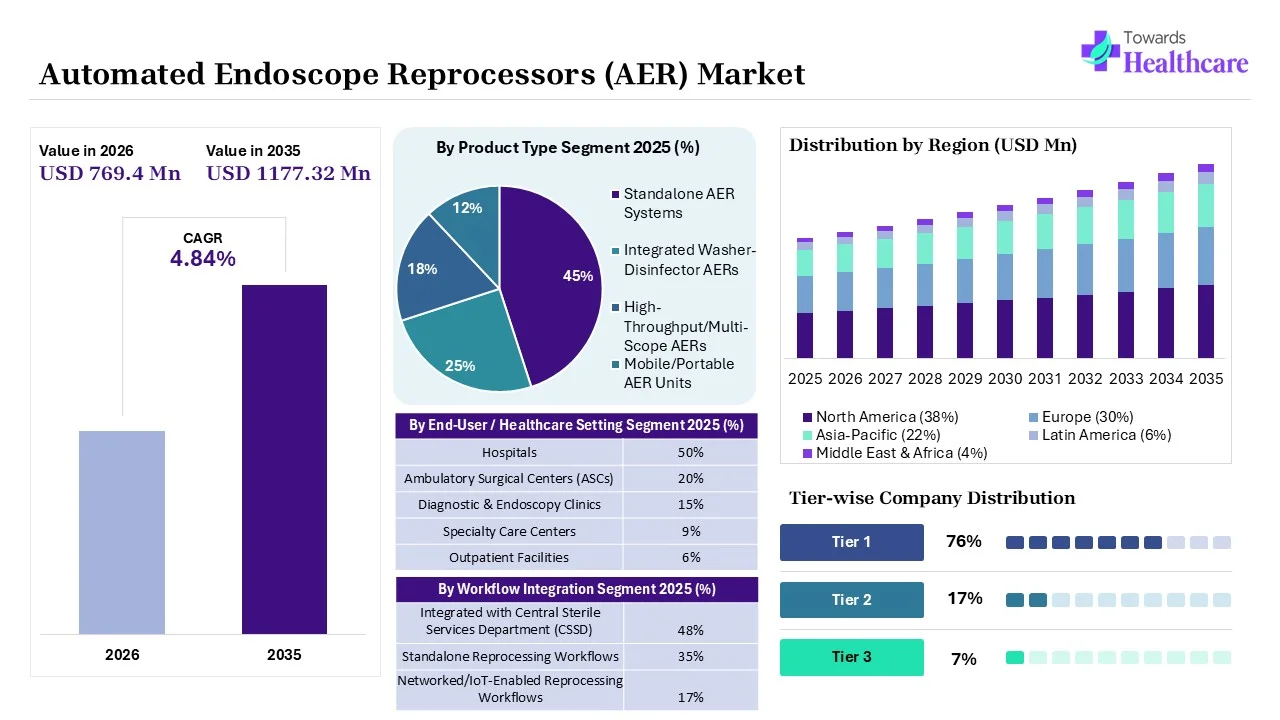

Market to Grow USD 769.4 Million by 2026")

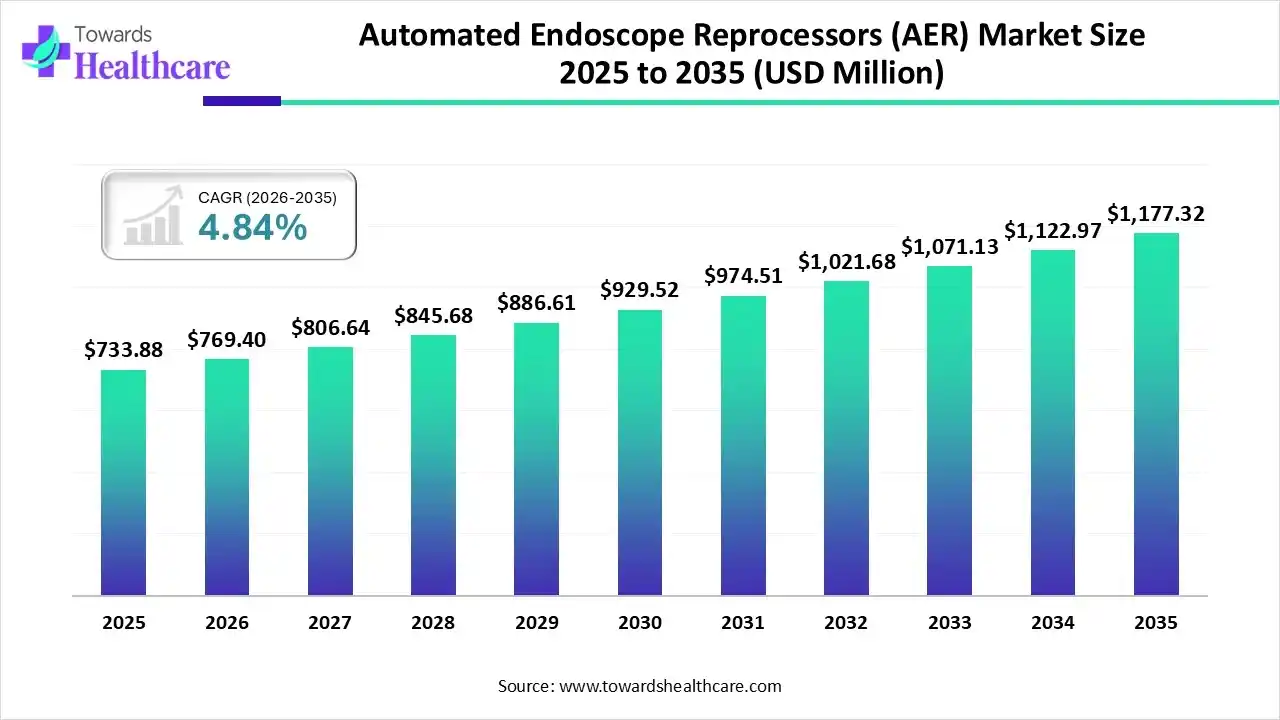

The global automated endoscope reprocessors (AER) market size is expected to be worth around USD 1177.32 million by 2035, from USD 733.88 million in 2025, growing at a CAGR of 4.84% during the forecast period from 2026 to 2035.

Market Size 2025 to 2035")

The automated endoscope reprocessors (AER) market is primarily driven by the increasing endoscopic procedures and an enhanced focus on patient safety. AERs are used in healthcare settings to reprocess endoscopes and their accessories. The demand for AERs is increasing, particularly in emerging economies, driven by the rapid expansion of healthcare infrastructure. Regulatory agencies establish stringent regulations on infection control, necessitating healthcare professionals to use AERs.

The automated endoscope reprocessors (AER) market comprises automated systems designed to clean, disinfect, and reprocess flexible and rigid endoscopes used in medical diagnostic and surgical procedures. AERs standardize and automate high-level disinfection (HLD), reducing manual handling, enhancing infection control, improving turnaround times, and ensuring compliance with healthcare sterilization standards. The market includes standalone AERs, integrated washer-disinfector systems, and accessory products (trays, connectors, disinfectants) used across hospitals, ambulatory surgical centers, specialty clinics, and endoscopy units.

Automated endoscope reprocessors (AERs) are specialized medical devices designed to automatically clean, disinfect, rinse, and dry reusable endoscopes, ensuring consistent reprocessing and reducing the risk of cross-contamination between patients. The automated endoscope reprocessors market is expanding due ti the increasing volume of minimally invasive procedures, growing emphasis on infection prevention, and stricter regulatory standards for endoscope reprocessing. Key trends include the adoption of smart AER systems with digital traceability, automated cycle documentation, and connectivity with hospital information systems. Technological advancements such as IoT-enabled monitoring, enhanced disinfectant technologies, and workflow automation are improving operational efficiency and patient safety. Future opportunities are driven by rising healthcare investments, increasing demand for advanced sterilization solutions in ambulatory surgical centers, and expansion of healthcare infrastructure in emerging, and continuous innovation in endoscope reprocessing technologies for improved compliance and performance.

As regulatory authorities and healthcare accreditation agencies emphasize standardized protocols for reprocessing of endoscopes, investment in advanced automated endoscope reprocessors (AERs) continues to grow. New technology innovations such as digital workflow integration, automated traceability, remote monitoring capability, and improved drying can increase reprocessing efficiencies while meeting compliance and quality assurance standards.

Continuing investments into healthcare infrastructure, increased endoscopy service capacity in developing countries, and rising use of minimally invasive procedures create the opportunity to expand the market; the transition toward patient safety, operational automation, and data-based sterilization management will drive the need for next-generation AERs. Because infection prevention and efficiency of procedures are a main focus of healthcare providers, an increased reliance on Automated Endoscope Reprocessor (AER) equipment will be an integral part of the modern endoscopy workflow and sterile processing environment.

Artificial intelligence (AI) plays a crucial role in introducing automation in AERs, thereby minimizing manual errors and enhancing operational efficiency. AI-based robotic systems are used for cleaning endoscopic systems. AI can detect the level of cleanliness in endoscopes and suggest a repeat reprocessing cycle. The robotic system is configured under lab conditions to grab, lift, and position a special cleaning tray with high accuracy. AI can avoid action against a given resistance through forced feedback control.

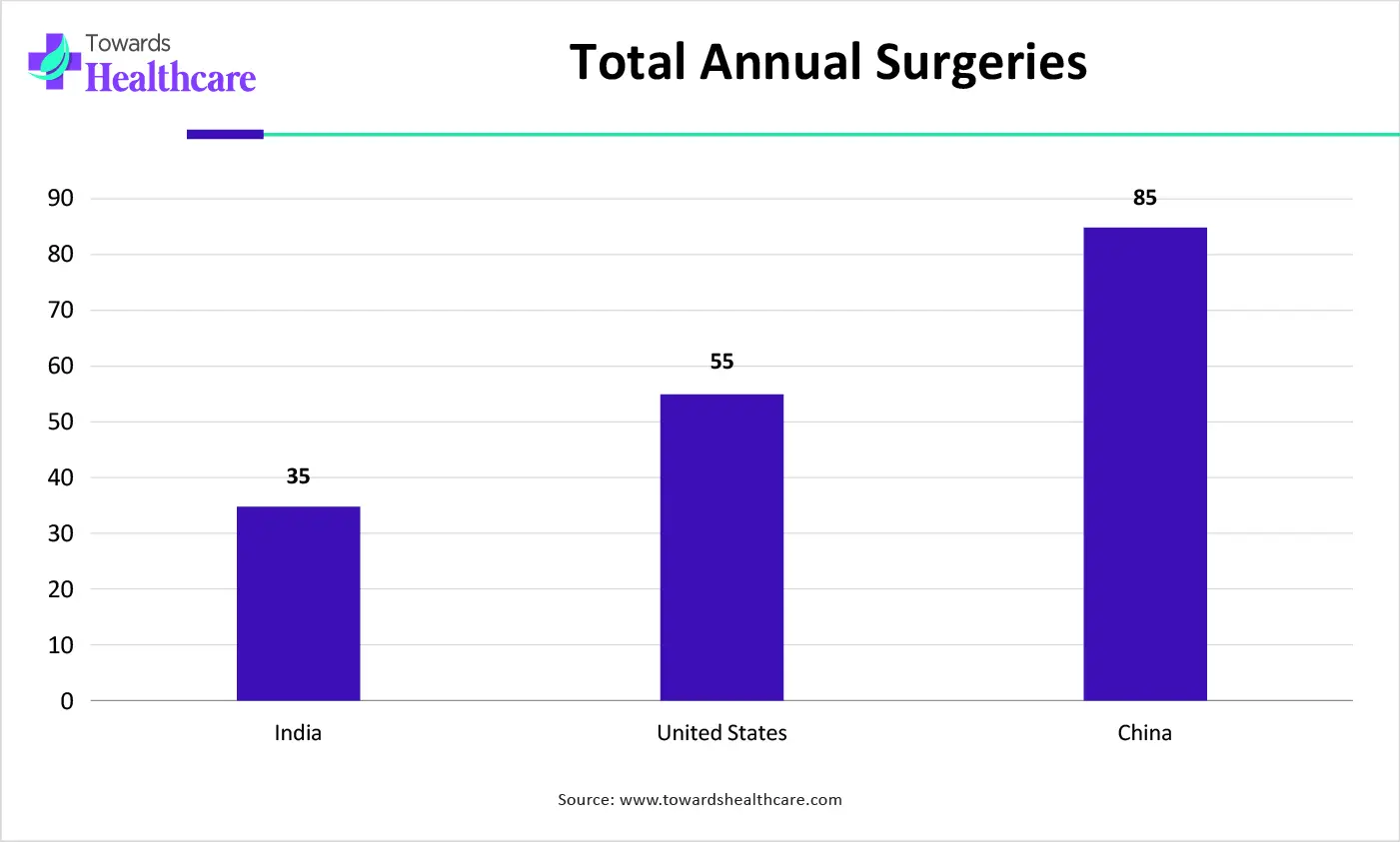

| Countries | Total Annual Surgeries |

| India | 35 |

| United States | 55 |

| China | 85 |

| Key Elements | Scope |

| Market Size in 2026 | USD 769.4 Million |

| Projected Market Size in 2035 | USD 1177.32 Million |

| CAGR (2026 - 2035) | 4.84% |

| Leading Region | North America by 38% |

| Key Applications | Gastrointestinal Endoscopy, Bronchoscopy, Urology, ENT Procedures, Pulmonology, Surgical Endoscopy |

| Primary End Users | Hospitals, Ambulatory Surgery Centers (ASCs), Specialty Clinics, Endoscopy Centers, Academic Medical Centers |

| Key Growth Drivers | Rising endoscopy procedures, stricter infection control regulations, increasing HAI concerns, automation adoption, digital traceability requirements |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Disinfection Technology, By End-User/Healthcare Setting, By Workflow Integration, By Service & Support, By Distribution Channel, By Region |

| Top Key Players | Advanced Sterilization Products, Custom Ultrasonics, Inc., STERIS Corporation, Olympus Corporation, Wassenburg Medical, Inc., Getinge AB, Ecolab, Steelco, MMM Group |

| Segments | Shares % |

| Standalone AER Systems | 45% |

| Integrated Washer-Disinfector AERs | 25% |

| High-Throughput/Multi-Scope AERs | 18% |

| Mobile/Portable AER Units | 12% |

Why Did the Standalone AER Systems Segment Dominate the Automated Endoscope Reprocessors (AER) Market?

The standalone AER systems segment held a dominant position with a share of approximately 45% in the market in 2025, due to their widespread availability and the ability to reprocess endoscopes efficiently. Standalone systems are easy to install in a healthcare facility and have a compact design. They are comparatively easy to use by healthcare professionals. They are adopted by smaller facilities, such as hospitals and ambulatory surgery centers, which have space constraints.

High-Throughput/Multi-Scope AERs

The high-throughput/multi-scope AERs segment is expected to grow at the fastest CAGR of approximately 14% in the market during the forecast period. Multi-scope AERs can be used to clean multiple endoscopes simultaneously. The dual basin system is most widely preferred as it improves workflow flexibility with two independent basins. It is highly consistent and enhances compliance with endoscope reprocessing.

| Segments | Shares % |

| High-Level Chemical Disinfection Systems | 60% |

| Automated Thermal/Heat-Assisted Disinfection | 18% |

| Hybrid (Chemical + Thermal) Systems | 14% |

| Enzymatic Pre-wash + Automated Disinfection | 8% |

Which Disinfection Technology Segment Dominated the Automated Endoscope Reprocessors (AER) Market?

The high-level chemical disinfection systems segment held the largest revenue share of approximately 60% in the market in 2025, due to the need for reprocessing of thermolabile endoscopes. Chemical sterilant processing systems circulate the disinfectant solution around the exterior and through the device channels for a limited exposure period after cleaning. They eliminate all viable microbial life, including bacterial spores.

Hybrid (Chemical + Thermal) Systems

The hybrid (chemical + thermal) systems segment is expected to grow with the highest CAGR of approximately 16% in the market during the studied years. Hybrid systems offer numerous combined benefits of both chemical and thermal systems. They can be used for a wide range of endoscopes, including those that are heat-sensitive and heat-resistant. They perform multiple functions, such as leak testing and high-level disinfection.

| Segments | Shares % |

| Hospitals | 50% |

| Ambulatory Surgical Centers (ASCs) | 20% |

| Diagnostic & Endoscopy Clinics | 15% |

| Specialty Care Centers | 9% |

| Outpatient Facilities | 6% |

How the Hospitals Segment Dominated the Automated Endoscope Reprocessors (AER) Market?

The hospitals segment contributed the biggest revenue share of approximately 50% in the market in 2025, due to favorable infrastructure and the increasing number of inpatient admissions. Patients prefer visiting hospitals for their treatment due to reimbursement policies and the presence of skilled professionals. Hospitals have professionals from various disciplines, providing multidisciplinary expertise to patients.

Ambulatory Surgical Centers (ASCs)

The ambulatory surgical centers (ASCs) segment is expected to expand rapidly with a CAGR of approximately 14% in the market in the coming years. The shifting trend towards ASCs encourages them to adopt AERs for endoscopic reprocessing. ASCs prefer outpatient services, eliminating the need for patients to stay overnight. They save exorbitant costs and time for patients and providers. They possess specialized equipment and infrastructure to provide outpatient services.

| Segments | Shares % |

| Integrated with Central Sterile Services Department (CSSD) | 48% |

| Standalone Reprocessing Workflows | 35% |

| Networked/IoT-Enabled Reprocessing Workflows | 17% |

Which Workflow Integration Segment Led the Automated Endoscope Reprocessors (AER) Market?

The integrated with central sterile services department (CSSD) segment led the market with a share of approximately 48% in the market in 2025, due to the need to deliver safe medical equipment and devices for surgery and patient care services. CSSD plays a pivotal role in patient safety through incorporating infection prevention and control principles with validated decontamination processes. The segmental growth is also attributed to stringent regulatory guidelines by regulatory agencies or the WHO.

Networked/IoT-Enabled Workflows

The networked/IoT-enabled workflows segment is expected to witness the fastest growth with a CAGR of approximately 18% in the market over the forecast period. AERs are increasingly connected with IoT-enabled technology to enhance safety, efficiency, and compliance in healthcare settings. IoT-enabled technologies facilitate automated documentation and connectivity around the healthcare ecosystem. The increasing integration of digitization in healthcare organizations boosts the segment’s growth.

| Segments | Shares % |

| Preventive Maintenance | 42% |

| Consumables/Accessories Supply Services | 22% |

| Installation & Training | 15% |

| Validation & Compliance Support | 12% |

| Remote Diagnostics & Monitoring | 9% |

What Made Preventive Maintenance the Dominant Segment in the Automated Endoscope Reprocessors (AER) Market?

The preventive maintenance segment accounted for the highest revenue share of approximately 42% in the market in 2025. Preventive maintenance enables healthcare professionals to maintain high-quality endoscopes before any surgery, reducing delays in patient treatment. Regulatory agencies release guidelines to conduct annual maintenance or cleaning procedures of AERs. Concerned authorities maintain records of preventive maintenance and reprocessing equipment, such as leak testers.

Remote Diagnostics & Monitoring

The remote diagnostics & monitoring segment is expected to show the fastest growth with a CAGR of 19% over the forecast period. Service providers offer remote diagnostics & monitoring services of endoscopes to check for the desired maintenance. This eliminates the need for healthcare professionals to visit the service center. They have skilled professionals to provide relevant expertise and solutions to complex problems.

| Segments | Shares % |

| Direct OEM/Manufacturer Sales | 55% |

| Distributors & Dealers | 25% |

| Group Purchasing Organizations (GPOs) | 12% |

| Online/E-commerce Channels | 8% |

Why Did the Direct OEM/Manufacturer Sales Segment Dominate the Automated Endoscope Reprocessors (AER) Market?

The direct OEM/manufacturer sales segment registered its dominance over the global market with a share of approximately 55% in 2025. Providers can directly purchase AERs from manufacturers or original equipment manufacturers (OEMs) at affordable rates. This reduces the extra costs associated with wholesalers or distributors. The increasing awareness of local/indigenous manufacturing of AERs favors the segment’s growth.

Online/E-commerce Channels

The online/e-commerce channels segment is expected to account for the highest growth with a CAGR of approximately 15% over the forecast period. The advent of online platforms, the burgeoning e-commerce sector, and the increasing adoption of smartphones propel the segment’s growth. Online platforms enable professionals to purchase high-quality AERs from anywhere across diverse geographical locations. The rapidly evolving supply chain infrastructure also potentiates the demand for online platforms for purchasing medical devices.

Market NA, EU, APAC, LA and MEA Share 2025 (%)")

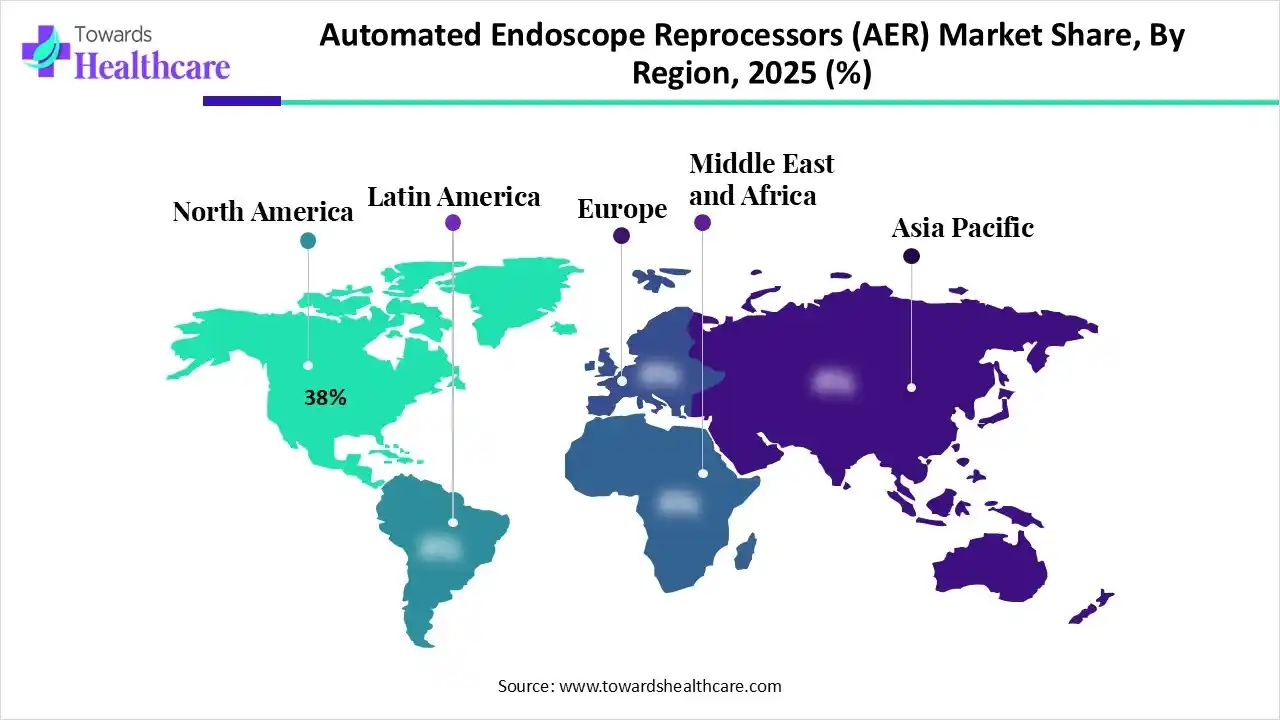

North America dominated the global market by 38% share in 2025. The presence of key players, a robust healthcare infrastructure, and favorable regulatory support are factors that contribute to market growth in North America. The increasing number of inpatient surgeries and the rising adoption of advanced technologies favor market growth. North American hospitals also drive the demand for efficient and compliant disinfection.

U.S.

The U.S. recorded over 34 million hospital admissions in 2023, according to the AHA Survey 2025. This is due to the increasing chronic disease prevalence among Americans. Key players, such as Custom Ultrasonics, Inc., Ecolab, and STERIS Corporation, are major contributors to the market in the U.S. The Food and Drug Administration (FDA) regulates the approval of AERs in the U.S.

Canada

Canada’s automated endoscope reprocessors (AER) market is steadily expanding due to the increased emphasis on infection control and patient safety within the healthcare system. Companies that provide endoscopic surgical procedures are growing at a rapid pace because of increased demand for these types of surgeries, continued investment in modernizing hospitals, and increasing compliance with strict guidelines related to the reprocessing of medical devices. AER systems are being implemented by healthcare facilities that use them for both improving efficiency and consistency in the reprocessing of medical devices, as well as sustaining regulatory compliance with various health authorities.

Mexico

Mexico has steadily been growing in the automated endoscope reprocessor market because of the increased number of endoscopic procedures, growing hospital infrastructure, and increased focus on infection control in healthcare facilities. The investment in automated reprocessing technologies by healthcare facilities is improving patient safety, reducing risks of contamination, and ensuring compliance with changing standards for sterilization and disinfection.

Asia-Pacific is expected to grow at the fastest CAGR in the market during the forecast period. The rising prevalence of chronic disorders, the growing geriatric population, and the increasing hospital admissions boost the market. Government organizations of various countries, like China and India, provide funding to adopt advanced technological products in healthcare organizations. Government bodies promote the indigenous manufacturing of medical devices, encouraging foreign companies to set up their manufacturing facilities in the region.

China

China’s national prevalence of chronic disorders is approximately 81.1%, representing 179.9 million Chinese older adults. The Chinese government has launched the “Action Plan for Promoting Large-Scale Equipment Renewal and the Trade-in of Consumer Goods” to boost equipment investments in the healthcare sector by over 25% by 2027 from 2023.

India

India's growth in the automated endoscope reprocessor market is primarily due to the increase in gastrointestinal and pulmonary endoscopy procedures, the expansion of healthcare infrastructure, and increasing awareness of infection control. The growth of private hospitals and specialty clinics is helping to drive adoption of automated systems that improve the efficiency of reprocessing and compliance with regulations.

Japan

Japan is a major player in the market for automated endoscope reprocessors, including an elderly population, high rates of endoscopic diagnostic procedures, and some of the most advanced hospitals and healthcare systems in the world. Because of the need to implement new automated technologies for reprocessing endoscopes to improve infection control, reduce the risk of human error during manual processing, and comply with stringent reprocessing standards for all medical devices, infectious disease providers have made significant investments in automated reprocessing technologies.

Europe is expected to grow at a notable CAGR in the foreseeable future. Favorable government support and the growing demand for digitization in the healthcare sector propel the market. The presence of key players and the increasing investments and collaborations among companies augment market growth. European nations are becoming hubs for advanced treatment owing to the burgeoning healthcare sector. The growing awareness of infection risks boosts the adoption of AER for patient safety.

Companies like STERIS Corporation, Olympus Corporation, and PFE Medical provide high-quality AER machines in the UK. The increasing number of laparoscopic surgeries potentiates the demand for AERs. It is estimated that over 60,000 laparoscopic cholecystectomies (LC) are performed annually in the UK.

Germany

Germany is one of the leading European markets for automated endoscope reprocessors because of advanced healthcare technology, strict hygiene regulations, and a high number of procedures performed. Hospitals and diagnostic centers are increasingly implementing automated reprocessing solutions to provide reliable disinfecting quality, operational efficiency, and compliance with the strict standards applied to protect patient safety.

Netherlands

The Netherlands is experiencing an increase in demand for automated endoscope reprocessors as the country places a strong emphasis on healthcare quality and infection control. The use of advanced reprocessing technologies by healthcare providers has enabled streamlined workflows, minimization of the potential for human error, and compliance with the highest standards for cleaning and disinfecting endoscopes in a variety of medical facilities.

")

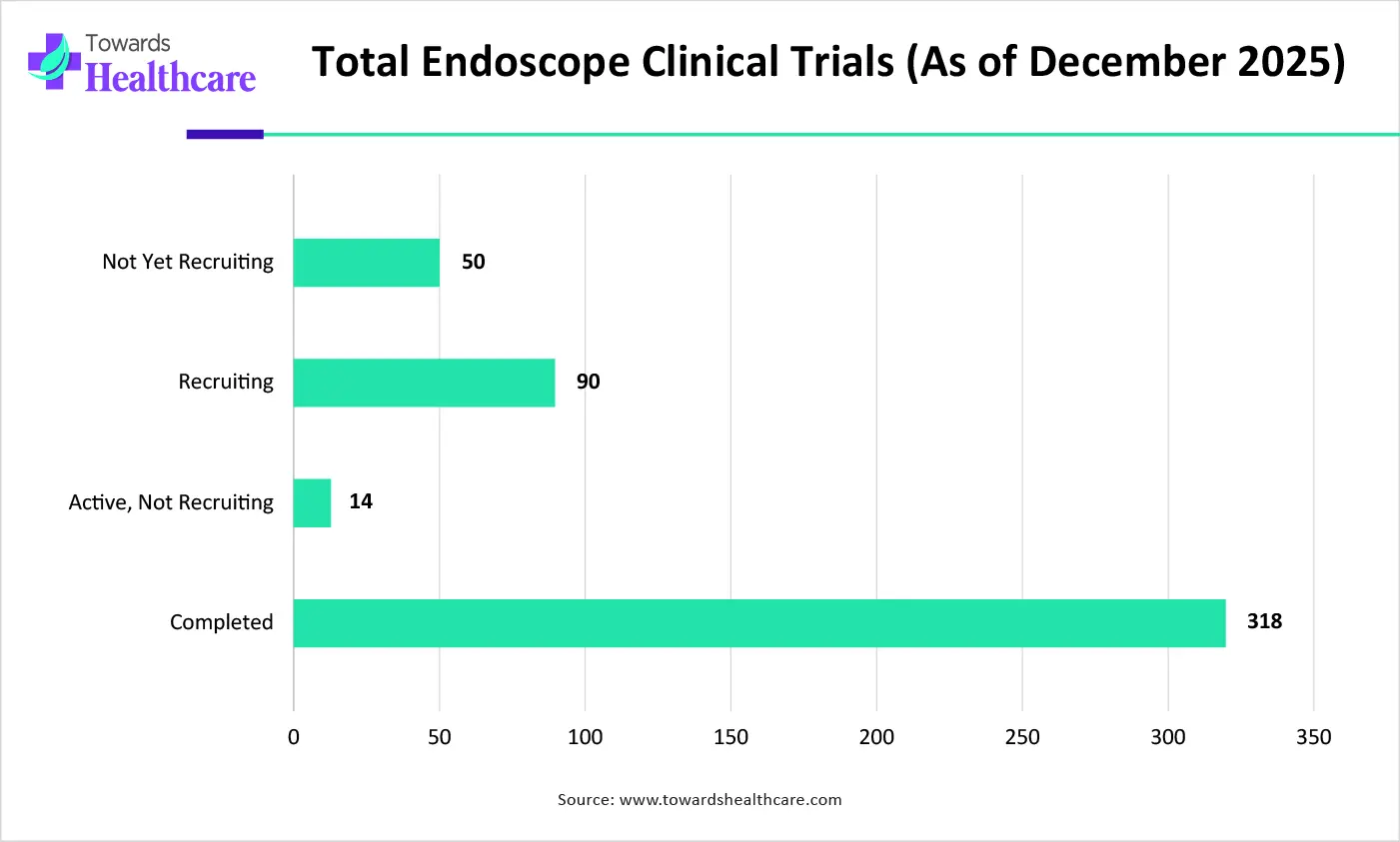

| Stages of Clinical Trials | Total Number of Endoscope Clinical Trials (as of December 2025) |

| Not Yet Recruiting | 50 |

| Recruiting | 90 |

| Active, Not Recruiting | 14 |

| Completed | 318 |

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Olympus, STERIS, Getinge, Soluscope | Develop reprocessing technologies, automation systems, disinfection protocols |

| Product Manufacturers | STERIS, Olympus, Getinge, Cantel Medical (Medivators), Steelco | Manufacture AER equipment and supporting accessories |

| Service Providers | STERIS, Getinge, Olympus | Installation, maintenance, validation, training, lifecycle support |

| Platform Providers | Olympus, STERIS, Getinge | Integrated infection prevention and reprocessing workflow platforms |

| CROs/CDMOs (Limited Relevance) | Not a primary segment | AER market is primarily device-driven rather than outsourced development-driven |

| Software Vendors | Steelco, Getinge, Olympus | Traceability, workflow management, compliance documentation software |

| Research Institutions | CDC-linked research centers, university hospitals, infection prevention institutes | Conduct validation studies and reprocessing effectiveness research |

| End-User Industries | Healthcare Providers, Hospitals, Ambulatory Surgery Centers | Primary users of AER systems |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 68% | 24% | 8% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| STERIS plc | Dublin | Ireland | Global leader in infection prevention and endoscope reprocessing | System 1E, Reliance Endoscope Processing Systems, AER solutions |

| Olympus Corporation | Tokyo | Japan | World's largest endoscopy manufacturer with integrated reprocessing portfolio | OER Series AERs, endoscope reprocessing systems |

| Getinge AB | Gothenburg | Sweden | Major infection control and sterile processing supplier | ED-FLOW AER, washer-disinfectors, reprocessing solutions |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Steelco S.p.A. | Riese Pio X, Treviso | Italy | Specialized reprocessing equipment manufacturer | EW Series AER systems |

| Soluscope SAS | Aubagne | France | Dedicated endoscope reprocessing company | Soluscope Series AERs |

| Wassenburg Medical B.V. | Dodewaard | Netherlands | Highly specialized AER provider with strong European footprint | WD440 PT, WD425 Series |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| SciCan Ltd. | Toronto, Ontario | Canada | Active in instrument and endoscope reprocessing technologies | Endoscope cleaning and disinfection systems |

| Shinva Medical Instrument Co., Ltd. | Zibo, Shandong | China | Growing presence in hospital disinfection equipment | Automated endoscope reprocessors |

| Matachana Group | Barcelona | Spain | Infection control and reprocessing specialist | Endoscope washer-disinfectors |

Strengths

Weaknesses

Opportunities

Threats

In June 2026, “Endoscopy departments are under increasing pressure to ensure consistent, validated endoscope reprocessing while keeping procedures running safely and on time,” says Stéphane Le Roy, President, Surgical Workflows at Getinge. “Aquadis Endo 110 is built to deliver reliable and fully traceable reprocessing, helping our customers maintain control, consistency and confidence in demanding daily operations.”

By Product Type

By Disinfection Technology

By End-User/Healthcare Setting

By Workflow Integration

By Service & Support

By Distribution Channel

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar