Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

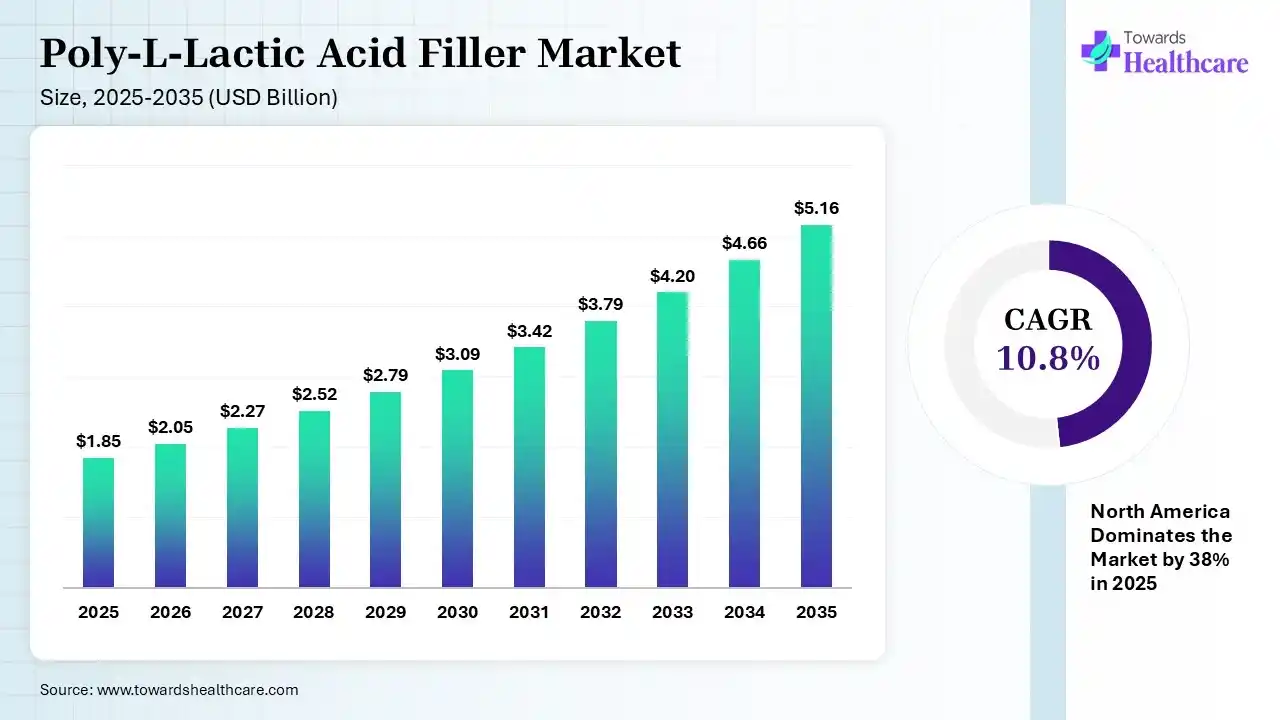

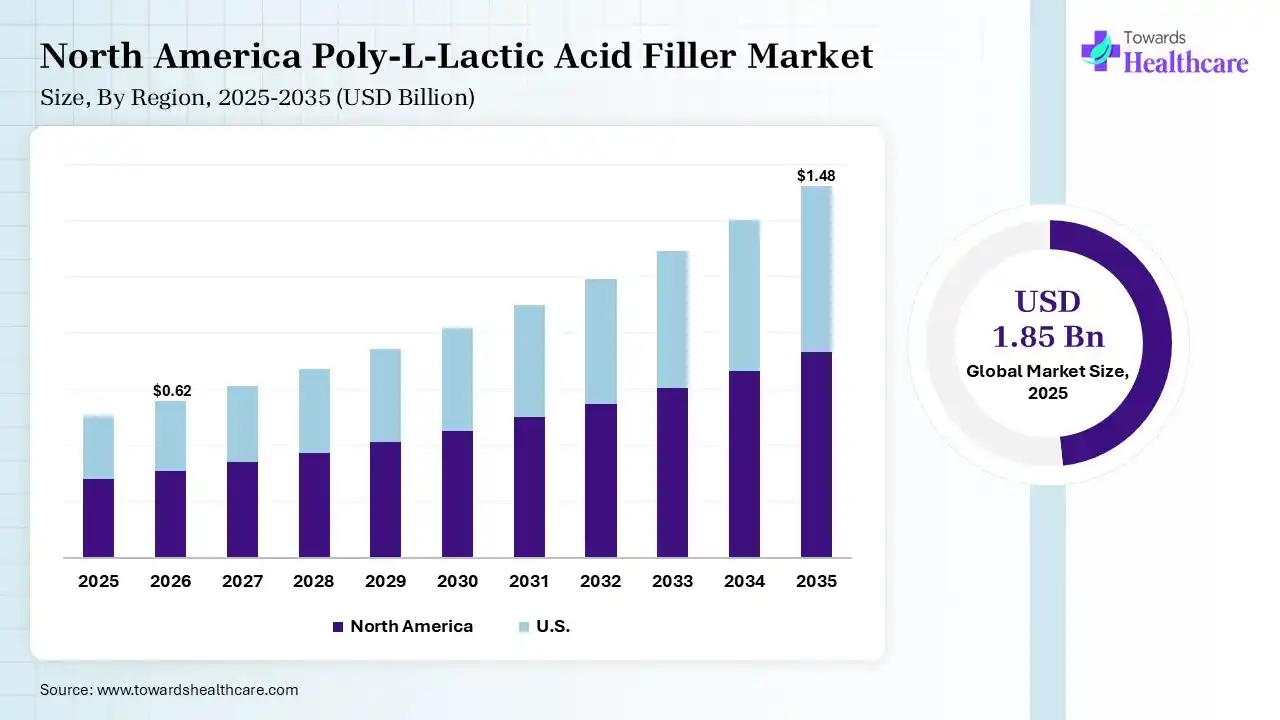

The global poly-l-lactic acid filler market size was estimated at USD 1.85 billion in 2025 and is predicted to increase from USD 2.05 billion in 2026 to approximately USD 5.16 billion by 2035, expanding at a CAGR of 10.8% from 2026 to 2035. The poly-l-lactic acid filler market is growing because it improves skin elasticity and firmness, lowering wrinkles, and encouraging tissue renewal and scar remodelling.

")

The poly-l-lactic acid filler market is increasing, as it is used to create structure, framework, and volume to the face. Poly-l-lactic acid filler is known commercially as Sculptra and Sculptra Aesthetic. PLLA particles initially fill the wrinkles and gradually degrade, stimulating the body's production of novel collagen. Optimum administration of poly-L-lactic acid (PLLA) includes deep dermal injection to lower the incidence of side effects. Poly-L-lactic acid (PLLA) filler, which increases volume and collagen synthesis, is applied for skin rejuvenation. Subcutaneous adipose tissue (SAT) comprises precursors that differentiate into mature adipocytes that secrete adiponectin, which modulates SAT function and increases adipogenesis. Poly-l-lactic acid filler increases adipogenesis and adiponectin in old subcutaneous tissue.

AI-based technology integration has revolutionized product processes by allowing precise control over injection molding parameters, enhancing production efficiency, and reducing waste. AI-based technology is playing a transformative role in filler planning, with novelties like 3D facial volumetric analysis, deep learning-based wrinkle classification , and extrapolative modeling of injection parameters improving both clinical results and training. AI-based algorithms combined with high-frequency ultrasound allow for real-time visualization of anatomical structures, allowing practitioners to evade blood vessels and nerves during PLLA injection.

Recent technological advancement in PLLA porous microsphere group demonstrated significantly rapid onset of action compared to the control, with noticeable collagen deposition as early as week, improved inflammatory cell infiltration, more homogeneous tissue distribution, and significantly less microaggregates upon histological inspection. Modification of PLLA microspheres has effectively sped up their onset of action while lowering nodule formation, thus offering new insights for healthcare applications. PLLA microspheres were also found to be more effective in treating wrinkles and skin folds, and had rare adverse reactions as compared to various fillers.

Regenerative Aesthetics:

PLLA has often been used to manage facial rejuvenation challenges such as cutaneous depressions and static wrinkles, which always involve unsatisfactory facial expression.

Body Contouring Expansion:

Poly-l-lactic acid filler is currently utilized in body management to improve volume, enhance body contour, address skin laxity, lower the appearance of cellulite, and manage scars and stretch marks.

Combination Therapies:

Recent advancements in poly-l-lactic acid (PLLA) filler technology have shifted from simple volume replacement to sophisticated regenerative aesthetics via multifaceted combination protocols.

| Table | Scope |

| Market Size in 2026 | USD 2.05 Billion |

| Projected Market Size in 2035 | USD 5.16 Billion |

| CAGR (2026 - 2035) | 10.8% |

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Application, By End User, By Distribution Channel, By Gender, By Age Group, By Region |

| Top Key Players | Galderma, Sinclair Pharma, Regen Biotech, Dermapharm |

| Segment | Share 2025 (%) |

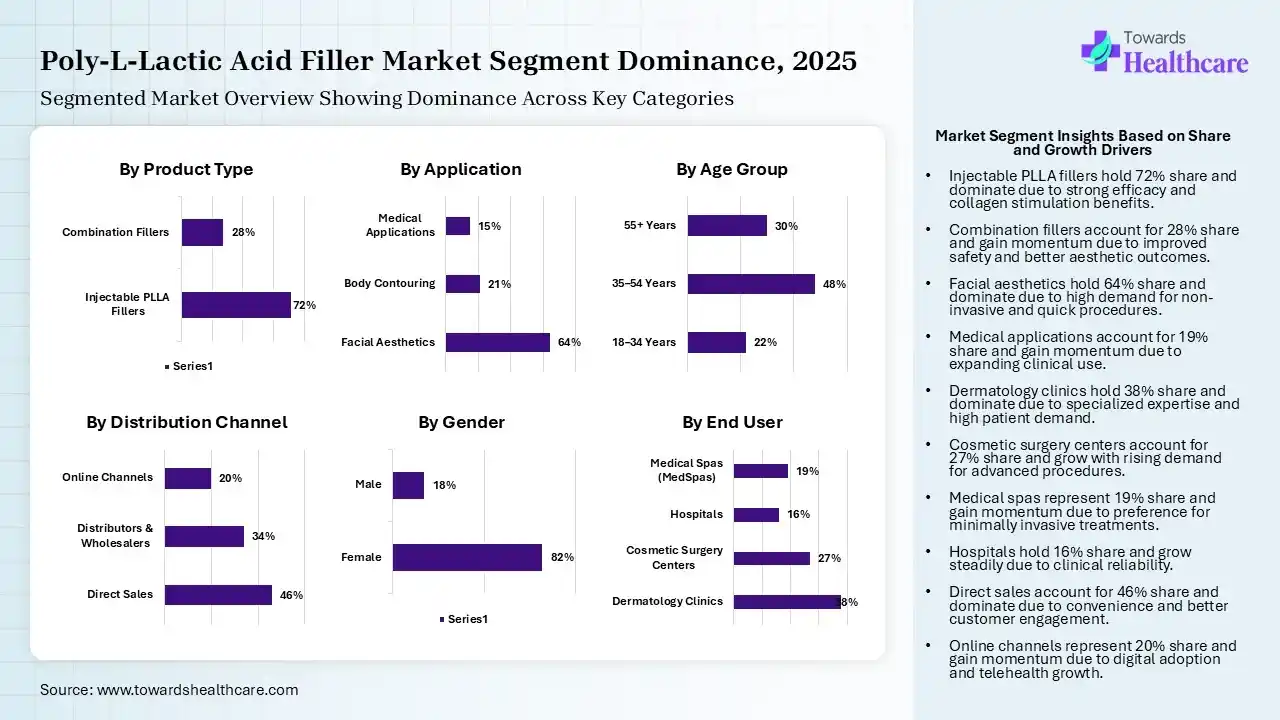

| Injectable PLLA Fillers | 72% |

| Combination Fillers | 28% |

The injectable PLLA Fillers Segment Led the Poly-L-Lactic Acid Filler Market in 2025

The injectable PLLA fillers segment contributed the largest market share of 72% in 2025, as injection of PLLA is a safe and efficient technology for facial volume and contour restoration. Injectable agents, which serve as transient, spaceoccupying fillers, PLLA stimulates nucleogenesis for a natural result. They enhance density, skin firmness, and elasticity, managing deep wrinkles, facial sagging, and hollow regions.

The combination fillers segment held a significant share of 28% in the market, expected to grow at the fastest rate of 12.50% during the forecast period, as the combined PLLA and HA regimen improves facial harmony and skin quality. It potentially enhances the safety profile, lowers the challenges of nodules and granulomas, and offers superior skin elasticity, hydration, and long-term transformation.

| Segment | Share 2025 (%) |

| Facial Aesthetics | 64% |

| Body Contouring | 21% |

| Medical Applications | 15% |

Facial Aesthetics Segment Led the Poly-L-Lactic Acid Filler Market in 2025

The facial aesthetics segment contributed the largest market share of 64%, as facial aesthetics enhances confidence, increases features, provides rapid procedures, and offers long-lasting results. Facial aesthetics treatments are non-surgical and non-invasive, which means limits recovery times and reduce the challenges of side effects. Facial aesthetic treatments do more than smooth out wrinkles; they boost confidence, reduce the aging process, and offer natural-looking outcomes.

The body contouring segment held a significant share of 21% the market, as PLLA works through restoring lost volume and progressively stimulating collagen manufacturing, which enhances skin quality and contour over time. PLLA excites the proliferation and regeneration of cutaneous collagen.

The medical applications segment held a significant share of 19% market in 2025 and is expected to grow at the fastest rate of 12.90% during the forecast period, as poly-l-lactic acid (PLLA) is an absorbable, semi-permanent, injectable implant that restores volume and progressively stimulates collagen development. Poly-l-lactic acid is a filler newly approved by the US FDA for the correction of economic lipoatrophy in patients infected with the human immunodeficiency virus (HIV).

| Segment | Share 2025 (%) |

| Dermatology Clinics | 38% |

| Cosmetic Surgery Centers | 27% |

| Hospitals | 16% |

| Medical Spas (MedSpas) | 19% |

Dermatology Clinics Segment Led the Poly-L-Lactic Acid Filler Market in 2025

The dermatology clinics segment contributed the largest market share of 38%, as PDLLA demonstrates significant benefits in enhancing skin elasticity and firmness, reducing wrinkles, and promoting tissue regeneration and scar remodeling. Poly-d,l-lactic acid (PDLLA) is a biodegradable and biocompatible polymer that has gained significant attention in the field of dermatology.

The cosmetic surgery centers segment held a significant share of 27% in the market, as the comprehensive analysis of outcomes indicates that PLLA is a safe and efficient management for the correction of midfacial volume loss and midfacial contour defects. It restores facial roundness lost via ageing or illness, enhances skin firmness, or softens deep lines and folds.

The medical spas segment held a significant share of 19% of the market, and is expected to grow at the fastest rate of 12.80% during the forecast period, as PLLA works deep in the skin to stimulate the body's own collagen manufacturing, enhancing skin firmness, structure, and elasticity. PLLA stimulates the regeneration and proliferation of cutaneous collagen.

The hospitals segment held a significant share of 16% in the market, as poly-l-lactic acid has significantly increased efficacy compared to hyaluronic acid for the treatment of midfacial volume loss and contour defects. PLLA is a significant, well-tolerated tool for clinicians to serve for the non-surgical augmentation of the ageing face.

| Segment | Share 2025 (%) |

| Direct Sales | 46% |

| Distributors & Wholesalers | 34% |

| Online Channels | 20% |

Direct Sales Segment Led the Poly-L-Lactic Acid Filler Market in 2025

The direct sales segment contributed the largest market share of 46%, as customers are advantaged from direct selling due to the convenience and service it offers, including personal demonstration and clarification of products, home delivery, and substantial satisfaction guarantees. Direct selling provides businesses with superior control over the sales technology and distribution channels.

The distributors & wholesalers segment held a significant share of 34% in the market, as distributors provide better rates, which add up to considerable savings over time, particularly for high-volume medicines used daily in the facility. Extensive distributors significantly utilize a fee- for-solution model.

The online channels segment held a significant share of 20% in the market, expected to grow at the fastest rate of 13.40% during the forecast period, which allows video or phone actions between a patient and their healthcare physician, advantageous both in terms of health and convenience. Telehealth offers access to resources and care for patients in rural areas or areas with provider limitations.

")

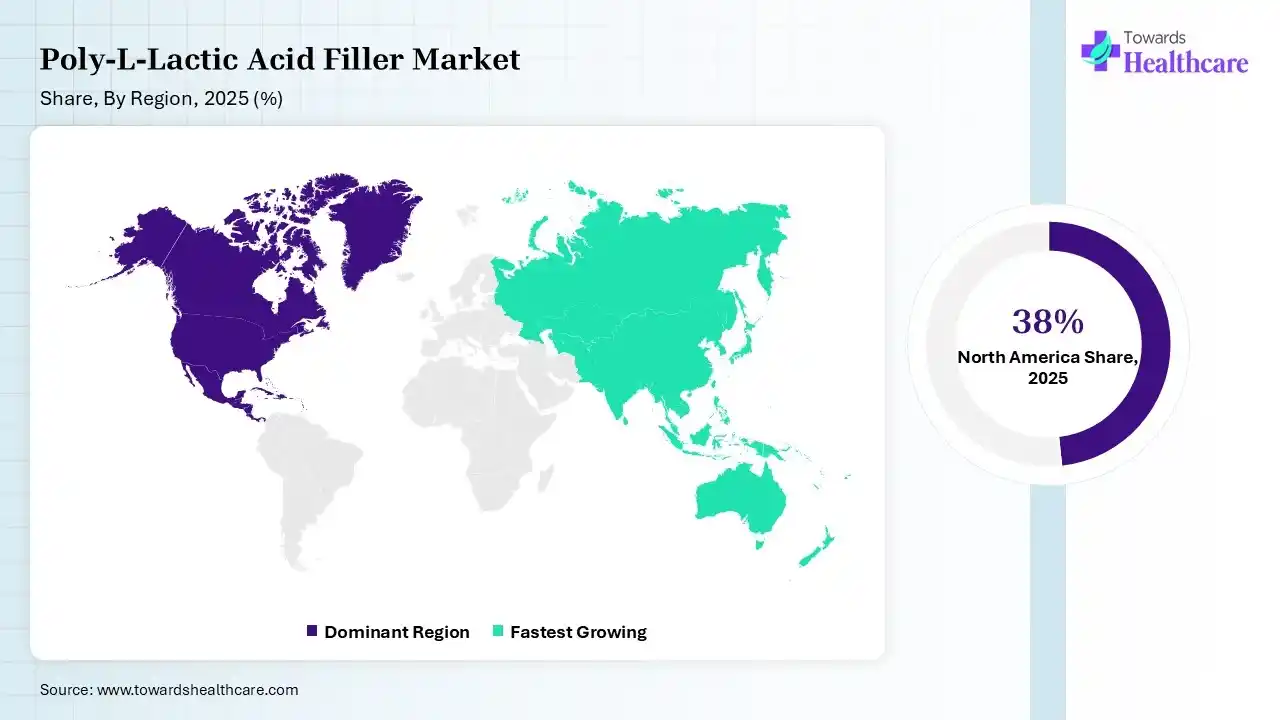

In 2025, North America dominated the poly-l-lactic acid filler market with a share of 38% in 2025, as increasing medical aesthetics, which is the use of technologies or products for a therapeutic indication, is conservatively used for aesthetics. Increasing demand for non-invasive measures because of factors like increased videoconferencing, social distancing, and private recovery choices, which contribute to the growth of the market.

U.S. Market Trends

In the U.S., increasing disposable incomes, growing awareness related to the advantages of non-invasive technologies, and scientific advancements. PLLA is shown to produce continued volumization and wrinkle enhancement over a long period of time, therefore lowering the chances of re-treatment.

Asia Pacific held 24% share of the market and is expected to have the fastest growth with 12.30% CAGR during the forecast period, as the number of individuals aged 80 years or older is expected to triple between 2020 and 2050 to reach 426 million, which causes increasing awareness regarding youth-preserving treatments, which drive the growth of the market.

India Market Trends

In India, the cosmetic clinic sector is experiencing a surge in demand because of the rising popularity of non-surgical beauty technology, which is driving the growing demand for poly-l-lactic acid filler. As disposable incomes rise, more Indians are able to spend on discretionary requirements for aesthetic treatments.

R&D:

Manufacturing Processes:

Patient Services:

| Company | Headquarters | Latest Update |

| Galderma | Switzerland | In February 2025, Galderma, the pure-play dermatology category leader, announced the launch of Restylane Defyne and Restylane Refyne, the first OBT‘based hyaluronic acid injectables ever authorized in Japan. |

| Sinclair Pharma | England | Sinclair continues to differentiate Lanluma with a focus on body contouring and facial rejuvenation. |

| Regen Biotech | South Korea | Regen is the global third and South Korea's first organization to obtain monitoring approval to sell polylactic acid skin filler products. |

| Dermapharm | Germany | Dermapharm Holding SE strives to be recognized as a significant player in the growing Poly-L-Lactic Acid filler. |

| Prollenium Medical Technologies | Ontario | In September 2025, PROLLENIUM is proudly manufactured in Canada under FDA-approved superiority standards and holds a seven-year safety record with its REVANESSE product line. |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Application

By End User

By Distribution Channel

By Gender

By Age Group

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar