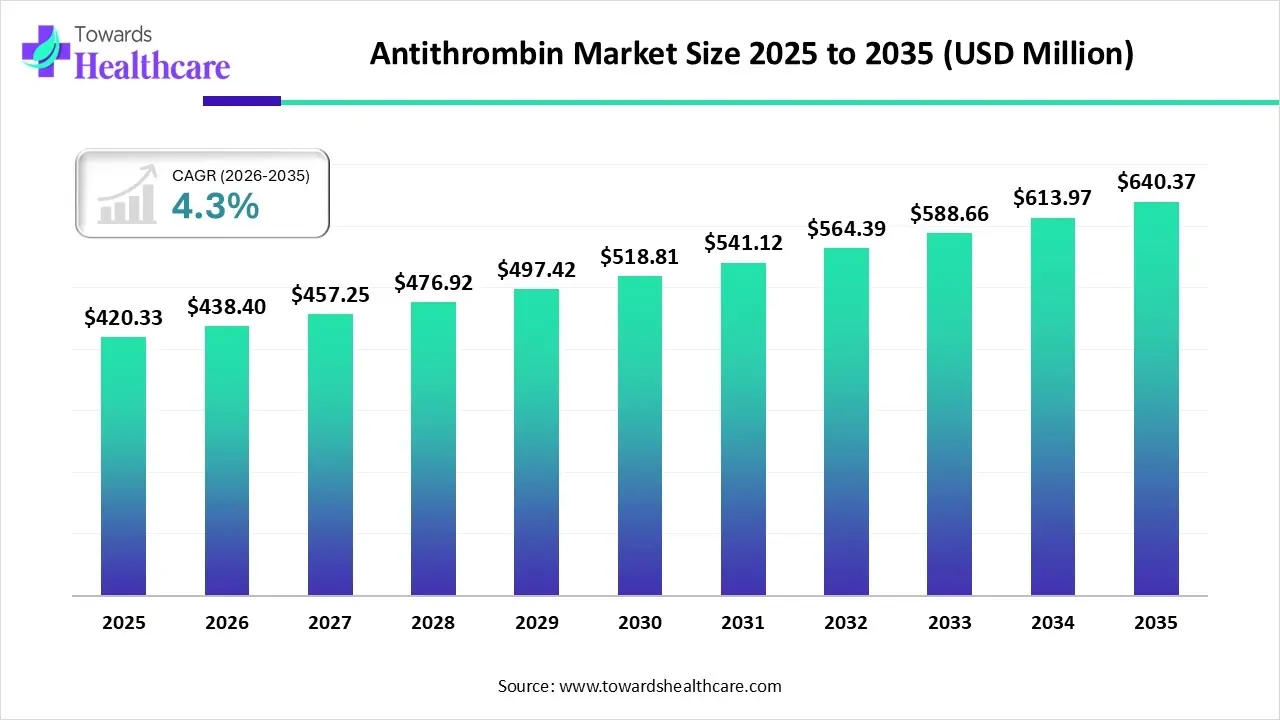

The global antithrombin market size is calculated at US$ 420.33 in 2025, grew to US$ 438.4 million in 2026, and is projected to reach around US$ 640.37 million by 2035. The market is expanding at a CAGR of 4.3% between 2026 and 2035.

")

Technological convergence and changing clinical paradigms are driving a significant transformation in the antithrombin market. As scientists work to restore endogenous antithrombin synthesis through genome correction techniques, emerging gene editing platforms are upending traditional ideas of protein replacement. In the meantime, engineered antithrombin variants with increased inhibitory profiles or longer half-lives are being found more quickly thanks to developments in bioinformatics and molecular modeling.

| Key Elements | Scope |

| Market Size in 2025 | USD 420.33 Million |

| Projected Market Size in 2035 | USD 640.37 Million |

| CAGR (2025 - 2035) | 4.3% |

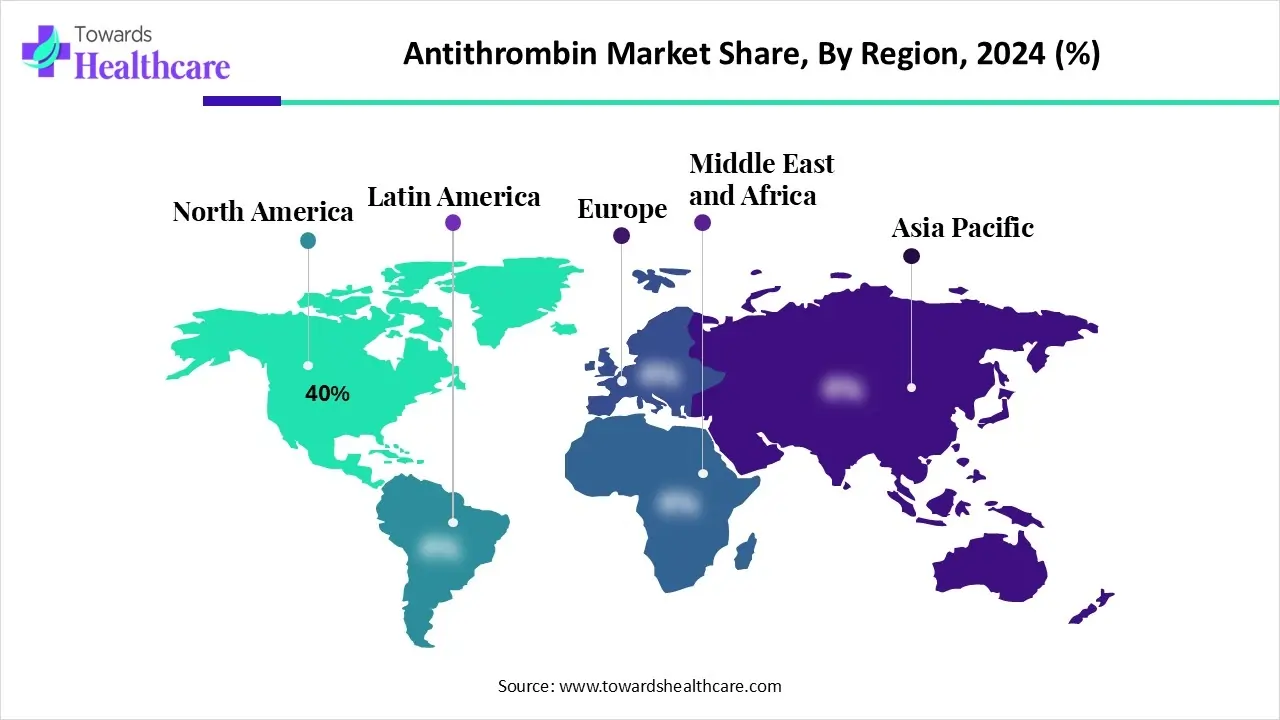

| Leading Region | North America by 40% |

| Market Segmentation | By Product Type, By End-User, By Route of Administration, By Distribution Channel, By Region |

| Top Key Players | CSL Limited, Grifols, S.A., Takeda Pharmaceutical Company Limited (which acquired Shire Plc), Octapharma AG, LFB USA, Kedrion S.p.A, Lee Biosolutions, Scripps Laboratories, rEVO Biologics, Inc., Thermo Fisher Scientific, Siemens Healthcare GmbH, Diapharma Group, Inc., Merck KGaA, Pfizer Inc., Sanofi, Novartis AG, Bio-Techne Corporation, Biocon Ltd., Jiangsu Hengrui Medicine Co., Ltd., China Biologic Products, Inc. |

The antithrombin market is driven by the increasing prevalence of thrombosis, rising use in surgical and obstetric care, adoption in neonatal/pediatric care, growing biologics manufacturing, wider application in rare disease management, and advances in recombinant technology that improve production scalability and safety profiles.

The global antithrombin market covers the production, purification, formulation, distribution, and clinical use of antithrombin (AT) products, including antithrombin III concentrates derived from plasma, recombinant antithrombin produced through bioengineering, and antithrombin used in research and diagnostics. Antithrombin is an essential serine protease inhibitor used to prevent and treat thrombotic complications in patients with hereditary antithrombin deficiency, disseminated intravascular coagulation (DIC), sepsis-related coagulopathy, cardiopulmonary bypass surgery, and in heparin-resistant conditions.

The antithrombin’s production and quality control frameworks are changing due to automation and artificial intelligence. AI algorithms are being used more and more for formulation modeling, process optimization, and protein structure prediction, which lowers human error and speeds up drug development. Furthermore, AI-powered platforms are being incorporated into clinical trial management and pharmacovigilance to improve patient safety profiling and enable real-time adverse event monitoring.

Which Product Type Dominated the Antithrombin Market in 2024?

Plasma-Derived Antithrombin

The plasma-derived antithrombin segment accounted for approximately 60% of market revenue in 2024. The delicate balance between clotting and bleeding is demonstrated by the use of products derived from human plasma to prevent thrombosis and control bleeding. Concentrates of plasma-derived antithrombin (pdAT) can be used to treat congenital antithrombin (AT) deficiency-related venous thromboembolism (VTE).

Recombinant Antithrombin (rAT)

The recombinant antithrombin (rAT) segment is expected to grow at the highest rate of 10-12% in the antithrombin market during 2025-2034. The main benefit of recombinant antithrombin over plasma-derived products is its improved safety profile, which removes the possibility of spreading blood-borne infections. Because it doesn't rely on human blood donations, it also offers more consistent potency and a dependable supply.

Antithrombin Assay Kits

The antithrombin assay kits segment is estimated to achieve a significant growth rate in the market during the upcoming period. An activity assay should be used for preliminary testing in order to diagnose antithrombin deficiency. One recommendation for laboratory testing to identify antithrombin deficiency is to use an activity assay for preliminary testing. In order to effectively guide and monitor anticoagulation therapy, they are also crucial.

How Hospitals & Surgical Centers Dominated the Antithrombin Market in 2024?

The hospitals & surgical centers segment dominated the market, accounting for approximately 55% of revenue in 2024. The Centers for Disease Control and Prevention state that compared to a traditional hospital setting, the surgical hospital setting is frequently safer and cleaner, lowering the risk of infection by almost half. Additionally, procedures carried out in a surgery center usually result in faster completion times and shorter recovery times.

Speciality Clinics

The specialty clinics segment is expected to grow at the highest growth rate of 10% in the antithrombin market during 2025-2034. Specialized clinics have a positive impact on patient care and outcomes that goes beyond the individual healthcare provider. Specialized clinics will continue to play a crucial role in developing clinical expertise, encouraging innovation, and influencing the direction of healthcare as medicine advances.

Diagnostic Laboratories

The diagnostic laboratories segment is estimated to achieve a significant growth rate in the market during the upcoming period. Precision medicine, expedited workflows, and data-driven decision-making are the hallmarks of the transformative era that the health care and diagnostics sector is entering. Artificial intelligence (AI) and automation are being strategically integrated into laboratories as personalized healthcare becomes the norm.

How did the Intravenous Segment Dominate the Antithrombin Market in 2024?

The intravenous segment dominated the market, accounting for approximately 90% of revenue in 2024. For acute, life-threatening conditions like severe sepsis or disseminated intravascular coagulation (DIC), intravenous administration offers instantaneous and complete bioavailability, enabling a quick onset of action. In a controlled hospital setting, the doctor can precisely achieve high plasma concentrations of the drug and closely monitor its effects.

Subcutaneous

The subcutaneous segment is expected to grow at the highest growth rate of 15% in the antithrombin market during 2025-2034. For chronic conditions (such as maintenance therapy for hereditary AT deficiency), subcutaneous administration is recommended, with an emphasis on patient comfort and quality of life. It eliminates the need for repeated IV access, cuts down on time spent in the infusion clinic, requires fewer resources for medical professionals, and permits at-home treatment.

What Made Hospital Pharmacies Dominant in the Antithrombin Market in 2024?

The hospital pharmacies segment accounted for approximately 50% of market revenue in 2024. One of the most important divisions in hospitals that handles the acquisition, storage, compounding, dispensing, production, testing, packaging, and distribution of medications is the hospital pharmacy. This department is also in charge of pharmaceutical science and education research, which is conducted by qualified and experienced pharmacists. The hospital pharmacy significantly affects the cost of medical care.

Specialty Drug Distributors

The specialty drug distributors segment is expected to grow at a 9-10% CAGR in the antithrombin market during the forecast period. In order to support pharmaceutical companies and guarantee that patients with uncommon illnesses have access to the medication they require at the appropriate time, specialty distributors are essential. In order to meet patient demand, a lot of specialty pharmacies now provide distribution services.

Online/Direct Biopharma Supply

The online/direct biopharma supply segment is estimated to achieve a significant growth rate in the market during the upcoming period. By utilizing digital technologies and optimizing the supply chain, online/direct biopharma supply offers notable benefits in terms of efficiency, cost-effectiveness, and patient experience.

")

North America accounted for approximately 40% of the antithrombin market revenue in 2024. This is mostly because antithrombin concentrates are growing in the region. The expansion of the regional market is also boosted by supportive U.S. government investments on plasma-derived products.

Venous thromboembolism affects up to 900,000 in the U.S. annually. About 25% of individuals with PE experience sudden death as their initial symptom. Between 60,000 and 100,000 Americans are thought to die from VTE every year. According to economic analyses, the U.S. spends between $5 and $10 billion annually on healthcare related to VTE, with direct medical costs of about $20,000 per case of incidence.

Asia Pacific is estimated to host the fastest-growing antithrombin market during the forecast period. Interest in advanced antithrombin products is being driven by the rapid expansion of hospital infrastructure, the rising incidence of coagulation disorders, and the growing awareness among clinicians. Public health investments in sepsis management and government initiatives to improve critical care capabilities further accelerate market evolution. At the same time, developing domestic biopharma capabilities in nations like China, Japan, and India promises to bring in new players, competitive pricing structures, and possible export dynamics.

In India, intravascular thrombosis-related cardiovascular disease (CVD) is becoming a major public health issue due to a complex interaction of socioeconomic, genetic, and lifestyle factors. In the upcoming years, reducing the rising incidence of CVD and intravascular thrombosis will require raising public health awareness, encouraging treatment compliance, and expanding access to medical resources.

Europe is expected to grow at a significant CAGR in the antithrombin market during the forecast period, motivated by the rising incidence of thrombotic disorders, robust healthcare systems, and significant R&D expenditures made by major pharmaceutical companies. Significant adoption is occurring in nations such as France, the United Kingdom, and Germany due to their sophisticated hospital networks and established clinical research facilities. Growth in the market is also being aided by the expansion of specialty treatment facilities and the regulatory approval of innovative treatments.

Of the 3.4 million admitted patients in the UK, 91% had a VTE risk assessment. Both NHS and independent sector providers achieved an assessment rate of 91%. London received the highest assessment (93%), while Yorkshire, the North East, and the North West received the lowest (88%). Remarkably, only 29% of integrated care boards (12 out of 42) met the operational requirement of evaluating 95% or more of their admissions.

The South America antithrombin market is poised for considerable expansion, driven by rising awareness and improving healthcare infrastructure across the region. A significant driver is the high burden of venous thromboembolism hospitalization, especially in Brazil, which reports an average of over 46,000 cases annually. This growing incidence heightens the need for effective anticoagulant therapies.

Brazil stands out as a key growth engine in South America's antithrombin market due to its massive patient population and rising number of surgical procedures. Data from the broader Brazilian anticoagulation therapy market, which includes antithrombin use, indicates that Deep Vein Thrombosis treatment alone accounts for a substantial share of revenue. This underscores the robust demand.

The MEA antithrombin market is poised for promising growth, particularly in the therapeutics segment. Advancements in critical care settings and increased investment in sophisticated healthcare services are bolstering adoption. The region is seeing diversification of demand across various applications, including cardiovascular surgery, which accounts for over 40% of global consumption.

The United Arab Emirates is a focal point for growth, supported by substantial government initiatives and favorable reimbursement policies for antithrombotic drugs. As a high-income country, the UAE is rapidly adopting advanced recombinant products to treat conditions such as deep vein thrombosis.

It includes preclinical testing to find novel antithrombin products and comprehend mechanisms, as well as basic research and target identification (such as SERPINC1 gene variants).

Companies involved in the research and development phase include Grifols, CSL Behring, Takeda, Octapharma, LFB, Kedrion, and Siemens Healthineers.

It involves using human subjects in a series of trial phases to demonstrate safety and efficacy before submitting and receiving regulatory approval (e.g., FDA, EMA).

Companies managing clinical trials and seeking regulatory approvals include Grifols, CSL Behring, Takeda, Octapharma, LFB, Kedrion, and Siemens Healthineers.

It involves converting the active pharmaceutical ingredient (API) into a final product (e.g., injectable solution, specific dosage units) that is stable and ready for the market.

Companies responsible for formulating and preparing the final antithrombin products for market include Grifols, CSL Behring, Takeda, Octapharma, LFB, Kedrion, and Siemens Healthineers.

Company Overview

Company Overview

| Company | Offerings | Contributions to Antithrombin Market | Market Role | Key Highlights |

| Takeda Pharmaceutical Company Limited | Plasma-derived antithrombin; coagulation therapies | Expands global therapeutic access and supports critical-care use | Major global supplier | Strong regulatory focus and large manufacturing base |

| Octapharma AG | Human plasma-derived antithrombin concentrates | Ensures reliable supply for surgical and ICU thrombosis management | Leading European producer | Robust plasma-fractionation capabilities |

| LFB USA | Antithrombin concentrates | Serves hereditary AT deficiency and specialized clinical needs | Niche U.S. biotherapeutics player | Focus on rare-disease biologics |

| Kedrion S.p.A | Plasma-derived antithrombin | Expands donor-based production for hospitals worldwide | Key plasma-therapy provider | Broad global plasma-collection network |

| Lee Biosolutions | Antithrombin reagents and biomarkers | Supports diagnostics, assays, and research applications | Specialized biochemical supplier | Enables lab testing and innovation in AT analysis |

By Product Type

By End-User

By Route of Administration

By Distribution Channel

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar