Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

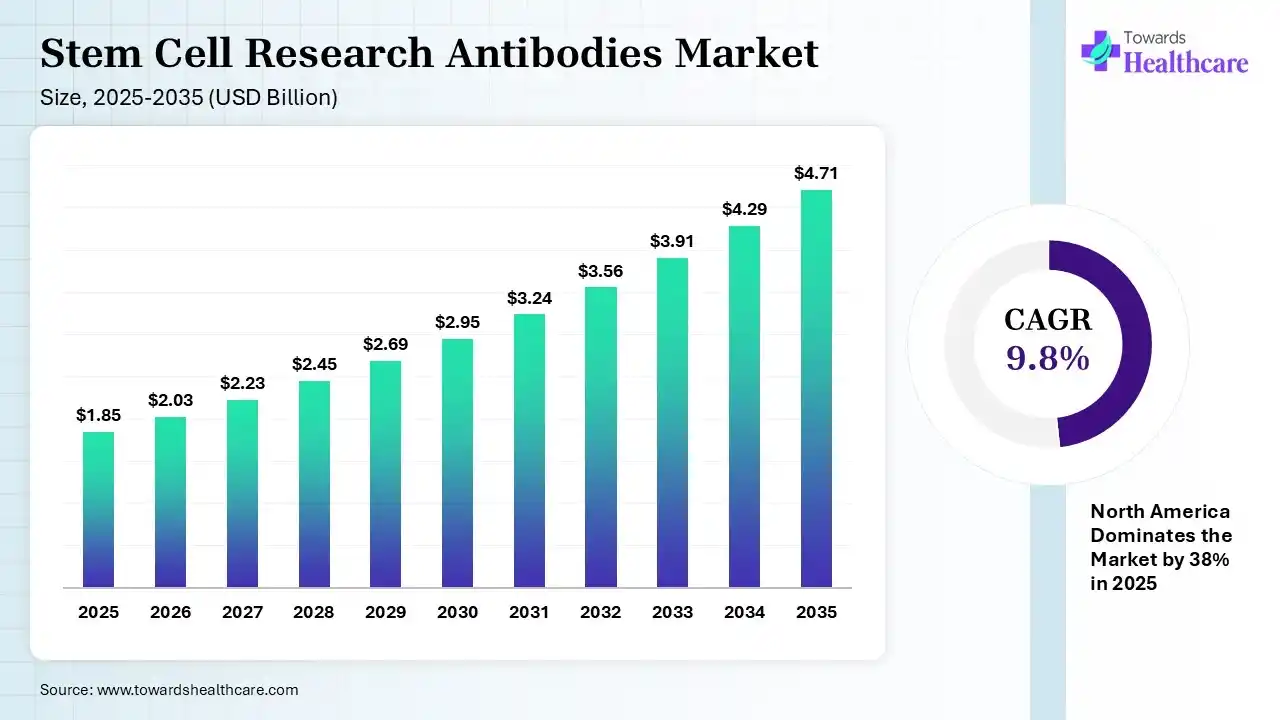

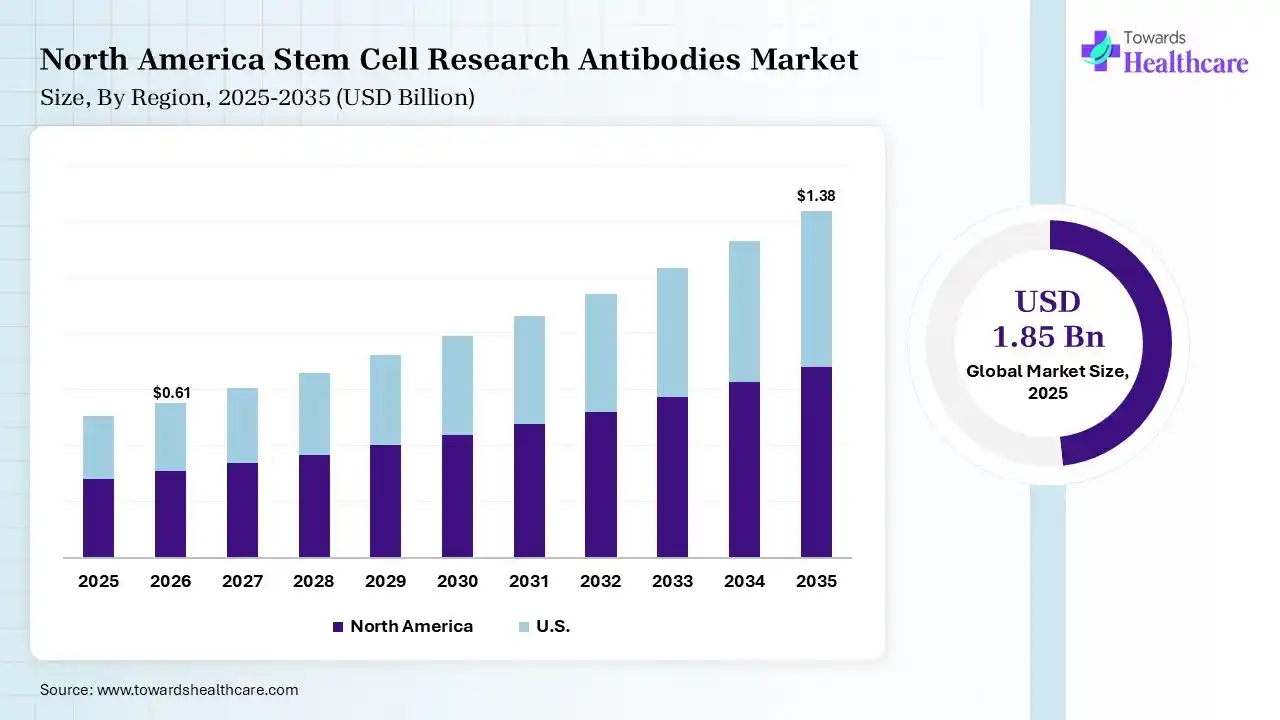

The global stem cell research antibodies market size was estimated at USD 1.85 billion in 2025 and is predicted to increase from USD 2.03 billion in 2026 to approximately USD 4.71 billion by 2035, expanding at a CAGR of 9.8% from 2026 to 2035. Growing R&D activities globally are increasing the adoption of stem cell research antibodies. Increasing demand for personalized medicines, early disease diagnosis, technological innovations, and new product launches are also enhancing the market growth.

")

The stem cell research antibodies market is driven by the growing chronic disease burden and increasing demand for regenerative medicines. The stem cell research antibodies refer to the specialized antibodies utilized for the identification, detection, and study of stem cells. They also help in stem cell isolation, sorting, differentiation, and characterization, which promotes their use in R&D activities involving regenerative medicine development, drug discovery, and disease research.

Stem cell research antibodies are specialized antibodies used to identify, isolate, characterize, and monitor stem cells by targeting specific cellular markers during regenerative medicine and biomedical research. The stem cell research antibodies market is expanding due to increasing investments in stem cell biology, regenerative medicine, and advanced drug discovery. Growing demand for precision cell characterization and rising research into cancer, neurological disorders, and tissue regeneration are further driving adoption. Technological advancements, including highly specific monoclonal antibodies, multiplex immunoassays, single-cell analysis, and AI-enabled biomarker discovery, are improving research accuracy and reproducibility. A key market trend is the integration of stem cell research with gene editing and personalized medicine. Future opportunities lie in next-generation antibody development, organoid research, cell therapy manufacturing, and translational medicine, supported by expanding clinical research programs and continuous innovation in life science technologies.

AI plays an important role in the stem cell research antibodies market by promoting the prediction of antibody structure and its optimization. It also helps in the identification of new stem cell biomarkers, analysis of large datasets, stem cell image analysis, and accelerated drug screening. AI also helps in improving the antibody specificity and development of personalized stem cell therapies.

Blooming Regenerative Medicine

Increasing interest in regenerative medicine is driving its demand and innovations, promoting a rise in the adoption of stem cell research antibodies. They help in the identification of stem cells suitable for tissue repair or organ regeneration.

Expanding R&D

The growing collaboration and funding are increasing the R&D activities focused on drug discovery and personalized medicines. This increases the use of stem cell research antibodies for drug screening, toxicity testing, and identification of stem cell markers, and promotes integration with genomics.

Flourishing Technologies

The expanding technological advancements are driving the development of antibody production technologies such as custom antibody production platforms, high-throughput screening systems, and AI/ML-powered antibody design platforms. They help in the development of more precise and sensitive antibodies.

| Table | Scope |

| Market Size in 2026 | USD 2.03 Billion |

| Projected Market Size in 2035 | USD 4.71 Billion |

| CAGR (2026 - 2035) | 9.8% |

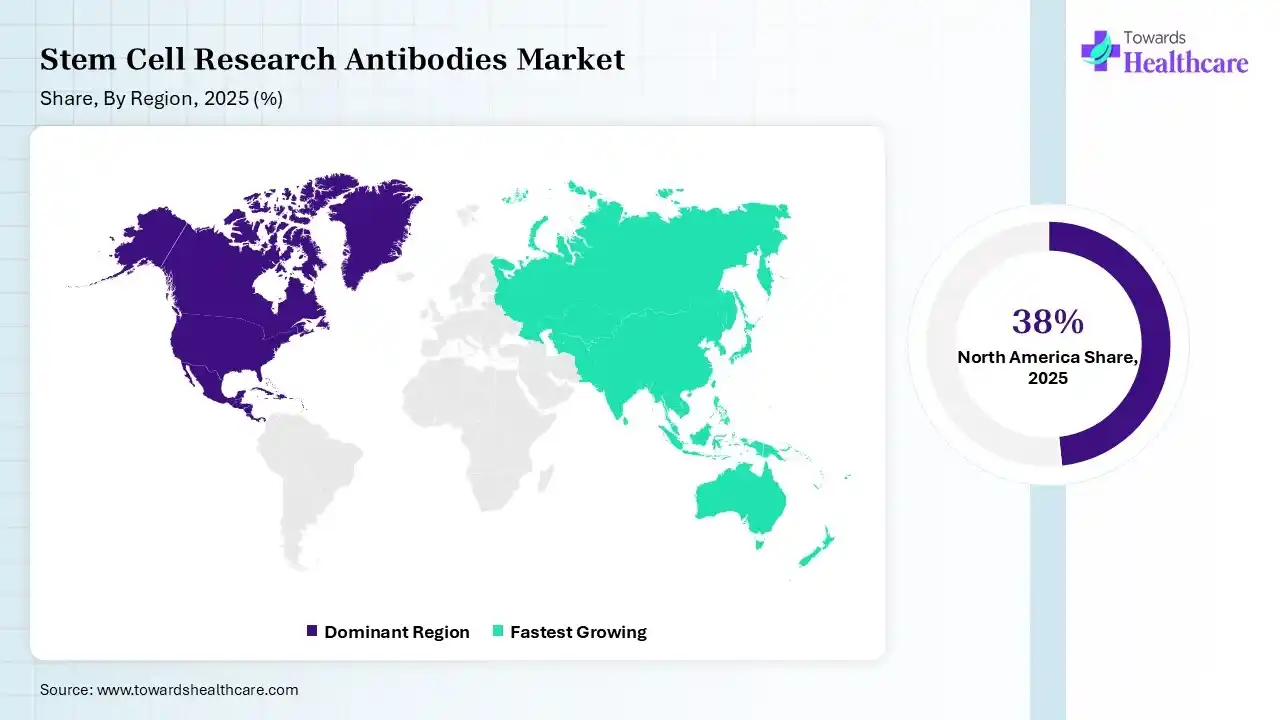

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Source, By Application, By Technology, By End User, By Region |

| Top Key Players | Thermo Fisher Scientific, BD Biosciences, Abcam (Danaher), Cell Signaling Technology, Merck KGaA, Bio-Rad Laboratories, Bio-Techne, Santa Cruz Biotechnology, STEMCELL Technologies, Miltenyi Biotech |

")

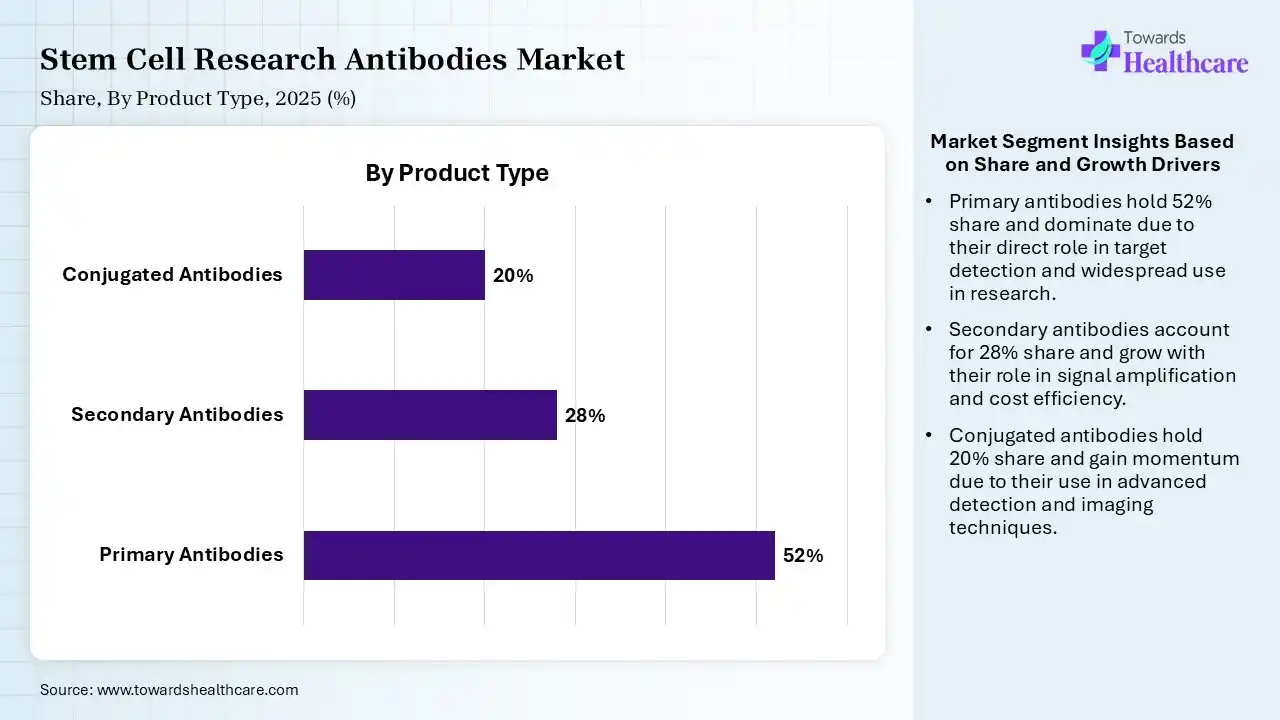

| Segment | Share 2025 (%) |

| Primary Antibodies | 52% |

| Secondary Antibodies | 28% |

| Conjugated Antibodies | 20% |

The Primary Antibodies Segment Dominated the Market With 52% in 2025

The primary antibodies segment led the stem cell research antibodies market with 52% share in 2025, due to their accuracy in stem cell detection and characterization. They also supported advanced biomarker identification in regenerative medicine. Growth in their use in translational research also fueled their demand.

The secondary antibodies segment held the second-largest share of 28% of the market in 2025, as it enhances signal amplification in assays, improving sensitivity. They are widely used in multi-step detection techniques. Growing adoption in lab automation also boosts its usage.

The conjugated antibodies segment held 20% of the stem cell research antibodies market share in 2025 and is expected to witness the fastest growth with a CAGR of 11.40% during the forecast period, driven by rising demand for high-throughput screening. It also enables multiplexing and real-time imaging applications. Their increasing integration in advanced diagnostics also drives their expansion.

")

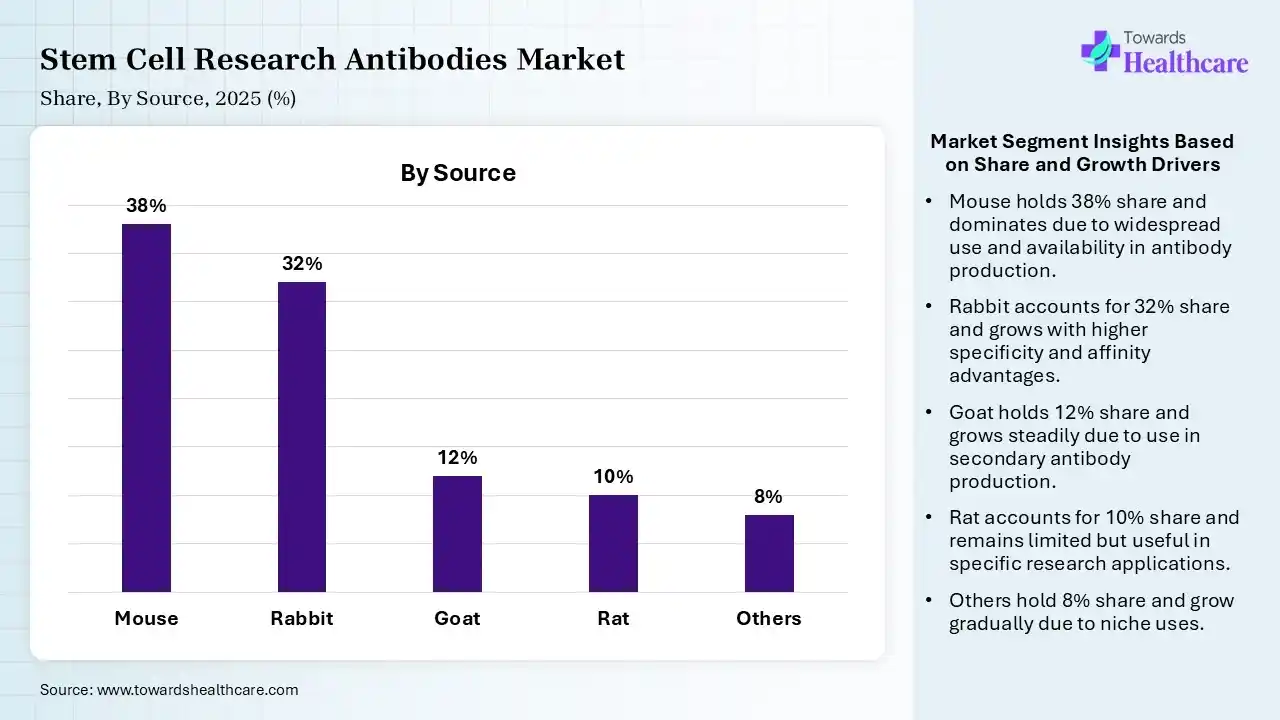

| Segment | Share 2025 (%) |

| Mouse | 38% |

| Rabbit | 32% |

| Goat | 12% |

| Rat | 10% |

| Others | 8% |

The Mouse Segment Dominated the Market With 38% in 2025

The mouse segment accounted for the highest revenue share of 38% of the stem cell research antibodies market in 2025, as they offered high specificity and consistency for monoclonal antibodies. They were widely used in hybridoma technology. Their strong presence in research laboratories also increased their demand.

The rabbit segment held the second-largest share of 32% of the market in 2025 and is expected to show the highest growth with a CAGR of 10.60% during the forecast period, as it provides higher affinity antibodies with better sensitivity. Increasing preference in stem cell signaling studies also boosts their growth. Expanding use in advanced assays also supports their adoption.

The goat segment held 12% of the stem cell research antibodies market share in 2025, as they are commonly used for secondary antibody production. They also support broad compatibility across assays. Additionally, their immunodetection applications also drive their stable demand.

The rat segment held 10% of the market share in 2025, due to its increasing application in specific stem cell markers. They are also useful for niche immunological studies. Moreover, growing specialized research needs are also increasing their adoption rates.

")

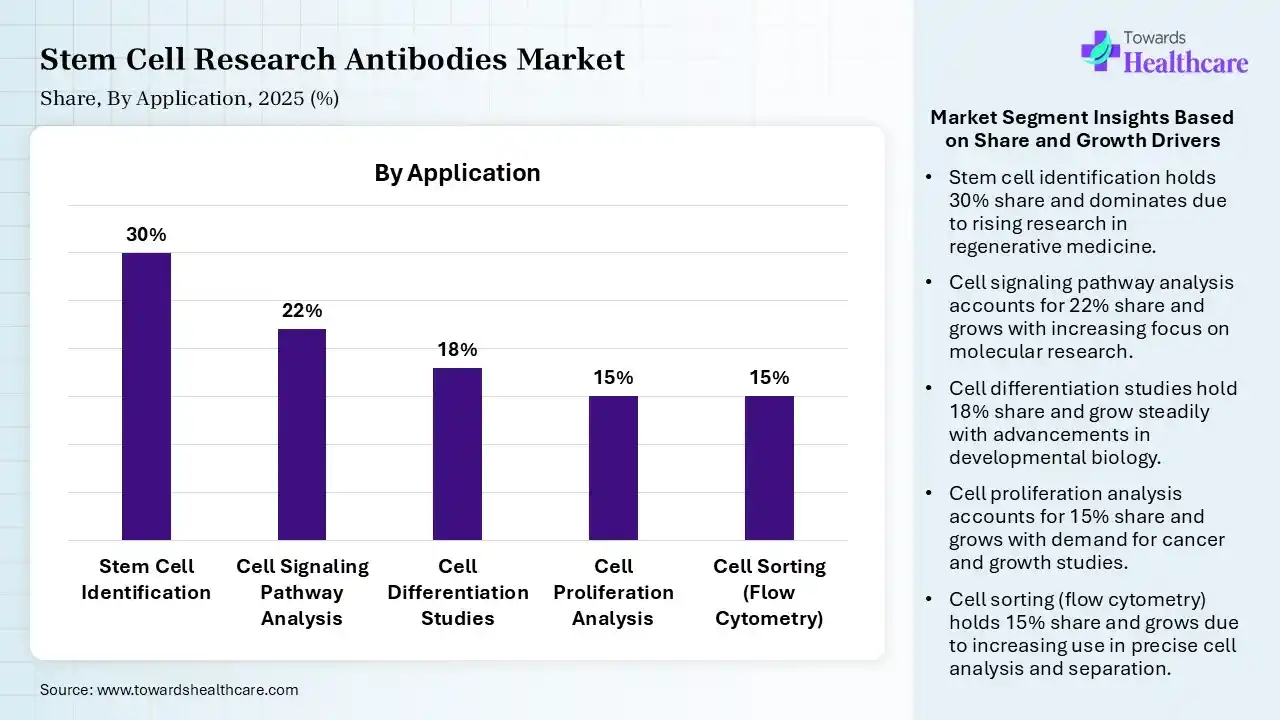

| Segment | Share 2025 (%) |

| Stem Cell Identification | 30% |

| Cell Signaling Pathway Analysis | 22% |

| Cell Differentiation Studies | 18% |

| Cell Proliferation Analysis | 15% |

| Cell Sorting (Flow Cytometry) | 15% |

The Stem Cell Identification Segment Dominated the Market With 30% in 2025

The stem cell identification segment held a major revenue share of 30% of the stem cell research antibodies market in 2025, as stem cell research antibodies were essential for isolating and characterizing stem cells. They were also used to support regenerative medicine advancements. Growth in research funding also fueled their demand.

The cell signaling pathway analysis segment held the second-largest share of 22% of the market in 2025, as stem cell research antibodies enable the understanding of molecular mechanisms in stem cells. They are essential for drug discovery and development. Growing interest in targeted therapies also drives their usage.

The cell differentiation studies segment held 18% of the stem cell research antibodies market share in 2025, driven by the increasing use of stem cell research antibodies in monitoring stem cell maturation processes. It also supports tissue engineering applications. Rising clinical research also enhances their adoption.

The cell sorting (flow cytometry) segment held 15% of the market share in 2025 and is expected to expand rapidly with a CAGR of 11.20% during the forecast period, as stem cell research antibodies enable the precise isolation of stem cell populations. Increasing use in personalized medicine also accelerates their demand. Advances in cytometry technologies also boost their adoption.

")

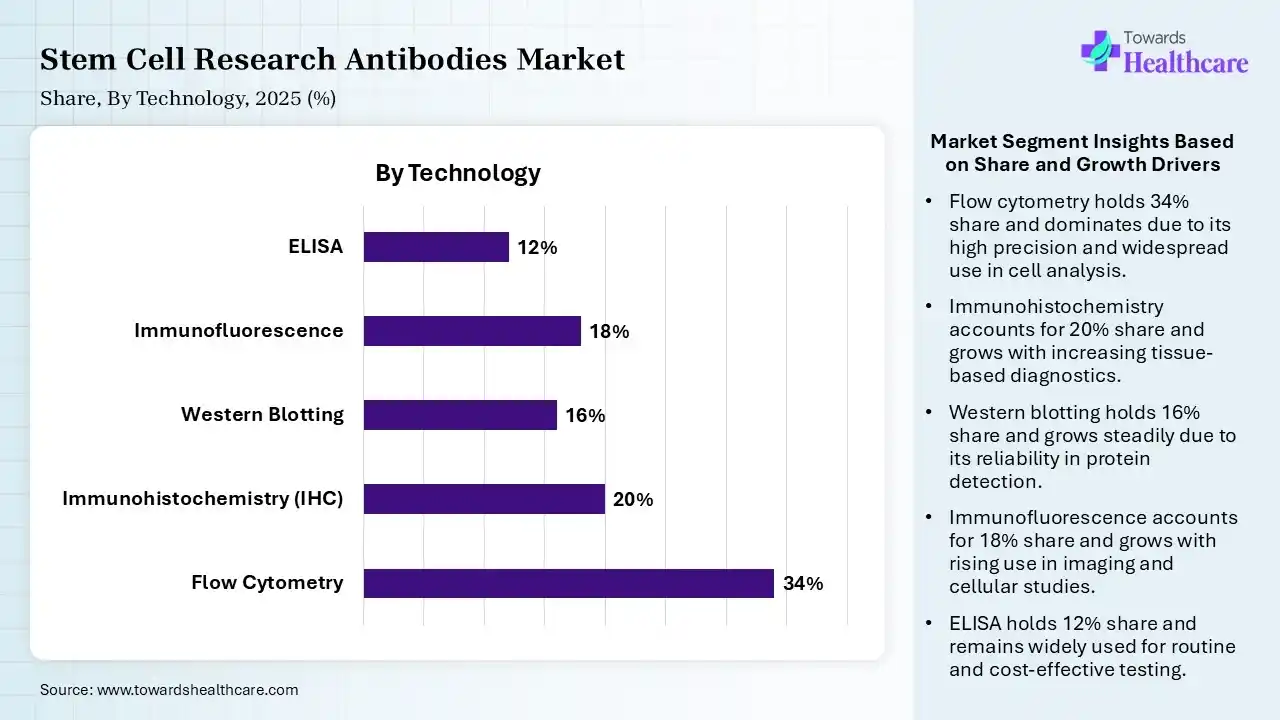

| Segment | Share 2025 (%) |

| Flow Cytometry | 34% |

| Immunohistochemistry (IHC) | 20% |

| Western Blotting | 16% |

| Immunofluorescence | 18% |

| ELISA | 12% |

The Flow Cytometry Segment Dominated the Market With 34% in 2025

The flow cytometry segment held the largest revenue share of 34% of the stem cell research antibodies market in 2025, as it enables high-throughput cell analysis and sorting. They were critical for stem cell characterization. Additionally, technological advancements have also increased their widespread adoption.

The immunohistochemistry (IHC) segment held the second-largest share of 20% of the market in 2025, as it provides spatial localization of stem cells in tissues. They are also being used in regenerative and cancer research, driving the demand for antibodies, which also supports clinical diagnostics. Stable demand in pathology labs also increases their use.

The immunofluorescence segment held 18% of the market share in 2025 and is expected to grow with the fastest CAGR of 11.00% during the forecast period, as it enables visualization of cellular structures and markers. Increasing use in live-cell imaging also boosts their growth. Rising demand in advanced research also drives their adoption.

The western blotting segment held 16% of the stem cell research antibodies market share in 2025, due to high use for protein detection and validation. They are also used for basic stem cell research. Additionally, as it is an established technique, it also contributes to its consistent demand.

")

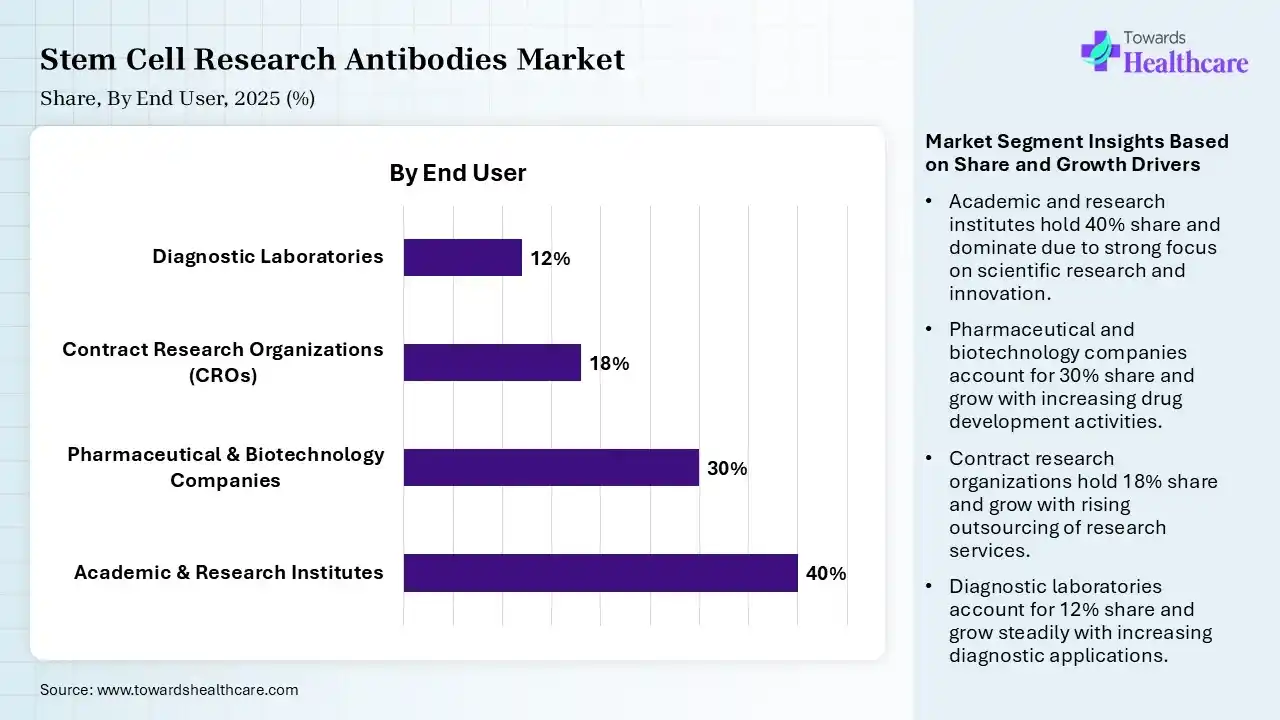

| Segment | Share 2025 (%) |

| Academic & Research Institutes | 40% |

| Pharmaceutical & Biotechnology Companies | 30% |

| Contract Research Organizations (CROs) | 18% |

| Diagnostic Laboratories | 12% |

The Academic & Research Institutes Segment Dominated the Market With 40% in 2025

The academic & research institutes segment contributed the biggest revenue share of 40% of the stem cell research antibodies market in 2025, as they are the major contributors to stem cell research advancements. High funding from governments also supported their growth. Extensive use of antibodies in basic research also promoted their use.

The pharmaceutical & biotechnology companies segment held the second-largest share of 30% of the market in 2025 and is expected to gain the highest share with a CAGR of 10.4% during the forecast period, due to increasing investment in regenerative medicines. The growing development of biologics also drives demand for high-quality antibodies. The increasing pipeline of stem cell therapies also fuels their growth.

The contract research organizations (CROs) segment held 18% of the stem cell research antibodies market share in 2025, due to the growing outsourcing of research activities. They also provide cost-effective research solutions, increasing the use of stem cell research antibodies. Expanding clinical trials also support their growth.

The diagnostic laboratories segment held 12% of the market share in 2025, as it utilizes antibodies for disease detection and monitoring. The growing role of personalized medicine also increases its use. Stable demand from clinical diagnostics is also promoting their acceptance rates.

")

North America dominated the stem cell research antibodies market with 38% in 2025, due to the strong presence of biotech firms and research institutes. High R&D investment and a favorable regulatory environment also supported the growth of stem cell research antibodies. Rise in collaborations and technological advancements also contributed to the market growth.

U.S. Market Trends

The U.S. leads global research output and funding, which drives the adoption of stem cell research antibodies. Advanced infrastructure and strong industry-academia collaborations also enhance their growth. Well-developed industries, regulatory framework, and investments also promote their use and advancements.

Canada Advanced Stem Cell Research Through Scientific Excellence

Canada stem cell research antibodies market is witnessing significant growth due to strong government funding for regenerative medicine, expanding stem cell research programs, and increasing collaborations between academic institutions and biotechnology companies. Rising investment in cell therapy development, advanced biomedical research infrastructure, and growing adoption of high-specificity research antibodies are accelerating innovation. These factors are strengthening Canada’s position as a leading center for stem cell research and life sciences.

Asia Pacific held 22% share of the stem cell research antibodies market in 2025 and is expected to grow at the fastest CAGR of 11.20% during the forecast period, due to the rapid expansion of research infrastructure. Increasing government funding and biotech industries also drive their growth. Large patient population and government support are also enhancing the market growth.

China Market Trends

The strong government initiatives in China are supporting the growth of stem cell research antibodies. The presence of a large research base and patient volume also increased their demand. Expanding biotech industries, clinical trials, and R&D investments are also accelerating their innovations.

India Emerges as a Rising Hub for Stem Cell Research Innovation

India’s stem cell research antibodies market is growing significantly due to expanding regenerative medicine research, increasing biotechnology investments, and rising academic and clinical research activities. Growing demand for advanced research tools, supportive government initiatives for life sciences, and rapid expansion of biopharmaceutical research are driving market growth. Additionally, increasing collaboration between research institutes and biotechnology companies is accelerating innovation and strengthening India’s Stem cell research ecosystem.

R&D:

Clinical Trials and Regulatory Approvals:

Patient Support and Services:

| Companies | Headquarters | Stem Cell Research Antibodies |

| Thermo Fisher Scientific | Waltham, U.S. | Invitrogen antibodies |

| BD Biosciences | Franklin Lakes, U.S. | BD Pharmingen/BD Horizon |

| Abcam (Danaher) | Cambridge, UK | RabMab |

| Cell Signaling Technology | Danvers, U.S. | Validated Antibodies |

| Merck KGaA | Darmstadt, Germany | Millipore Antibodies |

| Bio-Rad Laboratories | Hercules, U.S. | PrecisionAb |

| Bio-Techne | Minneapolis, U.S. | R&D Systems Antibodies |

| Santa Cruz Biotechnology | Dallas, U.S. | Primary Antibodies |

| STEMCELL Technologies | Vancouver, Canada | Stem Cell Research Antibodies |

| Miltenyi Biotech | Bergisch Gladbach, Germany | REAfinity Recombinant Antibodies |

In June 2026, "Universal donor cell therapies represent one of the most critical frontiers for regenerative medicine, yet scalable manufacturing and immune compatibility remain major barriers for the field," said Rama Modali, CEO of REPROCELL USA Inc.

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Source

By Application

By Technology

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar