")

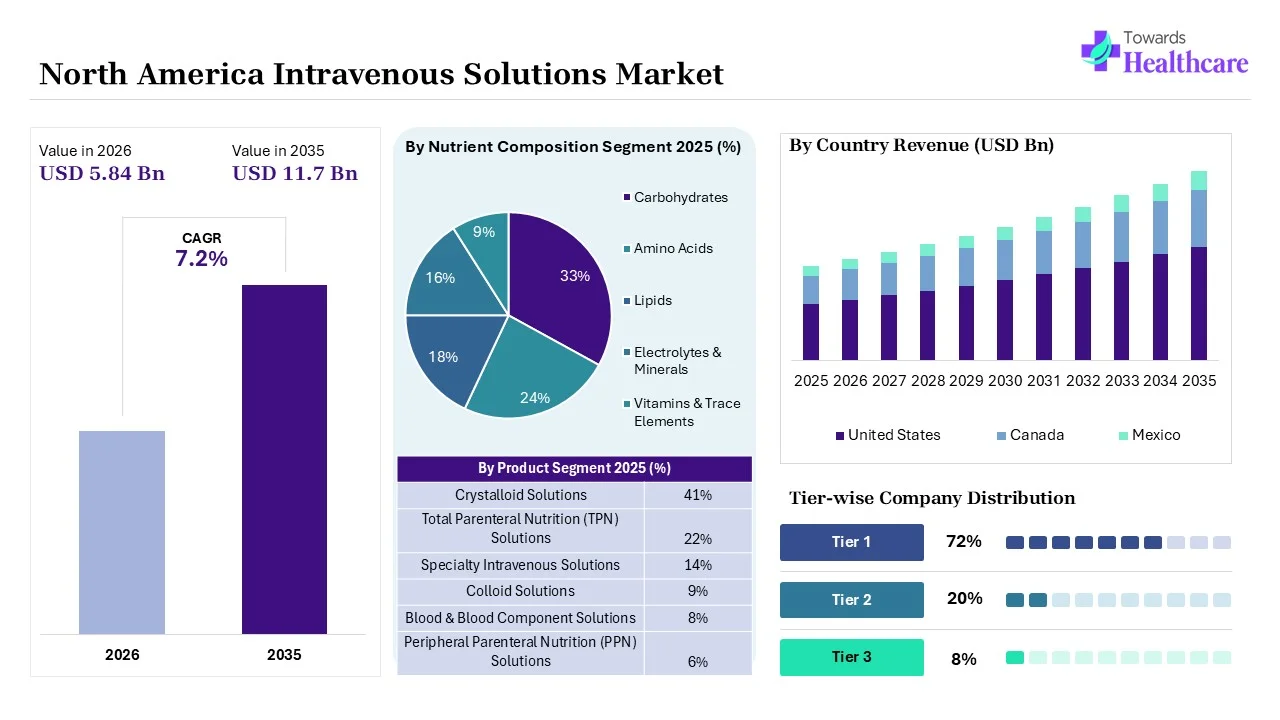

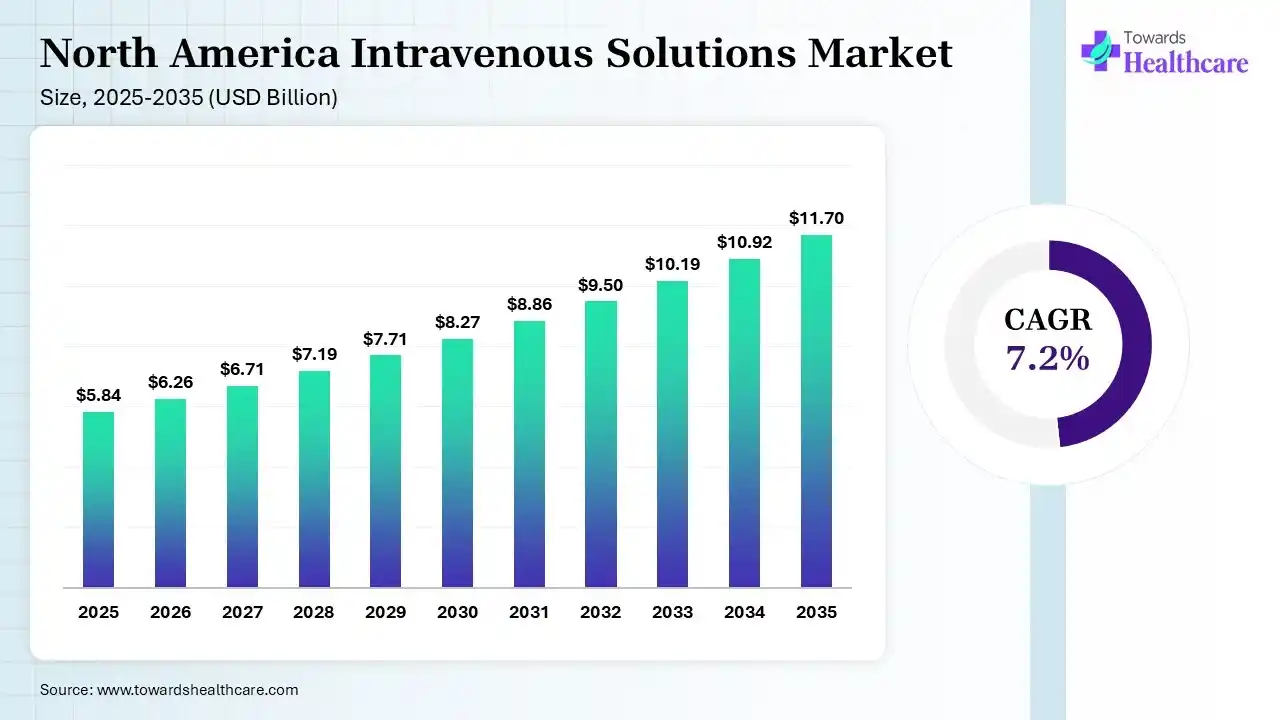

The North America intravenous solutions market size was estimated at USD 5.84 billion in 2025 and is predicted to increase from USD 6.26 billion in 2026 to approximately USD 11.7 billion by 2035, expanding at a CAGR of 7.2% from 2026 to 2035. The growth in the chronic disease burden in North America is increasing the use of intravenous solutions. Growing demand for ready-to-use solutions, increasing innovations, healthcare expenditures, and new solution launches are also enhancing the market growth.

")

The North America intravenous solutions market is driven by growing surgical procedures and at-home infusions. The intravenous solutions refer to the sterile liquid formulations across the healthcare sector. They are used for the treatment of infection, chronic disease, and dehydration.

AI offers a wide range of applications in the North America intravenous solutions market, by offering detection of contamination risk and forecasting IV solution demand. It is also used for the detection of infusion-related complications, reducing medication errors, and enhancing drug compatibility. AI is also used for personalized IV solution development, remote infusion therapy monitoring, and to develop smart infusion pumps.

Growing Home Infusion Therapy

Increasing telehealth platforms and home healthcare are encouraging remote patient monitoring. This is increasing the use of IV solutions for chronic disease management, enhancing affordability and patient convenience.

Escalating Ready-to-Use IV Solutions

To reduce the preparation time and contamination risk, the demand for ready-to-use intravenous solutions is increasing. They also help in reducing errors and promote their use during emergency conditions.

Expanding Innovations

With the growing health awareness and patients' needs, various intravenous solutions are being developed. Parenteral nutrition, specialty drugs, electrolyte-balanced, and customized IV solutions are also being formulated.

| Table | Scope |

| Market Size in 2026 | USD 6.26 Billion |

| Projected Market Size in 2035 | USD 11.7 Billion |

| CAGR (2026 - 2035) | 7.2% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Nutrient Composition, By Packaging Type, By Application, By End User, By Osmolarity, By Route of Administration, By Patient Group, By Distribution Channel, By Region |

| Top Key Players | Bedrocan International, Stenocare A/S, PharmaHemp, Endoca, Kanabo Group |

")

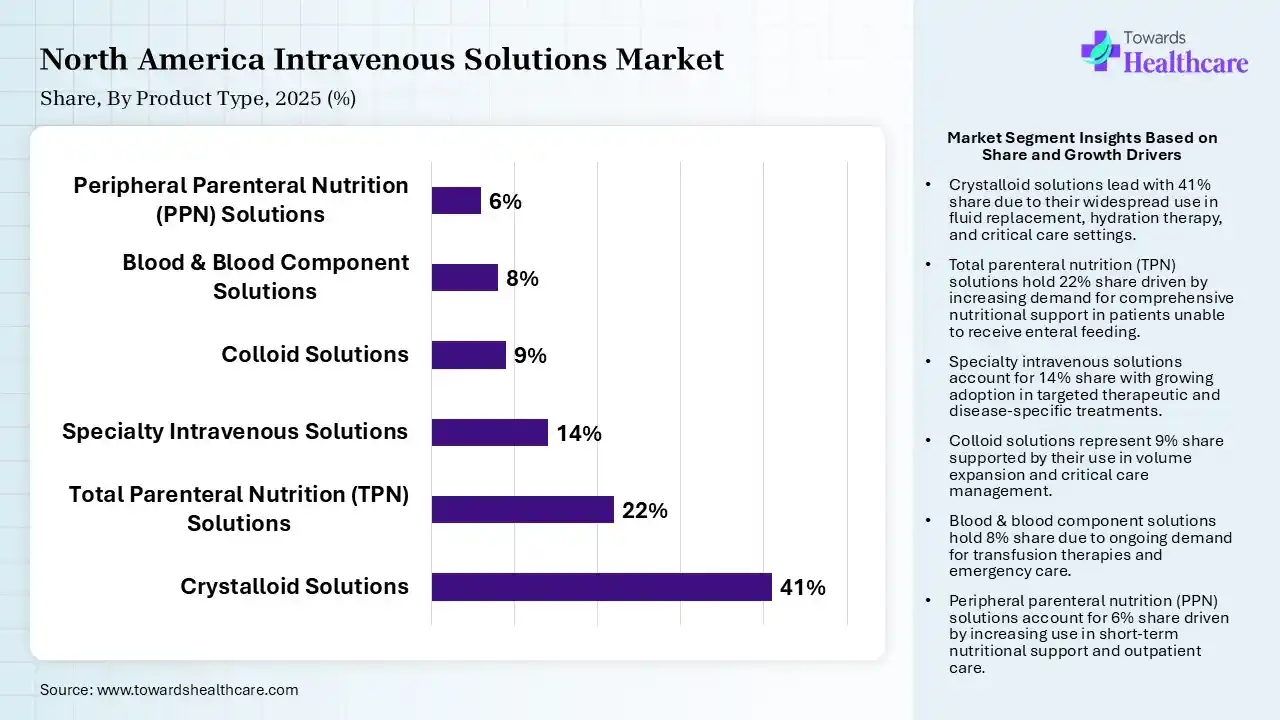

| Segment | Share 2025 (%) |

| Crystalloid Solutions | 41% |

| Total Parenteral Nutrition (TPN) Solutions | 22% |

| Specialty Intravenous Solutions | 14% |

| Colloid Solutions | 9% |

| Blood & Blood Component Solutions | 8% |

| Peripheral Parenteral Nutrition (PPN) Solutions | 6% |

The Crystalloid Solutions Segment Dominated the Market With 41% in 2025

The crystalloid solutions segment led the North America intravenous solutions market with 41% share in 2025, due to hospitals increasingly using crystalloids for hydration and emergency care. Growth in surgical admissions continued to drive routine IV fluid consumption. Lower cost and broad clinical applicability also supported their large-scale adoption.

The total parenteral nutrition (TPN) solutions segment held the second-largest share of 22% of the market in 2025, due to the increasing prevalence of gastrointestinal disorders, which boosts demand for nutritional support. Critical care utilization also continues to expand across North America. Advanced TPN formulations also improve patient recovery and outcomes.

The specialty intravenous solutions segment held 14% of the North America intravenous solutions market share in 2025 and is expected to witness the fastest growth with a CAGR of 8.80% during the forecast period, driven by growing oncology infusion therapies, which accelerate specialty IV solution demand. Dialysis and chronic disease management also increase infusion requirements. Precision electrolyte replacement therapies also support market expansion.

The colloid solutions segment held 9% of the market share in 2025, driven by trauma care and plasma volume restoration applications, which are sustaining demand. Intensive care units continue to utilize colloids in critical conditions. Improved albumin availability also supports hospital usage.

")

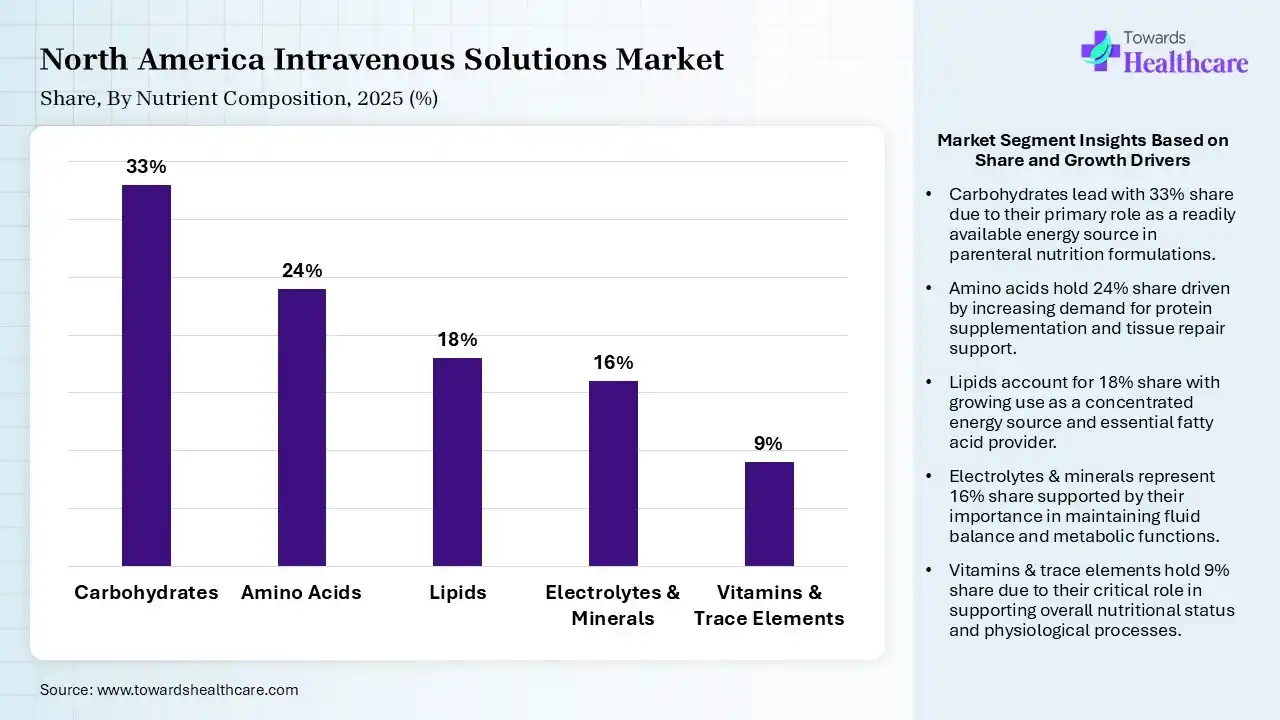

| Segment | Share 2025 (%) |

| Carbohydrates | 33% |

| Amino Acids | 24% |

| Lipids | 18% |

| Electrolytes & Minerals | 16% |

| Vitamins & Trace Elements | 9% |

The Carbohydrates Segment Dominated the Market With 33% in 2025

The carbohydrates segment accounted for the highest revenue share of 33% of the North America intravenous solutions market in 2025, as dextrose-based IV solutions remained essential for energy supplementation. Hospitals extensively utilize carbohydrate formulations in acute care. Growth in metabolic disorder management also supported their consistent demand.

The amino acids segment held the second-largest share of 24% of the market in 2025, as clinical nutrition programs increasingly incorporate amino acid infusions. The growing demand for recovery support in surgical patients also increases their use. Advanced amino acid blends are improving therapeutic effectiveness.

The lipids segment held 18% of the North America intravenous solutions market share in 2025 and is expected to show the highest growth with a CAGR of 8.40% during the forecast period, driven by the adoption of fish oil and mixed lipid emulsions in critical care. Improved nutritional efficacy also drives physician preference for lipid therapies. Long-term parenteral nutrition demand also continues to expand.

The electrolytes & minerals segment held 16% of the market share in 2025, as electrolyte imbalance treatments remain common in hospital settings. Emergency and renal care applications also support their continuous usage. Rising dehydration-related admissions also increase their demand.

")

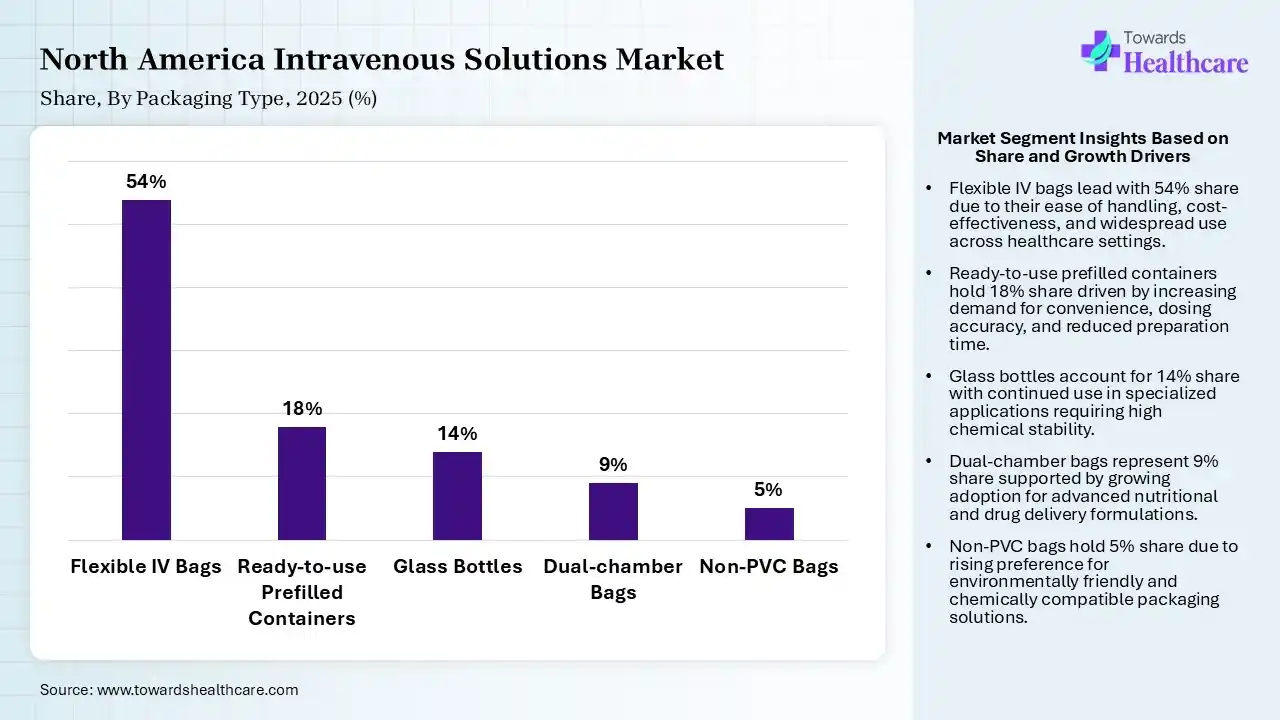

| Segment | Share 2025 (%) |

| Flexible IV Bags | 54% |

| Ready-to-use Prefilled Containers | 18% |

| Glass Bottles | 14% |

| Dual-chamber Bags | 9% |

| Non-PVC Bags | 5% |

The Flexible IV Bags Segment Dominated the Market With 54% in 2025

The flexible IV bags segment held a major revenue share of 54% of the North America intravenous solutions market in 2025, due to their reduced contamination risks and improved storage efficiency. Hospitals also preferred them as a lightweight packaging solution. Large-scale emergency preparedness programs also supported their procurement.

The ready-to-use prefilled containers segment held the second-largest share of 18% of the market in 2025 and is expected to expand rapidly with a CAGR of 8.3% during the forecast period, as they minimize medication preparation errors. Healthcare facilities prioritize workflow optimization and safety, promoting their use. Demand rises for rapid-response infusion products, increasing their adoption.

The glass bottles segment held 14% of the North America intravenous solutions market share in 2025, due to specialized pharmaceutical applications, which continue supporting their usage. High chemical stability also maintains relevance in sensitive formulations. Established manufacturing infrastructure also supports their supply continuity.

The dual-chamber bags segment held 9% of the market share in 2025, driven by their improved product shelf life and convenience. Hospitals are also increasingly adopting multi-compartment nutritional solutions. Advanced compounding capabilities also enhance their adoption.

")

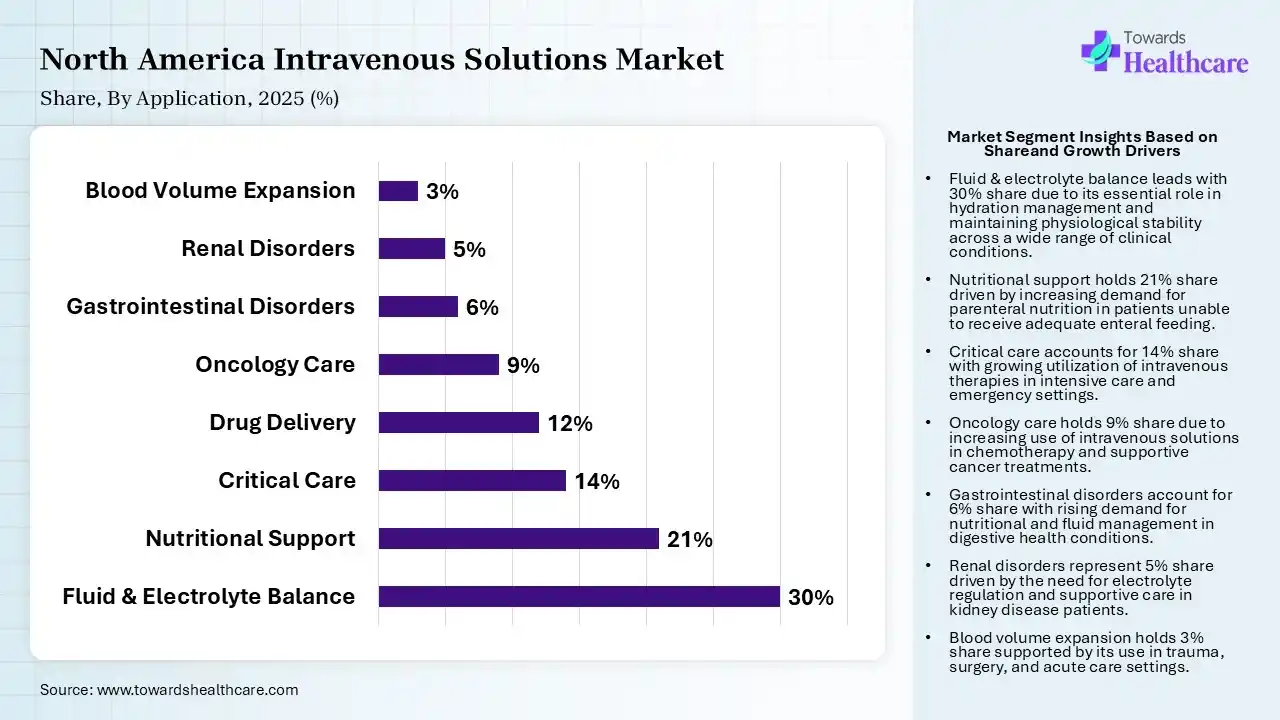

| Segment | Share 2025 (%) |

| Fluid & Electrolyte Balance | 30% |

| Nutritional Support | 21% |

| Critical Care | 14% |

| Drug Delivery | 12% |

| Oncology Care | 9% |

| Gastrointestinal Disorders | 6% |

| Renal Disorders | 5% |

| Blood Volume Expansion | 3% |

The Fluid & Electrolyte Balance Segment Dominated the Market With 30% in 2025

The fluid & electrolyte balance segment contributed the biggest revenue share of 30% of the North America intravenous solutions market in 2025, as hydration therapy remains the primary use of intravenous solutions. Growth in emergency admissions also increased electrolyte management procedures. Hospitals continued prioritizing fluid stabilization treatments.

The nutritional support segment held the second-largest share of 21% of the market in 2025, due to increasing malnutrition and gastrointestinal disorders. Critical care units increasingly depend on parenteral nutrition. Home infusion programs also expand long-term support utilization.

The critical care segment held 14% of the North America intravenous solutions market share in 2025 and is expected to gain the highest share with a CAGR of 8.60% during the forecast period, due to ICU expansion, which drives advanced infusion therapy demand. Severe infection and trauma management also require continuous IV support. Technological advancements also improve intensive care treatment delivery.

The drug delivery segment held 12% of the market share in 2025, as intravenous drug administration remains essential in hospitals. Specialty biologics and antibiotics increase infusion frequency. Precision medicine approaches also expand IV-based therapeutics.

")

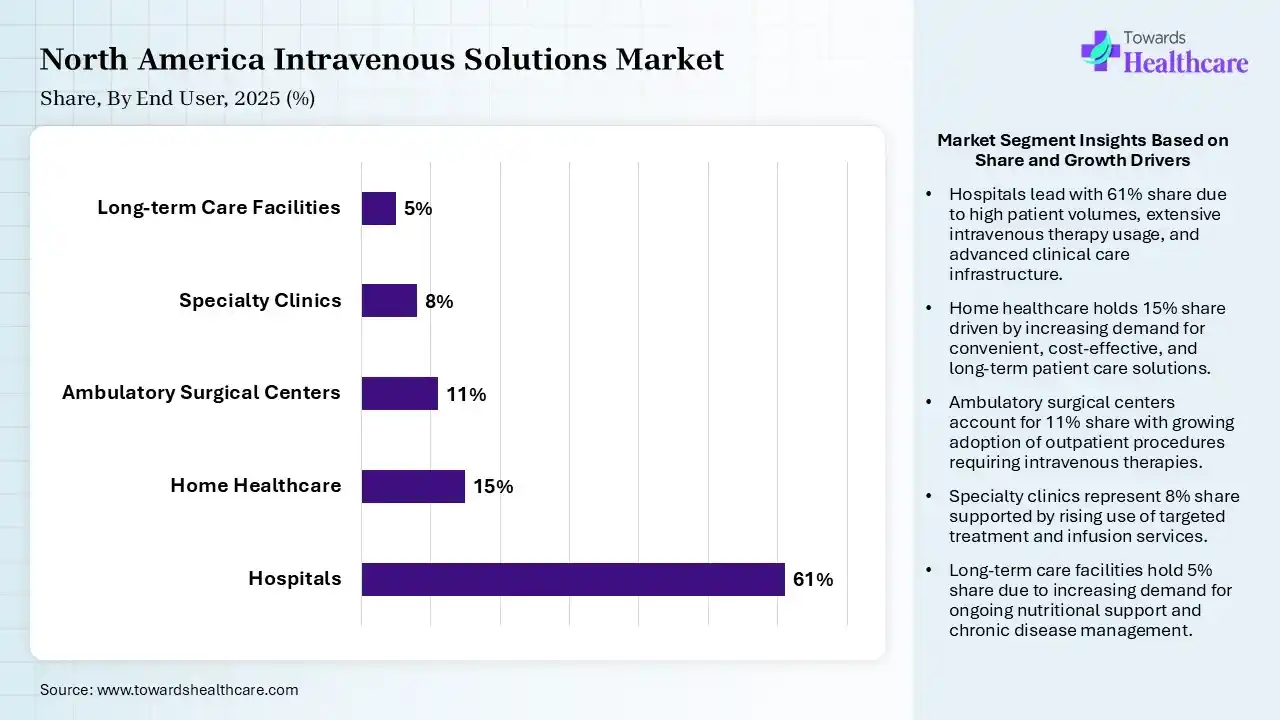

| Segment | Share 2025 (%) |

| Hospitals | 61% |

| Home Healthcare | 15% |

| Ambulatory Surgical Centers | 11% |

| Specialty Clinics | 8% |

| Long-term Care Facilities | 5% |

The Hospitals Segment Dominated the Market With 61% in 2025

The hospitals segment held the largest revenue share of 61% of the North America intravenous solutions market in 2025, driven by high inpatient admissions, which sustain bulk IV solution procurement volumes. They were the largest consumers of intravenous therapies. Expansion of emergency and surgical services also supported their demand.

The home healthcare segment held the second-largest share of 15% of the market in 2025 and is expected to grow with the fastest CAGR of 8.70% during the forecast period, due to increasing home infusion therapy adoption. Patients increasingly prefer decentralized treatment settings. Reimbursement support also improves accessibility of home care services.

The ambulatory surgical centers segment held 11% of the North America intravenous solutions market share in 2025, as outpatient surgeries require perioperative intravenous fluid support. ASC expansion increases demand for compact infusion systems. Faster patient turnover also supports IV solution consumption.

The specialty clinics segment held 8% of the market share in 2025, as oncology and dialysis clinics increasingly utilize infusion therapies. Chronic disease management also boosts specialty clinic admissions. Advanced therapies also expand intravenous treatment usage.

The North America intravenous solutions market held a significant share in 2025, due to the presence of advanced healthcare infrastructure. Growth in health expenditure and the adoption of advanced infusion technologies also increased the innovations and adoption of IV solutions. Increased chronic disease burden and home healthcare also contributed to their growth.

U.S. Market Trends

The U.S. intravenous solutions market size was estimated at USD 5.82 billion in 2025 and is predicted to increase from USD 6.19 billion in 2026 to approximately USD 10.82 billion by 2035, expanding at a CAGR of 6.4% from 2026 to 2035.

")

The U.S. consists of well-established hospitals and healthcare infrastructure, which increases the adoption of intravenous solutions. Increasing investments and chronic disease burden are also increasing their use of IV therapies. The industries are also developing smart infusion technologies, leading to new collaborations.

Canada Market Trends

The growing geriatric population and health awareness are increasing the use of intravenous solutions in Canada for critical care and parenteral nutrition. Expanding home health care and outpatient care services are also increasing their use. Growing government support is also driving the development of new IV solutions.

R&D

Clinical Trials and Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | North America Intravenous Solutions |

| Baxter International Inc. | Deerfield, U.S | Viaflex, Mini-bag plus, Viaflo, and Olimel |

| Pfizer Inc. | New York City, U.S. | Hospira |

| B. Braun Medical Inc. | Melsungen, Germany | EXCEL, Duplex, and isotone Kochsalz-Losung |

| Terumo Corporation | Tokyo, Japan | Solasia |

| Fresenius Kabi AG | Bad Homburg, Germany | Freeflex, Kabiven, and Perikabiven |

| JW Life Science | Seoul, South Korea | Winuf |

| ICU Medical, Inc. | San Clemente, U.S. | LifeCare, VisIV, Liposyn, and Fleboflex |

| Vifor Pharma | St. Gallen, Switzerland | Injectafer & Venofer |

| Grifols, S.A. | Barcelona, Spain | Gri-Fill and Fleboflex |

| Otsuka Pharmaceutical | Tokyo, Japan | Otsuka America Lines |

Strengths

Weaknesses

Opportunities

Threats

By Product Type

By Nutrient Composition

By Packaging Type

By Application

By End User

By Osmolarity

By Route of Administration

By Patient Group

By Distribution Channel

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar