Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

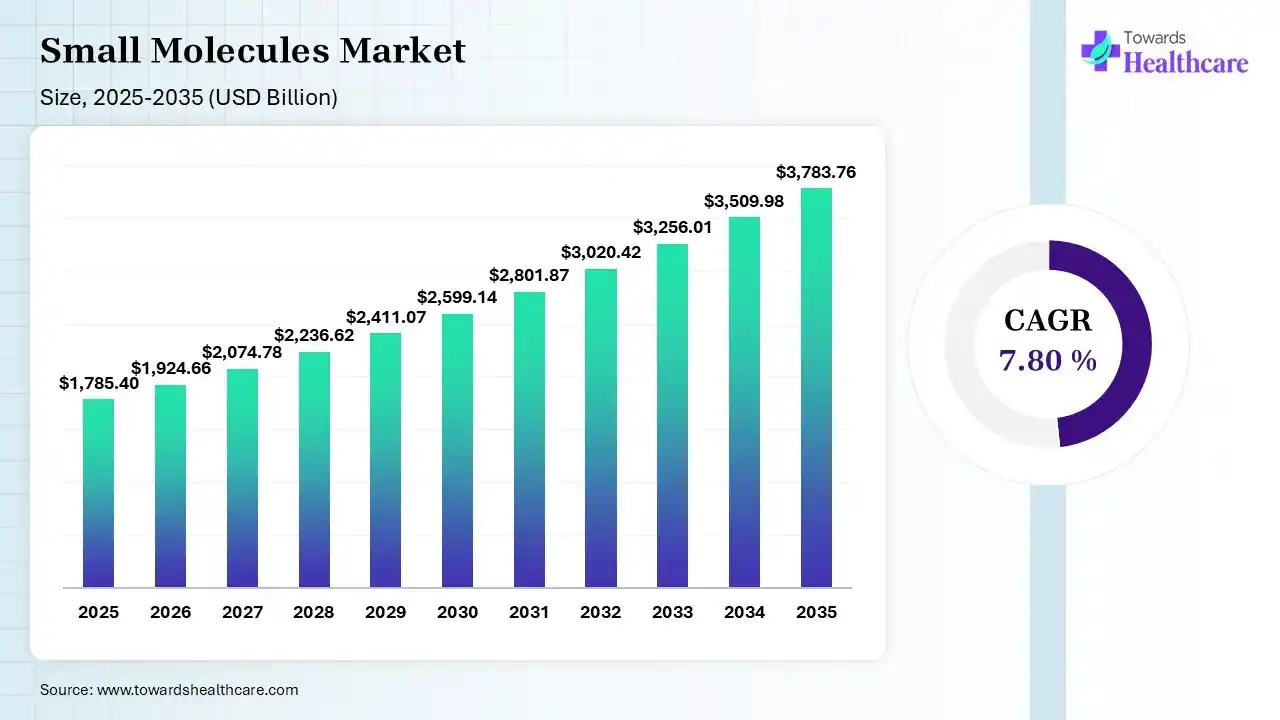

The small molecules market size was estimated at USD 1785.4 billion in 2025 and is predicted to increase from USD 1924.66 billion in 2026 to approximately USD 3783.76 billion by 2035, expanding at a CAGR of 7.80% from 2026 to 2035.

")

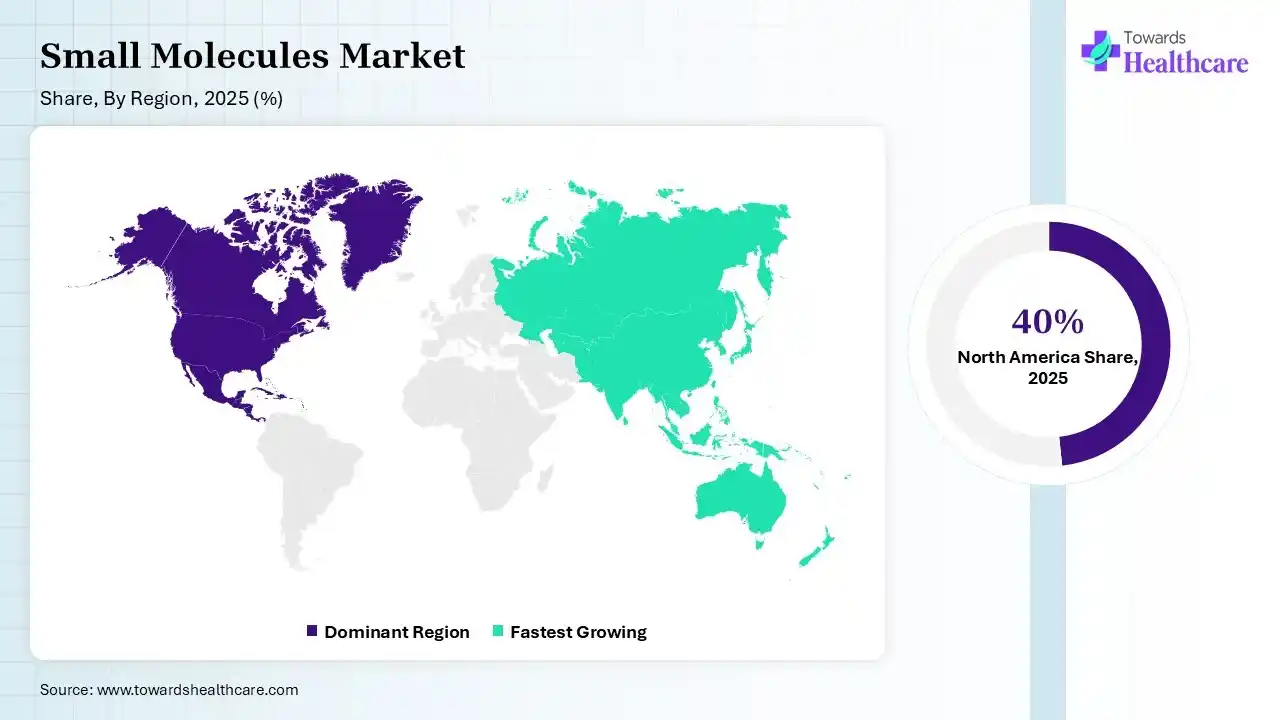

The small molecules market is expanding rapidly due to its significant role pharmaceutical industry, as it has the capacity to easily penetrate cells and regulate biological function. These molecules are broadly used in developing drugs for various diseases such as infectious diseases, cardiovascular diseases, cancer, and diabetes. North America is dominant in the market due to increasing technological advancement in healthcare and growing healthcare spending, while the Asia Pacific is the fastest growing due to increasing trends of drug discovery and increasing spending in R&D.

The small molecules market covers the discovery, development, manufacturing, and commercialization of low-molecular-weight drugs (typically <900 Da) that modulate biological targets via well-defined chemical structures. It spans patented/innovator brands, generics (including complex generics), OTC medicines, and the CDMO/outsourcing ecosystem that synthesizes active pharmaceutical ingredients (APIs) and finishes dosage forms. Advantages include oral bioavailability, scalable chemical synthesis, broad target coverage, and comparatively lower cost per treated patient versus biologics.

Recent developments shaping small-molecule drug manufacturing, like technological innovations and QbD principles that are allowing superior efficacy and enhancements, which drive the growth of the market.

For instance,

Increasing development in advanced technology of small molecule manufacturing drives the growth of the market.

For Instance,

Integration of AI in small molecules drives the growth of the market, as AI-driven technology has transformed the sector of medication molecule design, predominantly in the areas of de novo molecular design and molecular generative modeling. The introduction of deep generative models marks a transformative shift in the field. Deep generative models are entirely data-driven and less dependent on operative expertise and experience than outdated drug design strategies. Incorporating AI-based processes predominantly reduces the workload involved in drug development and improves the effectiveness of early-stage drug discovery. AI-driven technology in small-molecule drug discovery marks a profound shift in how life sciences companies attack multifaceted risks such as molecule screening, lead optimization, and lowers the time-to-market for new therapeutics.

Driver

Increasing Burden of Chronic Diseases

Small molecules are set to play a crucial role in alleviating the burden of chronic diseases. This diverse group of small chemical compounds offers numerous benefits for scientists and researchers. They have a wide range of uses, are relatively low-cost, and can be easily administered, including orally. Due to their small size, they can pass through cell membranes to reach their targets. They have a proven track record, deliver consistent results, and are relatively easy to produce. They can also be tailored to specific patient groups. As a result, small molecule drugs are valued for their versatility and effectiveness in treating a wide range of conditions, from chronic diseases like hypertension to acute infections like bacterial pneumonia. This drives the growth of the small molecules market.

Restraint

What are the Challenges in Developing Small Molecules?

Manufacturing small-molecule drugs involves many complexities. It needs specialized expertise and the latest technologies to handle formulation, process optimization, late-phase development, and commercial supply capabilities. On top of that, regulatory compliance is a major hurdle, especially when it comes to CMC (chemistry, manufacturing, and controls), which can limit the growth of the small molecules market.

Opportunity

Recent Advancements in 3D Structures of Small Molecules

Introducing a new system for predicting the 3D structures of small molecules that fast, accurate, and open to the academic research community, making it freely available. Predicting the 3D structure of small molecules is vital for both structure-based and ligand-based drug design. In structure-based drug design, having the bioactive conformations of compounds is essential for identifying and optimizing leads. Meanwhile, ligand-based drug design methods like 3D shape similarity search, 3D pharmacophore modeling, and 3D-QSAR present opportunities in the small molecules market.

For Instance,

| Table | Scope |

| Market Size in 2026 | USD 1924.66 Billion |

| Projected Market Size in 2035 | USD 3783.76 Billion |

| CAGR (2026 - 2035) | 7.80% |

| Leading Region | North America by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Lifecycle, By Therapeutic Area, By Route/Formulation, By End Market/Channel, By Development & Sourcing Model, By Dosage Form Complexity, By Region |

| Top Key Players | Pfizer, Novartis, Merck & Co. (MSD), Bristol Myers Squibb, AstraZeneca, Eli Lilly, Johnson & Johnson (Janssen), GlaxoSmithKline (GSK), Bayer, Takeda, AbbVie, Sanofi, Teva Pharmaceuticals, Sandoz, Viatris, Sun Pharmaceutical Industries, Dr. Reddy Laboratories, Cipla, Aurobindo Pharma, |

| Segments | Shares % |

| Patented/Innovator Small-Molecule Brands | 52% |

| Generics | 33% |

| OTC/Non-prescription | 15% |

Why the Patented/Innovator Small-Molecule Brands Segment Dominated the Market?

By product lifecycle, the patented/innovator small-molecule brands segment led the small molecules market by 52% share in 2025, as patented small molecule drugs are manufactured reproducibly, an advantage for investigators seeking a return on their spending. Once patent life expires, non-branded generic forms of the medicine will become increasingly available to patients. Patents provide a safety net, hopeful companies to take risks on novel and advanced therapies. The potential for a patent-protected monopoly on an effective medication provides the economic incentive needed to pursue advanced research.

On the other hand, the OTC/non-prescription segment is projected to experience the fastest CAGR from 2025 to 2034, as OTC medications provide self-management options for slight health issues. OTC drug products are available for a lower cost than their prescription substitutes to confirm larger volumes of sales. OTC drugs enable faster and cost-effective access to medical care.

| Segments | Shares % |

| Oncology | 30% |

| Cardiometabolic | 22% |

| CNS/Psychiatry & Neurology | 14% |

| Infectious Diseases | 10% |

| Respiratory & Allergy | 8% |

| Gastrointestinal & Hepatic | 6% |

| Pain & Inflammation | 7% |

| Rare/Orphan & Specialty | 3% |

Why the Oncology Segment Dominated the Market?

By therapeutic area, the oncology segment is dominant in the small molecules market by 30% in 2025, as it is effortlessly structurally modified to make it applicable to clinical requirements, and expedient to promote due to its affordability. Small-molecule targeted compounds have been developed in clinical medicine for decades, extending the survival time of cases subjected to advanced or stubborn cancer. Small-molecule inhibitors are primary targeted therapies for cancer because of their advantages in a broad range of targets, convenient medication, and the capability to penetrate the central nervous system.

The rare/orphan & specialty segment is projected to grow at the fastest CAGR from 2025 to 2034, as small-molecule medocation has advantages such that non-hereditary patients targeted and dosing suitability is higher than antibodies, nucleic acid drugs, cell therapies, and gene therapies, so advances in technology that get small molecules with exclusive characteristics support to produce best orphan drugs and offers numerus benefits to the patients.

| Segments | Shares % |

| Oral Solid Dose | 72% |

| Oral Liquids | 6% |

| Parenteral/Injectables | 11% |

| Topical/Transdermal | 5% |

| Inhaled/Nasal | 4% |

| Suppositories/Others | 2% |

Why was the Oral Solid Dose Segment Dominant in the Market in 2025?

By route/formulation, the oral solid dose segment led the small molecules market by 72% share in 2025, as it is the convenient, highly patient-compliant, affordable, and safer route of administration to treat different diseases. Oral solid dosage (OSD) refers to a end drug product that is swallowed through the mouth, liquified in the digestive system, and delivered to the body by absorption into the blood circulation. The most general OSD forms, tablets and capsules, are effective and affordable to produce, shelf-stable, and simple to administer. They are preferred by pharmaceutical manufacturers owing to the advantage of economies of scale.

The parenteral/Injectables segment is projected to experience the fastest CAGR from 2025 to 2034, as it offers many benefits as compared to the oral route of administration; due to the evasion of the drug absorption processes, the gastrointestinal enzyme degradation, and the liver first pass effect. The parenteral administration route is the most efficient and common form of delivery for active drug substances with low bioavailability and medications with a narrow therapeutic index.

| Segments | Shares % |

| Retail Pharmacy | 62% |

| Hospital / Acute Care | 24% |

| Specialty Pharmacy | 14% |

Why is the Retail Pharmacy Segment Dominant in the Market?

By end market/channel, the retail pharmacy segment led the small molecules market by 62% in 2025, as these pharmacies play a significant role in healthcare by offering appropriate access to medications, a broad range of products. Retail pharmacy is a pharmacy located characteristically in a community setting, where medicines and healthcare goods are distributed to the public. These pharmacies provide services such as health screenings, immunizations, and personalized counseling on medicine use.

On the other hand, the specialty pharmacy segment is projected to experience the fastest CAGR from 2025 to 2034, as the specialty pharmacy helps the healthcare provider relationship to better manage complex and rare chronic disease conditions. It is covered under the pharmacy benefit, the medical benefit, or both benefits, based on the benefit structure applied to the coverage policy. Specialty pharmacies offer services for insurers and providers by streamlining the distribution process and smoothing out the risks in medical care delivery and financing.

| Segments | Shares % |

| In-house R&D & Manufacturing | 55% |

| Outsourced to CDMOs / CMOs | 45% |

Why was the In-house R&D & Manufacturing Segment Dominant in the Market?

By development & sourcing model, the in-house R&D & manufacturing segment led the small molecules market by 55% share in 2025, as in-house R&D and formulation ability allow a company to fully control the excellence and timing of the R&D process and the advancement of product outcomes from those R&D efforts. In-house product expansion and manufacturing support protect the organization IP. In-house R&D makes it simple for different departments, like production, marketing, and engineering, to collaborate.

On the other hand, the outsourced to CDMOs/CMOs segment is projected to experience the fastest CAGR from 2025 to 2034, as it provides many benefits for pharmaceutical organizations, including improved flexibility, rapid market entry, challenges mitigation, and affordability, enabling them to lower financial exposure to small molecule APIs. CMOs/CDMOs continue to work towards making each complex procedure simple, improving efficiency, enhancing production, removing wastage, and evading bottlenecks while maintaining the high standard of compliance.

| Segments | Shares % |

| Conventional Immediate-Release | 58% |

| Modified/Controlled-Release | 25% |

| Complex Dosage Forms | 17% |

Why was the Conventional Immediate-Release Segment Dominant in the Market?

By Dosage Form Complexity, the Conventional Immediate-Release segment led the market by 58% share in 2025, as it provides precise dosing, improved bioavailability, fast action, and ease of administration, predominantly advantageous for patients who have challenges in swallowing outdated tablets. They liquify rapidly in the mouth, enabling rapid absorption in the oral cavity, leading to an earlier onset of action than the conventional dosage forms.

On the other hand, the complex dosage forms segment is projected to experience the fastest CAGR from 2025 to 2034, as it includes long-acting implantables and injectables, transdermals, MDIs, which have complex active constituents, formulations, dosage forms, or are complex drug-device combination products.

")

North America is dominant in the market share 40% in 2025, with a strong presence of pharmaceutical organizations with an innovative drug development pipeline. Growing medical care spending in North America is due to the increasing adoption of novel, expensive technologies, an increasing prevalence of chronic conditions, and higher drug costs, which contribute to the growth of the market.

For Instance,

U.S. Small Molecules Market Trends

In the U.S., many people have different types of chronic conditions like cancer, diabetes, and CVD An estimated 129 million people in the US have at least one major chronic disease, which increases the demand for small molecules. Increasing government support and the rate of regulatory approval for new drugs also contribute to the growth of the market.

Canada Small Molecules Market Trends

In Canada, increasing adoption of new technology like precision medicine and AI-based drug discovery. Canadian healthcare technology advancements are often funded by and focused on American markets, so the technologies rapidly commercialize and become profitable, which contributes to the growth of the market.

Asia Pacific is the fastest-growing region in the small molecules market by 23% share in the forecast period, as growing health awareness leads to increased advanced medical care facilities demand which has pressured the ruling governments in the region to spend in the health sector, leading to different opportunities for health sector growth, which contributes to the growth of the market.

R&D

Drug research and discovery for small molecules starts with recognising a biological target, like an enzyme or receptor linked to a disease, and designing chemical compounds that modulate that target. This small-molecule drug discovery phase takes many years of iterative enterprise and testing to produce a feasible drug candidate for advancement.

Key Players: Pfizer, AbbVie, AstraZeneca, and Sai Life Sciences

Clinical Trials

Small-molecule drugs entering clinical trials must undergo rigorous preclinical testing. This phase appraises the drug efficacy, safety, and pharmacokinetics to confirm it meets government standards for human trials.

Key Players: IQVIA, Parexel, Medpace, and Charles River Laboratories

Patient Support and Services

Small-molecule drugs are low-molecular-weight complexes, generally under 900 daltons, that are chemically synthesized or derived from a natural source. Small-molecule drugs modulate the opening and closing of these channels to treat diseases like epilepsy.

Key Players: Alacritas, Genelife Clinical Research, Altasciences, Pharmaron, IQVIA Laboratories, and ICON

In April 2025, Bruce Cozadd, chairman and chief executive officer of Jazz, stated, “Bringing Chimerix into Jazz adds a novel medicine to our oncology portfolio and advances our efforts to address unmet patient needs.”

By Product Lifecycle

By Therapeutic Area

By Route/Formulation

By End Market/Channel

By Development & Sourcing Model

By Dosage Form Complexity

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar