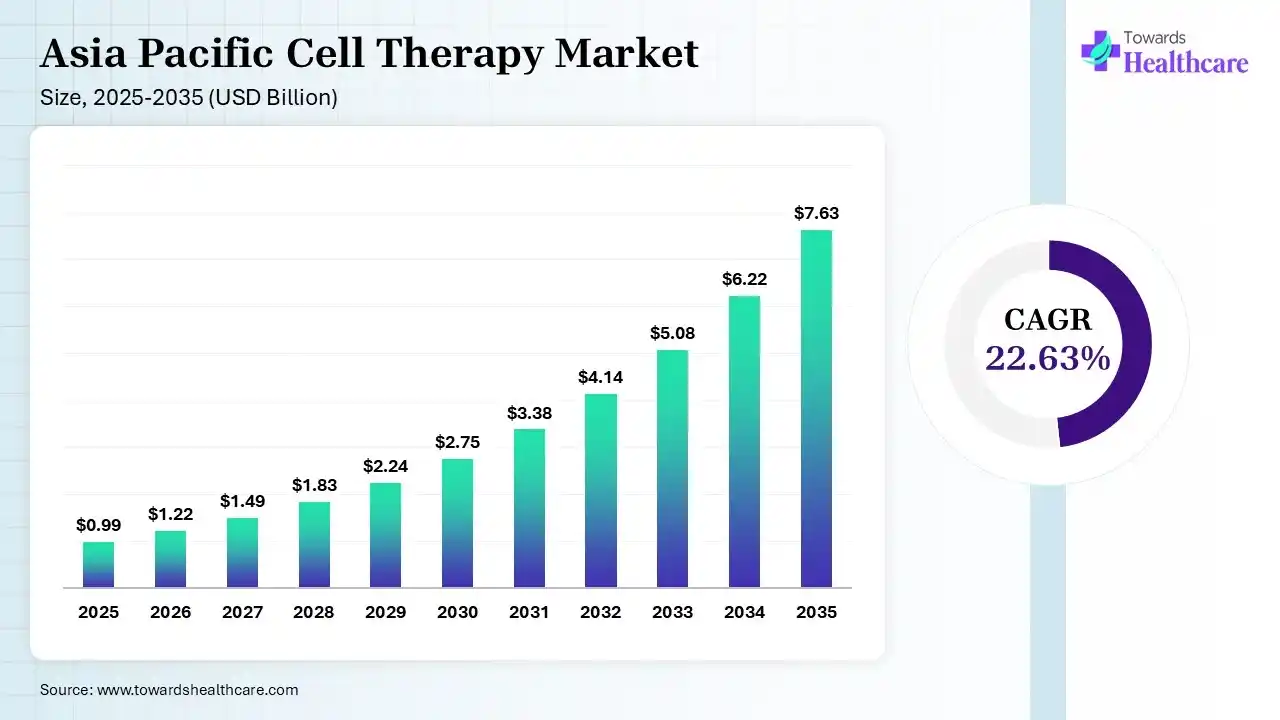

The Asia Pacific cell therapy market size was estimated at USD 0.99 billion in 2025 and is predicted to increase from USD 1.22 billion in 2026 to approximately USD 7.63 billion by 2035, expanding at a CAGR of 22.63% from 2026 to 2035. The increasing chronic disease patient population across the Asia Pacific is increasing the use of cell therapies. Growing clinical trials, investments, R&D activities, and new product launches are also enhancing the market growth.

")

The Asia Pacific cell therapy market is driven by growing cancer incidences and a shift towards localized biomanufacturing hubs. The Asia Pacific cell therapy refers to research, manufacturing, and commercialization of cell therapies across the Asia Pacific. These therapies help in modifying or replacing patients' cells to fight against disease and restore normal body function.

The use of AI in the Asia Pacific cell therapy market is increasing to accelerate cell therapy development and the identification of suitable targets and biomarkers. It also helps in the development of personalized therapies by offering faster and more accurate genomic data analysis and prediction of treatment outcomes. AI also helps in enhancing manufacturing efficiency, optimizing cell therapies, and ensuring stringent quality control.

Expanding Industries

The rapid expansion of the biotechnology and pharmaceutical sector is increasing the development of new cell therapies. This expansion is also leading to a rise in collaborations, clinical trials, and outsourcing trends.

CAR-T and Stem Cell Therapies on the Rise

The growing incidences of cancer, cardiovascular diseases, neurological diseases, and orthopaedic conditions are increasing the demand for these CAR-T and stem cell therapies.

Escalating Manufacturing Technologies

With the rapidly expanding cell therapies market in the Asia Pacific, the companies are heavily investing in advanced manufacturing technologies. Improved cell processing, automation, and gene editing technologies are being utilized by the companies.

| Table | Scope |

| Market Size in 2026 | USD 1.22 Billion |

| Projected Market Size in 2035 | USD 7.63 Billion |

| CAGR (2026 - 2035) | 22.63% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Therapy Type, By Cell Type, By Therapeutic Area, By Technology, By Source, By End User, By Application, By Region |

| Top Key Players | Legend Biotech, Mesoblast Limited, JW Therapeutics, Medipost Co., Ltd., Novartis, Bristol Myers Squibb, Gilead Sciences, JCR Pharmaceuticals, ImmunoChina Pharmaceuticals, SCG Cell Therapy |

")

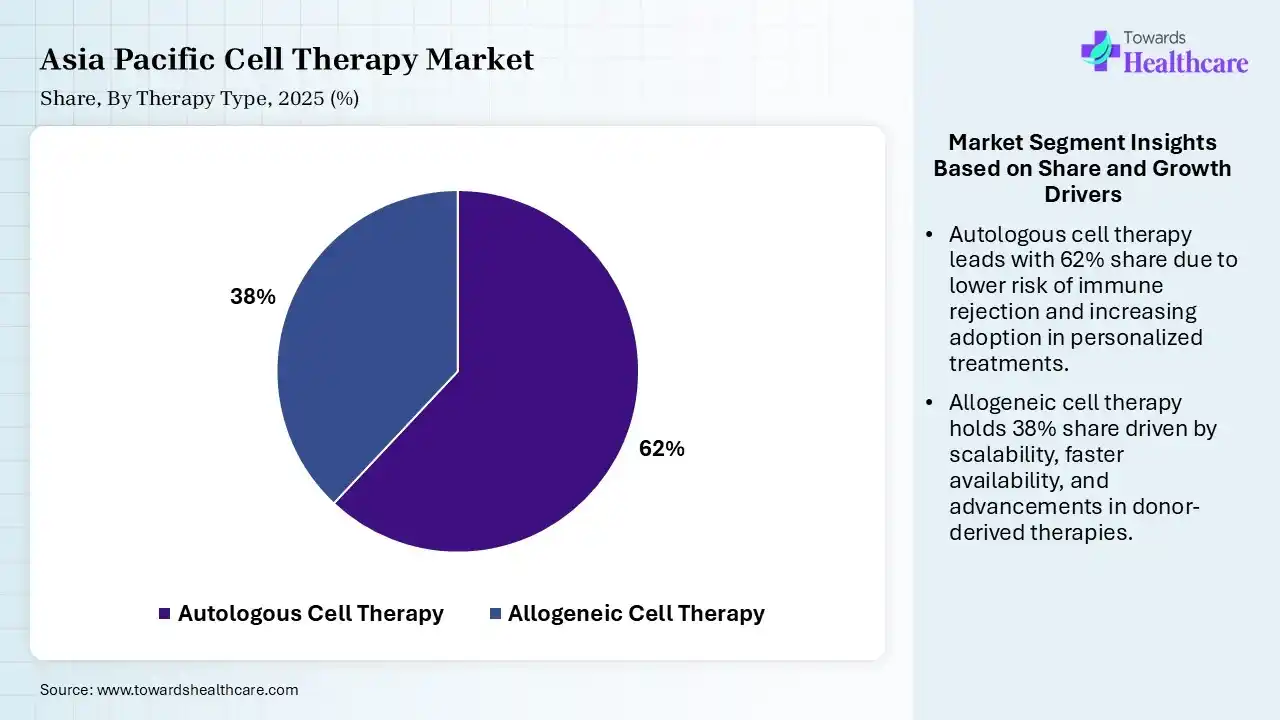

| Segment | Share 2025 (%) |

| Autologous Cell Therapy | 62% |

| Allogeneic Cell Therapy | 38% |

The Autologous Cell Therapy Segment Dominated the Market With 62% in 2025

The autologous cell therapy segment held the largest revenue share of 62% of the Asia Pacific cell therapy market in 2025, due to strong adoption of patient-specific therapies, which improved safety outcomes. Rising CAR-T approvals in China and Japan also accelerated commercialization. Expansion of the reimbursement frameworks also supported clinical utilization.

The allogeneic cell therapy segment held the second-largest share of 38% of the market in 2025 and is expected to witness the fastest growth during the forecast period, due to off-the-shelf manufacturing, which lowers production timelines and costs. Biotech firms are also expanding scalable cell banking capabilities. Increasing investment in NK-cell platforms also fuels their rapid growth.

")

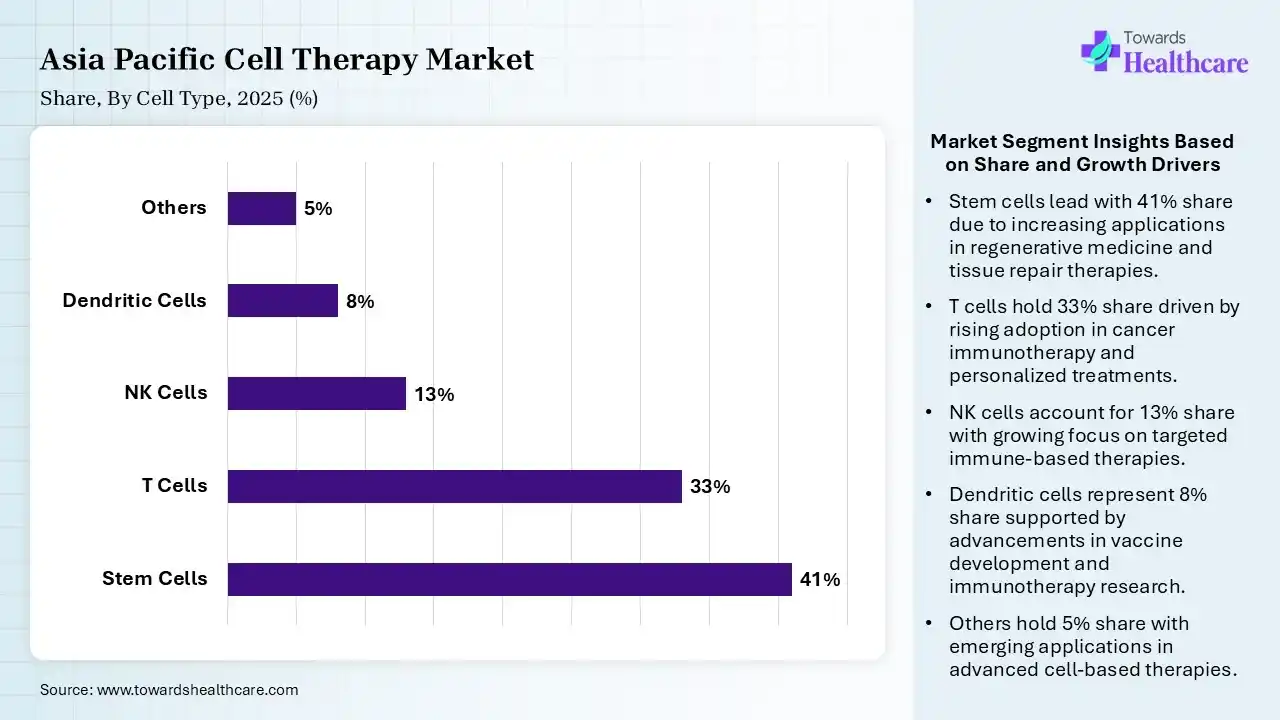

| Segment | Share 2025 (%) |

| Stem Cells | 41% |

| T Cells | 33% |

| NK Cells | 13% |

| Dendritic Cells | 8% |

| Others | 5% |

The Stem Cells Segment Dominated the Market With 41% in 2025

The stem cells segment accounted for the highest revenue share of 41% of the Asia Pacific cell therapy market in 2025, driven by regenerative medicine applications, which continued its expansion across orthopedic and neurological diseases. Growth in government support also enhanced the stem cell clinical trials and translational research. Increased stem cell banking infrastructure also improved their accessibility.

The T cells segment held the second-largest share of 33% of the market in 2025, due to the rapid commercialization of CAR-T products, which strengthens demand across oncology centers. Hospitals are also expanding hematologic cancer treatment capacity. Strong pipeline development also supports sustained adoption.

The NK cells segment held 13% of the Asia Pacific cell therapy market share in 2025 and is expected to show the highest growth during the forecast period, due to their scalable allogeneic treatment opportunities. Companies are also prioritizing next-generation immunotherapy platforms. Improved persistence technologies also enhance their therapeutic potential.

The dendritic cells segment held 8% of the market share in 2025, driven by cancer vaccine development, which supports clinical demand for dendritic cell therapies. Research institutes also increase immunotherapy collaborations, increasing their demand. Personalized treatment approaches also encourage their adoption.

")

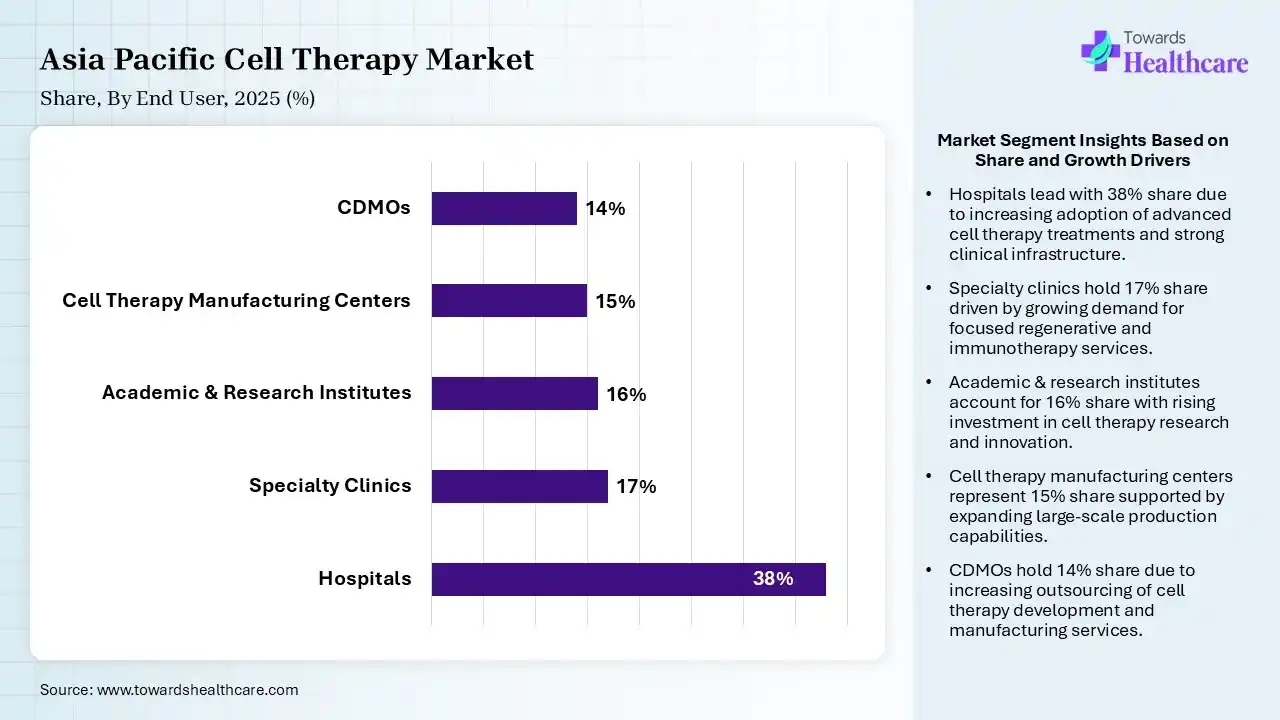

| Segment | Share 2025 (%) |

| Hospitals | 38% |

| Specialty Clinics | 17% |

| Academic & Research Institutes | 16% |

| Cell Therapy Manufacturing Centers | 15% |

| CDMOs | 14% |

The Hospitals Segment Dominated the Market With 38% in 2025

The hospitals segment held a major revenue share of 38% of the Asia Pacific cell therapy market in 2025, due to their cell therapy administration and patient management activities. Expansion of oncology departments also increased treatment capacity. Reimbursement support also strengthened institutional adoption.

The specialty clinics segment held the second-largest share of 17% of the market in 2025, as they attract increasing patient volumes. Their outpatient treatment models also improve accessibility. Private investments also support advanced therapy infrastructure.

The academic & research institutes segment held 16% of the Asia Pacific cell therapy market share in 2025, due to their intensified stem cell and immunotherapy research programs. Government grants also stimulate translational innovation. Collaborative clinical trials also enhance commercialization opportunities.

The CDMOs segment held 14% of the market share in 2025 and is expected to expand rapidly during the forecast period, driven by growing outsourcing demand as biotech firms seek cost-efficient production. They are also expanding GMP-compliant facilities across Asia-Pacific. Increasing strategic partnerships also accelerates therapy commercialization.

")

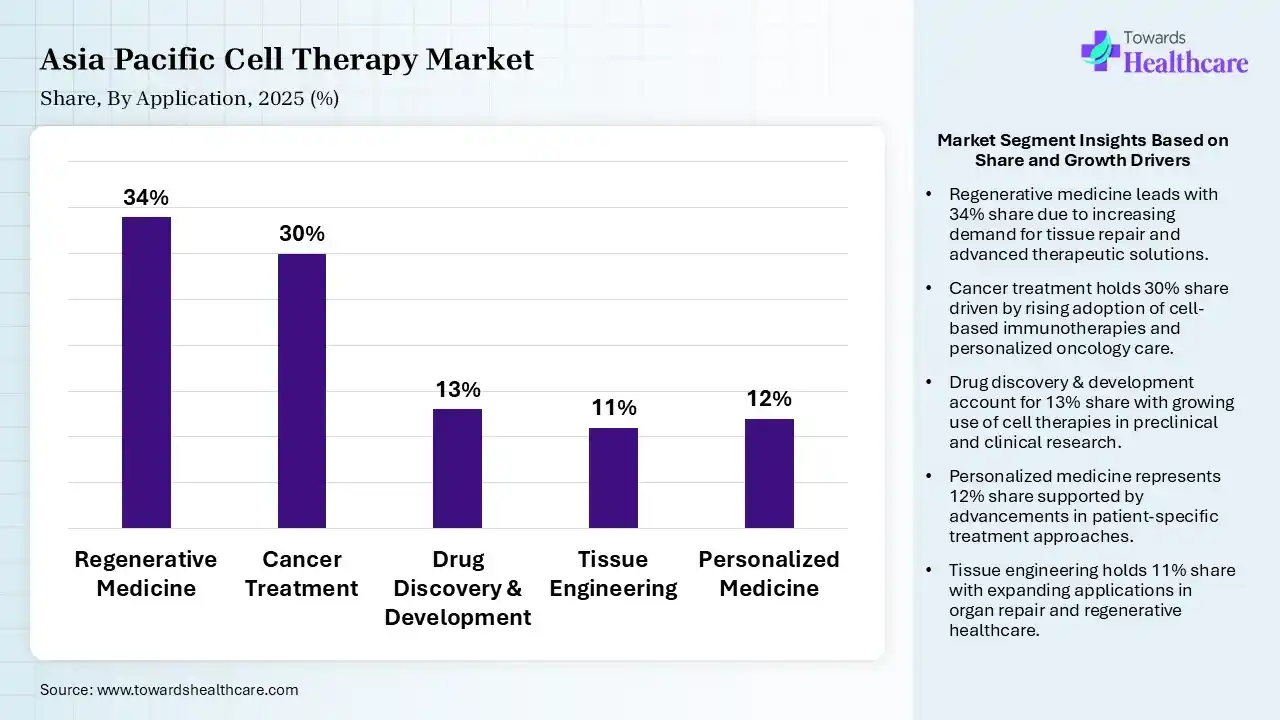

| Segment | Share 2025 (%) |

| Regenerative Medicine | 34% |

| Cancer Treatment | 30% |

| Drug Discovery & Development | 13% |

| Tissue Engineering | 11% |

| Personalized Medicine | 12% |

The Regenerative Medicine Segment Dominated the Market With 34% in 2025

The regenerative medicine segment contributed the biggest revenue share of 34% of the Asia Pacific cell therapy market in 2025, driven by increased chronic disease burden, which promoted regenerative therapy demand. Stem cell technologies have also improved tissue repair outcomes. Government support also expanded their clinical research programs.

The cancer treatment segment held the second-largest share of 30% of the market in 2025, as the CAR-T and TCR therapies are revolutionizing hematologic cancer treatment. Increasing oncology approvals are also enhancing treatment accessibility. Hospitals invest heavily in immunotherapy infrastructure, promoting their adoption.

The drug discovery & development segment held 13% of the Asia Pacific cell therapy market share in 2025, as its cell-based platforms are improving preclinical testing efficiency. Pharmaceutical firms are expanding personalized screening programs. AI-integrated cell models are also accelerating discovery timelines.

The personalized medicine segment held 12% of the market share in 2025 and is expected to gain the highest share during the forecast period, driven by its precision medicine strategies, which increase the adoption of patient-specific therapies. Genomic integration also enhances therapeutic targeting capabilities. Healthcare systems also prioritize individualized treatment approaches.

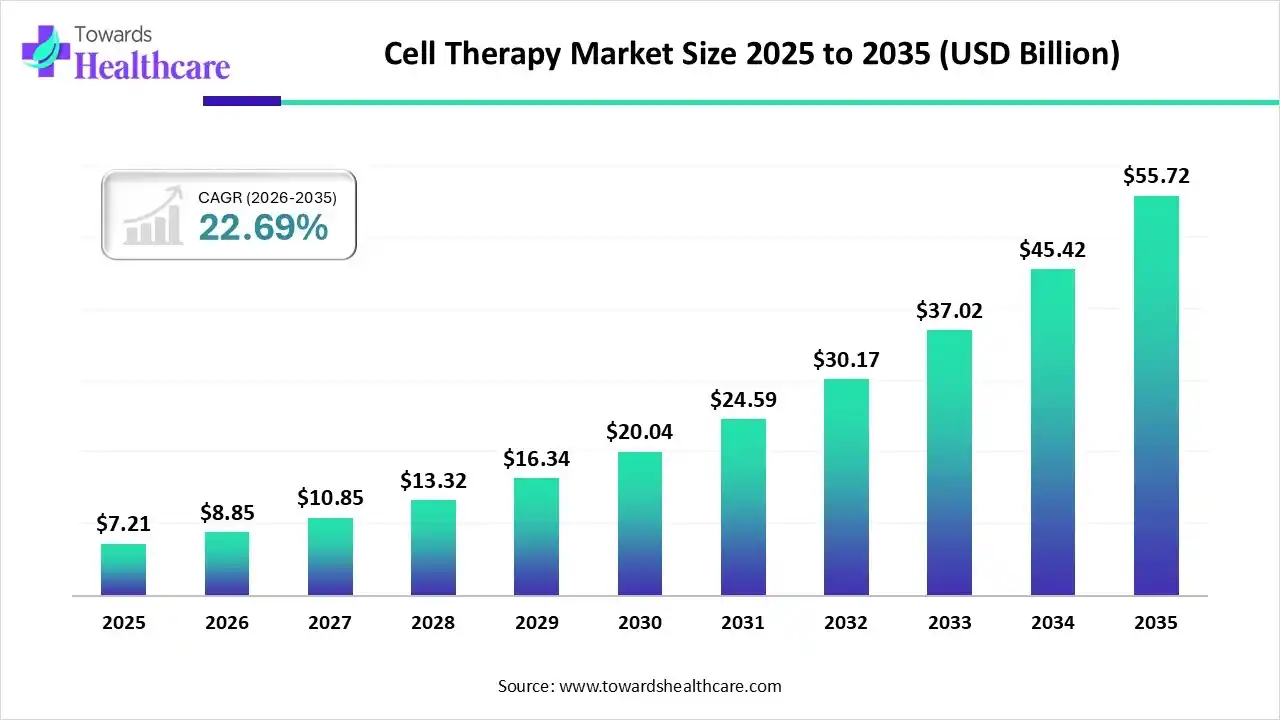

The global cell therapy market size was estimated at US$ 7.21 billion in 2025 and is projected to grow to US$ 55.72 billion by 2035, rising at a compound annual growth rate (CAGR) of 22.69% from 2026 to 2035.

The Asia Pacific cell therapy market held a significant share in 2025, due to the presence of a large patient population. Rapid expansion of industries, hospitals, and manufacturing capabilities also increased the adoption of cell therapies. Growth in government support, clinical trials, and a rise in health awareness also enhanced the market growth.

China Market Trends

China consists of a large patient population, where the growth in cancer and other chronic diseases has increased the adoption of cell therapies. Availability of affordable manufacturing facilities also increased the outsourcing trends. Expansion of the R&D activities and clinical trials also increased their use.

India Market Trends

Increasing cancer cases in India are promoting the adoption of cell therapies. Expanding industries and healthcare infrastructure are also driving the adoption of these therapies. Increasing investments, government initiatives, and collaborations are also fueling their innovations.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Asia Pacific Cell Therapy Solutions |

| Legend Biotech | Somerset, U.S. | Carvykti |

| Mesoblast Limited | Melbourne, Australia | Remestemcel-L |

| JW Therapeutics | Shanghai, China | Carteva |

| Medipost Co., Ltd. | Seongnam, South Korea | Cartistem |

| Novartis | Basel, Switzerland | Kymriah |

| Bristol Myers Squibb | Princeton, U.S. | Abecma and Breyanzi |

| Gilead Sciences | Foster City, U.S. | Yescarta and Tecartus |

| JCR Pharmaceuticals | Ashiya, Japan | Temcell HS Inj |

| ImmunoChina Pharmaceuticals | Beijing, China | CNCT19 |

| SCG Cell Therapy | Singapore | SCG101 |

Strengths

Weaknesses

Opportunities

Threats

By Therapy Type

By Cell Type

By Therapeutic Area

By Technology

By Source

By End User

By Application

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar