Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

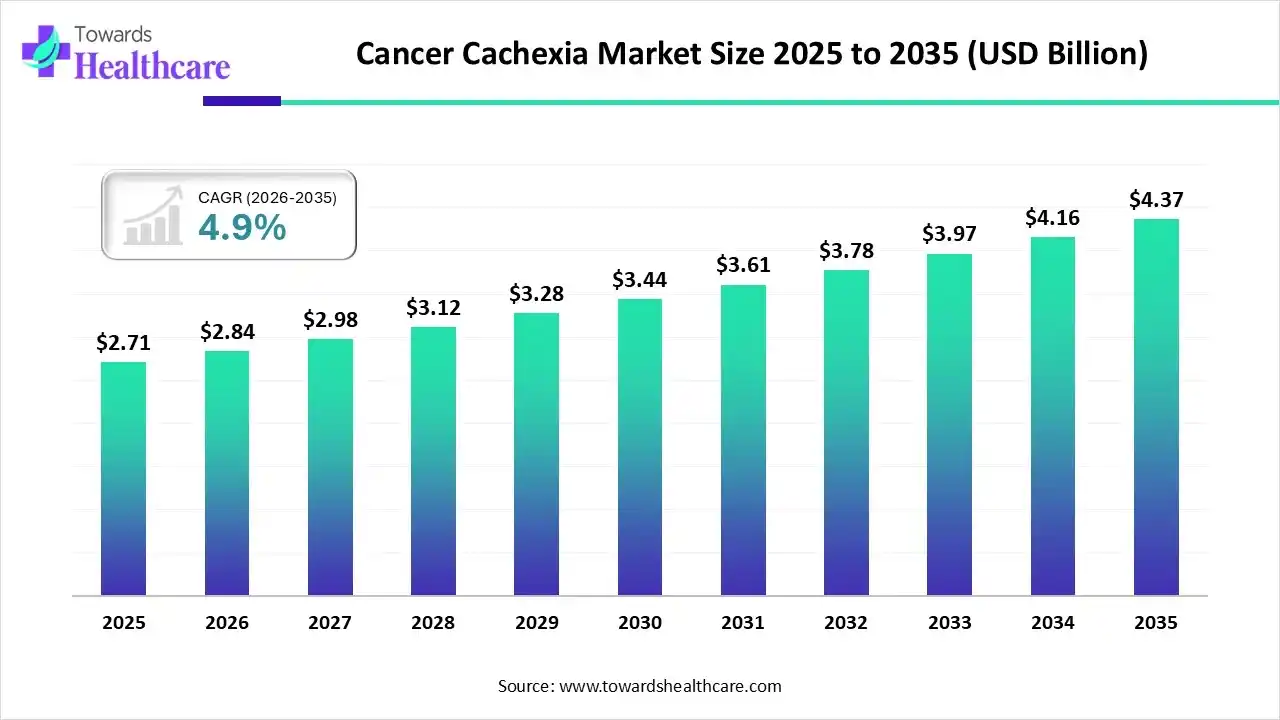

The global cancer cachexia size was estimated at USD 2.71 billion in 2025 and is predicted to increase from USD 2.84 billion in 2026 to approximately USD 4.37 billion by 2035, expanding at a CAGR of 4.9% from 2026 to 2035.

The growing global cancer burden is increasing the cases of cancer cachexia, which is fueling the demand for their effective treatment options. AI is also being used to develop and optimize various treatment options and monitoring devices, where companies are investing and launching various products targeting the disease. Moreover, the presence of advanced healthcare, growing adoption of advanced treatment options, and stringent regulations are promoting the market growth.

| Key Elements | Scope |

| Market Size in 2026 | USD 2.84 Billion |

| Projected Market Size in 2035 | USD 4.37 Billion |

| CAGR (2026 - 2035) | 4.9% |

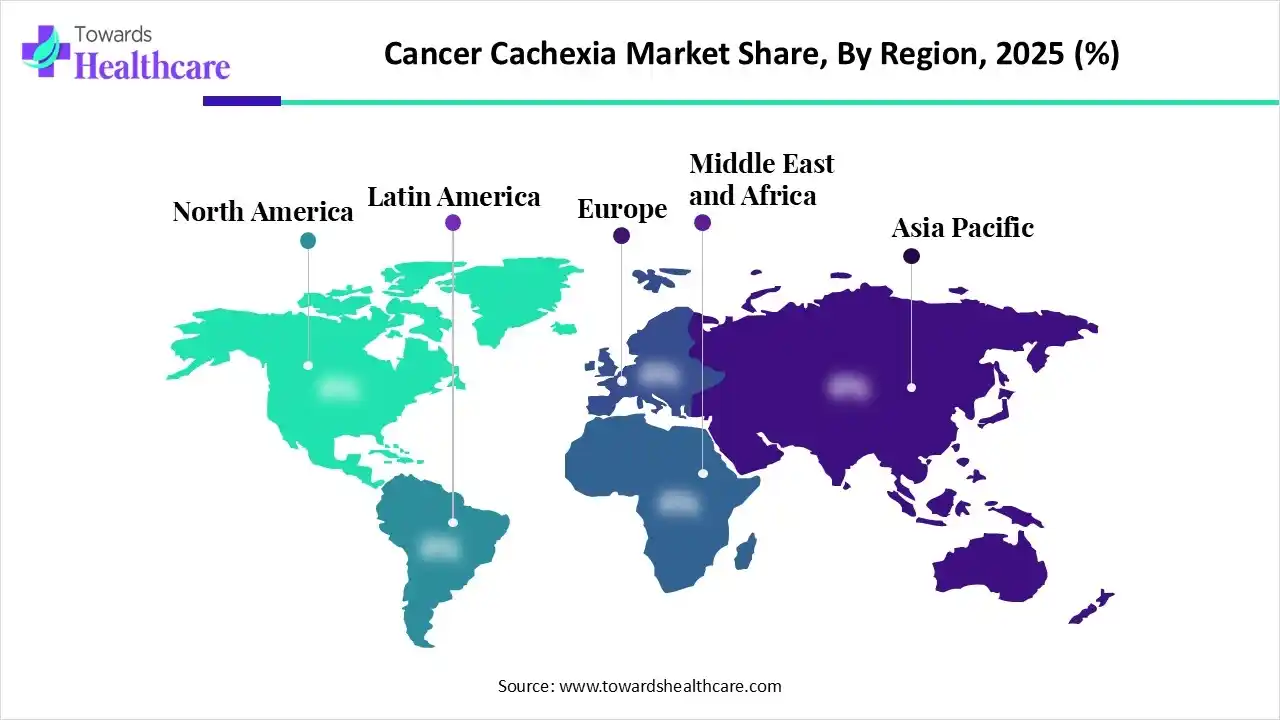

| Leading Region | North America |

| Market Segmentation | By Treatment, By Type, By Distribution Channel, By Region |

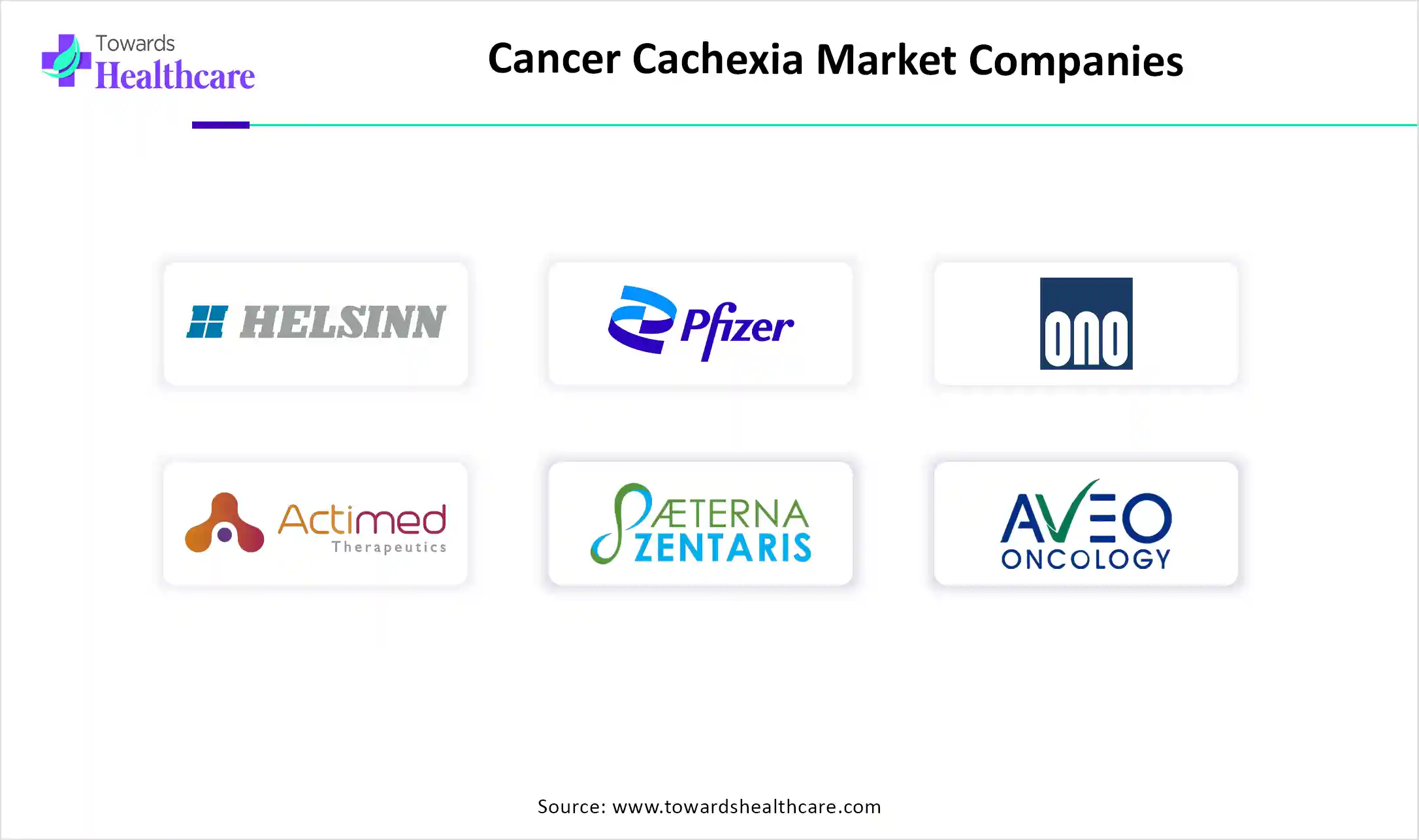

| Top Key Players | Helsinn Group, Pfizer, Inc., Ono Pharmaceutical Co., Ltd., Actimed Therapeutics, Aeterna Zentaris Inc., AVEO Oncology, Artelo Biosciences, Tetra Bio-Pharma, NGM Biopharmaceuticals, Endevica Bio |

The cancer cachexia market is driven by increasing cancer burden and unmet clinical need for effective weight and muscle preservation treatments. Cancer cachexia refers to the complex metabolic syndrome leading to weight loss, appetite loss, and muscle wasting, which occurs in various cancer patients. Therefore, treatments such as appetite stimulants, anti-inflammatory agents, anabolic agents, metabolic modulators, and nutritional interventions are provided to the patient with cancer cachexia.

Cancer cachexia metabolic syndrome associated with cancer, characterised by progressive loss of skeletal muscle mass, weight loss, reduced appetite, and functional decline that cannot be fully reversed by conventional nutritional support. The cancer cachexia market is expanding due to the increasing global burden of cancer, growing recognition of cachexia as a critical unmet medical need, and rising demand for comprehensive supportive oncology care. Key trends include the development of targeted therapies, combination treatment approaches, and personalized nutrition strategies. Technological advancements in biomarker discovery, molecular diagnostics, and precision medicine are improving early identification and pateint managements. Future opportunities are emerging drug development, expanding research on anti-inflammatory and anabolic therapies, and greater integration of multidisciplinary care to improve patient outcomes and quality of life.

Different types of AI models are being developed to detect patients at high risk of developing cachexia. It also detects biomarkers and predicts patient response to the treatment, identifying early metabolic changes and promoting the development of personalized therapies. It is used in drug discovery and development, where their continuous disease monitoring also helps in tracking the cachexia progression, which is increasing their use in the development of various devices.

The incidence of various cancer types like gastrointestinal, lung, and pancreatic cancer is increasing the number of cachexia cases, which is driving the demand for effective treatment options.

The companies are focusing on developing personalized medications depending on the patient's genetic and metabolic profile.

Different types of wearable devices and software are being developed to monitor the muscle mass and weight of cancer cachexia patients, which is increasing their adoption rates.

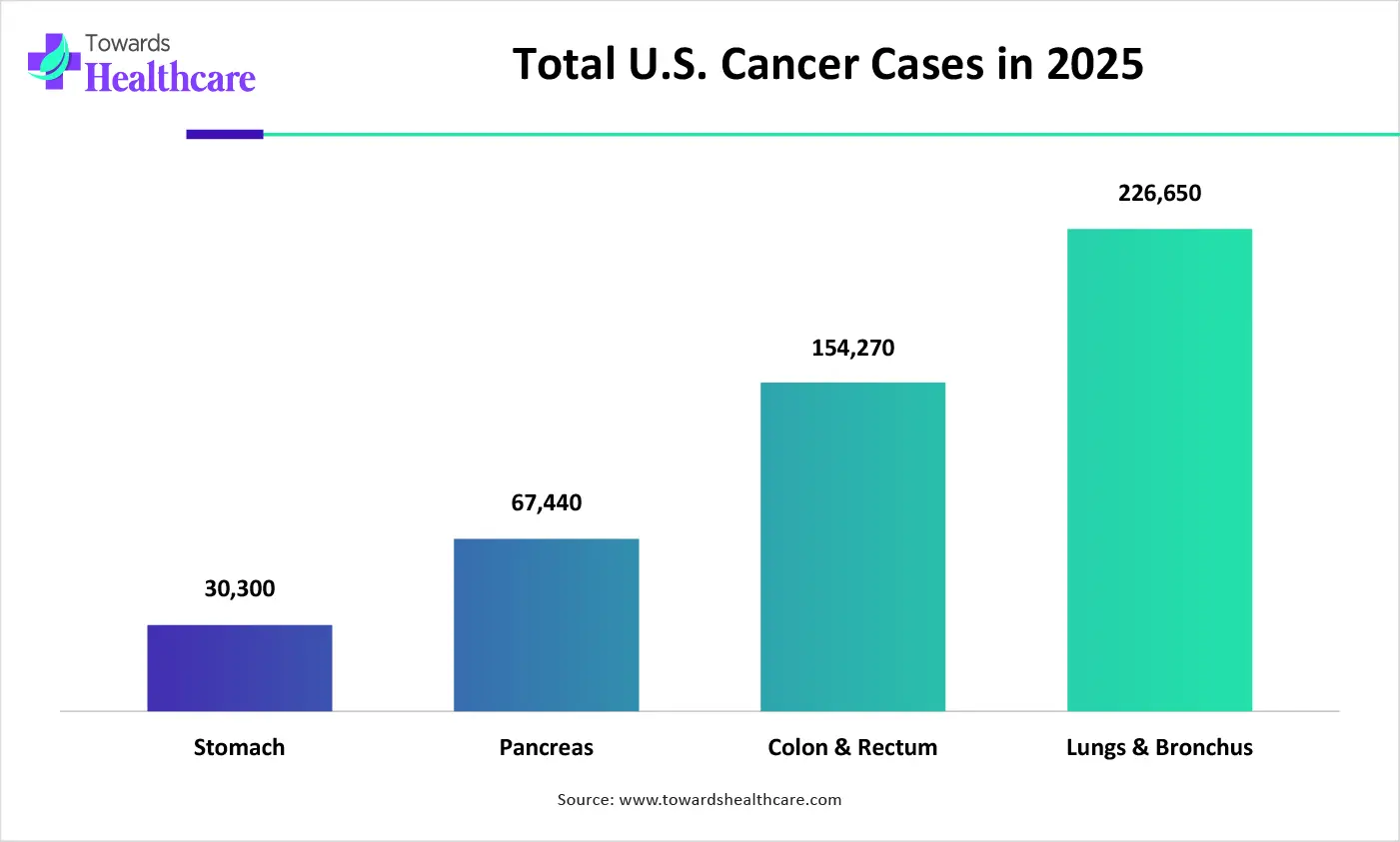

| Cancer Types | New cases |

| Stomach | 30,300 |

| Pancreas | 67,440 |

| Colon & Rectum | 154,270 |

| Lungs & Bronchus | 226,650 |

Why Did the Appetite Stimulants Segment Dominate in the Cancer Cachexia Market in 2025?

The appetite stimulants segment held the largest share in the market in 2025, as they helped in addressing weight loss by increasing appetite and calorie intake. They also offered a rapid onset of action, which increased their adoption rates. Additionally, their wide availability also increased their use and acceptance rates.

Cannabinoid Receptor Agonists

The cannabinoid receptor agonists segment is expected to show the fastest growth rate during the predicted time, due to their appetite stimulation action by targeting CB1 or CB2 receptors. At the same time, the growing preference for natural therapies and protective relief from pain and nausea is also increasing their use.

Which Type Segment Held the Dominating Share of the Cancer Cachexia Market in 2025?

The lung cancer segment held the dominating share of the market in 2025, due to growth in its incidence rates. This increased the number of patients with cancer cachexia, which enhanced the use of various treatment options. This, in turn, increased their innovations to reduce muscle wasting and weight loss.

Pancreatic Cancer

The pancreatic cancer segment is expected to show the highest growth during the forthcoming years, as it can lead to maximum cancer cachexia cases. Moreover, their rapid progression is also increasing their severity. Similarly, the lack of treatment options is increasing the use of various treatment options and enhancing innovations.

What Made Hospital Pharmacies the Dominant Segment in the Cancer Cachexia Market in 2025?

The hospital pharmacies segment led the market in 2025, due to growth in the patient volume. They also provided supportive care along with other treatment options. At the same time, they also offered supervision, which helped to monitor the severe cases, which enhanced the patient trust, and increased patient outcomes and dependence on them.

Online Pharmacies

The online pharmacies segment is expected to show the fastest growth rate during the upcoming years, as they offer a wide range of treatment options and enhance accessibility across remote areas. They are also providing home deliveries, which is enhancing the patient's convenience and comfort. Similarly, discounts are also attracting them.

")

North America dominated the cancer cachexia market in 2025, due to the growth in the incidence of cancer cases. The presence of advanced healthcare infrastructure also increased the use of various treatment options, where the early adoption of advanced solutions also enhanced their acceptance rates. The industries are also contributing to their R&D, where the growing healthcare investments have also increased their use, which has contributed to the market growth.

U.S. Drives Growth in the Cancer Cachexia Market

The U.S. is witnessing significant growth in the cancer cachexia market due to the high prevalence of cancer, strong investments in oncology research, increasing pharmaceutical companies, ongoing clinical trials, advanced healthcare infrastructure, and growing adoption of innovative therapies, which are further accelerating market growth.

The presence of the advanced healthcare sector is increasing the use of various treatments in the U.S. to tackle the growing cancer cachexia. This, in turn, is driving the innovation where the R&D investments are supporting them. Additionally, increasing awareness is also increasing their early diagnosis and demand for effective treatment.

| Stomach Cancer Deaths in 2025 | 10,780 |

| Stomach Cancer New Cases in 2025 | 30,300 |

Canada Strengthens Its Cancer Cachexia Marekt

Canada is witnessing growth in the cancer cachexia market due to increasing cacner prevalence, rising investments in oncology research, and growing awareness of supportive cancer care. Expanding clinical trials, improved access to advanced healthcare services, and increasing adoption of perosnalized treatment approaches are enhancing patient management and driving continued market growth.

Asia Pacific is expected to host the fastest-growing cancer cachexia market during the forecast period, due to expanding healthcare infrastructure. This is increasing the number of oncology centers, which is increasing the use of various advanced therapies and appetite stimulants, while rapid urbanization is also increasing their incidence rates. The growing government initiatives are also increasing their acceptance rates, enhancing the market growth.

The growing pancreatic and gastrointestinal cancer cases in India are increasing the demand for effective treatment options to reduce the risk of cancer cachexia. India is also experiencing a rise in the oncology centres, which are increasing the adoption of various cancer cachexia treatment options, which are supported by funding.

China Accelerates Growth in the Cancer Cachexia Marekt

China is witnessing significant growth in the cancer cachexia market due to its large patient population, expanding oncology healthcare infrastructure, and increasing investments in cancer research. Rising awareness of supportive care, growing adoption of innovative therapies, improving access to advanced treatment options, and government initiatives to strengthen cancer care services are further driving market expansion.

India Emerges as a High-Growth Cancer Cachexia Market

India is witnessing notable growth in the cancer cachexia market due to the increasing burden of cancer, rising awareness of supportive oncology care, and expanding healthcare infrastructure. Growing investment sin cancer treatment facilities, increasing clinical research activities, improved access to advanced therapaies, and greater focus on early access to advanced therapies, and greater focus on early nutritional intervention are further supporting market growth.

Europe is expected to grow significantly in the cancer cachexia market during the forecast period, due to the presence of an advanced healthcare sector, which is increasing the use of appetite stimulants and other supportive treatment options. The increasing cancer incidences are also driving their R&D and clinical trials where the growing government health awareness programs are also increasing their early diagnosis, promoting the market growth.

UK Market Growth

The UK is increasingly adopting various supportive treatment options to overcome cancer cachexia. The presence of an advanced healthcare system and growing cancer cases are also increasing their use. Moreover, the growing focus on enhancing the quality of life is also promoting their innovations.

Germany Strengthens Its Cancer Cachexia Market

Germany is witnessing significant growth in the cancer cachexia market due to its advanced oncology care infrastructure, increasing cancer prevalence, and strong investments in clinical research. Growing adoption of personalized treatment approaches, supportive government healthcare policies, and the presence of leading pharmaceutical companies are accelerating the development and adoption of innovative cachexia therapies.

| Companies | Headquarters | Cancer Cachexia Treatment Products |

| Helsinn Group | Lugano, Switzerland | Anamorelin and Adlumiz |

| Pfizer, Inc. | New York, U.S. | Ponsegromab |

| Ono Pharmaceutical Co., Ltd. | Osaka, Japan | Anamorelin |

| Actimed Therapeutics | Berkshire, UK | S-pindolol benzoate |

| Aeterna Zentaris Inc. | Quebec City, Canada | AEZS-130 |

| AVEO Oncology | Massachusetts, U.S. | Rilogrotug |

| Artelo Biosciences | California, U.S. | ART27.13 |

| Tetra Bio-Pharma | Ontario, Canada | Caumz |

| NGM Biopharmaceuticals | Francisco, U.S. | NGM120 |

| Endevica Bio | Michigan, U.S. | TCMCB07 |

By Treatment

By Type

By Distribution Channel

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar