")

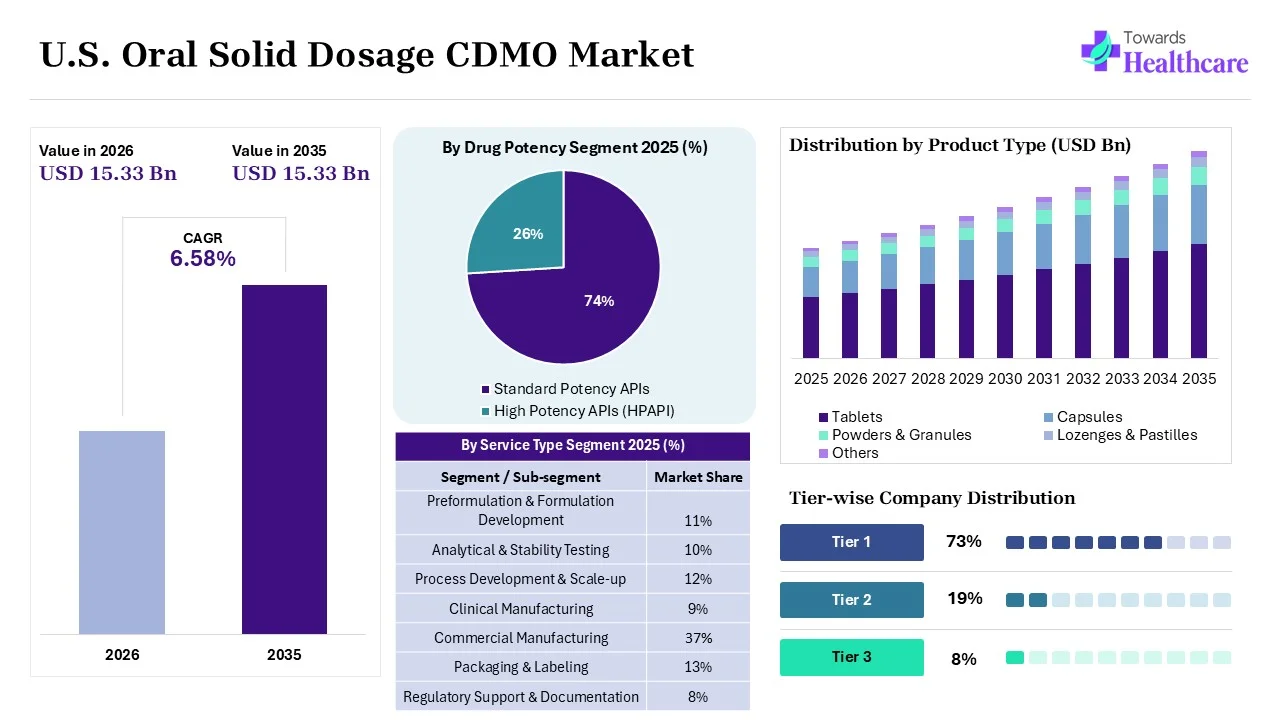

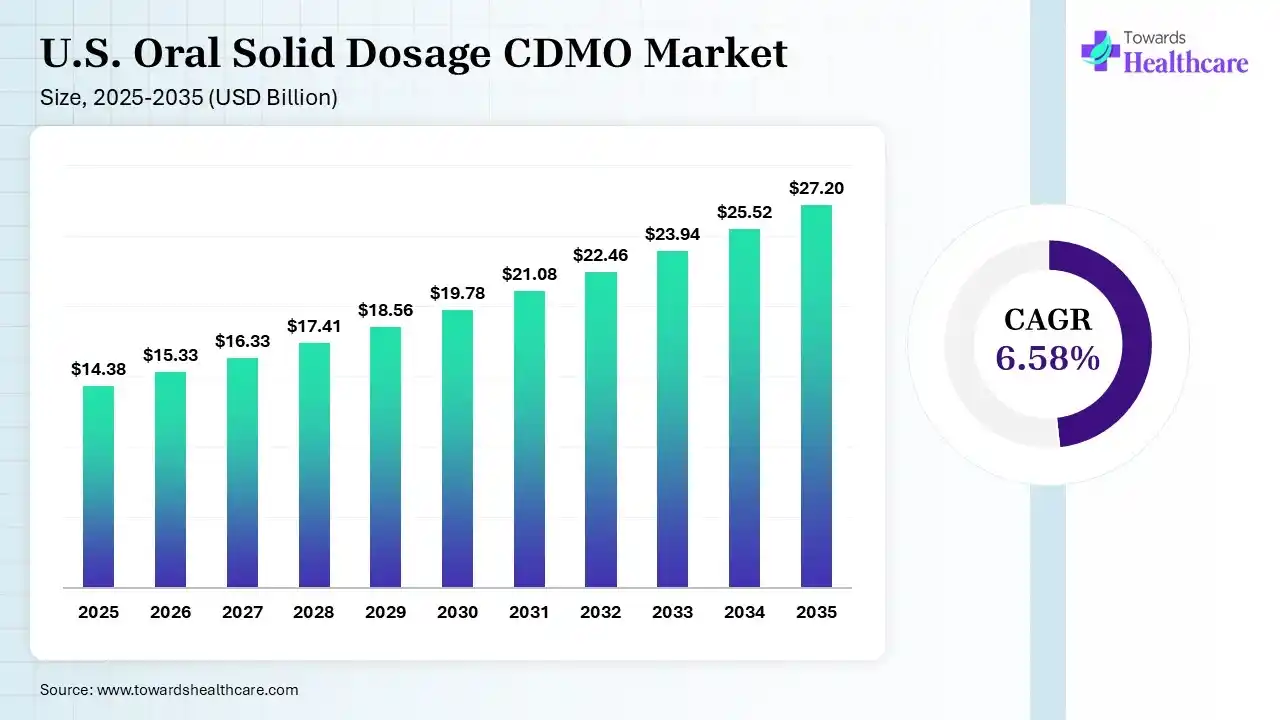

The U.S. oral solid dosage CDMO market size is calculated at USD 14.38 billion in 2025, driven by expanding outsourcing trends across the U.S. for the development of complex oral solid formations. The market continues to grow USD 15.33 Bn in 2026 due to the rising demand for specialized manufacturing technologies, generic drugs, and personalized medicine. It is expected to reach USD 27.2 billion by 2035, registering a CAGR of 6.58% during the period. As integration of AI technologies, growing chronic disease burden, and rising demand for specialized formulation accelerate market expansion.

")

The U.S. oral solid dosage CDMO market is driven by growth in the outsourcing of complex formulations, urgent demand for specialized manufacturing technologies, and an expanding generic drug pipeline. The U.S. oral solid dosage CDMO encompasses contract development and manufacturing organizations across the U.S., providing services for the development of oral solid dosage drugs. These CDMOs offer a wide range of services such as drug formulation and development, process development and optimization, commercial-scale manufacturing, clinical trial manufacturing, packaging and labelling, and regulatory support. They help pharma and biotech companies to reduce manufacturing costs, scale production efficiently, accelerate drug development, access specialized technologies, and maintain regulatory compliance.

At the same time, with the growing use of oral solid formulations across the U.S., the demand for oral solid dosage CDMOs is increasing. The common types of oral formulation driving their use involve tablets, capsules, granules, modified release formulations, powders, lozenges, and controlled release formulations. Furthermore, the growing incidence of cancer, cardiovascular diseases, diabetes, gastrointestinal disorders, infectious diseases, respiratory disorders, rare diseases, and mental health disorders is fueling the development of novel oral products, opening new doors for CDMOs. Expanding clinical trial manufacturing demand, increasing healthcare investments, growing focus on quality control, and rising demand for specialized formulations are also contributing to the market expansion.

The use of AI in the U.S. oral solid dosage CDMO market is increasing as it helps in the optimization of oral formulation and enhances manufacturing efficiency. It is also used for detecting defects and production errors, where it is also used for real-time process monitoring and predictive maintenance. AI also helps in accelerating drug development, enhancing quality control, and improving batch consistency, where it also offers process automation, documentation management, and assists in regulatory compliance, reducing the chances of product failure.

Expanding Generic Drug Manufacturing

A rise in patent expiration and increasing demand for cost-effective medications are increasing the demand for generic oral formulations. This, in turn, is increasing the use of oral solid dosage CDMOs for formulation development, commercial production, scale-up, and regulatory support, where the expanding outsourcing trends are also increasing their use. Furthermore, growing government support and healthcare expenditure are also expanding the generic drug pipeline, promoting the use of high-volume manufacturing capabilities of the CDMOs.

Adoption of Continuous Manufacturing

In order to enhance production efficiency and minimize manufacturing costs, the demand for continuous manufacturing is increasing. They also offer real-time monitoring, better process control, and improved batch consistency, enhancing product quality. It also helps in reducing production time and minimizing material waste, and supports flexible production volume, where the growing demand for advanced manufacturing technologies and automation is also increasing their use.

Rising Demand for Personalized Medicines

Growing focus on patient-specific therapies is increasing the demand for personalized medicine, which is fueling the development of specialized oral dosage formulations, driving the use of oral solid dosage CDMOs. Additionally, growing demand for targeted therapies and affordable prescription medicines is also increasing their use, and advancements in biomarker-based therapies are also driving their demand. Their flexible manufacturing capabilities and customized drug development expertise also attract clients.

| Table | Scope |

| Market Size in 2026 | USD 15.33 Billion |

| Projected Market Size in 2035 | USD 27.2 Billion |

| CAGR (2026 - 2035) | 6.58% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Service Type, By Therapeutic Area, By Customer Type, By End User, By Drug Potency, By Manufacturing Scale, By Release Profile |

| Top Key Players | Catalent, Inc., Aenova Group, Lonza Group AG, Cambrex Corporation, Thermo Fisher Scientific Inc., Piramal Pharma Solutions, Recipharm AB |

")

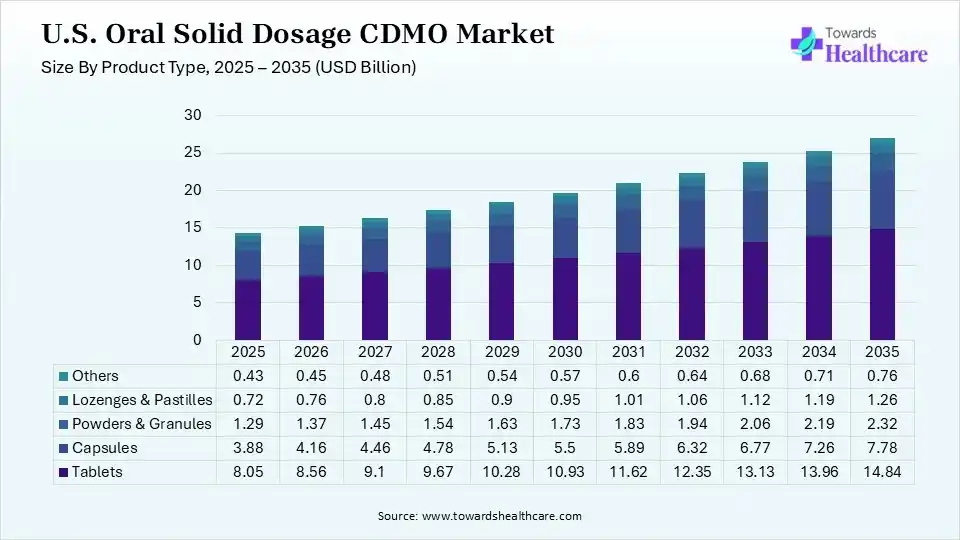

| Segment | Share 2025 (%) |

| Tablets | 56% |

| Capsules | 27% |

| Powders & Granules | 9% |

| Lozenges & Pastilles | 5% |

| Others | 3% |

The Tablets Segment Dominated the Market With 56% in 2025

The tablets segment led the U.S. oral solid dosage CDMO market with 56% share in 2025, as they were the preferred dosage form due to manufacturing efficiency. Strong demand for chronic therapies sustained their outsourcing, which increased the use of oral solid dosage CDMOs. Continuous formulation innovations also expanded production volumes.

The capsules segment held the second-largest share of 27% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 7.21% during the forecast period, due to growing demand for specialty formulations, which supports expansion. Better patient compliance drives adoption. Additionally, increasing nutraceutical and prescription products fuel outsourcing.

The powders & granules segment held 9% of the U.S. oral solid dosage CDMO market share in 2025, due to sachet-based therapies continuing to expand. Pediatric applications also increase demand, which ultimately fuels the adoption of CDMO services. At the same time, their flexible packaging solutions also support their growth.

The lozenges & pastilles segment held 5% of the market share in 2025, driven by consumer preference for throat-care products, which boosts production. OTC launches create new manufacturing opportunities. Their localized drug delivery and easy administration also increase their production rates. Growing flavor innovations also increase their demand, increasing the use of oral solid dosage CDMOs.

")

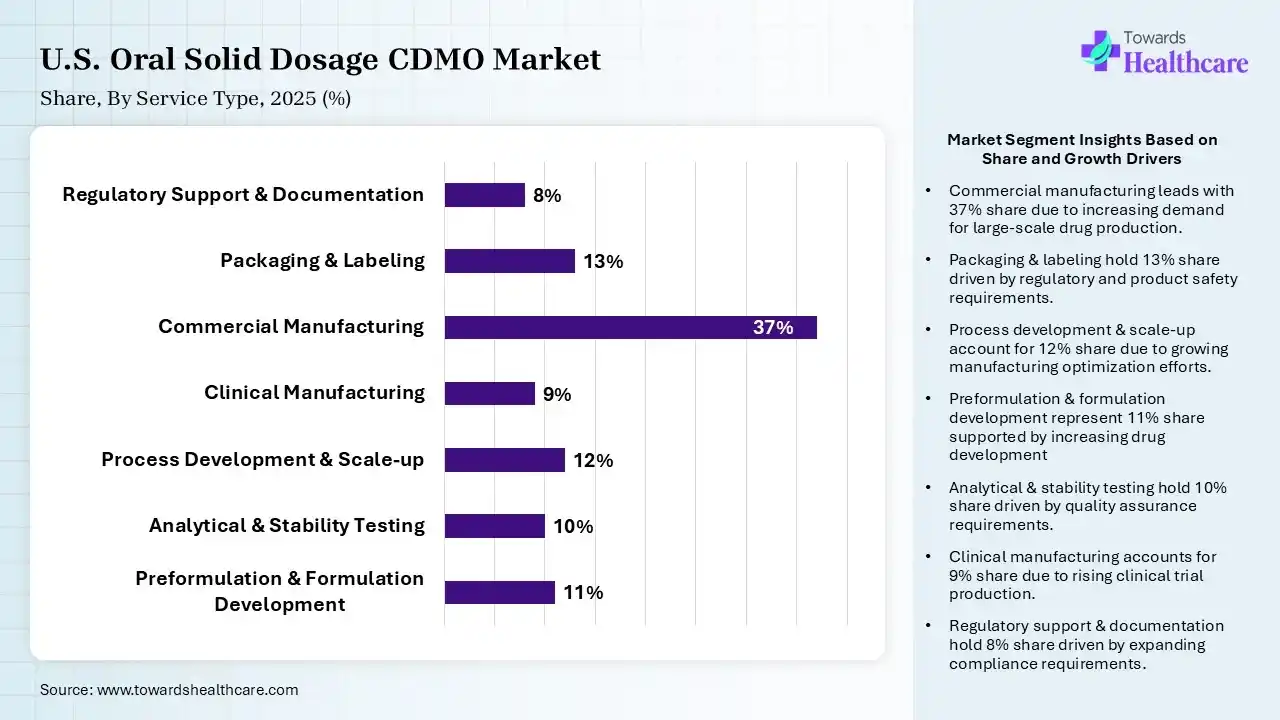

| Segment | Share 2025 (%) |

| Preformulation & Formulation Development | 11% |

| Analytical & Stability Testing | 10% |

| Process Development & Scale-up | 12% |

| Clinical Manufacturing | 9% |

| Commercial Manufacturing | 37% |

| Packaging & Labeling | 13% |

| Regulatory Support & Documentation | 8% |

The Commercial Manufacturing Segment Dominated the Market With 37% in 2025

The commercial manufacturing segment accounted for the highest revenue share of 37% of the U.S. oral solid dosage CDMO market in 2025, as commercial launches required large-scale capacity. Pharmaceutical companies optimize manufacturing costs, which drives the demand for these services. Reliable supply chains strengthen outsourcing demand, which encourages the use of these services.

The packaging & labeling segment held the second-largest share of 13% of the market in 2025 and is expected to show the highest growth with a CAGR of 7.34% during the forecast period, as serialization requirements increase outsourcing demand. Growing demand for patient-friendly packaging also increases its demand. Automated packaging technologies improve their efficiency.

The process development & scale-up segment held 12% of the U.S. oral solid dosage CDMO market share in 2025, as process optimization reduces production costs. Technology transfer activities continue rising, which increases the demand for expertise, driving the use of these services. Scale-up expertise also helps shorten commercialization timelines.

The preformulation & formulation development segment held 11% of the market share in 2025, due to complex formulations requiring early development expertise. CDMOs accelerate development timelines, which increases the acceptance rates. Advanced formulation technologies also improve success rates. They also help in enhancing drug solubility, bioavailability, and stability, which increases their use.

")

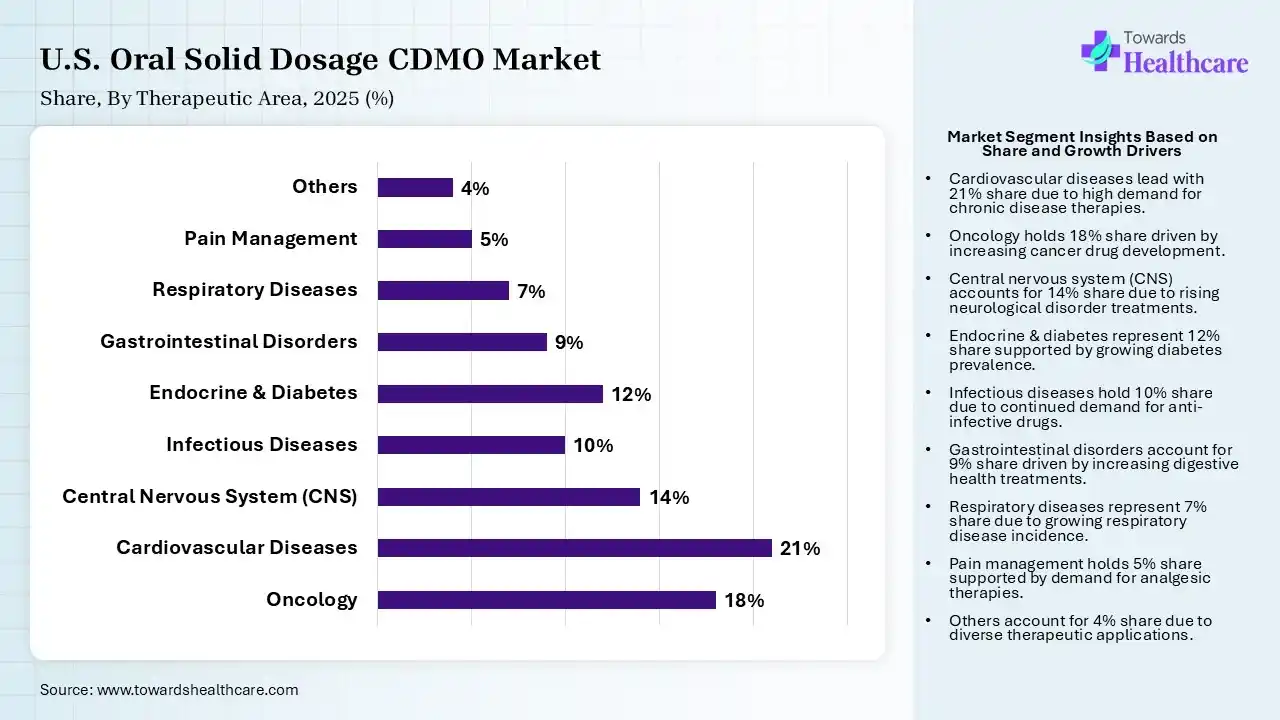

| Segment | Share 2025 (%) |

| Oncology | 18% |

| Cardiovascular Diseases | 21% |

| Central Nervous System (CNS) | 14% |

| Infectious Diseases | 10% |

| Endocrine & Diabetes | 12% |

| Gastrointestinal Disorders | 9% |

| Respiratory Diseases | 7% |

| Pain Management | 5% |

| Others | 4% |

The Cardiovascular Diseases Segment Dominated the Market With 21% in 2025

The cardiovascular diseases segment held a major revenue share of 21% of the U.S. oral solid dosage CDMO market in 2025, driven by growth in chronic disease prevalence, which supported consistent production. Generic medicines maintained high volumes, which increased the use of oral solid dosage CDMO services. Aging populations have also increased their prescriptions.

The oncology segment held the second-largest share of 18% of the market in 2025 and is expected to expand rapidly with a CAGR of 8.12% during the forecast period, due to rapid oncology pipeline expansion, which increases outsourcing. Growing HPAPI manufacturing investments are also supporting their CDMO services usage. Precision medicine strengthens demand, contributing to a rise in the use of these services.

The central nervous system (CNS) segment held 14% of the U.S. oral solid dosage CDMO market share in 2025, due to neurological disorders continuing to increase. Novel CNS therapies support outsourcing to leverage various CDMO services. Improved patient access also boosts their demand, encouraging the use of oral solid dosage CDMOs.

The endocrine & diabetes segment held 12% of the market share in 2025, as diabetes prevalence continues to increase. Long-term medication usage supports large volume development of oral formulations, which ultimately increases the use of oral solid dosage CDMO services. Growing innovations are also expanding oral therapies, fueling new collaborations.

")

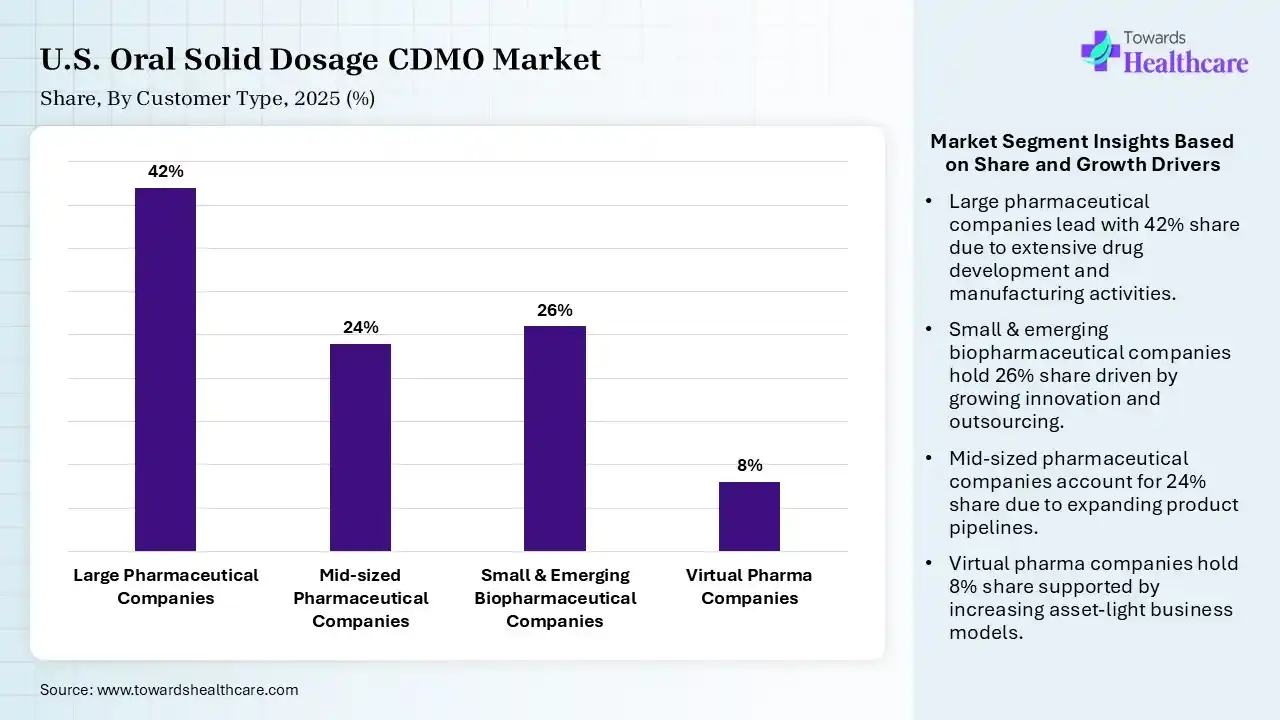

| Segment | Share 2025 (%) |

| Large Pharmaceutical Companies | 42% |

| Mid-sized Pharmaceutical Companies | 24% |

| Small & Emerging Biopharmaceutical Companies | 26% |

| Virtual Pharma Companies | 8% |

The Large Pharmaceutical Companies Segment Dominated the Market With 42% in 2025

The large pharmaceutical companies segment contributed the biggest revenue share of 42% of the U.S. oral solid dosage CDMO market in 2025, due to capacity optimization, which encouraged outsourcing. Global supply chain strategies also increased their partnerships. Cost efficiency also remained a priority, which increased their use.

The small & emerging biopharmaceutical companies segment held the second-largest share of 26% of the market in 2025 and is expected to gain the highest share with a CAGR of 8.13% during the forecast period, driven by asset-light business models increasing CDMO dependence. Venture-backed pipelines expand rapidly, prompting their use. Specialized manufacturing capabilities also attract outsourcing.

The mid-sized pharmaceutical companies segment held 24% of the U.S. oral solid dosage CDMO market share in 2025, driven by portfolio expansion, which increases manufacturing needs. Limited internal capacity also drives outsourcing, driving the demand for CDMO services. At the same time, faster commercialization also supports their growth.

The virtual pharma companies segment held 8% of the market share in 2025, due to virtual business models relying entirely on external manufacturing. Flexible production supports commercialization, which is increasing the demand for oral solid dosage CDMO services. A rise in innovations is also fueling their demand.

")

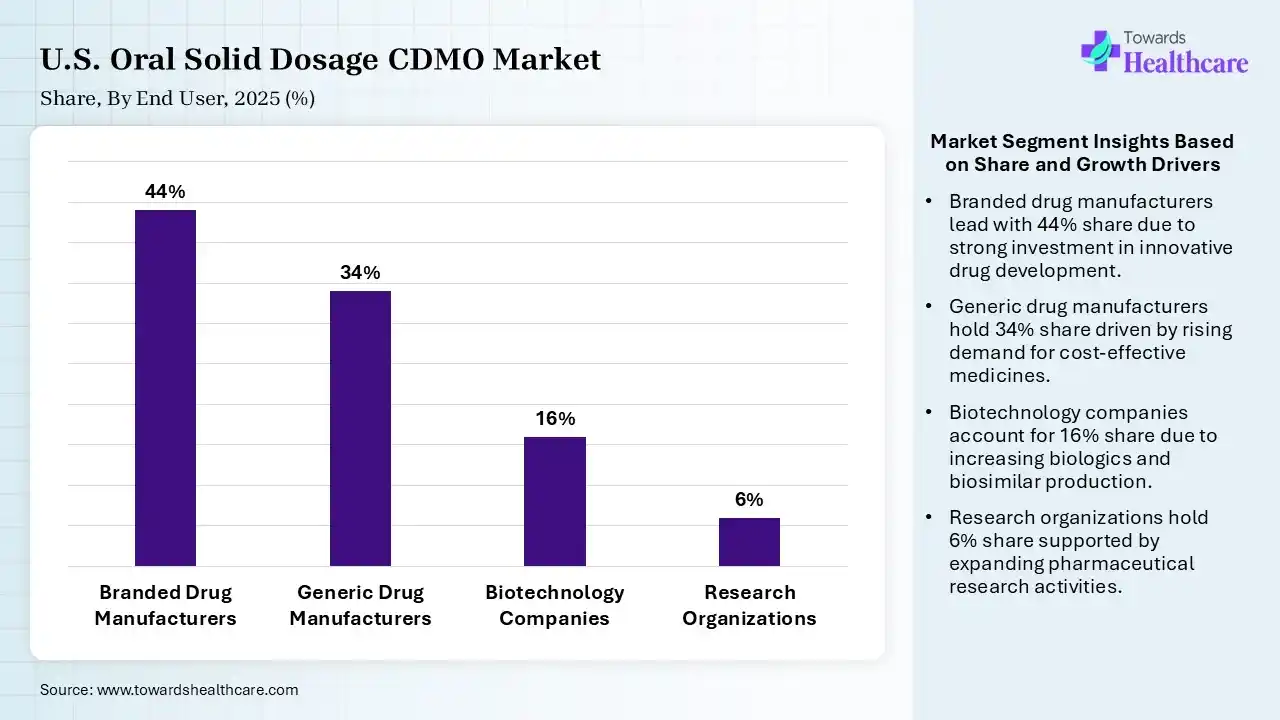

| Segment | Share 2025 (%) |

| Branded Drug Manufacturers | 44% |

| Generic Drug Manufacturers | 34% |

| Biotechnology Companies | 16% |

| Research Organizations | 6% |

The Branded Drug Manufacturers Segment Dominated the Market With 44% in 2025

The branded drug manufacturers segment held the largest revenue share of 44% of the U.S. oral solid dosage CDMO market in 2025, driven by lifecycle management, which supported outsourcing. Product differentiation also increased specialized manufacturing. Additionally, global launches required scalable production, which increased the demand for oral solid dosage CDMOs.

The generic drug manufacturers segment held the second-largest share of 34% of the market in 2025, due to growing patent expirations, which are expanding generic opportunities. Cost-efficient manufacturing remains essential, which drives the use of oral solid dosage CDMO services. At the same time, large production volumes also sustain CDMOs.

The biotechnology companies segment held 16% of the U.S. oral solid dosage CDMO market share in 2025 and is expected to grow with the fastest CAGR of 7.86% during the forecast period, due to small-molecule biotech pipelines continuing to expand. Limited manufacturing infrastructure is also encouraging outsourcing. Growing innovation also accelerates new partnerships.

The research organizations segment held 6% of the market share in 2025, driven by early-stage development projects, which are increasing the demand for oral solid dosage CDMOs. Specialized manufacturing supports research, which also drives their use. Clinical programs require flexible production, encouraging their collaborations.

The U.S. oral solid dosage CDMO market held a significant share in 2025 and is expected to show lucrative growth during the forecast period, as large innovators and generic markets sustained their demand. An extensive CDMO infrastructure attracts investment, where strong drug development activity also increases its use. Growth in outsourcing trends and a rise in complexity in drug development also increase collaborations among the CDMOs. At the same time, increased demand for affordable and advanced manufacturing solutions is also increasing their use, where the demand for personalized medicine also promotes their adoption, which contributed to the market growth.

R&D

Packaging and Serialization

Patient Support and Services

| CDMOs | Headquarters | Oral Solid Dosage Forms |

| Catalent, Inc. | Somerset, U.S. | Zydis ODT, OptiShell, and OptiMelt |

| Aenova Group | Starnberg, Germany | Aenova Effer-Gran and SoluKey |

| Lonza Group AG | Basel, Switzerland | Capsugel, Colorectal-Targeted Caps, and Vcaps Plus |

| Cambrex Corporation | East Rutherford, U.S. | Cambrex HP-OSD and Cambrex MicroSphere |

| Thermo Fisher Scientific Inc. | Waltham, U.S. | Patheon Quadrant and Patheon Quick to Clinic |

| Piramal Pharma Solutions | Mumbai, India | Piramal InteliDose and Piramal SecureCore |

| Recipharm AB | Stockholm, Sweden | Recipharm Advance OSD and ReciCap |

In December 2025, after the announcement of a strategic alliance to provide end-to-end services for oral solid dose (OSD) development and manufacturing between Bora Pharmaceuticals Co., Ltd. and Corealis Pharma Inc., the President of Bora’s CDMO division, J.D. Mowery, stated that “This collaboration is all about bridging capability and culture.” “By combining Bora’s scale-up strength with Corealis’ early-phase expertise and leveraging the customer service and reliability focus of both organizations, we’re setting a new standard for CDMO collaboration.”

By Product Type

By Service Type

By Therapeutic Area

By Customer Type

By End User

By Drug Potency

By Manufacturing Scale

By Release Profile

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar