Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

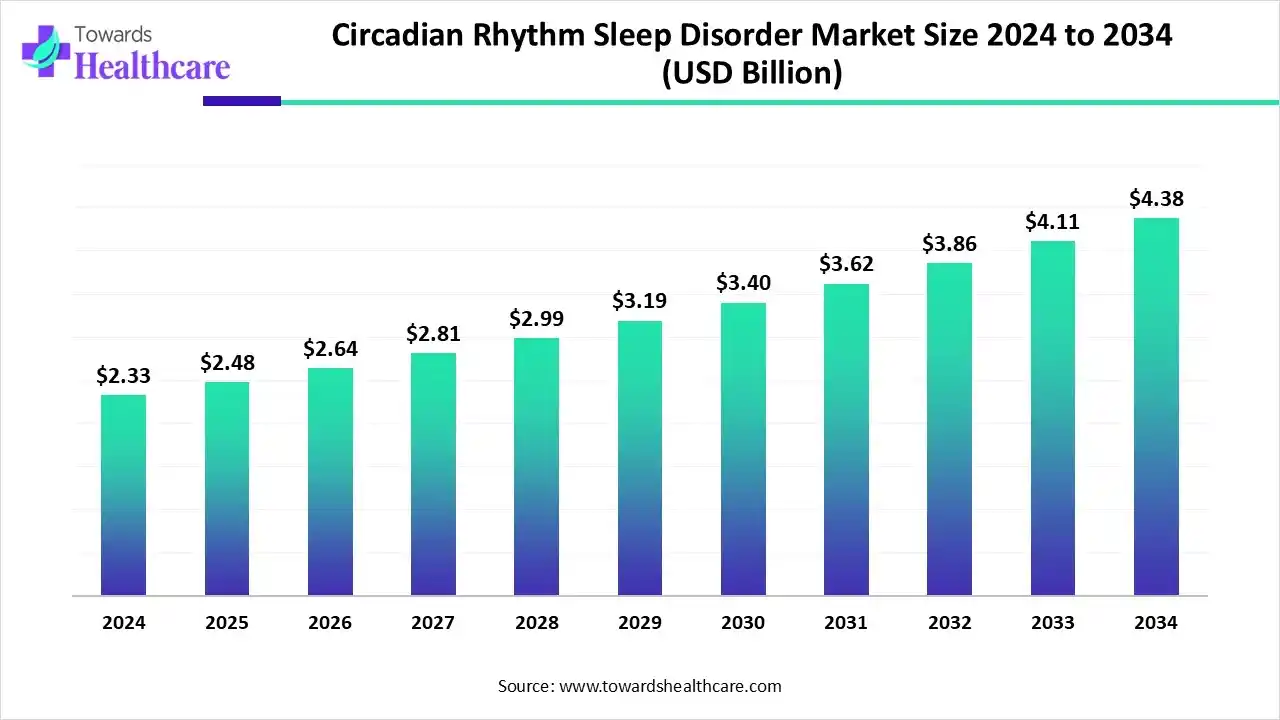

The global circadian rhythm sleep disorder market size is calculated at US$ 2.48 billion in 2025, grew to US$ 2.65 billion in 2026, and is projected to reach around US$ 4.69 billion by 2035. The market is expanding at a CAGR of 6.56% between 2026 and 2035.

More public health efforts, education campaigns, and the spread of knowledge via digital platforms are all responsible for the growing awareness of circadian rhythm sleep problems. Another element influencing the increase in diagnostic rates is patients' and doctors' growing awareness of CRSD symptoms. The circadian rhythm sleep disorder market is expanding because more people are searching for suitable treatment and management options as diagnosis becomes more accessible.

The circadian rhythm sleep disorder market is driven by rising awareness among the population about sleep disorders and the importance of their treatments. Circadian rhythm sleep disorders are a group of conditions in which the internal body clock (circadian system) is misaligned with the external 24-hour day or sleep-wake requirements, producing chronic or recurrent sleep timing problems and daytime impairment. Common CRSDs include non-24-hour sleep-wake disorder, delayed sleep-phase disorder, advanced sleep-phase disorder, irregular sleep-wake rhythm, and shift-work sleep disorder.

Diagnosis relies on clinical history, sleep diaries, actigraphy, and sometimes polysomnography; treatments combine behavioral interventions (sleep scheduling, light therapy, chronotherapy), pharmacologic approaches (melatonin and melatonin receptor agonists, wake-promoting agents where indicated), and device/diagnostic solutions for sleep monitoring. The market therefore spans pharmaceuticals (including melatonin receptor agonists and other sleep drugs), medical devices and diagnostics (sleep study equipment, wearable/monitoring devices), and digital therapeutics/behavioral solutions.

Clinical artificial intelligence has great promise for transforming the circadian rhythm sleep disorder market through automated sleep study grading and early sleep problem detection. Large-scale datasets are analysed by machine learning (ML) algorithms to categorise relationships between treatment results, sleep physiology, and patient characteristics.

More effective sleep therapies, early problem identification, and real-time health optimisation are being made possible by AI's integration of machine learning with wearable sensors, cloud-based monitoring, and smart home technologies. AI-driven sleep research will advance in precision, predictiveness, and personalisation as technology develops further, eventually resulting in better sleep habits and general well-being for people everywhere.

| Table | Scope |

| Market Size in 2026 | USD 2.65 Billion |

| Projected Market Size in 2035 | USD 4.69 Billion |

| CAGR (2026-2035) | 6.56% |

| Leading Region | North America by 45% |

| Key Applications | Sleep disorder treatment, circadian rhythm regulation, shift-work management, blind patient sleep regulation, sleep monitoring, chronotherapy |

| Primary End Users | Hospitals, sleep clinics, specialty sleep centers, home-care patients, employers, military organizations, research institutions |

| Key Growth Drivers | Rising prevalence of sleep disorders, growing shift-work population, increased awareness of circadian health, expansion of digital therapeutics, adoption of wearable sleep tracking technologies |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Disorder Type, By Treatment Type, By End-User/Customer Segment, By Patient Demographics / Age Group, By Region |

| Top Key Players | Vanda Pharmaceuticals, Inc., Takeda Pharmaceutical Company Limited, Pfizer Inc., Teva Pharmaceutical Industries Ltd., Jazz Pharmaceuticals plc, Merck & Co., Inc., GlaxoSmithKline (GSK), Eisai Co., Ltd., ResMed Inc., Koninklijke Philips N.V. (Philips Respironics), Fisher & Paykel Healthcare Corporation Limited, Compumedics Limited, Natus Medical Incorporated, Becton, Dickinson and Company (BD), Medtronic plc, Arena Pharmaceuticals, Neurocrine Biosciences, Inc., Harmony Biosciences Holdings, Inc., Boehringer Ingelheim GmbH, Fabre-Kramer Pharmaceuticals |

")

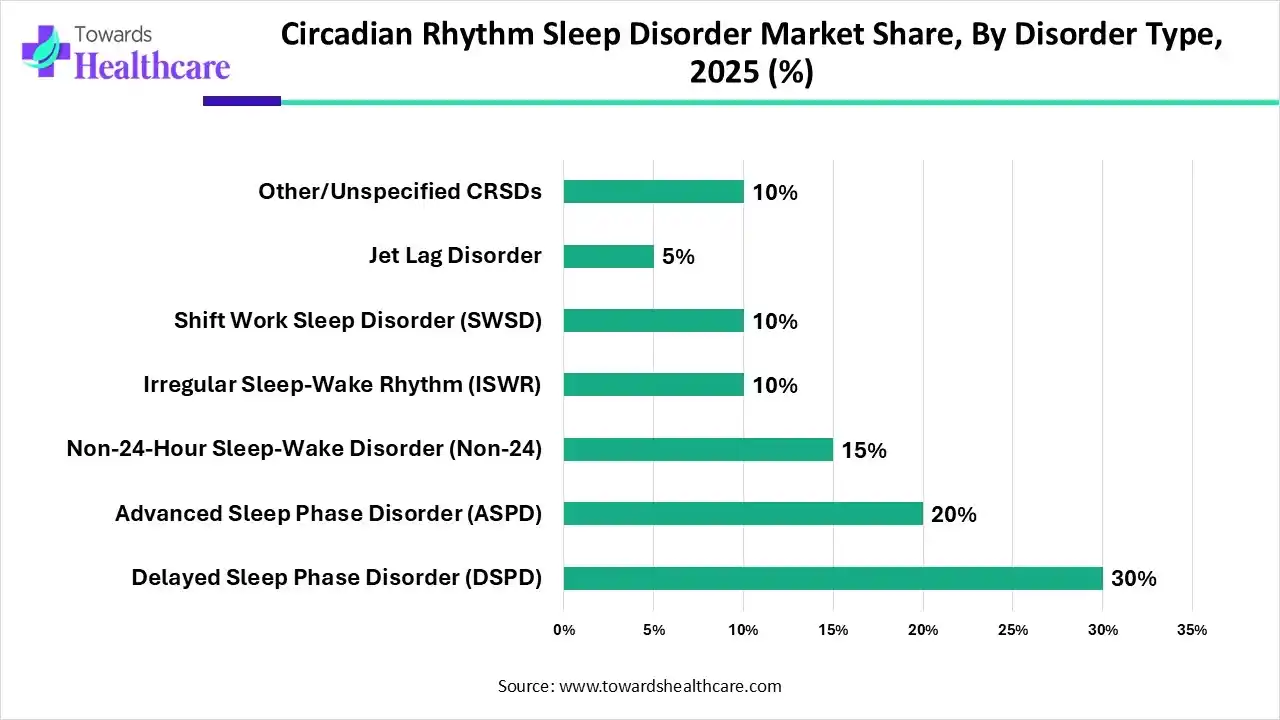

| Segments | Shares % |

| Delayed Sleep Phase Disorder (DSPD) | 30% |

| Advanced Sleep Phase Disorder (ASPD) | 20% |

| Non-24-Hour Sleep-Wake Disorder (Non-24) | 15% |

| Irregular Sleep-Wake Rhythm (ISWR) | 10% |

| Shift Work Sleep Disorder (SWSD) | 10% |

| Jet Lag Disorder | 5% |

| Other/Unspecified CRSDs | 10% |

Explanation

Which Disorder Type Dominated the Market in 2025?

By disorder type, the delayed sleep phase disorder (DSPD) segment captured the largest revenue of 30% of the circadian rhythm sleep disorder market in 2025. Between 1 to 16 percent of teenagers and young adults have DSPD. The effects on the person are profound, especially when it comes to mental health and performance at work and in school. Administering melatonin seems to be a straightforward and successful therapy for DSPD in adolescents. The more intricate combination of bright light therapy and cognitive behavioural therapy is equally beneficial after treatment and seems to have long-term effects.

By disorder type, the non-24-hour sleep-wake disorder segment is estimated to witness the highest growth during the forecast period. It is estimated that non-24-hour sleep-wake disorder affects around half of all blind individuals. While non-24-hour sleep-wake syndrome can strike sighted people at any age, it often manifests in childhood. Tasimelteon, an FDA-approved melatonin receptor agonist, and melatonin supplements are frequently used to treat non-24-hour sleep-wake disorder.

In 2025, the advanced sleep phase disorder (ASPD) segment accounted for a notable share of the market. This is highly susceptible to an ageing population, & also it also has a rigorous hereditary connection. Whereas rising awareness & genetic screening capabilities are fueling early diagnosis & subsequent treatment demands.

The irregular sleep–wake rhythm (ISWR) segment is predicted to witness significant expansion in the circadian rhythm sleep disorder market. Key drivers cover linkage to progressive brain concerns, such as Alzheimer's & Parkinson's disease, propelled by the degeneration of the suprachiasmatic nucleus (SCN). ISWR is also driven by changes in melatonin secretion cycles, often because of impaired pineal gland function or genetic mutations in melatonin receptors.

Why was the Pharmacological Therapies Segment Dominant in the Market in 2025?

By treatment type, the pharmacological therapies segment captured the largest revenue of 50% of the circadian rhythm sleep disorder market in 2025. Benzodiazepines (e.g., temazepam, flurazepam) and non-benzodiazepine hypnotics (e.g., zolpidem, eszopiclone) for insomnia, melatonin receptor agonists (e.g., ramelteon) for regulating the sleep-wake cycle, and dopamine agonists (e.g., modafinil) for excessive daytime sleepiness in conditions like narcolepsy are examples of pharmaceutical treatments for sleep disorders.

By treatment type, the digital therapeutics & mobile apps segment is estimated to witness the highest growth during the forecast period. Digital therapies for sleep problems are now available via platforms including the Internet, smartphone apps, and virtual reality thanks to the quick growth of digital technology in recent years. Data tracking, individualised care, remote care, and many more uses are beneficial.

The light therapy devices/phototherapy segment held a lucrative share of the market in 2025, due to irregular working hours & extended indoor confinement leading to social jet lag, where bright light therapy offers realigning circadian rhythms before, during, or after night shifts. The use of short-wavelength (blue) light facilitates a robust impact on the retina's intrinsically photosensitive retinal ganglion cells (ipRGCs), which relay signals to the suprachiasmatic nucleus to lower melatonin production.

Moreover, the behavioral/chronotherapy interventions segment is estimated to grow at a significant CAGR in the circadian rhythm sleep disorder market. Specifically, Chronotherapy acts on the principle that underlying clock genetics describe a patient's natural rhythm. While behavioral interventions aim to uncouple the genetic predisposition from maladaptive social or environmental patterns.

| Segments | Shares % |

| Hospitals & Sleep Clinics | 35% |

| Primary Care/General Practitioners | 15% |

| Occupational Health & Corporate Wellness | 20% |

| Home Users/Direct-to-Consumer | 13% |

| Pharmacies & Retail (OTC distribution) | 7% |

| Research Institutes/CROs (Diagnostics & Trials) | 10% |

Explanation

How the Hospitals & Sleep Clinics Segment Dominated the Market in 2025?

By end-user/customer segment, the hospitals & sleep clinics segment captured the largest revenue of 35% of the circadian rhythm sleep disorder market in 2025. Deeper knowledge, sophisticated diagnostics like sleep studies, and individualised, comprehensive treatment programmes are all provided by specialised sleep clinics. Compared to general care, this targeted strategy results in more precise diagnoses and improved long-term patient outcomes.

By end-user/customer segment, the occupational health & corporate wellness segment is estimated to witness the highest growth during the forecast period. In order to ensure the general well-being of employees, sleep is an essential part of corporate wellness programmes. Businesses may assist their workers get better sleep, which will improve their health, productivity, and job happiness. They can do this by integrating sleep tests into executive health checks, encouraging exercise, and putting effective stress management strategies into practice.

In 2025, the primary care/general practitioners segment captured a significant share, because it serves as the first point of contact for patients reporting increased daytime sleepiness or insomnia. Physicians are increasingly employing assessment tools & may suggest lifestyle/behavioral therapy, bright light therapy, or chronotherapy. However, practising physicians are focusing on actigraphy & diagnostic apps to monitor circadian rhythm metrics.

On the other hand, the home users/direct-to-consumer segment is expected to expand notably in the coming era. A major driver sis rising penetration of smartwatches, fitness trackers, & specialized bedside sensors enabling consumers to monitor sleep-wake cycles & actigraphy on their own. Growing awareness about the long-term health consequences of sleep deprivation is fueling the popularity of over-the-counter sleep aids, specialized wake-up light alarm clocks, & melatonin supplements.

| Segment | Share 2025 (%) |

| Adolescents (13–17) | 20% |

| Young Adults (18–34) | 30% |

| Adults (35–64) | 25% |

| Elderly (65+) | 15% |

| Pediatric (0–12) | 10% |

Explanation

What Made the Young Adults Segment Dominant in the Market in 2025?

By patient demographics/age group, the young adults segment captured the largest revenue of 30% of the circadian rhythm sleep disorder market in 2025. The prevalence of identified sleep disorders described in the literature ranges from 5% to 15%, with between 10% and 30% of the general adult population suffering from poor sleep quality and sleep issues. Due to lifestyle issues including excessive screen time, unpredictable sleep cycles, and late-night digital device use, younger individuals frequently struggle to initiate sleep.

By patient demographics/age group, the adolescents segment is estimated to witness the highest growth in the circadian rhythm sleep disorder market during the forecast period. About 40% of people have a mental problem by the time they are 14 years old, and almost all psychiatric disorders peak during adolescence. Intervention and early detection are crucial. Numerous interventions, including delaying school start times, limiting mobile and social media use, and promoting physical exercise, may be implemented at the individual, family, and school levels to enhance and sustain the length and quality of teenage sleep.

The adults (35–64) segment held a lucrative share of the circadian rhythm sleep disorder market in 2025. This age group mainly experiences rotating or night shifts, which directly force the body's natural circadian rhythms out of sync with environmental light-dark cycles. Accelerating consumption of artificial blue light from personal electronic devices & greater reliance on caffeine or alcohol disturbs the body’s natural melatonin production among these patients.

Whereas elderly (65+) segment is predicted to expand notably. They majorly suffer from a ‘phase advance’, that means their circadian rhythms shift earlier & often leads to early evening sleepiness & uncomfortably early morning awakenings. Additionally, CRSWDs in older adults often stem from multimorbidity, along with chronic illness dementia, cardiovascular disease, osteoarthritis, & respiratory disorders, resulting in sleep disruptions.

")

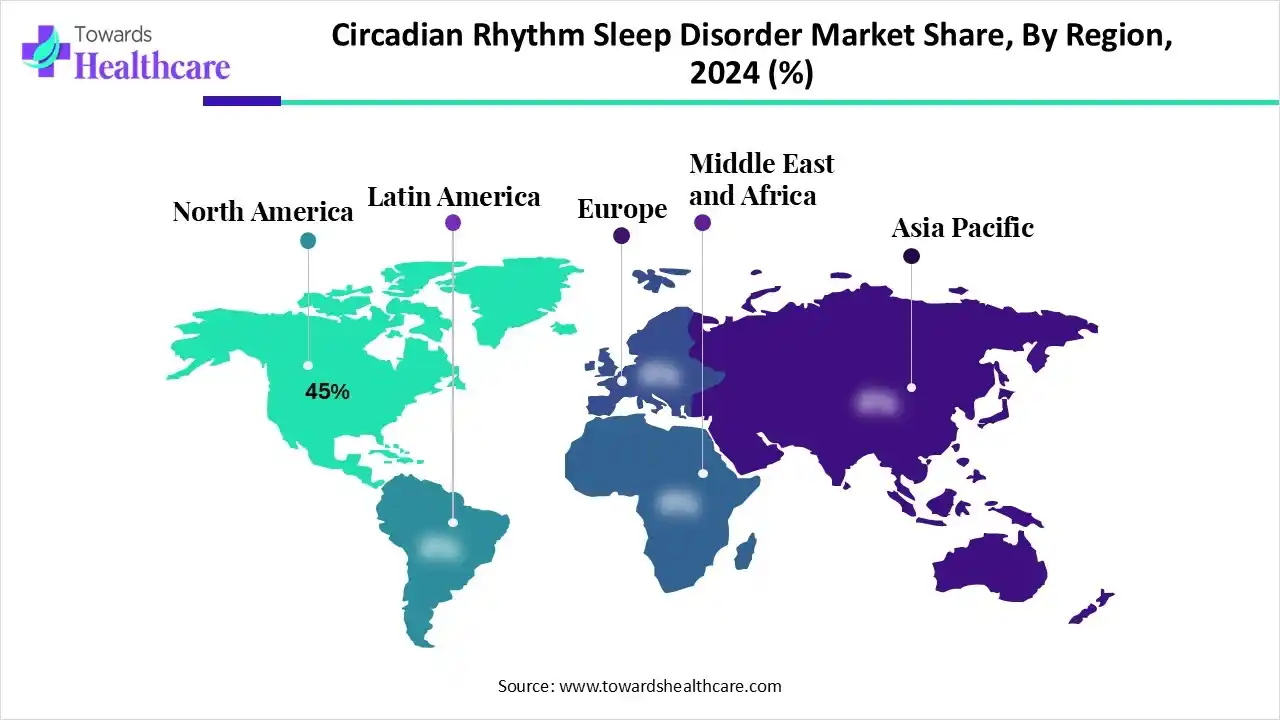

North America dominated the circadian rhythm sleep disorder market share by 45% in 2025, with a share of 45% due to the prevalence of sleep disorders in the region. The presence of significant market participants, research facilities, and state-of-the-art healthcare infrastructure is driving the industry's growth. The market is expanding as a result of the established healthcare system and sizable patient base in the United States.

Rising Sleep Disorders are Driving the U.S.

About 50 to 70 million adults in the United States suffer from chronic sleep disorders, the most common of which are sleep apnea and insomnia. An estimated 80.6 million people suffered from obstructive sleep apnea in 2024, and a 2024 survey found that roughly one-third of Americans sleep in a different room from their partners because of sleep problems like snoring or restlessness.

Limitations of Natural Light & Emerging Research Drive Canada

The circadian rhythm sleep disorder market in Canada is mainly fueled by the presence of massively shorter days during winter months, which lack strong morning light exposure, & mitigating the internal biological clock from efficiently resetting every 24 hours. Gradually, institutions, such as the Douglas Mental Health University Institute, are researching how late-night digital media & light exposure during youth impact melatonin production & sleep-wake phases. Although McGill University has investigated how minimal circadian amplitude after menopause contributes to sleep disruptions.

Asia Pacific is estimated to host the fastest-growing circadian rhythm sleep disorder market during the forecast period. Increases in sleep-related health problems have been caused by the region's mass-market potential, rapidly ageing population, rapid urbanisation, rising work-related stress, and the relatively recent adoption of Westernised lifestyles (especially with regard to technology use and artificial light exposure). Sleeping well with natural light is a part of traditional lifestyles in Asia Pacific nations like China, Japan, India, and South Korea.

Rising Sleep Disorders in Children are Driving China

Loss of sleep is no longer a problem that only affects adults in China. A growing public health concern that also impacts children is inadequate sleep, which is brought on by late bedtimes, trouble falling asleep, and other sleep-related issues.

China plans to open sleep and mental health clinics in every city at the prefecture level by the end of 2025 as part of a larger initiative to address sleep and mental health issues for people of all ages. This will increase access to professional assistance for people who are experiencing psychological and sleep-related anxiety.

Expansion of Competitive Work Hrs & Specialized Sleep Hubs Supports India

India is estimated to expand fastest in the circadian rhythm sleep disorder market, due to the huge rise in the demographic of night-shift workers, especially in IT sectors, BPOs, & call centers. This further results in the loss of natural circadian rhythms. To resolve these kinds of sleep concerns, many key institutions, like the Institute of Sleep Health at Apollo Hospitals in Chennai, have developed multidisciplinary centers that unite pulmonology, neurology, & psychology to objectively diagnose circadian misalignment, leveraging actigraphy & dim light melatonin onset (DLMO) testing.

Hectic Schedules & Emerging Digital Diagnostics Spur South Korea

Primarily, South Korea is experiencing an intense corporate work culture, including late-night shifts & a highly competitive education system, which leads to major disturbances to natural sleep-wake cycles. To overcome these developing challenges, researchers from this nation have enforced AI algorithms capable of forecasting sleep disorder risks with over 90% accuracy, utilizing a simple 5-question survey.

Europe is expected to grow at a significant CAGR in the circadian rhythm sleep disorder market during the forecast period. The European Commission predicts that the old-age dependence ratio in Europe, the proportion of people 65 and older compared to those between the ages of 15 and 64, will increase from 29.6% in 2021 to 51.2% in 2030, making sleep problems more common in the future. Thanks to the European Medicines Agency's coordinated regulatory procedures and universal coverage, Europe continues to grow steadily.

What are the France Market Trends?

Between 13 and 18 million people in France suffer from sleep disorders, making them a public health concern. Given that 13% of French people have been diagnosed with chronic insomnia and 19% report having its symptoms, chronic insomnia is a serious public health concern. Additionally, OSAS is 4.8% and restless legs syndrome is 8.5% common in the French population.

South America is expected to grow significantly in the circadian rhythm sleep disorder market during the forecast period, due to increasing health awareness, which is increasing the early diagnosis of circadian rhythm sleep disorders. The rapid urbanization and lifestyle change are also increasing their incidence, where the growing digital health platforms and OTC products are also enhancing the market growth.

Brazil Market Trends

Brazil is experiencing a rise in circadian rhythm sleep disorders, which is increasing the demand for accurate and effective diagnostic and treatment options. This, in turn, is increasing the expansion of the sleep clinics and adoption of the chronotherapy services. Additionally, increasing health awareness is also increasing the demand for advanced therapies.

MEA is expected to grow significantly in the circadian rhythm sleep disorder market during the forecast period, due to increasing incidences of circadian rhythm sleep disorders driven by rapid urbanization, which are increasing the demand for their effective diagnostics and treatment options. The growing health awareness and increasing healthcare investments are also increasing the development of their treatment options, where expanding telehealth solutions are also promoting the market growth.

Saudi Arabia Market Trends

The growing health awareness in the Saudia Arabia is increasing the use of various sleep aids for the treatment of circadian rhythm sleep disorders. The expanding healthcare is also increasing the adoption of various prevention and treatment options, where the growing government initiatives are also driving their R&D activities.

Strengths

Weaknesses

Opportunities

Threats

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Philips, ResMed, Oura Health, Apple, Garmin | Develop sleep monitoring and circadian tracking technologies |

| Product Manufacturers | Vanda Pharmaceuticals, Eisai, Takeda, Neurim Pharmaceuticals | Develop pharmaceuticals and melatonin-based therapies |

| Service Providers | Mayo Clinic Sleep Medicine, Cleveland Clinic Sleep Disorders Center, Stanford Sleep Medicine Center | Diagnosis and treatment services |

| Platform Providers | SleepScore Labs, Oura Health, WHOOP | Digital sleep analytics and patient engagement platforms |

| CROs/CDMOs | IQVIA, ICON plc, Syneos Health | Clinical trials and drug development support |

| Software Vendors | SleepScore Labs, Philips Digital Health, ResMed Digital Health | Sleep monitoring and data management solutions |

| Research Institutions | Harvard Medical School, Stanford University Sleep Research Center, University of Pennsylvania Sleep Center | Circadian biology and sleep disorder research |

| End-User Industries | Healthcare, Defense, Transportation, Aviation, Manufacturing, Corporate Wellness | Utilize sleep management and fatigue reduction programs |

R&D

Research and development for sleep disorders is a multi-phase process that moves from basic scientific discovery to clinical implementation and improvement. Understanding sleep mechanisms, finding and confirming novel therapeutic targets, creating and evaluating novel interventions, and establishing best practices for their application are all part of this process. The ultimate objective is to develop safer, more individualised, and more effective treatments for diseases like narcolepsy, sleep apnea, and insomnia.

Clinical Trials and Regulatory Approvals

Phase I–III clinical trials for safety and efficacy, FDA review of the New Drug Application (NDA), approval, post-market phase IV surveillance for long-term safety, and preclinical testing are among the steps.

Patient Support and Services

To ensure adherence and manage progress, steps include diagnosing and educating patients, offering therapy like CBT-I, providing equipment like CPAP machines, and conducting ongoing counselling and monitoring.

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 65% | 25% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Vanda Pharmaceuticals | Washington, D.C. | USA | Market leader in approved circadian rhythm sleep disorder therapies | Hetlioz (tasimelteon), sleep disorder therapeutics |

| Eisai Co., Ltd. | Tokyo | Japan | Global leader in sleep medicine and insomnia treatments | Dayvigo, sleep disorder portfolio |

| Takeda Pharmaceutical Company | Tokyo | Japan | Strong neuroscience and sleep disorder presence | Circadian and sleep disorder therapeutics |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Neurim Pharmaceuticals | Tel Aviv | Israel | Pioneer in circadian rhythm therapeutics | Circadin, prolonged-release melatonin |

| Jazz Pharmaceuticals | Dublin | Ireland | Strong presence in sleep disorder treatments | Xywav, Xyrem sleep therapies |

| Idorsia Ltd | Allschwil | Switzerland | Commercial sleep medicine products | Quviviq and sleep-focused pipeline |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Oura Health | Oulu | Finland | Leading wearable sleep analytics company | Oura Ring sleep tracking platform |

| SleepScore Labs | Carlsbad, California | USA | Specialized sleep assessment technology | SleepScore mobile platform |

By Disorder Type

By Treatment Type

By End-User/Customer Segment

By Patient Demographics / Age Group

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar