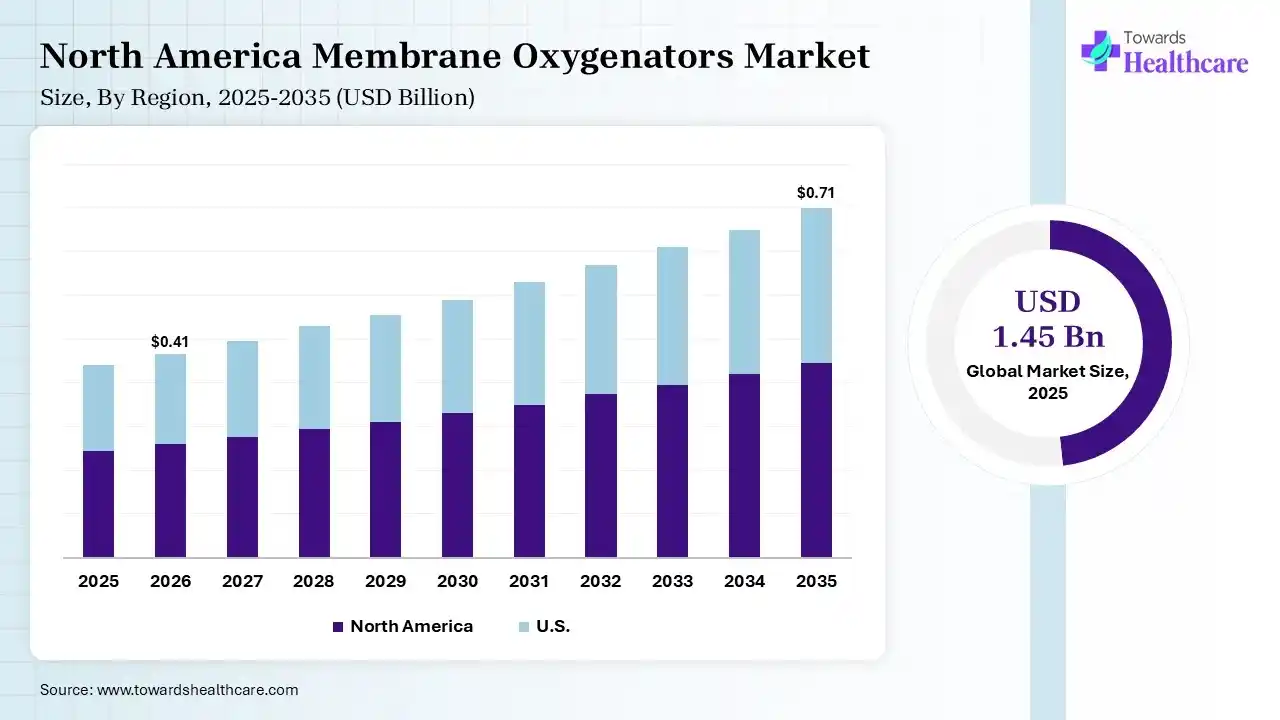

The global membrane oxygenators market size was estimated at USD 1.45 billion in 2025 and is predicted to increase from USD 1.55 billion in 2026 to approximately USD 2.83 billion by 2035, expanding at a CAGR of 6.9% from 2026 to 2035. The market is expanding because of the growing need for advanced life-support devices in cardiac surgeries, emergency care, and severe respiratory treatment.

")

The membrane oxygenator is a medical device that temporarily performs the function of the lungs by supplying oxygen to the blood and removing carbon dioxide through a special membrane. The membrane oxygenators market is growing due to the rising prevalence of cardiovascular and respiratory disorders, increasing use of ECMO in critical care, and a growing number of cardiac surgeries worldwide. Technological advancements in hollow fiber oxygenators and improved hospital infrastructure are further supporting adoption. Additionally, the rising geriatric population and demand for advanced life-support systems continue to accelerate market expansion.

AI can influence the market by enabling smarter patient monitoring, early risk detection, and real-time support for clinical decisions during ECMO and cardiac procedures. It also improves device efficiency, helps personalize treatment plans, and encourages the adoption of advanced oxygenation systems across hospitals and intensive care units.

Growing demand for critical care support

The increasing number of patients requiring cardiac surgery and respiratory assistance is driving demand for membrane oxygenators. Hospitals are expanding intensive care capabilities, which is expected to support long-term market growth and wider adoption of advanced oxygenation systems.

Innovation in device design and performance

Future trends include more compact, efficient, and biocompatible oxygenators that improve blood oxygen exchange while minimizing complications. Continuous product innovation is likely to enhance treatment outcomes and increase usage across both adult and pediatric care settings.

Expansion across developing healthcare markets

Emerging economies are investing more in hospital infrastructure and advanced life-support technologies. As access to specialized critical care improves, these regions are expected to create strong future growth opportunities for membrane oxygenator manufacturers.

| Table | Scope |

| Market Size in 2026 | USD 1.55 Billion |

| Projected Market Size in 2035 | USD 2.83 Billion |

| CAGR (2026 - 2035) | 6.9% |

| Leading Region | North America by 34% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Material, By Application, By Age Group, By End User, By Region |

| Top Key Players | Medtronic, Fresenius SE & Co. KGaA, Getinge AB, TERUMO CORPORATION, MicroPort Scientific Corporation, Nipro Medical Corporation, Kewei Medical |

| Segment | Share 2025 (%) |

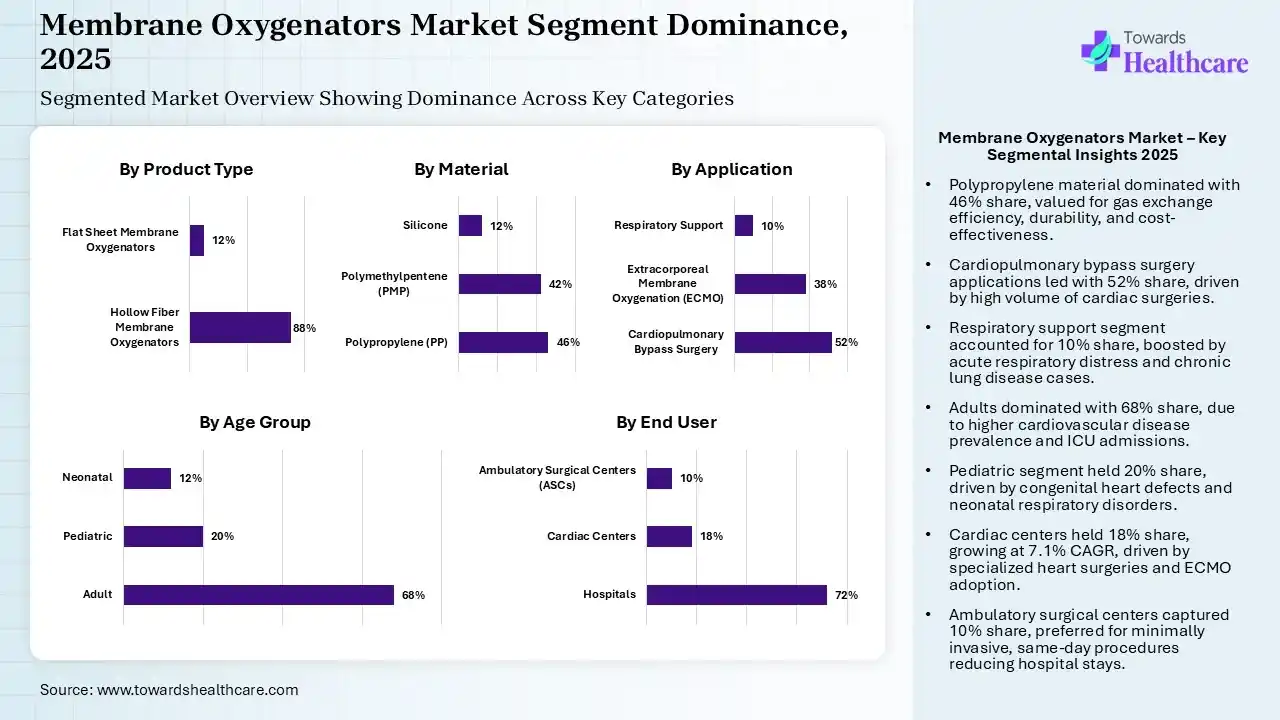

| Hollow Fiber Membrane Oxygenators | 88% |

| Flat Sheet Membrane Oxygenators | 12% |

The Hollow Fiber Membrane Oxygenators Segment Dominated the Market in 2025

The hollow fiber membrane oxygenators segment dominated the membrane oxygenators market with shares of 88% in 2025 and is expected to grow at the fastest CAGR of 6.90% during the forecast period, because it offers efficient oxygen and carbon dioxide exchange, reliable performance during long procedures, and reduced risk of blood damage. Its extensive use in ECMO, cardiac surgeries, and critical care settings made it the most widely preferred product type across hospitals and specialty centers.

The flat sheet membrane oxygenators segment held the second largest market share of 12% in 2025 due to its stable performance, effective gas transfer, and suitability for specific cardiac and short-term extracorporeal procedures. Its simple structural design, ease of integration into existing systems, and continued use in specialized surgical applications supported its strong position in the market.

| Segment | Share 2025 (%) |

| Polypropylene (PP) | 46% |

| Polymethylpentene (PMP) | 42% |

| Silicone | 12% |

The Polypropylene (PP) Segment Led the Market in 2025 with the Largest Share

The polypropylene (PP) segment led the membrane oxygenators market with shares of 46% in 2025 because of its high gas exchange efficiency, durability, and compatibility with blood-contact applications. Its lightweight nature and cost-effective manufacturing make it widely used in membrane oxygenators, particularly for ECMO and cardiac procedures, strengthening its leading position in the market.

The polymethylpentene (PMP) segment held the second largest market share of 42% in 2025 and is expected to grow at the fastest CAGR of 8.20% in the market during the forecast period due to its superior gas permeability, excellent biocompatibility, and long-term stability. Its low plasma leakage and high durability make it highly suitable for prolonged ECMO support and advanced critical care applications, driving faster adoption during the forecast period.

The silicon segment held 12% of the membrane oxygenators market share in 2025 due to its excellent flexibility, high oxygen permeability, and strong biocompatibility, making it suitable for efficient blood oxygenation applications. Its ability to maintain stable performance during prolonged procedures and reduce the risk of adverse reactions is increasing its use in specialized membrane oxygenators and advanced critical care systems.

| Segment | Share 2025 (%) |

| Cardiopulmonary Bypass Surgery | 52% |

| Extracorporeal Membrane Oxygenation (ECMO) | 38% |

| Respiratory Support | 10% |

The cardiopulmonary bypass Surgery Segment Led the Market in 2025 with the Largest Share

The cardiopulmonary bypass surgery segment led the membrane oxygenators market with shares of 52% in 2025 due to the high volume of cardiac surgeries requiring temporary heart and lung support. Membrane oxygenators are essential in these procedures for maintaining blood oxygenation and circulation, making them widely used across hospitals and specialized cardiac care centers.

The extracorporeal membrane oxygenation (ECMO) segment held the second largest market share of 38% in 2025 and is expected to grow at the fastest CAGR of 8.50% in the market during the forecast period due to the rising use of advanced life-support systems for severe cardiac and respiratory failure. Increasing ICU admissions, growing awareness of ECMO therapy, and expanding critical care infrastructure are driving its rapid adoption during the forecast period.

The respiratory support segment held 10% of the membrane oxygenators market share in 2025 due to the increasing incidence of acute respiratory distress, chronic lung diseases, and critical care admissions requiring advanced oxygenation support. Rising demand for membrane oxygenators in ICU settings, especially for patients with severe respiratory failure, is boosting adoption. Improvements in hospital infrastructure and greater availability of life-support technologies are further supporting the segment’s growth.

| Segment | Share 2025 (%) |

| Adult | 68% |

| Pediatric | 20% |

| Neonatal | 12% |

The Adult Segment held a dominant position in the Market in 2025

The adult segment held a dominant position in the membrane oxygenators market with a share of 68% in 2025 due to the higher prevalence of cardiovascular diseases, respiratory disorders, and cardiac surgeries among the adult and elderly populations. Adults account for the majority of ECMO and cardiopulmonary bypass procedures, leading to greater demand for membrane oxygenators. Additionally, rising age-related health complications and ICU admissions further strengthened this segment’s market leadership.

The pediatric segment held 20% of the market share in 2025 due to the rising diagnosis of congenital heart defects and neonatal respiratory disorders, and the increasing need for specialized critical care support in infants and children. Advancements in pediatric ECMO and oxygenation technologies, along with improved neonatal intensive care facilities, are further driving demand for membrane oxygenators in this segment.

The neonatal segment held 12% of the membrane oxygenators market share in 2025 and is expected to grow at the fastest CAGR of 7.60% in the market during the forecast period due to the rising incidence of premature births, neonatal respiratory distress, and congenital heart conditions. Increasing investments in neonatal intensive care units and advancements in specialized oxygenation systems for newborns are driving rapid growth in the segment during the forecast period.

| Segment | Share 2025 (%) |

| Hospitals | 72% |

| Cardiac Centers | 18% |

| Ambulatory Surgical Centers (ASCs) | 10% |

The Hospitals Segment Dominated the Market in 2025

The hospitals segment led the membrane oxygenators market with a share of 72% in 2025 due to the high volume of cardiac surgeries, ECMO procedures, and critical care treatments performed in hospital settings. Hospitals are equipped with advanced infrastructure, specialized surgical teams, and intensive care units, making them the primary users of membrane oxygenators. Rising patient admissions for cardiovascular and respiratory conditions further strengthened this segment’s leading position.

The cardiac centers segment held the second largest market share of 18% in 2025 and is expected to grow at the fastest CAGR of 7.1% in the market during the forecast period due to the increasing number of specialized heart surgeries, rising prevalence of cardiovascular diseases, and growing preference for dedicated cardiac care facilities. This advanced surgical infrastructure, expert specialists, and higher adoption of ECMO and bypass technologies are driving rapid market growth during the forecast period.

The ambulatory surgical centers (ASCs) segment held 10% of the membrane oxygenators market share in 2025 due to the rising preference for minimally invasive and same-day surgical procedures that reduce hospital stay and overall treatment costs. Increasing advancements in compact oxygenation systems and improved surgical capabilities at ASCs are supporting their adoption. Additionally, faster patient turnover and growing demand for cost-effective cardiac and respiratory interventions are driving segment growth.

")

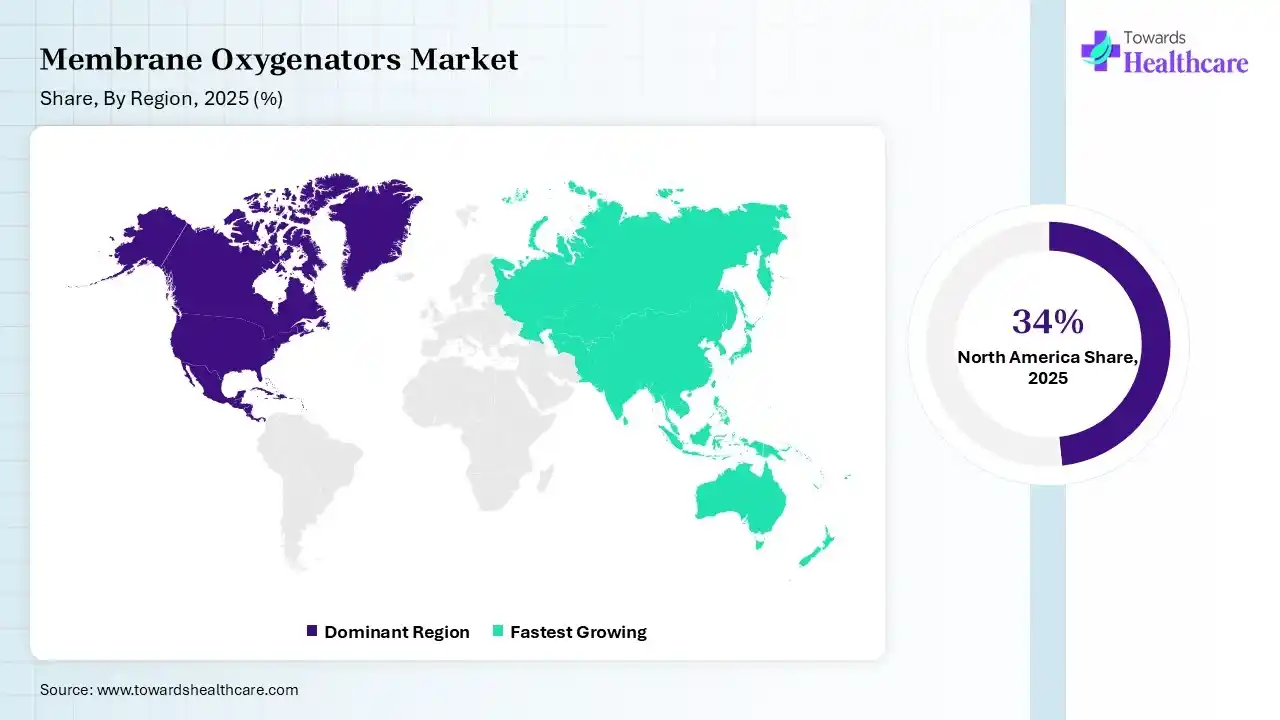

North America dominated the membrane oxygenators market with a share of 34% in 2025 due to its well-established healthcare infrastructure, high number of cardiac surgeries, and widespread use of ECMO in critical care. Strong investments in advanced medical technologies, the presence of key industry players, and increasing cases of heart and respiratory disorders further supported the region’s leading market position.

U.S. Market Trends

The U.S. membrane oxygenators market is expanding because of the increasing demand for advanced life-support systems in cardiac surgeries and intensive care. A growing burden of heart and lung disorders, strong hospital infrastructure, and continuous technological upgrades in oxygenation devices are further driving adoption and supporting steady market growth across the country.

Asia Pacific is anticipated to grow at the fastest CAGR in the membrane oxygenators market during the forecast period due to rapid healthcare infrastructure development, rising investments in critical care facilities, and increasing cases of cardiovascular and respiratory diseases. Growing awareness of advanced oxygenation therapies, expanding hospital networks, and improving access to specialized surgical care are further accelerating market growth across the region.

India Market Trends

India is expected to grow at the fastest CAGR in the membrane oxygenators market during the forecast period due to the rapid expansion of healthcare infrastructure, rising cases of cardiac and respiratory disorders, and increasing access to advanced critical care treatments. Growing investments in hospitals, improving awareness of ECMO and oxygenation technologies, and a large patient population are further accelerating market demand across the country.

R&D

Clinical Trials

Patient Support and Services

| Companies | Headquarters | Offerings |

| Medtronic | Dublin, Ireland | Provides membrane oxygenators, perfusion circuits, and extracorporeal life-support systems used in cardiac surgeries and ECMO procedures. |

| Fresenius SE & Co. KGaA | Bad Homburg, Germany | Offers advanced critical care and extracorporeal support solutions, including systems used for respiratory and cardiac failure management. |

| Getinge AB | Gothenburg, Sweden | Develops ECMO platforms, membrane oxygenators, and cardiopulmonary support devices for hospital and ICU applications. |

| TERUMO CORPORATION | Tokyo, Japan | Offers oxygenation systems for adult, pediatric, and neonatal procedures, along with perfusion and bypass solutions. |

| MicroPort Scientific Corporation | Shanghai, China | Provides cardiopulmonary support equipment and oxygenation technologies for surgical and intensive care use. |

| Nipro Medical Corporation | Osaka, Japan | Manufactures hollow fiber oxygenators and extracorporeal circulation products for critical care and cardiac procedures. |

| Kewei Medical | Dongguan, China | Focuses on membrane oxygenators and related life-support devices used in operating rooms and ICUs. |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Material

By Application

By Age Group

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar