")

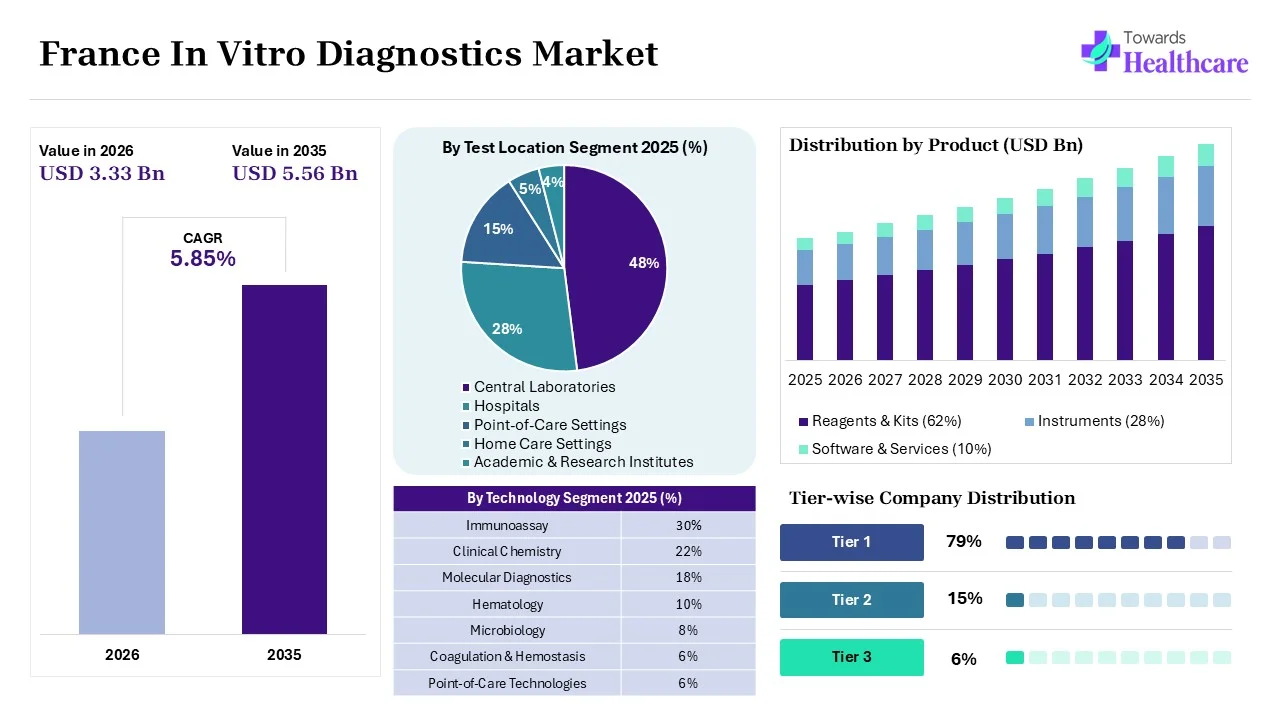

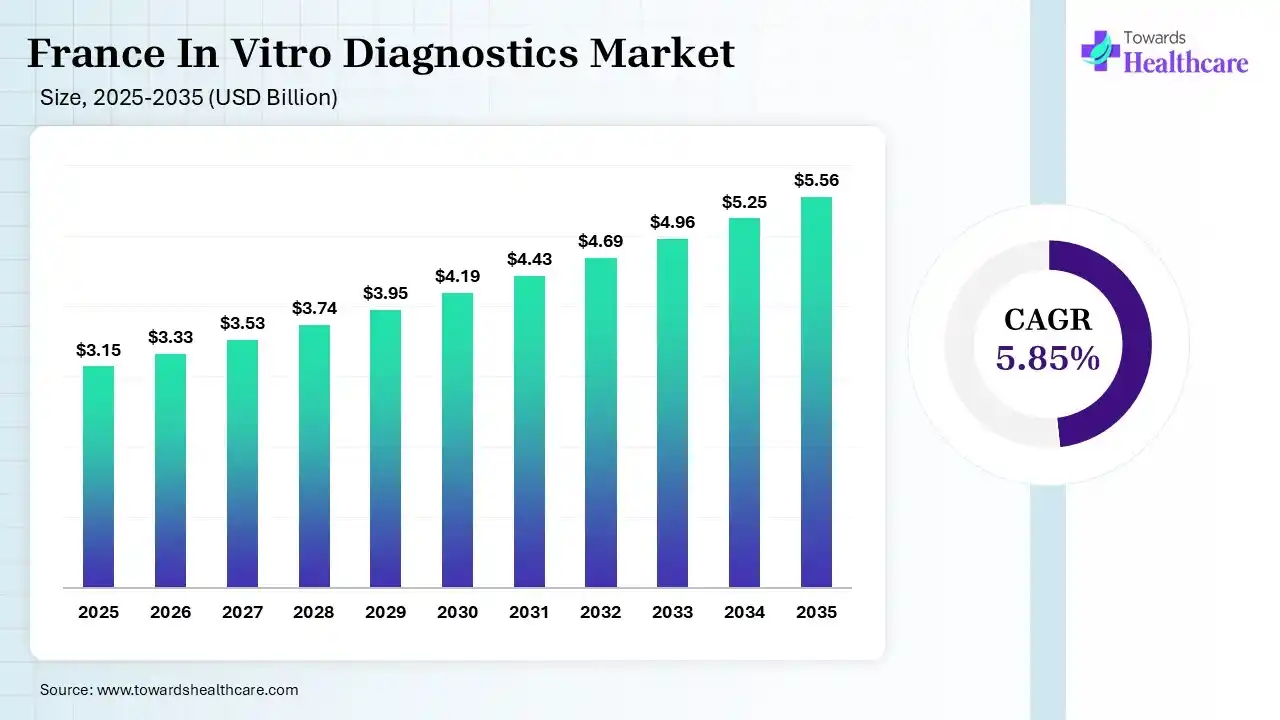

The France in vitro diagnostics market size was estimated at USD 3.15 billion in 2025 and is predicted to increase from USD 3.33 billion in 2026 to approximately USD 5.56 billion by 2035, expanding at a CAGR of 5.85% from 2026 to 2035. The growing chronic disease burden across France is increasing the demand for invasive diagnostics. Increasing health awareness, expanding molecular diagnostics, shifting towards personalized medicines, and technological advancements are also enhancing the market growth.

")

The France in vitro diagnostics market is driven by a growing aging population, chronic disease burden, and rising demand for rapid point-of-care testing kits. The market in vitro diagnostics encompasses various diagnostic tests and tools used for disease detection, monitoring, and treatment guidance across France. The growing diseases, such as infectious diseases, cardiovascular disease, diabetes, genetic disorders, and cancer, are increasing the demand for these diagnostic devices, where the use of biological samples, such as blood, urine, saliva, and tissue, is also driving their demand. They are also being used for monitoring disease progression, adjusting therapies, and evaluating treatment response.

At the same time, the growing health awareness and the advancing healthcare system are also increasing the use of various in vitro diagnostic kits across France. This, in turn, is increasing the demand for reagents, consumables, instruments, software, and diagnostic services to support the development and use of various in vitro diagnostic kits, such as molecular diagnostics, immunoassays, clinical chemistry, and point-of-care testing. With the growing focus on preventive healthcare, infection control, and increasing demand for personalized medicines, the demand for various in vitro diagnostics is also increasing. Additionally, increasing routine screening programs, demand for early disease detection, and technological advancements are also contributing to the market expansion.

AI plays an important role in the France in vitro diagnostics market as it helps in automated data analysis. It also helps in improving accuracy and enhancing interpretation, which drives their demand for early disease detection and supports molecular and genomic diagnostics, where it also offers predictive analytics, which help in personalized treatment planning. AI is also used for the assistance of digital pathology and real-time decision support, which accelerates disease diagnosis, increasing its demand.

Rising Focus on Preventive Healthcare

Increasing health awareness in France is driving the shift toward preventive healthcare and promoting its expansion. This, in turn, is increasing the demand for early disease detection, where the growing routine screening programs and government support are also increasing the use of in vitro diagnostic kits. They are being utilized for biomarker testing, regular health monitoring, and genetic testing, which help in reducing overall treatment costs and enhancing patient outcomes.

Point-of-Care Testing on the Rise

The rising demand for rapid testing and the growing shift towards self-health management are increasing the demand for point-of-care testing solutions. Their rapid disease testing, quick results, chronic disease monitoring, and decentralized disease diagnosis are also increasing their adoption rates, limiting the use of centralized laboratory testing. Furthermore, their portability and user-friendly diagnostic technique also increase their use, as they also help reduce hospital burden and enhance patient convenience.

Expanding Healthcare Digitalization

The growing digital transformation in the France healthcare sector is increasing the adoption of various digital tools such as electronic health records and cloud-based laboratory information systems, which are enhancing the efficiency and accuracy of various in vitro diagnostic tools. At the same time, expanding telemedicine platforms and remote patient monitoring trends are also increasing the demand for IVD kits, where their digital integration is enhancing their accessibility and accelerating the data transfer process as well. This is driving their use for personalized medicine development, real-time patient monitoring, and data sharing.

| Table | Scope |

| Market Size in 2026 | USD 3.33 Billion |

| Projected Market Size in 2035 | USD 5.56 Billion |

| CAGR (2026 - 2035) | 5.85% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By Technology, By Application, By Test Location, By End User |

| Top Key Players | bioMérieux SA, Diagnostica Stago SAS, Abbott Laboratories, F. Hoffmann-La Roche Ltd, Sebia SA, Siemens Healthineers AG, Eurobio Scientific |

")

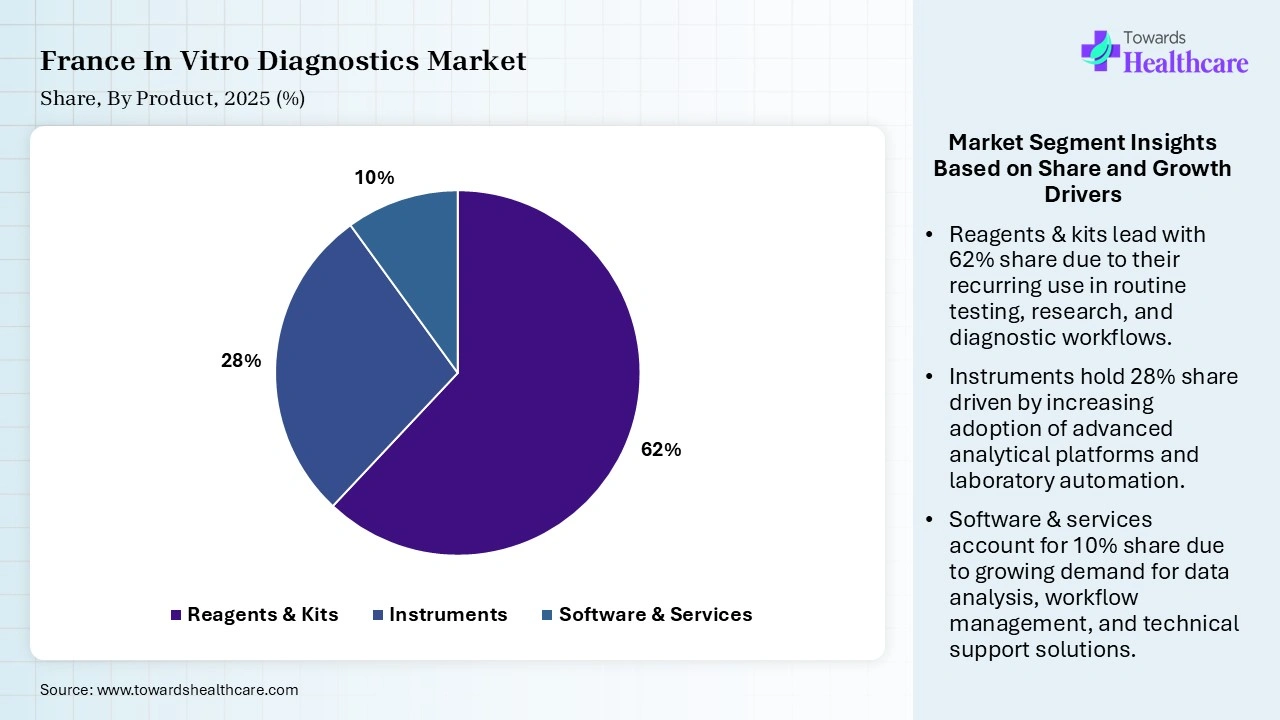

| Segment | Share 2025 (%) |

| Reagents & Kits | 62% |

| Instruments | 28% |

| Software & Services | 10% |

The Reagents & Kits Segment Dominated the Market With 62% in 2025

The reagents & kits segment led the France in vitro diagnostics market with a 62% share in 2025, due to high test volumes, which contributed to the recurring reagent consumption. Expansion of molecular testing and PCR testing has also increased their demand. Laboratories prioritized assay menu expansion, which increased their continuous usage.

The instruments segment held the second-largest share of 28% of the market in 2025, driven by increasing upgrades of automation platforms across hospitals. Increasing demand for high-throughput systems is also driving the adoption of various instruments. At the same time, digital laboratory transformation is also supporting their adoption.

The software & services segment held 10% of the France in vitro diagnostics market share in 2025 and is expected to witness the fastest growth with a CAGR of 7.50% during the forecast period, due to laboratories adopting AI-enabled workflows. Increasing connectivity requirements also promote their growth. Data management modernization accelerates investments, driving their expansion.

")

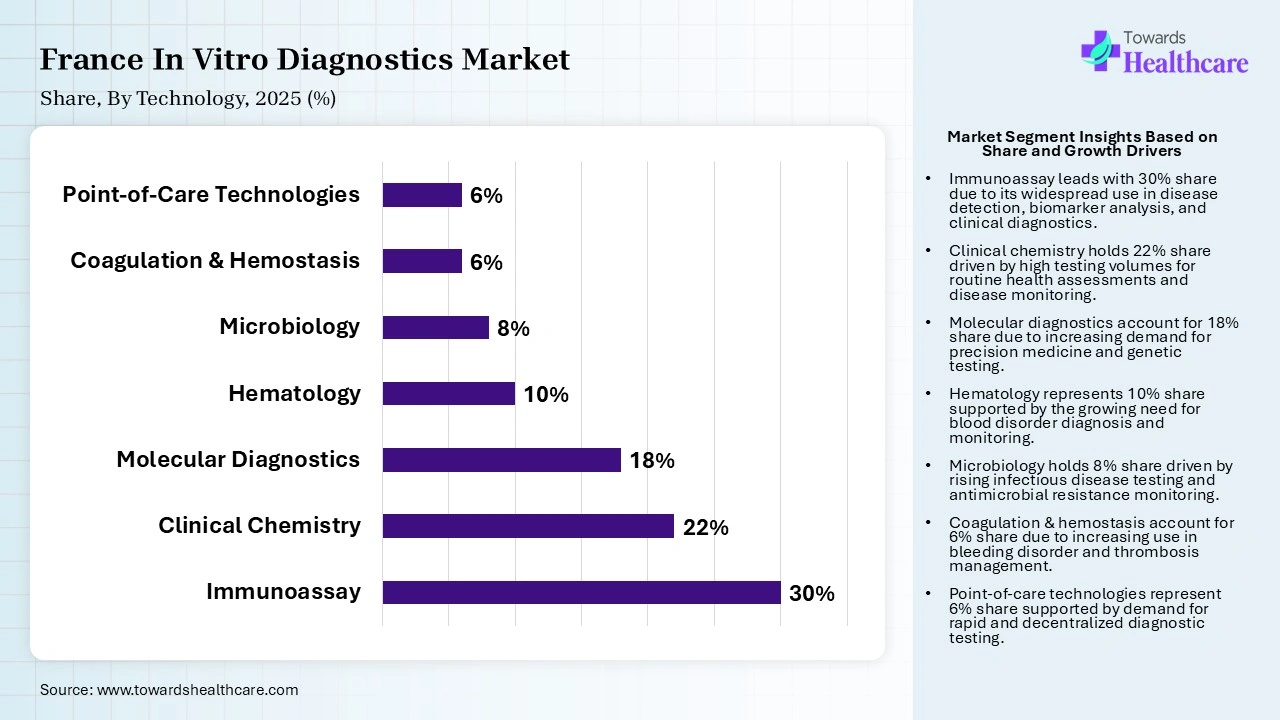

| Segment | Share 2025 (%) |

| Immunoassay | 30% |

| Clinical Chemistry | 22% |

| Molecular Diagnostics | 18% |

| Hematology | 10% |

| Microbiology | 8% |

| Coagulation & Hemostasis | 6% |

| Point-of-Care Technologies | 6% |

The Immunoassay Segment Dominated the Market With 30% in 2025

The immunoassay segment accounted for the highest revenue share of 30% of the France in vitro diagnostics market in 2025, driven by its widespread use in infectious disease and hormone testing. High clinical acceptance also supported their increased utilization. Growth in automation also improved laboratory efficiency, which increased their adoption rates.

The clinical chemistry segment held the second-largest share of 22% of the market in 2025, due to routine diagnostic screening, which sustains its demand. A rise in the aging population also increases testing volumes, driving their demand. The growing shift towards preventive healthcare is also expanding its utilization.

The molecular diagnostics segment held 18% of the France in vitro diagnostics market share in 2025 and is expected to show the highest growth with a CAGR of 8.2% during the forecast period, due to growing demand for precision medicine, which accelerates their adoption. PCR and NGS applications are also expanding rapidly. Early disease detection initiatives also support their growth.

The hematology segment held 10% of the market share in 2025, as CBC testing remains standard practice. The rise in the demand for chronic disease monitoring is also supporting the use of various hematology IVD kits. The growing advancements in hematology are also driving the development of automated solutions to improve workflow efficiency.

")

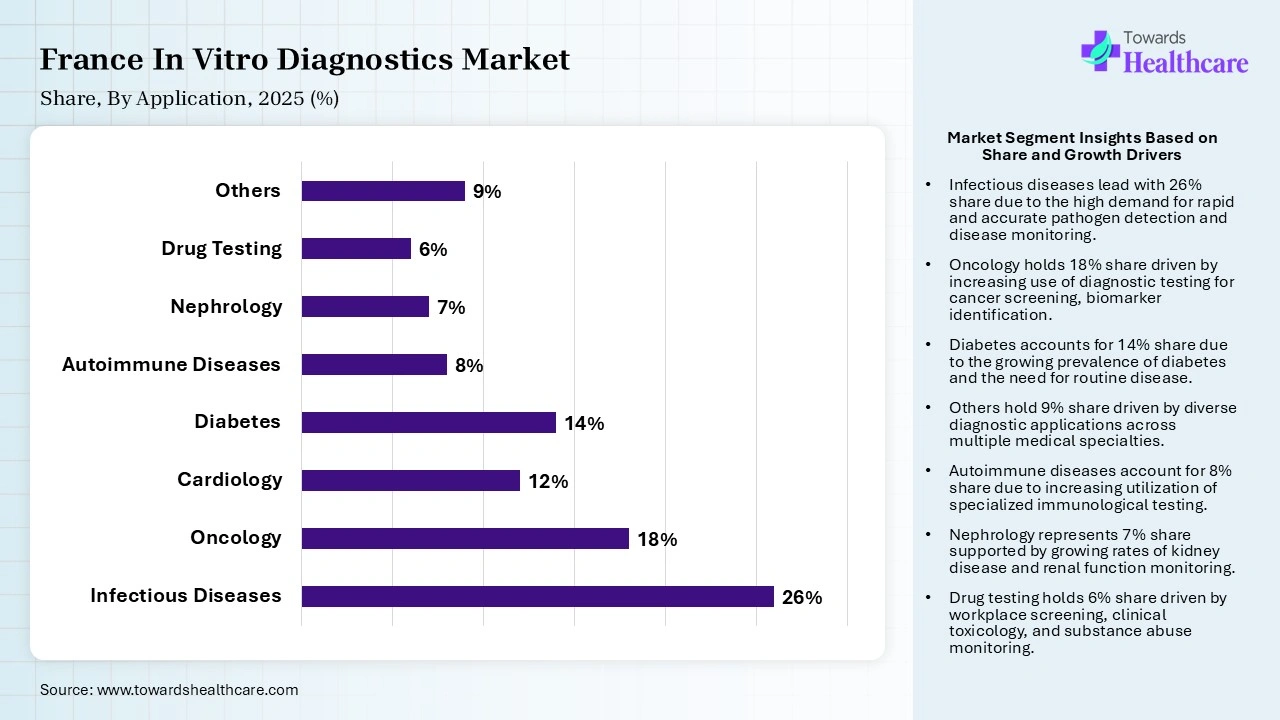

| Segment | Share 2025 (%) |

| Infectious Diseases | 26% |

| Oncology | 18% |

| Cardiology | 12% |

| Diabetes | 14% |

| Autoimmune Diseases | 8% |

| Nephrology | 7% |

| Drug Testing | 6% |

| Others | 9% |

The Infectious Diseases Segment Dominated the Market With 26% in 2025

The infectious diseases segment held a major revenue share of 26% of the France in vitro diagnostics market in 2025, due to the rise in continuous surveillance programs, which increased the testing demand. The growth in emerging infections also supported the in vitro diagnostics demand. Growth in public health initiatives also increased infectious disease screening, which contributed to its increased usage.

The oncology segment held the second-largest share of 18% of the market in 2025 and is expected to expand rapidly with a CAGR of 8.5% during the forecast period, driven by the rapid expansion of biomarker-based diagnostics. Increasing adoption of precision oncology is also driving the demand for IVD solutions. Early cancer detection also receives greater investment, encouraging the adoption of molecular diagnostics.

The diabetes segment held 14% of the France in vitro diagnostics market share in 2025, driven by the rising diabetic population, which increases monitoring demand. Expanding preventive screening programs and increasing health awareness are also increasing the adoption of various IVD kits. Frequent HbA1c testing also contributes to their rising demand.

The cardiology segment held 12% of the market share in 2025 due to the high cardiovascular disease burden. Expanding troponin and biomarker testing is also increasing new opportunities for IVD solutions. Hospitals emphasize rapid diagnosis, where routine diagnostic testing is also driving their demand. The growing shift towards preventive healthcare is also increasing the use of POC cardiac testing solutions.

")

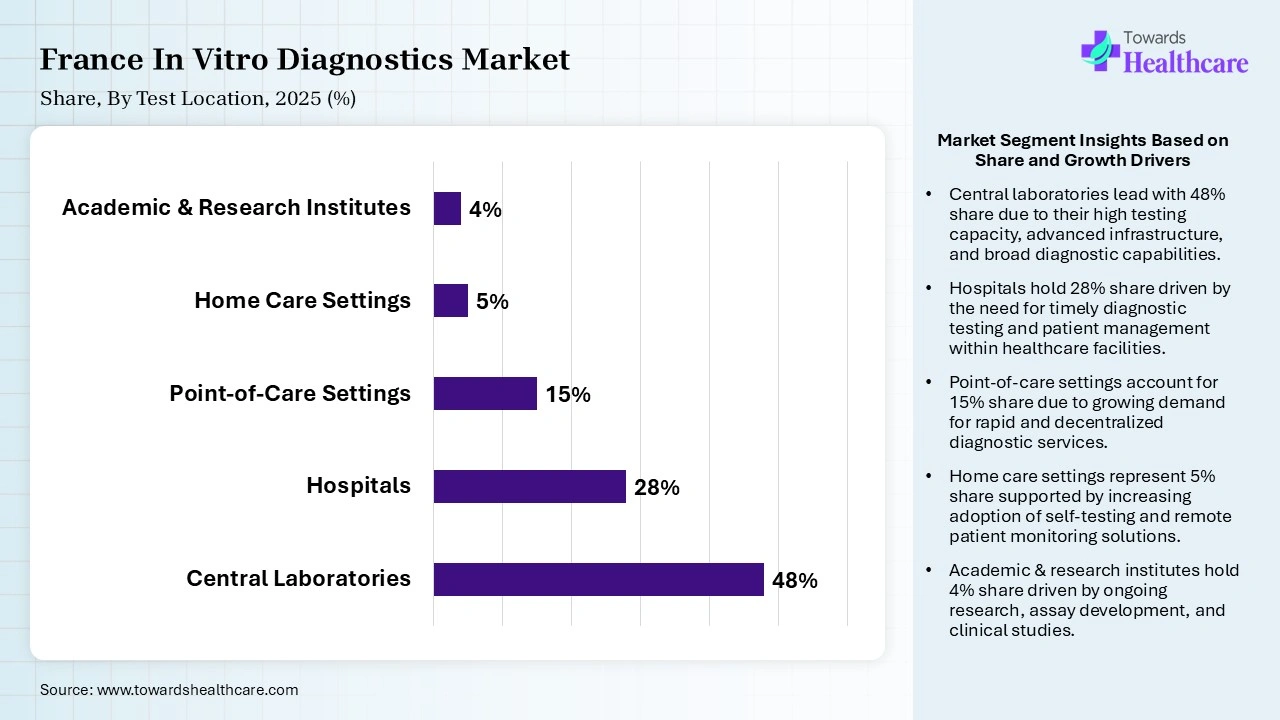

| Segment | Share 2025 (%) |

| Central Laboratories | 48% |

| Hospitals | 28% |

| Point-of-Care Settings | 15% |

| Home Care Settings | 5% |

| Academic & Research Institutes | 4% |

The Central Laboratories Segment Dominated the Market With 48% in 2025

The central laboratories segment held the largest revenue share of 48% of the France in vitro diagnostics market in 2025, driven by high-volume testing, which supported economies of scale. Advanced automation also improved its productivity, which increased its demand. Additionally, reference laboratories expand service portfolios, which also drive their adoption.

The hospitals segment held the second-largest share of 28% of the market in 2025 due to the presence of integrated diagnostic capabilities improving patient care. Increasing acute testing demand is also driving their preference. At the same continued investments in laboratory modernization are also increasing the adoption of advanced in vitro diagnostic products.

The point-of-care settings segment held 15% of the France in vitro diagnostics market share in 2025 and is expected to grow with the fastest CAGR of 8.1% during the forecast period, due to its rapid results improving clinical decisions. Expanding decentralized care models are also increasing their adoption rates. Rising portable diagnostic devices are also increasing their adoption.

The home care settings segment held 5% of the market share in 2025, driven by the increase in self-testing demand. A rise in digital health integration is also improving in vitro diagnostics accessibility. Growing focus on chronic disease management and increasing health awareness are also supporting their utilization.

")

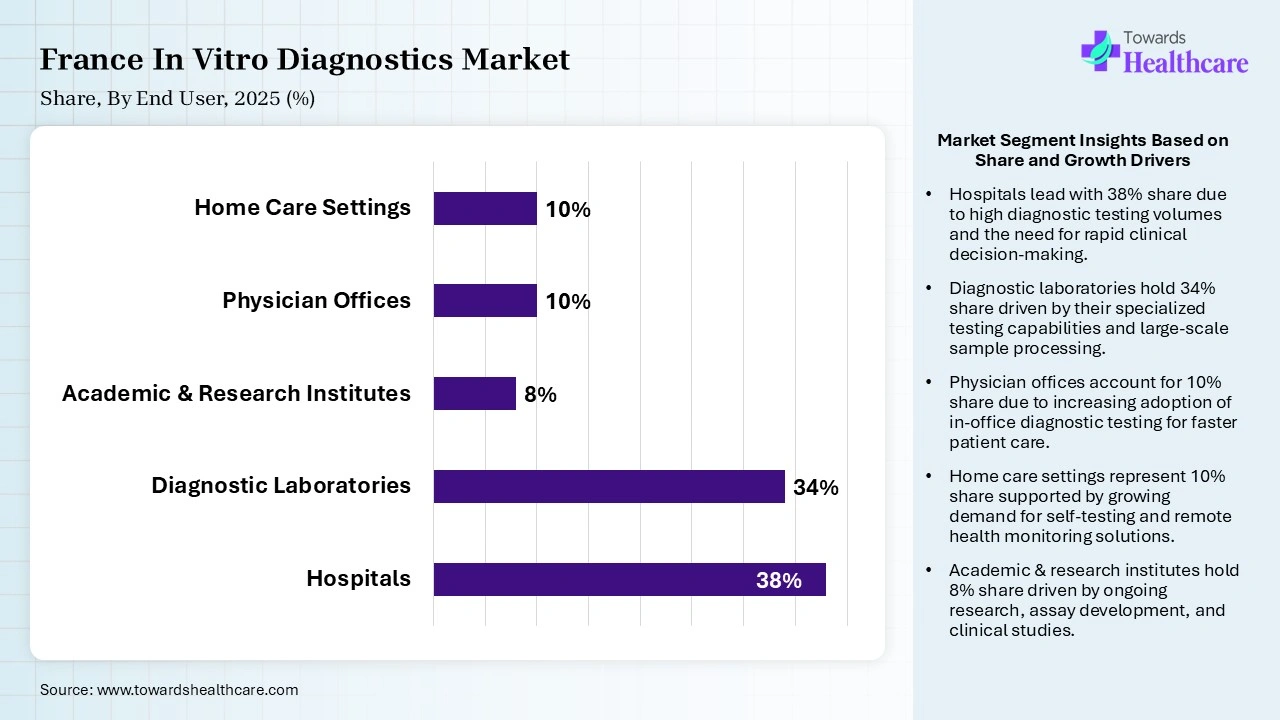

| Segment | Share 2025 (%) |

| Hospitals | 38% |

| Diagnostic Laboratories | 34% |

| Academic & Research Institutes | 8% |

| Physician Offices | 10% |

| Home Care Settings | 10% |

The Hospitals Segment Dominated the Market With 38% in 2025

The hospitals segment contributed the biggest revenue share of 38% of the France in vitro diagnostics market in 2025, due to large testing volumes, which sustained their demand. Continued investments in automated diagnostics also increased their adoption of advanced solutions. Clinical decision-making increasingly relies on laboratory data, which supports the use of various in-vitro diagnostic solutions.

The diagnostic laboratories segment held the second-largest share of 34% of the market in 2025, driven by an increase in outsourced testing volumes. The high-throughput platforms improve efficiency, which is attracting the clients. Specialized diagnostics drive service expansion, promoting new collaborations. Automated testing platforms are also increasing their use.

The home care settings segment held 10% of the France in vitro diagnostics market share in 2025 and is expected to gain the highest share with a CAGR of 8.0% during the forecast period, driven by increasing consumer self-testing. Expanding adoption of remote healthcare is also increasing the use of various home-based diagnostic solutions. Digital monitoring platforms are also supporting their growth.

The academic & research institutes segment held 8% of the market share in 2025, due to expanding biomarker discovery research activities. At the same time, growing public funding is also supporting innovations. Expanding clinical studies are also increasing the demand for advanced diagnostics. The growing focus on precision medicine is also increasing the use of IVD products.

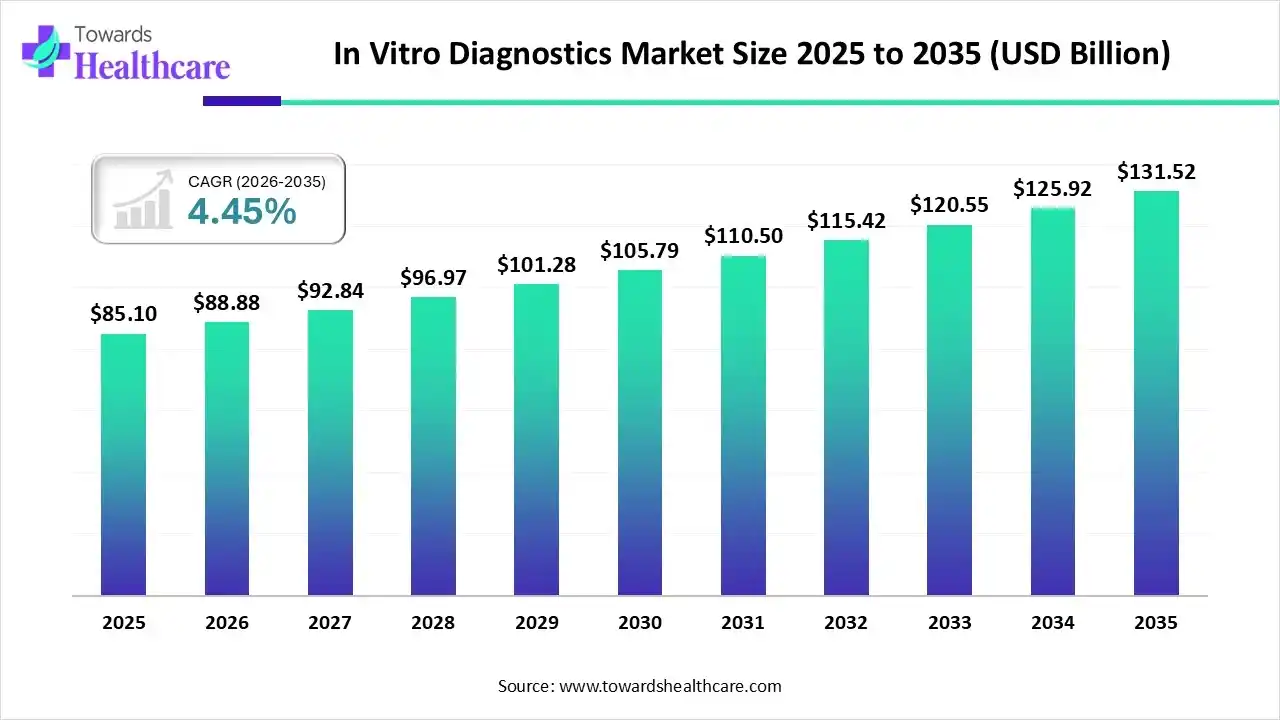

The global in vitro diagnostics market was estimated at US$ 85.1 billion in 2025 and is projected to grow to US$ 131.52 billion by 2035, rising at a compound annual growth rate (CAGR) of 4.45% from 2026 to 2035.

")

The France in vitro diagnostics market held a notable share and is expected to grow significantly during the forecast period, due to the growing incidence of chronic diseases. The rising geriatric population is also increasing the demand for in vitro diagnostic kits for the rapid and accurate detection of diabetes, infectious diseases, cardiovascular diseases, and cancer. Increasing demand for precision medicines and point-of-care testing is also driving the development of advanced in vitro diagnostic kits. Growing government initiatives, investments, and collaborations are also increasing the demand for these kits, which is enhancing the market growth.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | In Vitro Diagnostics in France |

| bioMérieux SA | Marcy-I’Etoile | BIOFIRE Panel, VIDAS Assays, VITEK Cards, and Bac T/Alert Blood Culture Bottles |

| Diagnostica Stago SAS | Asnieres-sur-Seine | STA-NeoPTimal, STA-Neoplastine R, C. K. Prest, STA Hepari Control Kits, and STA Liatest/ D-Dimer Kits |

| Abbott Laboratories | Abbott Park, U.S. | Panbio Kits, Alinity i/c Reagents, i-STAT Cartridges, and Architect Assays |

| F. Hoffmann-La Roche Ltd | Basel, Switzerland | Cobas PCR Kits, Cedex Kits, Elecsys Kits, and Accu-Check |

| Sebia SA | Lisses | HYDRASYS Immunofixation Kits, HYDRASHIFT Portfolios, and CAPILLARYS HbA1c |

| Siemens Healthineers AG | Illkirch-Graffenstaden | Advia Kits, Novus Strips, Atellica IM/CH Reagents, and Enlite/Dimension Packs |

| Eurobio Scientific | Les Ulis | EurobioPlex DermaTyping, EurobioPlex Meningitis kits, and EurobioPlex Viral Kits |

In November 2025, after announcing an exclusive distribution agreement between ABL Diagnostics, a French company specializing in advanced molecular diagnostics, and Eurobio Scientific, a leading in vitro diagnostics company, the CEO of ABL Diagnostics, Chalom Sayada, expressed, “This partnership with Eurobio Scientific is fully aligned with our growth strategy in the public hospital market. It allows us to optimize commercial coverage while ensuring proximity service and high-level technical support.”

By Product

By Technology

By Application

By Test Location

By End User

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar