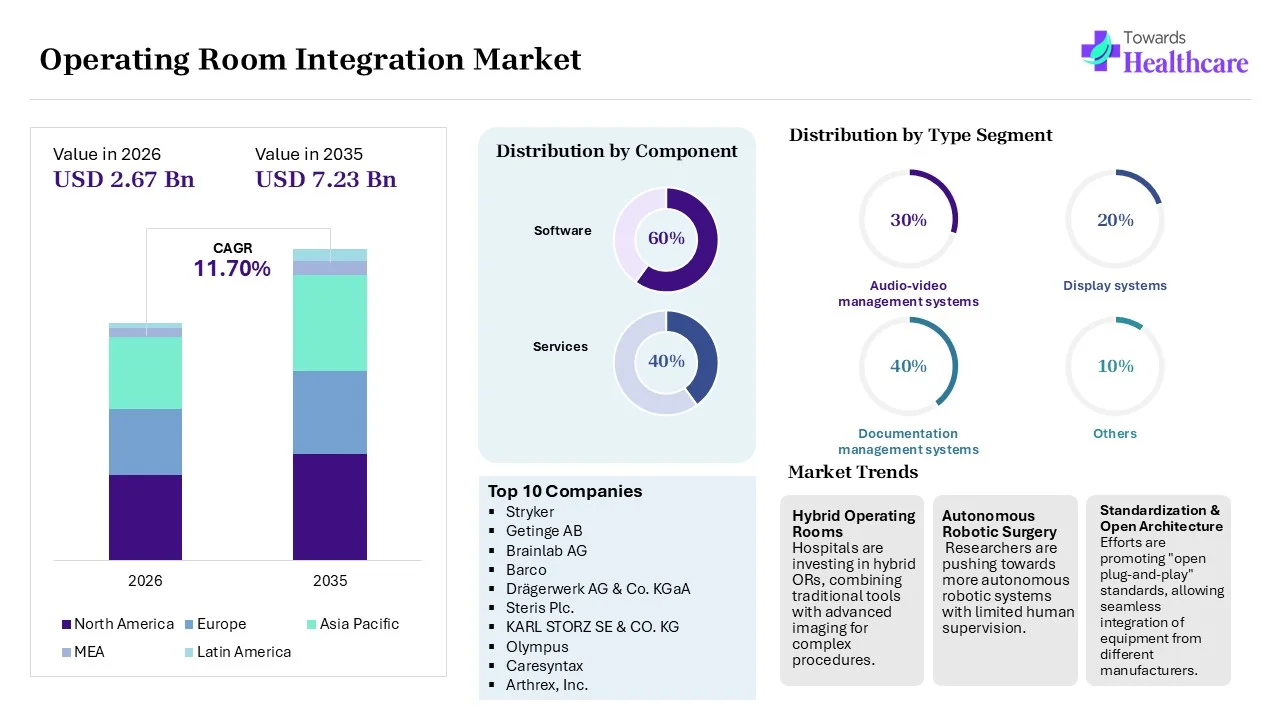

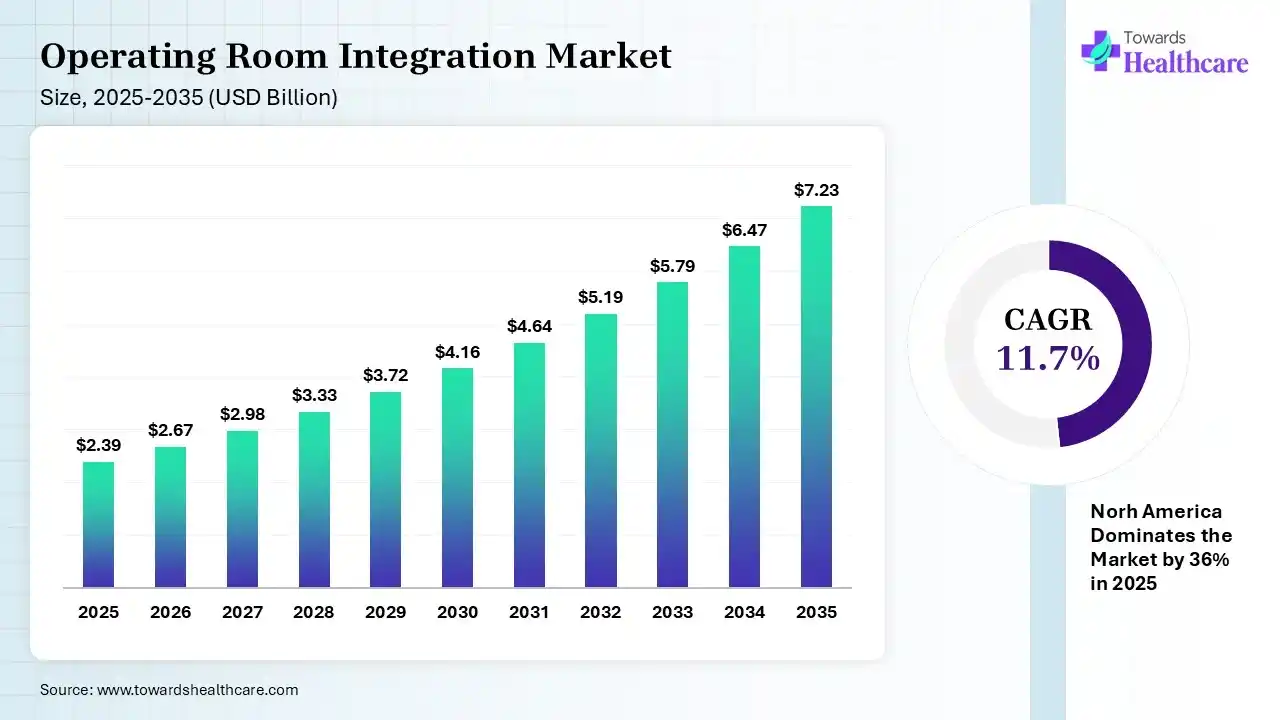

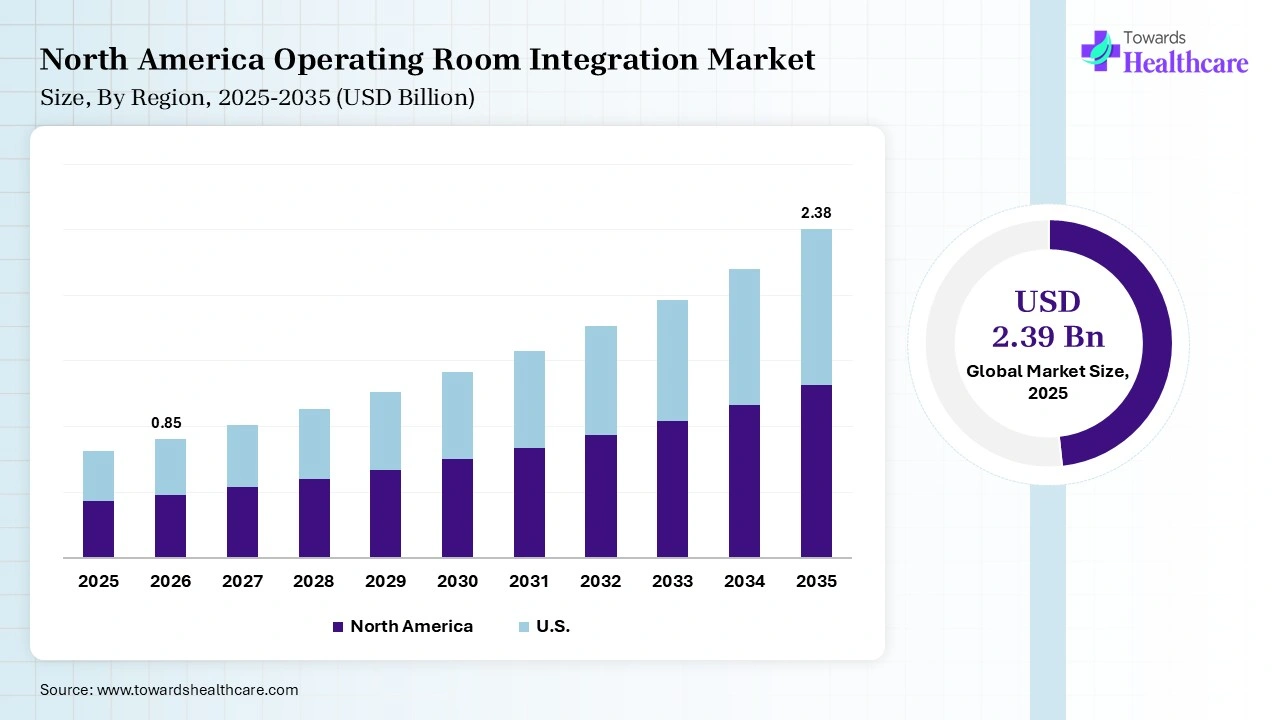

The global operating room integration market size was estimated at USD 2.39 billion in 2025 and is predicted to increase from USD 2.67 billion in 2026 to approximately USD 7.23 billion by 2035, expanding at a CAGR of 11.7% from 2026 to 2035.

The worldwide rise in cases of different kinds of cancers and other chronic conditions is demanding advanced minimally invasive procedures using AI and robotic technologies. Researchers are putting efforts into developing hybrid ORs, AR & VR solutions, and document management systems.

")

The global operating room integration market is putting efforts into driving innovations, including AI-assisted, cloud-connected digital hubs to centralize surgical data, imaging, and device control. Moreover, this covers key advances in 4K/3D imaging and enhanced telemedicine, which raises effectiveness, lowers cognitive load, and expands patient safety. These developments are propelled by growth in minimally invasive surgeries (MIS), the need for robust workflow efficiency, & the wider adoption of sophisticated, integrated imaging/robotic technology.

Ongoing advances in AI solutions are leveraging computer vision for further analysis of CT, MRI, or ultrasound images in real-time, like the TruDi Navigation System, which has combined AI for sinus surgery. Furthermore, AI algorithms are assisting in assessing procedural videos to find anatomical landmarks, detect instruments, & understand specific surgical steps, enabling automated assistance. Additionally, AI innovations are fostering OR management, with automation of scheduling, estimating case turnover times, & improving team communication.

Promoting Hybrid Operating Rooms

Nowadays, many hospitals are actively investing in hybrid ORs, which integrate traditional surgical tools with advanced imaging diagnostics (MRI, CT) to offer complex procedures in a single setting.

Pushing Autonomous Robotic Surgery

Researchers are significantly stepping towards higher levels of autonomy in robotic systems, where robots can operate specific tasks with restricted human supervision.

Expansion of Standardization & Open Architecture

Diverse research efforts are transforming ‘open plug-and-play’ standards for medical devices, which will enable equipment from various manufacturers to work together perfectly, & will omit the current concern of fragmented, proprietary systems.

| Table | Scope |

| Market Size in 2026 | USD 2.67 Billion |

| Projected Market Size in 2035 | USD 7.23 Billion |

| CAGR (2026 - 2035) | 11.7% |

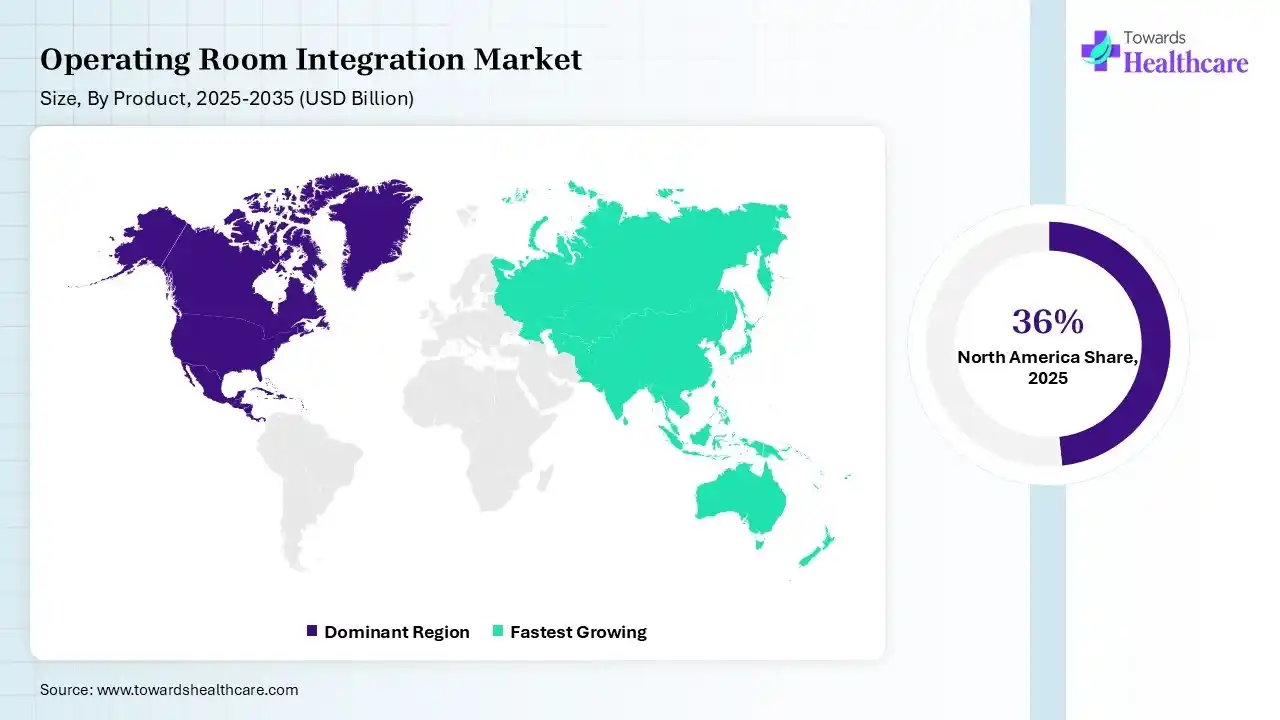

| Leading Region | North America by 36% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Component, By Type, By Application, By End Use, By Region |

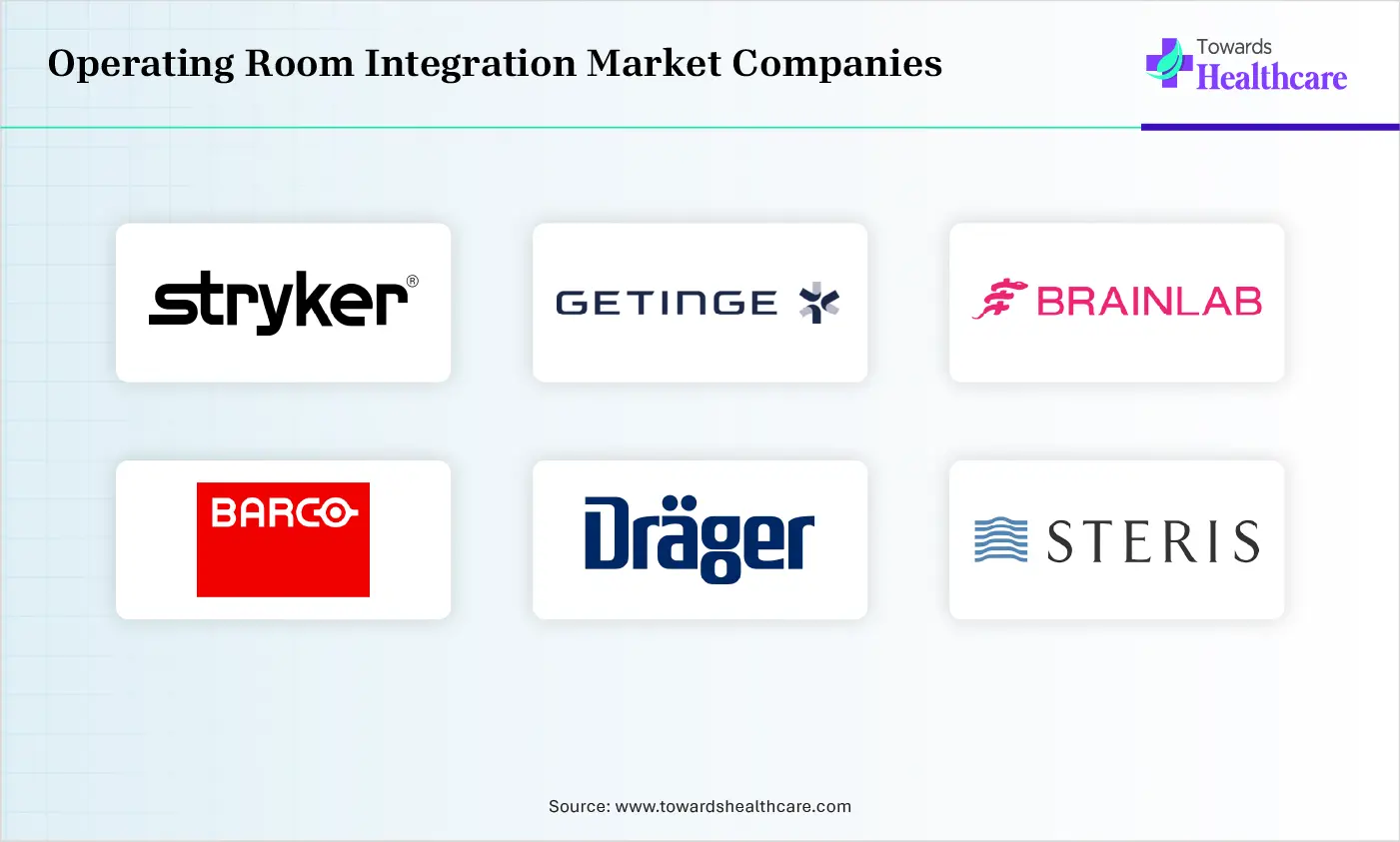

| Top Key Players | Stryker, Getinge AB, Brainlab AG, Barco, Drägerwerk AG & Co. KGaA, Steris Plc., KARL STORZ SE & CO. KG, Olympus, Caresyntax, Arthrex, Inc. |

Which Component Dominated the Operating Room Integration Market in 2025?

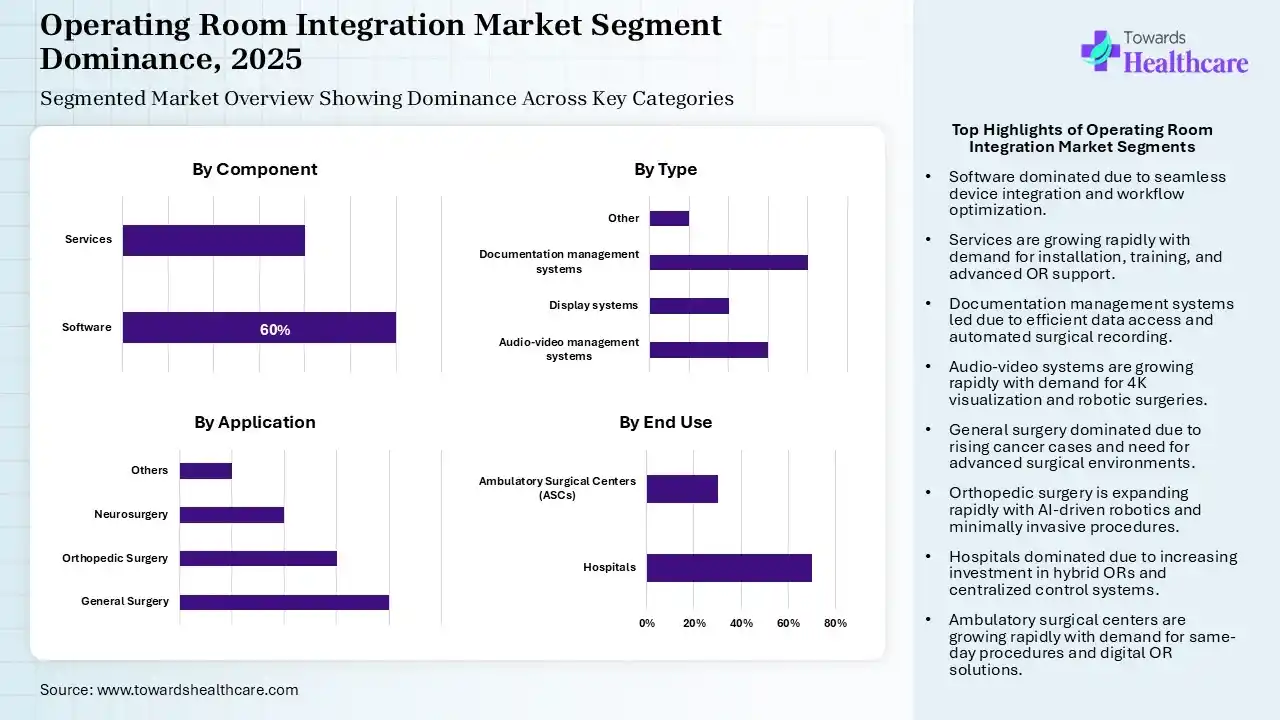

In 2025, the software segment registered dominance in the market by 60%. This is primarily driven by its key role in document management, device integration, and workflow enhancement. Integrated software enables perfect communication between robotic systems, imaging equipment, & patient monitoring. The latest trends are centered on exploring cloud-based data management, voice assistants, 3D imaging, and AI-powered clinical decision support.

Services

On the other hand, the services segment is predicted to expand fastest. This covers installation, training, maintenance, consulting, and system personalization for high-tech operating rooms. Day by day, the market is emphasizing the execution of advanced services, such as AI-enabled analytics, voice-activated controls, like Orva, robotic system standardization, & 3D imaging, which focuses on lowering OR clutter and allowing for telecollaboration.

| Segment | Share 2025 (%) |

| Audio-video management systems | 30% |

| Display systems | 20% |

| Documentation management systems | 40% |

| Other | 10% |

Why did the Documentation Management Systems Segment Lead the Market in 2025?

The documentation management systems segment held the biggest share of the operating room integration market by 30% in 2025. Its dominance is fueled by the fact that these systems allow for perfect access to patient history, high-quality documentation, and expanded communication, propelling efficiency in smart surgical settings. The emergence of advanced systems is automating logging of patient data and surgical video, recording 4K images & video directly into PACS systems without human intervention.

Audio-Video Management Systems

On the other hand, the audio-video management systems segment is anticipated to witness rapid growth. Surging need for laparoscopic & robotic surgeries, demanding sophisticated, high-fidelity visualization and simultaneous display of many imaging sources. Eventual progressions are executing AV-over-IP, which facilitates higher flexibility & scalability. Also, these kinds are assisting in high-fidelity 4K and 4K60 video streaming for enhanced visual accuracy.

Which Application Led the Operating Room Integration Market in 2025?

In 2025, the general surgery segment dominated the market by 40%. Across the globe, massively rising cases of breast, colorectal, and liver cancers, with GI and endocrine disorders, require efficient, tech-enabled surgical environments. One of the revolutionary technologies, AR, is highly employed to superimpose 3D models onto the real-time surgical view during minimally invasive procedures.

Orthopedic Surgery

The orthopedic surgery segment is anticipated to show the fastest expansion. In the growing orthopedic surgical procedures, OR integration solutions, like advanced imaging and navigation, are supporting smaller incisions, which show lowered blood loss, minimal post-operative pain, & rapid recovery. Surgeons are leveraging AI-driven robotic systems, which provide automated, real-time guidance to bolster precision in joint replacements.

How did the Hospitals Segment Dominate the Market in 2025?

In 2025, the hospitals segment captured a major share of the operating room integration market by 70%. The worldwide hospitals are experiencing a surge in demand for hybrid operating rooms, with hospital investment in healthcare IT to boost surgical workflow and data management, fueling the segmental expansion. The broader adoption of centralized control panels enables staff to manage lights, cameras, & equipment from one place, which minimizes setup times & speeds up room turnover between surgeries.

Ambulatory Surgical Centers (ASCs)

In the future, the ambulatory surgical centers (ASCs) segment is estimated to expand fastest. Respective progression is spurred by the accelerating preference for quicker, same-day procedures, escalated adoption of digital OR solutions, and suitable reimbursement policies. Innovative efforts are fostering advanced 3D image guidance, especially mobile C-arms, and 4K surgical displays for MIS.

")

North America led the operating room integration market by 36% due to the growing adoption of minimally invasive surgeries (MIS), rising demand for hybrid ORs, and faster digitization of hospitals. Also, the region has been exploring rigorous systems, which assist several robotic devices within one room, allowing for standardized management of robotic systems & widening collaborative technology.

For instance,

U.S. Market Trends

The U.S. market was a major contributor, as U.S. hospitals are shifting towards vendor-neutral integration systems, enabling equipment from diverse manufacturers to operate together seamlessly. Besides this, the U.S. is actively promoting 3D smart surgical imaging platforms and 4K fiber optic video routing for high-fidelity visualization.

In the coming era, the Asia Pacific is predicted to expand rapidly in the operating room integration market. APAC hospitals are encouraging integrated OR systems to raise efficiency, lower surgical time, and reduce medical errors, which finally lowers healthcare expenditures. Moreover, countries like China are immensely emphasizing domestic production for surgical consumables & robotic arms to decrease reliance on imports, especially for modern surgical robots.

For instance,

South Korea Market Trends

However, South Korea is estimated to expand at a rapid CAGR, with increased adoption of AI in the analysis of vast datasets from surgical equipment for predictive modeling, automated documentation, and real-time anomaly detection. Key hospitals, such as Asan Medical Center and Seoul National University Hospital (SNUH), have strengthened their robotic surgical capabilities.

| Company | Description |

| Stryker | This usually facilitates comprehensive operating room (OR) integration through its iSuite & Connected OR platform. |

| Getinge AB | A company explored Tegris, an OR integration and hospital efficiency software |

| Brainlab AG | Its offerings include a suite of Digital O.R. solutions to centralize information, simplify workflows, & integrate hardware and software into a single user interface. |

| Barco | A firm emphasizes Nexxis video-over-IP platform, which offers uncompressed, near-zero latency video & audio routing. |

| Drägerwerk AG & Co. KGaA | This mainly facilitates different solutions, aiming at interoperability, data management, and workflow automation. |

| Steris Plc. | This company unveiled the HexaVue IP Integration System & HexaVue Focus. |

| KARL STORZ SE & CO. KG | Its offerings cover OR1 NEO, OR1 AIR, OR1 FUSION, etc. |

| Olympus | Their solutions are offered under the EASYSUITE and ENDOALPHA brands. |

| Caresyntax | A company specializes in a vendor-neutral operating room (OR) integration platform. |

| Arthrex, Inc. | They offer various solutions through their Synergy product portfolio. |

Strengths

Weaknesses

Opportunities

Threats

By Component

By Type

By Application

By End Use

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar