Drug Reference Apps Market Size, Key Players with Insights and Trends

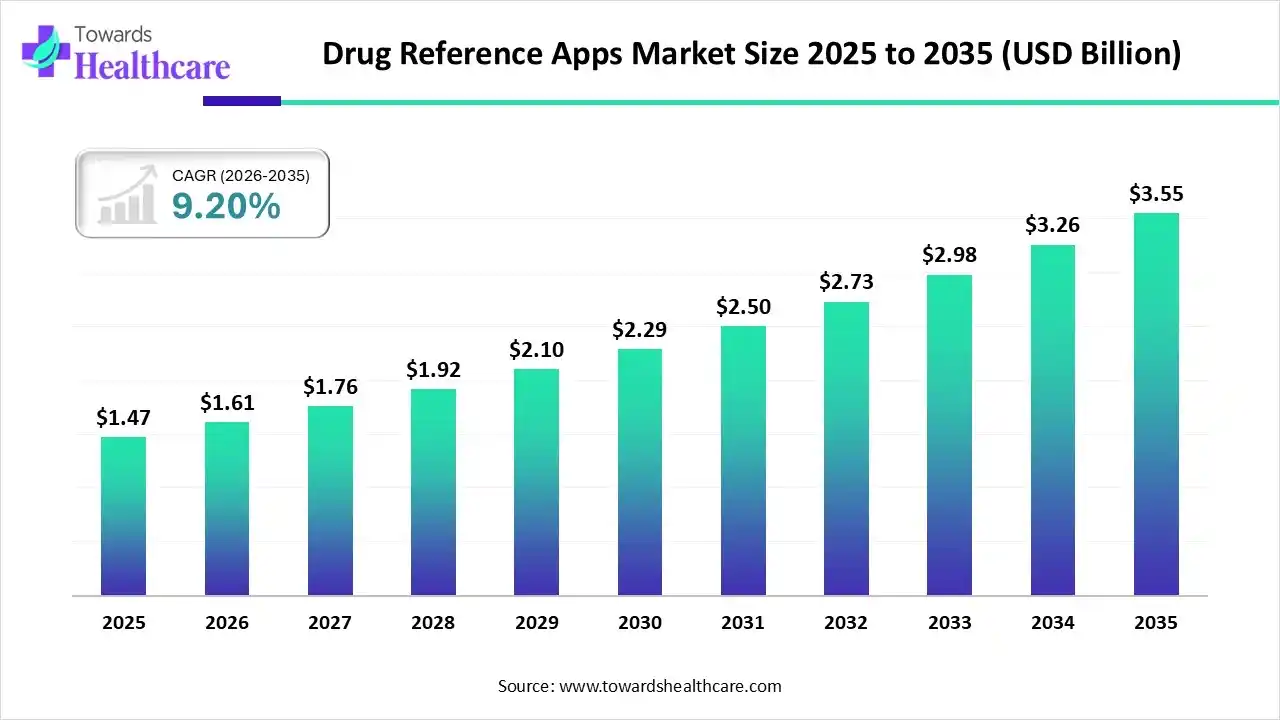

The global drug reference apps market size is calculated at US$ 1.47 billion in 2025, grew to US$ 1.61 billion in 2026, and is projected to reach around US$ 3.55 billion by 2035. The market is expanding at a CAGR of 9.20% between 2026 and 2035.

The growing emphasis on medication safety and digital integration in clinical workflows is the main factor propelling the drug reference apps market, as medical professionals depend more and more on real-time, evidence-based platforms to reduce prescription errors and enhance treatment accuracy. The need for integrated drug information systems that are accessible via mobile applications has increased due to the growing use of telemedicine and electronic health records (EHRs).

Key Takeaways

- Drug reference apps sector pushed the market to USD 1.61 billion by 2026.

- Long-term projections show USD 3.55 billion valuation by 2035.

- Growth is expected at a steady CAGR of 9.20% in between 2026 to 2035.

- North America dominated the drug reference apps market with the largest revenue in 2024.

- Asia Pacific is expected to grow at the fastest CAGR during the forecast period.

- By application, the drug information/drug database segment was dominant in the market in 2024.

- By application, the drug interactions segment is expected to witness the fastest CAGR during the forecast period.

- By pricing model, the freemium (free) segment was dominant in the drug reference apps market in 2024.

- By pricing model, the paid (subscription) segment is expected to witness the fastest CAGR during the forecast period.

- By device, the smartphones segment was dominant in the market in 2024.

- By device, the tablets segment is expected to witness the fastest CAGR during the forecast period.

- By end use, the healthcare professionals segment was dominant in the drug reference apps market in 2024.

- By end use, the patient segment is expected to register the fastest CAGR during the forecast period.

Quick Facts Table

| Key Elements |

Scope |

| Market Size in 2026 |

USD 1.61 Billion |

| Projected Market Size in 2035 |

USD 3.55 Billion |

| CAGR (2026 - 2035) |

9.20% |

| Leading Region |

North America |

| Market Segmentation |

By Application, By Pricing Model, By Device, By End Use, By Region |

| Top Key Players |

Epocrates, Medscape, UpToDate Lexidrug (formerly Lexicomp), Micromedex (Merative US L.P.), PillPack, Pill Identifier & Med Scanner, Mango Health, Drugs.com, MDCalc, Medisafe, MyTherapy |

What are Drug Reference Apps?

Both consumers and healthcare professionals can benefit greatly from drug information apps. These apps provide detailed information on drugs, including their uses, dosages, interactions, side effects, and safety measures. These apps have grown more complex due to technological advancements, offering features such as medication reminders, dosage calculators, pill identifiers, and drug interaction checkers.

Drug Reference Apps Market Outlook

- Global Expansion: Due to increased digitalization and growing healthcare needs, the market is growing quickly in all regions. North America is leading the way due to its developed infrastructure; Europe is following with strong government support and privacy regulations; Asia-Pacific is growing quickly due to growing awareness and large populations; and Latin America, the Middle East, and Africa are growing due to improved connectivity and infrastructure efforts.

- Major Investors: Major pharmaceutical companies and venture capital firms like General Atlantic, which has invested in businesses like GoodRx, are major investors in the drug reference apps market.

- Startup Ecosystem: In order to improve clinical safety and decision-making, innovators in the dynamic startup ecosystem of the drug reference apps market combine AI, real-time data, and EHR integration. Both well-established businesses and agile startups are part of this expanding market.

What is the Role of AI in the Drug Reference Apps Market?

AI healthcare software development has shifted from an optional feature to a crucial component in creating a more intelligent, effective, and accessible medical ecosystem as digital health innovations advance. Artificial intelligence is now used by drug reference apps to enhance their features. Examples include Epocrates' AI assistant for prescription decisions and other apps that offer succinct, fast responses from vast databases. These AI-powered tools make it quicker to access and process complex information by providing users, including patients and clinicians, with instant information on medication interactions, dosages, side effects, and other medical details.

Segmental Insights

Application Insights

Which Application Dominated the Market in 2024?

The drug information/drug database segment held the major revenue of the drug reference apps market in 2024. The most frequent reason for medication errors, which can result in adverse drug events that cause patients to suffer temporary or permanent harm as well as increased medical expenses, is a lack of knowledge about drugs. Numerous drug characteristics, including indications, dosage, administration, pharmaceutical compatibility, adverse reactions, interactions, and contraindications, are among the information required in an emergency department. As a result, applications that offer drug databases and information become crucial.

Drug Interactions

The drug interactions segment is estimated to be the fastest-growing segment during the forecast period.By rapidly identifying possible interactions between drugs, supplements, and even common foods, drug interaction-checking apps are designed to develop safer, more effective treatment plans. These apps offer trustworthy, understandable results to support decision-making when reviewing a new prescription, managing a complex regimen, or discussing options with a patient.

Pill/Drug Identification

The pill/drug identification segment is growing significantly in the market during the forecast period. The ability to swiftly and precisely identify medications is essential in today's world to guarantee safety and appropriate use. A useful tool that helps people identify pills by their imprint, color, and shape is a pill identifier.

Pricing Model Insights

How did the Freemium (Free) Segment Dominate the Market in 2024?

Freemium (Free)

The freemium (free) segment held the major revenue of the drug reference apps market in 2024. Freemium business models are well-liked because they make it simple to test out new services or apps by offering free trials to a large number of users. The majority of people are open to trying out new apps or services, which makes it simple for businesses to find new customers and track their usage patterns. Free users help businesses by gathering information, displaying advertisements, and increasing revenue to enhance the app.

Paid (Subscription)

The paid (subscription) segment is estimated to be the fastest-growing segment during the forecast period. Online retailers and service providers use subscription models with carefully chosen goods and services to create a consistent flow of income while providing customers with convenience and additional value. Companies that sell goods that need to be restocked can make it simple for customers to place new orders by offering subscriptions.

Device Insights

What Made Smartphones Dominant in the Market in 2024?

The smartphones segment accounted for the majority of the drug reference apps market revenue in 2024, driven by the rising use of mobile phones for all services, including healthcare. Early in 2023, there were 5.44 billion mobile phone users worldwide, accounting for 68% of the world's population. Over the past 12 months, the number of mobile phone users has increased by slightly more than 3 percent, adding 168 million users. By 2026, the number is predicted to surpass 7.5 billion.

Tablets

The tablets segment is estimated to be the fastest-growing segment during the forecast period. The tablet is one significant gadget that has developed in today's society, which is characterized as a learning society that integrates media and technology into healthcare. By utilizing mobile apps to enhance productivity, communication, and patient care quality, tablet computers have many benefits for the healthcare industry. Professionals' workflows are streamlined by their portability and specialized applications, which also enable patients to take charge of their own health.

End-Use Insights

Which End-Use Segment Dominated the Market in 2024?

The healthcare professionals segment held the major revenue of the drug reference apps market in 2024. Healthcare apps are now more popular than other information sources and have helped medical professionals by giving them faster access to information. Drug interaction detection is one of the most beneficial scenarios for healthcare apps. A greater number of clinically significant drug interactions may eventually be avoided or reduced by using this type of app, which enables medical professionals to review a patient's complete medication list for potentially dangerous interactions and view severity ratings ranging from minor to major.

Patient

The patient segment is estimated to be the fastest-growing segment during the forecast period. Mobility, hearing, and vision, communication, independent living, and computer use are just a few of the many areas where technology is increasingly being used to foster independence. During the transition to young adulthood, people with chronic conditions can be empowered to manage their own health issues by using both new and existing technology.

Pharmacist

The pharmacist segment is growing significantly in the drug reference apps market during the forecast period. Drug reference apps help pharmacists stay up to date on disease management guidelines, maintain sufficient pharmacy supplies, access drug information systems and patient health information, and use tools to accurately convert between units of measurement and calculate drug doses.

Regional Insights

What made North America Dominant in the Market in 2024?

North America dominated the drug reference apps market in 2024, due to the growing demand in the area for prompt, trustworthy, and readily available medical information. App usage is fueled by the growing use of smartphones among medical professionals as well as the need for precise drug interaction information and dosage recommendations. Adoption is further boosted by the region's robust digital healthcare infrastructure, encouraging laws, and focus on lowering prescription errors.

Why the U.S. Drug Reference App Market is Exploding Right Now?

The drug reference apps market is growing rapidly in the U.S. for several reasons. The U.S. healthcare industry is highly advanced, and healthcare professionals are continuously encouraged to adopt healthcare apps to improve service quality. Apart from this, U.S. citizens are well aware of various healthcare apps used frequently for medication adherence, drug identification, and other services.

Fast Adoption of Smartphones is Driving the Asia Pacific

Asia Pacific is estimated to be the fastest-growing market for drug reference apps during the forecast period. Due to the quick uptake of smartphones, increased internet access made possible by cutting-edge technologies, and an increase in the number of tech-savvy medical professionals. Government initiatives to promote telemedicine, geotagging, and mobile health, which are expanding at double-digit rates, are driving the emergence of digital health programs across many countries, including China, India, and Southeast Asia.

Digital Healthcare Boom: China's Next Frontier

China has made significant progress in this area in recent years. More than 25.9 million people have benefited from telemedicine services at the city and county levels, and more than 3,000 internet hospitals have been established. Opportunities frequently arise from challenges, and China has been implementing the "Healthy China 2030" plan for more than five years.

Rise in Digital Health is Driving Europe

Europe is expected to grow at a significant CAGR in the drug reference apps market during the forecast period, where drug reference apps are most widely used in countries such as France, Germany, and the United Kingdom. The market is growing due to the region's robust healthcare systems, widespread adoption of digital health technologies, and emphasis on patient safety.

NHS Data Drives Digital Health Revolution

The National Health Service (NHS) in the United Kingdom is a global leader in digital health and care, offering substantial opportunities for innovation through extensive data management. The 2019 NHS Long Term Plan, which sets goals and priorities for the next ten years, includes digital innovation as a major component.

South America is expected to grow significantly in the drug reference apps market during the forecast period. South American clinicians increasingly adopt drug reference apps driven by rising smartphone penetration and the need for localized Spanish and Portuguese content. Fragmented healthcare systems push pharmacists to use offline databases integrated with telemedicine, while local regulations like Anvisa shape deployment.

Brazilian Doctors Demand Localized Drug Data

Brazilian clinicians favor drug reference apps offering Portuguese content and national formulary alignment tailored to SUS. Apps integrating local drug utilization research and timely regulatory updates address unequal access, rural connectivity challenges, and support growing telehealth adoption across the country.

Emerging MEA Markets Embrace Clinical Apps

The Middle East and Africa are expected to grow at a lucrative CAGR in the drug reference apps market during the forecast period. MEA clinicians increasingly use drug reference apps offering Arabic and English interfaces, offline access, and hospital integration. Regulatory fragmentation across countries requires local compliance, while partnerships with regional health systems and pharmacists expand usage in urban centers and remote communities.

GCC Healthcare Accelerates App Adoption Rapidly

GCC health systems prioritize certified drug reference apps within national eHealth strategies and government digitization programs. High smartphone adoption and strong health tech investment encourage integration with electronic records. Official endorsements and bilingual support accelerate clinician and pharmacist trust rapidly.

Company Landscape

Epocrates (Part of athenahealth)

Company Overview:

- Epocrates is a premier provider of mobile drug and medical information, functioning as a point-of-care clinical decision support (CDS) tool for healthcare professionals.

- The application focuses on providing quick, reliable answers for safe prescribing and clinical efficiency.

Corporate Information:

- Headquarters: Watertown, Massachusetts, US (Parent company: athenahealth)

- Year Founded: 1998

- Ownership Type: Private (Subsidiary of athenahealth, which is owned by Hellman & Friedman and Bain Capital)

History and Background:

- Founded by three Stanford Business School students, Epocrates pioneered the concept of mobile drug reference, starting on the Palm Pilot and becoming one of the first critical medical apps on the iPhone.

- Acquired by athenahealth for approximately $293 million in 2013, integrating it into a larger ecosystem of clinical and financial management solutions.

Key Milestones/Timeline:

- 1998: Founded, launched the first mobile drug reference.

- 2013: Acquired by athenahealth.

- 2024 (Feb): David Minkin appointed President and General Manager of Epocrates.

- 2024 (Year): Top-viewed articles included GLP-1 agonists (Ozempic, Mounjaro) and ADA warnings on compounded GLP-1s.

- 2025 (Sept): Expected launch of new clinical engagement standards and conversational AI assistant features.

Business Overview:

- Revenue is generated through subscriptions for premium features (epocrates+) and, most significantly, through digital pharmaceutical marketing and advertising services targeted at HCPs via the app.

- The core business is delivering trusted, timely clinical content and acting as a conduit for targeted engagement from the life sciences industry.

Business Segments/Divisions:

- Clinical Reference Tools (Free and Subscription-based content).

- Digital Engagement and Advertising Solutions (Pharma/Life Sciences Marketing).

Geographic Presence:

- Strongest presence in the United States, with high penetration among U.S. physicians (estimated at 40%+ market share for the mobile reference segment).

- Serves a global user base, though the US remains the primary market focus.

Key Offerings:

- Epocrates (Free): Drug Reference (dosing, safety, interactions), Pill Identifier, Drug Interaction Checker, and Medical Calculators.

- epocrates+ (Subscription): Disease content, alternative medicine, lab tests, and infectious disease treatment monographs.

End-Use Industries Served:

- Healthcare Providers (Physicians, NPs, PAs, Pharmacists) for point-of-care decision support.

- Pharmaceutical and Biotech Companies for targeted digital marketing and education.

Key Developments and Strategic Initiatives:

- Mergers & Acquisitions: None recently outside of the parent company's activities.

- Partnerships & Collaborations: Ongoing collaborations with companies for delivering content, such as video messaging to HCPs.

- Product Launches/Innovations: Investing in an AI assistant for prescription queries and new engagement standards (RhythmIQ) planned for 2025.

- Capacity Expansions/Investments: Continued investment in the mobile platform's content and user experience; key leadership appointments in 2024 to drive growth.

- Distribution channel strategy: Primarily through Mobile App Stores (iOS/Android) for end-users and Direct B2B Sales to pharmaceutical clients.

Technological Capabilities/R&D Focus:

- Core Technologies/Patents: Proprietary, continually updated clinical databases and a highly optimized mobile user interface for rapid point-of-care access.

- Innovation Focus Areas: Integrating Conversational AI for quick Q&A; enhancing data-driven personalization of clinical and sponsored content.

Competitive Positioning:

- Strengths & Differentiators: High brand recognition, deeply embedded in U.S. clinical workflow, excellent mobile user experience, and a stable advertising revenue model.

- Market presence & ecosystem role: A fundamental utility app for U.S. clinicians; key platform for pharma digital engagement.

SWOT Analysis:

- S (Strengths): High physician market penetration, strong mobile performance, large clinical database.

- W (Weaknesses): Dependence on pharma ad revenue, core subscription faces competition from more comprehensive CDS tools.

- O (Opportunities): AI integration for advanced decision support, leveraging athenahealth's EHR ecosystem.

- T (Threats): Competition from Medscape and integrated EHR/CDS tools (e.g., UpToDate Lexidrug).

Recent News and Updates:

- Press Releases: Anticipated launch of new clinical engagement features and an AI assistant in September 2025.

- Industry Recognitions/Awards: N/A for 2024/2025; consistently ranked highly as a top medical reference app.

Medscape (Part of WebMD LLC)

Company Overview:

Medscape is a leading global resource for physicians and healthcare professionals, providing a vast library of medical news, expert commentary, drug and disease reference information, and continuing medical education (CME).

Corporate Information:

- Headquarters: Newark, New Jersey, US (Parent company: WebMD LLC, owned by Internet Brands)

- Year Founded: 1995

- Ownership Type: Private (Subsidiary of WebMD LLC)

History and Background:

- Launched as one of the first major medical content websites on the internet.

- Acquired by WebMD in 2001, allowing it to integrate its drug reference and news into a wider physician network.

- Has evolved from a website to a dominant multimedia platform, including a highly utilized mobile drug reference application.

Key Milestones/Timeline:

- 1995: Medscape website launched.

- 2001: Acquired by WebMD.

- 2008: Launched the Medscape mobile app.

- 2024 (Aug): Launched Affinity™ Platform for global HCP behavioral insights.

- 2025 (June): Established a dedicated presence in Australia to deepen local partnerships.

- 2025 (November): Continued coverage of major medical conferences (e.g., AHA, ASTRO, IACFS/ME) and publishing of key physician reports (e.g., Compensation, APRN Job Market).

Business Overview:

- The business model is built on providing free, registration-based access to a comprehensive content ecosystem, primarily monetized through pharmaceutical advertising, market research, and sponsored CME/CE offerings.

- The drug reference tool (Medscape Drug Reference) is a core user acquisition and engagement driver for the larger content platform.

Business Segments/Divisions:

- Medical News and Perspectives (Editorial Content).

- Drug and Disease Reference (Medscape Drug Reference/CME).

- Global Medical Affairs and Advertising (Pharmaceutical Marketing/Insights).

Geographic Presence:

- Global scale, with a strong presence in North America, Europe, Asia Pacific, and a recent expansion in Australia (June 2025).

- Reports over 13 million registered HCPs globally, demonstrating vast international reach.

Key Offerings:

- Medscape Drug Reference (MDR): Drug lookup, dosing, interactions, and a pill identifier.

- Clinical News, Conference Coverage, and Expert Commentaries.

- Continuing Medical Education (CME/CE) courses (thousands available).

End-Use Industries Served:

- Healthcare Professionals (across nearly all specialties).

- Pharmaceutical and Medical Device Companies (for advertising, education, and market research).

Key Developments and Strategic Initiatives:

- Product Launches/Innovations: Launch of the Affinity™ Platform in 2024, a proprietary tool that leverages behavioral data from its global HCP network for improved targeting and strategy for life sciences clients.

- Capacity Expansions/Investments: Continued investment in expanding its global editorial staff and its medical affairs/marketing services footprint, including the 2025 Australia expansion.

- Regulatory Approvals: N/A.

Distribution channel strategy:

- Primary distribution via its massive Web Portal and dedicated Mobile Applications (iOS/Android).

- Utilizes email newsletters and targeted digital outreach for content delivery.

Technological Capabilities/R&D Focus:

- Core Technologies/Patents: Robust content management system for complex clinical data; advanced digital advertising delivery; proprietary behavioral analytics (Affinity™ Platform).

- Innovation Focus Areas: Leveraging data science to understand global HCP behavior (Affinity™); enhancing content personalization; expanding multimedia and video content formats for CME/CE.

Competitive Positioning:

- Strengths & Differentiators: Largest global network of registered HCPs; unparalleled volume of up-to-the-minute medical news and conference coverage; strong authority in the CME/CE market.

- Market presence & ecosystem role: The go-to source for medical news and education; the drug reference tool provides essential clinical utility and acts as a funnel for the entire ecosystem.

SWOT Analysis:

- S (Strengths): Vast global scale (13M+ HCPs), comprehensive content (News, Reference, CME), robust behavioral data platform (Affinity™).

- W (Weaknesses): Dependence on pharmaceutical advertising revenue, size/breadth can sometimes make the app feel less focused than Epocrates.

- O (Opportunities): Monetizing global HCP insights via Affinity™, continued expansion in high-growth international markets.

- T (Threats): Competition from dedicated clinical decision support systems and other global medical news providers.

Recent News and Updates:

- Press Releases: June 2025 announcement of a dedicated presence in Australia.

- Industry Recognitions/Awards: Continuous accreditation and recognition for its extensive CME/CE programs. Numerous 2025 reports have been published covering physician compensation, job markets, and international clinical updates.

Top Vendors in the Drug Reference Apps Market & Their Offerings

- UpToDate Lexidrug strengthens the market by delivering continuously updated drug databases, interaction checkers, and clinical decision support trusted by healthcare providers.

- Micromedex enhances growth through evidence-based monographs, dosing tools, and mobile accessibility, enabling faster medication decisions and improving safety across clinical environments.

- PillPack contributes by integrating pharmacy services with a medication-management app, supporting adherence, simplifying schedules, and expanding consumer engagement within digital drug reference ecosystems.

- Pill Identifier & Med Scanner supports market expansion by enabling accurate pill recognition, reducing errors, empowering patients, and strengthening trust in mobile drug-information solutions.

- Mango Health drives adoption through reminders, adherence tracking, and drug guidance.

Top Companies in the Drug Reference Apps Market

- Epocrates

- Medscape

- UpToDate Lexidrug (formerly Lexicomp)

- Micromedex (Merative US L.P.)

- PillPack

- Pill Identifier & Med Scanner

- Mango Health

- Drugs.com

- MDCalc

- Medisafe

- MyTherapy

Recent Developments in the Drug Reference Apps Market

- In November 2025, UpToDate® Expert AI, Wolters Kluwer Health's GenAI clinical decision support solution, saw its first of several planned expansions. The AI resource will now incorporate comprehensive drug information from UpToDate Lexidrug, the drug reference tool that thousands of clinicians, pharmacists, and hospital pharmacies rely on for improved medication and therapeutic decision support.

- In May 2025, Pathway announced that its AI-powered medical knowledge platform now includes a fully integrated drug reference and drug-drug interaction checker. In the same interface that they currently use for clinical guidance, clinicians can now obtain thorough medication information for more than 2,000 medications and check for interactions.

Segments Covered in the Report

By Application

- Drug Information/Drug Data Base

- Drug Interactions

- Dosage Calculators

- Pill/Drug Identification

- Others

By Pricing Model

- Freemium (Free)

- Paid (Subscription)

By Device

By End Use

- Healthcare Professionals

- Patients

- Pharmacists

- Researchers and Educators

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

- Asia Pacific

- China

- Taiwan

- India

- Japan

- Australia and New Zealand

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

- MEA

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA