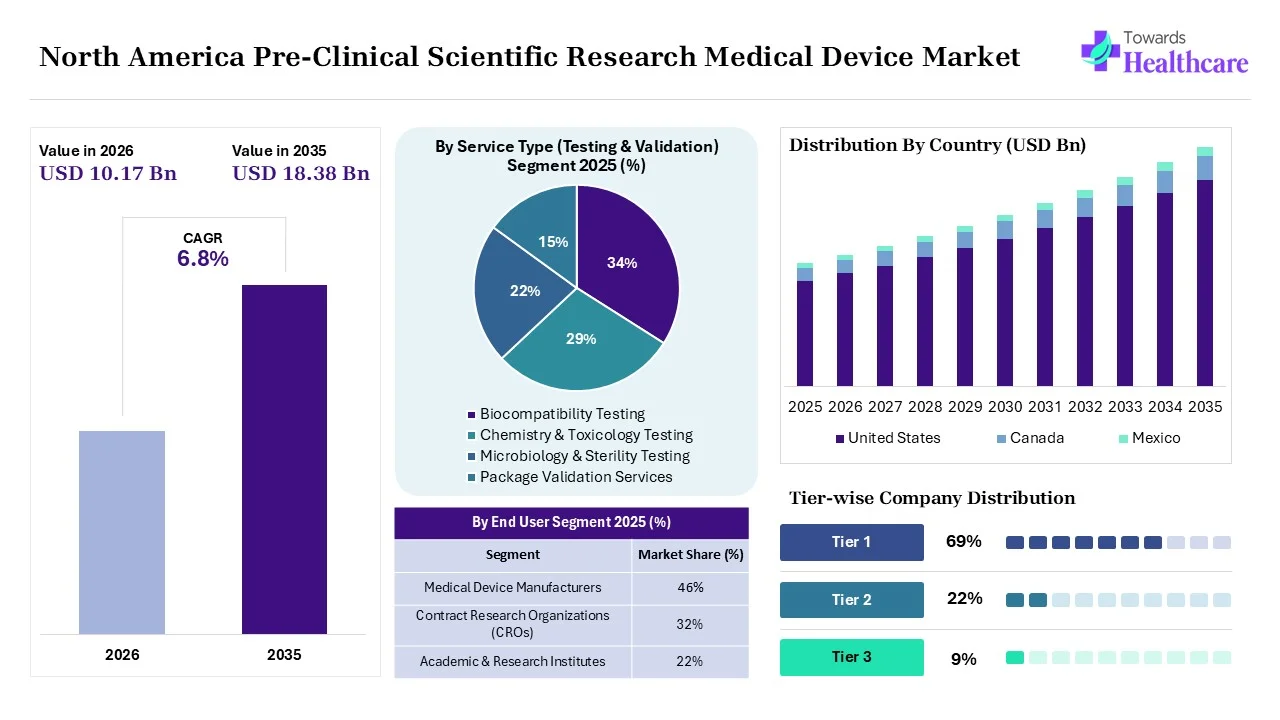

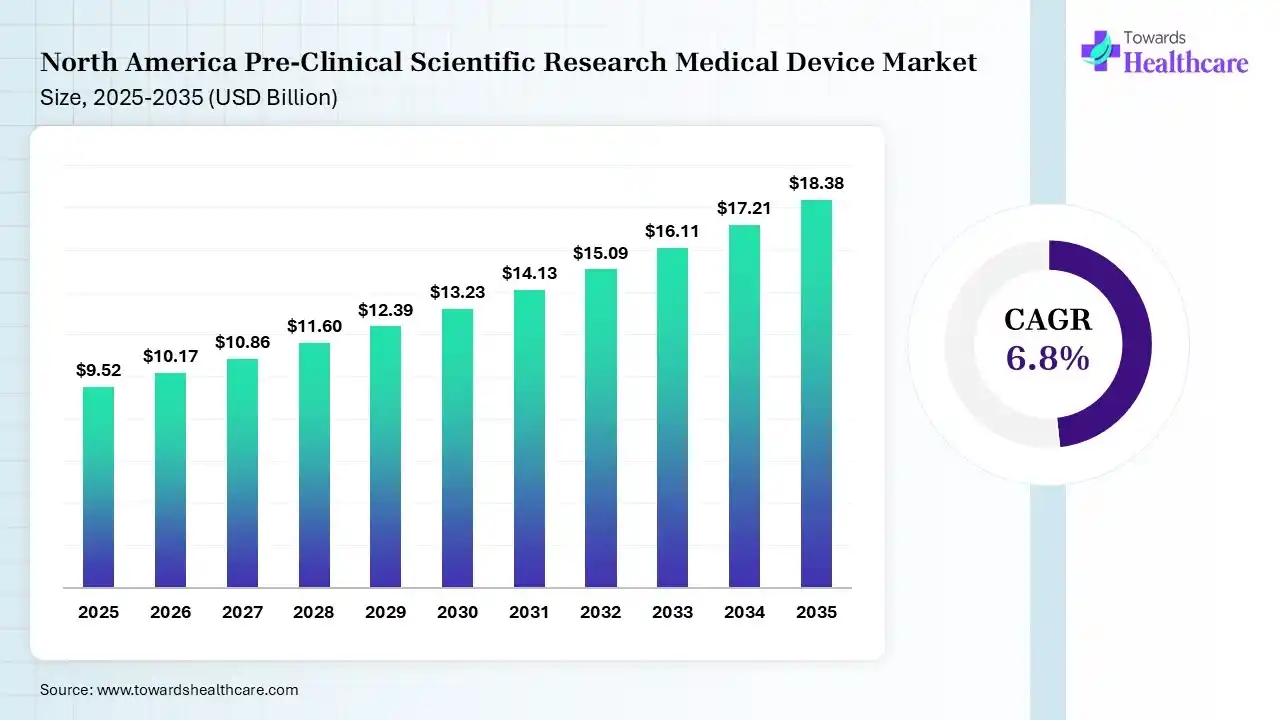

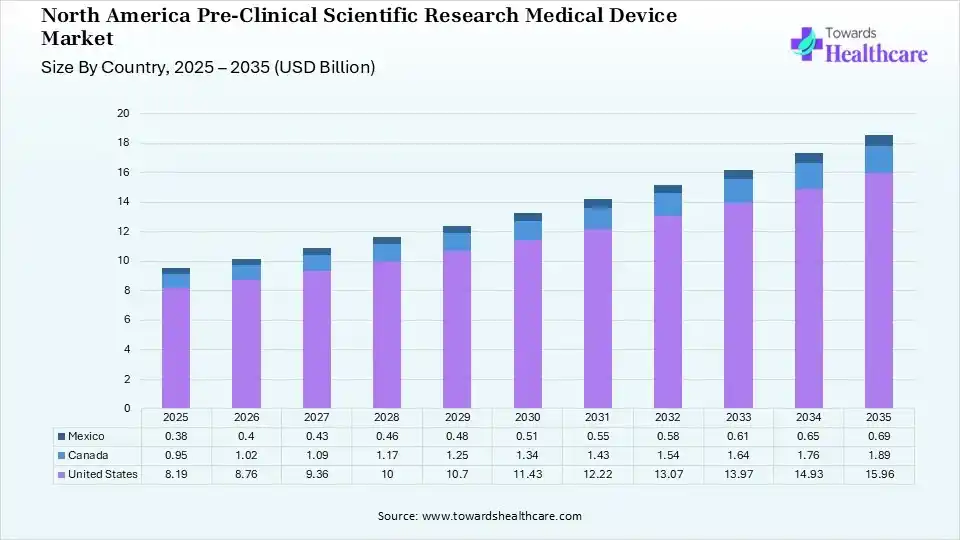

The North America pre-clinical scientific research medical device market size is calculated at USD 9.52 billion in 2025, driven by increasing R&D expenditure across North America. The market continues to grow USD 10.17 billion in 2026 due to the rising use of AI technologies, increasing use of translational research models, and new product launches. It is expected to reach USD 18.38 billion by 2035, driven by a CAGR of 6.8% over the forecast period. as a rise in the demand for high-throughput accelerated drug discovery, expanding precision medicine research, and technological services accelerates market expansion. The U.S. accounted for 86% of the market in 2025 due to its largest R&D spending, extensive CRO presence, and advanced research infrastructure.

")

")

The North America pre-clinical scientific research medical device market is driven by a surge in R&D expenditure, rising adoption of translational research models, expanding stringent regulations, and growing demand for high-throughput accelerated drug discovery. North America pre-clinical scientific research medical device encompasses medical devices used to evaluate the safety, performance, and efficacy of medical products in preclinical research. These devices are utilized to support preclinical studies focusing on drug discovery, safety testing, medical device development, and biomedical research.

Therefore, growing R&D activities and investments are also supporting preclinical scientific research and medical device adoption across North America. The common types of devices utilized in preclinical studies include preclinical imaging systems, surgical instruments, physiological monitoring systems, data acquisition systems, animal research monitoring equipment, and laboratory automation systems. This, in turn, drives their use for toxicology testing, translational research, medical device testing, disease modelling, and precision medicine research. Additionally, expanding digital technologies, growing outsourcing trends, increasing automated laboratory solutions, a shift towards alternative research models, and growing collaborations are also supporting the market expansion.

AI offers a wide range of applications in the North America pre-clinical scientific research medical device market by improving the analysis of preclinical research data and images. It also helps in accelerating drug discovery, biomarker discovery, predicting drug efficacy and drug safety, as well as identifying suitable targets. AI is also used for predictive disease modelling, structure optimization, and developing experimental design, where it also helps in automating laboratory workflows and improving the accuracy of preclinical studies.

Expanding Precision Medicine Research

In order to offer personalized and targeted treatment to patients, the demand for precision medicine is increasing, which is driving R&D activities across North America. They are being developed by utilizing individual patient disease profiles, genetic information, and other characteristics, which is increasing the demand for imaging, analytical, and monitoring tools for their research purposes. The growing investments in personalized medicines, genomics, and biomarker discovery are also supporting their advancements.

Rise of Alternative Research Models

Expanding stringent regulations and focus on reducing animal testing are increasing the demand for alternative research models in North America. This, in turn, is driving the development of new models such as 3D cell cultures, organ-on-chip systems, and tissue-engineered models to support non-animal testing approaches. Moreover, their human-relevant data and enhanced predictive accuracy are also driving the development of specialised preclinical devices.

Technological Advancements

Increasing R&D activities, technological advancements, and investments are increasing the innovation and adoption of pre-clinical scientific research medical devices. The companies are focusing on enhancing the performance, efficiency, and accuracy of the preclinical research devices, which is driving the development of new devices with AI integration. Moreover, new digital technologies are also being used to offer real-time data collection and analysis, reduce manual errors, and enhance laboratory productivity, as well as improve research outcomes.

| Table | Scope |

| Market Size in 2026 | USD 10.17 Billion |

| Projected Market Size in 2035 | USD 18.38 Billion |

| CAGR (2026 - 2035) | 6.8% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Service Type, By Application, By End User, By Region |

| Top Key Players | MILabs B.V., Revvity, Inc., Bruker Corporation, Siemens Healthineers, Mediso Medical Imaging Systems, PINGSENG Healthcare, MR Solutions |

")

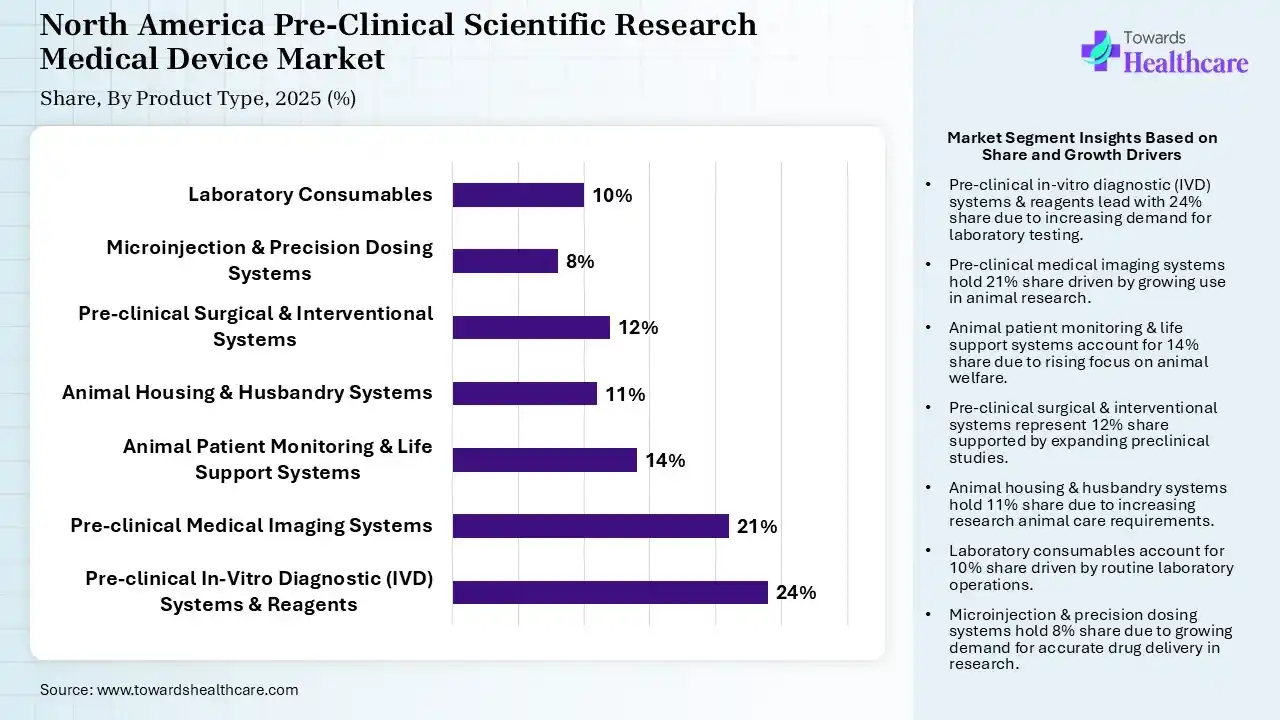

| Segment | Share 2025 (%) |

| Pre-clinical In-Vitro Diagnostic (IVD) Systems & Reagents | 24% |

| Pre-clinical Medical Imaging Systems | 21% |

| Animal Patient Monitoring & Life Support Systems | 14% |

| Animal Housing & Husbandry Systems | 11% |

| Pre-clinical Surgical & Interventional Systems | 12% |

| Microinjection & Precision Dosing Systems | 8% |

| Laboratory Consumables | 10% |

The Pre-clinical In-Vitro Diagnostic (IVD) Systems & Reagents Segment Dominated the Market With 24% in 2025

The pre-clinical in-vitro diagnostic (IVD) systems & reagents segment led the North America pre-clinical scientific research medical device market with 24% share in 2025, due to a rise in biomarker discovery programs. Increased molecular assays and growth in translational research investments also contributed to their continuous usage. Their high-throughput testing capabilities also increased their adoption rates.

The pre-clinical medical imaging systems segment held the second-largest share of 21% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 7.8% during the forecast period, driven by expanding multimodal imaging adoption. Higher demand for non-invasive studies also increases the use of these systems. AI-assisted imaging is also accelerating workflows.

The animal patient monitoring & life support systems segment held 14% of the North America pre-clinical scientific research medical device market share in 2025, driven by more complex animal procedures. Improved welfare requirements are also encouraging the adoption of these systems. Growth in long-duration studies is also driving a shift towards these devices.

The pre-clinical surgical & interventional systems segment held 12% of the market share in 2025, due to growth in minimally invasive research. Advanced surgical modelling is also increasing the demand for pre-clinical surgical & interventional systems. Additionally, increasing precision intervention studies are also promoting their adoption. They are also being used for implant validation.

")

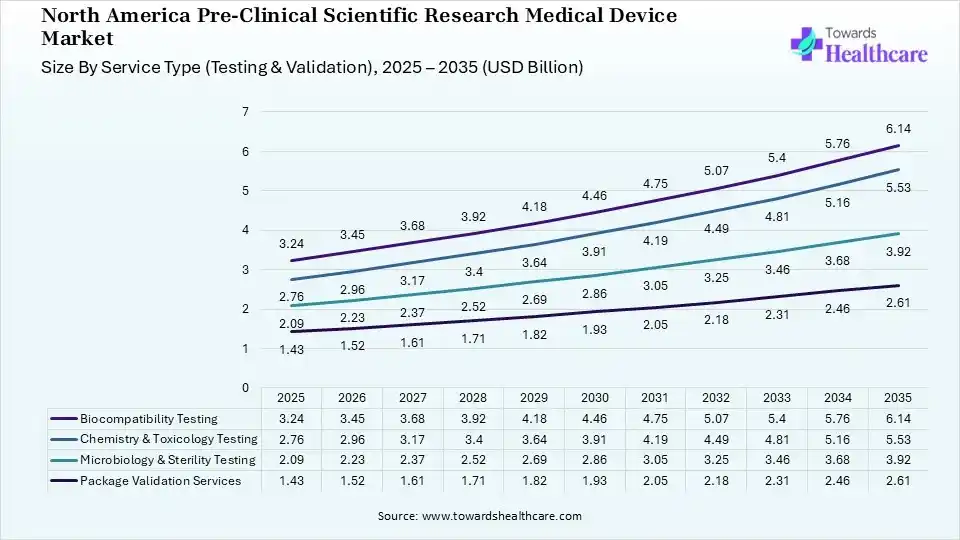

| Segment | Share 2025 (%) |

| Biocompatibility Testing | 34% |

| Chemistry & Toxicology Testing | 29% |

| Microbiology & Sterility Testing | 22% |

| Package Validation Services | 15% |

The Biocompatibility Testing Segment Dominated the Market With 34% in 2025

The biocompatibility testing segment accounted for the highest revenue share of 34% of the North America pre-clinical scientific research medical device market in 2025, driven by expanded device safety regulations. Increased ISO testing requirements also promoted the adoption of these services. Additionally, manufacturers prioritize compliance, which encourages their use.

The chemistry & toxicology testing segment held the second-largest share of 29% of the market in 2025 and is expected to show the highest growth with a CAGR of 7.2% during the forecast period, due to more combination products entering pipelines. Toxicology studies become broader, which drives the demand for toxicology testing. Regulatory scrutiny increases, which supports the adoption of these solutions.

The microbiology & sterility testing segment held 22% of the North America pre-clinical scientific research medical device market share in 2025, as sterility assurance remains essential. Infection prevention requirements rise, which increases the demand for microbiology & sterility testing products. Strengthening quality standards also drives the adoption of these testing solutions.

The package validation services segment held 15% of the market share in 2025, driven by packaging innovation expansion. Growing demand for shelf-life verification is also promoting the adoption of package validation services. Distribution testing becomes critical, which encourages the use of these services. Stringent regulations are also driving their demand.

")

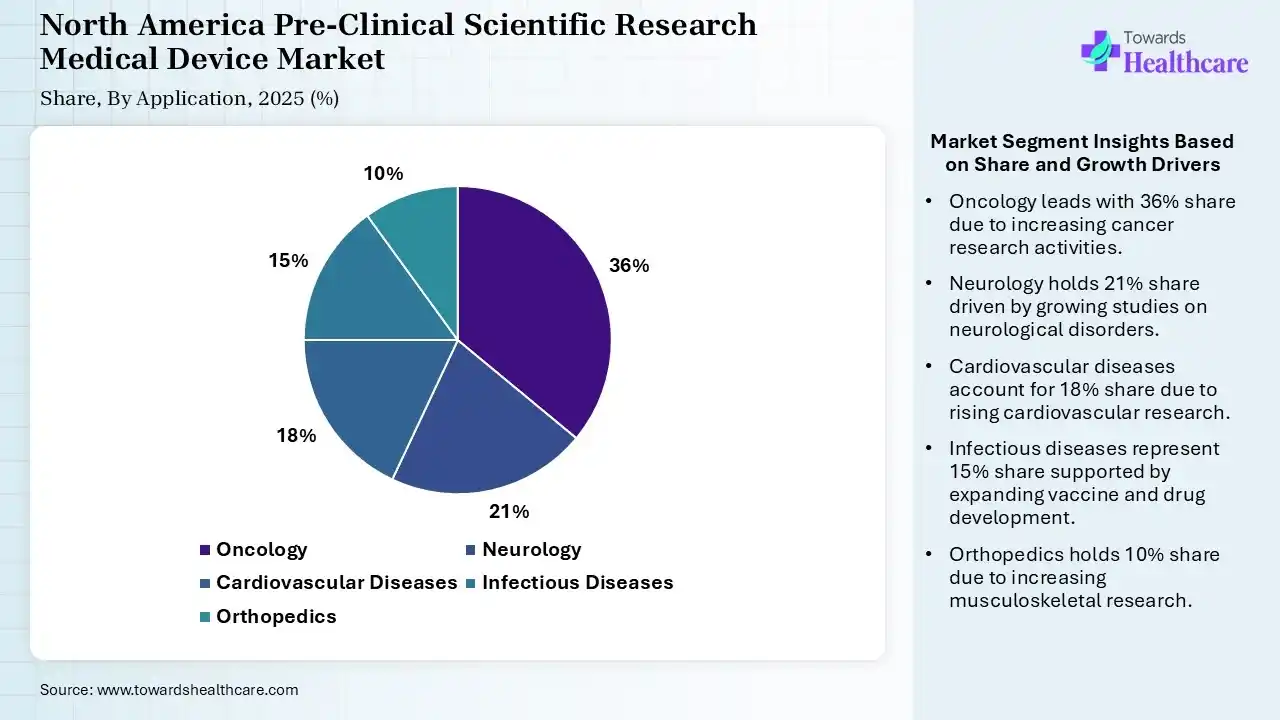

| Segment | Share 2025 (%) |

| Oncology | 36% |

| Neurology | 21% |

| Cardiovascular Diseases | 18% |

| Infectious Diseases | 15% |

| Orthopedics | 10% |

The Oncology Segment Dominated the Market With 36% in 2025

The oncology segment held a major revenue share of 36% of the North America pre-clinical scientific research medical device market in 2025 and is expected to expand rapidly with a CAGR of 7.6% during the forecast period, due to robust oncology pipelines. Precision medicine expansion also increased the demand for pre-clinical scientific research medical devices. Immunotherapy research has also increased its demand.

The neurology segment held the second-largest share of 21% of the market in 2025, driven by CNS disorders requiring advanced models. Neurodegenerative research funding increases, which drives the demand for pre-clinical scientific research medical devices. At the same time, imaging technologies are improving, which is leading to a rise in their adoption.

The cardiovascular diseases segment held 18% of the North America pre-clinical scientific research medical device market share in 2025, driven by continuous innovations in cardiovascular devices. The growth in the disease burden also increases the use of pre-clinical scientific research medical devices. Functional assessment technologies advance, increasing their adoption rates.

The infectious diseases segment held 15% of the market share in 2025, due to emerging pathogens requiring rapid evaluation, which drives the demand for pre-clinical scientific research medical devices. A rise in vaccine development also fuels the demand for these devices. Biosecurity investments expand, promoting their adoption rates.

")

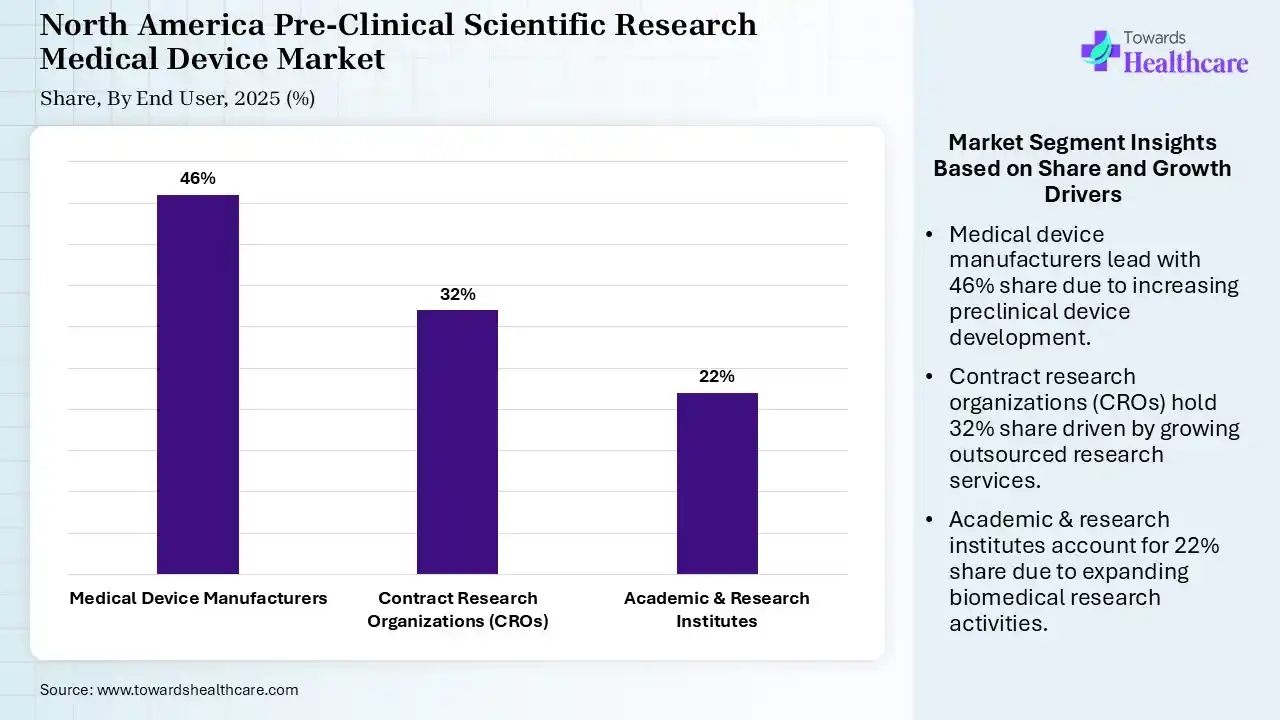

| Segment | Share 2025 (%) |

| Medical Device Manufacturers | 46% |

| Contract Research Organizations (CROs) | 32% |

| Academic & Research Institutes | 22% |

The Medical Device Manufacturers Segment Dominated the Market With 46% in 2025

The medical device manufacturers segment contributed the biggest revenue share of 46% of the North America pre-clinical scientific research medical device market in 2025, driven by their continuous product development. Internal R&D expansion and growth in regulatory testing investments also increased the demand for pre-clinical scientific research medical devices.

The contract research organizations (CROs) segment held the second-largest share of 32% of the market in 2025 and is expected to gain the highest share with a CAGR of 7.5% during the forecast period, due to outsourcing accelerating globally. Flexible research capacity attracts sponsors. The presence of specialized expertise also increases their preference.

The academic & research institutes segment held 22% of the North America pre-clinical scientific research medical device market share in 2025, driven by growing government grants, which support research. University collaborations increase, which leads to a rise in the use of pre-clinical scientific research medical devices. Innovation programs expand, increasing availability.

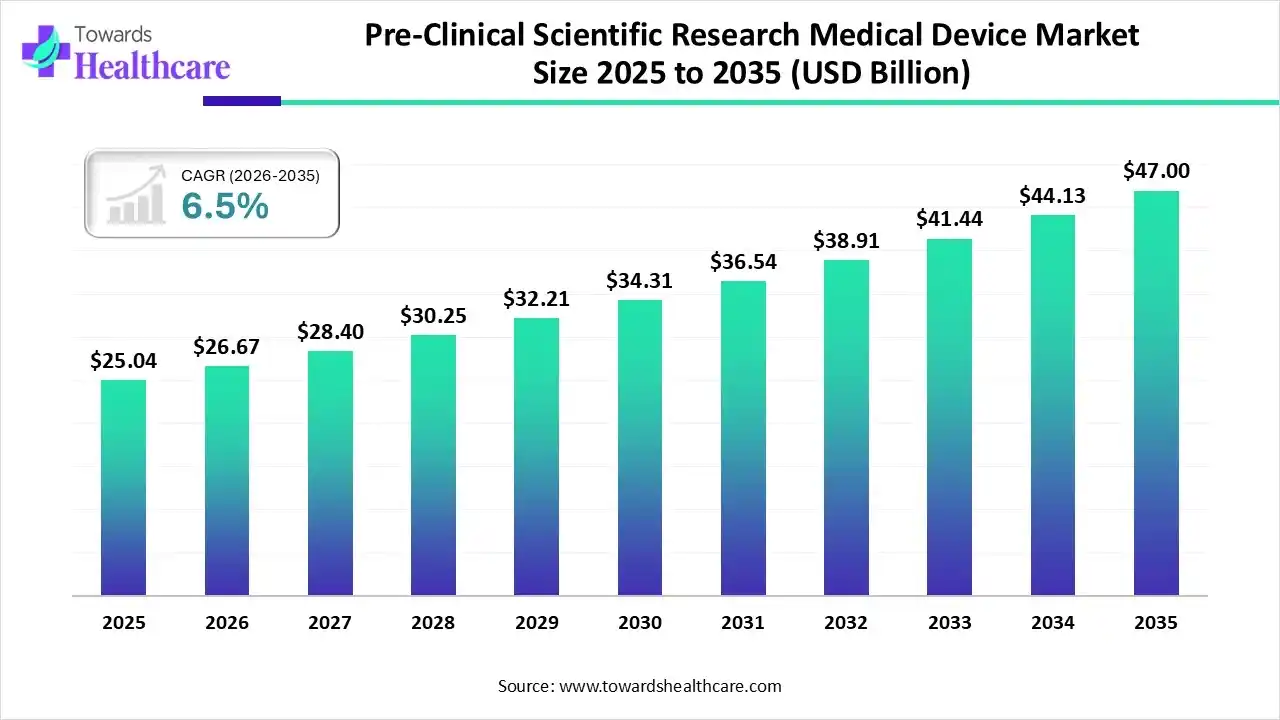

The global pre-clinical scientific research medical device market size was estimated at USD 25.04 billion in 2025 and is predicted to increase from USD 26.67 billion in 2026 to approximately USD 47 billion by 2035, expanding at a CAGR of 6.5% from 2026 to 2035.

")

")

North America pre-clinical scientific research medical device market held a significant share in 2025, due to the presence of leading medical device industries and well-developed R&D infrastructure. The high R&D investments and government funding also increased the adoption of various pre-clinical scientific research medical devices. Growth in healthcare expenditures and drug discovery and development also encouraged their use, while stringent regulatory frameworks also supported their innovations. Additionally, a rise in the adoption of advanced preclinical research technologies and growth in collaborations also contributed to the market growth.

US Market Growth

The U.S. held a share of 86% of the North America pre-clinical scientific research medical device market in 2025, due to the largest R&D spending. Extensive CRO presence and advanced research infrastructure also increased the use of pre-clinical scientific research medical devices. The presence of well-established medical device industries, pharma companies, biotech companies, research institutes, and universities also increased the demand for these devices, where expanding laboratories and government funding also encouraged their use. A rise in drug discoveries, drug development, translational research, and medical device innovations, supported by investments and funding are also created new opportunities.

Canada Market Growth

Canada held a 10% share of the North America pre-clinical scientific research medical device market in 2025 and is expected to grow at the fastest CAGR of 7.1% during the forecast period, due to the expansion of government-funded innovations. Strengthening university research and increasing biotechnology investment are also increasing the demand for pre-clinical scientific research medical devices. Expanding pharmaceutical and biotech companies and the outsourcing of clinical and preclinical research activities are also increasing their adoption rates. Growing collaborations are also accelerating drug discoveries, medical device innovations, and translational research activities, driving their demand.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Pre-Clinical Scientific Research Medical Devices |

| MILabs B.V. | Utrecht, Netherlands | U-SPECT CT and VECTor |

| Revvity, Inc. | Massachusetts, U.S. | IVIS Spectrum CT and Quantum GX2 |

| Bruker Corporation | Massachusetts, U.S. | Albira II and SkyScan 1276 |

| Siemens Healthineers | Erlangen, Germany | Inveon System |

| Mediso Medical Imaging Systems | Budapest, Hungary | nanoSPECT/CT and MultiScan LFER 150 |

| PINGSENG Healthcare | Suzhou, China | Mini SPECT/CT and ClariPET |

| MR Solutions | Guildford, UK | EVOLUTION and MRS*PET/CT Series |

In May 2026, after receiving the award of Medical Device Cybersecurity Partner of the Year at the MedTech World North America 2026 Awards, the Founder and CEO of Blue Goat Cyber, Christian Espinosa, expressed, “We’re honored, but this award really belongs to every manufacturer who decided that patient safety couldn’t wait.” “In medical device cybersecurity, a vulnerability isn’t a data breach; it’s a potential patient harm scenario. That’s why we do this work, and it’s why recognition from the MedTech community means so much. It tells us the industry is taking this as seriously as the stakes demand.”

By Product Type

By Service Type (Testing & Validation)

By Application

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar