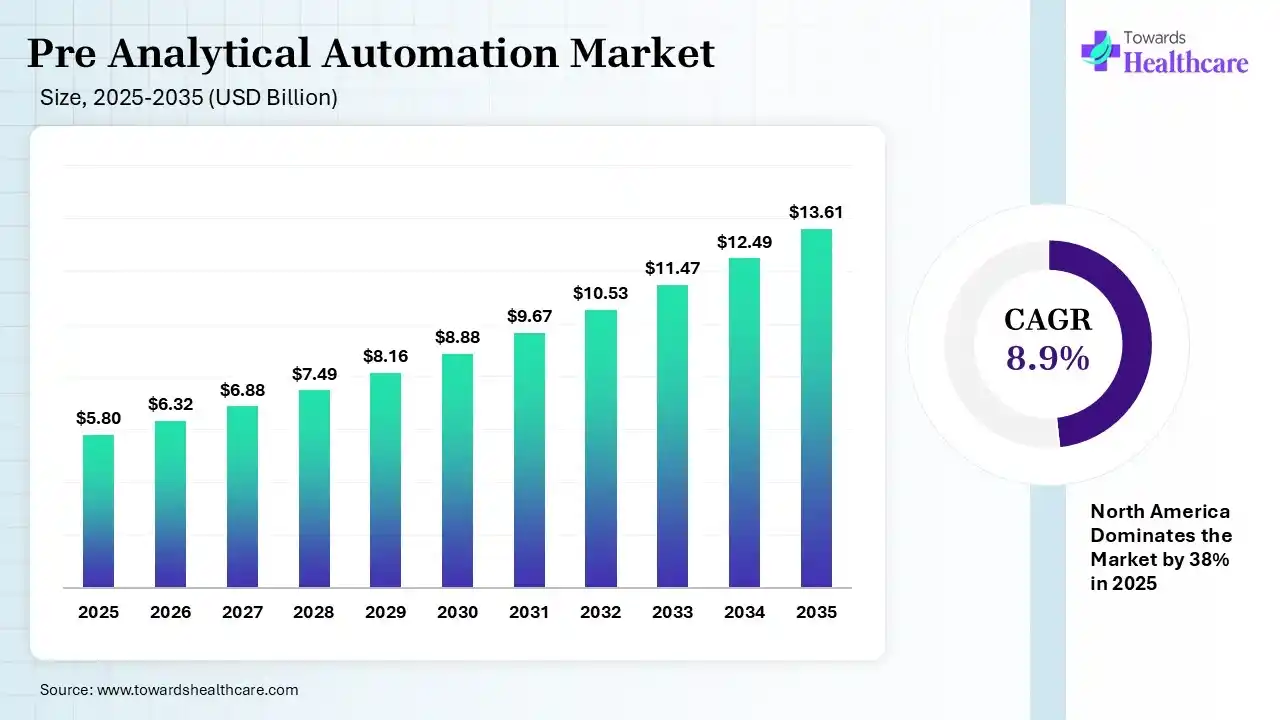

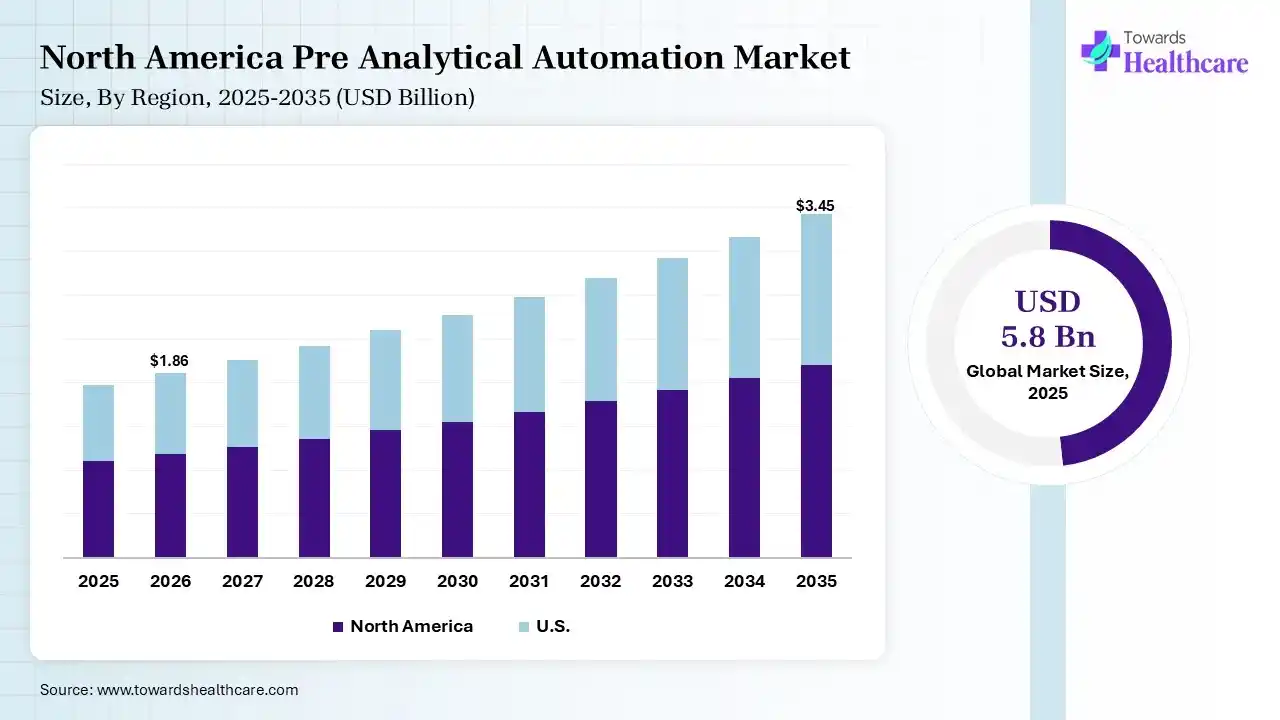

The global pre-analytical automation market size was estimated at USD 5.8 billion in 2025 and is predicted to increase from USD 6.32 billion in 2026 to approximately USD 13.61 billion by 2035, expanding at a CAGR of 8.9% from 2026 to 2035. Globally surging focus on reducing manual errors, streamlining the overall tasks is fueling the need for these advanced & automated systems. Alongside, a notably growing number of chronic disease cases are impacting the demand for innovative automation approaches, which assist clinicians in rigorous & consistent diagnosis.

")

To lower manual errors, the pre-analytical automation market is broadly leveraging robotic, mechanical, & computerized systems, which automate the stages of lab testing that occur before actual analysis, like sample transportation, sorting, centrifugation, and container capping/decapping. The overall adoption is fueled by the emergence of minimal error rates and rising sample volumes, which need expedited automated approaches. In certain areas, labs are facing a shortage of well-trained lab technicians, which fosters higher investment in these systems.

Firstly, AI solutions have a pivotal role in the analysis of images or sensors to assess for hemolytic, icteric, or lipemic (HIL) samples & ensure proper fill volumes. Moreover, the worldwide efforts are using automated vein identification devices & robotic blood collection systems to optimize first-stick success. However, another AI advancement covers ML models to evaluate patterns of previous errors to estimate & find risks, like wrong-blood-in-tube (WBIT) errors in real time.

Encouraging TLA & Track Systems

Gradual developments are reinforcing the use of closed track systems to link sorting, centrifuges, & analyzers to lower human handling.

Transforming Automated Sample Quality Evaluation

The market has been shifting towards sophisticated AI models for real-time segmentation & determination of clots, fibrin, & high HIL levels in centrifuged blood samples.

Projecting Robotic Phlebotomy

The upcoming era will pose the progression of needle-wielding robots by integrating ultrasound imaging & near-infrared (NIR) vein detection to enhance first-attempt success rates in blood drawing.

| Table | Scope |

| Market Size in 2026 | USD 6.32 Billion |

| Projected Market Size in 2035 | USD 13.61 Billion |

| CAGR (2026 - 2035) | 8.9% |

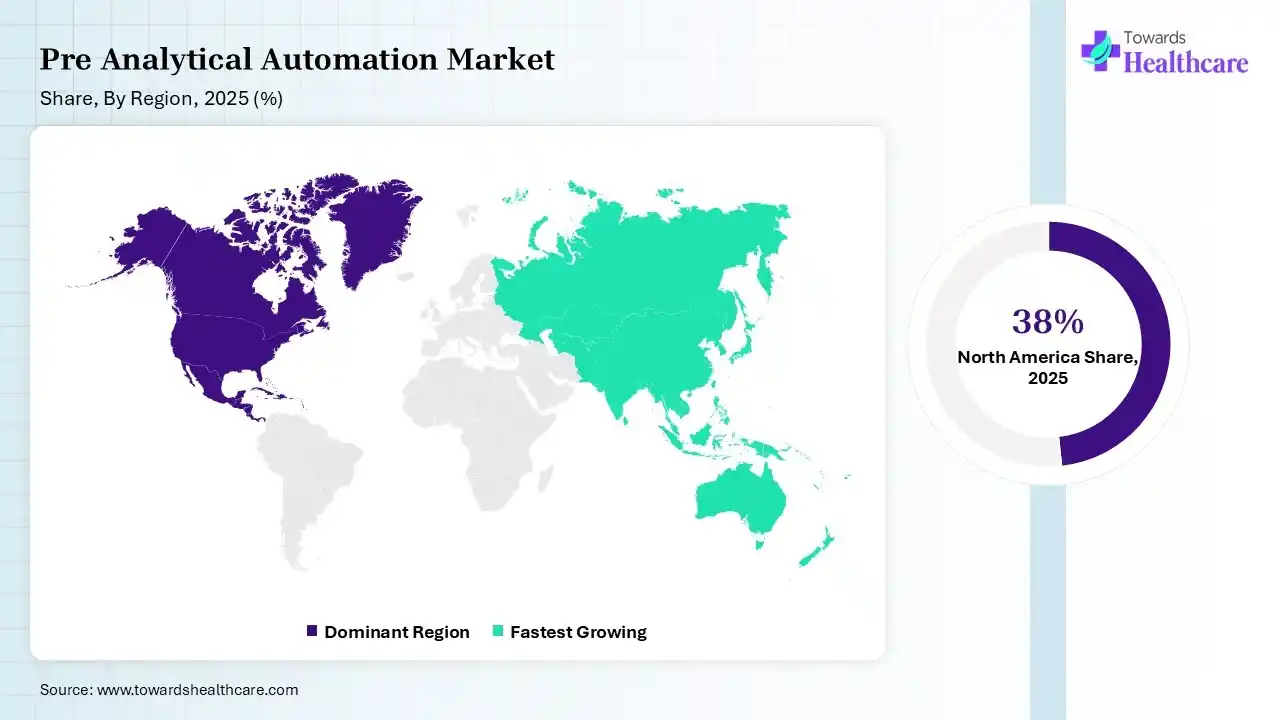

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Application, By End User, By Automation Type, By Region |

| Top Key Players | Beckman Coulter (Danaher Corporation), Abbott, Copan Diagnostics, HAMILTON, Roche, QIAGEN, SHIMADZU, Thermo Fisher Scientific, Inpeco, Sysmex |

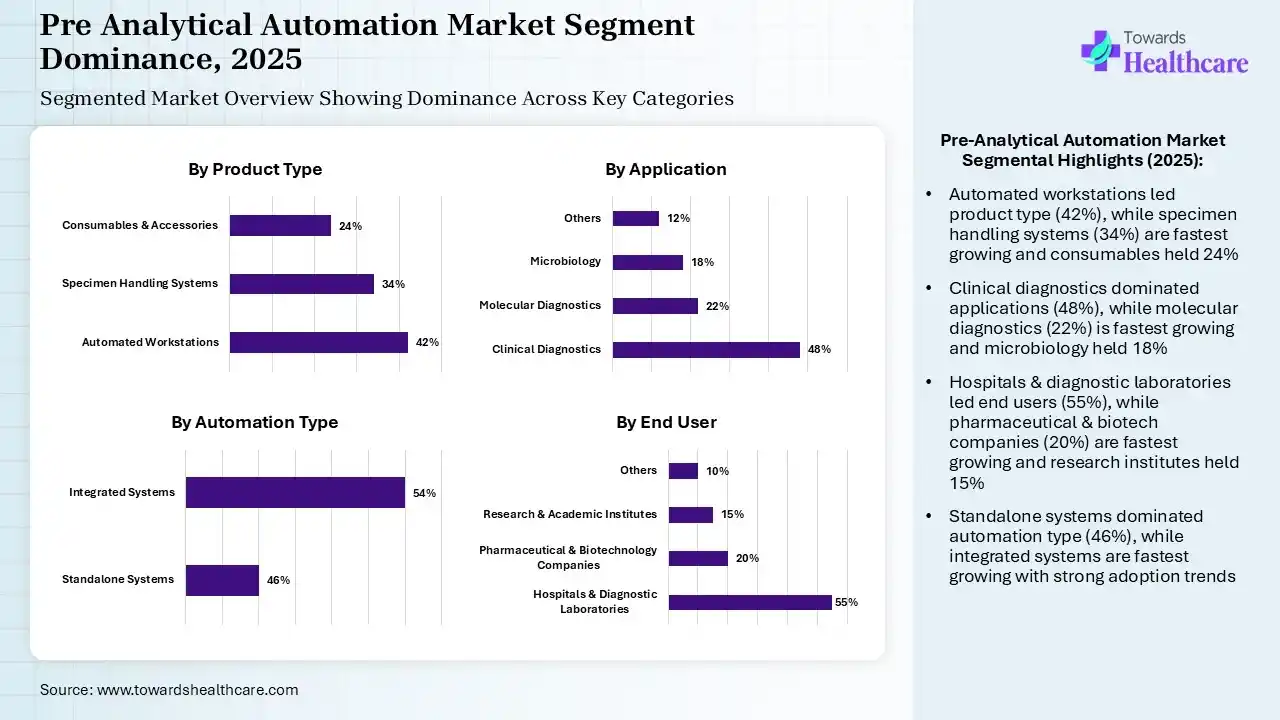

| Segment | Share 2025 (%) |

| Automated Workstations | 42% |

| Specimen Handling Systems | 34% |

| Consumables & Accessories | 24% |

The Automated Workstations Segment Dominated the Market in 2025

In 2025, the automated workstations segment held 42% share of the pre-analytical automation market. Dominance is driven by the urgent need for rapid diagnostic turnaround times, severe limitations of skilled lab technicians, & the reduction of human handling errors. Whereas firms are widely using RFID & advanced barcode scanning to scan 150 cassettes in 30 seconds, tracking, sorting, & directing specimens in real-time.

The specimen handling systems segment captured 34% share in 2025 & is predicted to expand at 9.6% CAGR. This majorly covers sorting, centrifugation, uncapping, and aliquoting, coupled with the surging sample volumes, which demand robust sorting & tracking solutions. A key trend follows the adoption of pathology specimen transfer systems (PSTS), which assist in tracking surgical specimens from removal to pathology.

The consumables & accessories segment held 24% share in 2025, due to the substantial demand from routine lab operations. Labs are pushing automation-validation tips for continuous robotic liquid handling, with alternatives for reduced retention & filtration to prevent contamination.

| Segment | Share 2025 (%) |

| Clinical Diagnostics | 48% |

| Molecular Diagnostics | 22% |

| Microbiology | 18% |

| Others | 12% |

The Clinical Diagnostics Segment Led the Market in 2025

The clinical diagnostics segment was dominant with 48% of the pre-analytical automation market share in 2025. A growing focus on lowering manual errors & escalating volume and complexity of diagnostic tests is driving the need for pre-analytical automation solutions. Emerging innovations are fostering prototypes for automated throat or nasopharynx swabbing by employing vision systems to find facial structure & appropriately place swabs, with minimal cross-infection demerits.

However, the molecular diagnostics segment held the second-largest share of 22% in 2025 & is predicted to expand at 10.4% CAGR. A significant driver is the increasing need for high-throughput testing, especially in oncology & infectious diseases. Persistent developments in microfluidic technology are implementing LAMP (Loop-mediated Isothermal Amplification) technology for accelerated extraction, purification, & detection.

The microbiology segment accounted for 18% share in 2025, due to rising infectious disease cases, which require advanced testing. Leading labs are spurring automated systems, including BD Kiestra & Copan WASPLab to manage inoculation, streaking, & incubation, standardizing the process, with optimized bacterial isolation.

| Segment | Share 2025 (%) |

| Hospitals & Diagnostic Laboratories | 55% |

| Pharmaceutical & Biotechnology Companies | 20% |

| Research & Academic Institutes | 15% |

| Others | 10% |

The Hospitals & Diagnostic Laboratories Segment Was Dominant in the Market in 2025

In 2025, the hospitals & diagnostic laboratories segment dominated with 55% share of the pre-analytical automation market. In terms of surging chronic diseases, these end users are emphasizing improving diagnostic accuracy, safety, & effectiveness by automating sample sorting, centrifugation, labeling, & transport. Broader use of LC-MS/MS in hospitals is supporting sample preparation, with increased accuracy testing.

Moreover, the pharmaceutical & biotechnology companies segment held the second-largest share of 20% in 2025 & is anticipated to show rapid growth at 9.8% CAGR. A major catalyst is a rise in drug discovery activities that need the rapid processing of thousands of compounds. In a biotech firm researchers are leveraging automated sample preparation, like liquid handling & NGS library preparation, to ensure reproducible results.

The research & academic institutes segment captured 15% share, due to the higher growth in research funding, which supports lab automation investments. Alongside, the number of academic labs is widely adopting automation for efficiency, and collaborating with industry further raises demand.

| Segment | Share 2025 (%) |

| Standalone Systems | 46% |

| Integrated Systems | 54% |

The Standalone Systems Segment Dominated the Market in 2025

The standalone systems segment captured 46% share of the pre-analytical automation market in 2025. Primarily, these are specialised, independent instruments created to automate particular, manual, & error-prone steps before sample analysis. Prospective smart standalone systems are using high-definition cameras & laser technology for automatic verification of sample quality, such as the detection of sample volume, hemolysis, icterus, & lipemia (HIL) before testing.

Although the integrated systems segment is estimated to expand rapidly at 10.2% CAGR. Their adoption is impelled by lowering manual handling of tubes, minimal contamination, pre-analytical cell settling & labelling mistakes. The latest advances include integration of modern LIS for real-time tracking & traceability of samples, coupled with AI-enabled expert rules to automate tasks.

")

North America registered dominance with 38% share of the pre-analytical automation market in 2025, due to the presence of well-established healthcare infrastructure & higher diagnostic volumes, with the possession of robust key leaders. The Canadian trend is bolstering Cobas p 312, which offers automated sorting, decapping, & favourable for smaller labs or space-restricted environments.

U.S. Market Trends

With a 30% share & immersive regulatory support, the U.S. market led in 2025. Additionally, the U.S. smaller labs are highly moving towards advanced modular systems, which enable labs to automate sample prep or storage without the huge investment necessary for Total Laboratory Automation (TLA).

In 2025, the Asia Pacific captured 23% share of the pre-analytical automation market & it is anticipated to expand fastest at 9.10% CAGR. This has been gradually progressing due to the rising need for TAT in advancing hospitals & diagnostic labs, which spurs the use of automated, centralized, & decapped sample management approaches. Particularly, China is encouraging smart hospitals with automated tasks, while India is involved in private healthcare investments & lab integrations.

China Market Trends

China is predicted to witness rapid growth at 9.30% CAGR, with accelerating diagnostic volumes. Also, China is aiming at robotic platforms, which automate ultrasonic and reflux extraction, combining with pharmacopoeia standards & also lowering labor-intensive, manual efforts.

Europe accounted for 27% share in 2025 & is estimated to expand at a notable CAGR of 7.50% in the pre-analytical automation market. Nowadays, the region is increasingly advancing the latest diagnostic testing, mainly in chronic diseases, which needs high-throughput, automated sample preparation & sorting systems. In addition, European countries, like Germany & France, are actively investing in modernizing lab infrastructure to meet strong safety & efficiency standards.

On the other hand, numerous German pathology labs are highly utilizing cobots, including the Tissue-Tek SmartConnect, which operate alongside technicians to convey cassettes between processing, embedding, & microtomy stations, with ensured traceability & lowered handling errors. Also, strengthening the use of robotic decappers for automated tube cap removal without the need for tube displacement.

| Company | Description |

| Beckman Coulter (Danaher Corporation) | A firm focuses on its automation solutions, relying on the testing volume & space limitations of the laboratory. |

| Abbott | Its offerings comprise GLP systems Track, ACCELERATOR a3600, AlinIQ INDEXOR, etc. |

| Copan Diagnostics | This usually facilitates groundbreaking sample collection systems & sophisticated, modular robotics for laboratory automation. |

| HAMILTON | It significantly provides automated workstations for primary sample handling, specialized platforms for blood fractionation & forensics, & modern sample storage solutions. |

| Roche | Its offerings cover cobas prime Pre-analytical System, cobas p 512 Pre-analytical System, cobas p 312 Pre-analytical System, etc. |

| QIAGEN | Their portfolio offers high-throughput, fully automated systems for nucleic acid & protein purification. |

| SHIMADZU | A company mainly emphasizes integrated robotic liquid handling with advanced Analytical Intelligence. |

| Thermo Fisher SCIENTIFIC | This has been providing diverse automation solutions, especially for the pre-analytical phase, to simplify sample management. |

| Inpeco | Their portfolio facilitates FlexLab & FlexLab X Total Laboratory Automation (TLA) systems. |

| Sysmex | This company explored the XR-Series or XN-Series for haematology & the CN-Series for hemostasis. |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Application

By End User

By Automation Type

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar