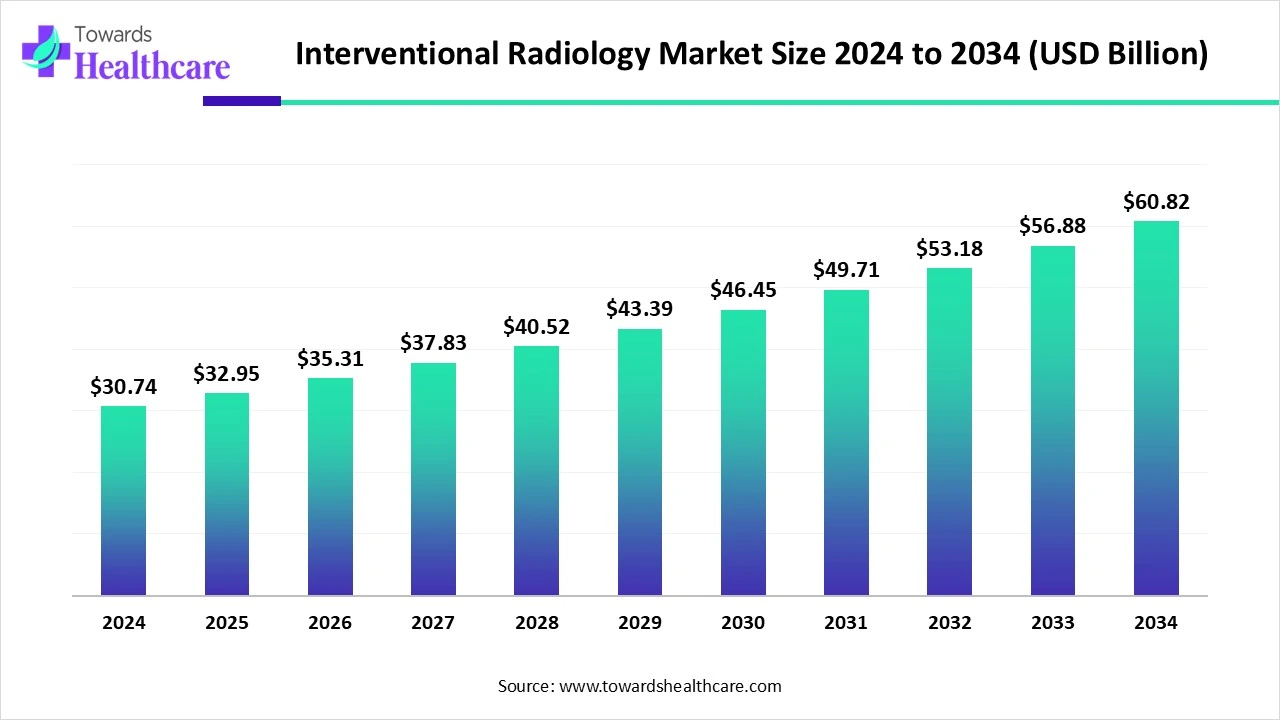

The global interventional radiology market size is calculated at US$ 30.74 billion in 2024, grew to US$ 32.95 billion in 2025, and is projected to reach around US$ 60.82 billion by 2034. The market is expanding at a CAGR of 7.17% between 2025 and 2034.

")

Due to the growing popularity of minimally invasive, image-guided medical treatments, the interventional radiology market has transformed into a force that is revolutionising contemporary healthcare. The management of several disorders affecting different organ systems, including central venous access procedures, currently depends heavily on IR techniques. By precisely guiding thin catheters and guidewires through blood vessels using cutting-edge imaging technologies, interventional radiologists can deliver fluids, food, and medications directly into the bloodstream while maintaining the patient's level of comfort and reducing the need for repeated needle insertions.

| Metric | Details |

| Market Size in 2025 | USD 32.95 Billion |

| Projected Market Size in 2034 | USD 60.82 Billion |

| CAGR (2025 - 2034) | 7.17% |

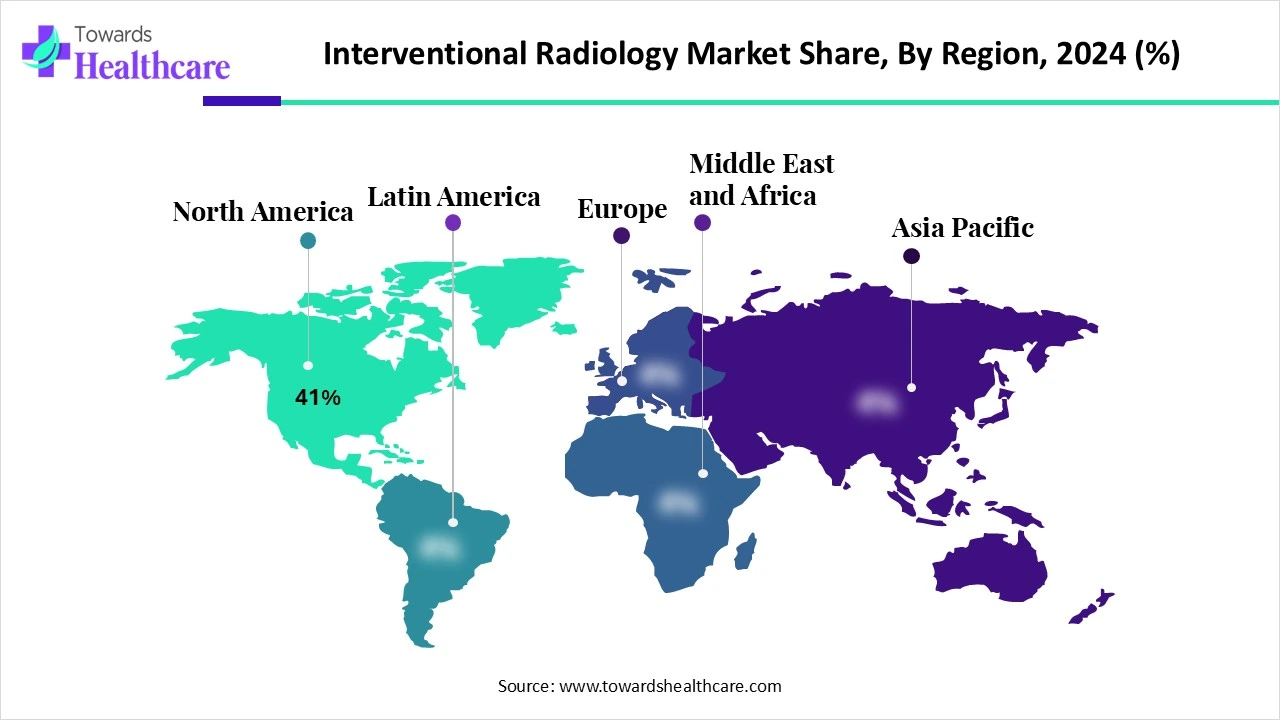

| Leading Region | North America share by 41% |

| Market Segmentation | By Product Type, By Procedure Type, By Application, By End User, By Imaging Modality, By Region |

| Top Key Players | Medtronic plc, Boston Scientific Corporation, Johnson & Johnson (Cordis), Stryker Corporation, Siemens Healthineers, GE HealthCare, Philips Healthcare, Cook Medical, Terumo Corporation, Becton, Dickinson and Company (BD), Abbott Laboratories, Merit Medical Systems, Inc., AngioDynamics, Inc., Penumbra, Inc., Canon Medical Systems Corporation, Ziehm Imaging GmbH, Shimadzu Corporation, BTG International (a part of Boston Scientific), Alpinion Medical Systems, Teleflex Incorporated |

The interventional radiology market refers to the segment of minimally invasive, image-guided procedures performed to diagnose and treat various medical conditions. Using advanced imaging modalities such as fluoroscopy, CT, ultrasound, or MRI, IR specialists guide catheters, stents, and other instruments through small incisions. These procedures are alternatives to open surgeries, offering faster recovery, reduced complications, and lower healthcare costs. IR is widely used in oncology, cardiology, neurology, nephrology, and vascular medicine, and is rapidly evolving with the integration of robotics, AI-guided imaging, and drug-device combinations.

Although AI is now widely used in diagnostic radiology, interventional radiology is just starting to see its effects. AI has the potential to significantly alter interventional radiology's routine practice on a number of levels. Recent developments in deep learning models, especially foundation models, allow for more autonomy and efficient handling of multimodality in the preoperative scenario because of their minimally supervised operation. The foundation for greater autonomy is being laid by AI. From the standpoint of research, the creation of artificial health data, such as AI-based data augmentation, offers a novel approach to this major problem and is expected to encourage further study in this field.

For instance,

How does the Demand for Minimally Invasive Diagnostics Promote the Market’s Expansion?

The market for interventional radiology is being driven by the need for less invasive technologies because of their many advantages. Modern medicine has greatly benefited from the development of less invasive technology. These technologies enable therapeutic and diagnostic procedures with less discomfort and tissue damage, as well as a quicker recovery. Typically, these approaches result in a significantly shorter hospital stay and lower expenses. According to the cost-benefit analysis, the intervention's cost reductions will often exceed its initial cost. As a result, intensive care units are increasingly utilizing these technological advancements to enhance patient care in several ways. In certain instances, these methods enable the timely identification of pathological processes and the implementation of effective therapies that can prevent further organ failure.

Restricted Access and Limited Availability

Not all clinics and hospitals have the required equipment and qualified experts, which is one of the major problems in interventional radiology. to carry out these processes. The fact that not all health systems provide funding for these operations is another drawback. And this might lead to financial obstacles that prevent people from accessing this field of medicine. Patients in underdeveloped nations or remote places might not have access to interventional radiologists or sophisticated imaging technology, which would restrict their ability to get these therapies.

What is the Future of Interventional Radiology?

There is a bright future for infrared, as technological and imaging developments will broaden the field's scope to a level that was previously thought to be unthinkable or unachievable. Interventional radiology has a promising future as new technologies, such as 3D printing and robotic-assisted surgery, become more widely accessible. IRs may now reach parts of the body that were previously inaccessible for direct treatment. Advances in imaging technology are also enhancing diagnostic capabilities and enabling IRs to execute effective treatments at a significantly greater rate. One new and promising technology in interventional radiology is the use of nanoparticles.

By product type, the catheters segment held the largest share of the interventional radiology market in 2024. When performing diagnostic angiograms or interventions in different vascular areas, the interventional radiologist's toolkit includes a variety of catheters to meet varied demands. Compared to open surgery, they have the advantages of less discomfort, quicker recovery, and a lower risk of infection. They make it possible to treat a variety of ailments with focused care and accurate administration of treatments like angioplasty and stenting.

By product type, the balloon catheters segment is estimated to grow at the highest CAGR during the upcoming period. Balloon catheters have become essential tools that are used in many therapeutic and diagnostic processes. By enabling less invasive operations, balloon catheters help to lower the risks and recovery periods associated with more conventional surgical techniques. Furthermore, a continuous dedication to efficiency and safety is seen in the balloon catheter technology's gradual evolution. Inventions like balloons that elute drugs.

Among the balloon catheters segment, the drug-coated balloons sub-segment is expected to grow at the fastest CAGR during the forecast period. As a first-line treatment for in-stent restenosis, DCBs offer better long-term vessel patency than traditional balloon angioplasty and may be on par with drug-eluting stents without the need for an extra stent layer. Patients who are at a high risk of bleeding may potentially benefit from DCBs.

By procedure type, the angioplasty & vascular stenting segment led the interventional radiology market in 2024. Cardiovascular disease claimed the lives of 919,032 people in 2023. That represents one death out of every three. Nearly one in six deaths from cardiovascular diseases (CVDs) in 2023 occurred in persons under the age of 65. Cardiovascular mortality is expected to grow by 90.0%, crude mortality by 73.4%, and crude DALYs by 54.7% between 2025 and 2050, resulting in an estimated 35.6 million cardiovascular deaths (up from 20.5 million in 2025). In addition, the requirement for vascular stenting and angioplasty will increase as the number of patients with CVD increases.

By procedure type, the thrombolysis & thrombectomy segment is anticipated to witness the fastest growth rate during the forecast period. Since thrombosis causes one out of every four fatalities globally, it is a top public health concern. To treat ischemic stroke, pulmonary embolism, and deep vein thrombosis (DVT), physicians may employ one or both of these therapy modalities. After an acute ischemic stroke, reperfusion either with intravenous thrombolytic medication therapy or, in some situations, with endovascular mechanical thrombectomy significantly increases the chance of a recovery free of impairment.

By application, the oncology segment dominated the interventional radiology market in 2024. As a specialisation of interventional radiology, interventional oncology focuses on employing image-guided, minimally invasive techniques to treat cancer patients. As a recent addition to the established pillars of medical oncology, surgery, and radiation oncology, interventional oncology has grown to be so crucial to the care of cancer patients that many people now view it as the fourth pillar of oncology. Interventional oncology has a bright future since it can make use of new technology.

By application, the neurological disorders segment is estimated to be the fastest-growing during 2025-2034. According to the 2024 Global Burden of Disease assessment, neurological diseases afflict 43% of the world's population. Regional differences in illness prevalence were probably caused by the global north-south divide, which affects a number of facets of the economy, including inequality, wealth, health spending, and access to care. Interventional neurology is a cutting-edge and quickly developing specialty that offers minimally invasive treatments for a variety of neurological conditions by combining the knowledge of several other fields.

By end-user, the hospitals segment captured the major share of the interventional radiology market in 2024. Even though many interventional radiology treatments are less invasive and can be done in outpatient settings, patients frequently choose hospitals for these procedures because of the complete care, state-of-the-art facilities, and expertise available. Patients, especially those with severe ailments or those who may need longer recovery periods, may find it reassuring that hospitals offer a greater selection of experts, emergency services, and the infrastructure to address any problems.

By end-user, the ambulatory surgical centers (ASCs) segment is expected to witness the highest CAGR during the predicted timeframe. Modern medical facilities specialising in same-day surgical treatment, including diagnostic and preventative procedures, are known as ambulatory surgery centres, or ASCs. With a solid reputation for high-quality treatment and successful patient outcomes, ASCs have provided millions of patients with a more convenient option to hospital-based outpatient operations, revolutionising the outpatient experience.

By imaging modality, the fluoroscopy/angiography systems segment was dominant in the intervention radiology market in 2024. The ability to provide real-time, moving images of internal body structures and processes is the primary reason why fluoroscopy and angiography technologies offer several significant benefits in medical imaging and treatment. This enables accurate diagnosis, successful treatment of various medical disorders, and precise guidance during treatments.

By imaging modality, the CT-guided procedures segment is estimated to grow at the fastest CAGR during the forecast decade. Many medical centres now use CT-guided operations as part of their standard diagnostic practice; in some, because of the large number of interventions, these facilities have special CT scanners for this reason. For CT-guided treatments, all manufacturers provide hardware and software enhancements to enhance working conditions, lowering radiation dosages and process times. CT-guided interventional treatments are a safe and efficient way to drain fluid collections and take biopsies from tumours that cannot be reached with endoscopic or US guidance.

")

North America dominated the interventional radiology market share by 41% in 2024. The high incidence of chronic diseases like diabetes, cancer, and cardiovascular disease in North America, especially the U.S., is a major factor in the need for interventional radiology procedures. The market's expansion is aided by the substantial need for less invasive therapies to address various ailments. Further propelling market development are North America's sophisticated healthcare system and advantageous reimbursement practices, which promote the use of cutting-edge interventional radiology technology.

According to a recent American Heart Association data study, heart disease is once again the country's top cause of death. Dr. Keith Churchwell, president of the American Heart Association, stated in a news release that about 2,500 Americans continue to lose their lives to cardiovascular disease every day. In the U.S., 57% of individuals have been diagnosed with Type 2 diabetes or prediabetes, and roughly 47% have high blood pressure, according to the report. Two of the main risk factors for cardiovascular disease are high blood pressure and diabetes.

In 2023, cancer and heart disease accounted for 43.7% of fatalities, up from 42.4% in 2022, making them the major causes of death. 22,147 fatalities in 2023, or slightly more than two-thirds (67.8%) of all deaths, were attributable to the top 10 causes of death. Compared to the rest of Canada (46.1%), the Atlantic provinces (59.0% in Newfoundland and Labrador, 55.8% in Prince Edward Island, 54.2% in Nova Scotia, and 55.0% in New Brunswick) and Manitoba (49.4%) had higher rates of having one or more chronic diseases in 2023.

Asia Pacific is estimated to host the fastest-growing interventional radiology market during the forecast period. Because of the growing number of people with diabetes, the rising incidence of chronic renal disease, and the growing healthcare system. Due mostly to increased rates of diabetes and hypertension, China, India, and Japan are seeing an increase in the number of CKD patients within this area. Private investments in this industry and government initiatives promoting access to healthcare have raised demand for dialysis services and the necessary technology. The use of home and portable dialysis systems has also increased significantly in the area; the healthcare system is considering this because of its affordability and variety of treatment options.

In China, there are at least 90 million RD sufferers. In China, RDs are surprisingly widespread while being referred to be rare, and they significantly impact healthcare and the economy. Nearly half of all RDs damage the nervous system and muscles, and rare neurological disorders (RNDs) make up a sizable fraction of all RDs. In the Chinese First National List of RDs, RNDs make up one-third of the 121 RDs. There is research from various nations and demographics that estimates the prevalence of RNDs to be between 8.9% and 53.4%.

Numerous neurological disorders (NDs) are more common in India due to both geographic and environmental causes. A startling 168% increase in Parkinson's disease (PD) cases is predicted for India by 2050, bringing with it a neurological tsunami. India will now account for 10% of the world's Parkinson's disease cases, with an estimated 2.8 million cases, a significant increase from 2021 levels. 25.2 million individuals worldwide are expected to have Parkinson's disease, a rise of 112% from 2021.

Europe is expected to grow significantly in the interventional radiology market during the forecast period. Europe's steady growth is supported by robust university hospital networks and strict device safety regulations. With 594 medical technology applications in 2024, Philips dominated European Patent Office submissions, enhancing the region's standing as a leader in innovation. European Union cohesion funds are used by Eastern European systems to improve angiography laboratories and increase procedure capacity.

By 2050, Germany's population is expected to drop by 16%, and the proportion of young to old is moving in favour of the elderly. An ageing society will face a greater burden of illnesses as the risk of sickness increases with age. From its 2007 population of 82.2 million to its 2050 population of 68.8 million, Germany will have lost around 16.3% of its total population.

Compared to 2021, the number of persons with Parkinson's disease may more than double by 2050, according to a British Medical Journal (BMJ) research. It is estimated that 11 million people in the United Kingdom suffer from a neurological ailment. Some cause death very quickly. Some lead to a slow deterioration in function. Some are crippling and persistent. Together, they account for almost 140,000 deaths annually in the UK, or one-fifth of all fatalities, and they are a major contributor to disability.

In March 2025, according to SIR Foundation head Maureen P. Kohi, MD, the Ernest H. Wood Distinguished Professor and head of the Department of Radiology at the University of North Carolina in Chapel Hill, research often suffers from uneven funding, leaving large gaps in important areas. With its wide network of committed funders and researchers who are all committed to furthering interventional radiology research, the SIR Foundation is particularly positioned to meet this challenge. (Source - Health Imaging)

By Product Type

By Procedure Type

By Application

By End User

By Imaging Modality

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar