Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

")

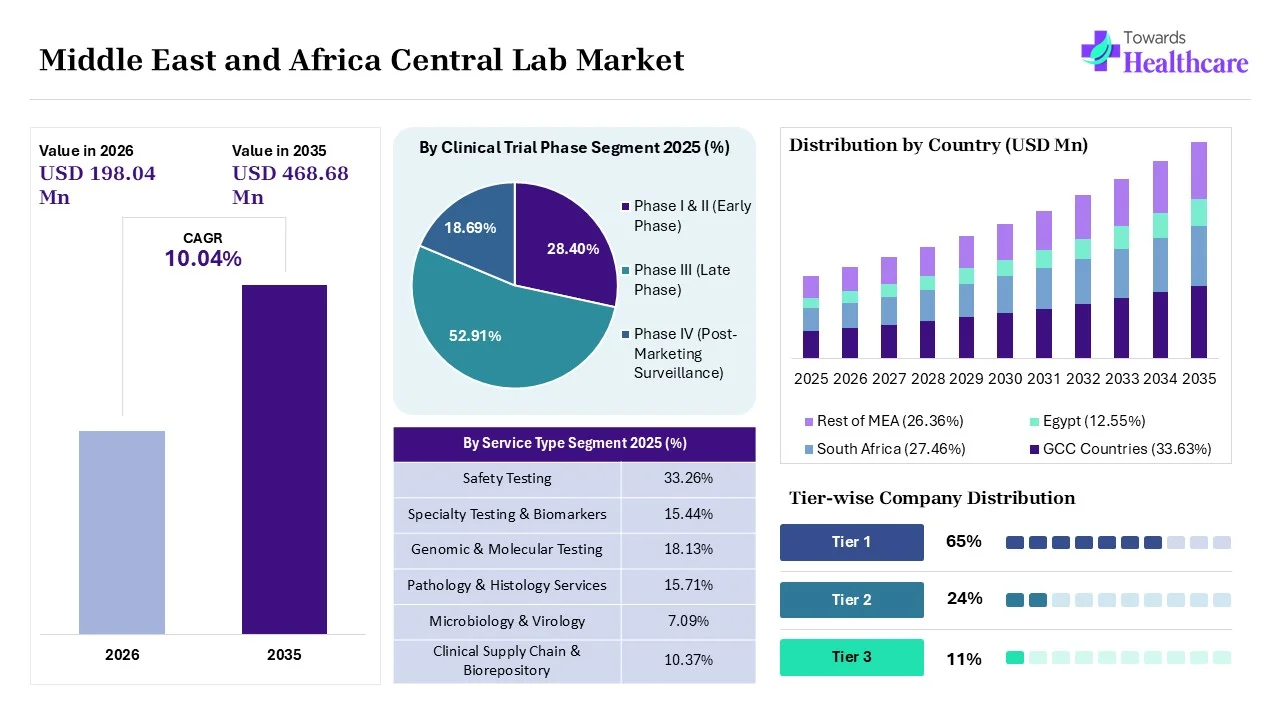

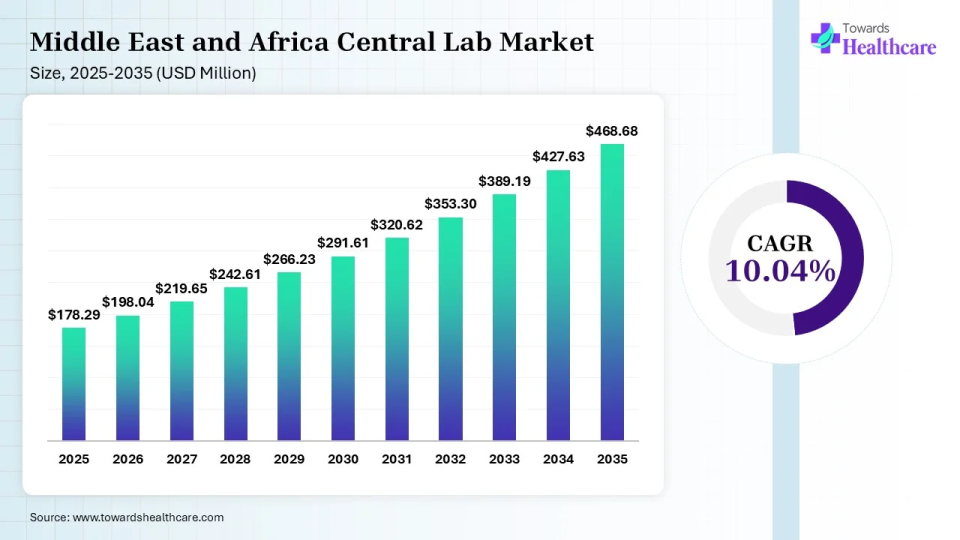

The Middle East and Africa central lab market size was valued at US$ 178.29 million in 2025 and is projected to grow to 198.04 million in 2026. Forecasts suggest it will reach approximately US$ 468.68 million by 2035, registering a CAGR of 10.04% during the period.

")

Central Laboratories in the Middle East & Africa are specialized facilities that provide standardized testing, sample analysis, and data management services for clinical trials, pharmaceutical research, and healthcare organizations. They ensure consistent and accurate results across multiple research sites while supporting services such as biomarker testing, molecular diagnostics, pathology, and genetic analysis.

These laboratories are increasingly adopting advanced technologies such as laboratory automation, artificial intelligence (AI)-driven analytics, next-generation sequencing (NGS), and cloud-based laboratory information management systems. Growing clinical research activities, expanding healthcare infrastructure, and the rising focus on precision medicine are enhancing the role of central laboratories in improving testing efficiency, data quality, and research outcomes across the region.

The Middle East and Africa central lab market is growing due to increasing investments in healthcare research, rising prevalence of chronic diseases, and expanding participation in global clinical studies. Supportive regulatory reforms, improving healthcare infrastructure, and growing pharmaceutical and biotechnology activities are further boosting demand for efficient clinical trial services across the region.

Artificial intelligence is significantly enhancing the Middle East & Africa central lab market by improving sample analysis, data interpretation, and workflow automation. AI-powered tools help reduce testing errors, accelerate clinical trial processes, and support predictive analytics for better research outcomes. Additionally, AI enables efficient management of large laboratory datasets, enhances diagnostic accuracy, and optimizes operational efficiency, driving greater productivity and innovation in central laboratory services.

Rising Demand for Biomarker and Molecular Testing

Central laboratories are witnessing increased demand for biomarker analysis, genetic testing, and molecular diagnostics as clinical research becomes more specialized. This trend is expected to strengthen the role of central labs in supporting precision medicine, targeted therapies, and advanced drug development programs across the region.

Expansion of Clinical Trial Activities

Growing pharmaceutical and biotechnology research investments are driving higher clinical trial volumes in the Middle East and Africa. Central laboratories are expected to benefit from the need for standardized testing, sample management, and consistent data generation across multiple study sites and research programs.

Advancements in Laboratory Automation and Digitalization

The adoption of automated testing platforms, digital data management systems, and integrated laboratory workflows is improving operational efficiency and testing accuracy. These advancements are expected to enhance laboratory productivity, reduce turnaround times, and support the increasing complexity of clinical research and diagnostic services.

| Table | Scope |

| Market Size in 2026 | USD 198.04 Million |

| Projected Market Size in 2035 | USD 468.68 Million |

| CAGR (2026 - 2035) | 10.04% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By Clinical Trial Phase, By Modality, By End User, By Region |

| Top Key Players | Lancet Laboratories, Ampath Laboratories, Pathcare, Al Borg Diagnostics, National Reference Laboratory, Unilabs Middle East, Synlab Nigeria |

")

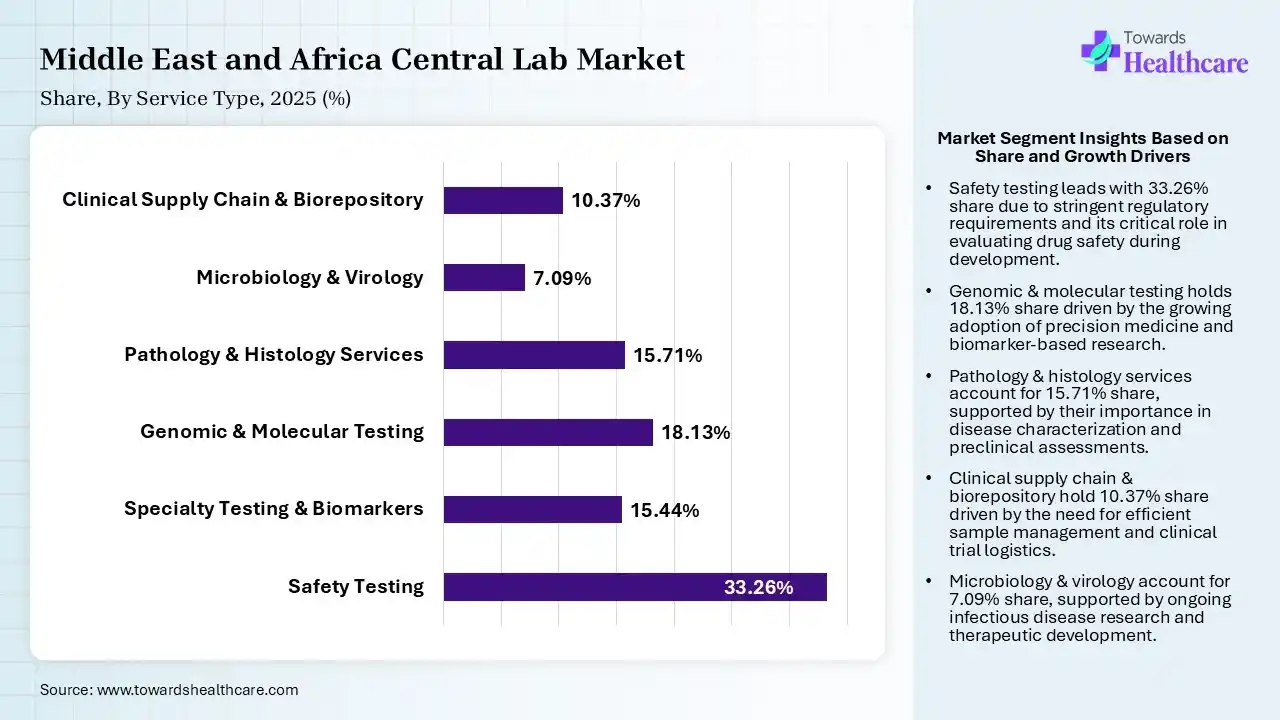

| Segment | Share 2025 (%) |

| Safety Testing | 33.26% |

| Specialty Testing & Biomarkers | 15.44% |

| Genomic & Molecular Testing | 18.13% |

| Pathology & Histology Services | 15.71% |

| Microbiology & Virology | 7.09% |

| Clinical Supply Chain & Biorepository | 10.37% |

The Safety Testing Segment Dominated the Middle East and Africa Central Lab Market in 2025.

The safety testing segment held a dominant share of 33.26% in 2025 due to its essential role in assessing drug safety, monitoring adverse events, and ensuring regulatory compliance throughout clinical trials. The increasing number of clinical studies, growing pharmaceutical research activities, and rising focus on patient safety have significantly boosted demand for safety testing services. Its importance in generating reliable and standardized trial data further strengthened segment dominance.

The genomic & molecular testing segment held the second-largest share of 18.13% in 2025 due to increasing demand for precision medicines, biomarker identification, and targeted therapy development. Growing clinical research activities and advancements in genetic analysis technologies supported segment growth. Pharmaceutical and biotechnology companies increasingly utilize these testing services to improve patient satisfaction, enhance trial accuracy, and support personalized treatment approaches.

The specialty testing & biomarkers segment held a 15.44% share in 2025 and is expected to grow at the fastest CAGR of 11.59% in the Middle East and Africa central lab market during the forecast period due to the increasing focus on precision medicine, targeted therapies, and personalized treatment approaches. Rising demand for biomarker identification in clinical trials, growing investments in advanced drug development, and the need for improved patient satisfaction are accelerating adoption. These services help enhance trial efficiency, treatment effectiveness, and clinical decision-making.

The pathology & histology services segment held 15.71% of the market due to the growing need for detailed tissue analysis and disease diagnosis in clinical trials and healthcare research. Rising incidences of cancer and other chronic diseases are increasing the demand for accurate pathological assessments. Additionally, expanding pharmaceutical research activities and the need for reliable diagnostic data to support drug development and treatment evaluation are driving segment growth across the region.

")

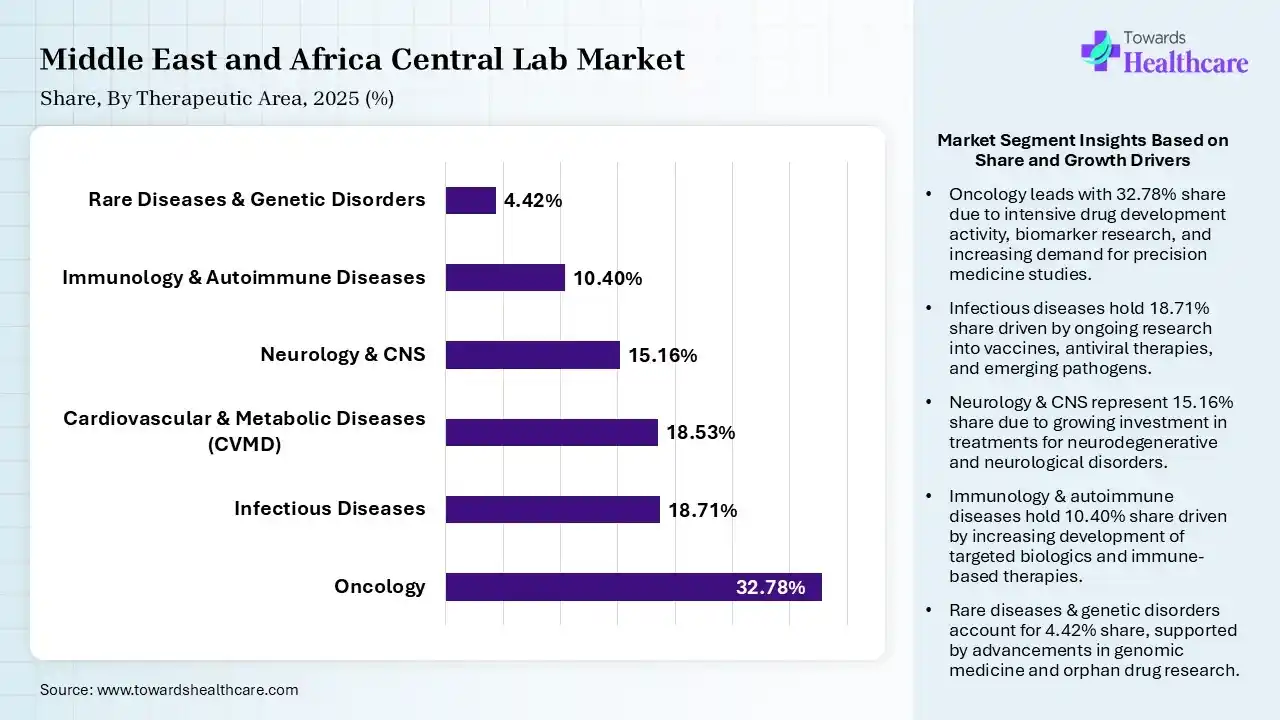

| Segment | Share 2025 (%) |

| Oncology | 32.78% |

| Infectious Diseases | 18.71% |

| Cardiovascular & Metabolic Diseases (CVMD) | 18.53% |

| Neurology & CNS | 15.16% |

| Immunology & Autoimmune Diseases | 10.40% |

| Rare Diseases & Genetic Disorders | 4.42% |

The Oncology Segment Led the Market in 2025 with the Largest Share

The oncology segment dominated the Middle East and Africa central lab market with a share of 32.78% in 2025 due to the increasing prevalence of cancer and the growing number of oncology-focused clinical trials. Pharmaceutical and biotechnology companies are investing heavily in cancer drug development, requiring extensive biomarker testing, pathology assessment, and molecular diagnostics. The complexity of oncology studies and the need for precise, standardized laboratory services further strengthened the segment’s leading market position.

The infectious diseases segment held the second-largest share of 18.13% in 2025 due to the high burden of infectious diseases across the region and the continued need for disease surveillance and clinical research. Increasing diagnostic testing, vaccine development programs, and infectious disease services. The requirement for accurate pathogen detection and standardized testing further supported the segments’ substantial market share.

The cardiovascular & metabolic diseases (CVMD) segment held an 18.53% market share due to the rising prevalence of heart diseases, diabetes, obesity, and related metabolic disorders across the Middle East and Africa. Increasing clinical research efforts, growing demand for advanced diagnostic testing, and the development of innovative therapies are driving segment growth. Central laboratories play a vital role in supporting these studies through standardized testing, biomarker analysis, and accurate data management.

The rare diseases & genetic disorders segment held a 4.42% share in 2025 and is expected to grow at the fastest CAGR of 14.29% in the Middle East and Africa central lab market during the forecast period due to increasing awareness, improved diagnostic capabilities, and rising investments in genetic research. Growing demand for specialized testing, biomarker analyses, and personalized treatment approaches is accelerating segment expansion. Additionally, the increasing number of clinical trials focused on rare diseases is creating significant opportunities for central laboratory services.

")

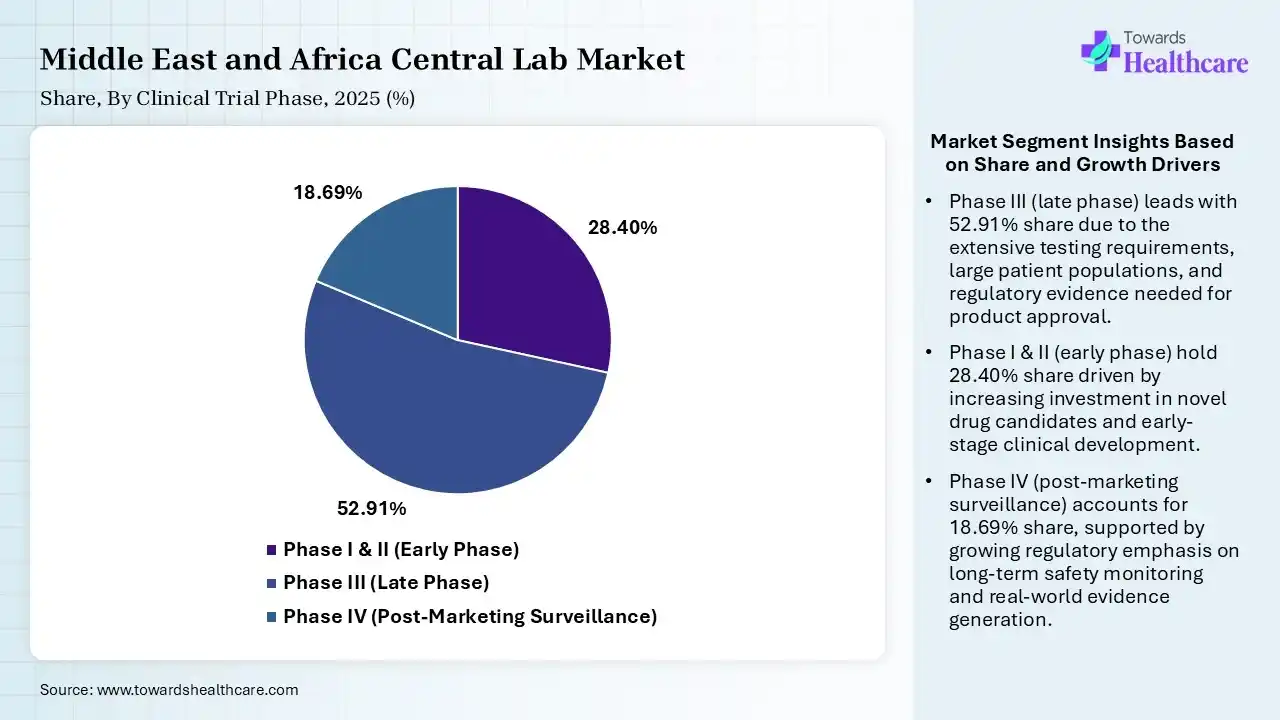

| Segment | Share 2025 (%) |

| Phase I & II (Early Phase) | 28.40% |

| Phase III (Late Phase) | 52.91% |

| Phase IV (Post-Marketing Surveillance) | 18.69% |

The Phase III (Late Phase) Segment Led the Middle East and Africa Central Lab Market in 2025 with the Largest Share

The phase III (late phase) segment held a dominant share of 52.91% in 2025 due to the large scale and complexity of these trials. Phase III studies involve a greater number of patients, extensive safety monitoring, and comprehensive laboratory testing requirements. Growing pharmaceutical investments and increasing late-stage clinical research activities further boosted demand for central laboratory services, making phase III trials the largest contributor to market revenue in 2025.

The phase I & II (early phase) segment held the second-largest share of 28.40% in 2025 and is expected to grow at the fastest CAGR of 10.87% in the market during the forecast period due to increasing drug discovery and early-stage clinical development activities. These trials require extensive biomarker testing, pharmacokinetic analysis, and safety assessment to evaluate innovative therapies and expanding pharmaceutical research pipelines, which contributed to the segment’s significant market presence.

The phase IV (post-marketing surveillance) segment held 18.69% of the Middle East and Africa central lab market share due to the increasing need to monitor long-term drug safety, effectiveness, and real-world patient outcomes after product approval. Regulatory authorities and pharmaceutical companies are placing greater emphasis on ongoing safety assessments and adverse event monitoring. Rising adoption of real-world evidence studies and expanding use of approved therapies are further driving demand for central laboratory services in Phase IV research.

")

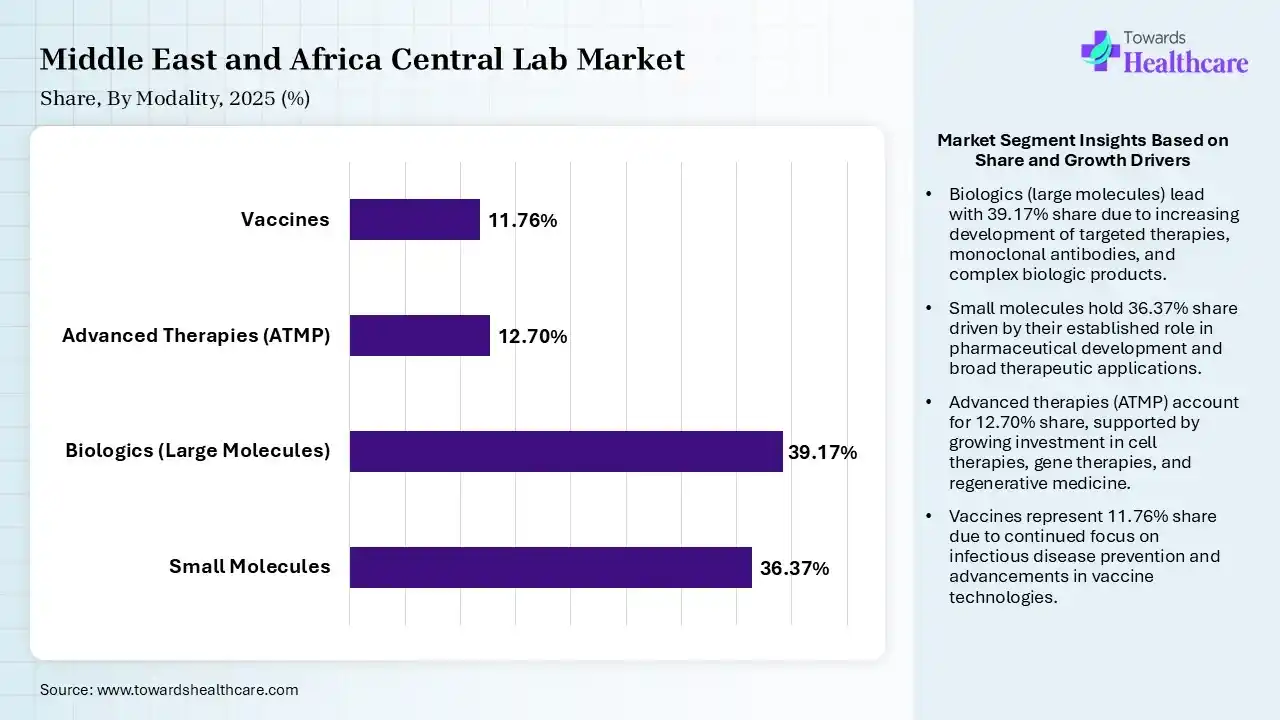

| Segment | Share 2025 (%) |

| Small Molecules | 36.37% |

| Biologics (Large Molecules) | 39.17% |

| Advanced Therapies (ATMP) | 12.70% |

| Vaccines | 11.76% |

The Biologics (Large Molecules) Segment Led the Middle East and Africa Central Lab Market in 2025 with the Largest Share

The biologics (large molecules) segment led the market with a share of 39.17% in 2025 due to the growing development of monoclonal antibodies, vaccines, cell therapies, and other biologic products. These therapies require complex laboratory testing, biomarker analysis, and specialized monitoring throughout clinical trials. Increasing investments in biotechnology research, rising demand for targeted treatments, and the expanding biologics pipelines further strengthened the segment’s dominant market position.

The small molecules segment held a 36.37% share of the Middle East and Africa central lab market in 2025. This significant share reflects the region's rising demand for specialized bioanalytical testing and robust support for clinical trials targeting chronic diseases. Driven by heavy investments in healthcare infrastructure in countries like Saudi Arabia and the UAE, the demand for conventional therapeutics continues to shape contract research priorities across the Middle East and Africa.

The advanced therapies (ATMP) segment held the second-largest share of 12.70% in 2025 and is expected to grow at the fastest CAGR of 14.38% in the market during the forecast period due to increasing research in cell therapies, gene therapies, and regenerative medicine. These innovative treatments require highly specialized laboratory testing, biomarker analysis, and stringent sample management. Growing investments in biotechnology, expanding clinical trial activity, and the rising focus on personalized medicine further supported the segment’s significant market position in 2025.

The vaccines segment held an 11.76% of the Middle East and Africa central lab market share due to increasing investment in vaccine research and development, rising immunization programs, and growing efforts to prevent infectious diseases across the Middle East and Africa. Central laboratories play a crucial role in supporting vaccine clinical trials through safety testing, biomarker analysis, and efficacy assessments. The continued focus on public health preparedness and disease prevention is further driving segment growth.

")

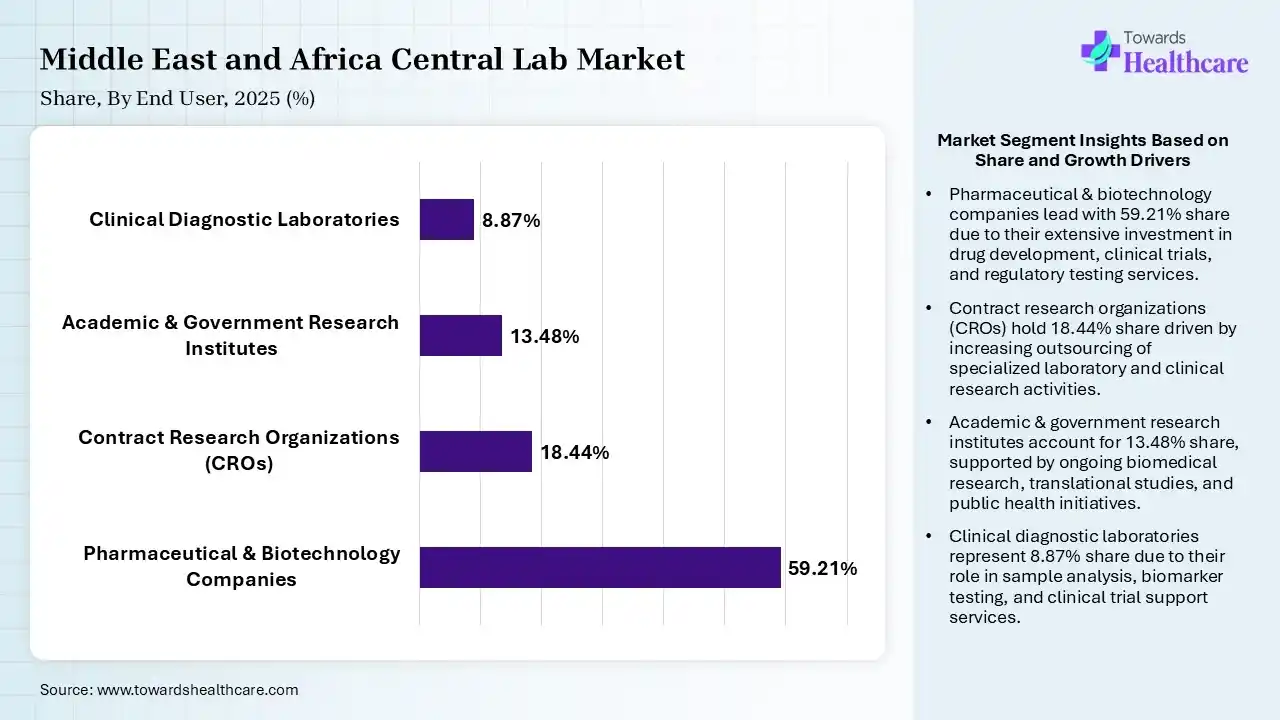

| Segment | Share 2025 (%) |

| Pharmaceutical & Biotechnology Companies | 59.21% |

| Contract Research Organizations (CROs) | 18.44% |

| Academic & Government Research Institutes | 13.48% |

| Clinical Diagnostic Laboratories | 8.87% |

The Pharmaceutical & Biotechnology Companies Segment Dominance Dominated the Middle East and Africa Central Lab Market in 2025

The pharmaceutical & biotechnology companies segment held a dominant share of 59.21% in 2025 due to substantial investments in drug discovery, clinical trials, and biologics development. These organizations rely heavily on central laboratories for standardized testing, biomarker analysis, safety assessment, and regulatory compliance. The growing pipelines of innovative therapies, increasing research and development activities, and rising outsourcing of laboratory services further strengthened the segment’s dominant market position.

The contract research organization (CROs) segment held the second-largest share of 18.44% in 2025 and is expected to grow at the fastest CAGR of 11.35% in the market during the forecast period due to the increasing outsourcing of clinical trial operations by pharmaceutical and biotechnology companies. CROs rely on central laboratories for standardized testing, sample management, and regulatory-compliant data generation. Growing clinical research activity, cost-efficiency benefits, and the need for specialized expertise further supported the segment’s strong market presence.

The academic & government research institutes segment held a 13.48% of the Middle East and Africa central lab market share due to increasing investments in biomedical research, public health studies, and clinical research programs across the Middle East and Africa. These institutions are expanding collaborations with pharmaceutical companies and healthcare organizations to advance disease research and therapeutic development. The growing need for high-quality laboratory testing, biomarker analysis, and standardized research data is further driving demand for central laboratory services.

The clinical diagnostic laboratories segment held an 8.87% market share due to the increasing demand for accurate disease diagnostics, routine testing, and specialized laboratory services across the Middle East and Africa. Rising prevalence of chronic and infectious diseases, growing healthcare utilization, and advancements in diagnostic technologies are driving testing volumes. Additionally, the need for standardized, high-quality laboratory results and faster turnaround times is supporting continued segment growth.

The Middle East and Africa central lab market is gaining strong traction due to increasing clinical trial activity, rising pharmaceutical and biotechnology investments, and expanding healthcare infrastructure. Growing demand for standardized laboratory testing, biomarker analysis, and regulatory-compliant data is further supporting market growth. Additionally, the region’s increasing focus on precision medicine, disease research, and clinical innovation is strengthening the role of central laboratories in healthcare and drug development.

The GCC countries dominated the Middle East and Africa central lab market with a share of 33.63% in 2025 and are expected to grow at the fastest CAGR of 11.26% in the market during the forecast period due to strong healthcare investments, expanding clinical research activities, and increasing pharmaceutical and biotechnology partnerships. Advanced healthcare infrastructure, supportive government initiatives, and rising demand for precision medicine and specialized laboratory testing are further accelerating the adoption of central laboratory services across GCC nations.

| Companies | Headquarters | Offerings |

| Lancet Laboratories | Johannesburg | Clinical diagnostics, pathology services, laboratory testing, research support |

| Ampath Laboratories | Centurion | Pathology testing, clinical laboratory services, specialized diagnostics |

| PathCare | Cape Town | Diagnostic testing, pathology services, clinical trial laboratory support |

| Al Borg Diagnostics | Jeddah | Laboratory diagnostics, molecular testing, pathology, and clinical laboratory services |

| National Reference Laboratory | Abu Dhabi | Reference testing, genomics, infectious disease testing, clinical research support |

| Unilabs Middle East | Dubai | Clinical diagnostics, laboratory testing, pathology, and specialty testing |

| Synlab Nigeria | Lagos | Clinical laboratory testing, pathology services, molecular diagnostics, and preventive healthcare testing |

In October 2025, "Our vision is to transform healthcare delivery in Saudi Arabia. We are committed to advancing medical excellence, supporting our workforce, and integrating smart technologies that will redefine patient care. Saudi Arabia is poised to become a global reference point for health innovation, and we are proud to be part of that journey."

By Service Type

By Therapeutic Area

By Clinical Trial Phase

By Modality

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar