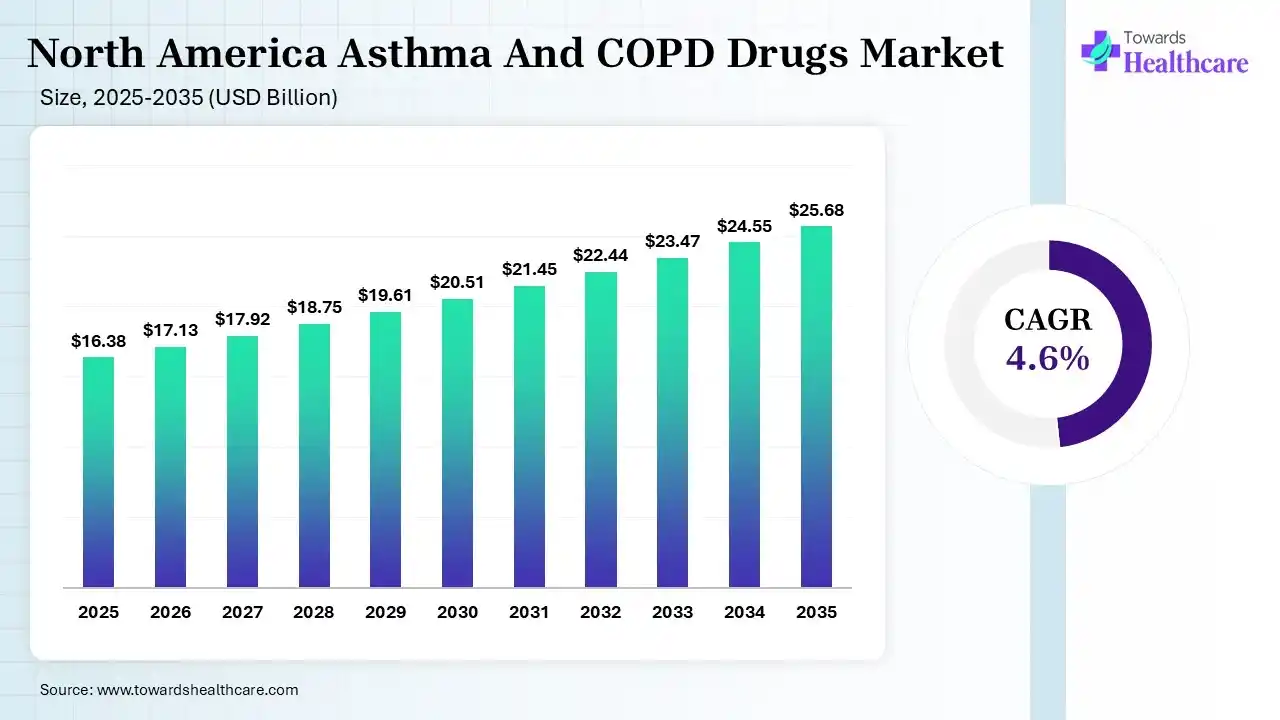

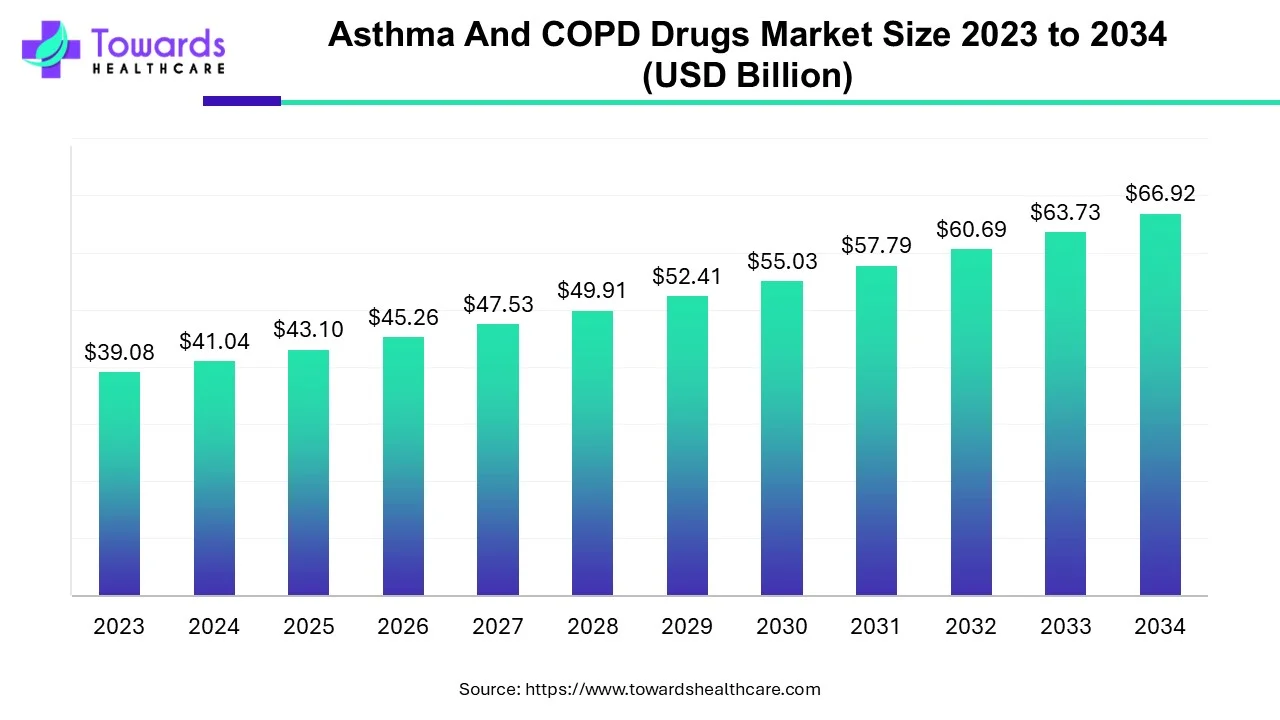

The North America asthma and COPD drugs market size was estimated at USD 16.38 billion in 2025 and is predicted to increase from USD 17.13 billion in 2026 to approximately USD 25.68 billion by 2035, expanding at a CAGR of 4.6% from 2026 to 2035. The growing geriatric population is leading to a rise in asthma and COPD diseases in North America, increasing the use of these medications. Growing demand for biologics, increasing health awareness, R&D activities, and new product launches are also enhancing the market growth.

")

The North America asthma and COPD drugs market was driven by increasing respiratory disease and demand for advanced drug delivery technologies. The North America asthma and COPD drugs refer to the development, production, and sales of drugs for the treatment of respiratory diseases across North America. These drugs help in improving lung function, reducing inflammation, and relieving symptoms, improving the patient's quality of life.

The use of AI in the North America asthma and COPD drugs market is increasing as they help in reducing asthma attacks and COPD flare-ups. It also helps in accurate disease detection and patient monitoring, ensuring improved treatment adherence. AI is also used in the development of smart inhalers, new respiratory drugs, and personalized treatment options, as it analyzes large healthcare datasets.

Expanding Adoption of Targeted Therapies

The growing health awareness and increasing incidences of asthma and COPD across North America are driving the demand for their effective treatment options. This, in turn, is increasing the adoption of targeted therapies for faster action and fewer side effects.

The Rise of New Drug Delivery Technologies

Growing technological advancements are increasing the development of advanced drug delivery solutions for the management of asthma and COPD. Smart inhalers and Bluetooth-enabled digital monitoring platforms are being developed.

Shift Towards Home Healthcare

Expansions of the telehealth platforms are promoting the shift towards home healthcare.This is driving online consultation, virtual disease management, remoted devices monitoring, and enhancing accessibility to the asthma and COPD drugs.

| Table | Scope |

| Market Size in 2026 | USD 17.13 Billion |

| Projected Market Size in 2035 | USD 25.68 Billion |

| CAGR (2026 - 2035) | 4.6% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Class, By Disease Type, By End User, By Prescription Type, By Region |

| Top Key Players | GlaxoSmithKline, Merck & Co., AstraZeneca, Viatris, Boehringer Ingelheim, Regeneron Pharmaceuticals, Teva Pharmaceuticals, Verona Pharma, Sanofi, Novartis |

")

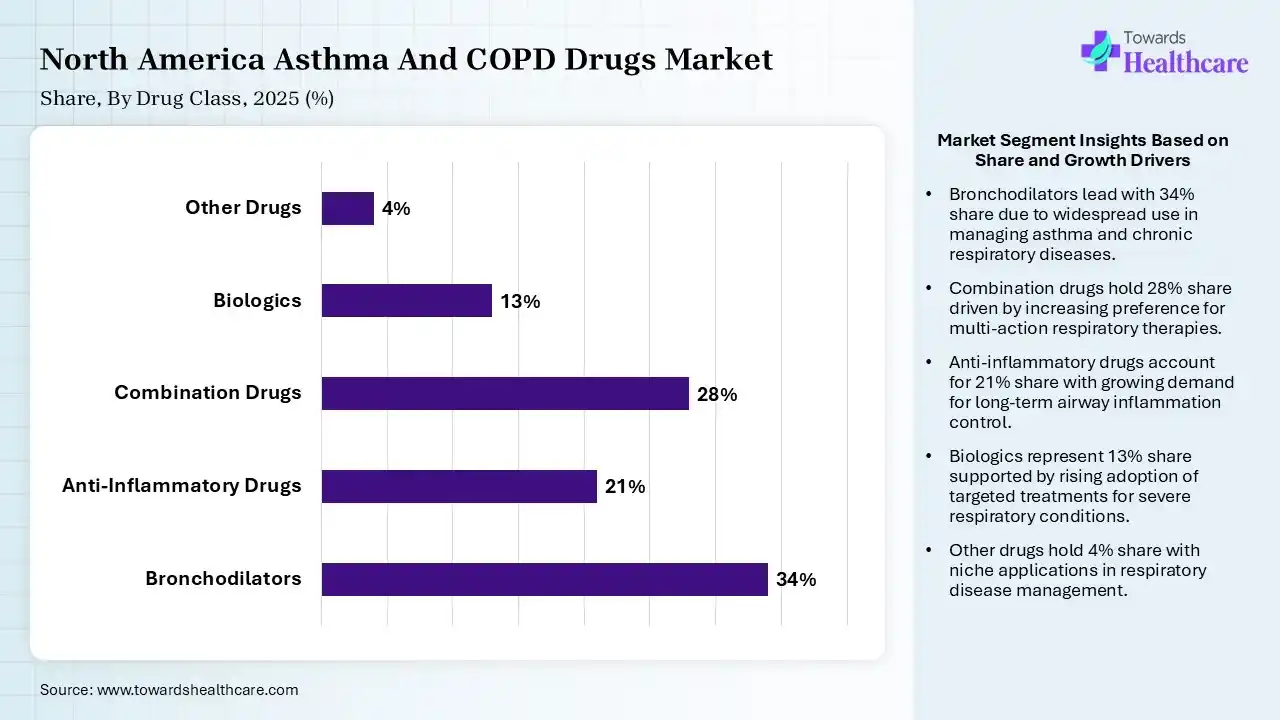

| Segment | Share 2025 (%) |

| Bronchodilators | 34% |

| Anti-Inflammatory Drugs | 21% |

| Combination Drugs | 28% |

| Biologics | 13% |

| Other Drugs | 4% |

The Bronchodilators Segment Dominated the Market With 34% in 2025

The bronchodilators segment led the North America asthma and COPD drugs market with 34% share in 2025, as physicians widely prescribed bronchodilators as first-line maintenance therapy for COPD and asthma management. Strong adoption of LABA and LAMA formulations also supported their long-term disease control. Growth in the smoking-related COPD prevalence also continued to sustain its demand.

The combination drugs segment held the second-largest share of 28% of the market in 2025, as they improve adherence and reduce exacerbation frequency in moderate-to-severe patients. Triple therapy adoption is also accelerating among COPD populations. Pharmaceutical companies continue launching advanced inhaler combinations.

The anti-inflammatory drugs segment held 21% of the North America asthma and COPD drugs market share in 2025, due to increasing diagnosis of chronic inflammatory airway diseases supporting corticosteroid utilization. Clinical guidelines also continue recommending ICS therapies for persistent asthma. Generic penetration also improves accessibility across North America.

The biologics segment held 13% of the market share in 2025 and is expected to witness the fastest growth with a CAGR of 8.20% during the forecast period, due to the rising prevalence of severe eosinophilic asthma. Precision medicine and biomarker-based treatment selection also increase biologic adoption. Favorable reimbursement for specialty respiratory drugs also supports market expansion.

")

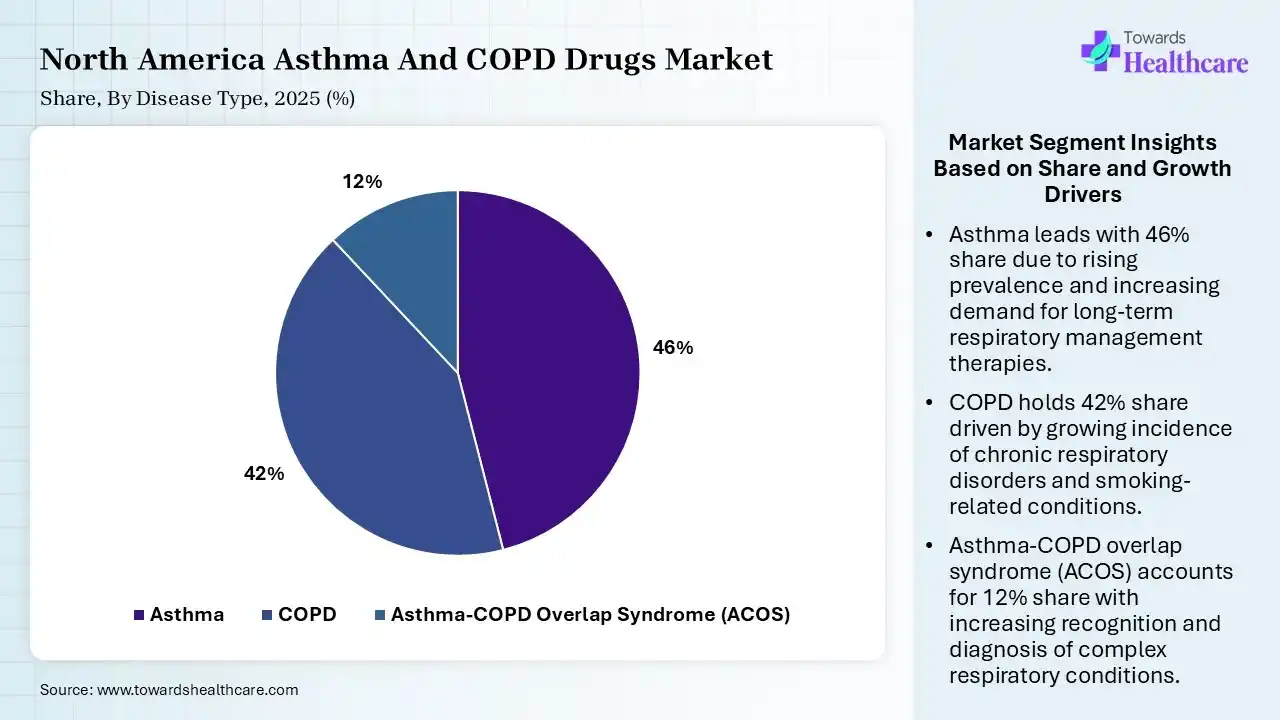

| Segment | Share 2025 (%) |

| Asthma | 46% |

| COPD | 42% |

| Asthma-COPD Overlap Syndrome (ACOS) | 12% |

The Asthma Segment Dominated the Market With 46% in 2025

The asthma segment accounted for the highest revenue share of 46% of the North America asthma and COPD drugs market in 2025, due to growth in environmental pollution and allergen exposure, which increased asthma prevalence rates. Early diagnosis initiatives also improved treatment penetration among pediatric and adult patients. Long-term controller therapy usage continued to expand.

The COPD segment held the second-largest share of 42% of the market in 2025, as aging populations and smoking-related lung damage increase COPD incidence across North America. Frequent hospitalizations also encourage preventive maintenance therapy adoption. Growing awareness campaigns also improve disease management compliance.

The asthma-COPD overlap syndrome (ACOS) segment held 12% of the North America asthma and COPD drugs market share in 2025 and is expected to show the highest growth with a CAGR of 6.20% during the forecast period, as physicians increasingly recognize overlap syndrome as a distinct respiratory condition. Combination biologics and triple therapies also improve treatment outcomes. Advanced diagnostic approaches are also supporting earlier identification of ACOS patients.

")

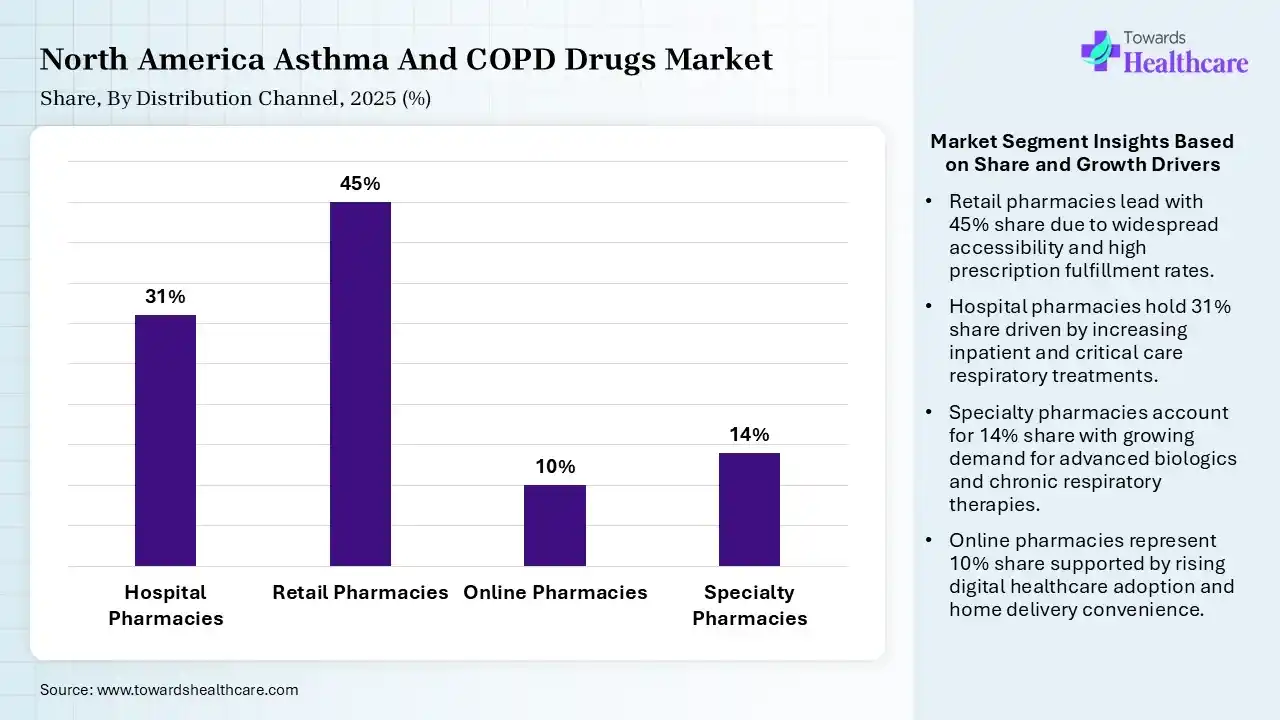

| Segment | Share 2025 (%) |

| Hospital Pharmacies | 31% |

| Retail Pharmacies | 45% |

| Online Pharmacies | 10% |

| Specialty Pharmacies | 14% |

The Retail Pharmacies Segment Dominated the Market With 45% in 2025

The retail pharmacies segment held a major revenue share of 45% of the North America asthma and COPD drugs market in 2025, driven by their strong accessibility for chronic respiratory medication refills. Broad insurance coverage also supported recurring prescription volumes. Chain pharmacy expansion also enhanced nationwide product availability.

The hospital pharmacies segment held the second-largest share of 31% of the market in 2025, as hospitals manage severe respiratory exacerbations requiring immediate drug dispensing. Growing inpatient COPD admissions also support institutional pharmacy sales. Growing specialty biologic therapies also increase hospital pharmacy utilization.

The specialty pharmacies segment held 14% of the North America asthma and COPD drugs market share in 2025, due to their efficient handling of high-cost biologics and complex respiratory therapies. Patient support programs also improve continuity of care. Growing biologic prescriptions also increase specialty dispensing demand.

The online pharmacies segment held 10% of the market share in 2025 and is expected to expand rapidly with a CAGR of 8.10% during the forecast period, driven by digital healthcare adoption, which accelerates online respiratory drug purchases. Home delivery convenience also improves medication adherence among chronic patients. E-prescription integration also supports online pharmacy growth.

")

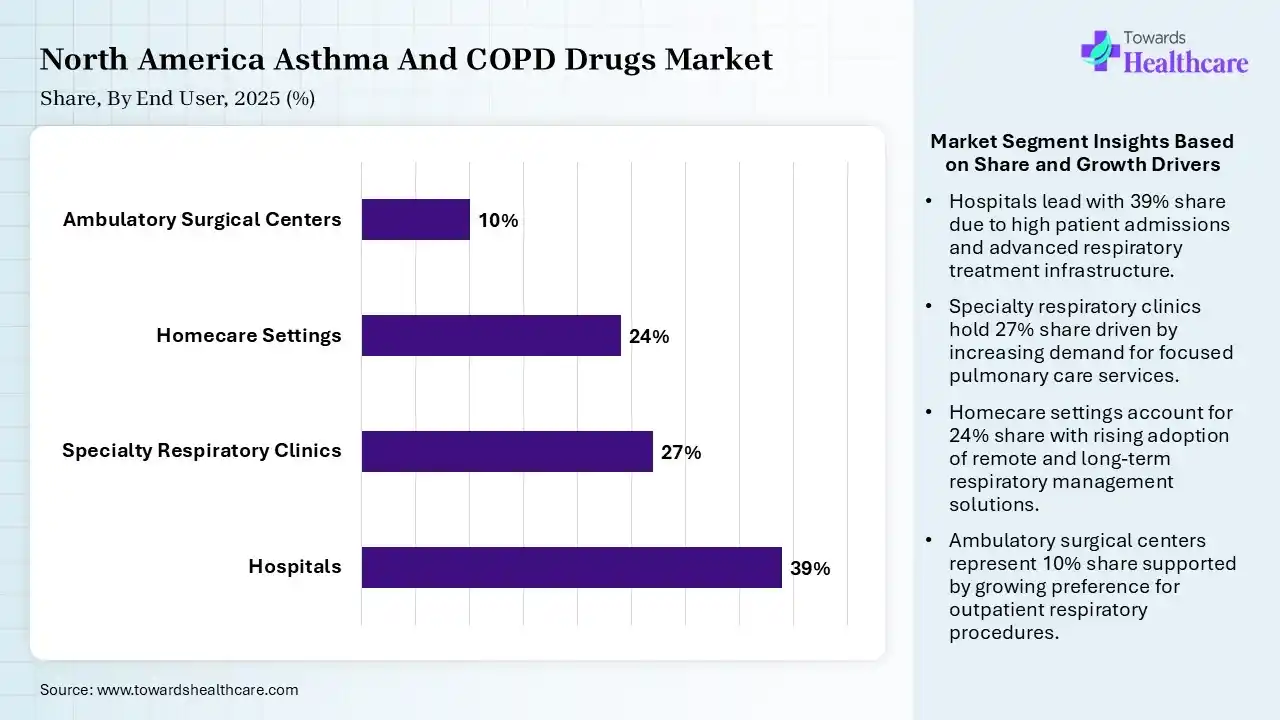

| Segment | Share 2025 (%) |

| Hospitals | 39% |

| Specialty Respiratory Clinics | 27% |

| Homecare Settings | 24% |

| Ambulatory Surgical Centers | 10% |

The Hospitals Segment Dominated the Market With 39% in 2025

The hospitals segment contributed the biggest revenue share of 39% of the North America asthma and COPD drugs market in 2025, as they are considered the primary treatment centers for acute asthma and COPD exacerbations. Growth in emergency admissions also sustained respiratory drug utilization. Advanced respiratory care infrastructure also supported therapeutic demand.

The specialty respiratory clinics segment held the second-largest share of 27% of the market in 2025, as specialized clinics increasingly manage severe and chronic respiratory disorders. Pulmonologists are adopting biologics and advanced inhalation therapies rapidly. Improved outpatient respiratory monitoring also supports clinic growth.

The homecare settings segment held 24% of the North America asthma and COPD drugs market share in 2025 and is expected to gain the highest share with a CAGR of 6.50% during the forecast period, due to growing chronic disease burden and aging populations. Portable nebulizers and inhalers also improve self-administration. Telehealth integration also enhances remote respiratory care.

The ambulatory surgical centers segment held 10% of the market share in 2025, as they support respiratory diagnostics and outpatient therapeutic procedures. Increasing minimally invasive pulmonary interventions sustains drug demand. Cost-effective outpatient care models also support market expansion.

The global asthma and COPD drugs market size was calculated at USD 43.10 billion in 2025, to reach USD 45.26 billion in 2026 is expected to be worth USD 70.27 billion by 2035, expanding at a CAGR of 5.01% from 2026 to 2035.

The North America asthma and COPD drugs market showed considerable growth, due to the growth in the asthma and COPD cases. High smoking rates and a geriatric population also contributed to their growth, which increased the use of various drugs. A rise in health awareness and R&D activities also enhanced the market growth.

U.S. Market Trends

The U.S. held the major revenue share of 78.8% in the North America asthma and COPD drugs market in 2025, due to large COPD and asthma patient pools, which supported consistent prescription volumes. High biologic adoption also promoted specialty respiratory therapy growth. Extensive insurance coverage also improved treatment accessibility.

Canada Market Trends

Canada held 21.2% share of the in 2025 and is expected to grow at the fastest CAGR of 4.80% during the forecast period, due to public healthcare coverage, which supports widespread respiratory treatment utilization. Rising pollution-related asthma cases are also increasing inhaler demand. Government awareness programs also improve disease diagnosis rates.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | North America Asthma and COPD Drugs |

| GlaxoSmithKline | Brentford, UK | Advair, Trelegy Eilipta, Ventolin, and Breo Ellipta |

| Merck & Co. | Rahway, U.S. | Singulair |

| AstraZeneca | Cambridge, UK | Symbicort, Fasenra, Pulmicort, and Breztri Aerosphere |

| Viatris | Canonsburg, U.S. | Wixela Inhub |

| Boehringer Ingelheim | Ingelheim am Rhein, Germany | Spiriva, Stiolto Respimat, and Combivent Respimat |

| Regeneron Pharmaceuticals | Tarrytown, U.S. | Dupixent |

| Teva Pharmaceuticals | Tel Aviv, Israel | ProAir HFA, Qvar RediHaler, and ArmonAir Digihaler |

| Verona Pharma | London, UK | Ohtuvayre |

| Sanofi | Paris, France | Dupixent |

| Novartis | Basel, Switzerland | Xolair |

Strengths

Weaknesses

Opportunities

Threats

By Drug Class

By Disease Type

By Distribution Channel

By End User

By Route of Administration

By Prescription Type

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar