Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

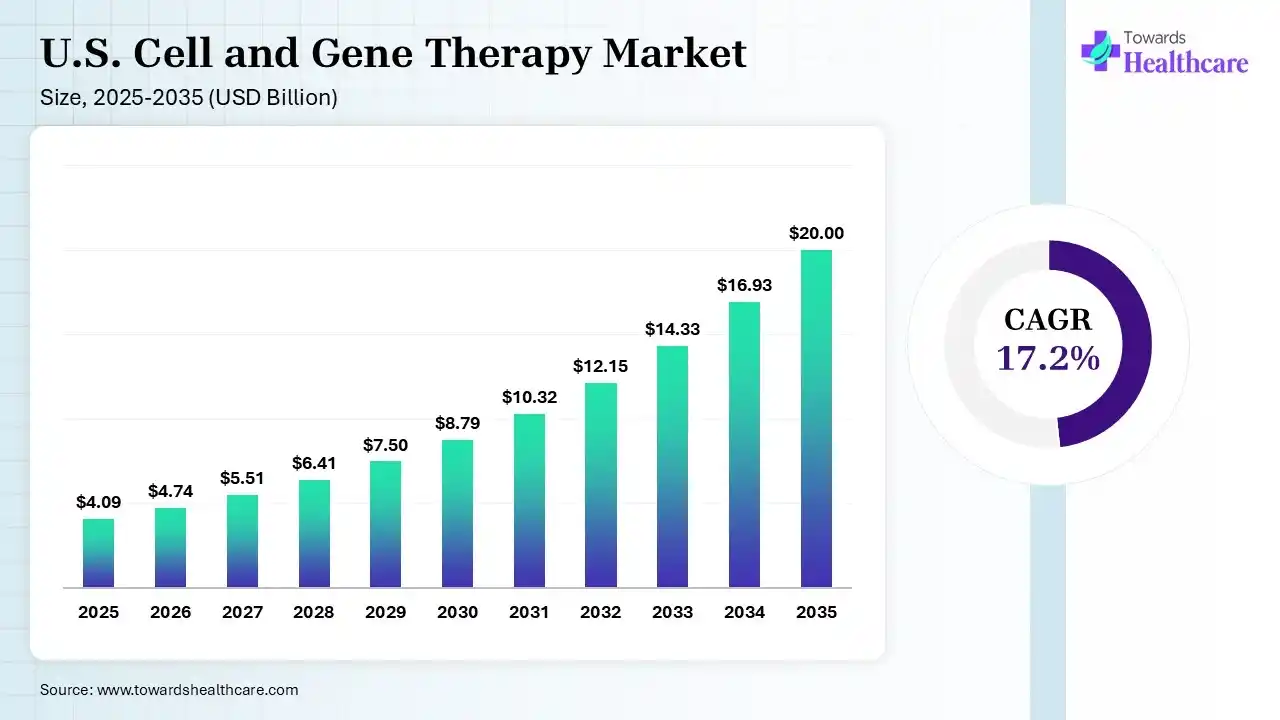

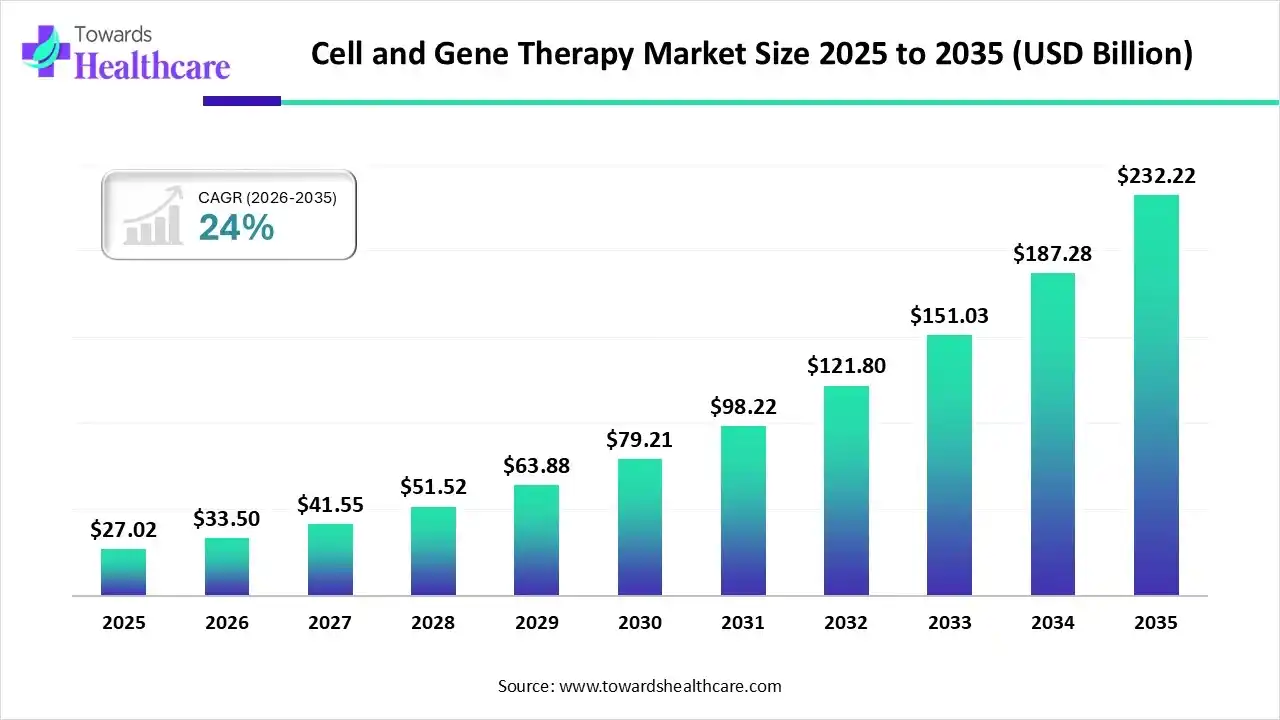

The U.S. cell and gene therapy market size was estimated at USD 4.09 billion in 2025 and is predicted to increase from USD 4.74 billion in 2026 to approximately USD 20 billion by 2035, expanding at a CAGR of 17.2% from 2026 to 2035. The market is rapidly expanding due to strong clinical innovation, increasing approvals of advanced therapies, and growing demand for curative treatments in oncology and rare genetic disorders. It is driven by heavy biotech investment, breakthroughs in gene editing and personalized medicine, and is positioned as a global leader in next-generation therapeutic development.

")

The U.S. cell and gene therapy market focuses on developing advanced treatments that modify or replace cells and genes to treat or cure diseases at their root cause. It is a rapidly growing sector driven by innovation in personalized medicines, especially for cancer and rare genetic disorders. The U.S. cell and gene therapy market is growing rapidly due to increasing approvals of advanced therapies, a strong pipeline of clinical trials, and rising demand for curative treatments in cancer and rare diseases. Significant investments from biotech and pharmaceutical companies, along with breakthroughs in gene editing and personalized medicine, further accelerate innovation, while supportive regulatory frameworks and advanced healthcare infrastructure strengthen market expansion.

| Treatment Type | Approx % of Curative Impact |

| Traditional treatment (Surgery, chemo, radiation-early stage) | 60-70% |

| Targeted/ Precision therapies | 5% |

| Immunotherapy (CAR-T) | 10-15% |

| Overall, the advanced-stage curative impact | <10% |

The U.S. cell and gene therapy market focuses on developing advanced therapies that modify or replace cells and genetic material to treat, prevent, or potentially cure cancer, rare genetic disorders, autoimmune diseases, and other complex conditions. The market is expanding due to increasing regulatory approvals, growing investments in biotechnology, and a robust pipeline of innovative therapies. Rising demand for personalized medicine, strong clinical trial activity, and expanding manufacturing capabilities are further driving growth. Technological advancements, including CRISPR-based gene editing, next-generation viral vectors, automated cell processing, AI-enabled therapy development, and advanced bioprocessing platforms, are improving therapeutic precision and production efficiency. Key trends include the shift toward allogeneic therapies and scalable manufacturing. Future opportunities lie in in vivo gene editing, regenerative medicine, novel delivery technologies, and expanded applications across chronic, neurological, and inherited diseases, supported by continuous research and commercialization efforts.

AI is transforming the market by accelerating drug discovery, optimizing clinical trial design, and improving patient selection through predictive analytics. It enhances manufacturing efficiency and quality control, reducing costs and timelines. AI-driven insights also support personalized treatment development, increasing success rates and enabling faster commercialization of advanced therapies.

Shift Toward Personalized & Precision Therapies

The market is increasingly focused on patient-specific treatments, including autologous cell therapies and targeted gene editing. Advances in precision medicine are improving treatment efficacy, especially in oncology and rare genetic disorders, driving demand for customized therapeutic solutions.

Expansion of Manufacturing & Commercial Scale-Up

Companies are investing in automated, scalable manufacturing technologies to meet rising demand and reduce costs. Innovations in vector production, cell processing, and supply chain optimization are improving accessibility and supporting the transition from clinical trials to large-scale commercialization.

Integration of Advanced Technologies like AI & Gene Editing

The adoption of AI, CRISPR, and next-generation platforms is accelerating research and development. These technologies enhance target identification, streamline trials, and improve success rates, positioning the U.S. as a leader in next-generation therapeutic innovation and future market growth.

| Table | Scope |

| Market Size in 2026 | USD 4.74 Billion |

| Projected Market Size in 2035 | USD 20 Billion |

| CAGR (2026 - 2035) | 17.2% |

| Key Applications | Oncology, Rare Genetic Disorders, Hematology, Neurology, Ophthalmology, Cardiovascular Diseases, Infectious Diseases |

| Primary End Users | Hospitals, Specialty Clinics, Cancer Centers, Academic Medical Centers, Research Institutes |

| Key Challenges | High manufacturing costs, reimbursement barriers, regulatory complexity, supply chain constraints, scalability issues |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Therapy Type, By Indication/Therapeutic Area, By Vectors Type, By Manufacturing Type, By End Use |

| Top Key Players | Alnylam Pharmaceuticals Inc., Amgen Inc., Biogen Inc, Dendreon Pharmaceuticals LLC., Helixmith Co. Ltd. |

")

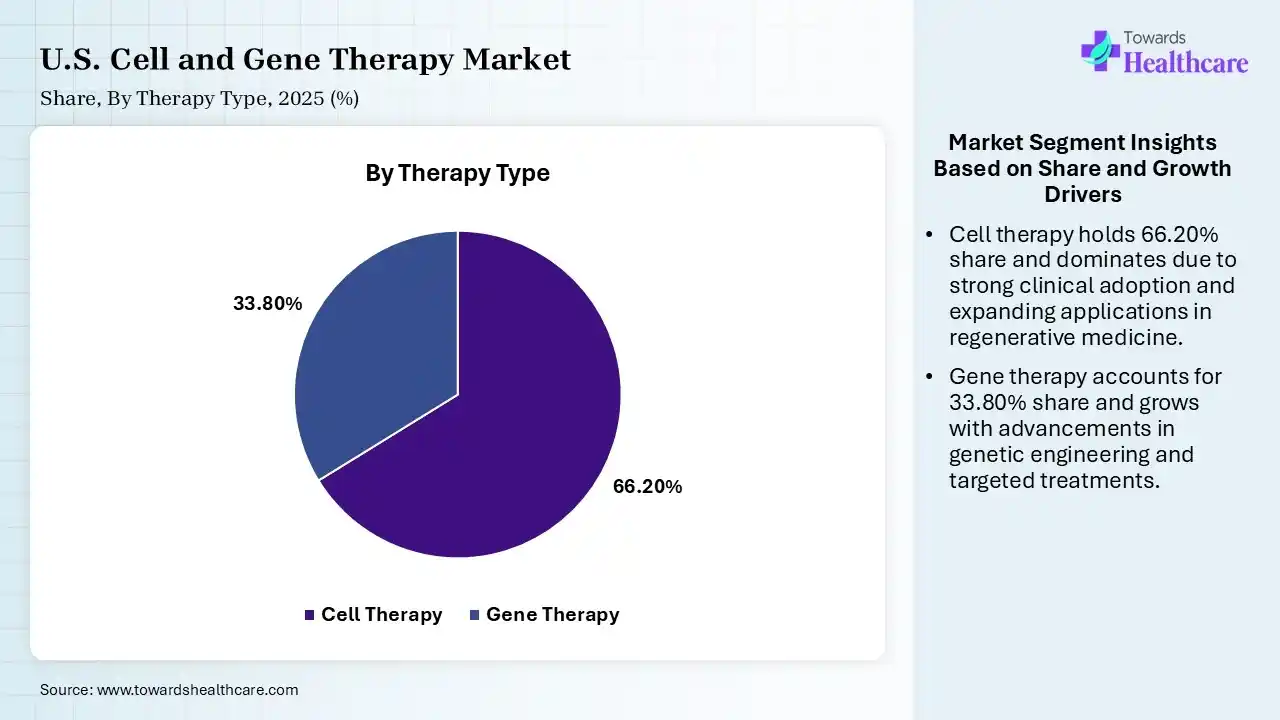

| Segment | Share 2025 (%) |

| Cell Therapy | 66.20% |

| Gene Therapy | 33.80% |

The Cell Therapy Segment Dominated the Market in 2025

The cell therapy segment dominated the U.S. cell and gene therapy market with shares of 66.20% in 2025 due to the higher number of approved therapies. particularly in oncology, and the strong clinical success of treatments like CAR-T. Increased adoption in hospitals, growing investment in regenerative medicines, and faster commercialization compared to gene therapies further supported its leadership, while expanding applications across multiple disease areas strengthened its market share.

The gene therapy segment held the second-largest share of 33.80% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to growing approvals of innovative, one-time treatments targeting rare genetic disorders and chronic conditions. Strong clinical pipelines, increasing investment in gene-editing technologies, and rising awareness of long-term therapeutic benefits supported its expansion. Additionally, improving regulatory support and advancements in viral vector delivery systems further strengthened its adoption across specialized treatment areas.

")

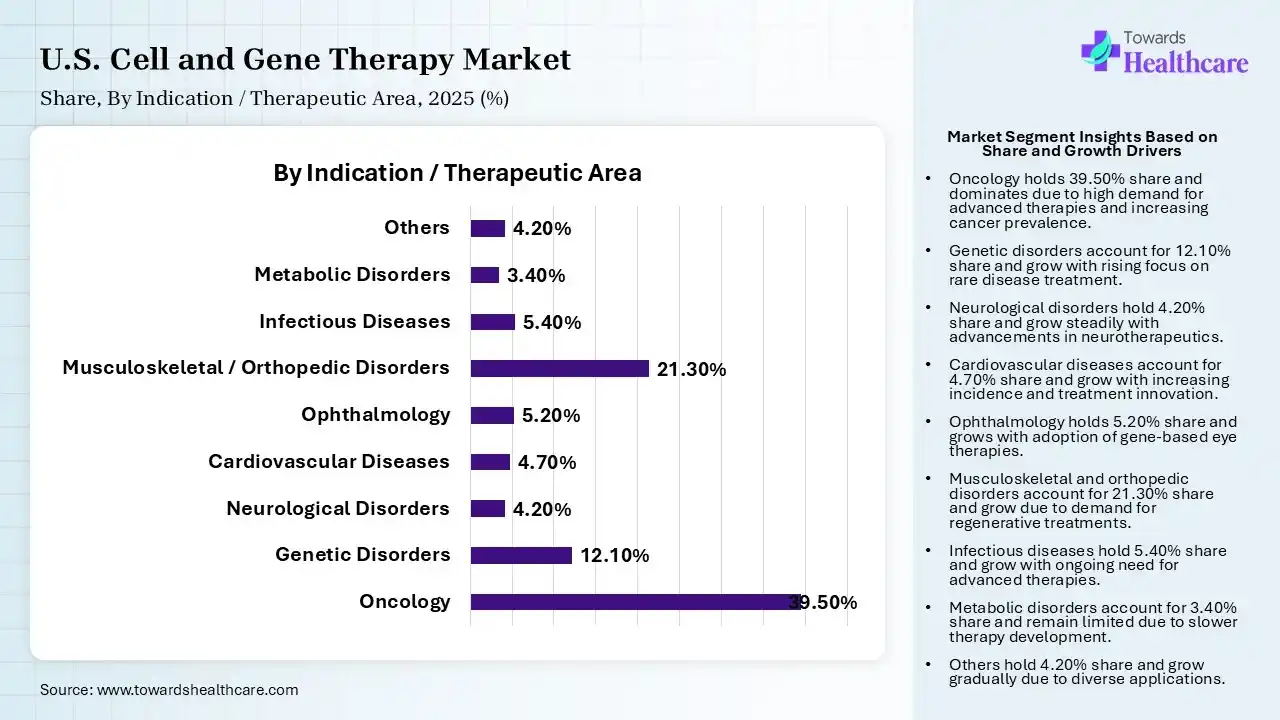

| Segment | Share 2025 (%) |

| Oncology | 39.50% |

| Genetic Disorders | 12.10% |

| Neurological Disorders | 4.20% |

| Cardiovascular Diseases | 4.70% |

| Ophthalmology | 5.20% |

| Musculoskeletal / Orthopedic Disorders | 21.30% |

| Infectious Diseases | 5.40% |

| Metabolic Disorders | 3.40% |

| Others | 4.20% |

The Oncology Segment Led the Market in 2025 with the Largest Share

The oncology segment held a dominant share in the U.S. cell and gene therapy market of 39.50% in 2025 due to the high prevalence of cancer and strong demand for advanced, targeted treatments. Significant success of cell therapies like CAR-T, extensive clinical pipelines, and continuous approvals accelerated adoption. Additionally, substantial investments from biotech and pharmaceutical companies, along with favorable reimbursement and regulatory support, further strengthened oncology’s dominant position in the market.

The musculoskeletal/orthopedic disorders segment held the second-largest share of 21.30% in 2025 due to the high prevalence of conditions like osteoarthritis, osteoporosis, and sports injuries. Growing demand for regenerative therapies, including stem cell-based treatments, is driving adoption. Increased aging populations, rising orthopedic procedures, and continuous research in tissue engineering repair further support the strong growth and expansion of this segment.

The genetic disorders segment held 12.10% share in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to increasing focus on curative gene therapies targeting rare and inherited diseases. Advancements in gene editing technologies, expanding clinical pipelines, and rising regulatory approvals are accelerating development. Additionally, growing investments, improved diagnostic capabilities, and strong demand for long-term treatment solutions are driving rapid adoption in this segment.

The infectious disease segment held 5.40% of the U.S. cell and gene therapy market share in 2025 due to increasing focus on advanced therapies for viral infections, including HIV and emerging pathogens. Rising demand for long-lasting and potentially curative treatment, along with expanding research in gene-modified immune cells and antiviral gene therapies, is driving growth. Additionally, heightened awareness after global outbreaks and increased funding for infectious disease innovation are accelerating development and adoption in this segment.

, 2025 (%)")

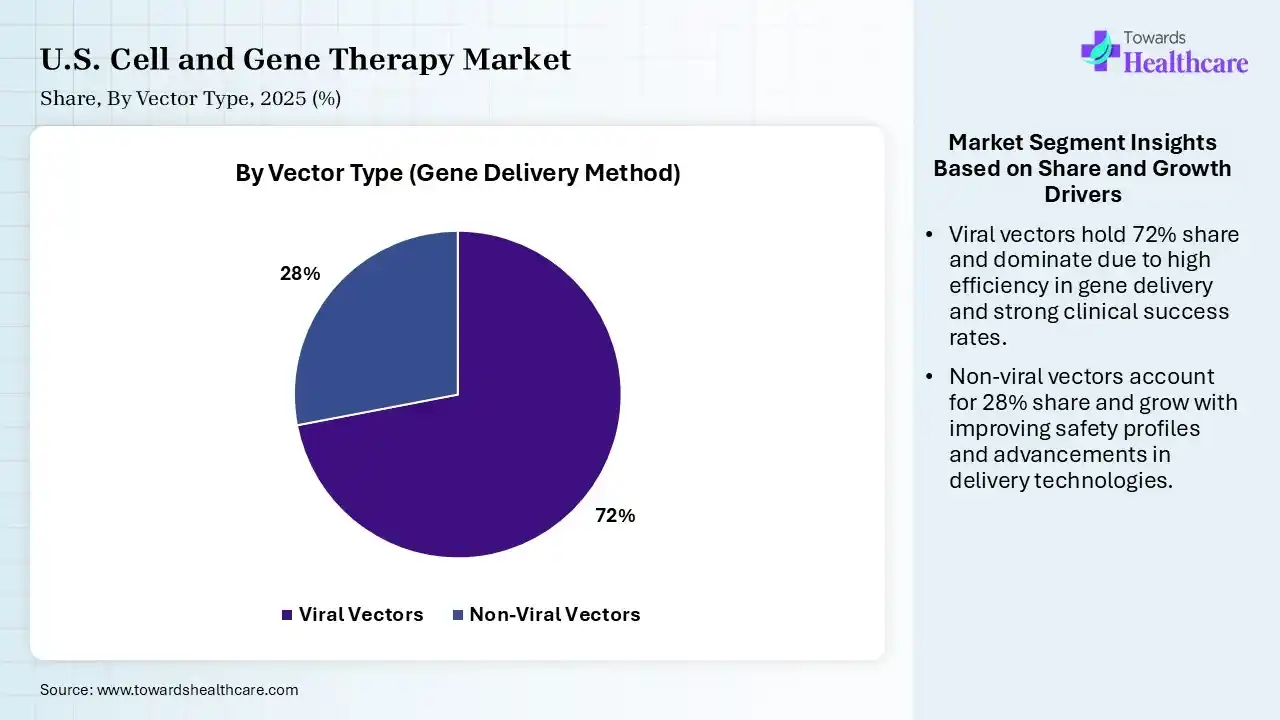

| Segment | Share 2025 (%) |

| Viral Vectors | 72% |

| Non-Viral Vectors | 28% |

The Viral Vectors Segment Led the Market in 2025 with the Largest Share

The viral vectors segment held a dominant share of 72% in the U.S. cell and gene therapy market in 2025 due to their high efficiency in delivering genetic material into target cells and proven success in approved gene therapies. Strong clinical validation, especially with adeno-associated and lentiviral vectors, supported widespread adoption. Additionally, well-established manufacturing processes, regulatory familiarity, and their ability to enable long-term gene expression made viral vectors the preferred choice over non-viral alternatives.

The non-viral vectors segment held the second-largest share of 28% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to its advantages in safety, lower immunogenicity, and reduced risk of insertional mafugenesis compared to the viral system. Growing research in liquid nanoparticles and polymer-based delivery, along with easier manufacturing and scalability, supported adoption. Additionally, increasing use in mRNA therapies and gene editing applications further strengthened its position in the market.

")

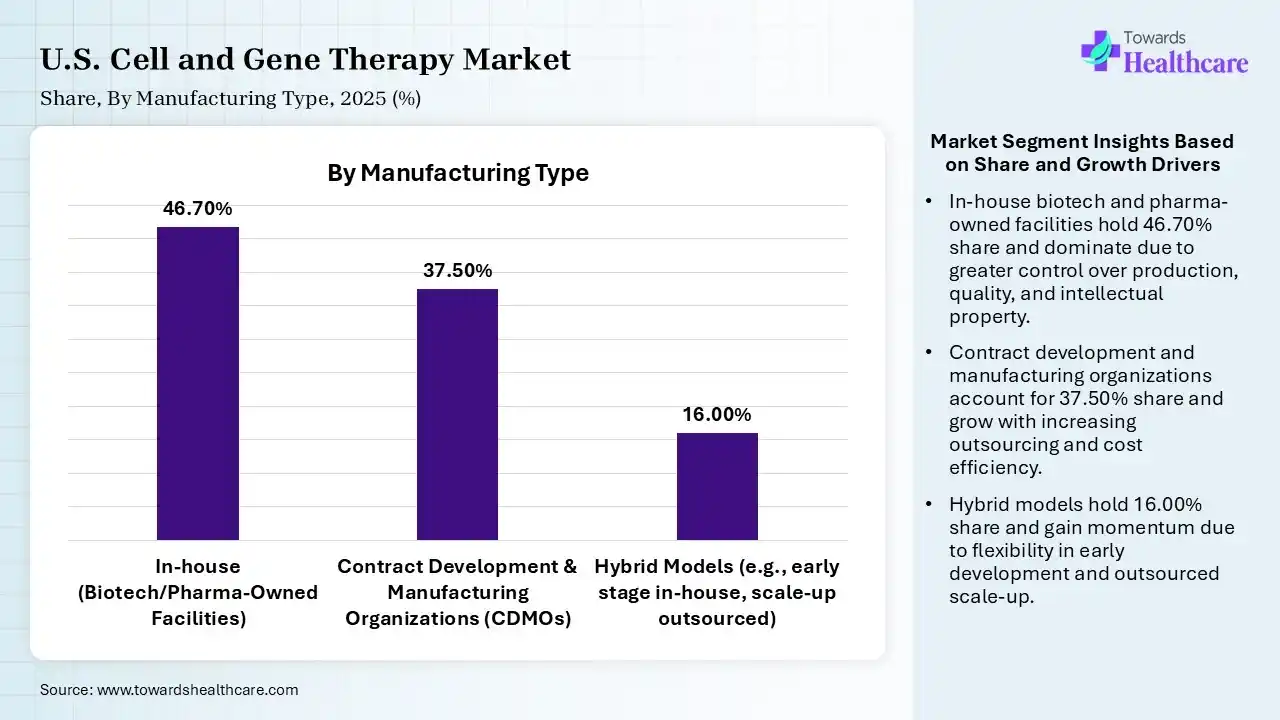

| Segment | Share 2025 (%) |

| In-house (Biotech/Pharma-Owned Facilities) | 46.70% |

| Contract Development & Manufacturing Organizations (CDMOs) | 37.50% |

| Hybrid Models (e.g., early stage in-house, scale-up outsourced) | 16.00% |

The In-house Segment held a Dominant Position in the Market in 2025

The in-house segment held a dominant share of 46.70% in the U.S. cell and gene therapy market in 2025 due to the need for strict quality control, intellectual property protection, and process standardization in complex cell and gene therapy manufacturing. Companies prefer internal production to ensure consistency, reduce dependency on third parties, and accelerate timelines. Additionally, large investments in dedicated manufacturing infrastructure and capacity expansion further strengthened its dominance in in-house operations.

The contract development & manufacturing (CDMO) segment held the second-largest share of 37.50% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to rising outsourcing by biotech firms lacking in-house capabilities. CDMOs offer specialized expertise, flexible capacity, and cost-effective production for complex therapies. Increasing clinical trials activity, scalability needs, and faster time-to-market further drove demand, while partnership between pharma companies and CDMOs strengthened their role in the cell and gene therapy value chain.

The hybrid models segment held 16% of the U.S. cell and gene therapy market share in 2025 as companies seek a balance between in-house control and outsourced flexibility. It allows firms to maintain critical processes internally while leveraging CDMOs for scalability and cost efficiency. This approach supports risk mitigation, faster commercialization, and optimized capacity utilization. Additionally, the increasing complexity of cell and gene therapies is driving the adoption of hybrid strategies to enhance operational efficiency and supply chain resilience.

")

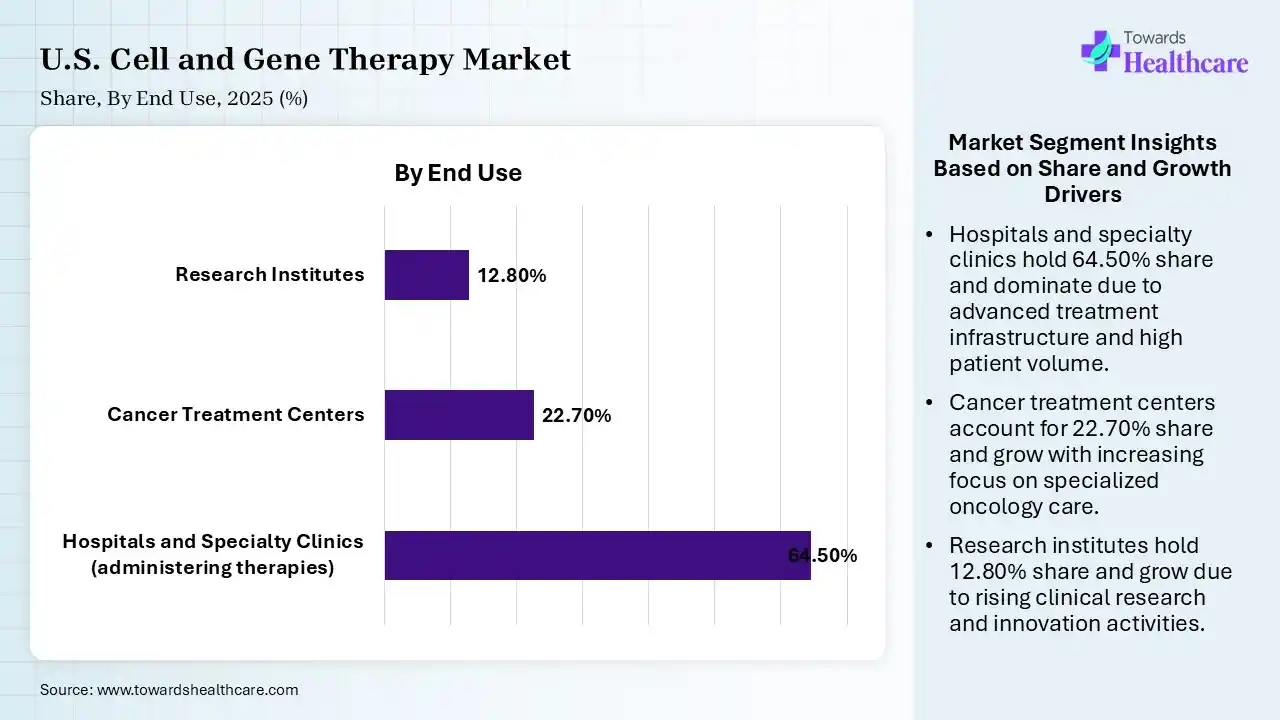

| Segment | Share 2025 (%) |

| Hospitals and Specialty Clinics (administering therapies) | 64.50% |

| Cancer Treatment Centers | 22.70% |

| Research Institutes | 12.80% |

The Hospitals and Specialty Clinics Segment Dominated the Market in 2025

The hospitals and specialty clinics segment led the U.S. cell and gene therapy market with a share of 64.50% in 2025 due to their advanced infrastructure and ability to handle complex cell and gene therapies requiring specialized administration and monitoring. These facilities have skilled professionals, access to critical care, and established treatment protocols. Additionally, higher patient inflow, availability of reimbursement support, and integration with clinical trials further strengthen their leading role in therapy delivery and adoption.

The cancer treatment centers segment held the second-largest share of 22.70% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to the high concentration of oncology patients and increasing adoption of advanced therapies like CAR-T. These centers offer specialized expertise, dedicated infrastructure, and access to clinical trials. Additionally, rising cancer incidence, growing focus on personalized treatment, and collaborations with biotech firms are driving greater utilization of cell and gene therapies in these settings.

The research institutes segment held 12.80% of the U.S. cell and gene therapy market share in 2025 due to increasing focus on early-stage discovery and translational research in cell and gene therapies. Rising funding from government and private organizations, along with growing academic industry collaboration. is accelerating innovation. These institutes play a key role in clinical trials development, biomarker discovery, and technology, driving pipeline growth and supporting long-term market expansion.

The cell and gene therapy market size touched US$ 8.94 billion in 2025, with expectations of climbing to US$ 10.44 billion in 2026 and hitting US$ 47.18 billion by 2035, driven by a CAGR of 18.1% over the forecast period.

")

The U.S. cell and gene therapy market leads globally due to its advanced biotechnology ecosystems, strong investments in research and development, and a high concentration of innovative biopharmaceutical companies. Extensive clinical trials activity, early adoption of cutting-edge gene editing technologies, and well-established manufacturing infrastructure further strengthen market leadership. Additionally, supportive regulatory pathways and continuous innovation in personalized medicine continue to accelerate the development and commercialization of advanced cell and gene therapies.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | CRISPR Therapeutics, Editas Medicine, Beam Therapeutics | Gene-editing platforms and therapeutic development technologies |

| Product Manufacturers | Novartis, Gilead Sciences/Kite, Bristol Myers Squibb, Bluebird Bio | Commercial production of approved cell and gene therapies |

| Service Providers | AmerisourceBergen, McKesson, EVERSANA | Distribution, patient support, commercialization services |

| Platform Providers | 2seventy bio, Adaptimmune, Sana Biotechnology | Cell engineering and therapeutic development platforms |

| CROs/CDMOs | Lonza, Catalent, Charles River Laboratories, WuXi Advanced Therapies | Clinical development and manufacturing support |

| Software Vendors | Veeva Systems, IQVIA, Medidata | Clinical trial management, data analytics, regulatory software |

| Research Institutions | University of Pennsylvania, Memorial Sloan Kettering Cancer Center, MD Anderson Cancer Center, Stanford University | Research, translational medicine, clinical trials |

| End-User Industries | Hospitals, Cancer Centers, Specialty Clinics, Academic Medical Centers | Administration and monitoring of therapies |

In May 2026, “It has been an honor to serve as Allogene’s CEO for the past eight years,” said Dr. Chang. “As we enter the Company’s next phase, now is the right time for a leadership transition, and Zach is the right person to lead Allogene forward. He is a deeply respected physician-scientist and energizing leader with a clear vision for how emerging technologies can continue to expand the potential of allogeneic CAR T.”

Clinical Trials

Regulatory Approvals

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 62% | 26% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Novartis AG | Basel | Switzerland | Pioneer in commercial CAR-T therapies with strong U.S. footprint | Kymriah, gene therapy programs |

| Gilead Sciences (Kite Pharma) | Foster City, California | USA | Leading U.S. CAR-T therapy provider | Yescarta, Tecartus |

| Bristol Myers Squibb | Princeton, New Jersey | USA | Major cell therapy player through Celgene acquisition | Breyanzi, Abecma |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Bluebird Bio | Somerville, Massachusetts | USA | Commercial gene therapy leader focused on rare diseases | Lyfgenia, Zynteglo, Skysona |

| Sarepta Therapeutics | Cambridge, Massachusetts | USA | Strong gene therapy franchise in neuromuscular diseases | Elevidys, gene therapy pipeline |

| BioMarin Pharmaceutical | San Rafael, California | USA | Commercial gene therapy developer | Roctavian |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Beam Therapeutics | Cambridge, Massachusetts | USA | Pioneer in base-editing technology | Base-editing therapeutics |

| Editas Medicine | Cambridge, Massachusetts | USA | Advanced CRISPR-based gene editing programs | EDIT platform |

| Intellia Therapeutics | Cambridge, Massachusetts | USA | In vivo gene editing innovator | NTLA gene-editing pipeline |

Strengths

Weaknesses

Opportunities

Threats

By Therapy Type

By Indication/Therapeutic Area

By Vectors Type

By Manufacturing Type

By End Use

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar