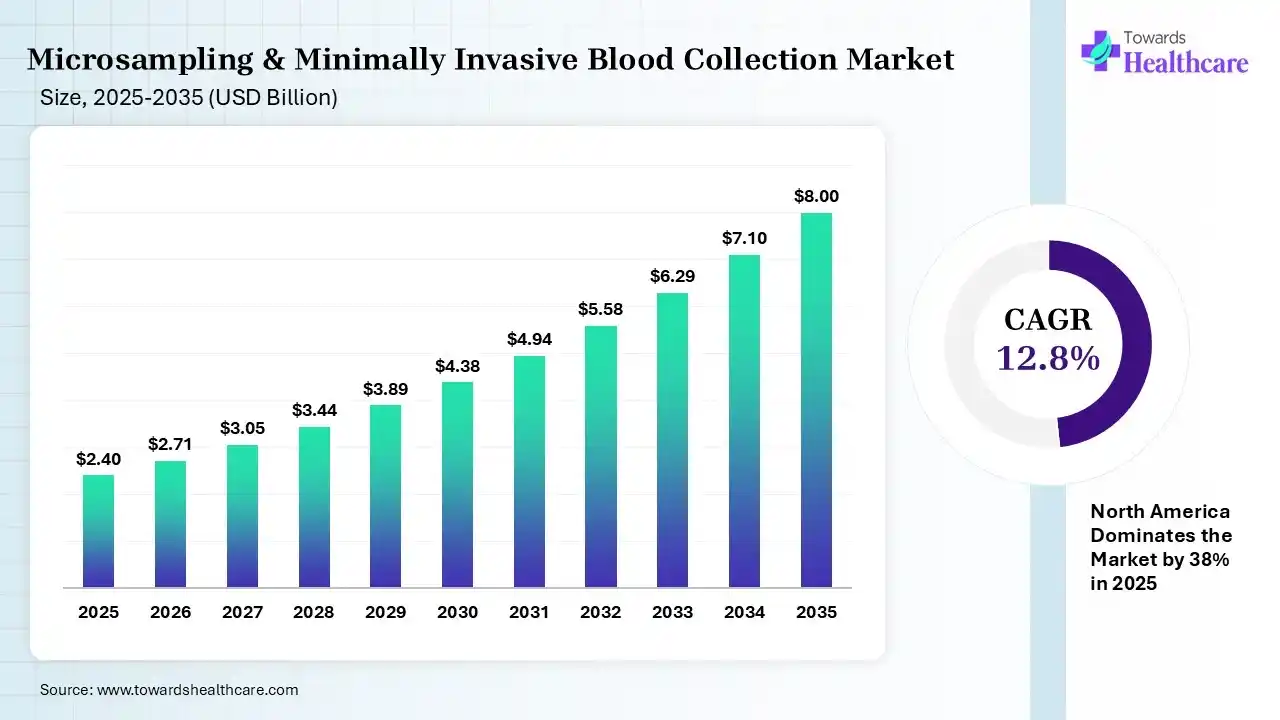

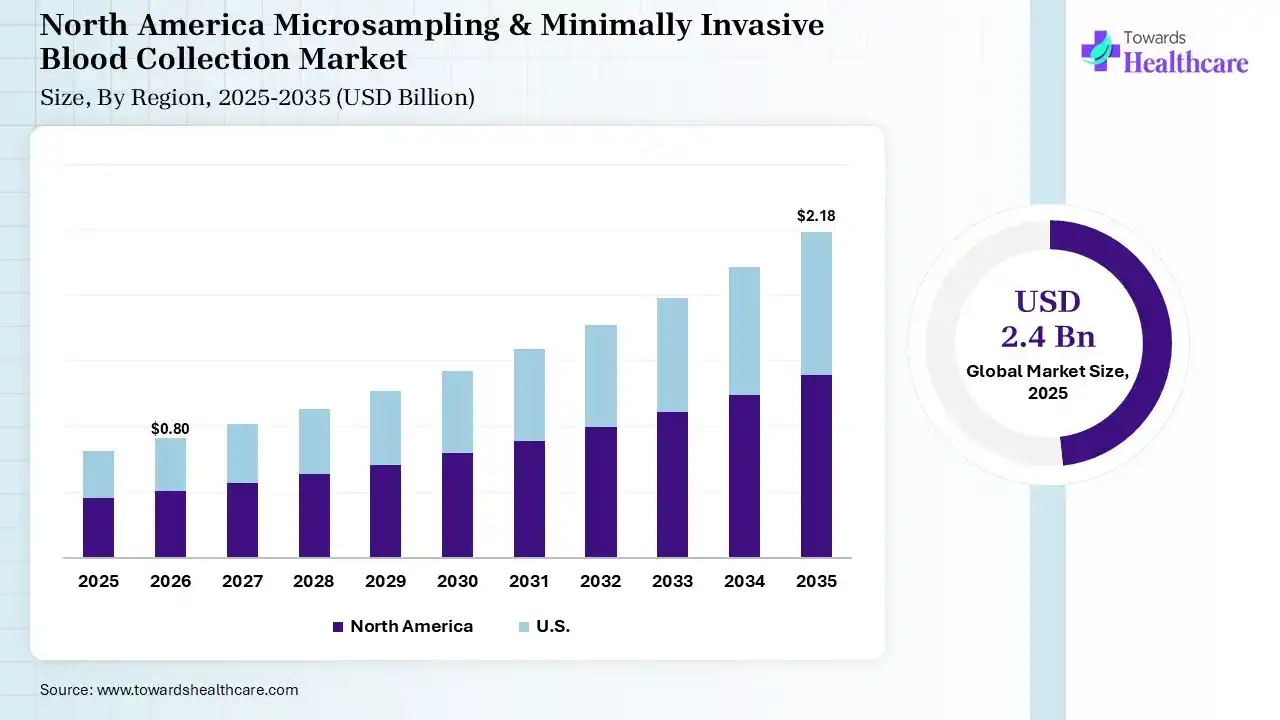

The global microsampling & minimally invasive blood collection market size was estimated at USD 2.4 billion in 2025 and is predicted to increase from USD 2.71 billion in 2026 to approximately USD 8 billion by 2035, expanding at a CAGR of 12.8% from 2026 to 2035. The market is growing steadily due to rising demand for patient-friendly diagnostic and home-based sample collection. Increasing use in clinical research, chronic disease monitoring, and advanced low-volume collection technologies is driving continued market expansion.

")

Microsampling & minimally invasive blood collection is the process of obtaining small blood volumes using low-pain, patient-friendly techniques such as finger-prick or microneedle methods. The microsampling & minimally invasive blood collection market is growing due to increasing demand for convenient, low-pain diagnostic methods and home-based testing solutions. Rising prevalence of chronic diseases, expanding use in remote patient monitoring, and growing adoption in decentralized clinical trials are further driving market growth, supported by continuous innovation in low-volume and easy-to-use blood collection technologies.

AI can significantly impact the market by improving sample analysis accuracy, enabling faster diagnostic insights, and supporting predictive disease monitoring. It also enhances device design through smart sensors, automates data interpretation, and strengthens remote patient monitoring systems. These advancements improve efficiency, patient convenience, and clinical decision-making, thereby accelerating market adoption across diagnostics and decentralized healthcare settings.

| Table | Scope |

| Market Size in 2026 | USD 2.71 Billion |

| Projected Market Size in 2035 | USD 8 Billion |

| CAGR (2026 - 2035) | 12.8% |

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Technique, By Application, By End User, By Distribution Channel, By Region |

| Top Key Players | BD, Abbott Laboratories, F. Hoffmann-La Roche Ltd, Terumo Corporation, PerkinElmer, Inc, Neoteryx |

| Segment | Share 2025 (%) |

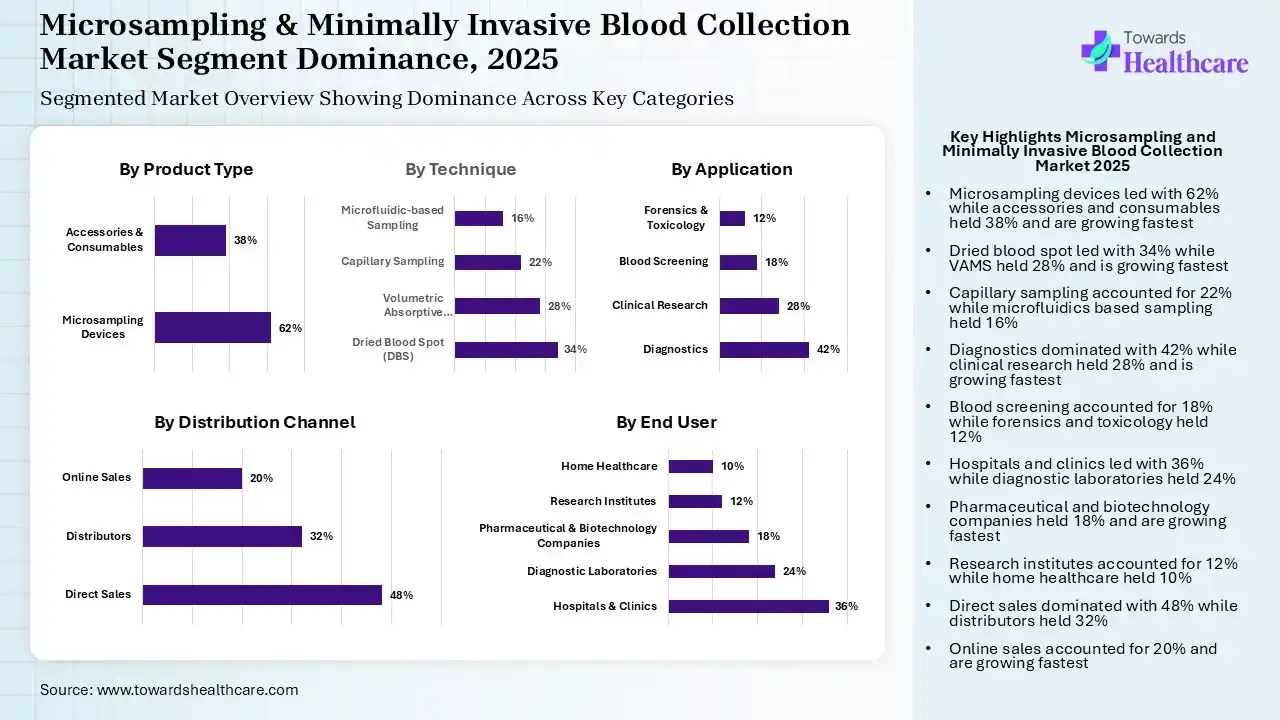

| Microsampling Devices | 62% |

| Accessories & Consumables | 38% |

The Microsampling Devices Segment Dominated the Market in 2025

The microsampling devices segment dominated the microsampling & minimally invasive blood collection market with a share of 62% in 2025 due to increasing demand for accurate, low-pain, and patient-friendly blood collection solutions. Their widespread use in home-based testing, chronic disease monitoring, and decentralized clinical trials, along with ease of handling and improved sample reliability, made them the leading product type across diagnostic and research applications.

The accessories & consumables segment held the second-largest share of 38% of the market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to recurring demand for lancets, capillary tubes, collection cards, and other single-use components required for every test. Rising testing volumes, increasing home-based diagnostics, and continuous repeat purchase across clinical, research, and remote monitoring applications.

| Segment | Share 2025 (%) |

| Dried Blood Spot (DBS) | 34% |

| Volumetric Absorptive Microsampling (VAMS) | 28% |

| Capillary Sampling | 22% |

| Microfluidic-based Sampling | 16% |

The Dried Blood Spot (DBS) Segment Led the Market in 2025 with the Largest Share

The dried blood spot (DBS) segment led the microsampling & minimally invasive blood collection market with a 34% share in 2025 due to its cost-effectiveness, ease of sample collection, and convenient storage and transport. Its strong adoption in neonatal screening, chronic disease testing, and remote diagnostics, along with minimal sample volume requirement and high sample stability, supported its leading market position.

The volumetric absorptive microsampling (VAMS) segment held the second-largest share of 28% of the market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to its ability to collect precise, fixed blood volumes with improved accuracy and reproducibility. Rising adoption in clinical trials, therapeutic drug monitoring, and decentralized testing, where reliable low-volume sampling is increasingly essential.

The capillary sampling segment held 22% of the microsampling & minimally invasive blood collection market share in 2025 due to its simplicity, low invasiveness, and suitability for rapid point-of-care and home-based testing. Its increasing use in glucose monitoring, infectious disease screening, and pediatric diagnostics, along with rising demand for convenient sample collection methods, is driving strong adoption across clinical and remote healthcare settings.

The microfluidics-based sampling segment held 16% of the microsampling & minimally invasive blood collection market share in 2025 due to its ability to handle ultra-low blood volumes with high precision and faster analysis. Growing adoption in point-of-care diagnostics, wearable health devices, and advanced biosensing applications, along with demand for automated and minimally invasive testing solutions, is driving its rapid growth across modern healthcare and research settings.

| Segment | Share 2025 (%) |

| Diagnostics | 42% |

| Clinical Research | 28% |

| Blood Screening | 18% |

| Forensics & Toxicology | 12% |

The Diagnostics Segment Led the Market in 2025 with the Largest Share

The diagnostics segment led the microsampling & minimally invasive blood collection market with a 42% share in 2025 due to the rising demand for early disease detection, routine health screening, and chronic disease monitoring. Widespread use of minimally invasive blood collection in hospitals, diagnostic labs, and home-testing kits, along with faster turnaround times and patient convenience, strongly supported its market leadership.

The clinical research segment held the second-largest share of 28% of the market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to increasing use of microsampling in decentralized clinical trials, pharmacokinetic studies, and biomarker analysis. Its ability to enable low-volume, patient-friendly sample collection improves participant compliance, reduces site visits, and supports efficient data collection, making it highly valuable for modern research and drug development studies.

The blood screening segment held 18% of the microsampling & minimally invasive blood collection market share in 2025, rising demand for early detection of infectious diseases, metabolic disorders, and chronic health conditions. Increasing use in routine health check-ups, donor screening, and population-wide testing programs, along with the convenience of minimally invasive sample collection, is driving adoption across hospitals, laboratories, and community healthcare settings.

The forensics & toxicology segment held 12% of the market share in 2025 due to increasing demand for accurate drug testing, alcohol screening, and forensic evidence analysis. Minimally invasive microsampling methods enable easy sample collection, secure storage, and efficient transport, making them highly suitable for law enforcement, workplace testing, and legal investigations, thereby supporting steady market growth.

| Segment | Share 2025 (%) |

| Hospitals & Clinics | 36% |

| Diagnostic Laboratories | 24% |

| Pharmaceutical & Biotechnology Companies | 18% |

| Research Institutes | 12% |

| Home Healthcare | 10% |

The Hospitals & Clinics Segment held a Dominant Position in the Market in 2025

The hospitals & clinics segment held a dominant position in the microsampling & minimally invasive blood collection market with a share of 36% in 2025 due to high patient volumes, frequent diagnostic testing, and strong adoption of minimally invasive blood collection methods for routine care. Their established infrastructure, access to skilled professionals, and growing focus on patient comfort and faster diagnostics supported the segment’s leading position.

The diagnostic laboratories segment held the second-largest share of 24% of the market in 2025 due to the high volume of blood testing conducted for disease diagnosis, routine screening, and chronic condition monitoring. Growing demand for accurate low-volume sample analysis, faster turnaround times, and increasing adoption of advanced microsampling technologies have strengthened its role across centralized and specialized testing services.

The pharmaceutical & biotechnology companies segment held 18% share in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to increasing use of microsampling in drug development, pharmacokinetic studies, and decentralized clinical trials. Rising demand for efficient low-volume sample collections, improved patient compliance, and faster biomarker analysis is driving strong adoption across research and therapeutic development activities.

The research institutes segment held 12% of the microsampling & minimally invasive blood collection market share in 2025 due to rising investment in biomedical research, clinical studies, and biomarker discovery programs. Microsampling enables precise low-volume sample collection, making it ideal for pediatric, preclinical, and longitudinal studies. Increasing focus on personalized medicine, disease monitoring, and innovative diagnostic research is further driving adoption across academic and research institutions.

The home healthcare segment held 10% of the market share in 2025 due to rising demand for convenient, patient-friendly testing and remote disease monitoring. Increasing prevalence of chronic conditions, growing preference for self-collection kits, and the expansion of telehealth services are driving adoption. Minimally invasive blood collection methods support easy at-home use, improving compliance and reducing hospital visits.

| Segment | Share 2025 (%) |

| Direct Sales | 48% |

| Distributors | 32% |

| Online Sales | 20% |

The Direct Sales Segment Dominated the Market in 2025

The direct sales segment dominated the microsampling & minimally invasive blood collection market with a revenue share of 48% in 2025 due to strong procurement by hospitals, diagnostic laboratories, pharmaceutical companies, and research institutes through direct supplier partnerships. This channel ensures bulk purchasing, customized product offerings, reliable after-sales support, and faster supply chain management, making it the preferred choice for large-volume institutional buyers.

The distributors segment held the second-largest market share of 32% in 2025 due to its wide regional reach and ability to efficiently supply products to hospitals, clinics, laboratories, and smaller healthcare facilities. Their strong distribution networks, inventory management capabilities, and timely product availability helped expand market penetration, especially across emerging and underserved healthcare markets.

The online sales segment held 20% share in 2025 and is expected to grow at the fastest CAGR due to increasing adoption of e-commerce platforms, rising demand for home healthcare products, and easy access to self-collection kits. Convenience, wider product availability, competitive pricing, and doorstep delivery are further driving strong growth, particularly among individual users and small healthcare providers.

")

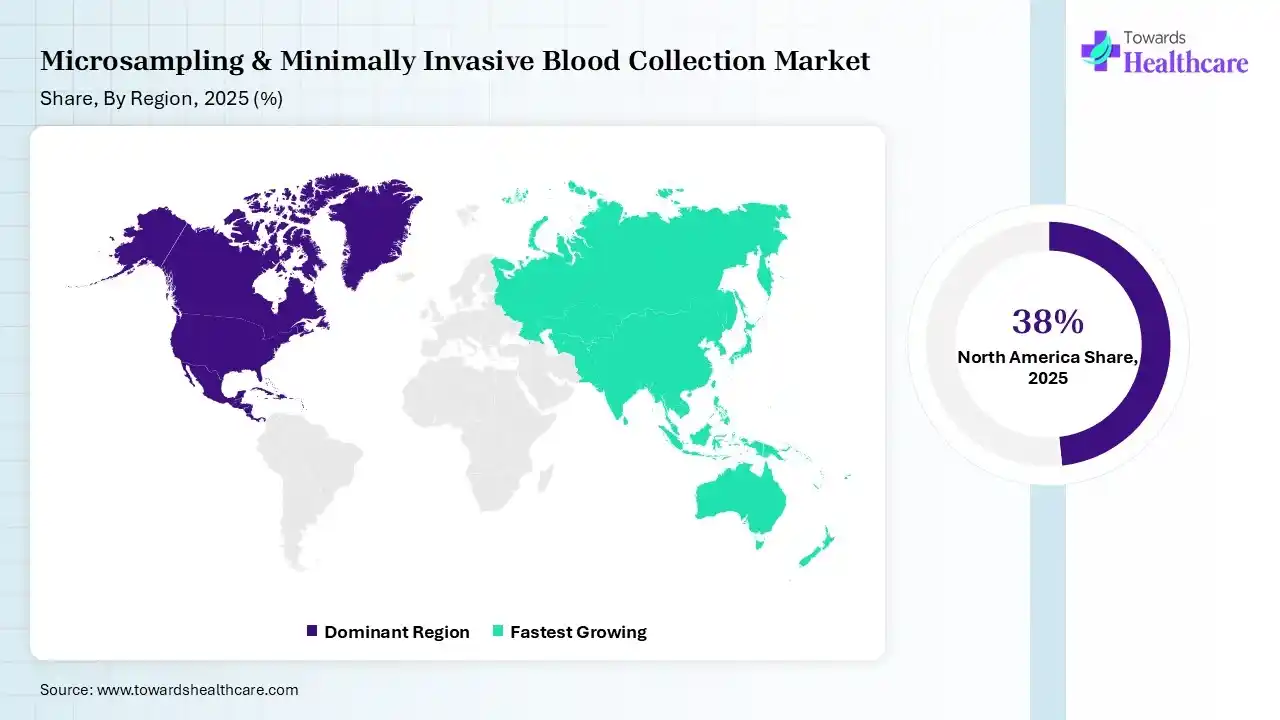

North America dominated the microsampling & minimally invasive blood collection market with a revenue share of 38% in 2025 due to advanced healthcare infrastructure, strong adoption of home-based diagnostics, and the presence of major industry players. Rising chronic disease cases, increasing decentralized clinical trials, and faster regulatory approvals further strengthened the region’s market leadership.

U.S. Market Trends

The U.S. microsampling & minimally invasive blood collection market is leading due to its advanced healthcare ecosystem, strong presence of major industry players, and rapid adoption of home-based testing solutions. Growing chronic disease burden, rising decentralized clinical trials, and continuous investments in research, diagnostics, and patient-centric technologies are further supporting market leadership.

Asia Pacific captured 22% of the market share in 2025 and is anticipated to grow at the fastest CAGR in the microsampling & minimally invasive blood collection market due to improving healthcare infrastructure, rising awareness of early diagnostics, and increasing demand for home-based testing solutions. Growing chronic disease prevalence, expanding clinical research activities, and rapid adoption of advanced blood collection technologies across emerging economies are further accelerating market growth.

India Market Trends

India is anticipated to grow at the fastest CAGR in the microsampling & minimally invasive blood collection market during the forecast period due to expanding healthcare infrastructure, rising demand for affordable diagnostics, and increasing adoption of home-based testing solutions. Growing chronic disease burden, higher clinical research activity, and rapid penetration of advanced blood collection technologies are further driving strong market growth.

Clinical Trails

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| BD | New Jersey, U.S. | Lancets, micro blood collection tubes, capillary sampling devices, blood collection kits |

| Abbott Laboratories | Abbott Park, Illinois, U.S. | Point-of-care diagnostics, glucose monitoring, and finger-prick blood collection solutions |

| F. Hoffmann-La Roche Ltd | Basel, Switzerland | Diagnostic systems, capillary blood testing solutions, and chronic disease monitoring tools |

| Terumo Corporation | Tokyo, Japan | Blood collection needles, capillary tubes, microsampling accessories |

| PerkinElmer, Inc. | Massachusetts, U.S. | Dried blood spot testing, neonatal screening, and laboratory diagnostic solutions |

| Neoteryx | California, U.S. | Mitra® VAMS®, hemaPEN®, remote microsampling kits, at-home blood collection devices |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Technique

By Application

By End User

By Distribution Channel

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar