Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

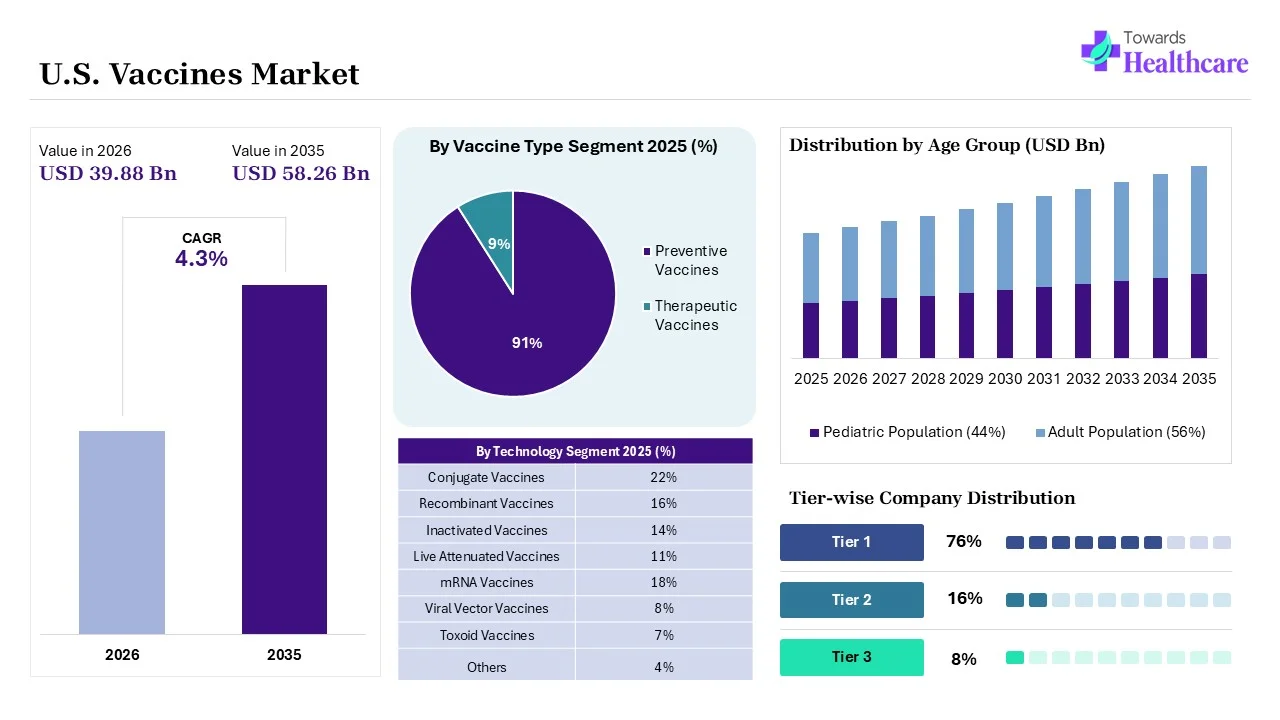

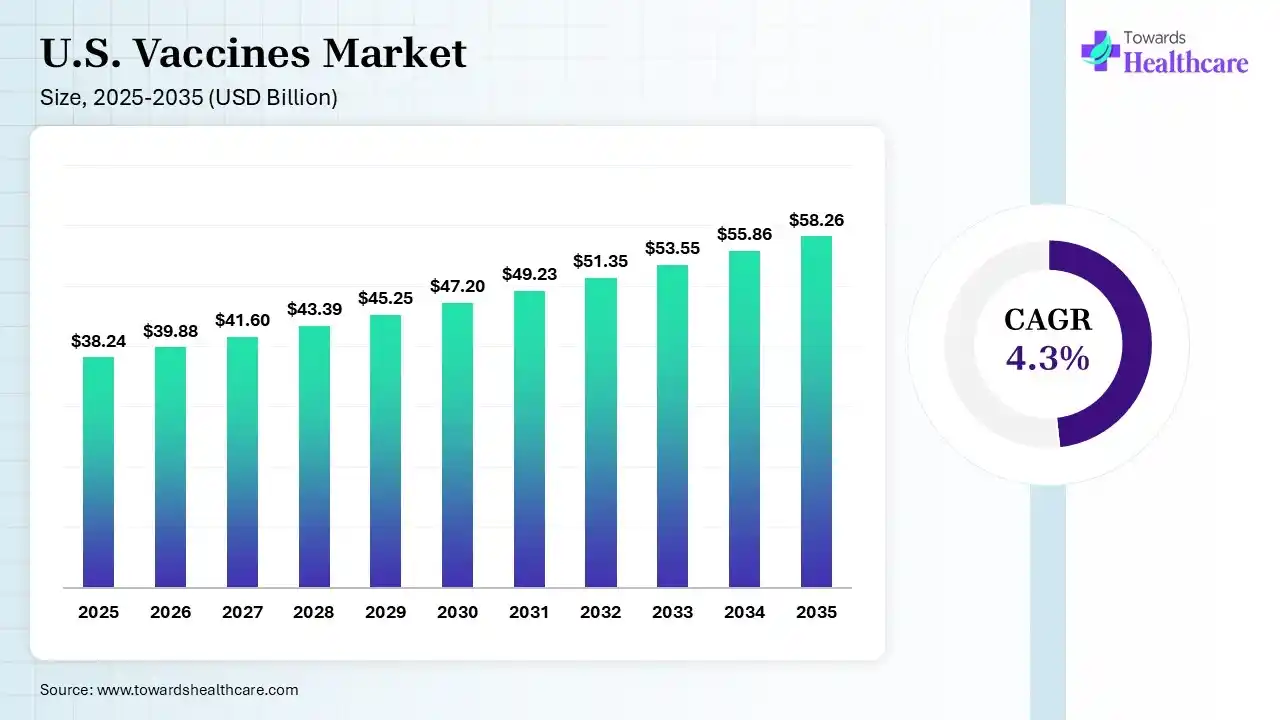

The U.S. Vaccines market size touched US$ 38.24 billion in 2025, with expectations of climbing to US$ 39.88 billion in 2026 and hitting US$ 58.26 billion by 2035, driven by a CAGR of 4.3% over the forecast period.

")

The U.S. vaccines market comprises the research, development, manufacturing, distribution, and administration of vaccines designed to prevent infectious diseases across pediatric, adolescent, adult, and geriatric populations. The market includes routine immunizations, seasonal vaccines, travel vaccines, and emerging preventive solutions targeting viral, bacterial, and other infectious threats. Strong government support, advanced healthcare infrastructure, and high awareness regarding disease prevention continue to drive market expansion.

National immunization programs, school vaccination requirements, and widespread access through hospitals, pharmacies, clinics, and public health agencies contribute significantly to vaccine uptake. Growing concerns regarding infectious disease outbreaks, coupled with increasing emphasis on preventive healthcare, have strengthened demand for both established and newly developed vaccines.

Technological advancements in vaccine development, including mRNA platforms, recombinant technologies, and next-generation adjuvants, are accelerating innovation and improving vaccine efficacy, safety, and scalability. Additionally, rising investments in pandemic preparedness and public health resilience are creating favorable conditions for sustained market growth.

The U.S. vaccines market is experiencing notable trends, including the expansion of adult immunization programs, increasing adoption of combination vaccines, and growing utilization of digital tools for vaccine tracking and patient engagement. Opportunities are emerging from the development of vaccines targeting respiratory infections, antimicrobial resistance-related pathogens, cancer prevention, and rare infectious diseases.

Pharmaceutical companies are increasingly focusing on personalized vaccine approaches and platform technologies that enable faster responses to evolving health threats. Strategic collaborations among biotechnology firms, government agencies, academic institutions, and healthcare providers are fostering research advancements and strengthening manufacturing capabilities. The integration of artificial intelligence, genomics, and data analytics into vaccine discovery processes is further enhancing innovation efficiency.

Rising healthcare expenditures, favorable reimbursement frameworks, and continuous public health initiatives are expected to support long-term market expansion. As the nation prioritizes disease prevention and preparedness, the U.S. vaccine market is anticipated to remain a global leader in vaccine innovation, production, and accessibility, creating substantial opportunities for stakeholders throughout the healthcare ecosystem over the coming decade.

Integration of AI-based technology in vaccine development has evolved as a transformative force, reforming the traditional paradigms of immunization research and deployment. AI-based technology has evolved as a revolutionary tool in vaccine research and advancement. AI-based algorithms with experimental validation and healthcare testing, scientists expedite the vaccine advancement technology.

Integration of AI-based technology in vaccine development characterizes a transformative leap forward, expediting the process, improving precision, and broadening understanding of infectious diseases. AI-driven is changing vaccine advancement by lowering timelines, improving precision, and growing efficacy and safety. The incorporation of artificial intelligence in vaccination programs shows a transformative technology address various health challenges.

| Table | Scope |

| Market Size in 2026 | USD 39.88 Billion |

| Projected Market Size in 2035 | USD 58.26 Billion |

| CAGR (2026 - 2035) | 4.3% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Vaccine Type, By Technology, By Route of Administration, By Age Group, By Disease Indication, By End User, By Distribution Channel |

| Top Key Players | Pfizer, Moderna, Merck, Sanofi, GlaxoSmithKline |

")

| Segment | Share 2025 (%) |

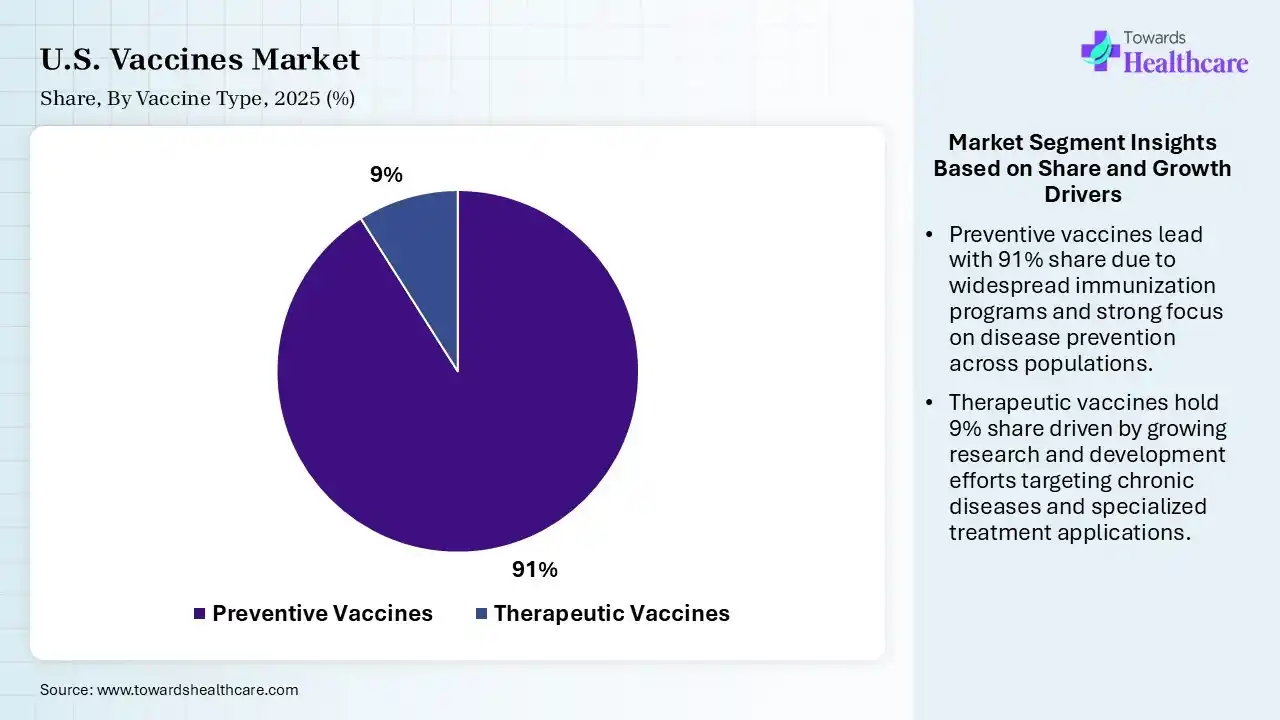

| Preventive Vaccines | 91% |

| Therapeutic Vaccines | 9% |

The Preventive Vaccines Segment Led the U.S. Vaccines Market in 2025

The preventive vaccines segment contributed the largest market share of 91% in 2025, as this vaccine contributed positively to immune fitness, insecurely defined as the capability to adapt to external risks. This vaccine, which prevents measles, tuberculosis, diphtheria, pertussis, Hib, and Neisseria meningitis, prevents respiratory diseases. Preventive vaccines, such as those applied to protect against infectious diseases.

The therapeutic vaccines segment held a significant share of 9% in the market and is expected to grow at the fastest CAGR of 8.20% during the forecast period. This vaccine is one that is applied after infection arises; it aims to induce antiviral immunity to modify the course of the disease. Therapeutic vaccines are made to target cells or molecules related to non-communicable diseases (NDCs) rather than pathogens or cells infected with pathogens.

")

| Segment | Share 2025 (%) |

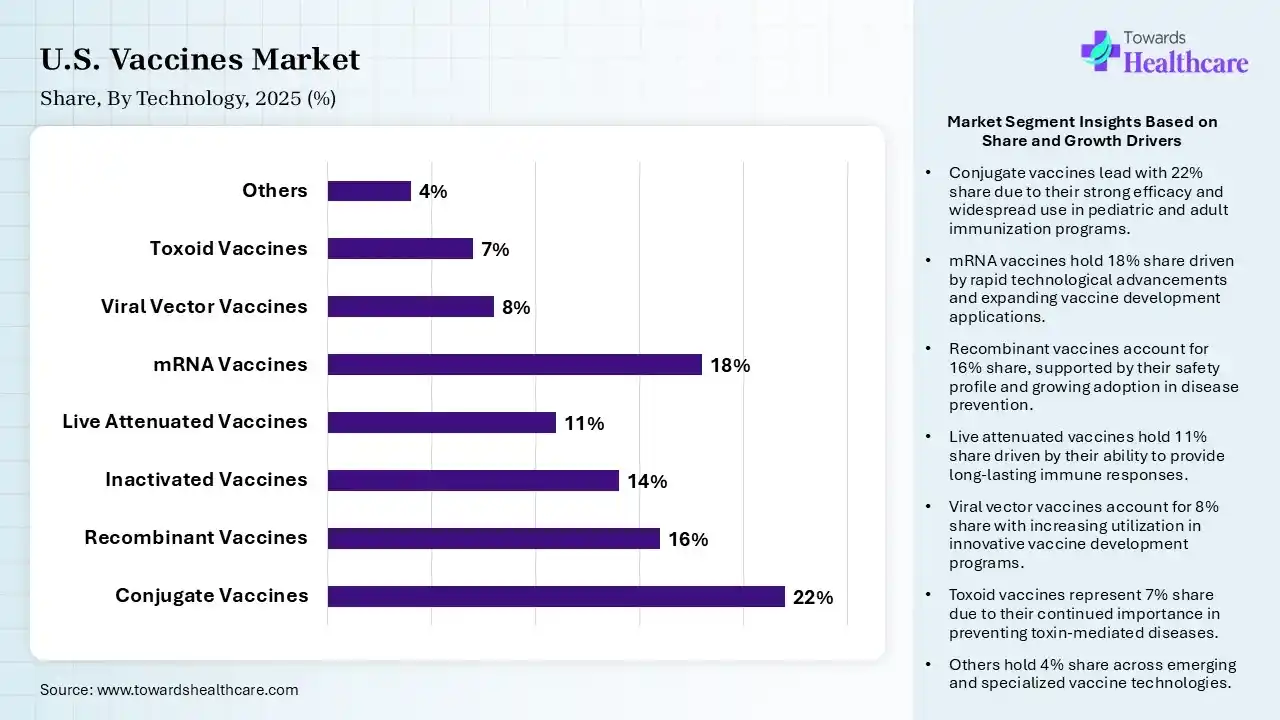

| Conjugate Vaccines | 22% |

| Recombinant Vaccines | 16% |

| Inactivated Vaccines | 14% |

| Live Attenuated Vaccines | 11% |

| mRNA Vaccines | 18% |

| Viral Vector Vaccines | 8% |

| Toxoid Vaccines | 7% |

| Others | 4% |

Conjugate Vaccines Segment Led the U.S. Vaccines Market in 2025

The conjugate vaccines segment contributed the largest market share of 22%, as this vaccine was developed to induce an advanced immune response against bacterial capsular polysaccharides (CPSs). Conjugate vaccines work by chemically connecting a polysaccharide antigen from bacteria to a transporter protein or peptide. Conjugate vaccines help immunological memory by enabling the polysaccharide to be accessible to the MHC on antigen-presenting cells to T cells.

The mRNA vaccines segment held a significant share of 18% of the market, and is expected to grow at the fastest CAGR of 9.80 % during the forecast period, as mRNA vaccines provide many advantages over traditional vaccines, involving the ease of their development, simple scale-up, and quick production. mRNA vaccines are their significantly limited advancement timeline as compared to traditional inactivated vaccines.

The recombinant vaccines segment held a significant share of 16% of the U.S. vaccines market, as this vaccine prevents infection risks due to its lack of live or inactivated viruses. Live recombinant bacteria or viral vectors efficiently stimulate the immune system, as in normal infections, and have intrinsic adjuvant characteristics. It has improved safety, rapid and more scalable production, targeted immune responses, and the capability to immunize without using the live pathogen.

The inactivated vaccines segment held a significant share of 14% of the market. It lowered manufacturing costs, improved the safety of the vaccine, and was comparatively straightforward to upscale. This type of vaccine is safe for pregnant and immunocompromised patients. There is no risk of vaccine-associated infection or shedding. Inactivated vaccines are composed of dead viruses and bacteria, enabling a safe process of immunising against these pathogens, as they do not behave as they usually do and cause disease.

")

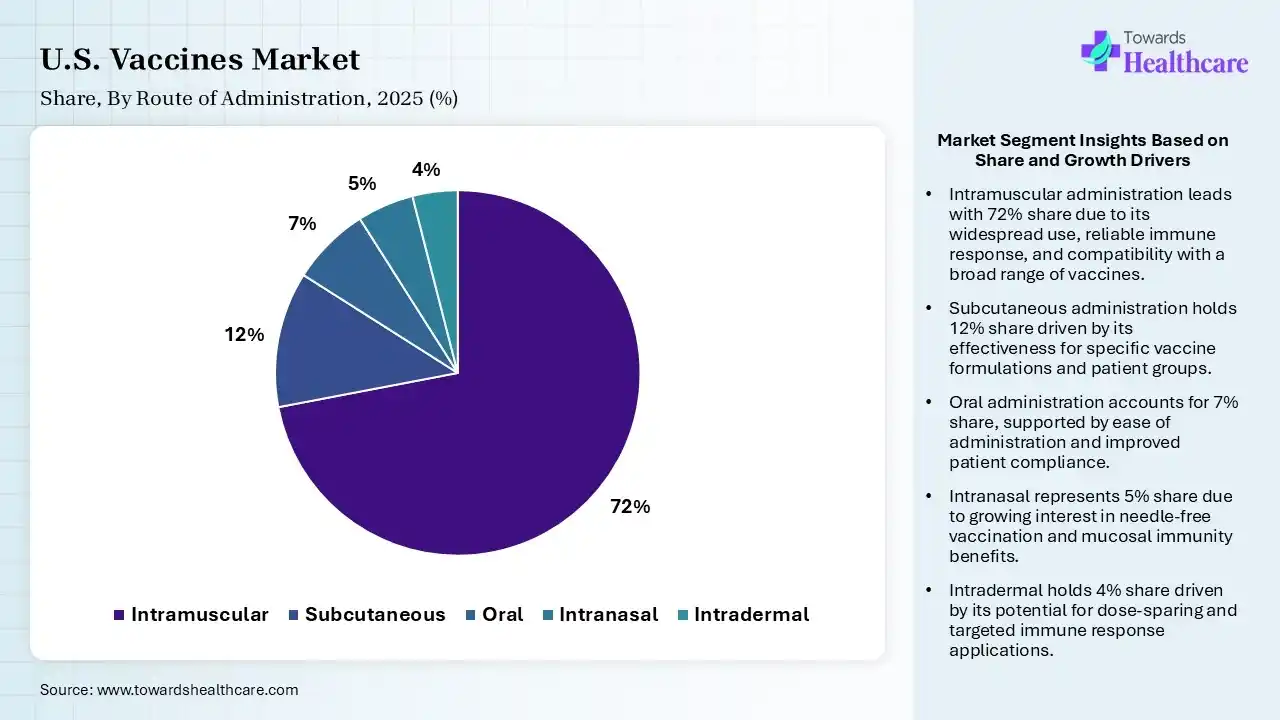

| Segment | Share 2025 (%) |

| Intramuscular | 72% |

| Subcutaneous | 12% |

| Oral | 7% |

| Intranasal | 5% |

| Intradermal | 4% |

The Intramuscular Segment led the U.S. Vaccines Market in 2025

The intramuscular segment held a significant share of 72% in the market. The intramuscular route delivers medications to the depth of precisely selected muscles. The huge muscles have significant vascularity, and so the injected drug rapidly reaches the systemic circulation and afterward in the particular area of action, avoiding the first-pass metabolism.

The subcutaneous segment held a significant 12% share of the market, as subcutaneous drug delivery provides a patient-approachable, less invasive process for medication administration, enhancing patient comfort. The subcutaneous route involves its simplicity and lack of need for vascular access, with its related risk of problems.

The oral segment held a significant share of 7% in the market, as oral administration of therapeutics is a convenient, affordable, and most commonly used medication administration route. The oral route is the most acceptable route of administration, including about 60% of existing small-molecule drug therapeutics.

The intranasal segment contributed a market share of 5% and is expected to grow at the fastest CAGR of 7.10% during the forecast period. It’s simple to administer, has a quick onset of action, and avoids first-pass metabolism, which consequently provides an interesting alternative to oral transmucosal, subcutaneous, intravenous, oral, or rectal administration in the management of pain associated with opioids. It provides increasing permeability, more vasculature, and fewer contacts with enzymes because of less nasal space.

")

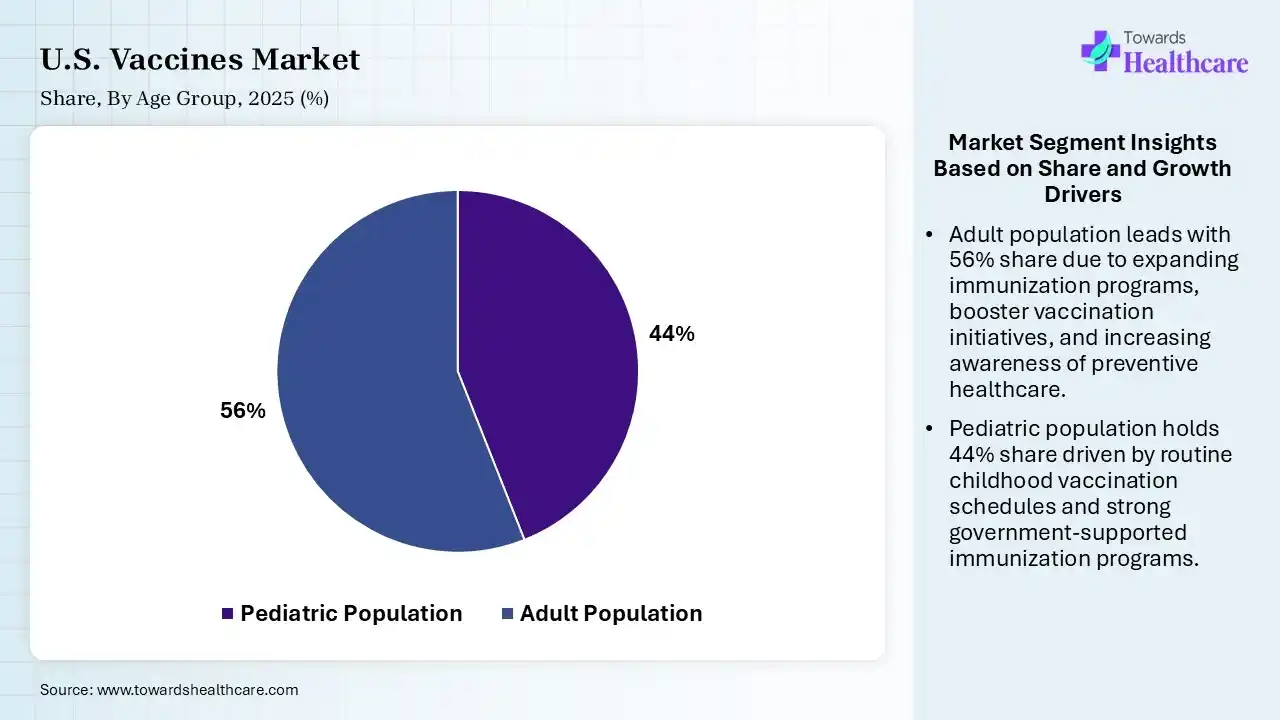

| Segment | Share 2025 (%) |

| Pediatric Population | 44% |

| Adult Population | 56% |

The Adult Population Segment led the U.S. Vaccines Market in 2025

The adult population segment contributed the largest market share of 56%, and is expected to grow at the fastest CAGR of 5.10% during the forecast period as vaccines support to prevent deadly diseases which sicken or kill and have killed major patients. Vaccines are severely tested and undergo numerous rounds of identification study and research before they are released and applied for the general public.

The pediatric population segment held a significant share of 44% in the market, as vaccines are found to be the most affordable strategies for lowering childhood disease load, specifically compared with interventions like clean water and enhanced sanitation, which lower disease transmission. It supports to protect and child from major, serious, and significantly deadly diseases.

")

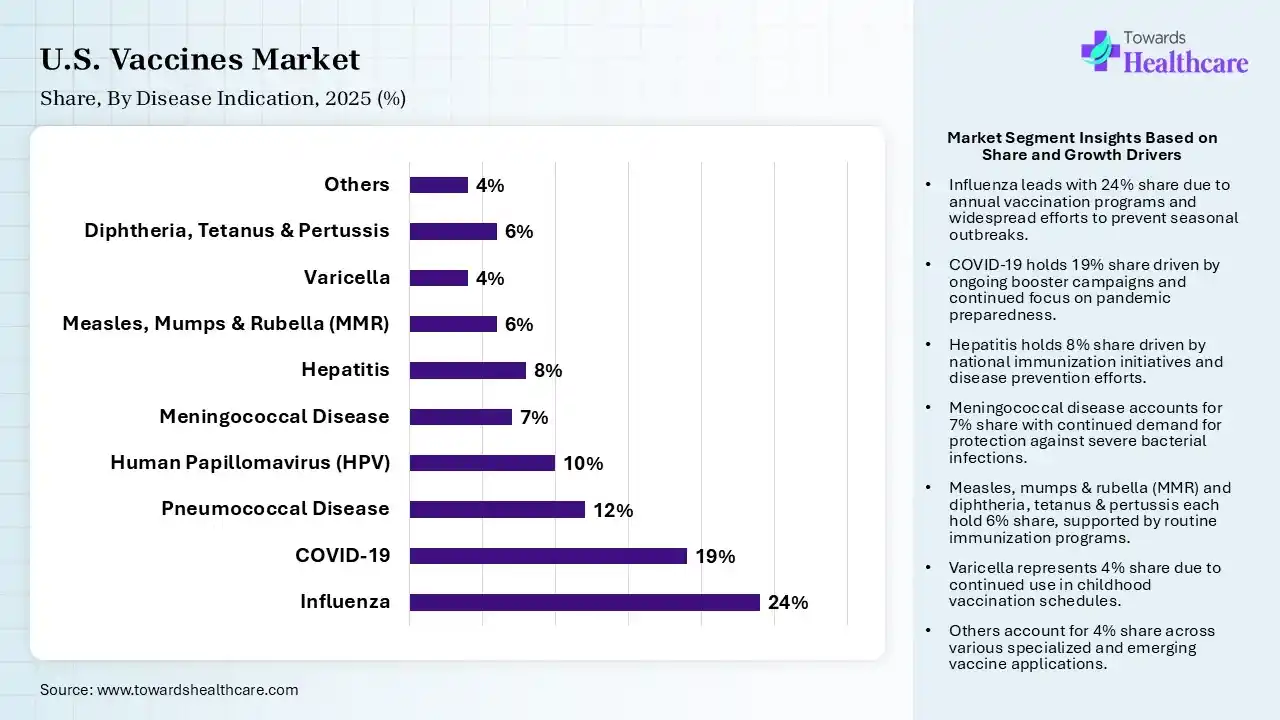

| Segment | Share 2025 (%) |

| Influenza | 24% |

| COVID-19 | 19% |

| Pneumococcal Disease | 12% |

| Human Papillomavirus (HPV) | 10% |

| Meningococcal Disease | 7% |

| Hepatitis | 8% |

| Measles, Mumps & Rubella (MMR) | 6% |

| Varicella | 4% |

| Diphtheria, Tetanus & Pertussis | 6% |

| Others | 4% |

The Influenza Segment led the U.S. Vaccines Market in 2025

The influenza segment contributed the largest market share of 24%. The influenza vaccine lowers the risk of getting influenza and the flu. The flu leads to fever, head and body aches, coughing, and a stuffy nose. It works by supporting the immune system to fight off future infection risks.

The COVID-19 segment held a significant share of 19% in the market, as vaccine supports to protect from serious illness, death, and hospitalization. The challenges of getting COVID-19 are higher for patients who are unvaccinated compared to those who are vaccinated. Vaccinated patients usually experience much rarer symptoms than those who are unvaccinated.

The pneumococcal disease segment held a significant share of 12% in the market, as pneumococcal vaccines help protect against pneumococcal infections, such as invasive disease. It lowers the chance of contracting and dying from pneumococcal disease. There are two types of pneumococcal vaccines, conjugate and polysaccharide, available in the U.S. region.

The other segment held a significant share of 4% in the market and is expected to grow at the fastest CAGR of 7 % during the forecast period, as vaccines are the most efficient way to prevent major infectious diseases. Vaccination saved more lives and prevented more serious diseases. Vaccines protect against life-challenging diseases such as tetanus, measles, and polio.

")

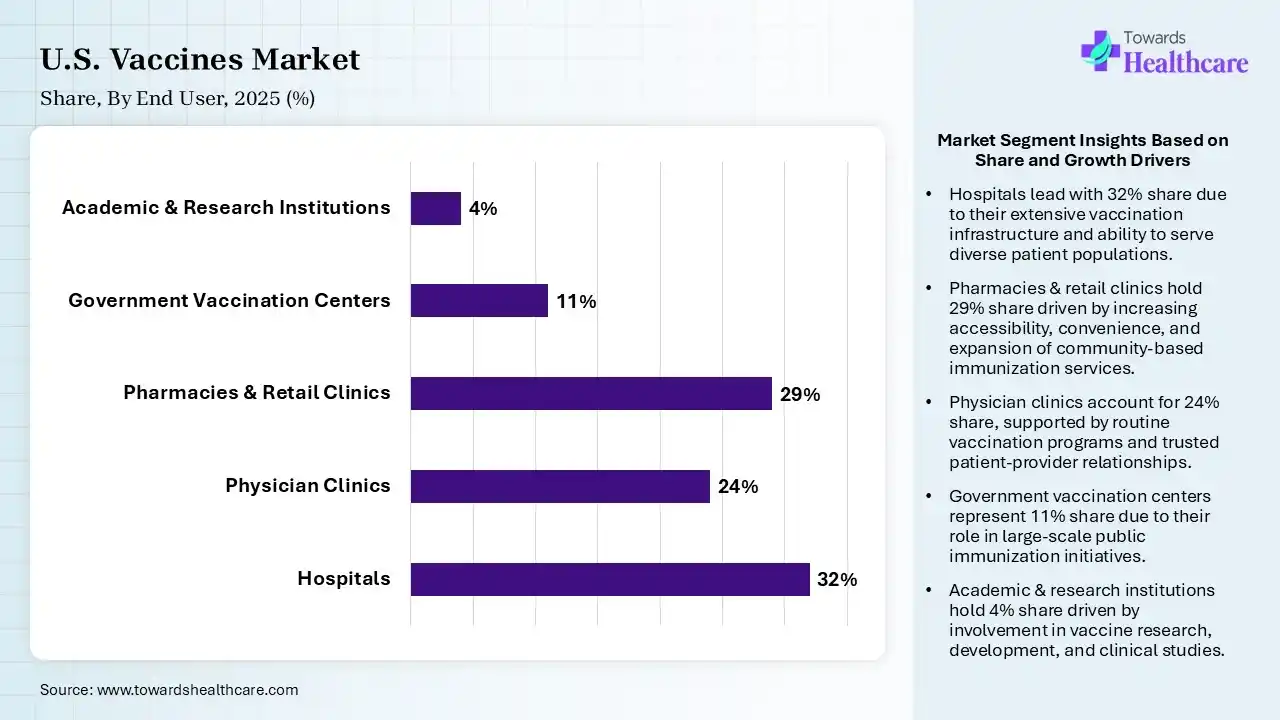

| Segment | Share 2025 (%) |

| Hospitals | 32% |

| Physician Clinics | 24% |

| Pharmacies & Retail Clinics | 29% |

| Government Vaccination Centers | 11% |

| Academic & Research Institutions | 4% |

The Hospitals Segment led the U.S. Vaccines Market in 2025

The hospitals segment contributed the largest market share of 32%, as vaccination is significant for avoiding infectious diseases beyond natural immunity. Vaccine-preventable diseases have not gone away. Vaccines contain either weakened or killed viruses, creating it impossible for vaccines to give the diseases they are intended to prevent.

The pharmacies & retail clinics segment held a significant share of 29% in the market and is expected to grow at the fastest CAGR of 6.50% during the forecast period, as it enhances public health access by offering unparalleled customer convenience, lowering the burden on primary care offices, and reducing overall societal healthcare expenses.

The physician clinics segment held a significant share of 24% in the U.S. vaccines market, as it offers a highly targeted, safe, and integrated medical care experience that massively outperforms the mass-distribution pharmacy sector. Physicians screen for suitability using the patient's inclusive healthcare records and unique contraindications.

The government vaccination centers segment held a significant share of 11% in the market, as these centers offer entirely subsidized, extremely regulated, and structurally monitored immunizations that remove financial challenges while ensuring supreme vaccine safety and quality.

The global vaccines market size is calculated at USD 84.97 billion in 2025, grew to USD 88.40 billion in 2026, and is projected to reach around USD 126.26 billion by 2035. The market is expanding at a CAGR of 4.04% between 2025 and 2035.

")

The U.S. vaccines market is driven by extensive immunization programs, adult vaccine expansion, and rapid innovation in mRNA, RSV, influenza, and combination vaccines. CDC data show RSV vaccination coverage among adults aged 75+ reached 43.2% by February 2026, while over 15.1 million RSV doses had been administered to adults aged 50+ by August 2025. Growing investments in next-generation vaccines, pandemic preparedness, and personalized immunization strategies continue strengthening market demand and product development.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Company | Headquarters | Latest Update |

| Pfizer | United States | In March 2026, Pfizer Inc. and Valneva SE announced topline results from the Phase 3 VALOR “Vaccine Against Lyme for Outdoor Recreationists” clinical trial of its new 6-valent OspA-driven Lyme disease vaccine candidate PF-07307405. |

| Moderna | United States | In June 2026, Moderna and other groups got $60 million to develop an Ebola vaccine. |

| Merck | United States | Significant advances in cutting-edge science are delivering transformative medicines and vaccines that are enhancing health outcomes. |

| Sanofi | United States | In December 2025, Sanofi acquired Dynavax, adding a marketed adult hepatitis B vaccine and a phase 1/2 shingles candidate to the pipeline. |

| GlaxoSmithKline | United States | In July 2025, GSK plc announced it had started shipping doses of its trivalent seasonal influenza vaccines to US healthcare suppliers and pharmacies in preparation for the 2025-26 flu season. |

In June 2026, “Industry transactions announced recently suggest that the vaccine sector may be entering a new strategic cycle,” said David Dodd, Chairman and Chief Executive Officer of GeoVax. “Historically, vaccine programs addressing emerging infectious diseases were often viewed primarily through a public health lens. We are encouraged that governments, healthcare systems, and industry leaders increasingly recognize that disease prevention, supply resilience, and rapid-response vaccine technologies represent critical strategic assets.”

By Vaccine Type

By Technology

By Route of Administration

By Age Group

By Disease Indication

By End User

By Distribution Channel

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar