics segment held a 9% of market share due to the increasing number of joint replacement surgeries, sports injuries, fracture treatments, and age-related musculoskeletal disorders. These procedures involve complex coding and multiple reimbursements, encouraging providers to outsource medical billing services. Growing patient volumes, rising demand for specialized orthopedic care, and the need to improve claim accuracy and revenue cycle efficiency are driving the segment’s continued growth.

The neurology segment held 4% share in 2025 and is expected to grow at the fastest CAGR in the U.S. medical billing outsourcing market during the forecast period due to the increasing prevalence of neurological disorders, rising demand for specialized diagnostic and treatment services, and growing complexity of reimbursement processes. Neurology practices handle extensive documentation, advanced imaging, and procedure-based billing, making outsourcing an effective solution for improving coding accuracy, accelerating reimbursements, and reducing administrative workload.

")

| Segment | Share 2025 (%) |

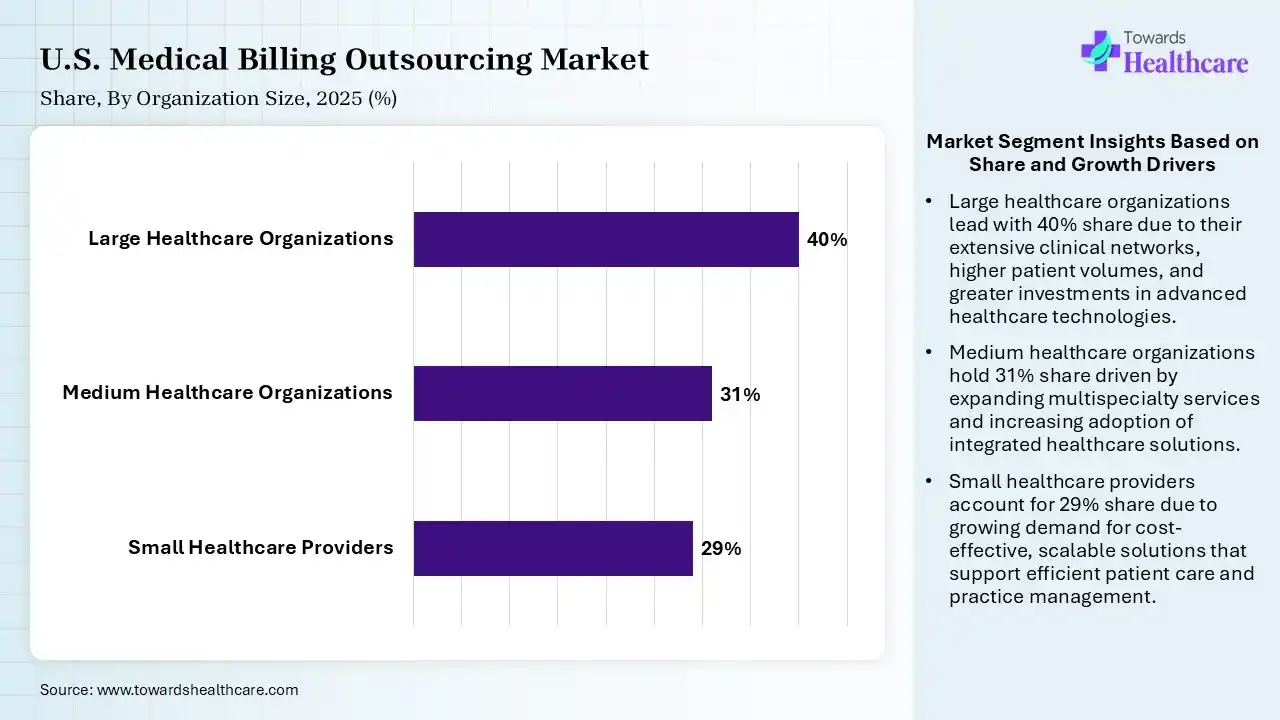

| Small Healthcare Providers | 29% |

| Medium Healthcare Organizations | 31% |

| Large Healthcare Organizations | 40% |

The Large Healthcare Organizations Segment Led the Market in 2025 with the Largest Share

The large healthcare organizations segment dominated the U.S. medical billing outsourcing market with a share of 40% in 2025 due to the high volume of patient claims, complex reimbursement processes, and extensive administrative requirements handled by large healthcare organizations. Outsourcing medical billing helps improve claim accuracy, accelerate reimbursement, reduce operational costs, and ensure regulatory compliance. Growing investments in advanced revenue cycle management solutions and the need to optimize financial performance further strengthen the segment’s leading position.

The medium healthcare organizations segment held the second-largest share of 31% in 2025 due to the growing need to manage large patient volumes, complex reimbursement processes, and multi-specialty billing operations. Outsourcing enables these organizations to improve revenue cycle efficiency, reduce administrative costs, enhance coding accuracy, and maintain regulatory compliance. Increasing investments in digital healthcare infrastructure and centralized billing solutions further supported the segment’s strong market position.

The small healthcare providers segment held 29% share in 2025 and is expected to grow at the fastest CAGR in the U.S. medical billing outsourcing market during the forecast period as independent clinics and physician-owned practices increasingly outsource billing to reduce administrative costs and improve cost flow. Limited in-house billing resources, rising insurance complexities, and growing compliance requirements are encouraging outsourcing adoption. Cloud-based revenue cycle management solutions and flexible services models are further accelerating growth among smaller healthcare providers.

")

| Segment | Share 2025 (%) |

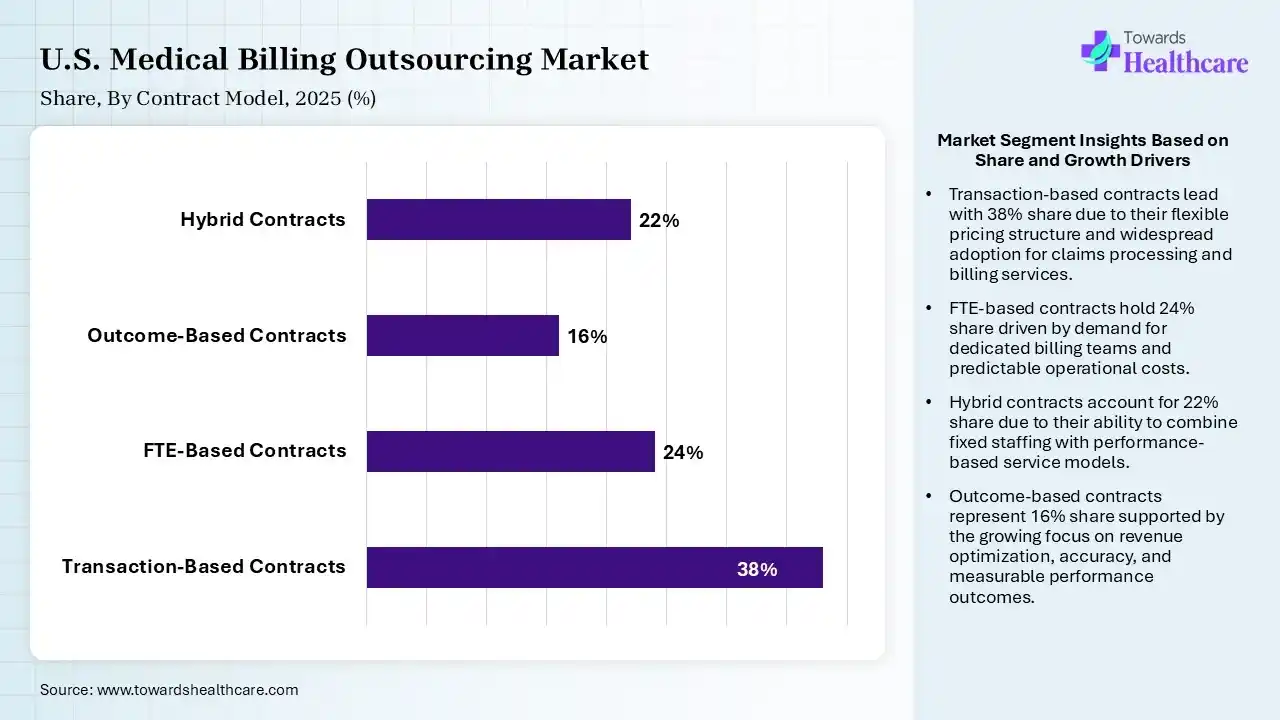

| Transaction-Based Contracts | 38% |

| FTE-Based Contracts | 24% |

| Outcome-Based Contracts | 16% |

| Hybrid Contracts | 22% |

The Transaction-Based Contracts Segment Dominated the U.S. Medical Billing Outsourcing Market in 2025

The transaction-based contracts segment held a dominant share of 38% in 2025 due to its flexible pricing model, allowing healthcare providers to pay only for the billing services they use. This approach helps control operational costs while improving scalability during fluctuations in patient volumes. Its suitability for practices of all sizes, combined with reduced financial risk and simplifying outsourcing arrangements, made transaction-based contracts the preferred choice across the U.S. medical billing outsourcing industry.

The FTE-based contracts segment held the second-largest share of 24% in 2025 because it provides healthcare organizations with dedicated billing professionals for managing continuous, high-volume revenue cycle operations. This model improves workflow consistency, enhances coding accuracy, and supports faster claims processing. Large hospitals and multi-specialty practices prefer FTE-based contracts for predictable staffing, better operational control, and long-term cost efficiency.

The hybrid contracts segment held a 22% of market share as healthcare providers seek a balanced approach that combines fixed staffing support with performance or transaction-based pricing. This model offers greater flexibility, improves cost control, and adapts to changing billing workloads. Its ability to optimize operational efficiency while ensuring consistent revenue cycle performance makes a hybrid contract an increasingly attractive option for healthcare organizations of all sizes.

The outcome-based contracts segment held 16% share in 2025 and is expected to grow at the fastest CAGR in the U.S. medical billing outsourcing market during the forecast period as healthcare providers increasingly prioritize measurable financial and operational results. These contracts link payments to key performance indicators such as claim accuracy, reimbursement rates, and denial reduction. Growing adoption of value-based healthcare, demand for accountability, and advances in analytics are accelerating the shift toward outcome-driven outsourcing models.

The global medical billing outsourcing market size is calculated at US$ 17.35 in billion 2025, grew to US$ 19.48 billion in 2026, and is projected to reach around US$ 55.35 billion by 2035. The market is expanding at a CAGR of 12.3% between 2026 and 2035.

The market lead is due to the widespread adoption of outsourced revenue cycle management services across hospitals, physician groups, and specialty clinics. Increasing claim volumes, complex reimbursement requirements, and the need to improve operational efficiency encourage providers to rely on specialized billing partners. Continuous investments in automation, AI-enabled billing solutions, and compliance-focused services further strengthened the country’s leadership.

| Companies | Headquarters | Offerings |

| R1 RCM Inc. | Murray, Utah, USA | End-to-end revenue cycle management, medical billing, coding, and patient payment solutions |

| GeBBS Healthcare Solutions | Culver City, California, USA | Medical billing, coding, risk adjustment, revenue cycle management |

| CorroHealth | Plano, Texas, USA | Medical billing, clinical documentation improvement, coding, and revenue integrity |

| Ventra Health | Dallas, Texas, USA | Revenue cycle management, anesthesia, and emergency medicine billing |

| ImagineSoftware | Charlotte, North Carolina, USA | Medical billing software, practice management, revenue cycle solutions |

| CareCloud | Somerset, New Jersey, USA | Medical billing, EHR, practice management, revenue cycle management |

| eClinicalWorks | Westborough, Massachusetts, USA | Medical billing, EHR, practice management, revenue cycle management |

In March 2026, “it's always a challenge to get paid by insurance, and especially nowadays, it's becoming more and more complicated. The payer rules are constantly changing. There are more prior authorization requirements. More denials are happening. Claims are getting rejected. Systems are more fragmented, so it's just harder to get paid by insurance for the services that you've already rendered. And there are a lot of reasons why that is, but I think we're just seeing mass frustration across the board from most physicians and providers in the industry,” said Roshan Patel, founder and CEO of a health care payments company.

By Service Type

By End User

By Specialty

By Deployment Model

By Organization Size

By Technology Integration

By Contract Model

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar