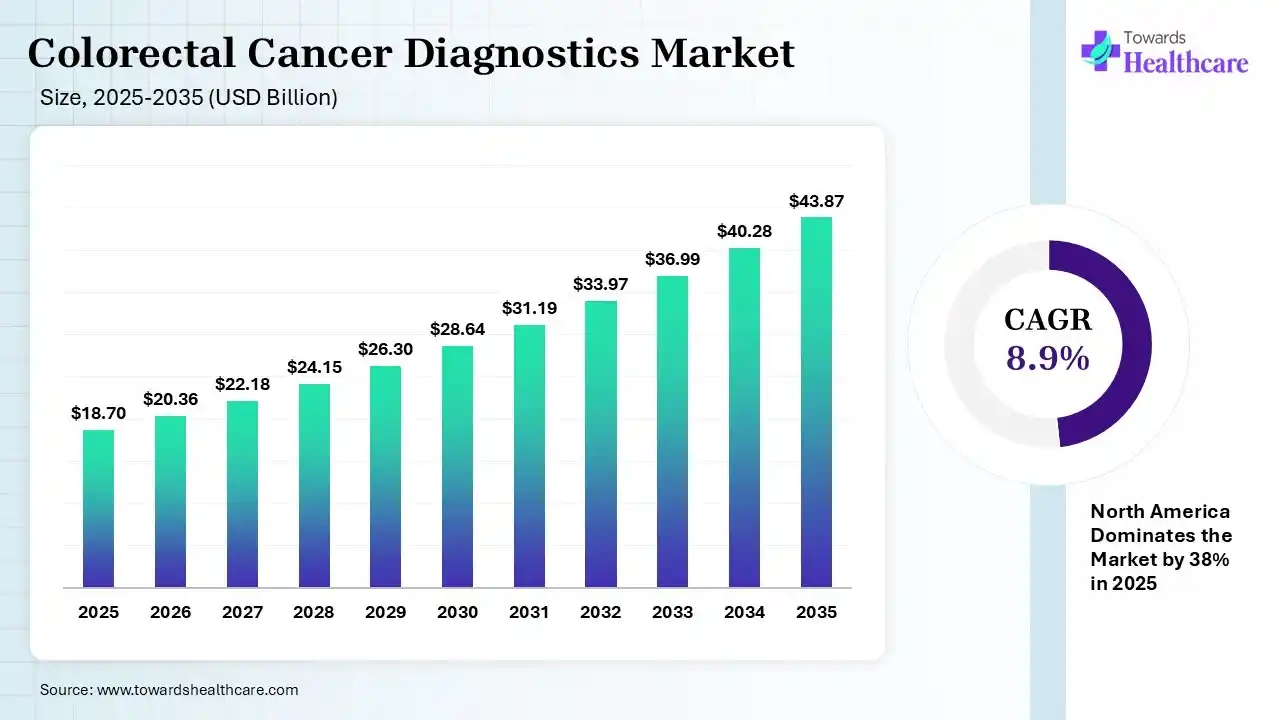

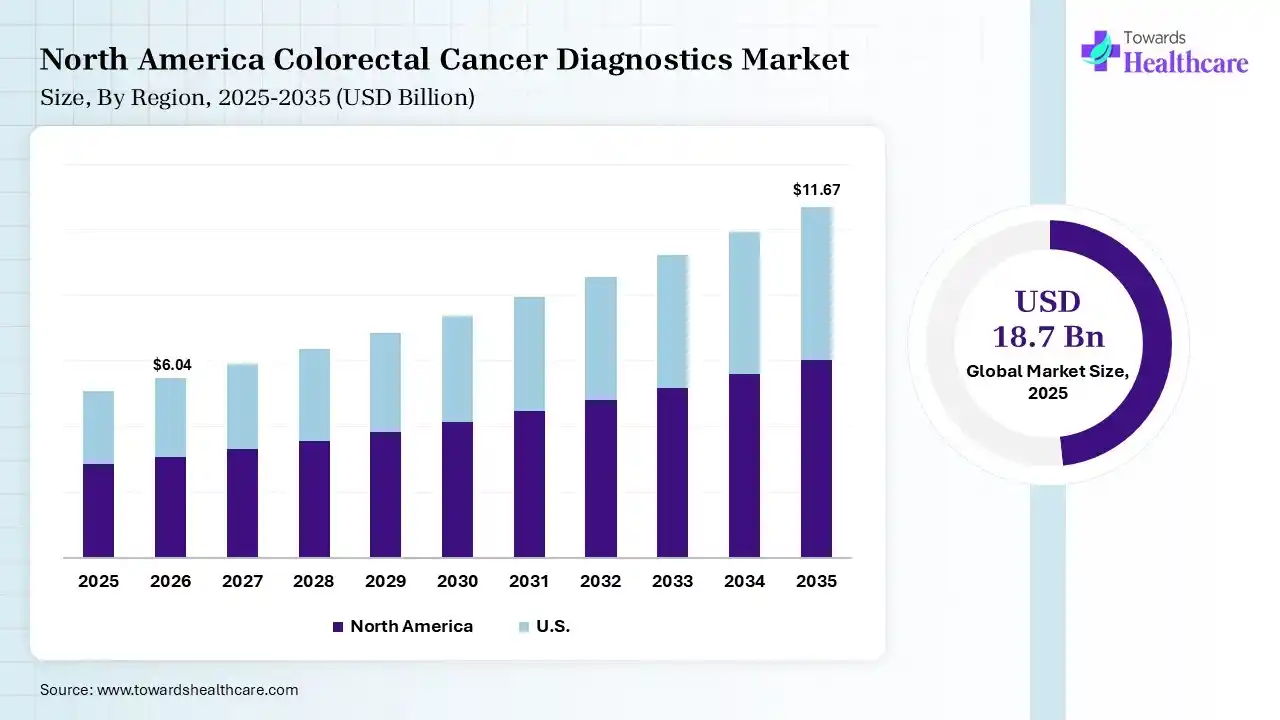

The global colorectal cancer diagnostics market size was estimated at USD 18.7 billion in 2025 and is predicted to increase from USD 20.36 billion in 2026 to approximately USD 43.87 billion by 2035, expanding at a CAGR of 8.9% from 2026 to 2035. A gradual rise in CRC incidence & broadening awareness, with robust screening programs, are driving the demand for these diagnostics. Besides this, the market is transforming AI-assisted solutions & the latest molecular diagnostics.

")

The colorectal cancer diagnostics market covers the integrated, systematic application of medical tests & imaging procedures to detect malignant cells in the colon or rectum. These approaches support locating tumors, finding pre-cancerous polyps, & ensure cancer presence by using tissue sampling. However, the global demand is driven by the increasing cases, broader adoption of non-invasive screening, and the latest molecular diagnostics.

Colorectal cancer diagnostics involve the use of screening, imaging, molecular testing, biomarker analysis, and laboratory techniques to detect colorectal cancer at an early stage, access diseases progression, and guide personalized treatment decisions. The colorectal cancer at an early stage, assess disease progression, and guide personalized treatment decisions. The colorectal cancer diagnostics market is expanding due to the rising incidence of colorectal cancer, increasing awareness of routine screening, and growing demand for early and accurate diagnosis.

Technological advancements in liquid biopsy, next-generation sequencing (NGS), artificial intelligence-assisted imaging, stool DNA testing, and molecular diagnostics are improving diagnostic accuracy and clinical efficiency. Growing adoption of non-invasive screening methods and precision oncology is creating significant future opportunities. Increased investments in cancer research, expanding diagnostic infrastructure, and supportive government screening initiatives are further accelerating market growth. Continuous innovation in biomarker discovery and companion diagnostics is expected to enhance early detection, improve patient outcomes, and support personalized cancer care.

Primarily, the leading healthcare organizations are employing AI algorithms to assess histopathologic images & whole-slide images (WSIs) to classify benign from malignant tissues. Whereas, eventual advances are promoting machine learning in the analysis of blood-based biomarkers, fluorescence spectroscopy, & complete blood counts. Additionally, the trend is rigorously fostering AI by utilizing CT & MRI imaging data to assist in anticipating tumor staging, grading & patient response to therapy.

Developing Liquid Biopsies & Biomarkers

Emerging blood tests spur the detection of circulating tumor DNA (ctDNA) or methylated DNA to find early-stage CRC and monitor recurrence.

Seeking Advanced Stool-Based Molecular Tests

Gradual efforts are innovating multitarget stool DNA tests & analyzing fecal miRNA signatures to enhance detection accuracy, especially for precancerous lesions.

Prospective Integrations

The market will explore the unification of AI with endoscopy (Computer-Aided Detection - CADe) & imaging to boost adenoma detection rates & lower false negatives during colonoscopy.

| Table | Scope |

| Market Size in 2026 | USD 20.36 Billion |

| Projected Market Size in 2035 | USD 43.87 Billion |

| CAGR (2026 - 2035) | 8.9% |

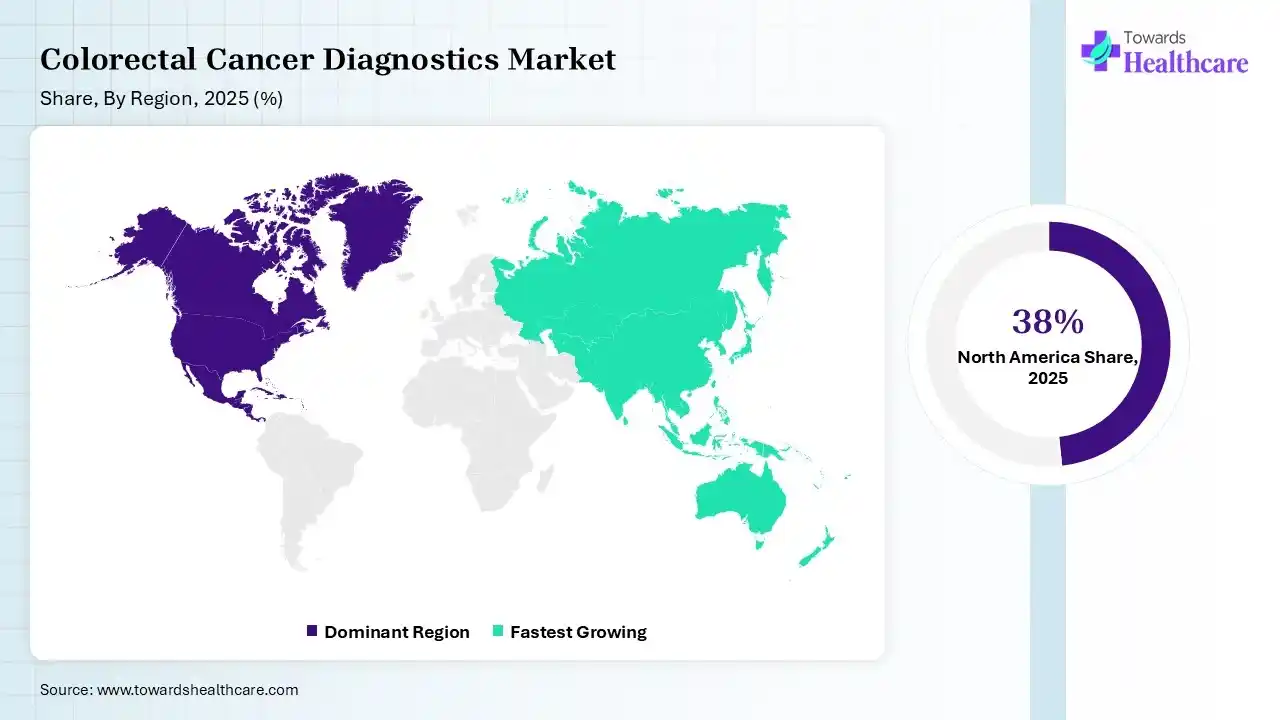

| Leading Region | North America by 38% |

| Key Applications | Screening, Early Detection, Diagnosis, Molecular Profiling, Treatment Selection, Disease Monitoring, Recurrence Detection |

| Primary End Users | Hospitals, Diagnostic Laboratories, Cancer Centers, Research Institutes, Ambulatory Surgical Centers |

| Key Growth Drivers | Rising CRC incidence, expansion of screening programs, adoption of liquid biopsy, molecular diagnostics, AI-assisted pathology and imaging, aging population |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Test Type, By Technology, By Application, By End User, By Region |

| Top Key Players | Exact Sciences Corporation, F. Hoffmann-La Roche Ltd (Roche Diagnostics), Quest Diagnostics Incorporated, Danaher Corporation, Guardant Health, Inc., Abbott, Fujifilm Holdings Corporation, Epigenomics AG, Eiken Chemical Co., Ltd , Olympus Corporation |

| Segment | Share 2025 (%) |

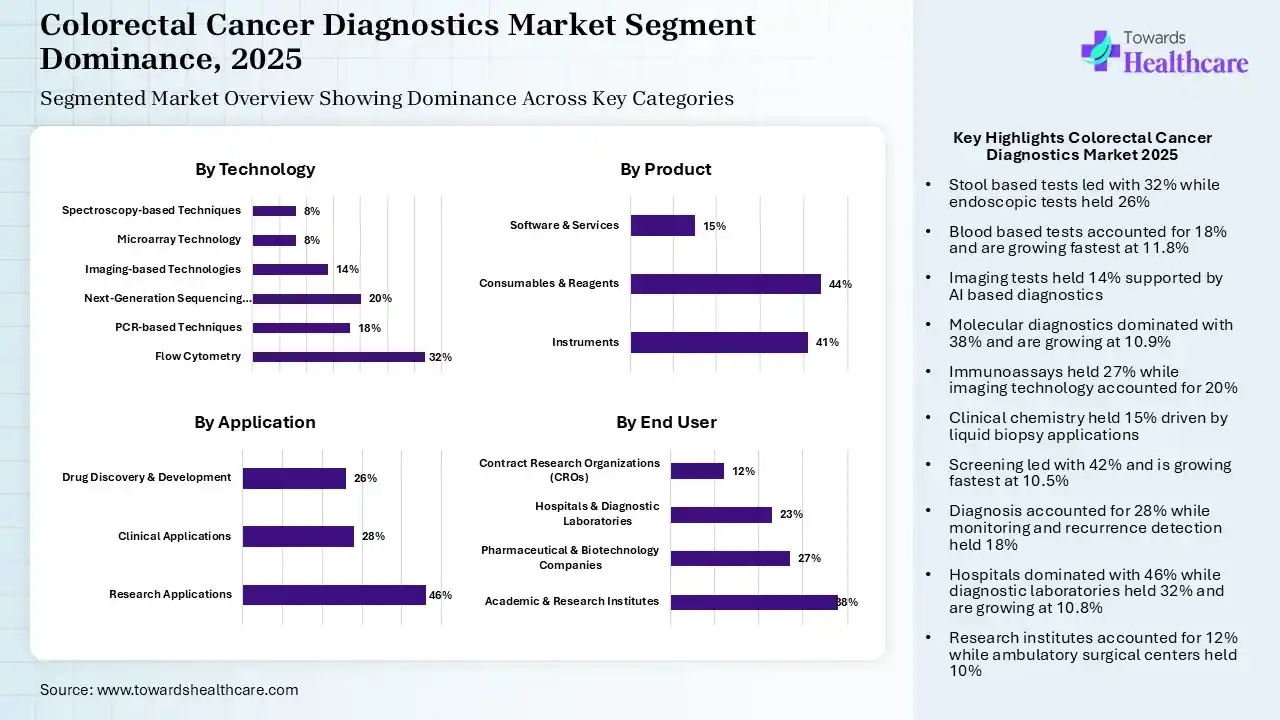

| Stool-Based Tests | 32% |

| Blood-Based Tests | 18% |

| Imaging Tests | 14% |

| Endoscopic Tests | 26% |

| Biopsy | 10% |

The Stool-Based Tests Segment Dominated the Market in 2025

The stool-based tests segment captured a major share of 32% of the colorectal cancer diagnostics market in 2025, due to the growing demand for non-invasive, home-based, & inexpensive tests to raise screening adherence, particularly among asymptomatic individuals. Along with government programs, firms are advancing next-generation multitarget stool RNA, which has approximately 94.4% sensitivity for colorectal cancer & 45.9% for advanced adenomas.

In 2025, the endoscopic tests segment held the second-largest share of 26% of the market. In the worldwide rising CRC instances, it is considered the gold standard in diagnosis, & also supports colorectal cancer (CRC) management, & facilitates both diagnosis & mitigation in one session. The latest adoption includes Confocal Laser Endomicroscopy (CLE), which offers real-time, microscopic imaging during the procedure.

However, the blood-based tests segment held 18% of the total market share and is predicted to expand rapidly at 11.8% CAGR in the coming era. Globally surging preference for minimally invasive procedures, these tests are offering more convenient, less patient anxiety & resolving hurdles. The FDA has authorized novel tests, including Shield for average-risk individuals.

The imaging tests segment accounted for a notable share of 14% of the colorectal cancer diagnostics market. These kinds of tests are improving detection accuracy & are also highly adopted in healthcare systems by combining with AI. The CT Colonography offers an alternative for incomplete colonoscopies or frail patients.

| Segment | Share 2025 (%) |

| Molecular Diagnostics | 38% |

| Immunoassays | 27% |

| Clinical Chemistry | 15% |

| Imaging Technology | 20% |

The Molecular Diagnostics Segment Led the Market in 2025

The molecular diagnostics segment dominated with a 38% share in 2025 & is estimated to expand at 10.9% CAGR. These tests are ensuring the section of precision targeted interventions for metastatic CRC. Ongoing utilization of next-generation sequencing (NGS) & molecular biomarkers encourages earlier detection, prognosis & personalised therapy. The market has executed the latest methylation markers & AI-powered analysis.

In 2025, the immunoassays segment held a 27% share of the colorectal cancer diagnostics market, due to the broader use in routine diagnostics & its affordability, with merged automation. The market is increasingly leveraging the lateral flow assays & highly sensitive enzyme immunoassays (EIA), enabling robust identification of hemoglobin or other biomarkers in stool.

The imaging technology captured a lucrative share of 20% in 2025. The progression is driven by massive investments in radiology infrastructure, accelerating screening awareness. This is further promoting the use of AI-driven imaging, which raises diagnostic capabilities.

The clinical chemistry segment held 15% share of the market, due to the advanced infrastructure, which assists in consistent application. This approach is widely implemented in liquid biopsies to detect circulating tumor DNA (ctDNA) & RNA-based biomarkers, boosting accuracy in early-stage detection.

| Segment | Share 2025 (%) |

| Screening | 42% |

| Diagnosis | 28% |

| Prognosis | 12% |

| Monitoring & Recurrence Detection | 18% |

The Screening Segment Was Dominant in the Market in 2025

In 2025, the screening segment accounted for a 42% share & is predicted to expand fastest at 10.5% CAGR in the colorectal cancer diagnostics market. Through the diverse, extensive government programs, the market is experiencing an expansion of screening, mainly for individuals aged 45 and older, led by public awareness initiatives. In these surging testing rates, blood-based & mt-sDNA tests are being employed as first-line alternatives to select patients for essential diagnostic colonoscopies.

The diagnosis segment held the second-largest share of 28% of the market, due to the substantial rise in cases of CRC, with the emergence of diagnostic tools & integrated imaging methods. Booming patient preferences for less invasive methods, with faster evolution of highly sensitive, automated molecular diagnostic kits & liquid biopsies, enable earlier & precise staging.

The monitoring & recurrence detection segment captured a 18% share of the colorectal cancer diagnostics market. A huge burden of the population needs consistent monitoring, where liquid biopsy allows real-time disease tracking. Companies are looking for non-invasive, at-home tests for surveillance instead of repeated colonoscopies.

| Segment | Share 2025 (%) |

| Hospitals | 46% |

| Diagnostic Laboratories | 32% |

| Research Institutes | 12% |

| Ambulatory Surgical Centers | 10% |

The Hospitals Segment Dominated the Market in 2025

The hospitals segment led with a 46% share of the market in 2025. To address the growing incidence of CRC, hospitals are facilitating end-to-end care, from screening to treatment, with significant approaches in the diagnostic & care ecosystem. They also execute well-trained personnel, sophisticated imaging, & gold-standard colonoscopies to find & discard precancerous polyps.

However, the diagnostic laboratories segment captured 32% share in 2025 & is estimated to expand rapidly at 10.8% CAGR. These laboratories are extensively offering precise, non-invasive, & molecular-level insights for early detection & tailored treatment. Certain key labs are conducting genetic testing on tumor tissues to foster precision therapeutic strategies.

The research institutes segment accounted for a 12% share of the colorectal cancer diagnostics market, due to escalating oncology research funding, which enhances demand. Alongside, these institutes are emphasizing biomarker discovery & alliances with biotech leaders to explore innovations.

The ambulatory surgical centers segment held a notable share of 10% in 2025. This expansion is propelled by the growing step towards outpatient procedures, with the implementation of affordable care models for appealing to patients. ASCs reduce waiting times & increases the availability of cancer screening colonoscopies.

")

In 2025, North America registered dominance with 38% share of the colorectal cancer diagnostics market. This dominance is fueled by extensive screening programs, well-established healthcare infrastructures & suitable reimbursement policies. Research activities are focusing on educating primary care providers to understand symptoms in younger patients, who are often initially misdiagnosed.

For instance,

U.S. Market Trends

Specifically, the U.S. market held a 30% share, with the promotion of research into ctDNA, DNA methylation markers, & tumor-derived exosomes in both blood & stool to determine early, pre-cancerous stages. Emerging developments cover the FDA approval of blood-based screening tests, & roll out of next-generation stool-based tests.

Canada Strengthens Innovation in Colorectal Cancer Diagnostics

Canada is witnessing significant growth in the colorectal cancer diagnostics market due to increasing colorectal cancer screening programs supporting awareness of early disease detection and strong government support for preventive healthcare. Growing adoption of technologies is improving diagnostic accuracy. Expanding investments in cancer research, advanced healthcare infrastructure, and precision oncology initiatives are further accelerating market growth.

Asia Pacific held 22% of the total market share in 2025 and is anticipated to witness rapid expansion at 11.2% CAGR in the colorectal cancer diagnostics market in the coming years. This is prominently impelled by the increasing burden of CRC incidences, particularly in China, Japan, & South Korea, along with progressing funding & government-powered, national-level screening incentives.

For instance,

China Market Trends

Whereas China is predicted to expand at 11.5% CAGR, as it has leveraged a two-step approach, i.e., initial risk assessment followed by high-precision diagnostics only for high-risk individuals. Also, China is highly deploying Computer-aided detection (CADe) & characterization (CADx) systems to raise Adenoma Detection Rates (ADR) & lower operator variability.

India Emerges as a Fast-Growing Colorectal Cancer Diagnostics Market

India is significantly growing in the colorectal cancer diagnostic burden of colorectal cancer, rising awareness of early screening, and improving access to advanced diagnostic technologies. Expansion of diagnostic laboratories, growing adoption of molecular testing and AI-assisted imaging and increasing investments in healthcare infrastructure are driving market growth. Government cancer control initiatives and rising demand for precision diagnostics are further supporting expansion.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Roche Diagnostics, Danaher (Cepheid, Beckman Coulter), Abbott, Fujifilm, Olympus | Develop molecular diagnostics, imaging systems, AI-assisted detection technologies |

| Product Manufacturers | Exact Sciences, Abbott, Roche Diagnostics, Epigenomics, Eiken Chemical | Manufacture CRC screening and diagnostic products |

| Diagnostic Service Providers | Quest Diagnostics, Labcorp, Mayo Clinic Laboratories | Offer testing services and laboratory-based CRC diagnostics |

| Platform Providers | Guardant Health, Exact Sciences, Roche Diagnostics | Provide molecular testing and liquid biopsy platforms |

| CROs & Clinical Research Organizations | IQVIA, ICON plc, Parexel | Support clinical validation and diagnostic studies |

| Software & AI Vendors | Fujifilm, Olympus, Paige AI, Ibex Medical Analytics | AI-enabled pathology and imaging solutions |

| Research Institutions | Dana-Farber Cancer Institute, MD Anderson Cancer Center, Mayo Clinic, University of Texas System | Biomarker discovery and clinical validation |

| End-User Industries | Hospitals, Cancer Centers, Diagnostic Laboratories, Academic Research Centers | Adoption and utilization of diagnostic solutions |

R&D

Regulatory Approvals

Patient Support & Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 68% | 23% | 9% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Exact Sciences | Madison, Wisconsin | USA | Global leader focused heavily on CRC screening | Cologuard, Oncodetect, molecular screening tests |

| F. Hoffmann-La Roche Ltd | Basel | Switzerland | Leading molecular diagnostics provider | PCR, NGS, companion diagnostics, pathology solutions |

| Danaher Corporation | Washington, D.C. | USA | Strong diagnostics portfolio through Cepheid and Beckman Coulter | Molecular testing, pathology diagnostics |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Guardant Health | Palo Alto, California | USA | Leader in liquid biopsy and ctDNA diagnostics | Shield, Guardant Reveal |

| Olympus Corporation | Tokyo | Japan | Global colonoscopy leader | EVIS X1 endoscopy systems |

| Fujifilm Holdings Corporation | Tokyo | Japan | Advanced endoscopic imaging provider | ELUXEO systems, AI endoscopy |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Epigenomics AG | Berlin | Germany | Pioneer in blood-based CRC diagnostics | Epigenetic blood screening assays |

| Freenome Holdings, Inc. | South San Francisco, California | USA | AI-enabled multiomics CRC detection developer | Blood-based early detection platform |

| Mainz Biomed N.V. | Berkeley Heights, New Jersey | USA | Commercial CRC screening developer | ColoAlert |

In July 2026, “The sensitivity for APL and APL with HGD for the updated SimpleScreen CRC test is a marked improvement and gets us closer to matching the performance of certain stool-based CRC screening tests, with potentially higher adherence,” says Aasma Shaukat, MD, MPH, professor of medicine at NYU Grossman School of Medicine and a co-lead principal investigator on the PREEMPT CRC study, in a release.

Strengths

Weaknesses

Opportunities

Threats

By Test Type

By Technology

By Application

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar