")

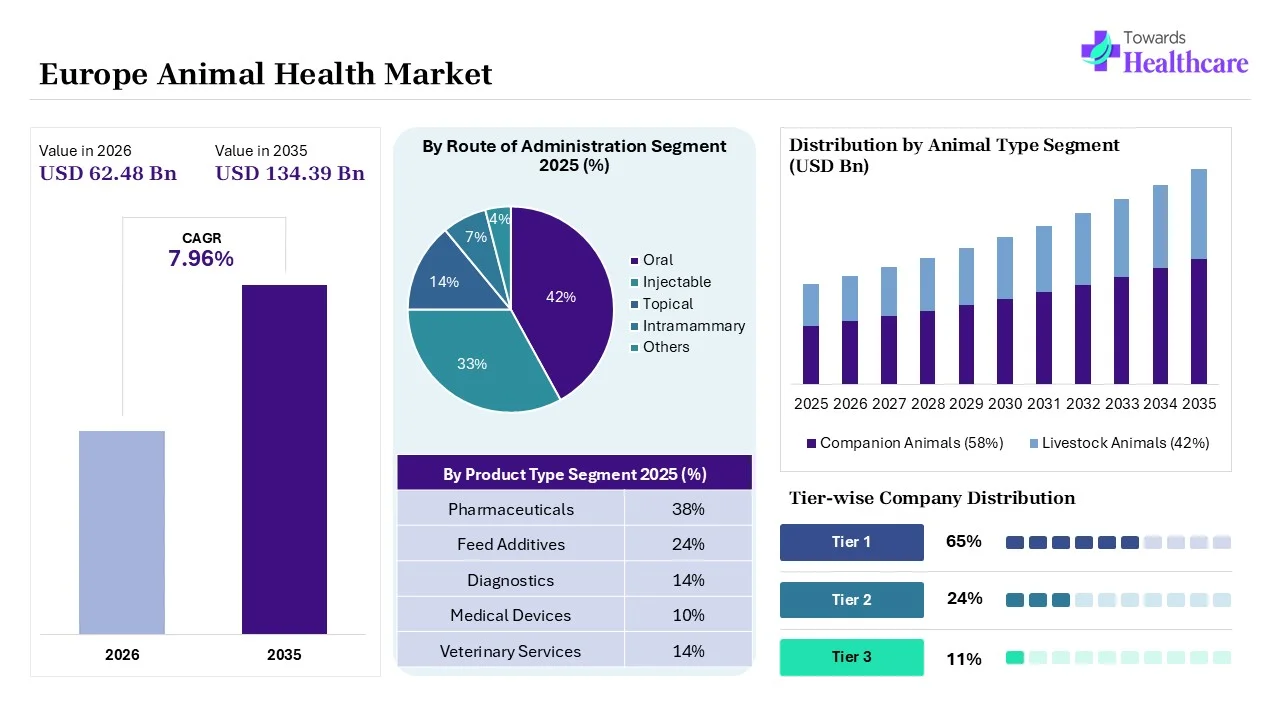

The Europe animal health market size was estimated at USD 62.48 billion in 2025 and is predicted to increase from USD 67.45 billion in 2026 to approximately USD 134.39 billion by 2035, expanding at a CAGR of 7.96% from 2026 to 2035. Growing pet ownership in Europe is increasing the demand for various animal health solutions. Growing zoonotic diseases, expanding pet insurance, sustainability initiatives, investments, and new product launches are also enhancing the market growth.

")

The Europe animal health market is driven by growing pet humanization trends, a shift towards preventive veterinary vaccines, and demand for animal monoclonal antibody therapies. The Europe animal health encompasses the development, production, and distribution of veterinary products for diagnosis, prevention, management, and treatment of animal diseases across Europe. They also help in controlling and preventing disease outbreaks, monitoring animal health, supporting breeding practices, and ensuring the quality and safety of animal-derived products.

The Europe animal health market is also benefiting from increasing adoption of digital veterinary services and connected livestock management systems. Farmers and veterinarians are using wearable sensors, health monitoring software, and data analytics to improve animal care and productivity. Rising awareness of zoonotic diseases is encouraging stronger surveillance and faster diagnosis across both livestock and companion animals. Growing investments in veterinary research are supporting the development of innovative biologics, advanced diagnostics, and targeted therapies. Sustainable livestock farming practices and stricter regulations on antibiotic use are creating demand for preventive healthcare solutions. Collaboration between research institutions, veterinary clinics, and pharmaceutical companies is accelerating innovation while improving disease management, food safety, and overall animal welfare across Europe.

AI plays a vital role in early animal disease diagnosis, where its predictive analytics also help in detecting disease outbreaks. It is also used in the development of smart wearable devices, personalized treatment plans, automated veterinary imaging solutions, and automated farm management. AI is also used in remote consultation, precision livestock farming, drug discoveries, and optimizing hospital workflow.

Expanding Veterinary Pharmaceutical and Diagnostic Solutions

Growing animal diseases are increasing the demand for effective diagnostic and treatment options. This is driving the development of advanced veterinary drugs, vaccines, biologics, molecular diagnostics, and point-of-care testing solutions.

Pet Insurance on the Rise

Expanding pet insurance policies are attracting the pet owners and enhancing the accessibility of advanced animal health solutions. This supports the growth of complex surgical and preventive healthcare.

Rising Sustainability Initiatives

The stringent European regulations are driving the sustainable farming processes to reduce the environmental impact. This is promoting the adoption of eco-friendly animal health care products.

| Table | Scope |

| Market Size in 2026 | USD 67.45 Billion |

| Projected Market Size in 2035 | USD 134.39 Billion |

| CAGR (2026 - 2035) | 7.96% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Animal Type, By Indication, By Distribution Channel, By End User, By Route of Administration, By Region |

| Top Key Players | Boehringer Ingelheim Animal Health, Zoetis Inc., MSD Animal Health, HIPRA, Ceva Santé Animale, Elanco Animal Health, Virbac S.A., Vetoquinol S.A., Krka, d.d., Dechra Pharmaceuticals PLC |

")

| Segment | Share 2025 (%) |

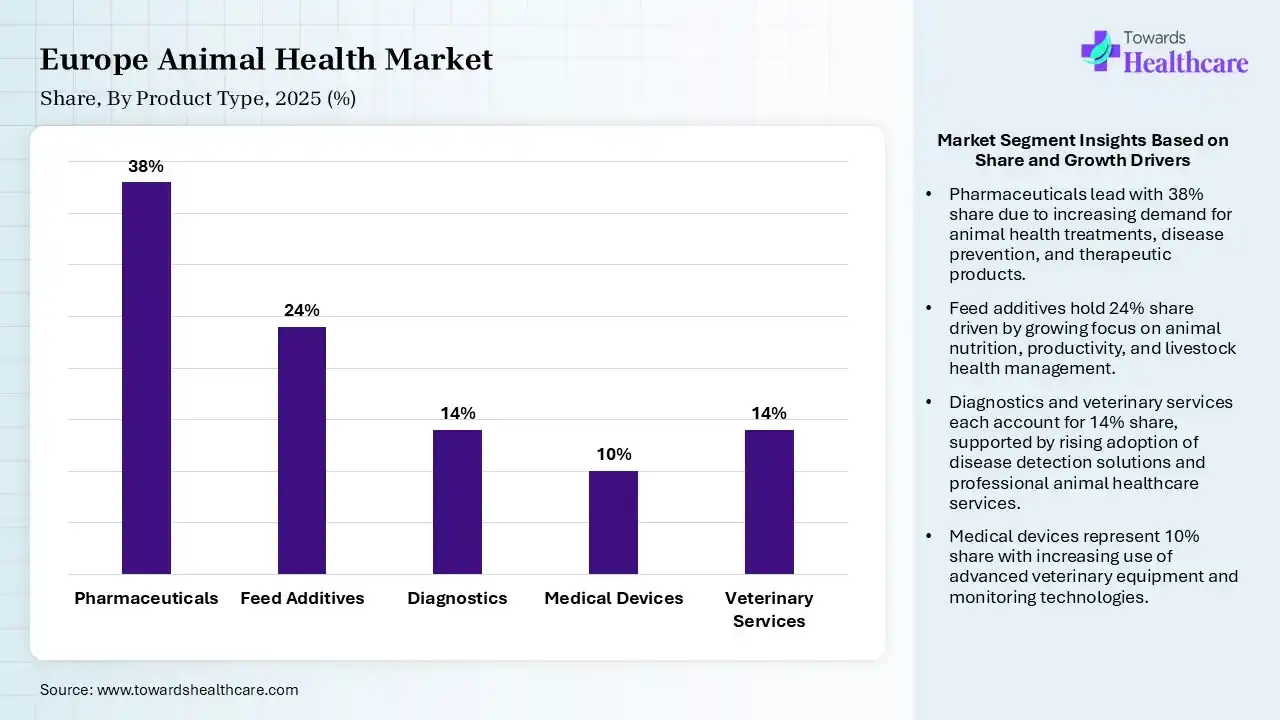

| Pharmaceuticals | 38% |

| Feed Additives | 24% |

| Diagnostics | 14% |

| Medical Devices | 10% |

| Veterinary Services | 14% |

The Pharmaceuticals Segment Dominated the Market With 38% in 2025

The pharmaceuticals segment led the Europe animal health market with 38% share in 2025, due to growth in the prevalence of zoonotic diseases among livestock and companion animals. Veterinary clinics continued expanding prescription drug utilization. Strong vaccine innovation also supported preventive healthcare demand.

The feed additives segment held the second-largest share of 24% of the market in 2025, due to livestock productivity optimization, which drives additive demand across poultry and cattle farming. Increasing restrictions on antibiotic growth promoters also encourage probiotic adoption. Sustainable nutrition trends also accelerate specialty additive penetration.

The diagnostics segment held 14% of the Europe animal health market share in 2025 and is expected to witness the fastest growth with a CAGR of 9.6% during the forecast period, as rapid disease detection technologies gain traction in commercial veterinary practices. Molecular diagnostics adoption is also increasing due to outbreak monitoring needs. Precision livestock farming also supports diagnostic investments.

The medical devices segment held 10% of the market share in 2025, driven by growing surgical procedures, which increase equipment utilization in veterinary hospitals. Monitoring technologies also improve pet treatment outcomes. Advancements in portable veterinary devices also support their adoption.

")

| Segment | Share 2025 (%) |

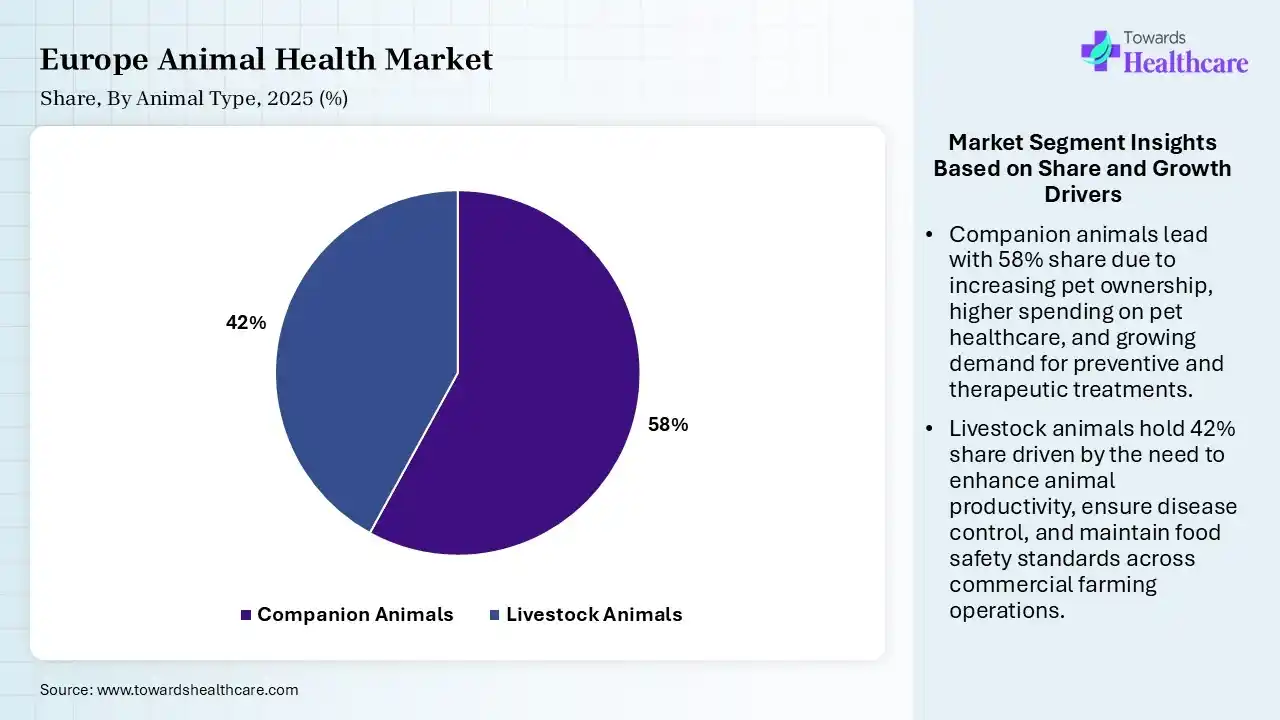

| Companion Animals | 58% |

| Livestock Animals | 42% |

The Companion Animals Segment Dominated the Market With 58% in 2025

The companion animals segment accounted for the highest revenue share of 58% of the Europe animal health market in 2025, and is expected to show the highest growth with a CAGR of 8.9% during the forecast period, driven by increased pet ownership across urban Europe, which drives healthcare spending. Premium veterinary care adoption continued rising. Humanization trends also strengthened demand for advanced therapies.

The livestock animals segment held the second-largest share of 42% of the market in 2025, as commercial livestock disease prevention sustains veterinary investments. Rising protein consumption also supports livestock productivity initiatives. Regulatory compliance also strengthens herd health monitoring.

")

| Segment | Share 2025 (%) |

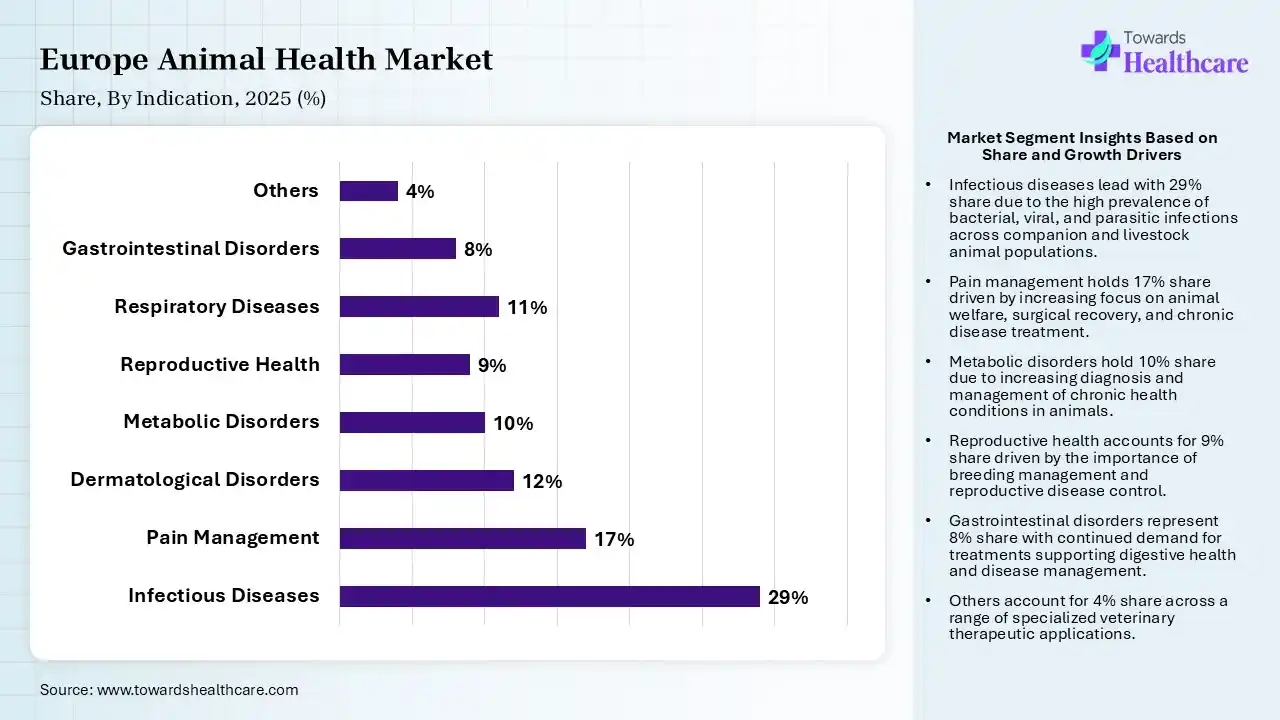

| Infectious Diseases | 29% |

| Pain Management | 17% |

| Dermatological Disorders | 12% |

| Metabolic Disorders | 10% |

| Reproductive Health | 9% |

| Respiratory Diseases | 11% |

| Gastrointestinal Disorders | 8% |

| Others | 4% |

The Infectious Diseases Segment Dominated the Market With 29% in 2025

The infectious diseases segment held a major revenue share of 29% of the Europe animal health market in 2025, as disease outbreaks continued driving vaccine and therapeutic demand. Cross-border livestock trade also increased monitoring requirements. Government surveillance programs also supported investment growth.

The pain management segment held the second-largest share of 17% of the market in 2025, as the aging pet population increases chronic pain treatment adoption. Orthopedic procedures also boost analgesic demand. Improved pain awareness also strengthens veterinary interventions.

The dermatological disorders segment held 12% of the Europe animal health market share in 2025, due to rising skin allergies and infections, supporting therapeutic utilization. Companion animal grooming trends also improve diagnosis rates. Advanced dermatology formulations also enhance treatment outcomes.

The metabolic disorders segment held 10% of the market share in 2025 and is expected to expand rapidly with a CAGR of 8.50% during the forecast period, driven by the continued increase in obesity and diabetes prevalence in pets. Specialized nutritional therapies are also supporting disease management. Early diagnostics also improve treatment adoption.

")

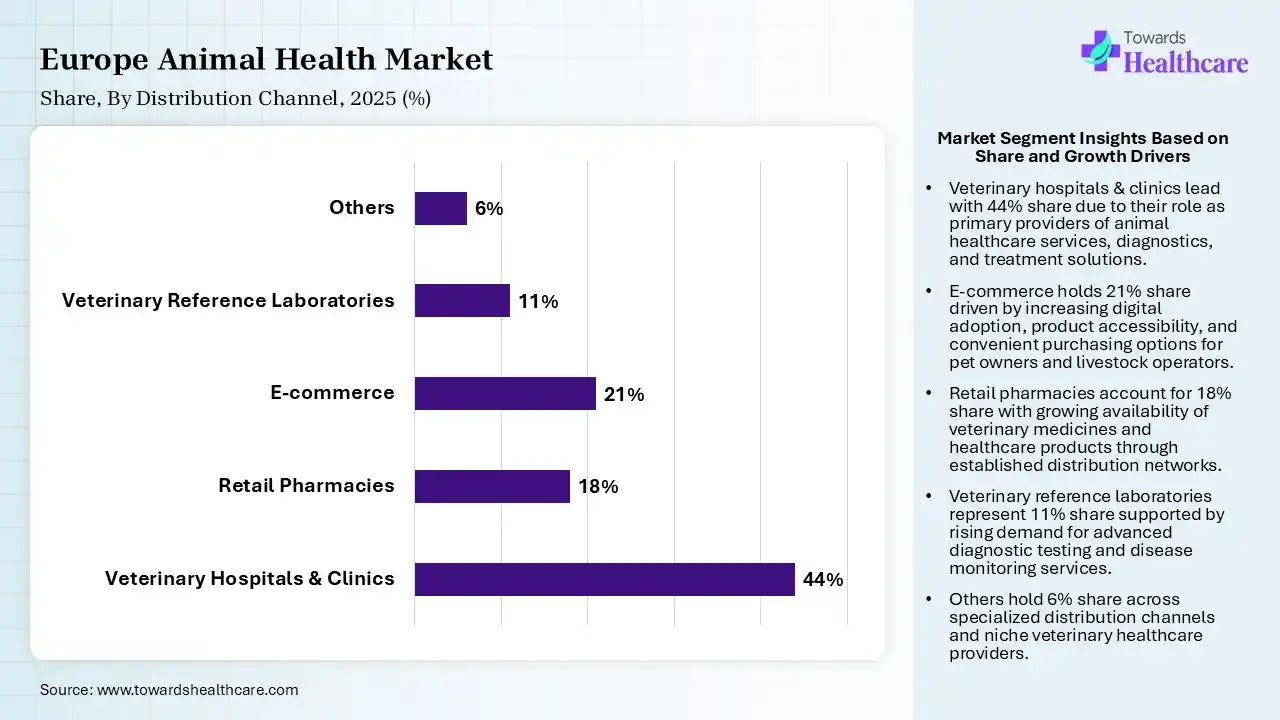

| Segment | Share 2025 (%) |

| Veterinary Hospitals & Clinics | 44% |

| Retail Pharmacies | 18% |

| E-commerce | 21% |

| Veterinary Reference Laboratories | 11% |

| Others | 6% |

The Veterinary Hospitals & Clinics Segment Dominated the Market With 44% in 2025

The veterinary hospitals & clinics segment contributed the biggest revenue share of 44% of the Europe animal health market in 2025, driven by increased clinical visits, which supported direct veterinary product sales. Advanced treatment infrastructure also strengthened purchasing volumes. Companion animal care expansion also increased channel growth.

The e-commerce segment held the second-largest share of 21% of the market in 2025 and is expected to gain the highest share with a CAGR of 11.8% during the forecast period, as digital purchasing platforms improve product accessibility across Europe. Subscription-based pet healthcare models also increase online sales. Competitive pricing also strengthens e-commerce adoption.

The retail pharmacies segment held 18% of the Europe animal health market share in 2025, driven by OTC veterinary products gaining accessibility through retail expansion. Pet wellness products also support recurring demand. Consumer convenience also strengthens pharmacy utilization.

The veterinary reference laboratories segment held 11% of the market share in 2025, as diagnostic outsourcing demand continues increasing among clinics. Advanced molecular testing also supports laboratory expansion. Disease surveillance programs also strengthen sample volumes.

")

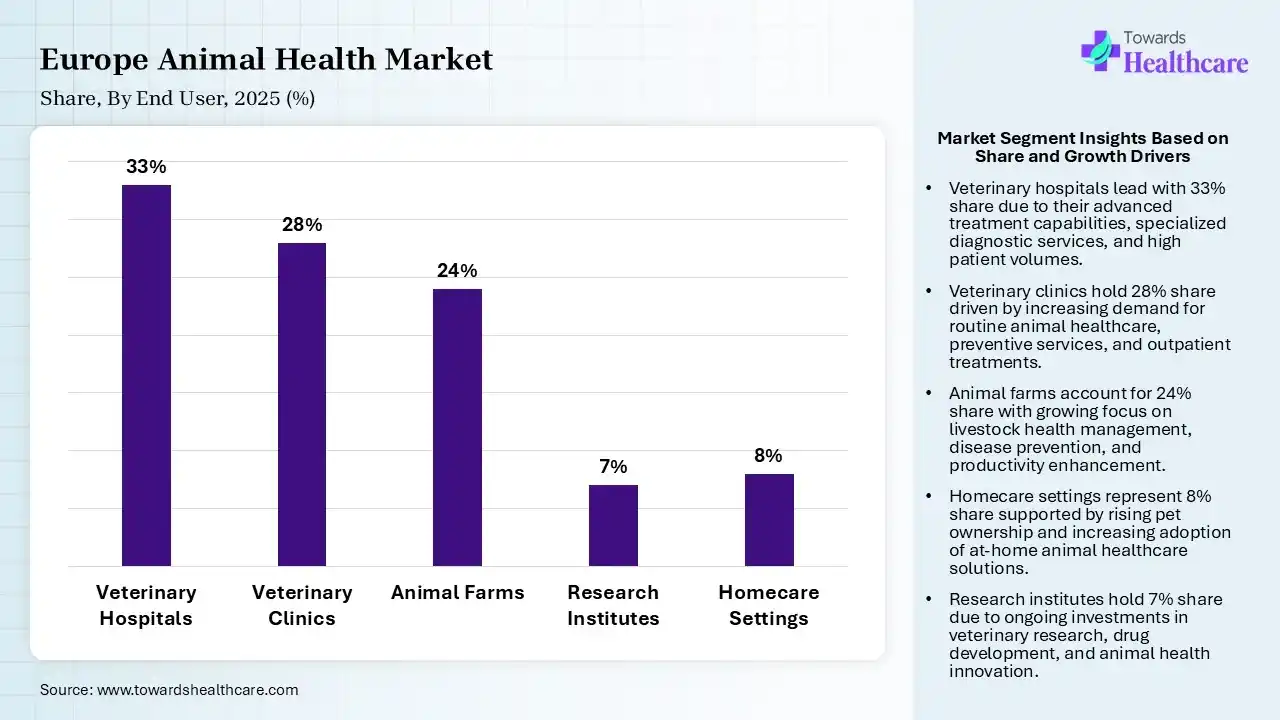

| Segment | Share 2025 (%) |

| Veterinary Hospitals | 33% |

| Veterinary Clinics | 28% |

| Animal Farms | 24% |

| Research Institutes | 7% |

| Homecare Settings | 8% |

The Veterinary Hospitals Segment Dominated the Market With 33% in 2025

The veterinary hospitals segment held the largest revenue share of 33% of the Europe animal health market in 2025, as advanced surgical and diagnostic capabilities attracted higher patient volumes. Emergency care expansion also supported hospital utilization. Premium companion animal care also strengthened revenue growth.

The veterinary clinics segment held the second-largest share of 28% of the market in 2025, due to preventive healthcare visits continuing to increase across clinics. Routine vaccinations and diagnostics are also sustaining recurring demand. Urban pet ownership also supports clinic expansion.

The animal farms segment held 24% of the Europe animal health market share in 2025, driven by livestock disease management programs, which drive veterinary product consumption. Productivity optimization also increases healthcare investments. Regulatory compliance also supports biosecurity spending.

The research institutes segment held 7% of the market share in 2025 and is expected to grow with the fastest CAGR of 8.9% during the forecast period, as veterinary R&D investments continue expanding across Europe. Advanced biologics and vaccine development also strengthen funding. Collaborative animal health research is also accelerating innovations.

Europe animal health market is significantly expanding during the forecast period, due to growing pet ownership. Increasing pet health awareness, the humanization trend, and spending are also increasing the adoption of various animal health products. Growing R&D activities, technological advancement, and government support are also enhancing the market growth.

UK Market Trends

The high companion animal volume in the UK drives the demand for animal healthcare products. The presence of robust veterinary clinics and insurance policies also attracts the pet owners. The growing focus on disease prevention is also increasing the demand for advanced diagnostic and treatment solutions.

Germany Market Trends

Germany consists of advanced veterinary hospitals, livestock industries, and veterinary pharmaceutical manufacturers, which promote the animal health products expansion. Increasing pet ownership and awareness are also increasing the demand for preventive animal health care products. Expanding tele-veterinary services and the focus on food safety have also increased their use.

France Market Trends

France remains a key market because of its strong livestock sector and growing pet care industry. The government supports animal health through disease surveillance programs, veterinary research funding, and strict animal welfare regulations. Rising adoption of vaccines, diagnostic tools, and digital livestock monitoring is driving market growth. Companies continue investing in research partnerships and new veterinary products to strengthen their presence. Competition remains strong as established manufacturers and emerging firms introduce innovative solutions for animal disease prevention and treatment

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Europe Animal Health Products |

| Boehringer Ingelheim Animal Health | Ingelheim, Germany | NexGard, Metacam, Ingelvac Circoflex, and Frontline |

| Zoetis Inc. | Parsippany, U.S. | Cytopoint, Librela, Apoquel, and Solensia |

| MSD Animal Health | Rahway, U.S. | Bravecto, Bovilis, and Nobivac |

| HIPRA | Amer, Spain | Hiprabovis, Ubac, and Suiseng |

| Ceva Santé Animale | Libourne, France | Feliway, Cardalis, Cevac, and Adaptil |

| Elanco Animal Health | Greenfield, U.S. | Seresto, Rumensin, Credelio, and Galliprant |

| Virbac S.A. | Carros, France | Canigen, Epi-Otic, Suprelorin, and Milpro |

| Vetoquinol S.A. | Lure, France | Zylkene, Flexadin, Marbocyl, and Cimalgex |

| Krka, d.d. | Novo Mesto, Slovenia | Enrorox, Rycarfa, Dehinel, and Fypryst |

| Dechra Pharmaceuticals PLC | Northwich, UK | Vetoryl, Cardisure, Felimazole, and Isathal |

In May 2026, VMD’s Deputy Chief Executive Officer and Director for Authorisations, Gavin Hall, said: “The launch of our new adverse event reporting service marks a significant step forward in how we gather and use safety data for animal medicines. Better reporting leads to better oversight, and ultimately better outcomes for animal health and welfare. We encourage anyone who observes problems with an animal medicine, whether that be a side effect in an animal, accidental exposure or injury to a human, or environmental contamination, to report it, and we’ve now made it easier than ever to do so.”

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Animal Type

By Indication

By Distribution Channel

By End User

By Route of Administration

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar