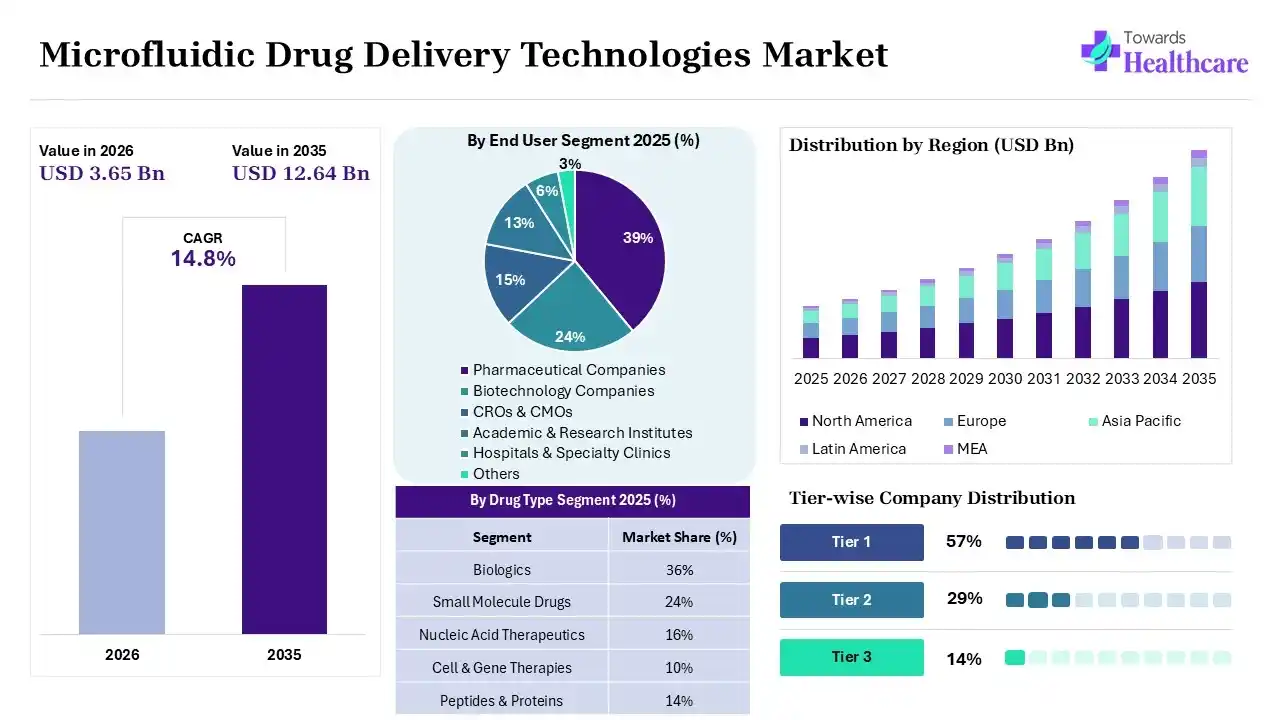

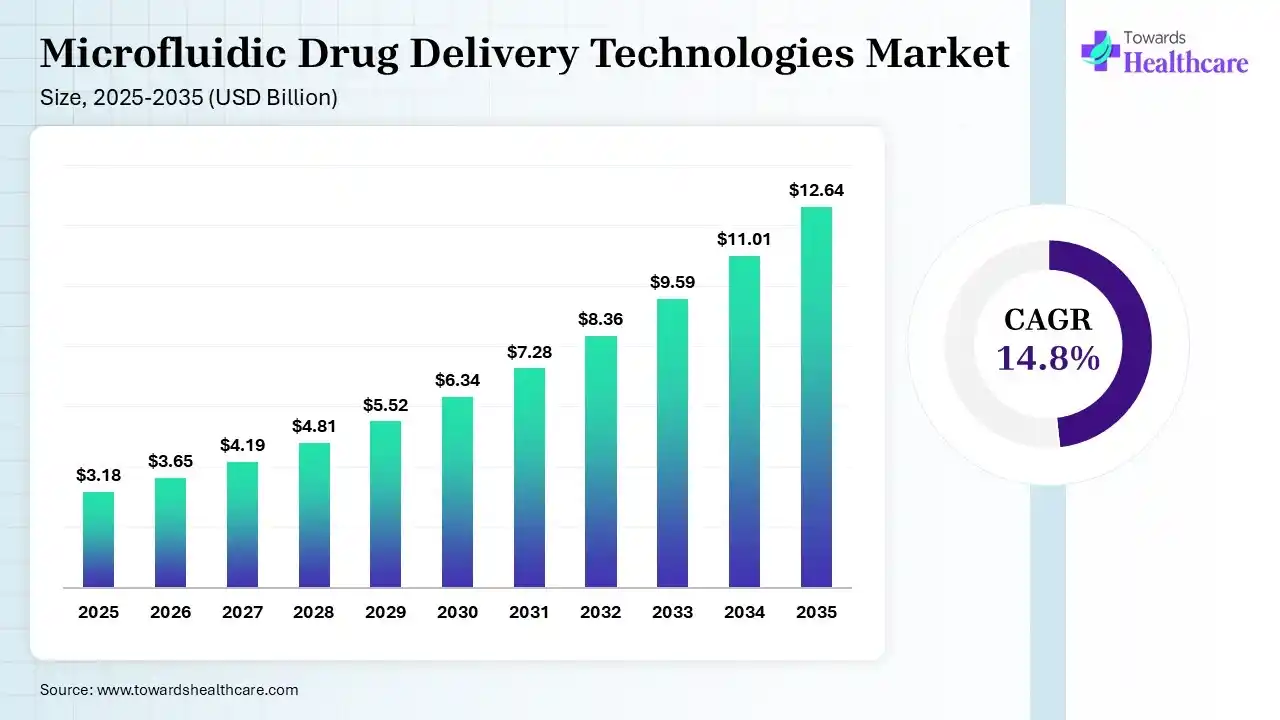

The global microfluidic drug delivery technologies market size is calculated at USD 3.18 billion in 2025, driven by increasing adoption of genomic therapeutics across clinical settings. The market continues to grow USD 3.65 billion in 2026 due to increasing personalized medicines, nanomedicines, and R&D activities. It is expected to reach USD 12.64 billion by 2035.Growth is expected at a steady CAGR of 14.8% in between 2026 to 2035 as continued expansion of manufacturing capabilities, healthcare investments, and technological advancements accelerate market expansion. North America accounted for 40% of the market in 2025 due to its robust biotechnology ecosystem, high R&D investments, and favorable regulatory pathways.

")

")

The microfluidic drug delivery technologies encompass microfluidic systems used for manipulating and controlling small volumes of fluids for drug delivery. It helps in precise mixing, formulation, and flow of fluids, maintaining enhanced accuracy and therapeutic performance.

Based on the information gathered by Payal Rabde, in order to overcome the off-target effects of conventional drug delivery, advancements in microfluidic drug delivery technologies have increased. Therefore, a shift towards the use of these devices has increased the number of innovations, which led to a rise in the development of new microfluidic devices.

Microfluidic drug delivery systems are currently used across biologics, vaccines, nanomedicine, cell therapy, and precision medicine areas. The rise in the demand for genomic therapeutics, organ-on-a-chip models, and wearable microfluid devices are also driving the market expansion.

Device manufacturers, pharmaceutical companies, CDMOs, technology providers, academic institutions, and regulators interact within the ecosystem. The rise in R&D activities, investments, technological advancements, and new collaborations is also contributing to the market ecosystem growth.

Increasing Adoption of Continuous Pharmaceutical Manufacturing

The industry's shift toward automated, continuous manufacturing enabled by microfluidic platforms are increasing the use of microfluidic drug delivery technologies. Their faster drug production, consistent quality, and lower manufacturing cost are increasing their demand.

Expansion of Lipid Nanoparticle and mRNA Manufacturing

mRNA therapeutics and nanoparticle-based drug delivery continue to accelerate market demand, increasing the adoption of microfluidic drug delivery technologies. They help in precise formulation production, with enhanced encapsulation efficiency, which encourages their use.

Growing Integration of Artificial Intelligence in Microfluidic Platforms

AI offers a wide range of applications in process optimization, predictive analytics, quality monitoring, and formulation design. Additionally, their automation and real-time monitoring applications are also promoting their integration in microfluidic platforms.

Rise of Personalized Drug Manufacturing

A growing shift towards precision medicine and patient-specific therapies are driving demand for flexible microfluidic systems. They offer flexible manufacturing, small batch production, and enhanced treatment efficiency, which accelerates their adoption.

Increasing Commercialization of Lab-on-a-Chip Technologies

Expanding commercialization trends, product launches, and broader industrial adoption of microfluidic drug delivery technologies are creating new opportunities. This, in turn, is supporting the development of automated and compact lab-on-a-chip microfluidic technologies.

Market Drivers

The major growth drivers in the microfluidic drug delivery technologies market include biologics expansion and rise in nanomedicine development. Additionally, growing shift towards automation, and increasing R&D investments are also driving the market expansion.

Market Restraints

Manufacturing complexity, regulatory uncertainty, high capital investment, and technical integration challenges act as the major restraints in the market.

Market Opportunities

Rapidly expanding market opportunities encompass rising gene therapy manufacturing, growth in the demand for personalized medicine, genomic therapeutics, growing emerging economies, and increasing AI-enabled platforms.

Market Challenges

The significant market challenges include commercialization barriers, scale-up limitations, validation issues, and supply chain constraints.

Raw Material Suppliers

Component Manufacturing

Device Integration

Pharmaceutical End Users

Global Supply Network

The global supply network of microfluidic drug delivery technologies involves sourcing, manufacturing, logistics, and distribution across global markets.

Supply Chain Risks

The supply chain risks of microfluidic drug delivery technologies highlight semiconductor shortages, specialty material low availability, geopolitical risks, and logistics disruptions.

Supply Chain Optimization Strategies

Supply chain optimization strategies of microfluidic drug delivery technologies focus on localization, supplier diversification, automation, and inventory optimization strategies.

Emerging Microfluidic Platform Technologies

Emerging microfluidic platform technologies focus on enhancing droplet, digital, acoustic, and continuous-flow technologies.

Next-Generation Manufacturing Technologies

Next-generation manufacturing technologies aim at utilizing automation, robotics, AI integration, digital twins, and smart manufacturing technologies.

Patent and Innovation Landscape

Patent and innovation landscape encompasses growing patent activity, emerging innovators, and technology commercialization trends.

Average Pricing by Product Category

Average pricing by product category focuses on pricing trends across chips, devices, consumables, software, and integrated systems.

Factors Influencing Product Pricing

Factors influencing product pricing include manufacturing complexity, material selection, customization, production scale, and regulatory compliance.

Pricing Trends Across Regions

Biopharmaceutical R&D hubs concentration, manufacturing infrastructure, and regulatory requirements drive the pricing trends across regions.

Purchasing Decision Framework

The purchasing decision framework of microfluidic drug delivery technologies focuses on key criteria influencing procurement decisions, including precision, scalability, compliance, automation, cost, and service support.

Buyer Segmentation

Buyer segmentation of microfluidic drug delivery technologies is driven by purchasing behavior among pharmaceutical companies, biotechnology firms, CROs, and research institutes.

Procurement Challenges

Procurement challenges for microfluidic drug delivery technologies encompass budget constraints, supplier evaluation, validation requirements, and technology adoption barriers.

Demand by Therapeutic Area

Demand for microfluidic drug delivery technologies by therapeutic area is driven by expanding oncology, vaccines, rare diseases, gene therapy, and biologics applications.

Demand by Manufacturing Scale

Demand for microfluidic drug delivery technologies by manufacturing scale depends on research-scale, pilot-scale, and commercial-scale demand.

Future Demand Outlook

Future demand outlook of microfluidic drug delivery technologies is expected to be driven by rising RNA-based therapeutics, gene therapies, personalized medicines, expanding applications, increasing investments, and technological advancements.

Venture Capital and Private Equity Investments

Venture capital and private equity investments include recent funding, startup investments, and technology commercialization.

Government Funding and Research Grants

Government funding and research grants encompass public investment supporting growing innovations and commercialization.

Mergers, Acquisitions, and Strategic Partnerships

Mergers, acquisitions, and strategic partnerships are driven by a rise in consolidation activities, licensing agreements, and technology collaborations.

Global Regulatory Environment

The global regulatory environment for microfluidic drug delivery technologies encompasses FDA, EMA, PMDA, NMPA, and other regulatory frameworks affecting commercialization.

Manufacturing Standards

The manufacturing standards of microfluidic drug delivery technologies depend on GMP, ISO standards, quality systems, and validation requirements.

Regulatory Challenges

Approval complexity and evolving compliance expectations are the major regulatory challenges for microfluidic drug delivery technologies.

| Table | Scope |

| Market Size in 2026 | USD 3.65 Billion |

| Projected Market Size in 2035 | USD 12.64 Billion |

| CAGR (2026 - 2035) | 14.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Technology, By Product, By Material, By Drug Type, By Application, By Route of Administration, By End User, By Region |

| Top Key Players | Danaher Corporation, Evonik Industries AG, IDEX Corporation, Fluigent, Enable Injections |

")

| Segment | Share 2025 (%) |

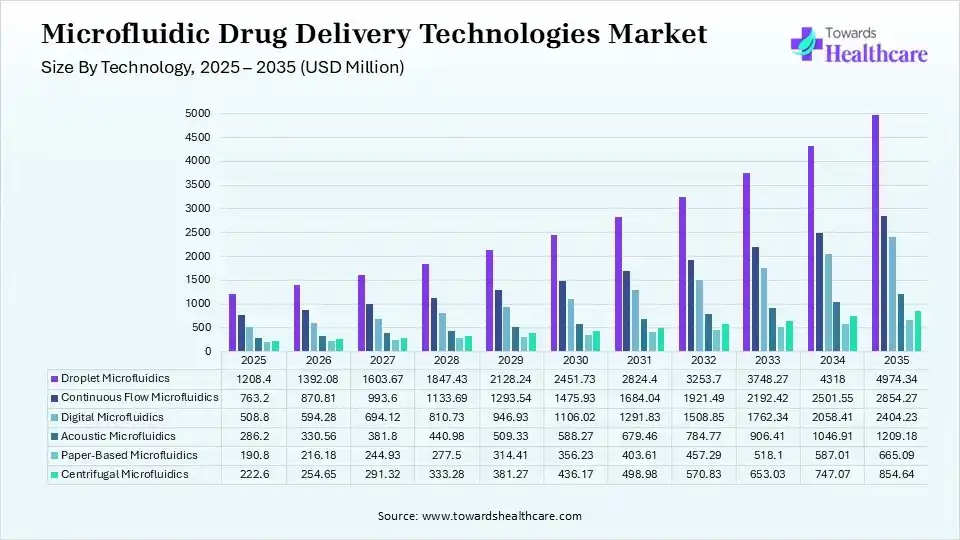

| Droplet Microfluidics | 38% |

| Continuous Flow Microfluidics | 24% |

| Digital Microfluidics | 16% |

| Acoustic Microfluidics | 9% |

| Paper-Based Microfluidics | 6% |

| Centrifugal Microfluidics | 7% |

The Droplet Microfluidics Segment Dominated the Market With 38% in 2025

The droplet microfluidics segment led the microfluidic drug delivery technologies market with a 38% share in 2025, reaching US$ 1392.08 million in 2026 and US$ 4974.34 million by 2035 at a CAGR of 15.2%. Driven by the ability to develop highly uniform particles. They also supported scalable nanoparticle manufacturing. They improved encapsulation efficiency for biologics, which increased their demand.

The digital microfluidics segment held the second-largest share of 16% of the market in 2025 and is expected to witness the fastest growth during the forecast period, due to advances in automation and programmable assays. Based on the information gathered by Payal Rabde, they also help in reducing reagent consumption, which increases their demand. They also expand personalized drug delivery applications.

")

| Segment | Share 2025 (%) |

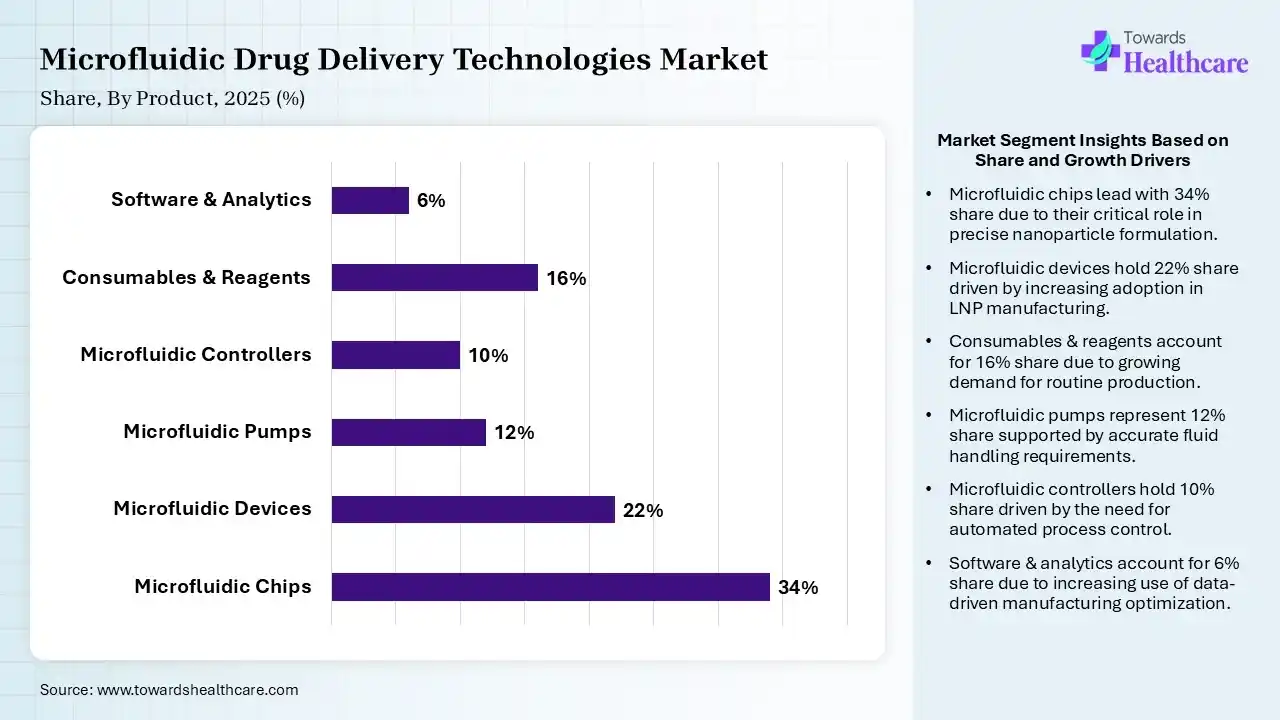

| Microfluidic Chips | 34% |

| Microfluidic Devices | 22% |

| Microfluidic Pumps | 12% |

| Microfluidic Controllers | 10% |

| Consumables & Reagents | 16% |

| Software & Analytics | 6% |

The Microfluidic Chips Segment Dominated the Market With 34% in 2025

The microfluidic chips segment accounted for the highest revenue share of 34% of the microfluidic drug delivery technologies market in 2025, due to increased chip integration, which improved precision manufacturing. It also supported high-throughput drug formulation, which increased their use. They also enabled miniaturized workflows.

The microfluidic controllers segment held the second-largest share of 10% of the market in 2025 and is expected to show the highest growth during the forecast period, as it accelerates digital automation. They also improve system monitoring, which drives their demand. They also enable smart manufacturing platforms.

")

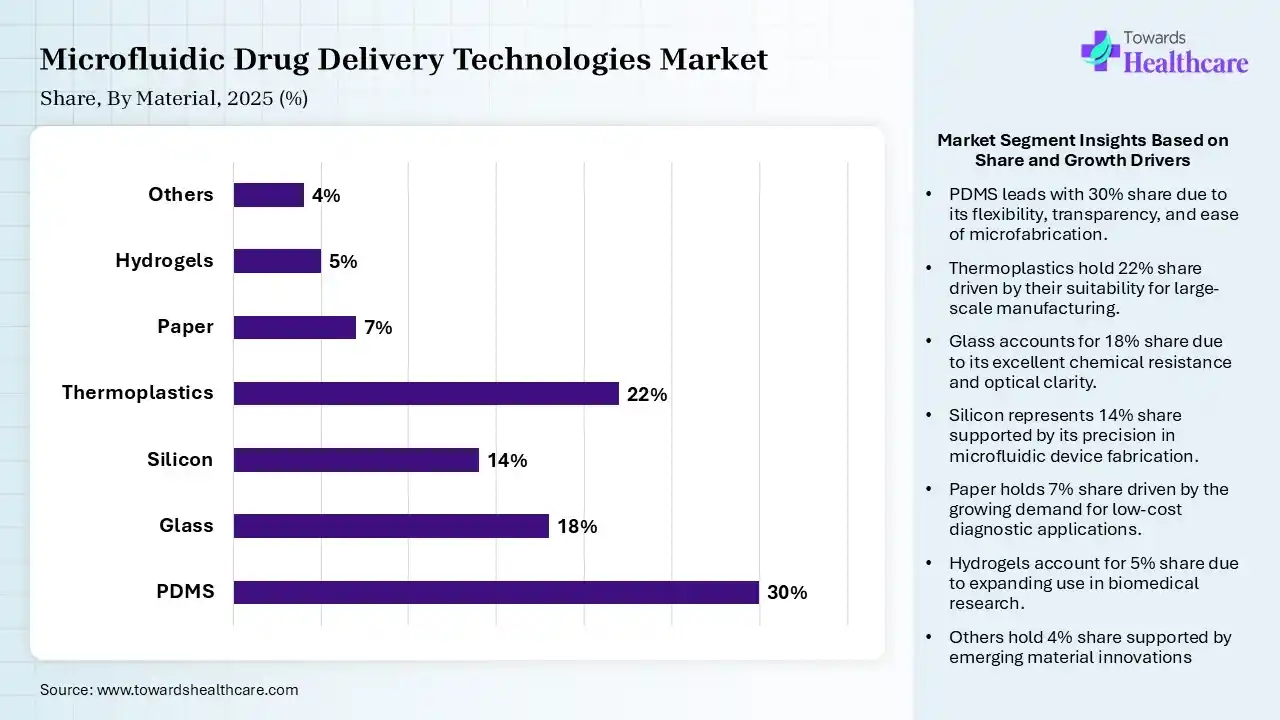

| Segment | Share 2025 (%) |

| PDMS | 30% |

| Glass | 18% |

| Silicon | 14% |

| Thermoplastics | 22% |

| Paper | 7% |

| Hydrogels | 5% |

| Others | 4% |

The PDMS Segment Dominated the Market With 30% in 2025

The PDMS segment held a major revenue share of 30% of the microfluidic drug delivery technologies market in 2025, driven by its flexibility and easy fabrication. It also supported rapid prototyping, which increased its demand. Additionally, they were widely used in research laboratories.

The thermoplastics segment held the second-largest share of 22% of the market in 2025 and is expected to expand rapidly during the forecast period, as it enables cost-effective mass production. It also supports disposable devices, which increases their adoption rates. It also improves commercialization potential.

")

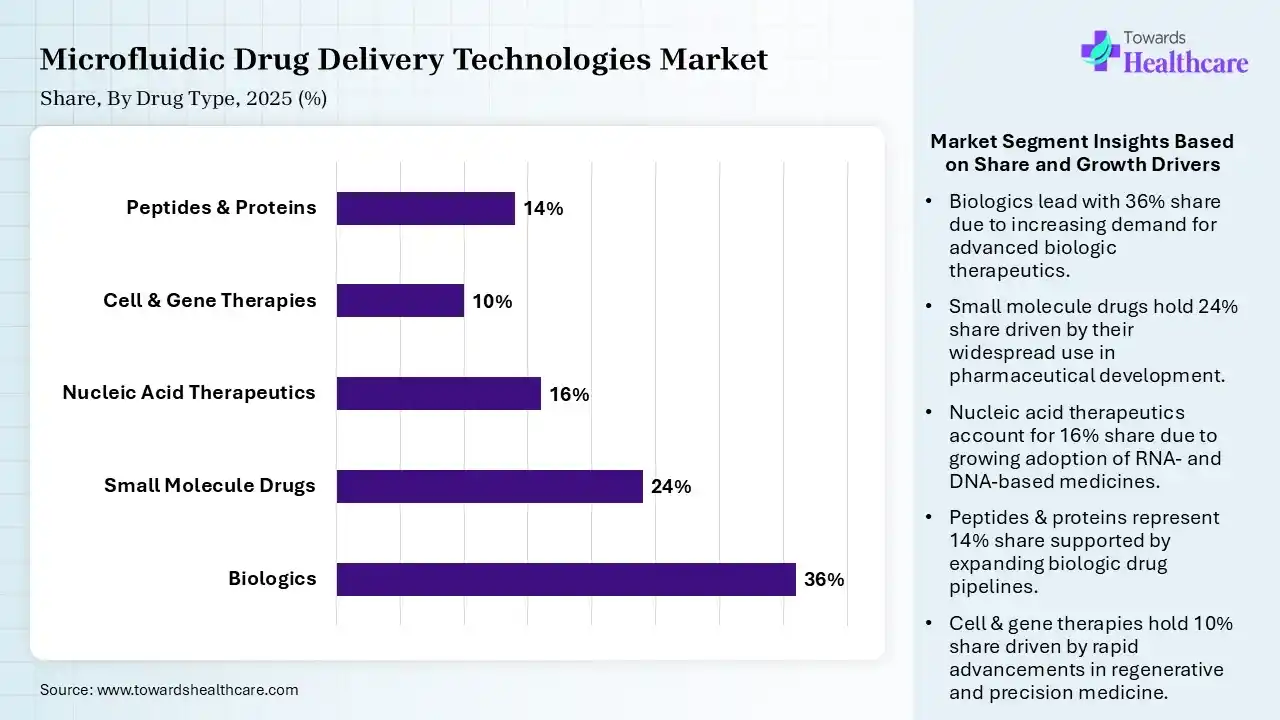

| Segment | Share 2025 (%) |

| Biologics | 36% |

| Small Molecule Drugs | 24% |

| Nucleic Acid Therapeutics | 16% |

| Cell & Gene Therapies | 10% |

| Peptides & Proteins | 14% |

The Biologics Segment Dominated the Market With 36% in 2025

The biologics segment contributed the biggest revenue share of 36% of the microfluidic drug delivery technologies market in 2025, driven by growth in biologic approvals, which increased their demand. They also required precise formulation, which increased the demand for microfluidic drug delivery technologies. Benefits from controlled encapsulation also increased their use.

The nucleic acid therapeutics segment held the second-largest share of 16% of the market in 2025 and is expected to gain the highest share during the forecast period, due to rising mRNA and gene-editing therapies, which accelerate the demand for microfluidic drug delivery technologies. It also improves nucleic acid stability and enables targeted delivery. Additionally, growth in start-up financing in Q4 2025 was reported to be worth $557.1 million, which demonstrated a rise of 27% in volume and a 141% increase in value compared with the previous quarter, creating new opportunities.

")

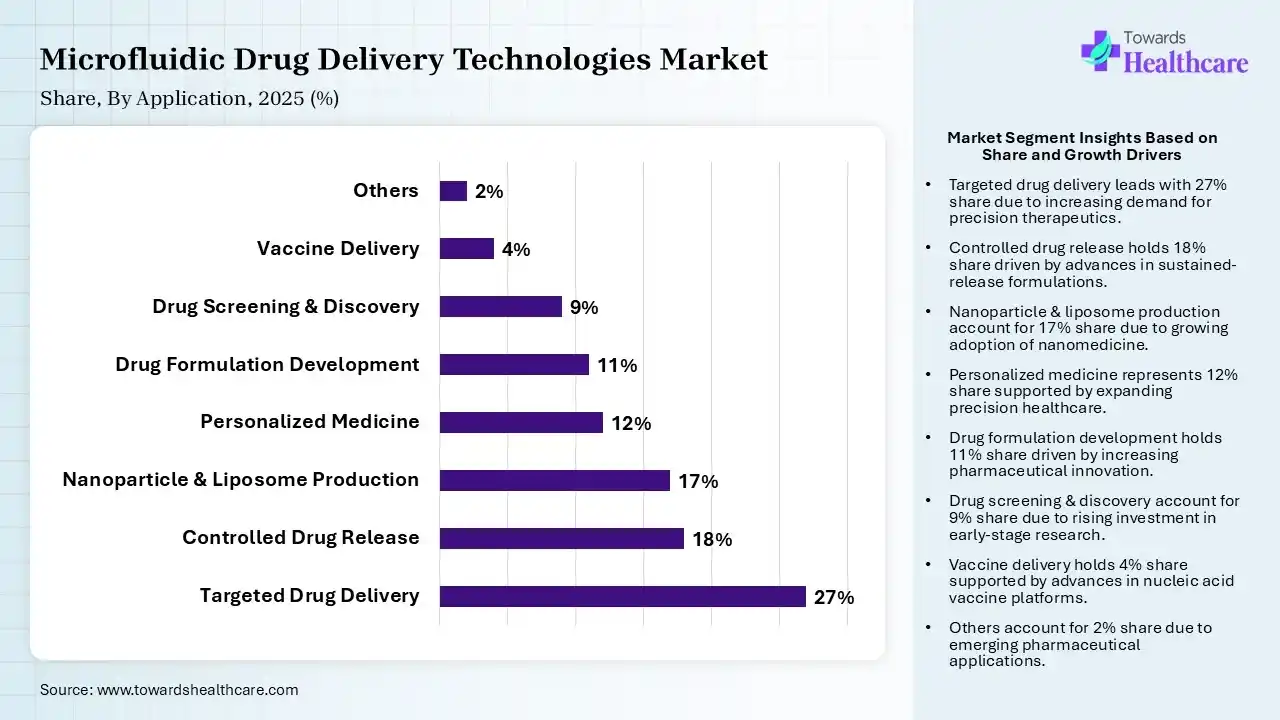

| Segment | Share 2025 (%) |

| Targeted Drug Delivery | 27% |

| Controlled Drug Release | 18% |

| Nanoparticle & Liposome Production | 17% |

| Personalized Medicine | 12% |

| Drug Formulation Development | 11% |

| Drug Screening & Discovery | 9% |

| Vaccine Delivery | 4% |

| Others | 2% |

The Targeted Drug Delivery Segment Dominated the Market With 27% in 2025

The targeted drug delivery segment held the largest revenue share of 27% of the microfluidic drug delivery technologies market in 2025, driven by improved treatment specificity. They also reduced systemic toxicity, which increased the use of microfluidic drug delivery technologies. They also supported precision medicine development.

The nanoparticle & liposome production segment held the second-largest share of 17% of the market in 2025 and is expected to grow with the fastest CAGR during the forecast period, due to expanding nanomedicine, which increases the demand for microfluidic drug delivery technologies. Based on the Payal Rabde survey, it helps in improving particle uniformity. It also supports mRNA therapeutics.

")

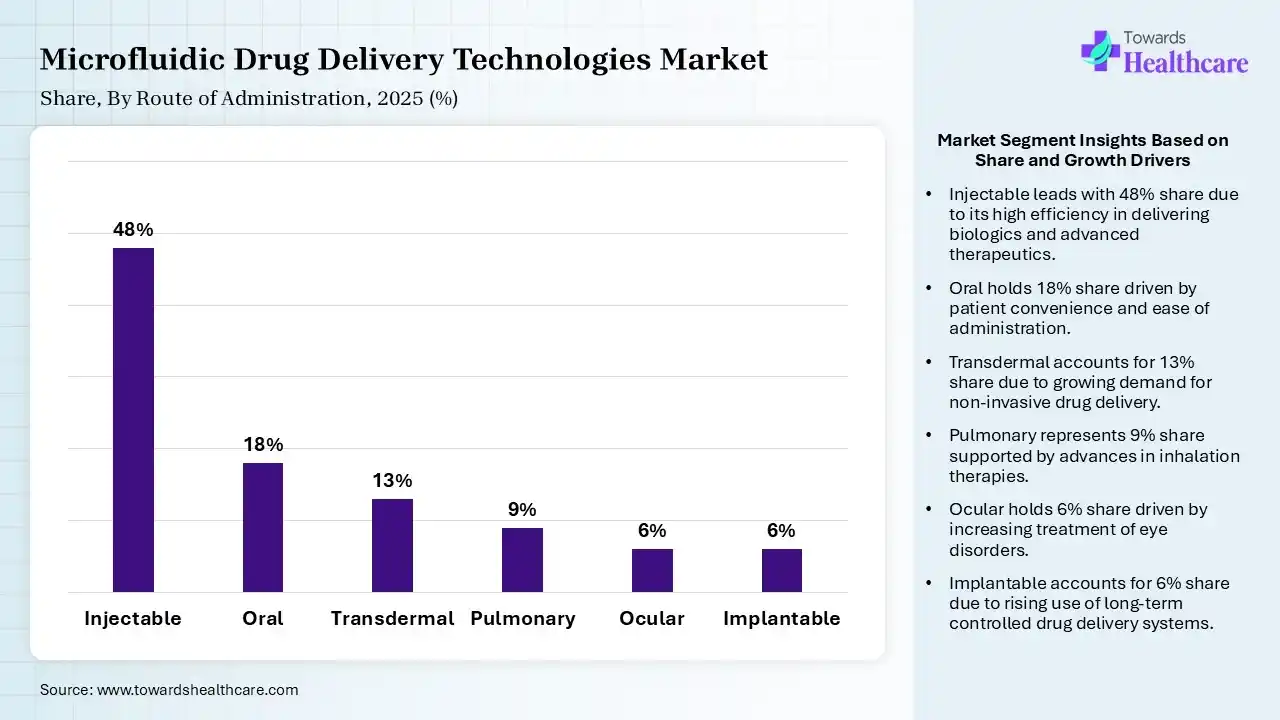

| Segment | Share 2025 (%) |

| Injectable | 48% |

| Oral | 18% |

| Transdermal | 13% |

| Pulmonary | 9% |

| Ocular | 6% |

| Implantable | 6% |

The Injectable Segment Dominated the Market With 48% in 2025

The injectable segment accounted for the highest revenue share of 48% of the microfluidic drug delivery technologies market in 2025, as it delivered biologics efficiently. It also enabled precise dosing, which increased its demand. Furthermore, they were also preferred for advanced therapeutics.

The transdermal segment held the second-largest share of 13% of the market in 2025 and is expected to show the highest growth during the forecast period, due to increasing adoption of minimally invasive therapies. They also improve patient adherence, which promotes their adoption. Enables sustained delivery, which is driving their demand.

")

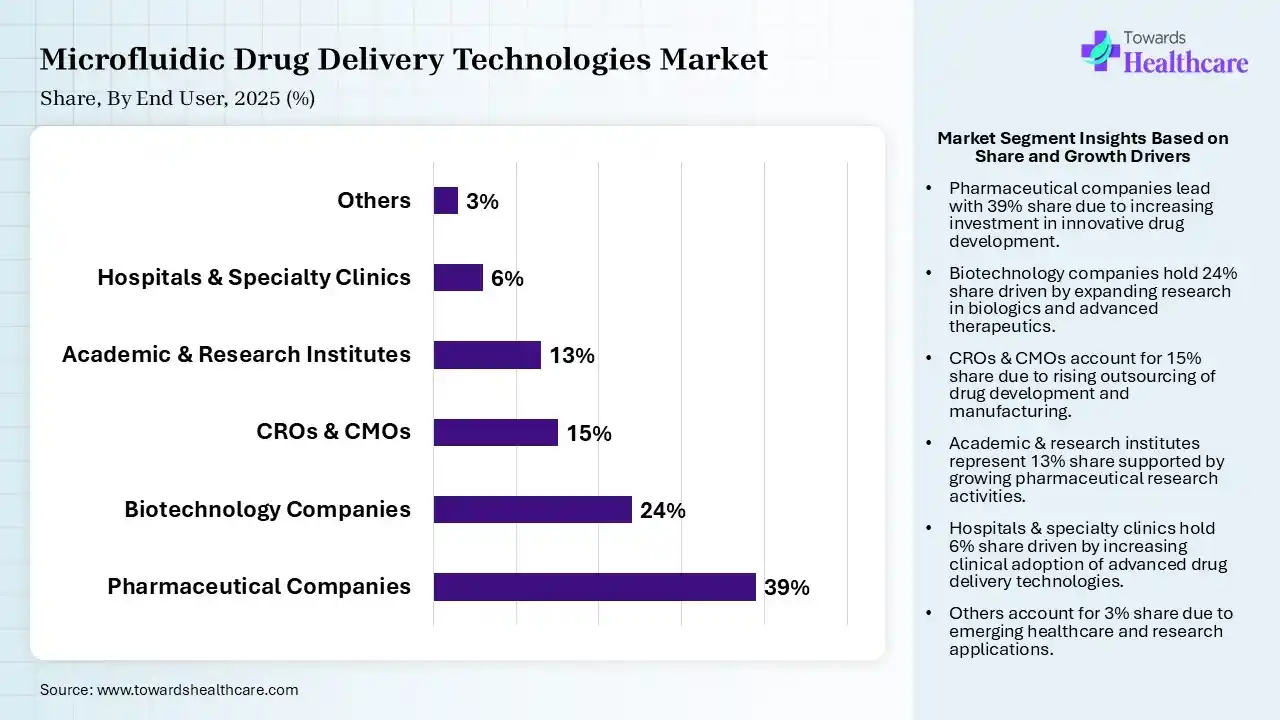

| Segment | Share 2025 (%) |

| Pharmaceutical Companies | 39% |

| Biotechnology Companies | 24% |

| CROs & CMOs | 15% |

| Academic & Research Institutes | 13% |

| Hospitals & Specialty Clinics | 6% |

| Others | 3% |

The Pharmaceutical Companies Segment Dominated the Market With 39% in 2025

The pharmaceutical companies segment held a major revenue share of 39% of the microfluidic drug delivery technologies market in 2025, driven by increased investment in advanced drug manufacturing. Microfluidic drug delivery technologies also improved formulation efficiency, which increased their use. They also helped accelerate commercialization.

The biotechnology companies segment held the second-largest share of 24% of the market in 2025 and is expected to expand rapidly during the forecast period, due to expanding biologics and gene therapy pipelines. Increasing R&D spending is also driving the adoption of microfluidic drug delivery technologies. Their rapid expansion is also driving the adoption of innovative microfluidic technologies.

")

")

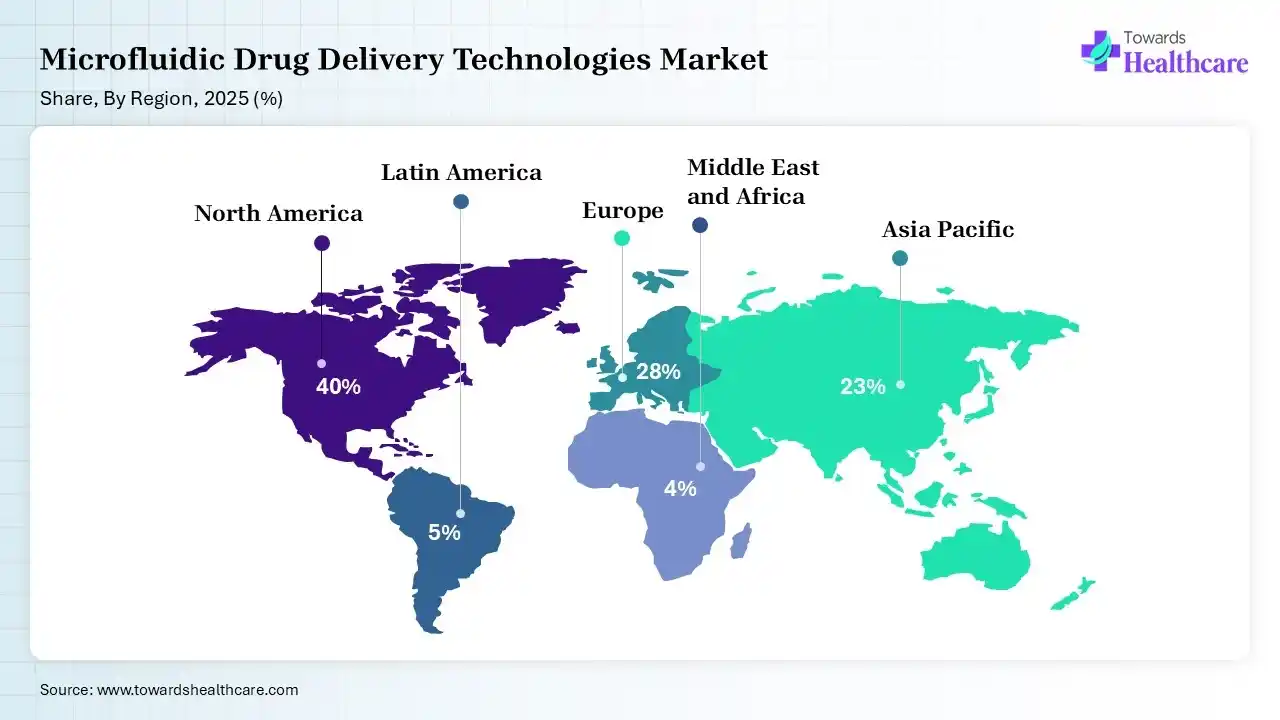

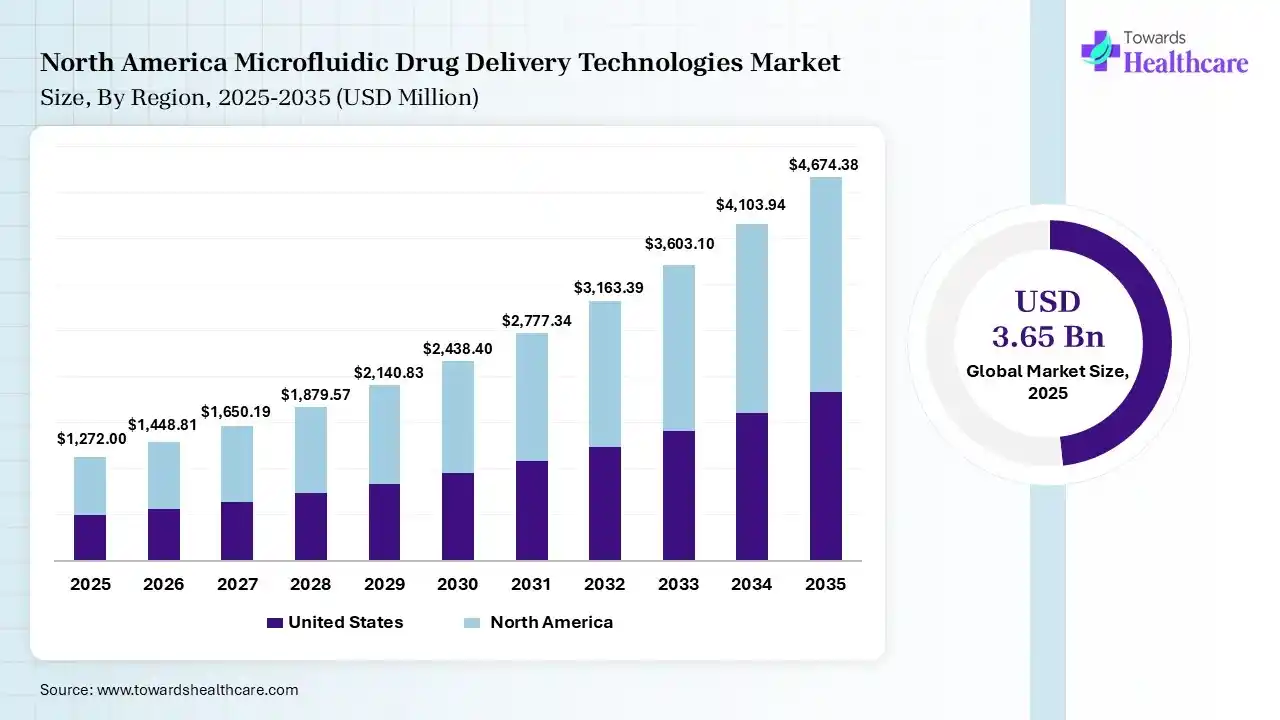

North America dominated the microfluidic drug delivery technologies market with 40% in 2025, due to the presence of a strong biotechnology ecosystem, which increased commercialization. High R&D investments also supported innovation, while favorable regulatory pathways also accelerated the microfluidic drug delivery technologies adoption. Growth in the development of advanced nanomedicine technologies and personalized medicines also increased their use. Rise in the use of AI integration and growth in clinical trials also contributed to the market growth.

US Market Growth

U.S. held a 31% share of the microfluidic drug delivery technologies market in 2025 and is expected to grow with the highest CAGR of 14% during the studied years, driven by advanced drug development. The study led by Payal Rabde also highlighted expanding biologics manufacturing as a market growth factor, where growth in their approval rates also increased the use of microfluidic drug delivery technologies. Growth in support from strong venture funding also increased their adoption rates, where a rise in research programs also encouraged their use. The presence of robust companies like Agilent Technologies Inc. also contributed to the market expansion, where its second quarter of 2026 reported a growth of 10% (reported revenue $1.83 billion) when compared with the second quarter of 2025.

Canada Market Growth

Canada held a 6% share in the market in 2025 due to strengthening translational research. Expanding life science investments and growing academic collaborations are also driving the demand for microfluidic drug delivery technologies. Growing biotechnology and pharmaceutical companies are also driving the adoption of these technologies, where increasing demand for personalized therapeutics and nucleic acid therapeutics is also driving their use. A rise in government support and emerging startups are also increasing their utilization.

Europe held a 28% share of the microfluidic drug delivery technologies market and is expected to grow significantly during the forecast period, due to the presence of strong pharmaceutical manufacturing facilities, which support market growth. Growing government funding also promotes innovation, where expanding precision medicine initiatives are also driving the adoption of microfluidic drug delivery technologies. Additionally, based on the survey conducted, a rise in R&D activities focused on genomic therapeutics and lipid nanoparticles are also increasing their demand, where growing collaborations are also increasing access to these technologies, driving market expansion.

Germany Market Growth

Germany held an 8% share in the microfluidic drug delivery technologies market in 2025, driven by growth in biomedical engineering. Expansion of pharmaceutical R&D activities and growth in the adoption of automation technologies also promoted microfluidic drug delivery technologies advancements. The presence of robust industries and initiatives also increased their use, where growth in investments and funding supported their adoption rates. A rise in the use of genomic therapeutics and biologics also increased their demand, where expansion of manufacturing facilities also increased their adoption rates. New collaborations and technological advancements also promoted their expansion.

UK Market Growth

UK held a 6% share in the market in 2025 and is expected to witness the fastest growth over the forecast period, due to growing biotech innovations. Expansion of precision therapeutics, where growing academic partnerships are also increasing the use of microfluidic drug delivery technologies. High investments and the presence of advanced industries are also driving their adoption rates, where well-established institutes are also increasing their use. Growth in collaboration and a rise in the demand for wearable technologies and organ-on-chip products are also increasing their adoption rates.

Asia Pacific held a 23% share of the microfluidic drug delivery technologies market in 2025 and is expected to grow at the fastest CAGR of 17.1% during the forecast period, due to rapid pharmaceutical expansion accelerating adoption. Growing biotech investments are also supporting innovations, where increasing healthcare spending also boosts microfluidic drug delivery technologies demand. The analysis by Payal Rabde states that the growth in drug delivery and biologics research are also increasing the use of microfluidic drug delivery technologies, where expansion of genomic therapeutics is also driving their demand. New collaborations and growing healthcare expenditure are also increasing their use, enhancing the market growth.

China Market Growth

China held a 9% share of the microfluidic drug delivery technologies market in 2025, driven by expansion of biologics manufacturing. Growth in domestic innovations and increased government funding also encouraged the adoption of microfluidic drug delivery technologies. Growth in nano-medicine and precision medicine demand also increased their use, while a rise in AI integration also fueled their demand. The presence of a large population also increased their use in the development of new solutions, where technological advancements also promoted a rise in the development of wearable devices.

India Market Growth

India held a 3% share in the market in 2025 and is expected to expand rapidly in the coming years, due to expanding pharmaceutical production. Increasing biotech startups and growing contract manufacturing ecosystems are also driving the demand for microfluidic drug delivery technologies. Expanding R&D activities focused on biologics, personalized medicines, and RNA therapeutics are also driving their demand, where new strategic partnerships are also expanding their availability. Rapid healthcare digitalization and growing government initiatives are also creating new opportunities.

Latin America held a 5% share in the microfluidic drug delivery technologies market in 2025 and is expected to show lucrative growth during the forecast period, due to expanding pharmaceutical manufacturing, which supports adoption. Increasing research investments also improve innovations, where healthcare modernization also boosts the demand for microfluidic drug delivery technologies. A rise in the demand for biologics, genomic therapeutics, and vaccines are also increasing their use, where growing health awareness are also driving the demand for personalized medicines, encouraging the use of these technologies, ultimately fueling the market growth.

Brazil Market Growth

Brazil held a 2% share in the microfluidic drug delivery technologies market in 2025 and is expected to gain the highest market share during the forecast period, driven by high regional pharmaceutical production. Expansion of biotechnology research also increased the demand for microfluidic drug delivery technologies, where strong clinical development also promoted their use. Growth in R&D activities and government support also increased their adoption rates, where new partnerships also increased their use. A rise in the adoption of digital technologies also increased the development of new organ-on-chip platforms.

The rest of Latin America held a 2% share in the market in 2025, due to expansion of healthcare infrastructure. Increasing drug manufacturing capabilities are also increasing the use of microfluidic drug delivery technologies, and expanding regional partnerships are also increasing their use. Growing vaccination programs and government support are also increasing their adoption, while a rise in R&D activities is also driving their use. Increasing interest in automation, wearable devices, and genomic therapeutics is also promoting their use and advancements.

MEA held a 4% share in the microfluidic drug delivery technologies market in 2025 and is expected to show notable growth during the forecast period, due to rising healthcare investments accelerating market growth. Governments diversify life science sectors, which fuels the use of microfluidic drug delivery technologies, where expanding biotech capabilities also drive their adoption. A rise in the chronic disease burden and government initiatives are also increasing the development of new therapeutics, which is increasing the demand for these technologies. Healthcare digitalization is also driving the adoption of advanced technologies, promoting their advancements.

Saudi Arabia Market Growth

Saudi Arabia held a 1.50% share in the microfluidic drug delivery technologies market in 2025 and is expected to show the fastest growth over the forecast period, driven by growth in investments in biotechnology. Expansion of pharmaceutical localization also increased the availability of microfluidic drug delivery technologies, where growth in healthcare transformation also increased their advancements. The rise in vision-driven initiatives also increased their use, where the rise in demand for personalized medicines and biologics also increased their demand. Expanding initiatives and emerging startups also increased R&D activities.

UAE Market Growth

United Arab Emirates (UAE) held a 1% share in the market in 2025, due to growing innovation hubs. The presence of well-established industries are also attracting global life science companies, expanding the use of microfluidic drug delivery technologies, where a growing R&D ecosystem is also driving the use of these technologies. Rise in the use of biologics, genomic therapeutics, and vaccines are also increasing their use, while growing technological advancements are also promoting the development of organ-on-chip and wearable technologies. Expansion collaborations are also driving the integration of advanced technologies with microfluidic drug delivery technologies, driving their advancements.

| Companies | Headquarters | Solutions |

| Danaher Corporation | Marlborough, U.S. | NanoAssemblr Ignite, NanoAssemblr Commercial Formulation System, and NanoAssemblr Blaze |

| Evonik Industries AG | Essen, Germany | LIPEX Flow |

| IDEX Corporation | Northbrook, U.S. | Microfluidizer M110P Procssors |

| Fluigent | Paris, France | Aria Automated Perfusion Loop |

| Enable Injections | Cincinnati, U.S. | enFuse On-Body Delivery System |

In July 2026, after the successful acquisition of Helvoet Polymer Technologies, Richard D. Phillips, Chief Executive Officer of Kimball Electronics, announced, “Helvoet is exactly the type of acquisition we’ve been building toward, a highly specialized medical CDMO with comprehensive capabilities in microfluidics, diagnostics, and drug delivery, serving blue-chip customers in the fastest-growing segments of healthcare. The acquisition is central to our strategy of establishing Kimball as a true global medical CMO platform with a strengthened presence in Europe, access to the India market, and a clear path for accelerating growth in the U.S. by leveraging our new manufacturing facility in Indianapolis.”

Market Structure and Competitive Intensity

The microfluidic drug delivery technologies market structure and competitive intensity depend on the expanding market concentration, competition levels, entry barriers, and competitive dynamics globally.

Strategic Positioning of Leading Companies

Danaher Corporation, IDEX Corporation, and Evonik Industries AG dominated the market based on innovation, technology portfolio, geographic presence, partnerships, manufacturing capabilities, and commercialization.

Competitive Benchmarking Matrix

Danaher Corporation, IDEX Corporation, and Evonik Industries AG were noted as the leading players across product portfolio, technology leadership, R&D intensity, regional presence, manufacturing scale, and strategic initiatives.

Recent Strategic Developments

Danaher Corporation, Evonik Industries AG, and IDEX Corporation were the market leaders in acquisitions, collaborations, product launches, facility expansions, and funding activities.

| Company Overview | Develops, manufactures, and supports the most advanced fluid control systems available for microfluidics |

| Product Portfolio | Microfluidic OEM and technologies |

| Recent Developments | Collaboration with RAN Biotechnologies to support the development of advanced droplet microfluidics solutions, with the integration of 008-FluoroSurfactant into the Fluigent catalog |

| SWOT Analysis |

Strengths: Offers microfluid control systems with high precision and automation. Ease of use drives their adoption across institutes. Weakness: Limited microfluid research activities Opportunities: Expanding organ-on-chip innovations. Rising gene therapy advancements. Threats: Limited funding support |

| Company Overview | Focus on human biology and technologies |

| Product Portfolio | AVA Emlaton Systems, Zoe-CM Culture Module, Chip-S1 Stretchable Chip, Chip-R1 Rigid Chip, Chip-A1 Accessible Chip, Chip Array |

| Recent Developments | Partnership with FUJIFILM Cellular Dynamics, Inc. to launch the Emulate Brain-Chip R1 |

| SWOT Analysis |

Strengths:

Weakness: High implementation costs Opportunities:

Threats: Competition from alternative in vitro technologies |

| Company Overview | Develops flexible platforms for single-cell interactions and functional dynamics |

| Product Portfolio | Droplet generation & loading, Droplet acquisition & filtering, Droplet arraying, Sample merging, Sample assaying, Sample dispensing, Envisia Platform |

| Recent Developments | Completion of a £38M (c. $49 million) Series B funding round to advance single-cell functional analysis with a flexible droplet-based platform that can load, select, process, analyze, and recover tens of thousands to hundreds of thousands of individual cells at the same time. |

| SWOT Analysis |

Strengths:

Weakness: Dependence on trained personnel Opportunities:

Threats: Rapid technological advancements |

High-Growth Revenue Opportunities

The high-growth revenue opportunities of the microfluidic drug delivery technologies market are expected to be driven by the adoption of most attractive technologies, expanding applications, growing customer groups, and expanding regional markets for future investment.

White Space Analysis

The white space analysis of the microfluidic drug delivery technologies market focuses on underserved markets, unmet customer needs, and emerging commercialization opportunities, leading to market expansion.

Investment Priority Matrix

Investment priority matrix of the microfluidic drug delivery technologies market focuses on investment opportunities based on market attractiveness, growth potential, competitive intensity, and profitability.

Market Outlook Through 2035

The microfluidic drug delivery technologies market is expected to grow significantly during the predicted time depending on technology evolution, commercial adoption, and expected market transformation.

Emerging Business Models

Manufacturing-as-a-service, integrated digital platforms, AI-enabled formulation development, and collaborative innovation ecosystems are anticipated to drive the market business models.

Long-Term Strategic Recommendations

Th strategic recommendations are aimed at manufacturers, investors, technology developers, pharmaceutical companies, and policymakers to capitalize on future market opportunities.

As per Payal Rabde's analysis, the microfluidic drug delivery technologies market is expanding rapidly based on various factors, creating new opportunities. The growing demand for personalized medicines, genomic therapeutics, expanding manufacturing capabilities, and technological advancements are driving advancements in microfluid drug delivery technologies. The rapid healthcare expansion and digitalization are also driving the integration of AI and other adopted technologies to enhance their applications. Segments such as digital microfluidics, nucleic acid therapeutics, nanoparticle & liposome production, and injectable are anticipated to show rapid growth, making them suitable for investments. Furthermore, Danaher Corporation, IDEX Corporation, and Fluigent demonstrate strong market presence, attracting new investments.

By Technology

By Product

By Material

By Drug Type

By Application

By Route of Administration

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar