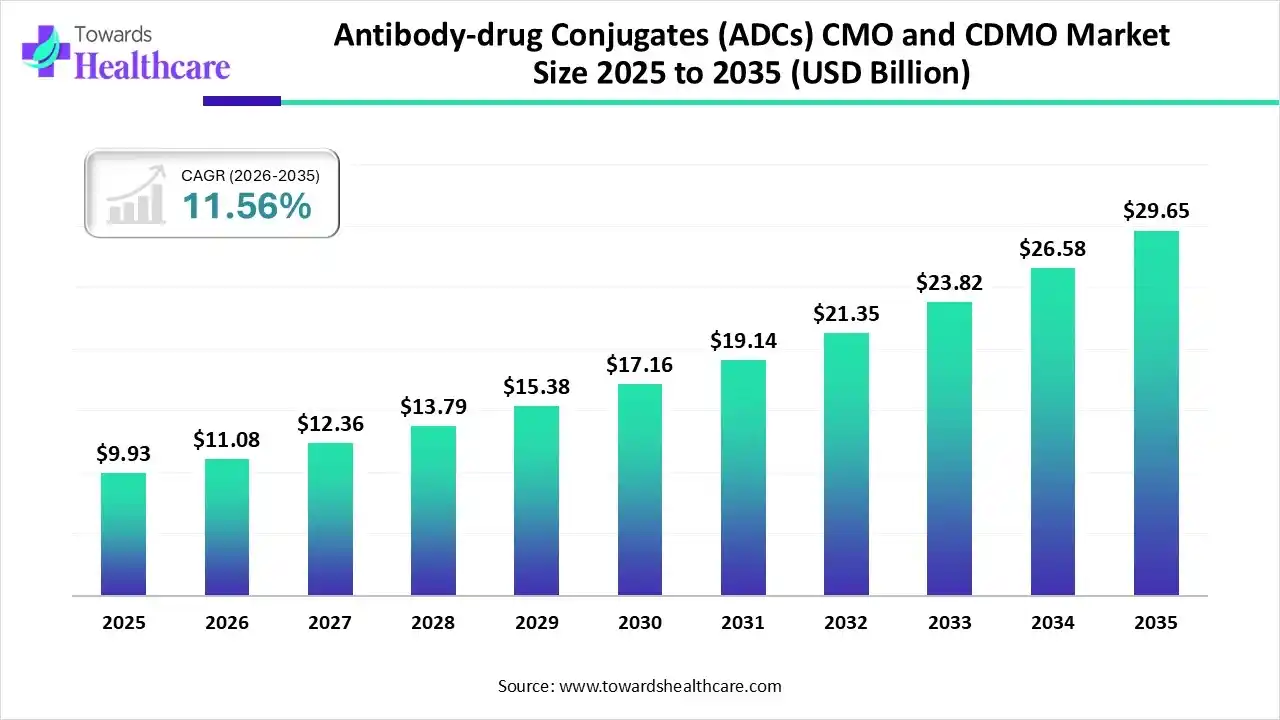

The global antibody-drug conjugates (ADCs) CMO and CDMO market size was estimated at USD 9.93 billion in 2025 and is predicted to increase from USD 11.08 billion in 2026 to approximately USD 29.65 billion by 2035, expanding at a CAGR of 11.56% from 2026 to 2035.

CMO and CDMO Market Size 2025 - 2035 (USD Billion)")

The market is expanding steadily, fueled by rising oncology pipelines growing outsourcing of complex biologics, the need for specialized conjugation capabilities, and increasing investments in scalable, compliant manufacturing infrastructure worldwide.

Antibody-drug conjugates (ADCs) CMO and CDMO are specialized contract partners that provide outsourced manufacturing, development, and scale-up services for ADCs, supporting pharmaceutical companies across process development, clinical production, and commercial supply. The antibody-drug conjugates (ADCs) CMO and CDMO market is growing due to rising oncology drug pipelines, increasing preference for outsourcing complex biology, and the need for specialized conjugation and cytotoxic handling expertise. High development costs, strict regulatory requirements, and demand for faster clinical-to-commercial transition are pushing pharma companies to rely on experienced contract partners.

AI is revolutionizing the antibody-drug conjugates (ADCs) CMO and CDMO market by optimizing antibody selection, linker design, and payload conjugation through predictive modeling. It accelerates process development, improves yield and quality control, enables real-time monitoring, and reduces manufacturing risks. AI-driven analytics also support faster scale-up, regulatory compliance, and cost-efficient production across clinical and commercial ADC manufacturing.

| Table | Scope |

| Market Size in 2026 | USD 11.08 Billion |

| Projected Market Size in 2035 | USD 29.65 Billion |

| CAGR (2026 - 2035) | 11.56% |

| Leading Region | North America |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type (The Workflow), By Process Component (The Molecule), By Linker Technology, By Phase of Development, By Target Indication (Disease Area), By Region |

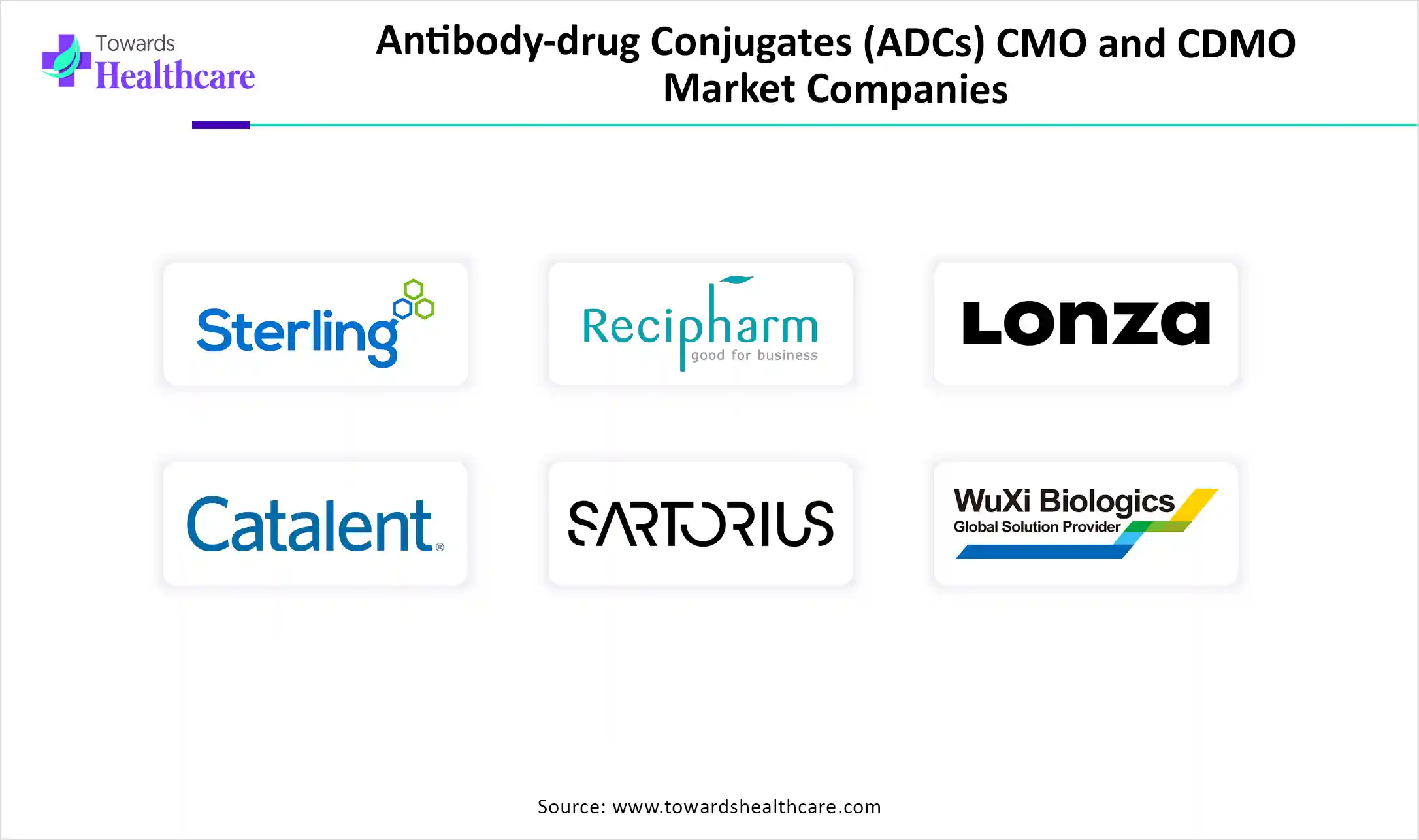

| Top Key Players | Recipharm, Lonza, Catalent, Sartorius, WuXi Biologics, Piramal Pharma Solutions |

Why Service Type Dominated the Market in 2025?

The cGMP Conjugation & Drug-linker Production segment dominated the antibody-drug conjugates (ADCs) CMO and CDMO market with a revenue share of approximately 39.7% in 2025 due to the high complexity and regulatory criticality of ADC manufacturing. Drug-linker synthesis and conjugation require specialized containment, strict cGMP compliance, and advanced expertise, making outsourcing essential. Growing clinical and commercial ADC approvals increased demand for reliable, scalable, and compliant conjugation services, driving higher revenue concentration in this segment.

Fill-finish Services

The fill-finish services segment is expected to grow at the fastest CAGR due to increasing ADC clinical trials and rising commercial launches requiring sterile, high-precision drug product handling. Complex ADC formulations demand specialized aseptic processing, containment, and compliance with stringent regulatory standards. Growing preferences for end-to-end outsourcing and the need to accelerate time-to-market are further driving strong demand for advance fill-sinish capabilities.

What Made the Antibody Manufacturing Segment Dominant in the Market in 2025?

The antibody manufacturing segment dominated the antibody-drug conjugates (ADCs) CMO and CDMO market with a revenue share of approximately 40% in 2025 due to the foundational role of monoclonal antibodies in ADC development. High demand for large-scale high-quality antibody production, increasing oncology pipelines, and stringent regulatory requirements drove reliance on experienced CDMOs and CDMOs. Additionally, complex cell culture processes, capacity constraints among pharma companies, and the need for scalable, cGMP-compliant manufacturing supported strong revenue dominance in this segment.

HPAPI/Cytotoxic Payloads

The HPAPI/cytotoxic payloads segment is expected to grow at the fastest CAGR due to increasing development of highly potent ADCs for oncology indications. These payloads require specialized containment, safety protocols, and advanced synthesis capabilities, prompting greater outsourcing to expert CDMOs. Rising clinical pipelines, innovation in level payloads chemistries, and limited in-house manufacturing capacity are accelerating demand for compliant, scalable HPAPI production service during the forecast period.

How did the Cleavable Linkers Segment Dominate the Market in 2025?

The cleavable linkers segment dominated the antibody-drug conjugates (ADCs) CMO and CDMO market with a revenue share of approximately 66.4% in 2025 due to their ability to release cytotoxic payloads selectively at tumor sites, improving efficacy and safety. Their proven clinical success, flexibility across multiple ADC designs, and compatibility with diverse payloads increased adoption. Growing regulatory confidence, higher ADC approvals, and strong demand for targeted cancer therapies further reinforced the dominance of cleavable linker technologies in the ADC manufacturing and outsourcing market.

Non-cleavable/Site-specific Linkers

The non-cleavable/site-specific linkers segment is expected to grow at the fastest CAGE due to their enhanced stability, controlled drug-to-antibody ratios, and improved safety profiles. These linkers reduce premature payloads relase and enable more consistent ADC performance. Increasing focus on next-generation ADCs, technological advancements in conjugation methods, and growing clinical evidence supporting precision linker design are accelerating adoption during the forecast period.

How the Pre-clinical & Phase I/II Segment Dominated the Market in 2025?

The pre-clinical & phase I/II segment dominated the antibody-drug conjugates (ADCs) CMO and CDMO market in 2025 due to the large volume of early-stage ADC candidates in oncology pipelines. High technical complexity, frequent process optimization, and limited in-house capabilities drove outsourcing for development, toxicity, and clinical batch production. Additionally, rising biotech activity and increased investment in novel ADC platforms accelerated demand for specialized early-phase manufacturing and development services.

Commercial Manufacturing

The commercial manufacturing segment is expected to grow at the fastest CAGR due to increasing ADC regulatory approvals and rising demand for large-scale, consistent production. Transition of successful candidates from clinical to commercial stages requires validated processes, robust supply chains, and strict cGMP compliance. Growing preference for long-term outsourcing partnerships, capacity expansion by CDMOs, and the need to ensure uninterrupted global supply are further accelerating growth in this segment.

Why Did the Solid Tumors Segment Dominate the Market in 2025?

The solid tumors segment dominated the antibody-drug conjugates (ADCs) CMO and CDMO market with revenue shares of approximately 57.9% in 2025 due to high global disease burden and strong clinical success of ADCs in these indications. Most approved and late-stage solid tumors are driving higher manufacturing demand. Advancements in tumor-specific antigens, increasing clinical trials, and favorable regulatory outcomes further reinforced the dominance of solid tumor-focused ADC development and outsourcing activities.

Non-oncology

The non-oncology segment is expected to grow at the fastest CAGR as ADC technologies expand beyond cancer. Improved linkers and payloads are designed enable targeted delivery with reduced systemic toxicity, making ADCs suitable for chronic and infectious conditions. rising unmet medical needs, growing R&D investments, and increasing clinical exploration of antibody-based targeted therapies are accelerating adoption in the non-oncology indication during the forecast period.

North America dominated the market with a revenue share of approximately 44.7% due to its strong biopharmaceutical ecosystem, high concentration of oncology-focused companies, advanced manufacturing infrastructure, and early adoption of complex biologics. The region benefits from robust funding, experienced contract manufacturing, favored regulatory support, and growing pipelines of ADC clinical trials, driving sustained outsourcing demand.

Why did the U.S. capture the Largest Revenue Share in 2025?

The U.S. led the market in 2025 due to its strong concentration of ADC innovators, advanced CMO/CDMO capabilities, and early adoption of high-value biologics. Robust oncology pipelines, significant R&D funding, mature regulatory frameworks, and large-scale commercial manufacturing capacity enabled faster development, approvals, and sustained outsourcing, driving the highest revenue share globally.

The Asia Pacific region is expected to register the fastest CAGR due to the expanding biopharmaceutical manufacturing capacity, rising oncology research, and increasing outsourcing to cost-efficient CDMO’s. Growing investments, improving regulatory frameworks, skilled workforce availability, and rapid adoption of advanced biologics manufacturing technologies are encouraging global pharma companies to shift ADC development and production activities to this region.

Why is India Emerging as a High-growth Market During the Forecast Period?

India is expected to grow at a rapid CAGR due to expanding biopharmaceutical manufacturing, rising oncology research, and increasing demand for cost-effective CDMO services. Strong government support, improving regulatory standards, skilled scientific talent, and growing investments in advanced biologics and ADC capabilities are attracting global pharmaceutical companies to outsourced development and manufacturing activities in India.

Europe is anticipated to grow at a notable rate due to strong biopharmaceutical research, increasing ADC clinical trials, and well-established CDMO networks. The region benefits from advanced manufacturing infrastructure, stringent quality standards, a supportive regulatory environment, and rising collaborations between biotech firms and contract manufacturers, driving steady demand for outsourced ADC development and commercial production.

Why is the UK for Rapid Antibody-Drug Conjugates (ADCs) CMO and CDMO Market Growth?

The UK is anticipated to grow at a rapid CAGR due to its strong life science ecosystems, rising ADC-focused research, and expanding CDMO capabilities. Increased government funding, advanced biologics manufacturing infrastructure, skilled scientific talent, and growing partnerships between academia, biotech firms, and contract manufacturing are accelerating innovation and outsourcing, supporting robust market growth during the forecast period.

CMO and CDMO Market Top Companies")

| Companies | Headquarters | Offerings |

| Sterling Pharma Solutions | United Kingdom | Provides ADC process development, bioconjugation, HPAPI and linker handling, analytical services, and GMP manufacturing for early- to mid-stage clinical programs |

| Recipharm | Sweden | Supports complex biologics manufacturing, sterile fill–finish, analytical development, and clinical supply, enabling ADC production through advanced formulation and aseptic capabilities. |

| Lonza | Switzerland | Offers end-to-end ADC solutions, including monoclonal antibody production, linker and payload synthesis, conjugation, analytical testing, and commercial-scale manufacturing. |

| Catalent | United States | Delivers biologics development, clinical and commercial manufacturing, sterile fill–finish, and advanced drug delivery support for ADCs. |

| Sartorius | Germany | Supplies critical bioprocessing technologies, single-use systems, and purification solutions that enable efficient and scalable ADC manufacturing for CMOs and CDMOs. |

| WuXi Biologics | China | Provides integrated ADC CRDMO services covering antibody development, payload and linker production, conjugation, analytical characterization, and commercial manufacturing. |

| Piramal Pharma Solutions | India | Offers HPAPI manufacturing, ADC development, formulation, and global clinical-to-commercial manufacturing through its multi-site CDMO network. |

By Service Type (The Workflow)

By Process Component (The Molecule)

By Linker Technology

By Phase of Development

By Target Indication (Disease Area)

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar