Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

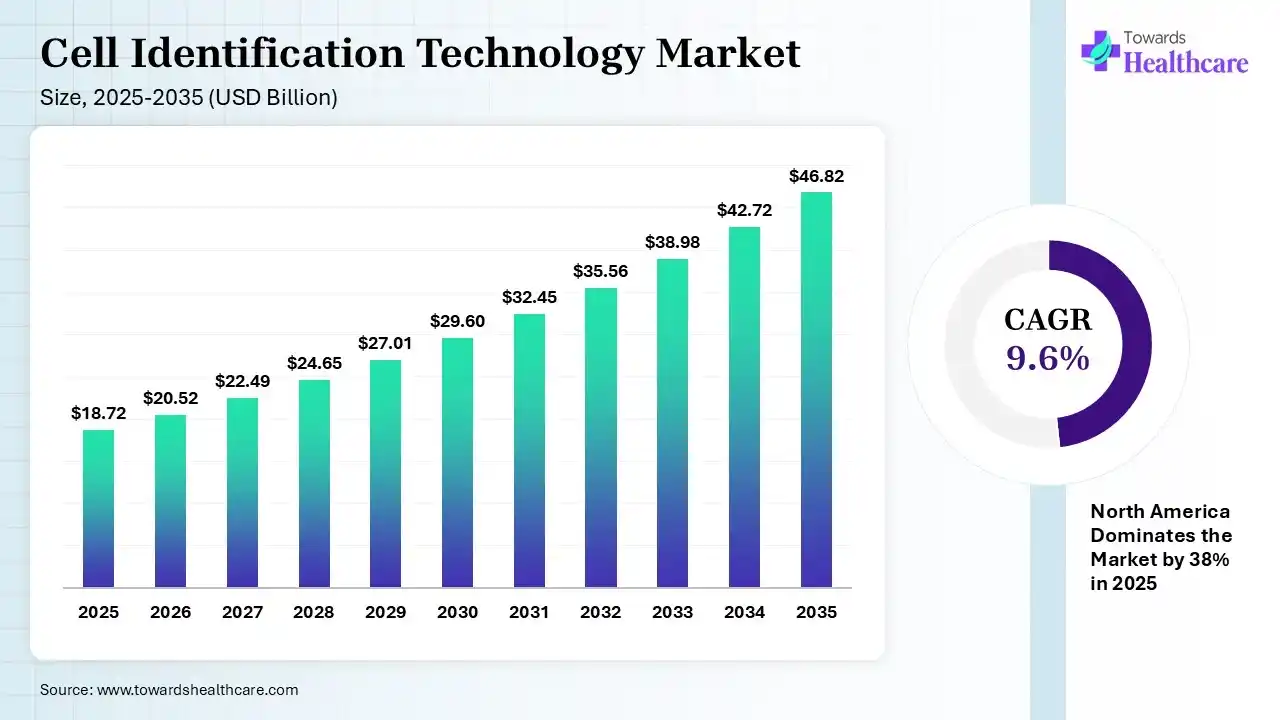

The global cell identification technology market size was estimated at USD 18.72 billion in 2025 and is predicted to increase from USD 20.52 billion in 2026 to approximately USD 46.82 billion by 2035, expanding at a CAGR of 9.6% from 2026 to 2035. The global market expansion is driven by a rise in technological breakthroughs, diverse chronic diseases, & broader purposes in research and clinical studies. The leading companies are fostering the development of AI-powered solutions, which streamlines the overall workflow with enhanced accuracy.

")

Firstly, the cell identification technology market is defined as the use of diverse methods, such as single-cell RNA sequencing (scRNA-seq), image processing/microscopy, & STR profiling, to categorise, identify, & authenticate cells or cell types within biological samples. The widespread adoption of these approaches is propelled by the rapid advances in flow cytometry, automation, & AI-driven high-content screening, with a prominent emphasis on tailored therapies that require deeper, individual-cell-level assessment.

The globe is extensively leveraging U-Net, Mask R-CNN, & StarDist to fragment cell cytoplasm & nuclei in microscopic images, which detects limits in crowded samples to enable accurate counting & morphology analysis. Alongside the use of AI assisting in identifying & classifying various cell types, which relied on morphological characteristics & biochemical markers, even in label-free, bright-field images.

Cell identification technology companies advanced analytical methods and instruments used to detect, classify, characterize, and monitor different cell types based on their genetic, molecular, phenotypic, and functional characteristics. It plays a vital role in biomedical research, clinical diagnostics, drug discovery, immunology, oncology, and regenerative medicine. The cell identification technology market is expanding due to the increasing demand for precision medicine, growing focus on cell-based therapies, and rising investments in life sciences research. Technological advancements in single-cell sequencing, flow cytometry, AI-powered imaging, multi-omics analysis, and automated cell sorting are improving accuracy and research efficiency. Growing applications in biomarker discovery, personalized medicines, and cancer diagnostics are creating significant future opportunities. Increasing collaborations between biotechnology companies and research institutions, along with expanding adoption of high-throughput analytical platforms, are further accelerating innovation and supporting long-term market growth.

Breakthrough in Single-Cell Analysis & High-Throughput Sorting

Researchers are stepping into droplet microfluidics to allow the faster & rigorous encapsulation of single cells, which is significant for assessing cell heterogeneity.

Fostering Label-Free Identification

The emerging microfluidics are shifting toward label-free separation based on intrinsic physical properties to preserve cell integrity.

Exploring Multimodal Molecular Imaging

The market is pushing the integration of PET & optical imaging to monitor stem cell viability & trafficking in vivo.

| Table | Scope |

| Market Size in 2026 | USD 20.52 Billion |

| Projected Market Size in 2035 | USD 46.82 Billion |

| CAGR (2026 - 2035) | 9.6% |

| Leading Region | North America by 38% |

| Key Applications | Cell biology research, immunology, oncology, stem cell research, precision medicine, disease diagnosis, drug discovery, biomarker identification, cell therapy development |

| Primary End Users | Academic research institutes, pharmaceutical companies, biotechnology firms, hospitals, diagnostic laboratories, CROs |

| Key Challenges | High instrument costs, data complexity, standardization issues, regulatory requirements, sample preparation variability, shortage of skilled personnel |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Technology, By Product, By Application, By End User, By Region |

| Top Key Players | Thermo Fisher Scientific, Becton Dickinson and Company, Danaher Corporation, Merck KGaA, Agilent Technologies, Bio-Rad Laboratories, Sartorius AG, Illumina, QIAGEN, Miltenyi Biotec |

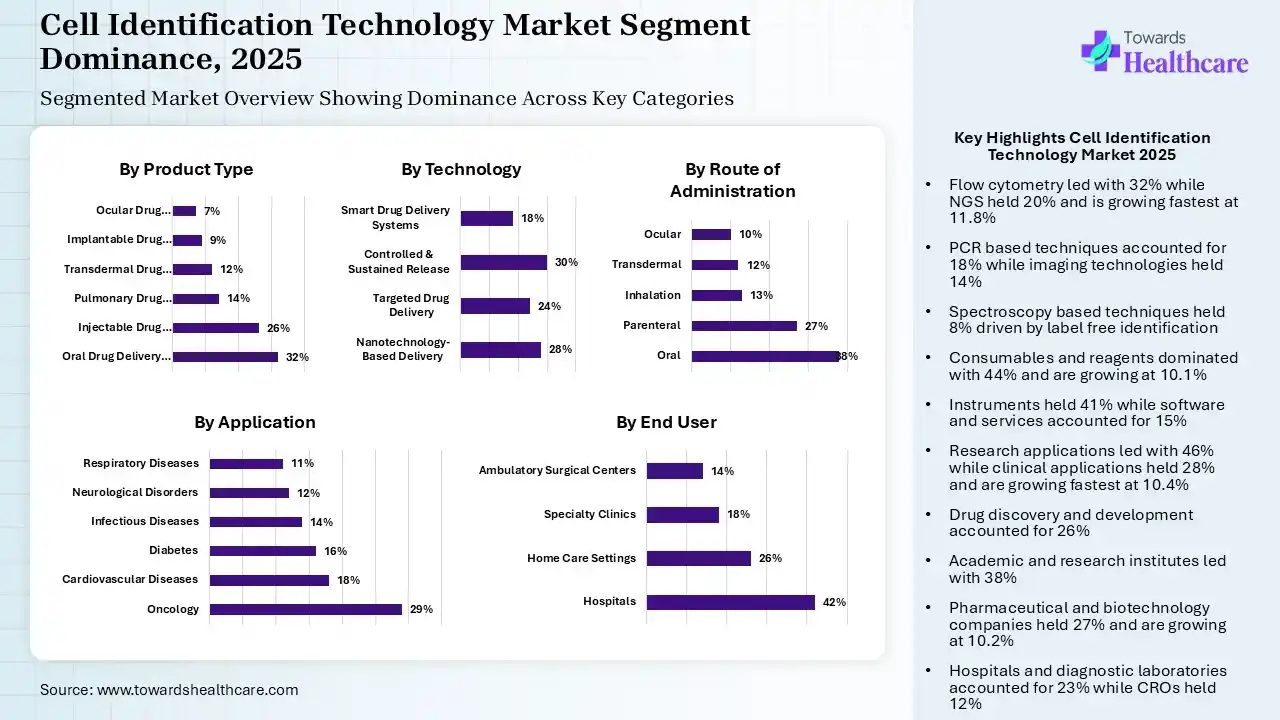

| Segment | Share 2025 (%) |

| Flow Cytometry | 32% |

| PCR-based Techniques | 18% |

| Next-Generation Sequencing (NGS) | 20% |

| Imaging-based Technologies | 14% |

| Microarray Technology | 8% |

| Spectroscopy-based Techniques | 8% |

The Flow Cytometry Segment Led the Market in 2025

In 2025, the flow cytometry segment held a 32% share of the cell identification technology market. This has a prominent role in immunophenotyping, evaluating cell viability, & determining rare cell populations in clinical & research conditions. The use of Spectral Flow Cytometry provides increased spectral resolution & multicolor detection, which enables more complex, high-dimensional cell analysis.

The next-generation sequencing (NGS) segment held 20% of the market share in 2025 and is predicted to expand at 11.8% CAGR. Key catalysts are the surging adoption of single-cell sequencing technologies, allowing detailed cellular profiling & genomic insights, with notable affordability. The trend is spurring integration of long-read sequencing with single-cell techniques to allow the detection of full-length transcripts and isoforms.

The PCR-based techniques segment captured a lucrative share of 18%, due to the escalating use in genetic analysis & infectious disease testing. Also, this has greater sensitivity in precise cell identification, & shift towards digital PCR, microfluidic lab-on-a-chip systems, & viability PCR (vPCR).

The imaging-based technologies segment accounted for 14% share of the cell identification technology market. Expansion is fueled by advancing high-content imaging that enhances cell visualization. Also, AI integration offers optimized accuracy of cell identification & broader utilisation in drug screening.

The spectroscopy-based techniques segment held 8% share in 2025, as it allows label-free cell identification with greater precision. Also, in advanced research environments, adoption is bolstering, coupled with immersive innovations in mass spectrometry.

| Segment | Share 2025 (%) |

| Instruments | 41% |

| Consumables & Reagents | 44% |

| Software & Services | 15% |

The Consumables & Reagents Segment Dominated the Market in 2025

The consumables & reagents segment captured a 44% share of the cell identification technology market in 2025 & is estimated to expand at 10.1% CAGR in the coming era. Dominance is driven by the growing demand for antibodies, assay kits, media, & probes required for flow cytometry, PCR, & cell culture. Moreover, progressing CAR-T cell therapies & regenerative medicine fosters the need for persistent, high-quality, clinical-grade reagents & culture consumables.

The instruments segment held 41% share in 2025, due to the rising capital investment in advanced analytical instruments. Also, the ongoing technological advances are boosting capabilities & emphasizing lab automation.

The software & services segment captured a notable share of 15% of the cell identification technology market in 2025. The world is experiencing a significant need for data analysis in complex datasets, while cloud platforms allow scalable solutions. Companies are pushing their unification with AI to boost decision-making efficiency.

| Segment | Share 2025 (%) |

| Research Applications | 46% |

| Clinical Applications | 28% |

| Drug Discovery & Development | 26% |

The Research Applications Segment Was Dominant in the Market in 2025

In 2025, the research applications segment held the largest share of a 46% of the market. Cell identification plays a key role in high-throughput screening, toxicity testing (ADMET studies), & validation of drug responses in preclinical studies. The cell identification technology has immense applications to track the differentiation & ageing of stem cells, especially in 3D organoid cultures, which mimic natural tissues more precisely.

The clinical applications segment captured 28% share of the cell identification technology market in 2025 & is anticipated to expand fastest at 10.4% CAGR. Along with a rise in chronic disease cases, the market is highly demanding accurate diagnostics & personalized treatments. Also, implementing the integration of these technologies into hospital workflows to assist in expansion.

The drug discovery & development segment accounted for 26% share, due to accelerating pharmaceutical R&D investments. This also covers a major role in biomarker identification and validation, & significant assistance in rapid & extensive drug pipelines. The use of CETSA is pushing direct drug-target interaction within living cells.

| Segment | Share 2025 (%) |

| Academic & Research Institutes | 38% |

| Pharmaceutical & Biotechnology Companies | 27% |

| Hospitals & Diagnostic Laboratories | 23% |

| Contract Research Organizations (CROs) | 12% |

The Academic & Research Institutes Segment Led the Market in 2025

The academic & research institutes segment held a major share of 38% of the cell identification technology market in 2025. With surging funding for biological research activities, these institutes are impelling research, product development, & validation of cell-based assay & roll out of technologies. Nowadays, they are using Short Tandem Repeat (STR) profiling, DNA barcoding, & karyotyping to ensure employed cells are labelled.

In the future, the pharmaceutical & biotechnology companies segment captured 27% of the total market share and is predicted to witness rapid growth at 10.2% CAGR. Their progression is propelled by escalating investment in drug discovery and development, with a vital requirement for precise cell identification in clinical trials. Also, certain regions are increasingly launching biotech startups, which raises demand for cell identification technologies.

Whereas, the hospitals & diagnostic laboratories segment held a significant share of 23% of the cell identification technology market. The worldwide rising demand for diagnostic accuracy in clinical settings, expanding patient volume, further assists in technology adoption.

The contract research organizations (CROs) segment captured 12% share in 2025, due to the accelerating outsourcing trend in pharmaceutical research, which drives the higher demand for these latest technologies. Their inexpensive services & broader advanced capabilities are impelling their substantial development across the global market.

")

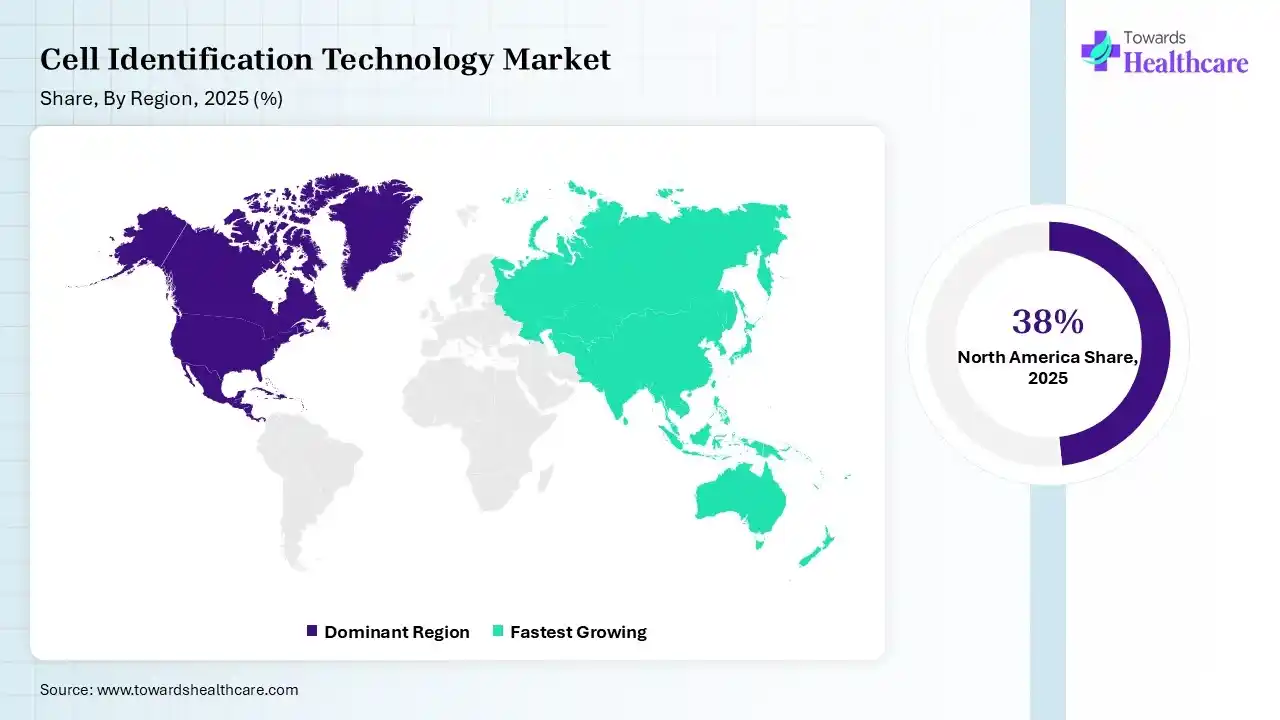

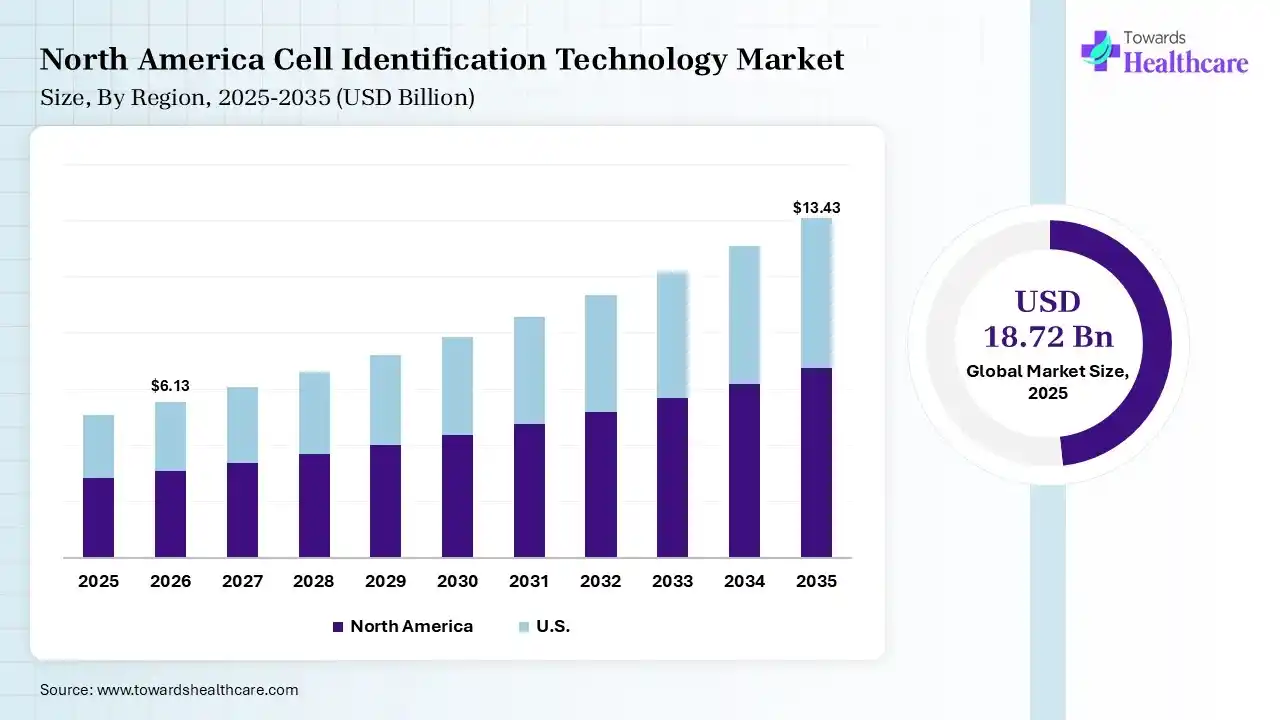

By capturing a 38% share of the cell identification technology market, North America registered dominance in 2025. The regional drivers include the possession of well-developed & leading biotech companies and research institutes, coupled with higher healthcare expenditure. However, Canada has authorized its first CRISPR-based therapy & strengthened CAR-T cell manufacturing capabilities.

U.S. Market Trends

Additionally, the U.S. market dominated with 30% share, with a key goal to establish AI-based, label-free cell identification by using convolutional neural networks (CNNs) to estimate DNA-level identities from microscopic images.

For instance,

Canada Accelerates Innovation in the Cell Identification Technology Market

Canada is experiencing significant growth in the cell identification technology market due to rising investments in life sciences research, expanding adoption of single-cell analysis and flow cytometry, and strong government support for precision medicine initiatives. Collaborations between biotechnology companies, research institutions, and healthcare organizations are accelerating innovation. Growing demand for advanced cancer research, regenerative medicines, and cell-based therapies is further driving market expansion.

Asia Pacific held 24% share in 2025 & is estimated to expand fastest at 10.8% CAGR in the cell identification technology market. Majorly, the region is experiencing pivotal investments in R&D, including drug discovery, clinical trials, & single-cell analysis for targeted cancer therapies. As well as particular countries, like China, Japan & India are actively investing in biosimilar development, cell therapies, & vaccine manufacturing.

India Emerges as a High-growth Hub for Cell Identification Technology

On the other hand, India has demonstrated the OptiDrop platform for affordable single-cell analysis, AI-powered diagnostics, & indigenous CAR-T cell therapy (NEXCAR-19) for cancer. These are significantly led by DBT and BIRAC, which focus on making tailored medicine accessible.

India is significantly growing in the cell identification technology market due to increasing in biotechnology and life science research, expanding adoption of advanced cell analysis technologies, and rising demand for precision diagnostics. Growth in biopharmaceutical research, regenerative medicine, and cancer studies, along with expanding research infrastructure and government support for biotechnology innovation, is further accelerating market expansion.

Europe accounted for 26% share in 2025 & is predicted to expand significantly at 9.2% CAGR. This region has a well-nurtured academic research base & alliances. Also, Europe is fostering precision medicine, with rigorous regulatory support that surges technology adoption. Europe has implemented CARAT, which enhances the automation & affordability of CAR-T cell manufacturing for cancer.

Germany Market Trends

Besides this, Germany is widely adopting more sophisticated, automated, single-cell analysis for oncology, stem cell research, & biopharma. Moreover, researchers are developing AI-assisted imaging, high-precision sorting, & molecular methods, such as SNP-based authentication, to ensure cell line integrity.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Thermo Fisher Scientific, BD, Danaher, Illumina, QIAGEN | Develop core cell analysis and identification technologies |

| Product Manufacturers | Bio-Rad, Sartorius, Agilent, Miltenyi Biotec, Merck KGaA | Manufacture instruments, reagents, assays, and consumables |

| Service Providers | Charles River Laboratories, Labcorp, Quest Diagnostics | Provide testing, validation, and analytical services |

| Platform Providers | 10x Genomics, Parse Biosciences, Standard BioTools | Deliver integrated single-cell and multiomics platforms |

| CROs/CDMOs | Charles River Laboratories, ICON plc, IQVIA | Support pharmaceutical and biotechnology research programs |

| Software Vendors | SOPHiA GENETICS, Standard BioTools, QIAGEN Digital Insights | Cell analytics, bioinformatics, AI-driven interpretation |

| Research Institutions | Broad Institute, Mayo Clinic, MD Anderson Cancer Center, NIH | Technology validation, translational research, biomarker discovery |

| End-User Industries | Biotechnology, Pharmaceuticals, Diagnostics, Academic Research, Cell Therapy | Major adopters of cell identification technologies |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 63% | 27% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Thermo Fisher Scientific | Waltham, Massachusetts | USA | Global leader in cell analysis, flow cytometry, imaging and molecular biology | Attune Flow Cytometers, Invitrogen reagents, cell imaging systems |

| Becton Dickinson and Company | Franklin Lakes, New Jersey | USA | Dominant player in flow cytometry and cell sorting | FACSymphony, FACSCanto, spectral flow cytometry platforms |

| Danaher Corporation | Washington, D.C. | USA | Owns Beckman Coulter Life Sciences and Molecular Devices | CytoFLEX, cell counters, imaging systems |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Agilent Technologies | Santa Clara, California | USA | Major provider of cell analysis and imaging technologies | Seahorse analyzers, cell imaging platforms |

| Bio-Rad Laboratories | Hercules, California | USA | Strong presence in flow cytometry and PCR technologies | ZE5 Cell Analyzer, ddPCR systems |

| Sartorius AG | Göttingen | Germany | Growing cell analysis and imaging portfolio | iQue Cytometers, CellCelector systems |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| 10x Genomics | Pleasanton, California | USA | Pioneer in single-cell sequencing technologies | Chromium Single Cell Platform |

| Standard BioTools | South San Francisco, California | USA | Advanced single-cell and proteomics platforms | Hyperion Imaging System, CyTOF |

| Parse Biosciences | Seattle, Washington | USA | Fast-growing single-cell transcriptomics company | Evercode Whole Transcriptome solutions |

In May 2026,“As we enter the Company’s next phase, now is the right time for a leadership transition, and Zach is the right person to lead Allogene forward. He is a deeply respected physician-scientist and energizing leader with a clear vision for how emerging technologies can continue to expand the potential of allogeneic CAR T”, said Dr. David Chang, M.D., Ph.D., will transition from his role as President and Chief Executive Officer, effective

Strengths

Weaknesses

Opportunities

Threats

By Technology

By Product

By Application

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar