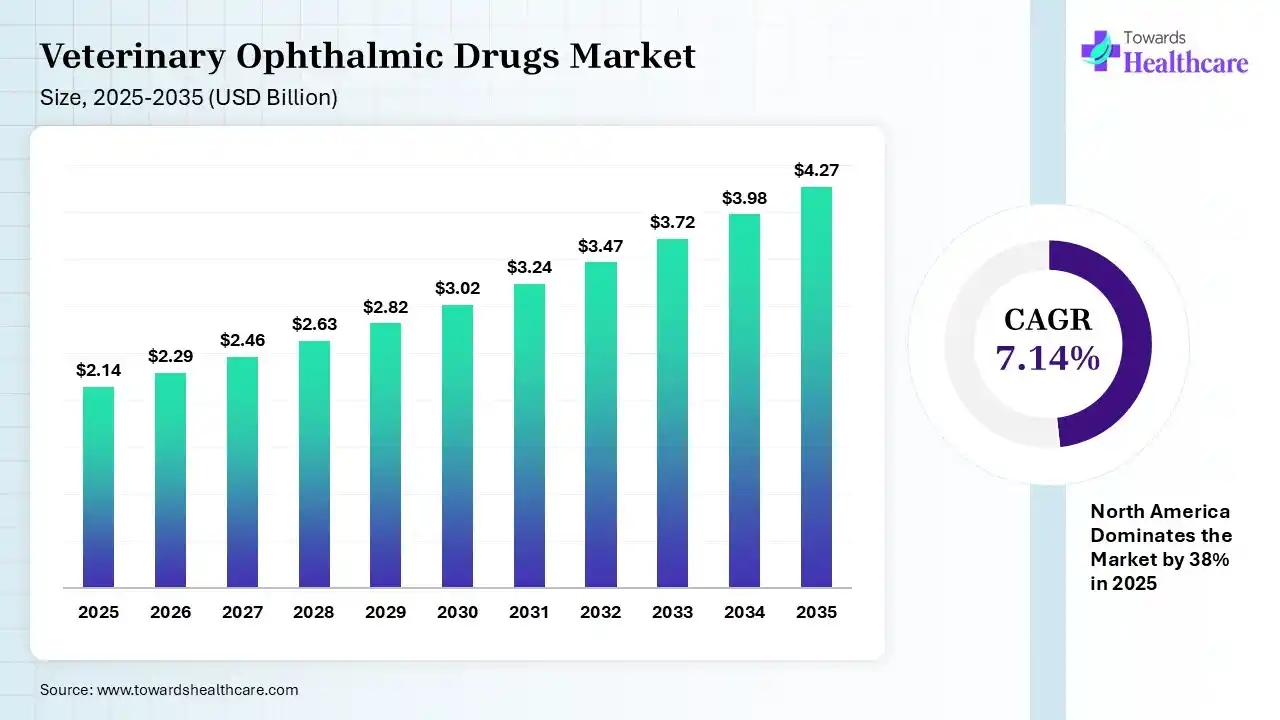

The global veterinary ophthalmic drugs market size was estimated at USD 2.14 billion in 2025 and is predicted to increase from USD 2.29 billion in 2026 to approximately USD 4.27 billion by 2035, expanding at a CAGR of 7.14% from 2026 to 2035. The market is growing consistently, supported by increased awareness of animal eye health, higher pet care expenditure, and rising adoption of specialized treatment products.

")

")

Veterinary ophthalmic drugs are pharmaceutical products specifically developed to manage, prevent, and treat eye diseases, infections, inflammation, and vision-related conditions in animals, including companion and farm animals. The veterinary ophthalmic drugs market is expanding due to the rising incidence of eye disorders such as infections, glaucoma, and dry eye in companion and livestock animals. Increasing pet ownership, higher spending on animal healthcare, and growing awareness about timely advancements in veterinary pharmaceuticals and improved access to specialized veterinary services are accelerating market growth worldwide.

Artificial intelligence can significantly influence the market by improving early diagnosis of eye disorders through image-based screening and predictive analytics. AI-powered tools help veterinarians detect conditions such as glaucoma, cataracts, and retinal issues more accurately, enabling timely treatment and better drug selection. It can also support drug discovery, personalized treatment planning, and monitoring of disease progression, thereby enhancing overall market growth.

| Table | Scope |

| Market Size in 2026 | USD 2.29 Billion |

| Projected Market Size in 2035 | USD 4.27 Billion |

| CAGR (2026 - 2035) | 7.14% |

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Class, By Animal Type, By Indication, By Dosage Forms, By Distribution Channel, By End User, By Region |

| Top Key Players | Merck & Co., Inc., Zoetis, Dechra Pharmaceuticals, Virbac, Ceva Santé Animale, Elanco, Bausch & Lomb |

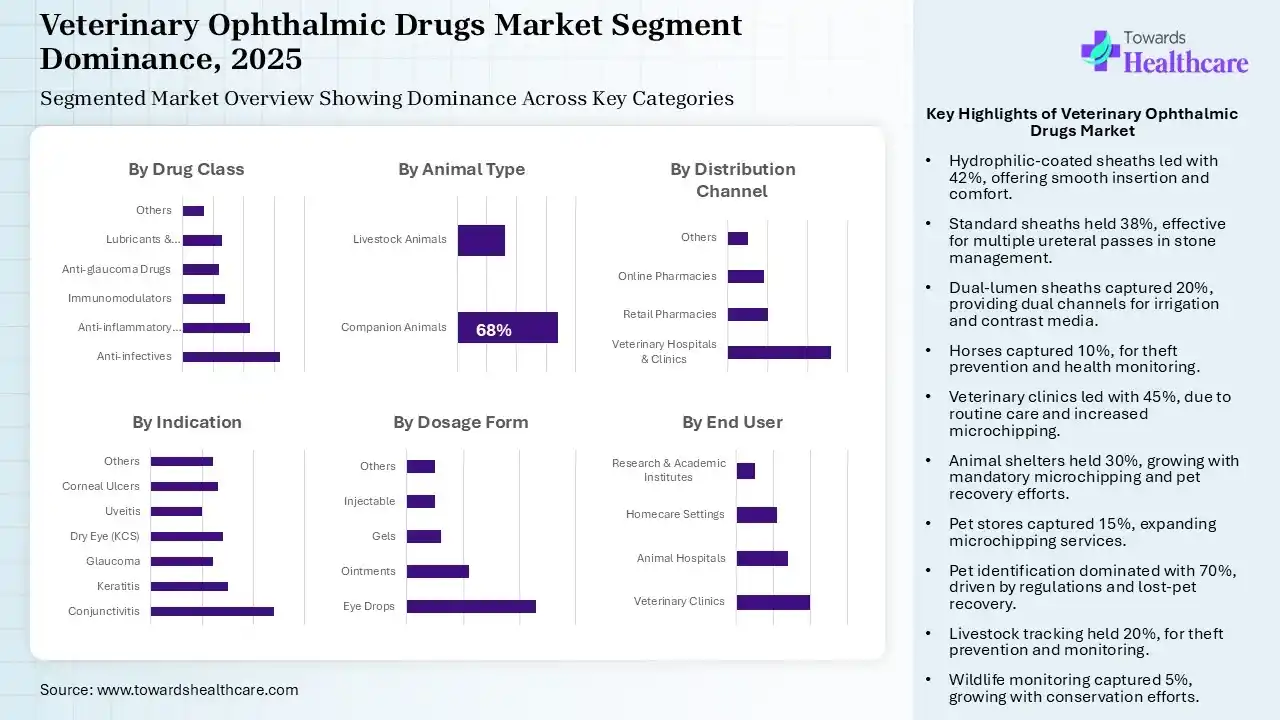

The Anti-infectives Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Anti-infectives | 32% |

| Anti-inflammatory Drugs | 22% |

| Immunomodulators | 14% |

| Anti-glaucoma Drugs | 12% |

| Lubricants & Artificial Tears | 13% |

| Others | 7% |

The anti-infectives segment dominated the veterinary ophthalmic drugs market with shares of 32% in 2025, owing to the frequent occurrence of eye infections in companion and farm animals. Conditions such as bacterial conjunctivitis and corneal infections require prompt medication, making these drugs highly utilized in veterinary practices. Growing awareness of animal eye health, increased pet adoption, and regular veterinary consultations further supported the segment’s strong market position.

The anti-inflammatory drugs segment held the second largest market share of 22% in 2025 due to the high incidence of ocular inflammation caused by allergies, infections, trauma, and post-surgical conditions in animals. These medications are widely used to reduce swelling, pain, and redness, improving recovery outcomes. Increased veterinary ophthalmic procedures and rising awareness of timely eye care among pet owners further contributed to the market presence.

The immunomodulators segment held 14% of the veterinary ophthalmic drugs market share in 2025 and is expected to grow at the fastest CAGR of 8.9% during the forecast period due to the rising prevalence of chronic and immune-mediated eye disorders in animals, such as dry eye and allergic inflammation. These drugs help regulate immune response and provide long-term disease management.

The lubricant & artificial tears segment held 13% of the market share in 2025 due to the increasing incidence of dry eye syndrome, corneal irritation, and tear film disorders in animals, particularly companion pets. These products are widely used to provide moisture, reduce discomfort, and support long-term eye health. Rising pet ownership, greater awareness of preventive ocular care, and increasing veterinary recommendations for routine eye management are further driving segment growth.

The anti-glaucoma drugs segment held 12% of the market share in 2025 due to increasing glaucoma diagnoses in aging pets. Growing awareness of advanced veterinary management. Growing awareness of advanced veterinary treatment, increasing pet healthcare spending, and continuous innovation in targeted therapies are further supporting segment growth.

The Companion Animals Segment Led the Market in 2025 with the Largest Share

| Segment | Share 2025 (%) |

| Companion Animals | 68% |

| Livestock Animals | 32% |

The companion animals segment dominated the veterinary ophthalmic drugs market with 68% market share in 2025, and is expected to grow at the fastest CAGR of 8.2% during the forecast period. Due to increasing pet ownership and a stronger emotional attachment between owners and pets. Higher spending on advanced veterinary care, including eye health, and rising awareness of early diagnosis and treatment are key factors. Additionally, frequent veterinary visits and demand for specialized ophthalmic therapies continue to accelerate segment growth.

The livestock animals segment held the second largest market share of 32% in 2025 due to the growing need to maintain the health and productivity of farm animals such as cattle, sheep, and horses. Eye infections and inflammatory conditions can directly affect animal performance and economic output. Increasing focus on disease prevention, regular veterinary care, and rising investments in livestock health management are key factors supporting the market position.

The Conjunctivitis Segment held a dominant position in the Market in 2025

| Segment | Share 2025 (%) |

| Conjunctivitis | 24% |

| Keratitis | 15% |

| Glaucoma | 12% |

| Dry Eye (KCS) | 14% |

| Uveitis | 10% |

| Corneal Ulcers | 13% |

| Others | 12% |

The conjunctivitis segment dominated the veterinary ophthalmic drugs market with shares of 24% in 2025 due to high prevalence among both companies and livestock animals. Factors such as bacterial infections, allergies, dust exposure, and environmental irritants frequently contribute to these conditions. As it requires prompt treatment to prevent discomfort and complications, the demand for effective ophthalmic drugs remains high, supporting the segment’s leading market share.

The keratitis segment held the second largest market share of 15% in 2025 due to the increasing occurrence of corneal inflammation and infections in animals. This condition is commonly caused by trauma, bacterial or viral infections, and dry eye disorders, requiring timely medical interventions. The growing focus on preventive vision health in pets and livestock, along with increased veterinary consultation, has contributed to the market presence.

The dry eye (KCS) segment held 14% of the veterinary ophthalmic drugs market share in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period due to the rising diagnosis of chronic tear deficiency and immune-related eye disorders in companion animals, especially dogs. Increasing awareness among pet owners, growing demand for long-term treatment solutions, and wider use of lubricants, immunomodulators, and supportive therapies are driving rapid segment expansion.

The glaucoma segment held 12% of the market share in 2025 due to the increasing prevalence of age-related and breed-specific eye disorders in companion animals, particularly dogs and cats. Early diagnosis and timely treatment are essential to prevent irreversible vision loss, driving demand for specialized ophthalmic drugs. Rising pet healthcare expenditure, improved veterinary diagnostic capability, and growing awareness of chronic eye disease management are further supporting the steady growth.

The Eye Drop Segment held the Largest Market Share in 2025

| Segment | Share 2025 (%) |

| Eye Drops | 46% |

| Ointments | 22% |

| Gels | 12% |

| Injectable | 10% |

| Others | 10% |

The eye drop segment held the largest veterinary ophthalmic drugs market share of 46% in 2025 due to its ease of administration, fast therapeutic action, and wide use in treating infections, inflammation, dry eye, and glaucoma in animals. Veterinarians and pet owners prefer this dosage form because it allows direct drug delivery to the affected area. Its convenience, cost-effectiveness, and availability across multiple drug classes further strengthened market dominance.

The ointment segment held the second largest market share of 22% in 2025 due to its longer contract time with the eye surface, which enhances drug absorption and prolongs therapeutic effects. It is widely used for infections, inflammation, and corneal conditions requiring sustained treatment. Veterinarians often prefer ointments for overnight use and chronic conditions, as they reduce dosing frequency and improve treatment effectiveness, supporting strong market demand.

The gels segment held 12% of the veterinary ophthalmic drugs market share in 2025 and is expected to grow at the fastest CAGR of 8.1% during the forecast period due to its superior ocular retention and prolonged drug release compared with conventional eye drops. These formulations improve moisture retention and reduce dosing frequency, making them highly suitable for chronic conditions such as dry eye and glaucoma. Increasing preference for advanced, long-acting therapies is further accelerating segment growth.

The injectable segment held 10% of the market share in 2025 due to the rising use of targeted and long-acting treatments for severe ocular infections, inflammation, and post-surgical care in animals. These formulations ensure rapid therapeutic action and accurate dosing, particularly in critical cases where topical treatments may be insufficient. Increasing veterinary ophthalmic procedures and growing demand for effective advanced therapies are further supporting the segment’s growth.

The Veterinary Hospitals & Clinics Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Veterinary Hospitals & Clinics | 52% |

| Retail Pharmacies | 20% |

| Online Pharmacies | 18% |

| Others | 10% |

The veterinary hospitals & clinics segment dominated the veterinary ophthalmic drugs market with a share of 52% in 2025 due to the high volume of animal eye disease diagnoses and treatments performed in professional care settings. Pet owners largely rely on veterinarians for accurate diagnosis, prescription-based ophthalmic drugs, and follow-up care. The availability of specialized expertise, advanced diagnostic equipment, and immediate treatment options further strengthened the segment’s leading market share.

The retail pharmacies segment accounted for the second largest market share of 20% in 2025 due to easy accessibility and convenience for pet owners purchasing prescribed and over-the-counter ophthalmic medications. These outlets offer a wide range of eye drops, ointments, and lubricants for routine animal eye care. Increasing pet healthcare awareness, repeat purchases for chronic conditions, and widespread pharmacy networks have further supported segment growth.

The online pharmacies segment held 18% of the veterinary ophthalmic drugs market share in 2025 and is expected to grow at the fastest CAGR of 8.6% during the forecast period due to increasing digital adoption and the convenience of home delivery for pet medications. Pet owners increasingly prefer online platforms for easy product comparison, repeat orders, and wider product availability. Rising internet penetration, growing e-commerce trust, and demand for hassle-free access to veterinary ophthalmic drugs are key growth drivers.

The Veterinary Clinics Segment Dominated the Market in 2025

| Segment | Share 2025 (%) |

| Veterinary Clinics | 40% |

| Animal Hospitals | 28% |

| Homecare Settings | 22% |

| Research & Academic Institutes | 10% |

The veterinary clinics segment led the veterinary ophthalmic drugs market with a share of 40% in 2025 due to the high number of routine consultations, eye examinations, and follow-up treatments performed in these settings. Most pet owners prefer clinics for early diagnosis, prescription-based ophthalmic drugs, and specialized veterinary guidance. The availability of trained professionals, advanced diagnostic support, and personalized treatment plans has significantly strengthened the segment’s dominant position in the market.

The animal hospitals segment held the second-largest market share of 28% in 2025 due to its strong role in handling complex and severe ocular conditions that require advanced treatment and surgical care. These facilities are equipped with specialized diagnostic tools and expert veterinary ophthalmologists, making them essential for critical cases. Rising admissions for emergency eye conditions and post-operative care continue to support segment growth.

The homecare settings segment held 22% of the veterinary ophthalmic drugs market share in 2025 and is expected to grow at the fastest CAGR of 8.6% during the forecast period due to increasing preference for at-home pet treatment and long-term management of chronic eye conditions. Pet owners are increasingly administering eye drops, gels, and lubricants at home for convenience and cost efficiency. Rising awareness, easy product availability, and the growth of online veterinary consultations are further accelerating segment expansion.

The research & academic institutes segment held 10% of the market share in 2025 due to the growing focus on veterinary ophthalmic drug development, clinical studies, and disease-specific research in animal eye health. These institutes play a key role in innovation, testing new formulations, and advancing treatment approaches for ocular disorders. Increasing research funding, collaboration with pharmaceutical companies, and rising academic interest in veterinary medicine are further supporting segment growth.

")

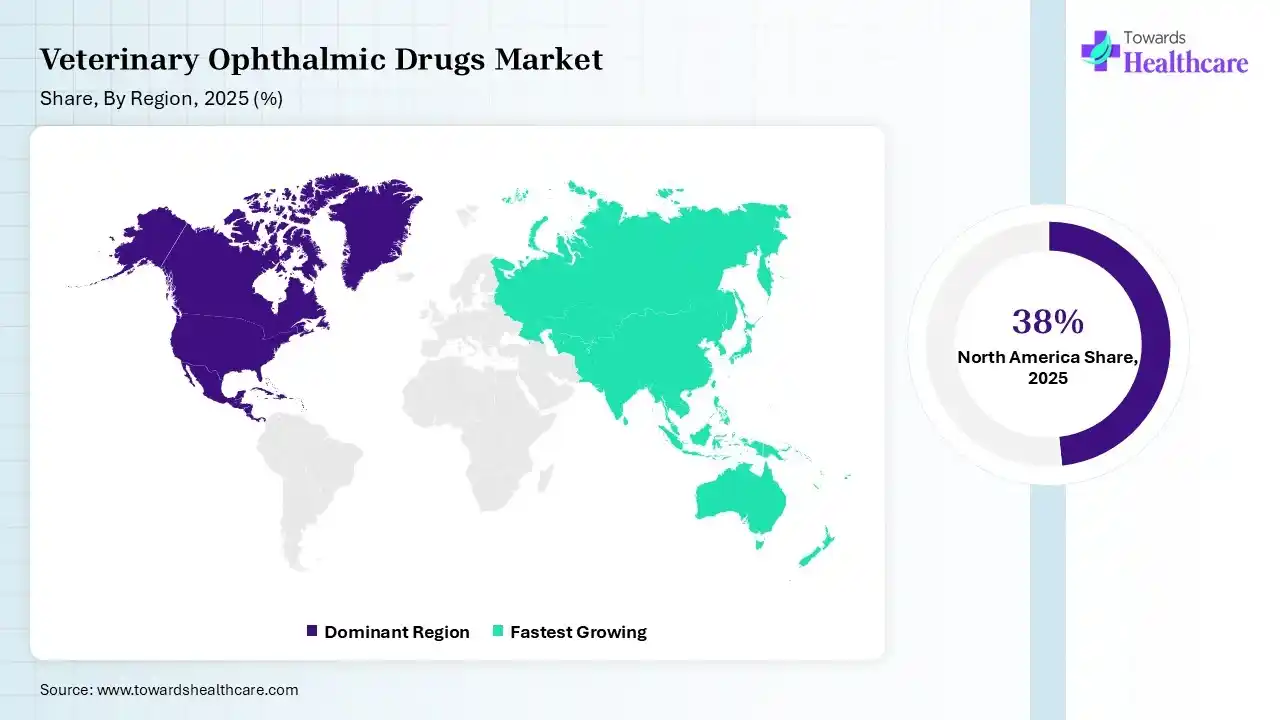

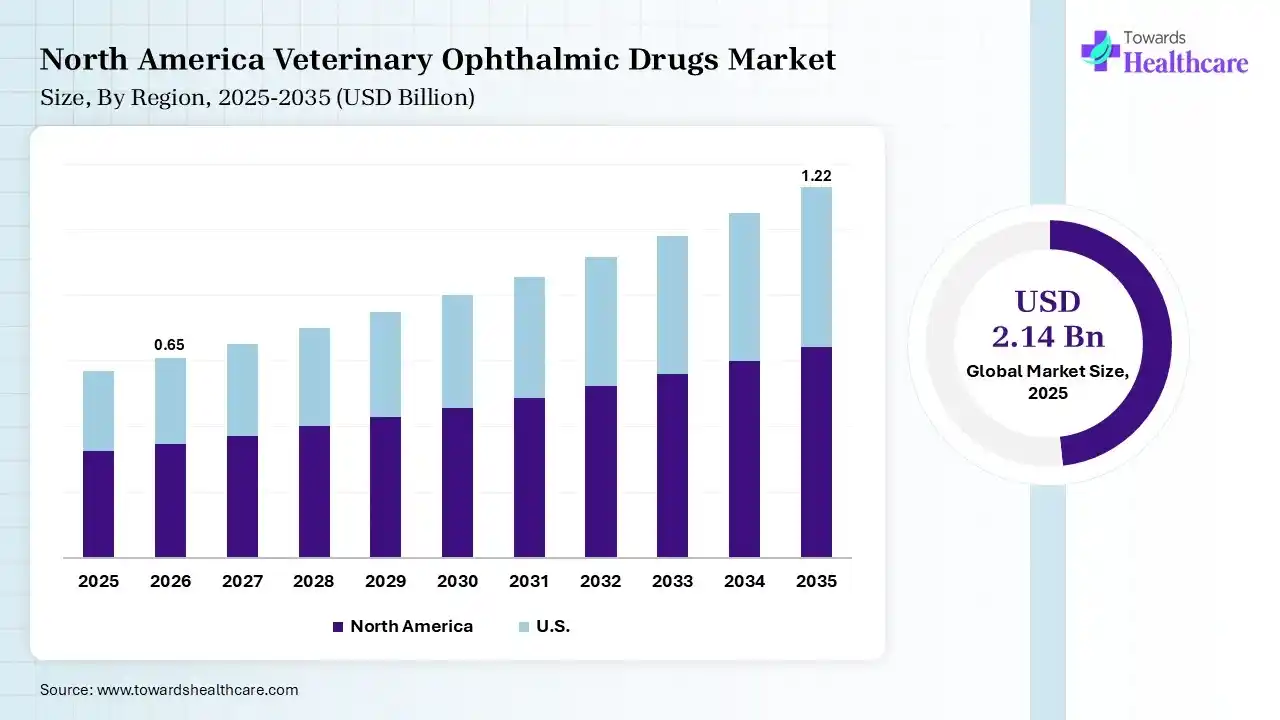

North America held the leading position in the global veterinary ophthalmic drugs market with 38% market share in 2025, owing to the large companion animal population, well-established veterinary care facilities, and strong focus on animal eye health. Greater expenditure on pet treatment, easy access to advanced ophthalmic therapies, and the presence of major animal healthcare players have further supported regional dominance. In addition, the growing use of pet insurance and early disease detection continues to reinforce market growth.

U.S. Market Trends

The U.S. holds a leading position in the veterinary ophthalmic drugs market due to the strong presence of companion animals and significant spending on pet wellness. The country benefits from advanced veterinary clinics, early detection of eye-related conditions, and quick adoption of specialized treatment options. Continuous innovation by major animal healthcare companies and growing awareness of preventive eye care further support its market leadership.

Asia-Pacific held 22% of the market share in 2025 and is expected to grow at the fastest CAGR of 9.3% in the veterinary ophthalmic drugs market during the forecast period due to rising pet ownership, increasing awareness of animal healthcare, and rapid improvement in veterinary infrastructure across emerging economies. Growing disposable incomes, expanding livestock healthcare investments, and increasing access to advanced ophthalmic treatments are key drivers. In addition, the region’s large animal population and growing demand for preventive care continue to accelerate market expansion.

India Market Trends

India is expected to grow at the fastest CAGR during the forecast period due to rising pet adoption, increasing awareness of animal healthcare, and improving access to veterinary services. Growing disposable incomes and greater spending on companion animal wellness are boosting demand for advanced ophthalmic treatments. Additionally, expanding livestock healthcare initiatives and the rapid development of veterinary infrastructure are further accelerating market growth across the country.

Clinical Trials

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| Merck & Co., Inc. | New Jersey, U.S. | Offers veterinary eye care solutions, including infection-control drugs, anti-inflammatory formulations, and prescription therapies for ocular disorders in pets and farm animals. |

| Zoetis | New Jersey, U.S. | Provides a broad portfolio of animal eye health products such as ophthalmic drops, lubricants, anti-infectives, and supportive therapies for companion animals. |

| Dechra Pharmaceuticals | Cheshire, U.K. | Focuses on specialty veterinary medicines, including dry eye therapies, prescription eye solutions, and long-term ocular disease management products. |

| Virbac | Carros, France | Develops eye drops, ointments, gels, and anti-infective formulations designed for routine and chronic eye conditions in animals. |

| Ceva Santé Animale | Libourne, France | Offers veterinary pharmaceutical products for managing eye infections, inflammation, and chronic ophthalmic conditions in companion and livestock animals. |

| Elanco | Indiana, U.S. | Provides advanced animal health therapies, including anti-inflammatory and infection-targeted ophthalmic solutions for pets and farm animals. |

| Bausch & Lomb | Ontario, Canada | Known for ocular lubricants, artificial tears, eye drops, and vision-support products that are also used in veterinary eye care applications. |

Strengths

Weaknesses

Opportunities

Threats

By Drug Class

By Animal Type

By Indication

By Dosage Forms

By Distribution Channel

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar