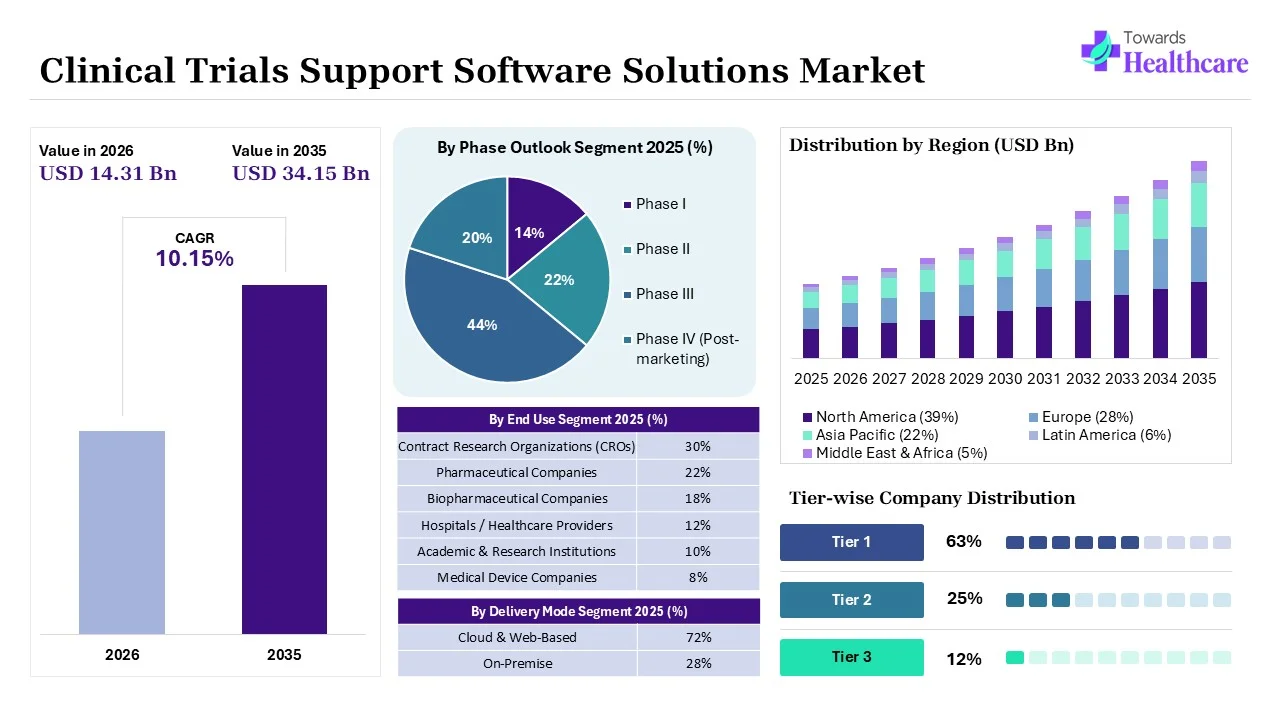

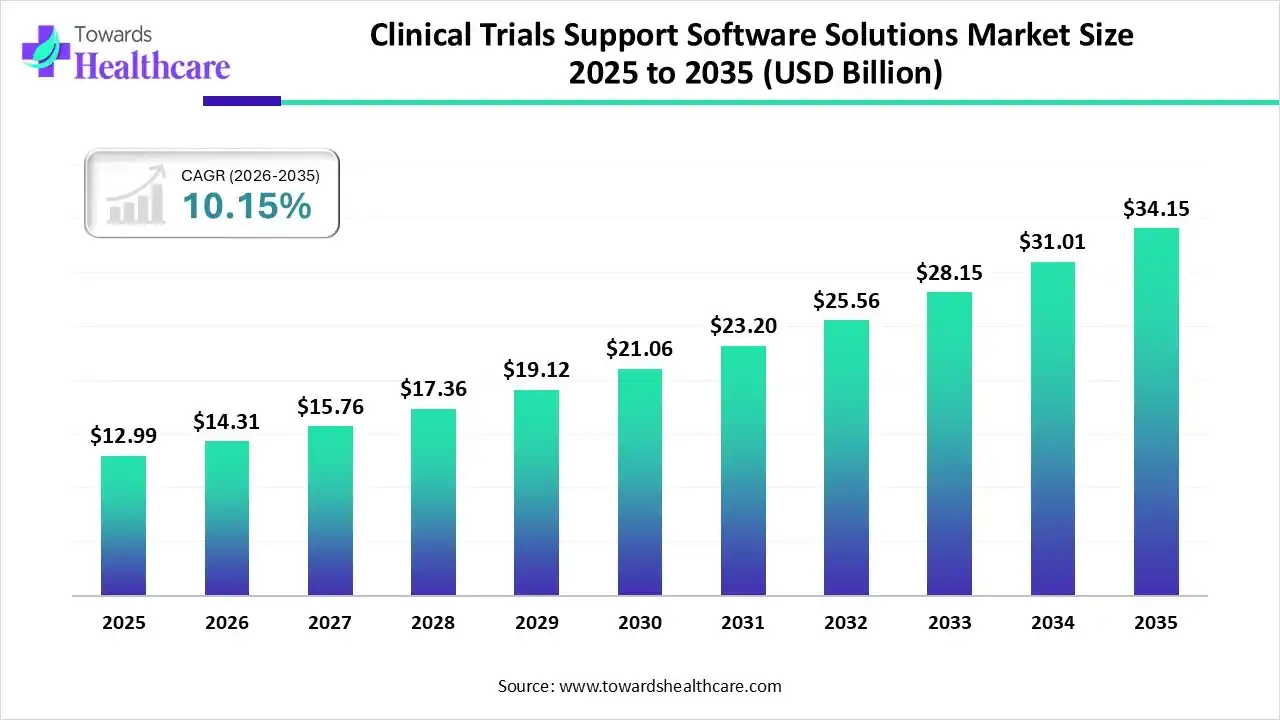

The global clinical trials support software solutions market size was estimated at USD 12.99 billion in 2025 and is predicted to increase from USD 14.31 billion in 2026 to approximately USD 34.15 billion by 2035, expanding at a CAGR of 10.15% from 2026 to 2035.

The global clinical trials support software solutions market is driven by these software services are specialized digital platforms intended to streamline the whole clinical trial lifecycle, from planning and implementation to analysis and reporting. These services enhance effectiveness, ensure government compliance, improve data accuracy and security, and lower operational expenses by replacing physical, paper-based processes.

The Clinical Trials Support Software Solutions Market includes digital platforms like SaaS, web-based, and on-premises tools designed to help with the planning, management, and regulatory compliance of clinical trials. Highly valued, it aids in data management, patient tracking, and site monitoring to speed up drug development. This market is crucial for accelerating drug development, reducing trial costs, and ensuring compliance with regulations by automating data management and patient recruitment.

These digital platforms enhance operational efficiency, enabling decentralized virtual trials, improving patient retention, and boosting data accuracy in complex global clinical studies. The demand for clinical trials support software solutions is mainly driven by the increasing complexity of trial protocols, rising R&D investments, and the urgent need for digital transformation, which includes AI integration and decentralized trial models. Additionally, strict regulatory requirements for data integrity, a growing focus on personalized medicine, and the need for faster patient recruitment are further encouraging the use of software solutions.

Clinical trials support software solution are digital platforms that help manage, monitor, and optimize clinical trials by improving data accuracy, regulatory compliance, and collaboration among sponsors, CROs, and research sites.

The clinical trials support software solutions market is growing due to the rising complexity of clinical studies, increasing adoption of decentralized trials, and greater demand for efficient trials management. AI, cloud computing, predictive analytics, and eClinical technologies are enhancing trials efficiency and decision-making. Future opportunities include real-world evidence integration, wearable health technologies, and digital biomarkers, while growing pharmaceutical R&D investments and CRO outsourcing continue to drive market expansion.

AI-driven technology has revolutionised ground-breaking ways of gathering data, biosimulation, and early disease diagnosis for clinical trials. AI-driven technology offers wide utility options through structured, standardised, and digitally driven elements in healthcare research. AI-driven technology authorizes trials to take proactive and decisive actions to enhance patient results and clinical trial outcomes. AI plays a significant role in automating processes that have conventionally been time-consuming and error-prone. It supports scientists to streamline trial design, match patients more efficiently, and analyze wide datasets with greater precision.

| Key Elements | Scope |

| Market Size in 2026 | USD 14.31 Billion |

| Projected Market Size in 2035 | USD 34.15 Billion |

| CAGR (2026 - 2035) | 10.15% |

| Leading Region | North America by 39% |

| Market Definition | The market comprises software platforms and digital solutions that support planning, design, execution, monitoring, data capture, analytics, and regulatory compliance of clinical trials across pharmaceuticals, biotechnology, and medical device development lifecycles. |

| Primary End Users | Pharmaceutical companies, biotechnology firms, medical device manufacturers, contract research organizations (CROs), academic medical centers, clinical investigators |

| Key Challenges | Data interoperability issues, regulatory compliance variability, high system integration costs, patient recruitment inefficiencies, cybersecurity & data privacy concerns, fragmented vendor ecosystem |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Outlook, By Phase Outlook, By End Use Outlook, By Regional Outlook |

| Top Key Players | IQVIA, Anju Software, QIAGEN, Advarra, Avetra, Oracle, Parexel, Syneos, ICON |

")

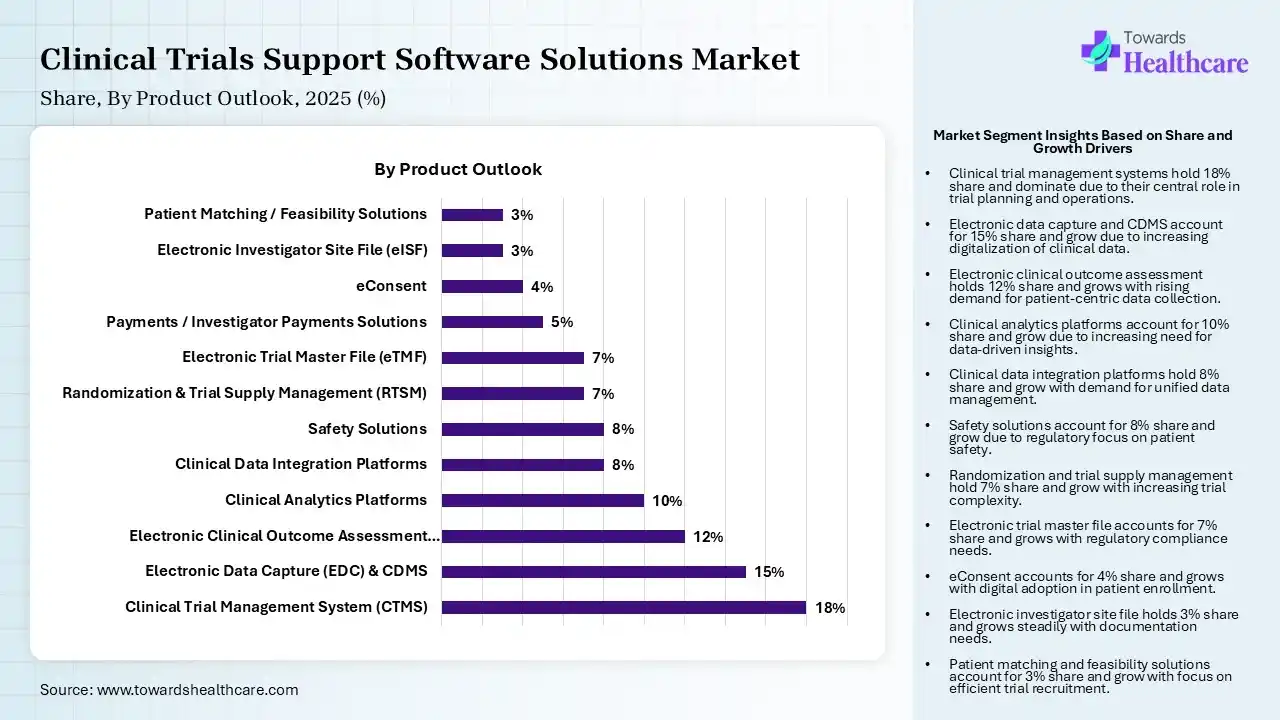

| Segments | Shares % |

| Clinical Trial Management System (CTMS) | 18% |

| Electronic Data Capture (EDC) & CDMS | 15% |

| Electronic Clinical Outcome Assessment (eCOA/ePRO) | 12% |

| Clinical Analytics Platforms | 10% |

| Clinical Data Integration Platforms | 8% |

| Safety Solutions | 8% |

| Randomization & Trial Supply Management (RTSM) | 7% |

| Electronic Trial Master File (eTMF) | 7% |

| Payments / Investigator Payments Solutions | 5% |

| eConsent | 4% |

| Electronic Investigator Site File (eISF) | 3% |

| Patient Matching / Feasibility Solutions | 3% |

Which Product Led the Clinical Trials Support Software Solutions Market in 2025?

In 2025, the CTMS segment held the dominating share of 18% of the market as CTMS, constructed on a unified data architecture, allows data to be entered once and used across all applications. A cloud-based CTMS service is a necessity to optimize clinical trial management by centralizing clinical and operational data, rationalization activities, and offering continuous oversight and visibility.

Payments/Investigator Payment Solutions

Whereas, the payments/investigator payment solutions segment is the fastest growing in the market as streamlined payment procedures improve the workload on trial sites, enabling staff to focus additional attention on participant care and research. By eliminating financial barriers, trials attract a more diverse pool of participants, resulting in more representative and comprehensive research results.

")

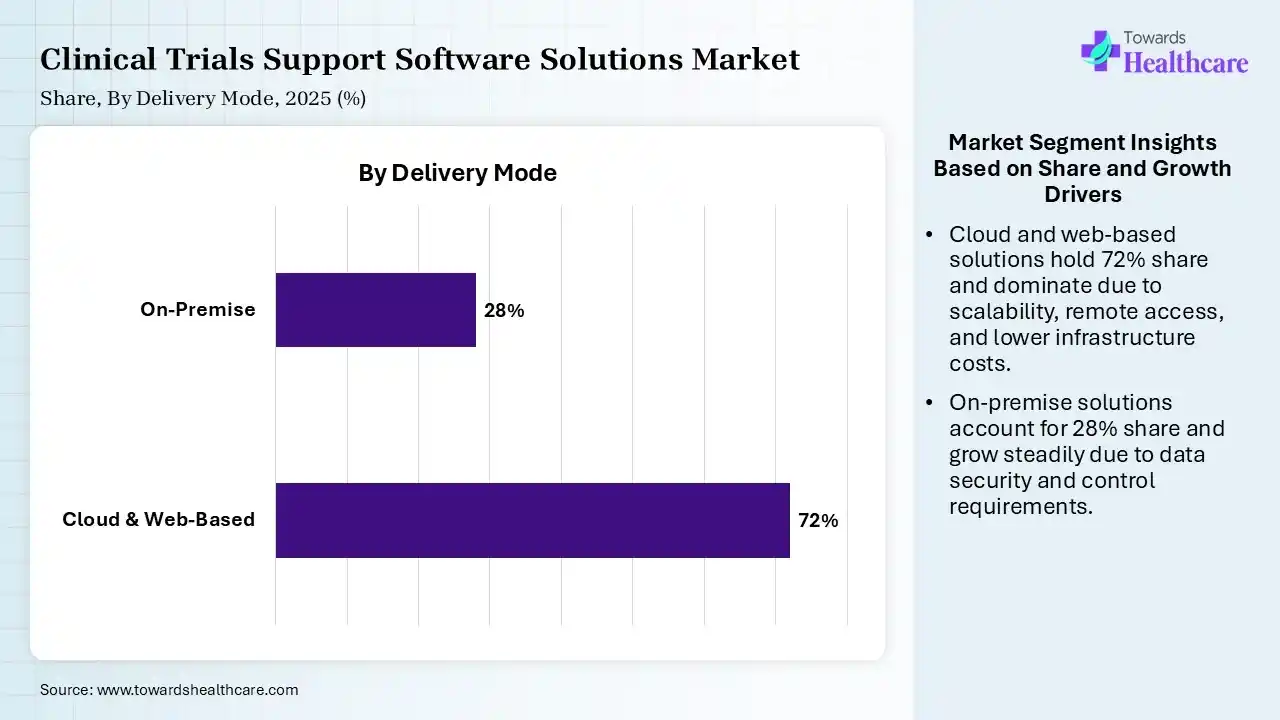

| Segments | Shares % |

| Cloud & Web-Based | 72% |

| On-Premise | 28% |

Why did the Cloud and Web-based Segment Dominate the Market in 2025?

The cloud and web-based segment captured the biggest revenue share of 72% of the clinical trials support software solutions market in 2025, as it lowers paperwork, reduces data entry challenges, and streamlines workflows. This helps cut down the overall expenses of running clinical trials. Investigators, sponsors, and regulators access trial data from anywhere, enabling them to track progress and adjust without postponement.

On-Premise

Whereas, the on-premise segment is estimated to grow significantly in the market during 2026-2035, as an on-premises CTMS offers complete control it provides over data management. It is highly modified to meet the specific requirements of an organization. From complex workflows to exclusive reporting features, on-premises systems are tailored in ways that cloud services may not allow.

")

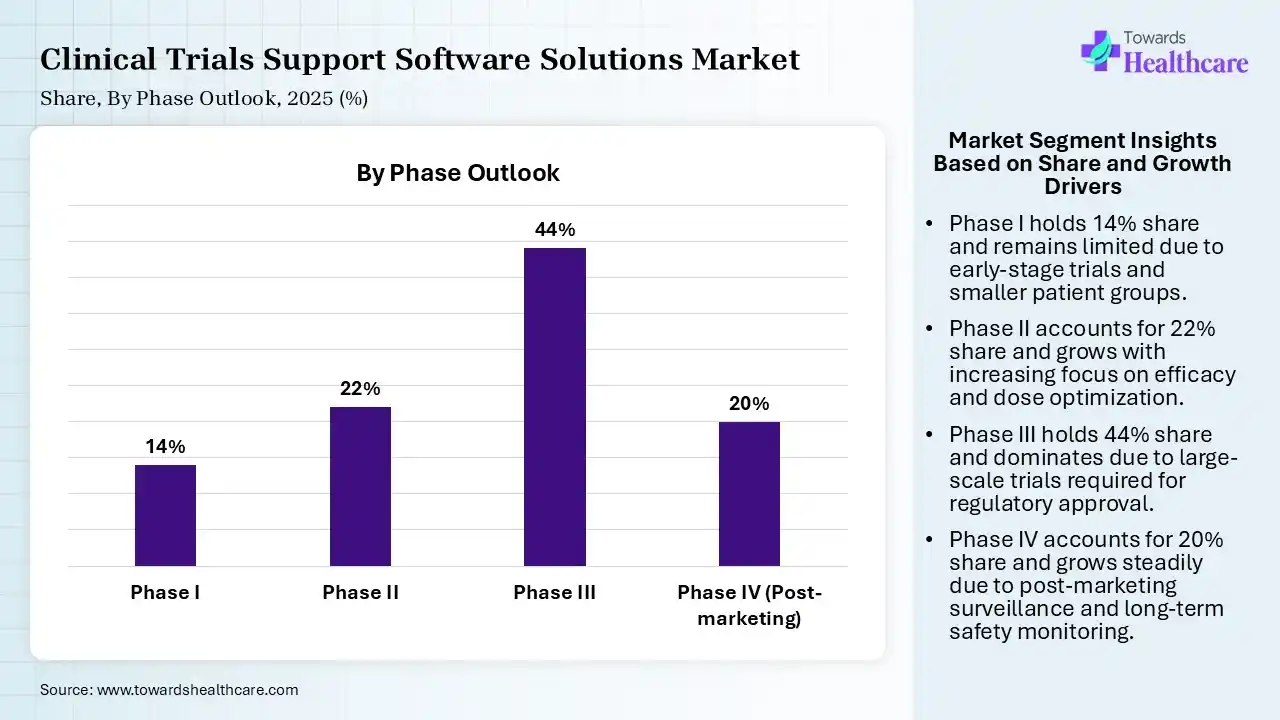

| Segments | Shares % |

| Phase I | 14% |

| Phase II | 22% |

| Phase III | 44% |

| Phase IV (Post-marketing) | 20% |

Why is Phase III Segment Dominant in the Market?

In 2025, the phase III segment held the dominating share of 44% of the clinical trials support software solutions market, as phase III trials offer a massive amount of data required for the package insert and labeling of a drug, after it has been FDA-approved. Phase III trials offer the highest level of indication for showing the effectiveness of novel interventions or treatments.

Phase I

Whereas, the phase I segment is the fastest growing in the market as phase 1 clinical trials are an important component of assessing products and solutions, including novel drugs, drug combinations. Phase 1 clinical trials enable novel treatments to progress further in drug development or halt that process altogether.

")

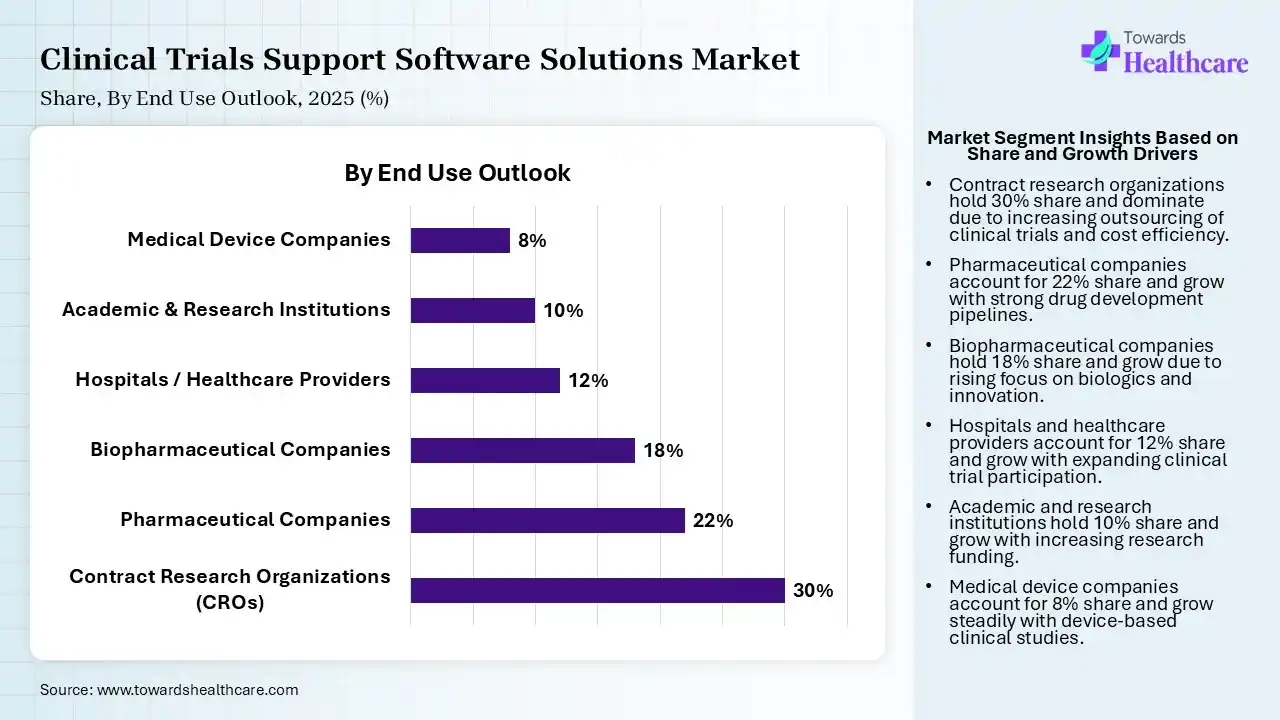

| Segments | Shares % |

| Contract Research Organizations (CROs) | 30% |

| Pharmaceutical Companies | 22% |

| Biopharmaceutical Companies | 18% |

| Hospitals / Healthcare Providers | 12% |

| Academic & Research Institutions | 10% |

| Medical Device Companies | 8% |

What Made the CROs Segment Dominant in the Clinical Trials Support Software Solutions Market in 2025?

In 2025, the CROs segment captured the largest revenue share of 30% of the market as CROs use advanced technologies and software stages to drive efficient communication, document sharing, and task tracking. By allowing more effective trial execution, CROs support patients in gaining earlier access to novel therapies. CROs support complex pre-clinical requirements such as toxicology programs followed by IND applications.

Biopharmaceutical Companies

Whereas the biopharmaceutical companies segment is the fastest growing in the clinical trials support software solutions market, as a flexible clinical trials platform has reduced running expenses and basic data management, enabling more creative trial designs and simple updates throughout a study. Clinical trial software corporations create tools that allow the well-organized planning, management, and tracking of clinical study information.

")

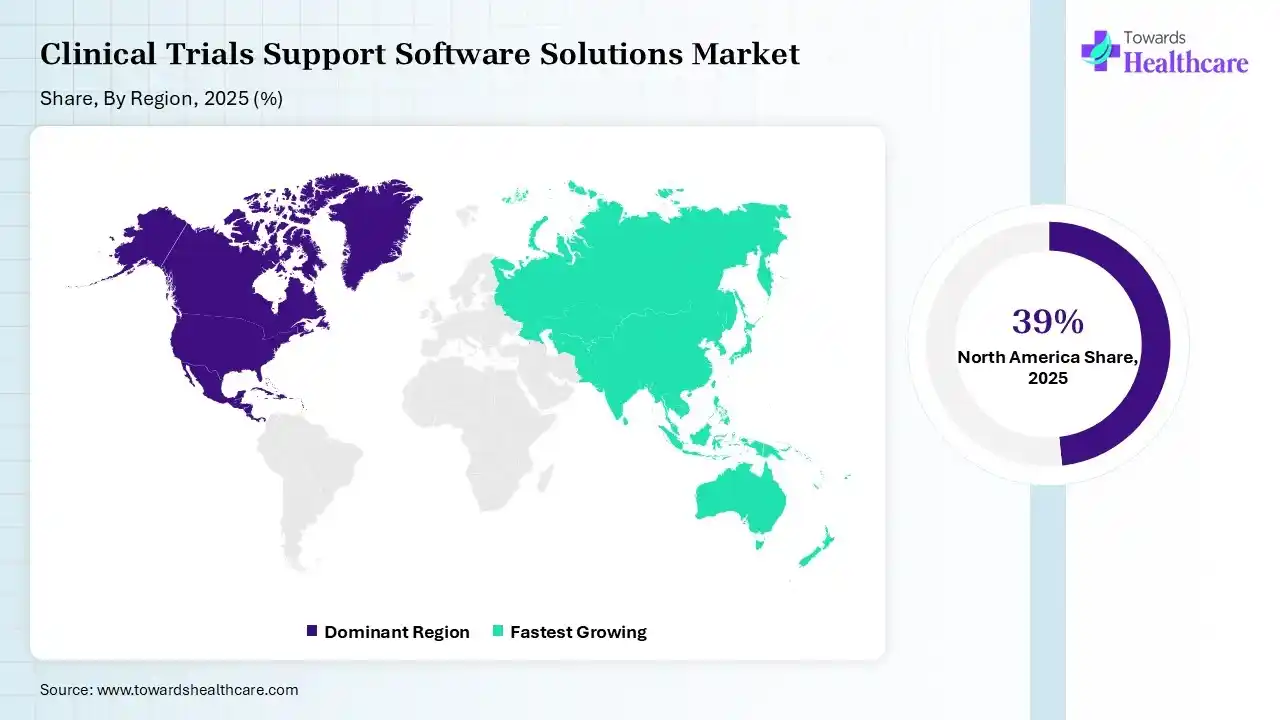

In 2025, North America dominated the clinical trials support software solutions market with the share of 39% by capturing a significant share, driven by its extremely advanced healthcare IT infrastructure, significant R&D spending, a supportive government environment, specifically from the FDA, and the presence of leading technology and pharmaceutical companies. Government bodies such as the U.S. Food and Drug Administration (FDA) and Health Canada offer clear guidelines and actively encourage the use of advanced technologies, like Artificial Intelligence (AI) and decentralized trial models.

For Instance,

US Market Growth

The U.S. is a focus of technological novelty, with various tech organizations and startups focusing on clinical trial solutions. There is a high rate of initial acceptance and implementation of advanced technologies such as AI, machine learning, cloud-based platforms, and remote patient monitoring equipment, which improves trial design, patient needs, and data monitoring.

For Instance,

Canada Strong Clinical Research Ecosystem Fuels Market Growth

Canada’s clinical trials support software solutions market is growing significantly due to increasing pharmaceutical and biotechnology research, expanding decentralized clinical trials, and strong government support for life science innovation. Rising adoption of cloud-based eClinical platforms, AI-driven trial management, and electronic data capture systems is improving trial efficiency. Additionally, the presence of leading CROs, advanced healthcare infrastructure, and growing investments in digital clinical research continue to drive market expansion.

Asia Pacific is expected to grow at the fastest CAGR in the clinical trials support software solutions market by 22% share, as the Asia Pacific is a hub to over half the world's population, offering a large and genetically varied pool of potential clinical trial participants. This increases the patient recruitment procedure, which is often a major bottleneck in other regions such as North America and Europe, meaningfully lowering trial timelines. Major countries in the region, such as China, Japan, South Korea, and India, have applied streamlined and effective government approval processes, aligning their standards with international guidelines such as Good Clinical Practice (GCP).

India Market Growth

In India, conducting clinical trials is 50% more affordable than in countries such as the U.S. or Europe due to lower operational costs and a competitive labor force. This expense advantage enables sponsors (pharmaceutical organizations) to exploit their research and development (R&D) funds while maintaining high-quality standards that meet international programmes (ICH-GCP).

Europe is poised for significant growth in the clinical trials support software solutions market by 28% share, with an integration of an advanced healthcare infrastructure, a helpful government environment, major R&D spending, and the early acceptance of advanced digital technologies. Strict regulations set by the European Medicines Agency (EMA) and national bodies, like the Clinical Trials Regulation (CTR) and the General Data Protection Regulation (GDPR), drive the demand for compliant, reliable digital platforms.

UK Market Growth

In the UK, proactive digital alteration, a unified healthcare system (NHS), a supportive government environment, and a focus on high-quality data and innovation. The National Health Service (NHS) offers a unique, national infrastructure with well-characterised and diverse patient populations, easing the collection of high-quality, real-world data vital for research

Germany’s Advanced Clinical Research Infrastructure Drive Market Growth

Germany’s clinical trials support software solutions makret is growing significantly due to its strong pharmaceutical and biotechnology industries, well-established clinical research infrastructure, and high adoption of digital health technologies. Increasing use of AI-powered trial management, cloud-based eClinical platforms, and electronic data capture systems is improving operational efficiency. Additionally, supportive regulatory frameworks, growing CRO partnerships, and rising investments in precision medicine continue to accelerate market expansion.

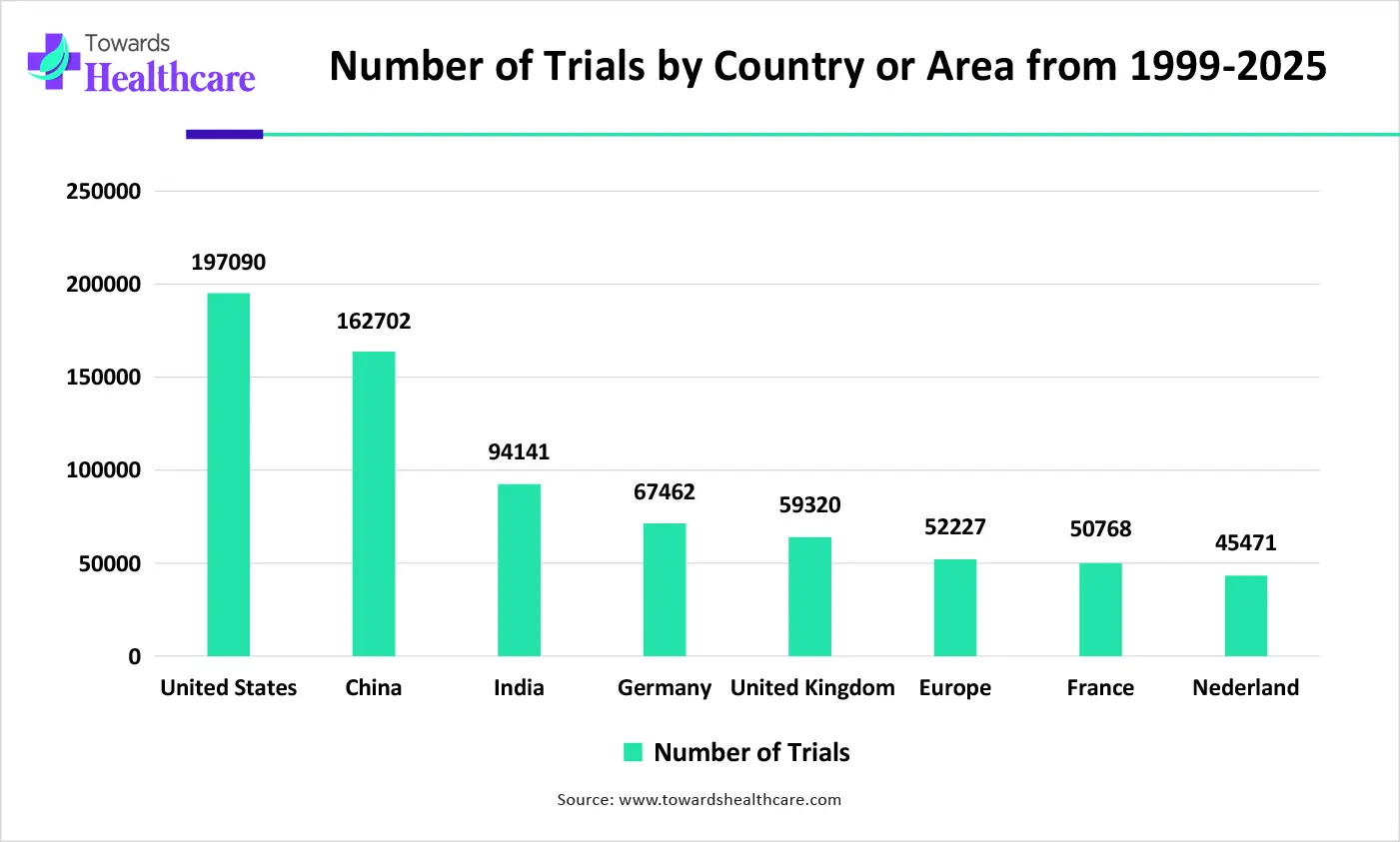

Number of trials by country or area from 1999-2025

| Region | Number of trials from 1999-2025 |

| United States | 197090 |

| China | 162702 |

| India | 94141 |

| Japan | 67462 |

| Germany | 59320 |

| United Kingdom | 52227 |

| France | 50768 |

| Nederland | 45471 |

| Ecosystem Category | Key Participants | Role in Market |

| Technology Providers | Oracle, Dassault Systèmes, Microsoft (cloud infrastructure) | Provide core cloud, database, and enterprise software infrastructure for clinical trial platforms |

| Product Manufacturers | Pharmaceutical & biotech companies (e.g., Pfizer, Novartis) | Generate demand and use platforms for trial execution |

| Service Providers | CROs like IQVIA, ICON, Parexel | Deliver outsourced clinical trial execution and integrated software services |

| Platform Providers | Medidata, Veeva Systems, Oracle Clinical One | Offer end-to-end clinical trial management ecosystems |

| CROs/CDMOs | IQVIA, ICON plc, Parexel | Manage trials and deploy proprietary or licensed clinical systems |

| Software Vendors | Medidata, Veeva, Medrio, Clario, Castor | Provide specialized EDC, CTMS, RTSM, and eCOA solutions |

| Research Institutions | NIH-funded centers, academic hospitals | Conduct investigator-led trials and adopt digital trial systems |

| End-User Industries | Pharma, biotech, medtech, diagnostics | Primary consumers of clinical trial software solutions |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 63% | 25% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medidata Solutions (Dassault Systèmes) | New York, New York | USA | Global leader in clinical trial cloud platforms with deep penetration in Phase I–IV trials | Medidata Rave EDC, CTMS, RTSM, eCOA, clinical analytics platform |

| IQVIA | Durham, North Carolina | USA | Combines CRO services with advanced clinical data and technology platforms at global scale | IQVIA Clinical Trial Management, analytics, real-world data platforms, EDC solutions |

| Veeva Systems | Pleasanton, California | USA | Dominant SaaS provider for life sciences with strong CTMS and clinical operations suite | Veeva Vault Clinical Suite (CTMS, eTMF, study startup tools) |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medrio | San Francisco, California | USA | Specialized EDC and eClinical software provider focused on mid-market and decentralized trials | Medrio EDC, ePRO, RTSM, data capture tools |

| Clario | Philadelphia, Pennsylvania | USA | Strong provider of endpoint data solutions for clinical trials, especially imaging and eCOA | Clinical endpoint analytics, imaging platforms, eCOA/ePRO systems |

| Signant Health | Blue Bell, Pennsylvania | USA | Focused on patient engagement and decentralized clinical trial technologies | eCOA, RTSM, patient engagement platforms |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| OpenClinica | Waltham, Massachusetts | USA | Established EDC platform widely used in academic and mid-scale trials | OpenClinica EDC, clinical data management tools |

| Lokavant | New York, New York | USA | AI-driven clinical trial intelligence and predictive analytics provider | Trial feasibility analytics, site selection intelligence |

In April 2026, “This collaboration represents an important step toward expediting how clinical trial data is submitted to and reviewed by the FDA. With Paradigm Health’s platform, clinical trial data can be analysed for key signals in near real time and shared with trial sponsors and the FDA in days, rather than months. This means that regulators, sponsors, and providers can have a continuous view of safety and efficacy. By modernising the flow of information from sites to sponsors to regulators, we have an opportunity to accelerate the delivery of innovative therapies to patients across the country”, said, Kent Thoelke, founder and CEO of Paradigm Health.

Strength

Weakness

Opportunity

Threats

By Product Outlook

By Phase Outlook

By End Use Outlook

By Regional Outlook (Revenue, USD Million, 2021 - 2033)

North America

Europe

Asia Pacific

Latin America

Middle East and Africa (MEA)

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar