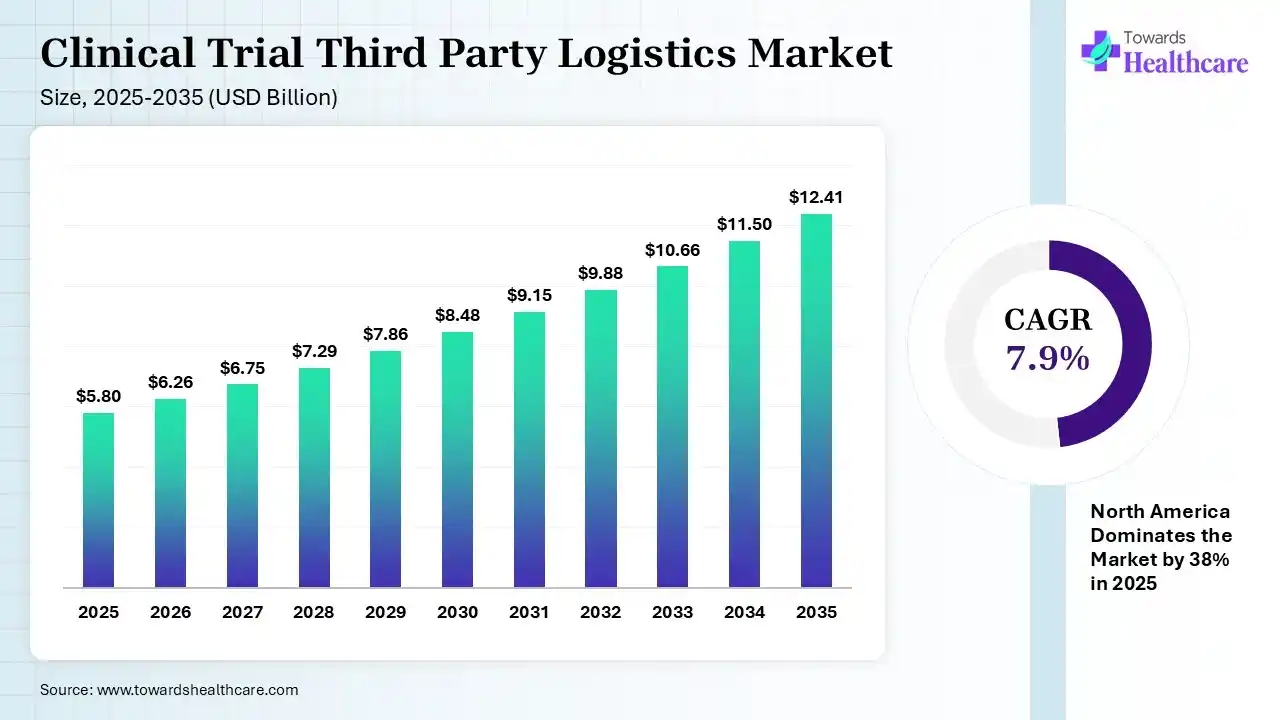

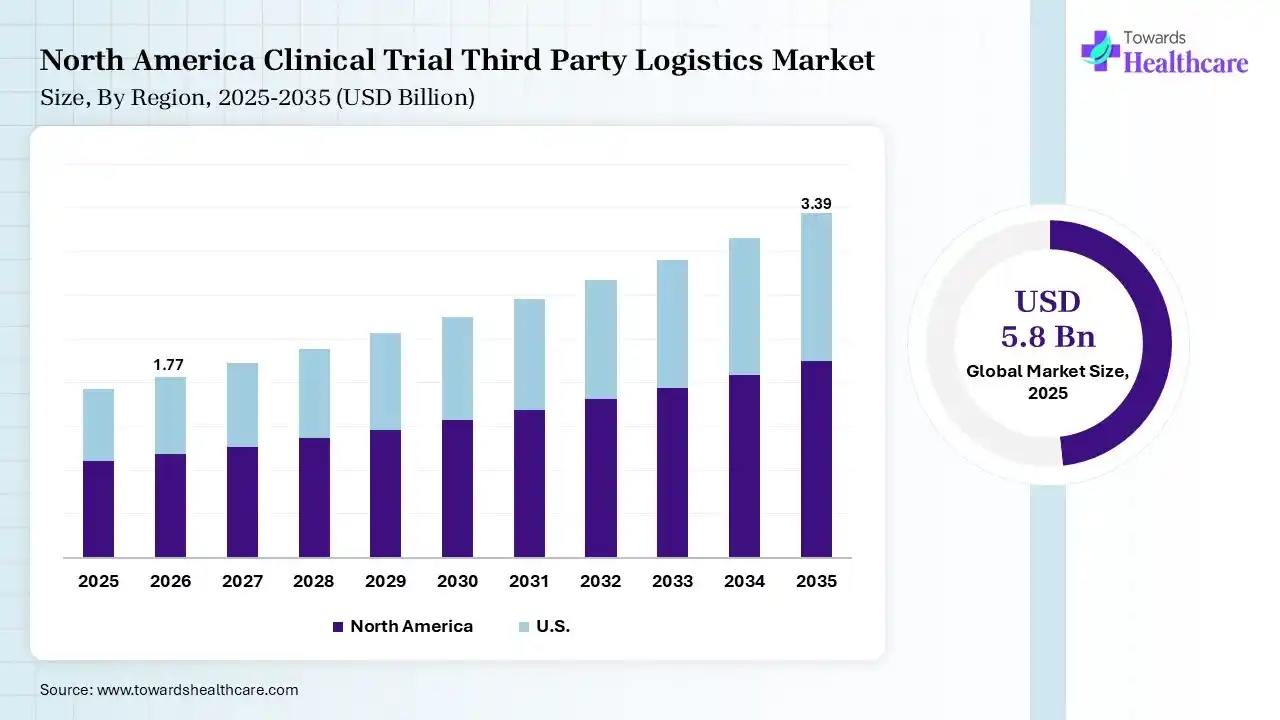

The global clinical trial third-party logistics market size was estimated at USD 5.8 billion in 2025 and is predicted to increase from USD 6.26 billion in 2026 to approximately USD 12.41 billion by 2035, expanding at a CAGR of 7.9% from 2026 to 2035. The growing clinical trials and R&D activities are increasing the use of clinical trial third-party logistics. The expanding healthcare sector, decentralized trials, technological innovations, and new collaborations are also enhancing the market growth.

")

The clinical trial third-party logistics market is driven by growing trial complexities and a shift towards specialized supply chain solutions. The clinical trial third-party logistics encompasses specialized logistic partners offering supply chain and logistics services. They help in safe and efficient storage, packing, labeling, and distribution of investigational drugs and clinical trial resources.

The demand for AI in the clinical trial third-party logistics market is increasing as it predicts the growth in the product demand, optimizes inventory, and prevents stockouts. It also helps in risk management and provides automated documentation, reducing the chances of errors. Its real-time monitoring, smart packaging, and regulatory compliance also increase its use.

Globalization of Clinical Trials

The rise in the multi-country trials, multisite trials, and decentralized trials is increasing the demand for clinical trial third-party logistics for regulatory compliance and product distribution.

Flourishing Biologics

The growing advancements in biologics are increasing the use of clinical trial third-party logistics for their specialized storage, packaging, handling, and transportation solutions.

Growing R&D Investment

The rise in R&D investments is accelerating the development of new drug candidates and clinical trials, driving the demand for clinical trial third-party logistics for clinical supply management, logistics support, and packaging and labelling.

| Table | Scope |

| Market Size in 2026 | USD 6.26 Billion |

| Projected Market Size in 2035 | USD 12.41 Billion |

| CAGR (2026 - 2035) | 7.9% |

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Temperature Range, By Phase, By End User, By Therapeutic Area, By Region |

| Top Key Players | DHL Supply Chain, UPS Healthcare (Marken), FedEx HealthCare Solutions, Thermo Fisher Scientific, Kuehne + Nagel, Almac Group, Catalent, Movianto (Walden Group), Biocair |

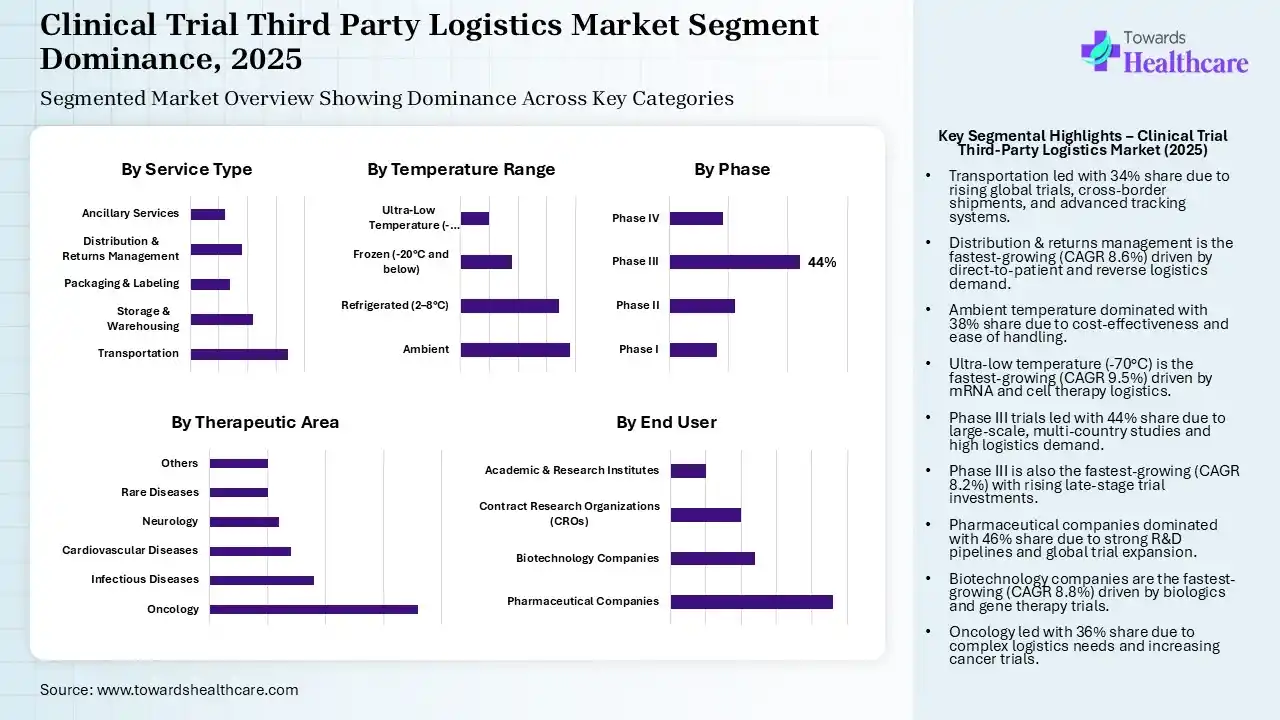

The Transportation Segment Dominated the Market With 34% in 2025

| Segment | Share 2025 (%) |

| Transportation | 34% |

| Storage & Warehousing | 22% |

| Packaging & Labeling | 14% |

| Distribution & Returns Management | 18% |

| Ancillary Services | 12% |

The transportation segment led the clinical trial third-party logistics market with 34% share in 2025, due to growth in the clinical trials, which increased the demand for cross-border shipments. The presence of advanced tracking systems also increased their use. Additionally, faster delivery timelines also increased their demand.

The storage & warehousing segment held 22% of the market share in 2025, driven by increasing advancements in biologics development. This is increasing the demand for specialized storage conditions, increasing the use of clinical trial third-party logistics. Growing decentralized trials and regulatory requirements are also increasing their use.

The distribution & returns management segment held 18% of the clinical trial third-party logistics market share in 2025 and is expected to witness the fastest growth with a CAGR of 8.6% during the forecast period, due to their real-time distribution optimization, which improves trial efficiency. The growing decentralized trials are also increasing the demand for direct-to-patient logistics. The growth in reverse logistics grows with unused drug returns, which are also increasing in use.

The packaging & labeling segment held 14% of the market share in 2025, due to growing demand patient centric packaging to enhance compliance and safety. The growing development of biologics is also increasing the demand for specialized packaging. Moreover, growing decentralized trials are also increasing direct-to-patient logistics.

The Ambient Segment Dominated the Market With 38% in 2025

| Segment | Share 2025 (%) |

| Ambient | 38% |

| Refrigerated (2–8°C) | 34% |

| Frozen (-20°C and below) | 18% |

| Ultra-Low Temperature (-70°C and below) | 10% |

The ambient segment accounted for the highest revenue share of 38% of the clinical trial third-party logistics market in 2025, driven by its affordability and simpler handling. The growth in the volume of conventional drugs also increased their adoption rates. Moreover, their simple transportation and faster delivery also increased their use.

The refrigerated (2–8°C) segment held 34% of the market share in 2025, due to growing development of biologics and vaccines. The growing clinical trials of the specialty drugs are also increasing their use. Stringent stability requirements and expansion of cold chain infrastructure are also increasing their use.

The frozen (-20°C and below) segment held 18% of the clinical trial third-party logistics market share in 2025, due to growing advanced therapies, which increase the demand for frozen storage conditions. The rise in the clinical trials of biologics has also increased their demand. Furthermore, increasing advancements in freezing technologies are also increasing their acceptance rates.

The ultra-low temperature (-70°C and below) segment held 10% of market share in 2025 and is expected to show the highest growth with a CAGR of 9.5% during the forecast period, due to growing investments in ultra-cold logistics. The rise in mRNA and cell therapies is also increasing their use. Additionally, expanding infrastructure due to pandemic-driven innovations is also increasing their use.

The Phase III Segment Dominated the Market With 44% in 2025

| Segment | Share 2025 (%) |

| Phase I | 16% |

| Phase II | 22% |

| Phase III | 44% |

| Phase IV | 18% |

The phase III segment held a major revenue share of 44% of the clinical trial third-party logistics market in 2025 and is expected to expand rapidly with a CAGR of 8.2% during the forecast period, driven by high investment in late-stage trials. The growth in the large-scale global trials also increased the demand for extensive logistics support. The expansion of the multi-country studies also increased the transportation demand.

The phase II segment held 22% of the market share in 2025, due to pipeline progression, which increases trial complexity and demand for third-party logistics. The patient recruitment expansion also drives logistics needs. The growing mid-scale logistics are also attracting companies.

The phase IV segment held 18% of the clinical trial third-party logistics market share in 2025, driven by the distribution to broader patient populations and growth in decentralized trials. The focus on real-world evidence is also increasing its use. The growing long-term studies are also increasing the demand for sustained logistics support.

The phase I segment held 16% of the market share in 2025, as Early-stage trials increase demand for small batch logistics. The growing biotech startups and rapid study cycles are also increasing their use. Additionally, the growing development of personalized medicines is also increasing their demand.

The Pharmaceutical Companies Segment Dominated the Market With 46% in 2025

| Segment | Share 2025 (%) |

| Pharmaceutical Companies | 46% |

| Biotechnology Companies | 24% |

| Contract Research Organizations (CROs) | 20% |

| Academic & Research Institutes | 10% |

The pharmaceutical companies segment contributed the biggest revenue share of 46% of the clinical trial third-party logistics market in 2025, due to high R&D investments, which increased the use of clinical trial third-party logistics. The growth in the drug pipeline also increased logistics demand. The expansion of the trial networks also increased shipment needs.

The biotechnology companies segment held the second-largest share of 24% of the market in 2025 and is expected to gain the highest share with a CAGR of 8.8% during the forecast period, due to growth in biologics and gene therapies. Growing outsourcing trends also increase the demand for logistics support. Increasing innovation-driven trials are also increasing the demand for specialized handling.

The contract research organizations (CROs) segment held 20% of the clinical trial third-party logistics market share in 2025, due to growth in outsourcing trends. The integrated trial services are also driving demand. Expanding CRO networks are increasing collaborations to leverage the logistic services.

The academic & research institutes segment held 10% of the market share in 2025, driven by expanding R&D activities. Limited internal logistics capabilities are also increasing the demand for clinical trial third-party logistics. Increasing government-funded trials are also promoting their use.

The Oncology Segment Dominated the Market With 36% in 2025

| Segment | Share 2025 (%) |

| Oncology | 36% |

| Infectious Diseases | 18% |

| Cardiovascular Diseases | 14% |

| Neurology | 12% |

| Rare Diseases | 10% |

| Others | 10% |

The oncology segment held the largest revenue share of 36% of the clinical trial third-party logistics market in 2025 and is expected to grow with the fastest CAGR of 8.7% during the forecast period, driven by growth in the demand for complex logistic support due to the rise in cancer trials. High investments also fuel their demand. Growth in personalized therapy also increased their use for storage and handling support.

The infectious diseases segment held 18% of the market share in 2025, due to the rise in vaccine trials. Growing global health initiatives are also increasing the demand for cold chain logistics. A rise in the patient value is also driving the demand for clinical trial third-party logistics.

The cardiovascular diseases segment held 14% of the clinical trial third-party logistics market share in 2025, due to growing incidence rates. The growing number of clinical trials is also increasing the demand for clinical trial third-party logistics. Growing adoption of standardised therapies is also increasing their use.

The neurology segment held 12% of the market share in 2025, due to neurodegenerative research and clinical trials. Their complex protocols are also increasing the demand for clinical trial third-party logistics. Rise in the disease incidence rates and geriatric population are also increasing the use of their treatment option, fueling the demand for logistic support.

")

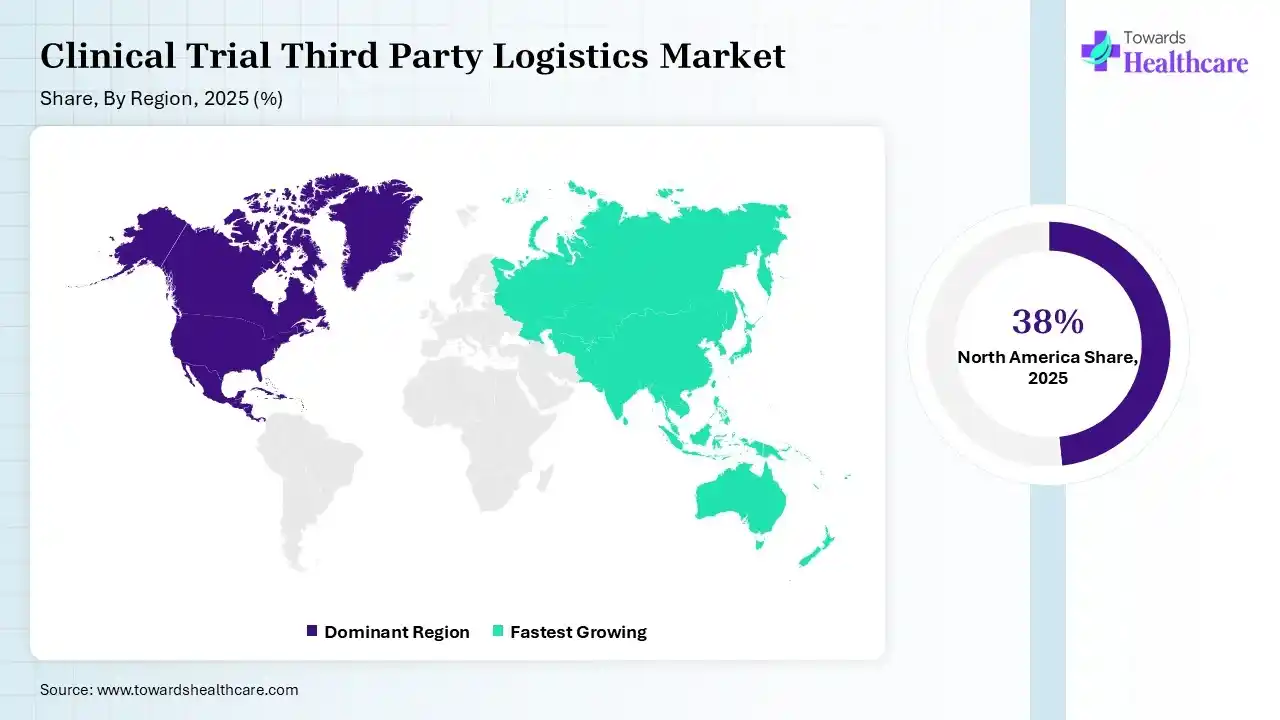

North America dominated the clinical trial third-party logistics market with 38% in 2025, due to the presence of a robust clinical trial infrastructure, which increased the use of clinical trial third-party logistics. The advanced cold chain capabilities also increased their demand. High R&D spending also increased their use, which contributed to the market growth.

U.S. Market Trends

The U.S. consists of large pharmaceutical and biotechnology companies, where the high R&D expenditure is increasing the use of clinical trials and third-party logistics. Stringent regulations and expanding clinical trials are also driving their adoption rates. Moreover, growing technological innovations are enhancing various features of logistics solutions.

Asia Pacific held 24% share of the clinical trial third-party logistics market in 2025 and is expected to show the highest growth with a CAGR of 9.1% during the forecast period, due to expanding healthcare infrastructure, which is driving the demand for clinical trial third-party logistics. A large patient population is increasing clinical trials, fueling their use. Additionally, expanding industry and R&D activities are also promoting the market growth.

China Market Trends

China is experiencing a rise in clinical trials, which is increasing the use of third-party clinical trial logistics. The presence of large patient pollution and expanding cold chain infrastructure is also fuelling their demand. Additionally, growing government support is also promoting their use.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Clinical Trial Third Party Logistics Solutions |

| DHL Supply Chain | Bonn, Germany | Integrated clinical supply chain |

| UPS Healthcare (Marken) | Alpharetta, U.S. | Specialized Marken solutions |

| FedEx HealthCare Solutions | Memphis, U.S. | Clinical trial integrated solutions |

| Thermo Fisher Scientific | Waltham, U.S. | End-to-end trial supply logistics |

| Kuehne + Nagel | Schindellegi, Switzerland | KN PharmaChain |

| World Courier (Cencora) | Conshohocken, U.S. | Specialist global courier services |

| Almac Group | Craigavon, UK | Comprehensive clinical trials supply solutions |

| Catalent | Somerset, U.S. | Clinically supply services |

| Movianto (Walden Group) | Paris, France | Specialized European healthcare logistics |

| Biocair | Cambridge, UK | Global specialist logistics |

Strengths

Weaknesses

Opportunities

Threats

By Service Type

By Temperature Range

By Phase

By End User

By Therapeutic Area

By Region

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar