Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

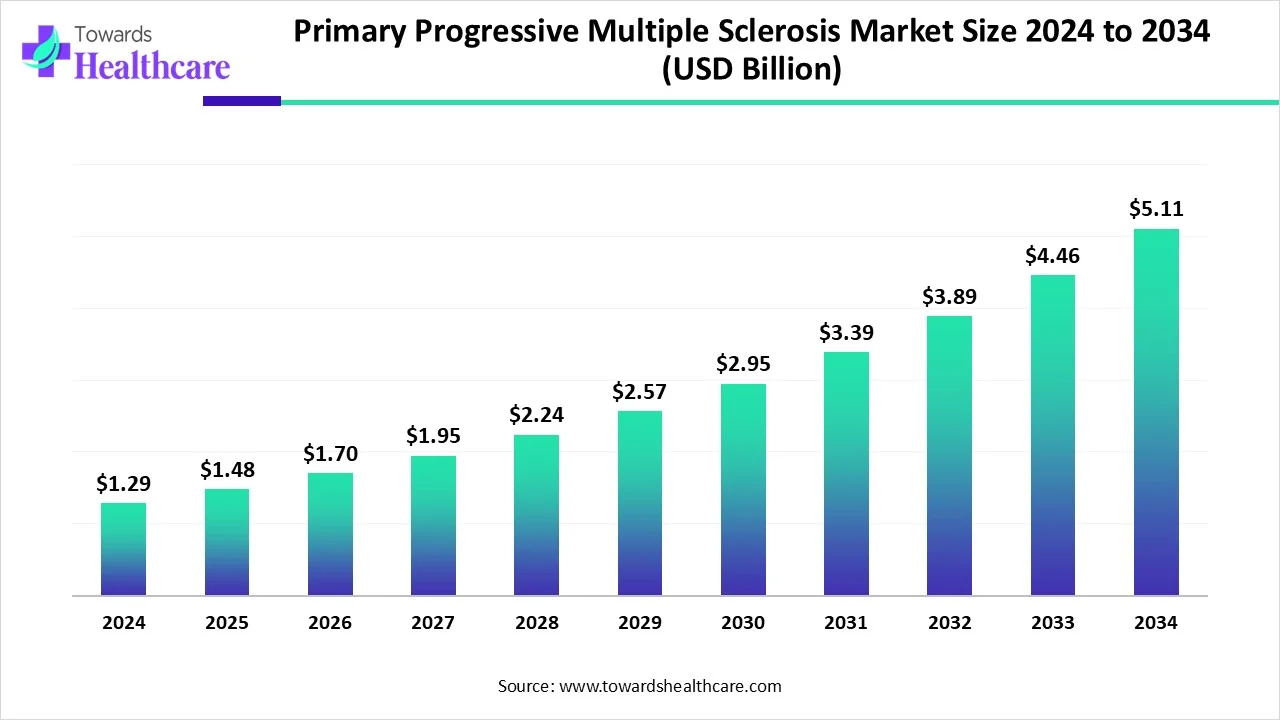

The global primary progressive multiple sclerosis market size is calculated at USD 1.29 in 2024, grew to USD 1.48 billion in 2025, and is projected to reach around USD 5.11 billion by 2034. The market is expanding at a CAGR of 14.84% between 2025 and 2034.

The primary progressive multiple sclerosis market is rapidly growing due to the increasing incidence of PPMS, growing advancement in disease-modifying treatments such as ocrelizumab, the first FDA-approved therapy for primary progressive multiple sclerosis. North America is dominated due to the expansion of PPMS treatment through various distribution channels such as retail pharmacy or e-pharmacy, also the presence of major players drives the growth of the market. Asia-Pacific is fastest fastest-growing segment in the market due to the growing government support and funding for the biotech sector.

| Metric | Details |

| Market Size in 2025 | USD 1.48 Billion |

| Projected Market Size in 2034 | USD 5.11 Billion |

| CAGR (2025 - 2034) | 14.84% |

| Leading Region | North America |

| Market Segmentation | By Drug Type, By Distribution Channel, By Region |

| Top Key Players | MedDay Pharma, Roche, MediciNova, Mapi Pharma, Brainstorm-Cell Therapeutics, Takeda Pharmaceuticals International, Inc., AB Science, Mallinckrodt, Atara Biotherapeutics, F. Hoffmann-La Roche Ltd. |

The primary progressive multiple sclerosis market is rapidly growing due to the early diagnosis and precise treatment of MS are significant for delaying disease progression as much as possible and enhancing patients' results. Through the provision of first- and second-line treatments, doctors support patients with PPMS in preventing exacerbations and reducing the progression of the disease. Workout and patient involvement play a significant role in PPMS treatment. Creating open communication and a robust therapeutic alliance lets physicians lessen patients’ fears and integrate their preferences into an inclusive plan of treatment. Primary progressive multiple sclerosis (PPMS), the rare type of multiple sclerosis (MS), is categorised by a particular course and clinical symptoms, and it is along with a poor prognosis. It needs widespread differential diagnosis and repeated long-term follow-up before accurate recognition.

AI integration in primary progressive multiple sclerosis is driving the growth of the market as the incorporation of AI in the management of PPMS marks a milestone in the medical care sector. Recently, applications of AI in research continue to advance steadily, and breakthroughs are impending at an ever-accelerating pace. As PPMS continues to develop, the integration of AI is more and more essential for ongoing development in diagnosis and treatment, as well as patient outcomes. Current advancements in the sector of artificial intelligence (AI) lead to the enhancements in the classification, detection, and quantification of diagnostic patterns in medical images for a variety of diseases, in specific for PPMS. AI-driven technology has the strength to discover new imaging insights and patterns, offering a deeper understanding of PPMS pathophysiology.

Increasing Multimodal Treatment Approaches

The increasing adoption of multimodal treatment strategies, integrating physical therapy, medication, and dietary support, enhances outcomes for patients with multiple sclerosis. The most effective symptom management model for individuals with MS encompasses a multimodal approach that emphasizes effective communication, patient education, physical modalities and activities, various therapies, and pharmacological treatments. Tailoring treatments to each patient requires early control of symptoms to prevent the onset of recurring symptom cycles, which drives the growth of the primary progressive multiple sclerosis market.

Challenges of High-Cost Treatment

The significant expenses linked to multiple sclerosis are largely due to costly disease-modifying treatments (DMTs). On average, living with multiple sclerosis incurs annual costs of $88,487 per individual. The three largest expense categories are retail prescription medications (54%), clinic-administered medications (12%), and outpatient care (9%), which restricts growth in the primary progressive multiple sclerosis market.

Increasing Approval in Immunomodulatory Strategies for Treatment of Primary Progressive Multiple Sclerosis

Several immunomodulatory strategies with modest yet clinically significant effects have received approval for managing progressive multiple sclerosis, particularly for individuals experiencing active inflammatory disease. The approval process for these medications involved extensive phase 3 trials designed to identify meaningful impacts on disability. Immunomodulators are sanctioned for the long-term treatment of MS. The effectiveness of various new concepts is currently being evaluated in clinical trials, while traditional immunosuppressive agents continue to play a role in MS treatment, thereby opening opportunities in the primary progressive multiple sclerosis market.

By drug type, the approved drugs segment dominated the market in 2024. In the Primary Progressive Multiple Sclerosis Market in 2024, the maximum approved drugs for primary progressive multiple sclerosis support the management of swelling and lessen the number of relapses. It is a significant way to provide accurate treatments for PPMs. This type of drug must undergo the agency's severe assessment procedure, which inspects everything about the drug from the design of clinical trials to the severity of side effects to the conditions under which the drug is manufactured.

The pipeline drugs segment is expected to grow at the fastest rate over the forecast period, as this type of pharmaceutical drug that are currently in development and has not received approval from government bodies such as the U.S. Food and Drug Administration (FDA). These types of drugs are undergoing preclinical and clinical trials to identify efficacy, safety, and the strength benefits of drugs in treating different health conditions. It plays a significant role in evolving medical science and enhancing patient outcomes.

By distribution channel, the retail pharmacies segment is dominant in the primary progressive multiple sclerosis market in 2024, as these types of pharmacies play a vital role in medical care by offering appropriate access to medicines, a broad range of products, and valuable supplementary facilities. In retail pharmacy, chemists work with primary care providers and specialists, adopting a more holistic method to patient care. Walk-in communication with pharmacists permits personalized consultations. They provide answers to questions related to medication interactions, adverse effects, or advice for cost-effective alternatives.

The e-commerce segment is expected to grow at the fastest CAGR over the forecast period, as e-commerce offers lower copays and longer supplies of prescriptions. This is a significant cost advantage, particularly for chronic medicines. Refill and manage prescriptions online or by phone, eradicating the requirement for in-person appointments. This is especially advantageous for patients with busy schedules, mobility challenges, and those living in remote areas. The online pharmacy model provides unparalleled levels of confidentiality and privacy.

North America is dominated in the primary progressive multiple sclerosis market with the largest revenue share, as increasing prevalence of multiple sclerosis likely a mutual effect of earlier diagnosis, due to the improvement and revisions of diagnostic criteria, improved longstanding prognosis related to earlier and more efficient treatment, and advances in the quality of information sources in North America. The medical care systems in North America are advanced due to the strong presence of novel technologies and skilled personnel, which support in enhancing the security systems' performance. A modern, well-known healthcare system, along with access to advanced diagnostics, specialists, and infusion centers for therapies, contributes to the growth of the market.

For Instance,

In the United States, a strong presence of telehealth and connected digital health involvement has established significant efficiency for a broad array of rare diseases, including primary progressive multiple sclerosis. Growing early adoption of new therapies that present patient-centered and holistic care, which increases satisfaction of patient satisfaction, reduces inequalities and lowers health costs, and expands the quality of care and health results by addressing the physiological, biological, social, and cultural requirements of patients. Strong pharmaceutical and biotech companies’ presence, like Novartis, Biogen, and Roche, drives the market growth.

In Canada, increasing healthcare spending, such as in 2024, health research expenditures in the country are expected to have totalled around 7.4 billion Canadian dollars, which is a major driver of the market growth. Growing government support, such as the government announced five-year plans for C$3.5 billion in novel research funding and research infrastructure, also C$600 million in new tax incentives for companies to invest in R&D, which contributes to the growth of the market.

The Asia Pacific region is projected to experience the fastest growth in the primary progressive multiple sclerosis market during the forecast period, due to the significant burden of neurological diseases like multiple sclerosis on low and middle-income countries. Advancements in the delivery of medical care to patients with PPMS in each country of the Asia Pacific contribute to the growth of the market. Many Asia Pacific countries are increasing the adoption of digital health tools, with national strategies and government bodies to achieve digital health options such as PPMS tracking apps and tele-neurology that help continuous disease management, which drives the growth of the market.

Modern research and development activities in China contribute to a better understanding of diseases and medicine targets, which lead to earlier and accurate diagnosis of primary progressive multiple sclerosis. Growing incomes, increasing awareness of health, and an aging population cause fast expansion of the medical sector in this region, also rising demand for healthcare services, medical tools, and pharmaceutical drugs in China drives the market growth.

The growing prevalence of multiple sclerosis (MS) in India is estimated to be 8-9 people per 100,000, which is a major driver of the market growth. PPMS is increasingly diagnosed in India, mostly because of an increase in the number of practicing neurologists and easy and cost-effective availability of magnetic resonance imaging (MRI). India's healthcare sector, increased by government initiatives and private investments, is progressing rapidly, with attractive access, innovation, and socio-economic advancement driving the market growth.

The European region is anticipated to experience considerable growth of the market due as More than 700,000 people suffer from multiple sclerosis (MS) in Europe. Rising technological innovations are renovating healthcare in Europe, with developments like telemedicine, EHRs, AI in diagnostics, robotic surgery, health apps, VR/AR in training, smart hospitals, 5G connectivity, blockchain, wearables, and cybersecurity, which contribute to the growth of the market.

In May 2025, Levi Garraway, M.D., Ph.D., Roche’s Chief Medical Officer, stated, “Fenebrutinib is potent, extremely selective, and the only reversible BTK inhibitor presently in Phase III trials for multiple sclerosis, and we look forward to seeing the first of those outcomes later this year.” (Source - Roche)

By Drug Type

By Distribution Channel

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar