Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

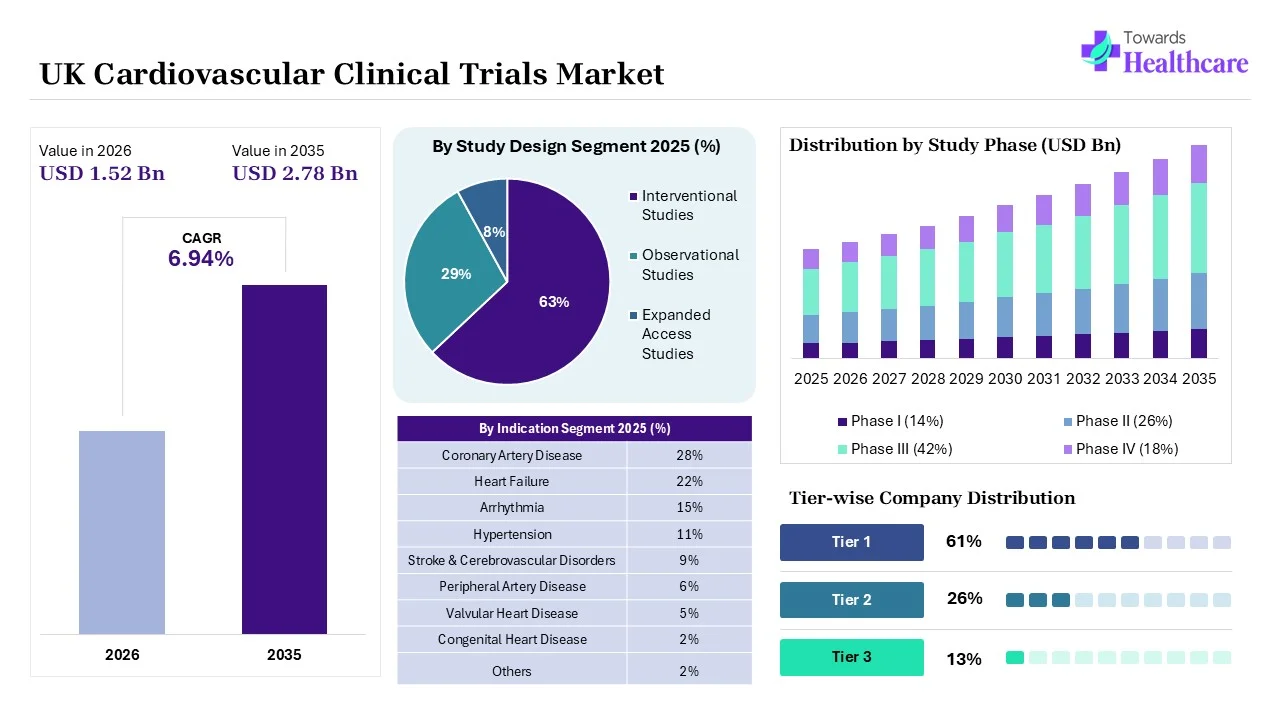

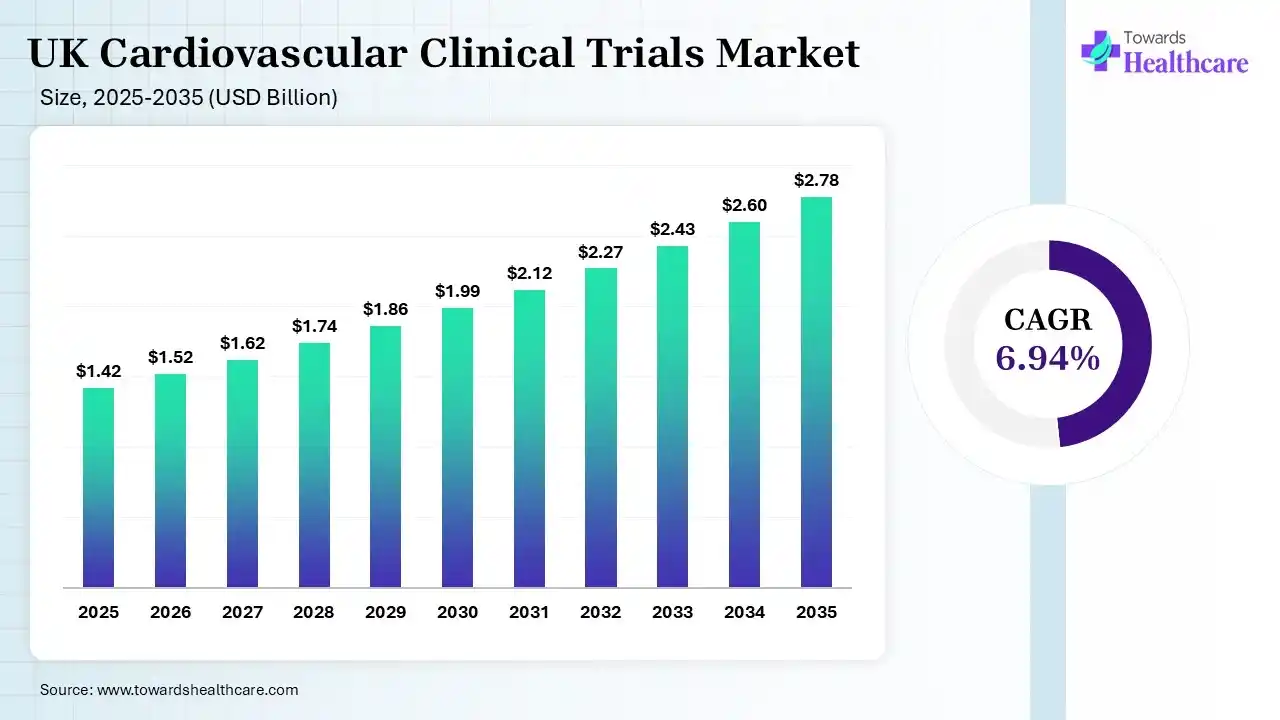

The UK cardiovascular clinical trials market size was estimated at USD 1.42 billion in 2025 and is predicted to increase from USD 1.52 billion in 2026 to approximately USD 2.78 billion by 2035, expanding at a CAGR of 6.94% from 2026 to 2035.

")

The UK cardiovascular clinical trials market encompasses the planning, execution, management, and evaluation of clinical studies investigating drugs, biologics, medical devices, diagnostics, and digital therapies intended to prevent, diagnose, or treat cardiovascular diseases.

The market includes Phase I through Phase IV trials conducted by pharmaceutical companies, biotechnology firms, contract research organizations, academic institutions, and healthcare providers. Strong research infrastructure, extensive patient registries, and access to diverse populations support trial activity across conditions such as coronary artery disease, heart failure, arrhythmias, hypertension, and stroke. Growing cardiovascular disease burden, aging demographics, and increasing prevalence of obesity, diabetes, and sedentary lifestyles continue to drive demand for innovative therapies.

The United Kingdom benefits from established regulatory frameworks, advanced healthcare systems, and collaborative research networks that facilitate patient recruitment and data collection. Increasing investments in precision medicine and biomarker-based studies are further strengthening the market landscape today while enhancing scientific competitiveness and research excellence nationwide.

The UK cardiovascular clinical trials market expansion is being shaped by several trends, including decentralized clinical trials, greater adoption of electronic data capture platforms, integration of artificial intelligence in patient selection, and increased use of real-world evidence. Sponsors are emphasizing personalized cardiovascular therapies, gene-based interventions, and advanced device evaluations to address unmet clinical needs. Opportunities are emerging through partnerships between industry participants, research centers, and public healthcare organizations that accelerate innovation and improve trial efficiency.

Enhanced digital monitoring tools, wearable technologies, and remote patient engagement solutions are improving data quality while reducing participant burden. Supportive government initiatives, growing funding for translational research, and strong expertise in cardiovascular science continue to attract global trial sponsors. The market is also benefiting from increasing focus on preventive cardiology, earlier disease detection, and outcome-driven study designs. As demand for innovative cardiovascular treatments rises, the United Kingdom is expected to remain a leading destination for cardiovascular clinical research and development.

Artificial intelligence is enhancing the market by improving patient recruitment, optimizing trial design, and enabling faster analysis of large clinical datasets. AI-powered tools help identify suitable participants, predict treatment outcomes, and support real-time monitoring, reducing trial timelines and costs. These capabilities improve research efficiency, accelerate the development of innovative cardiovascular therapies, and strengthen overall clinical trial success rates.

| Table | Scope |

| Market Size in 2026 | USD 1.52 Billion |

| Projected Market Size in 2035 | USD 2.78 Billion |

| CAGR (2026 - 2035) | 6.94% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Study Phase, By Study Design, By Indication, By Intervention Type, By Sponsor Type, By End User, By Patient Demographics, By Technology Integration |

| Top Key Players | hVIVO, Simbec-Orion, MAC Clinical Research, Richmond Pharmacology, LGC Clinical Diagnostics |

")

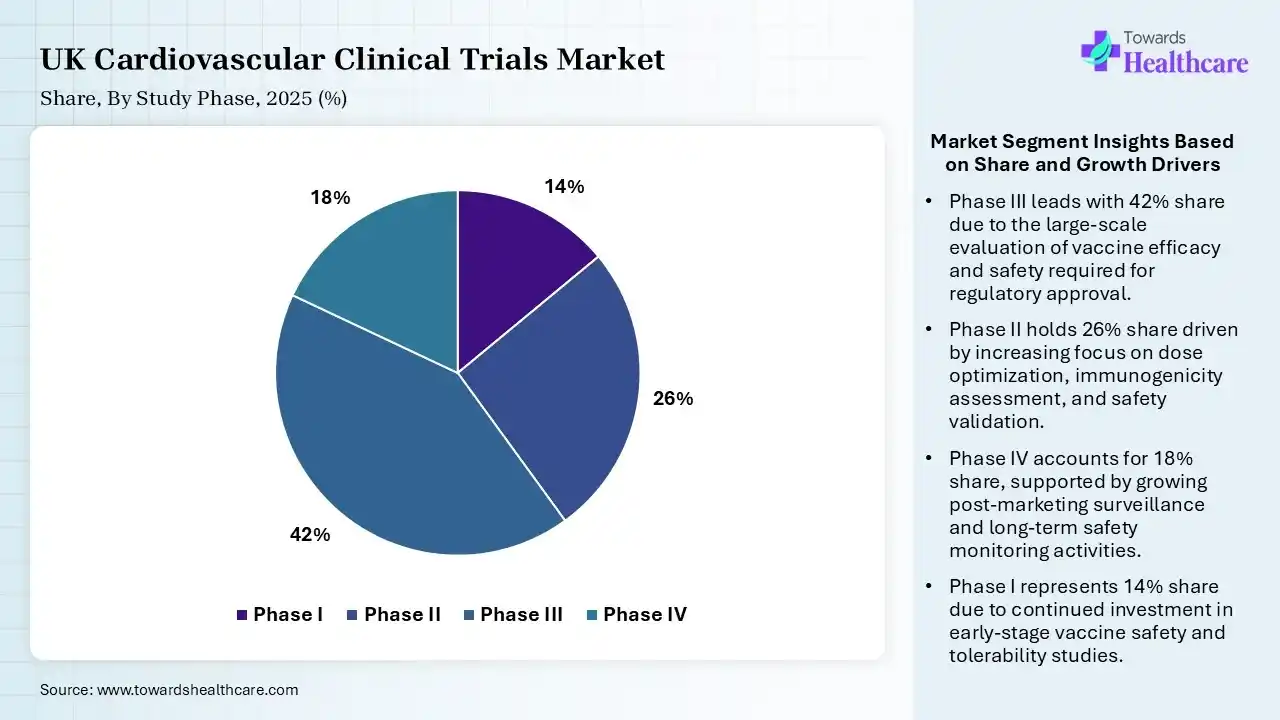

| Segment | Share 2025 (%) |

| Phase I | 14% |

| Phase II | 26% |

| Phase III | 42% |

| Phase IV | 18% |

The Phase III Segment Dominated the UK Cardiovascular Clinical Trials Market in 2025

The phase III segment held a dominant share of 42% in 2025 because these studies involve large patient populations to confirm the safety and effectiveness of new therapies before regulatory approvals. Cardiovascular treatments require extensive clinical validation due to their high-risk nature, leading to significant investments in phase III research. These growing pipelines of cardiovascular drugs and increasing demand for evidence-based treatments further strengthened the segment’s leading position.

The phase II segment held the second-largest share of 26% in 2025, as it plays a crucial role in assessing the efficacy and optimal dosage of new therapies after initial safety has been established. Increasing research activity focused on innovative cardiovascular drugs, coupled with a growing number of candidates advancing from phase I studies, continues to drive demand for phase II clinical trials.

The phase IV segment held 18% share in 2025 and is expected to grow at the fastest CAGR of 7.88% in the UK cardiovascular clinical trials market during the forecast period due to increasing emphasis on post-marketing surveillance and long-term safety monitoring of approved therapies. Regulatory authorities and healthcare providers are placing greater focus on real-world evidence to assess treatment effectiveness across broader patient populations. The growing adoption of advanced cardiovascular therapies is further driving demand for phase IV studies.

The Phase I segment held a 14% market share due to increasing investment in the development of novel cardiovascular drugs, biologics, and advanced therapies. Pharmaceutical and biotechnology companies are expanding their early-stage research pipelines to address unmet clinical needs. Additionally, the UK’s environment is encouraging more first-in-human studies, contributing to segment growth.

")

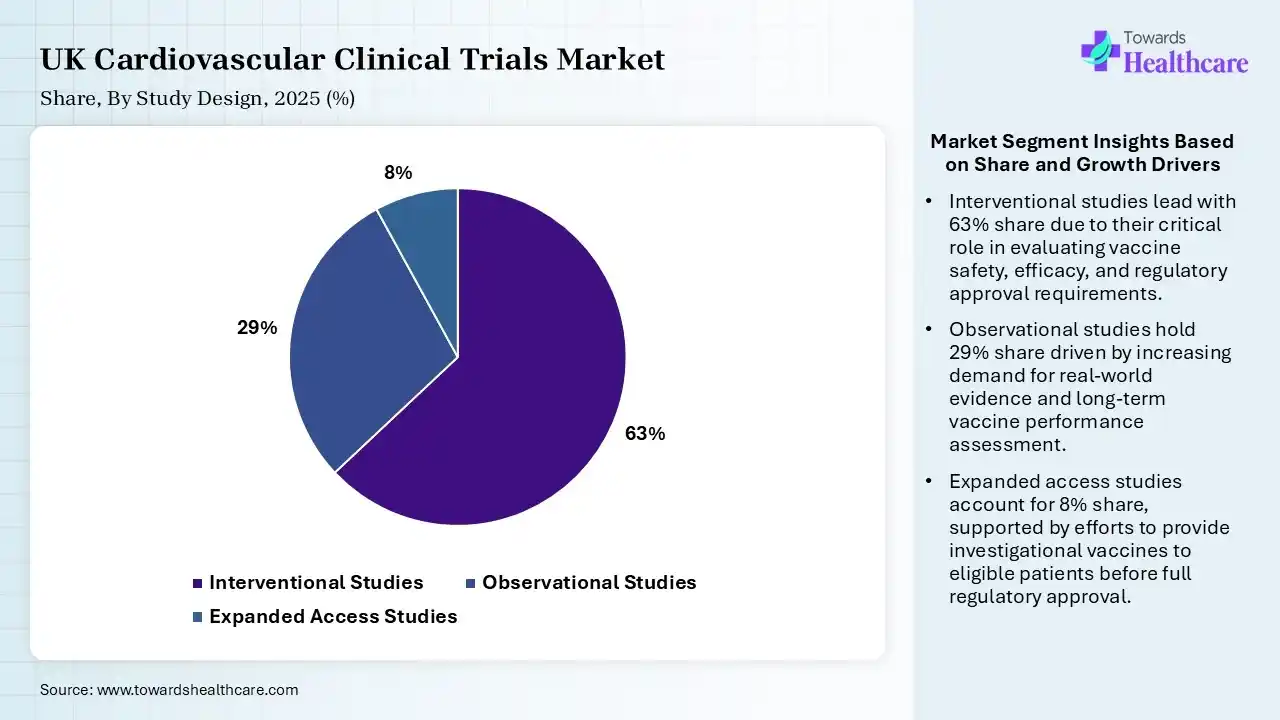

| Segment | Share 2025 (%) |

| Interventional Studies | 63% |

| Observational Studies | 29% |

| Expanded Access Studies | 8% |

The Interventional Studies Segment Led the UK Cardiovascular Clinical Trials Market in 2025 with the Largest Share

The interventional studies segment held a dominant share of 63% in 2025 because it is the primary study design used to evaluate the safety and efficacy of new drugs, medical devices, and therapeutic procedures. These trials generate the clinical evidence required for regulatory approval and commercialization. Rising investment in cardiovascular drug development and increasing demand for innovative treatment options continue to drive the dominance of interventional studies.

The observational studies segment held the second-largest share of 29% in 2025 due to its ability to assess disease patterns, treatment outcomes, and patient behavior in real-world settings. These studies are widely used to collect long-term clinical data without intervention, supporting healthcare decision-making and epidemiological research. The growing focus on patient-centric care and real-world evidence continues to drive demand for observational studies.

The expanded access studies segment held an 8% share in 2025 and is expected to grow at the fastest CAGR of 7.66% in the UK cardiovascular clinical trials market during the forecast period due to increasing demand for access to investigational therapies among patients with serious or life-threatening cardiovascular conditions. Growing awareness of compassionate use programs, a supportive regulatory framework, and the rising development of innovative cardiovascular treatments are encouraging broader adoption of expanded access pathways during the forecast period.

")

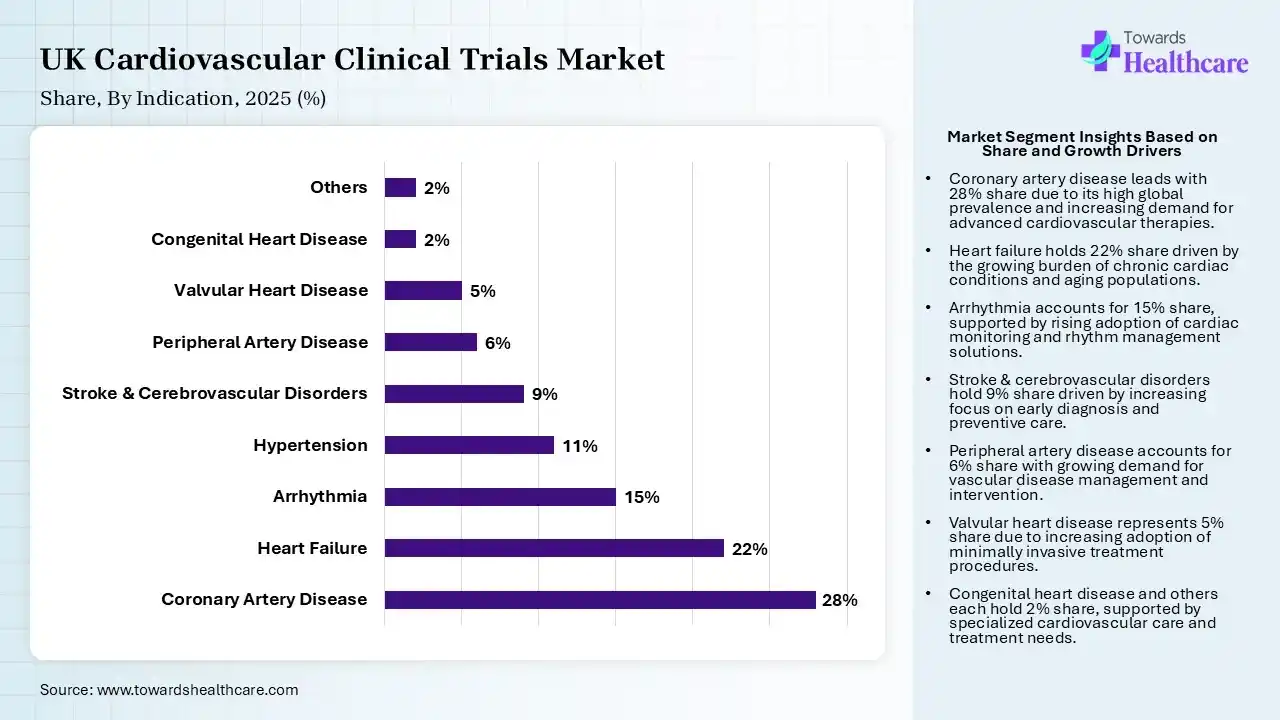

| Segment | Share 2025 (%) |

| Coronary Artery Disease | 28% |

| Heart Failure | 22% |

| Arrhythmia | 15% |

| Hypertension | 11% |

| Stroke & Cerebrovascular Disorders | 9% |

| Peripheral Artery Disease | 6% |

| Valvular Heart Disease | 5% |

| Congenital Heart Disease | 2% |

| Others | 2% |

The Coronary Artery Disease Segment Led the UK Cardiovascular Clinical Trials Market in 2025 with the Largest Share

The coronary artery disease segment led the market with a share of 28% in 2025 due to increasing demand for access to investigational therapies among patients with serious or life-threatening cardiovascular conditions. Growing awareness of compassionate use programs, supportive regulatory frameworks, and the rising development of innovative cardiovascular treatments are encouraging broader adoption of expanded access pathways during the forecast period.

The heart failure segment held the second-largest share of 22% in 2025 and is expected to grow at the fastest CAGR of 7.54% in the market during the forecast period due to the high prevalence of the condition, particularly among the aging population. The significant clinical and economic burden associated with heart failure has increased demand for effective therapies and disease management strategies. Continuous research into novel drugs, devices, and combination treatments is further driving the volume of clinical trials within this segment.

The arrhythmia segment held a 15% market share due to the increasing prevalence of cardiac rhythm disorders, particularly among elderly populations. Growing awareness of early diagnosis, advancements in catheter ablation and implantable cardiac devices, and ongoing development of innovative anti-arrhythmic therapies are driving research activity. Additionally, the need for improved long-term treatment outcomes continues to support the expansion of arrhythmia-focused clinical trials.

The hypertension segment held a 11% share of the UK cardiovascular clinical trials market due to the growing number of individuals affected by high blood pressure and its association with serious cardiovascular complications. Rising demand for more effective therapies, increasing focus on early disease management, and ongoing research into novel antihypertensive drugs are driving clinical trial activity. The need to reduce long-term healthcare burden further supports segment growth.

")

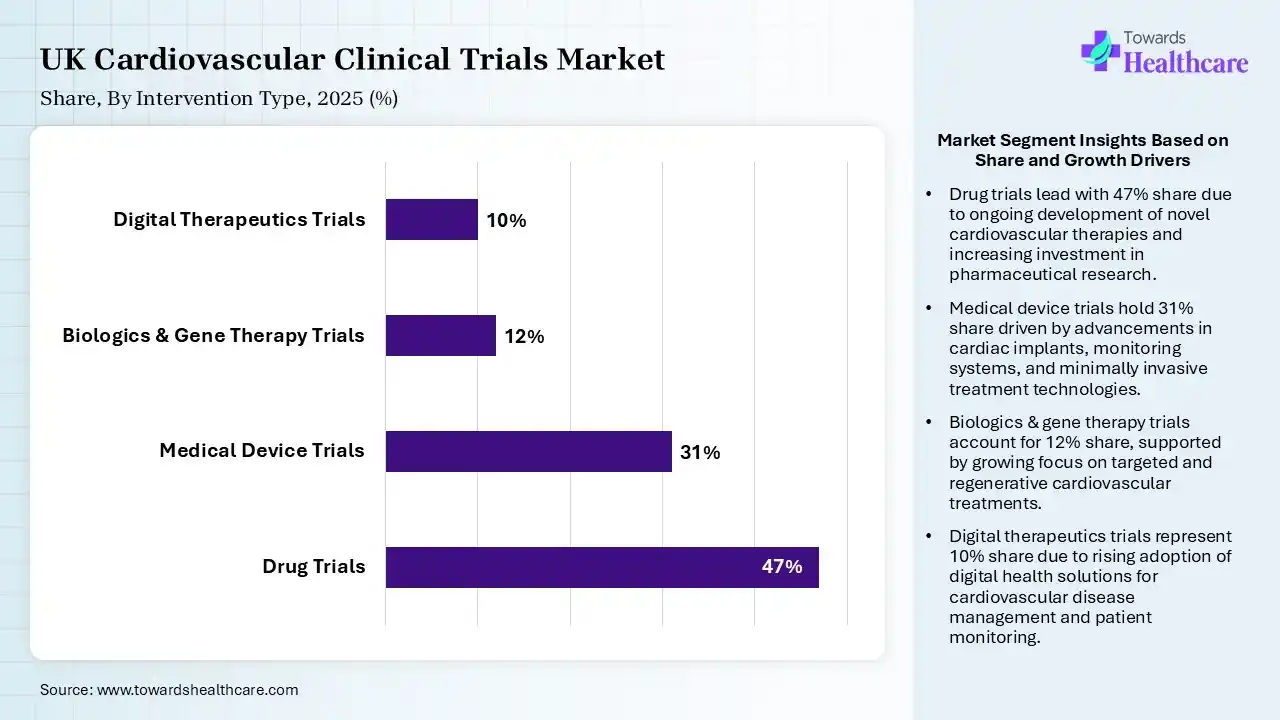

| Segment | Share 2025 (%) |

| Drug Trials | 47% |

| Medical Device Trials | 31% |

| Biologics & Gene Therapy Trials | 12% |

| Digital Therapeutics Trials | 10% |

The Drug Trials Segment Led the Market in 2025 with the Largest Share

The drug trials segment dominated the UK cardiovascular clinical trials market with a share of 47% in 2025 due to the continuous development of novel medications aimed at treating and preventing cardiovascular diseases. Pharmaceutical companies invest heavily in clinical research to evaluate the safety, efficacy, and optimal dosing of new therapies. The increasing burden of cardiovascular conditions, coupled with the need for improved treatment outcomes and regulatory approvals, continues to drive the dominance of drug trials.

The medical device trials segment held the second-largest share of 31% in 2025 due to the growing adoption of advanced cardiac devices such as pacemakers, stents, defibrillators, and heart monitoring systems. Increasing demand for minimally invasive treatment options and continuous technological advancements are driving clinical evaluation activities. Additionally, the rising prevalence of cardiovascular diseases is accelerating the development and testing of innovative medical devices.

The biologics & gene therapy trials segment held a 12% share in 2025 and is expected to grow at the fastest CAGR of 8.42% in the UK cardiovascular clinical trials market during the forecast period due to increasing research focused on targeted and regenerative treatment approaches for cardiovascular diseases. Advances in genetic medicine, rising investments in innovative biologic therapies, and growing interest in addressing the underlying cause of cardiac disorders are accelerating clinical development activities. Supportive research funding and technological progress further contribute to rapid segment growth.

The digital therapeutics trials segment held a 10% market share due to the increasing use of software-based interventions for disease management, patient monitoring, and behavioral modification. The growing adoption of mobile health applications, wearable technologies, and remote care solutions is driving clinical validation efforts. Additionally, the need for cost-effective, patient-centric cardiovascular care is encouraging greater investment in digital therapeutic development and clinical research.

")

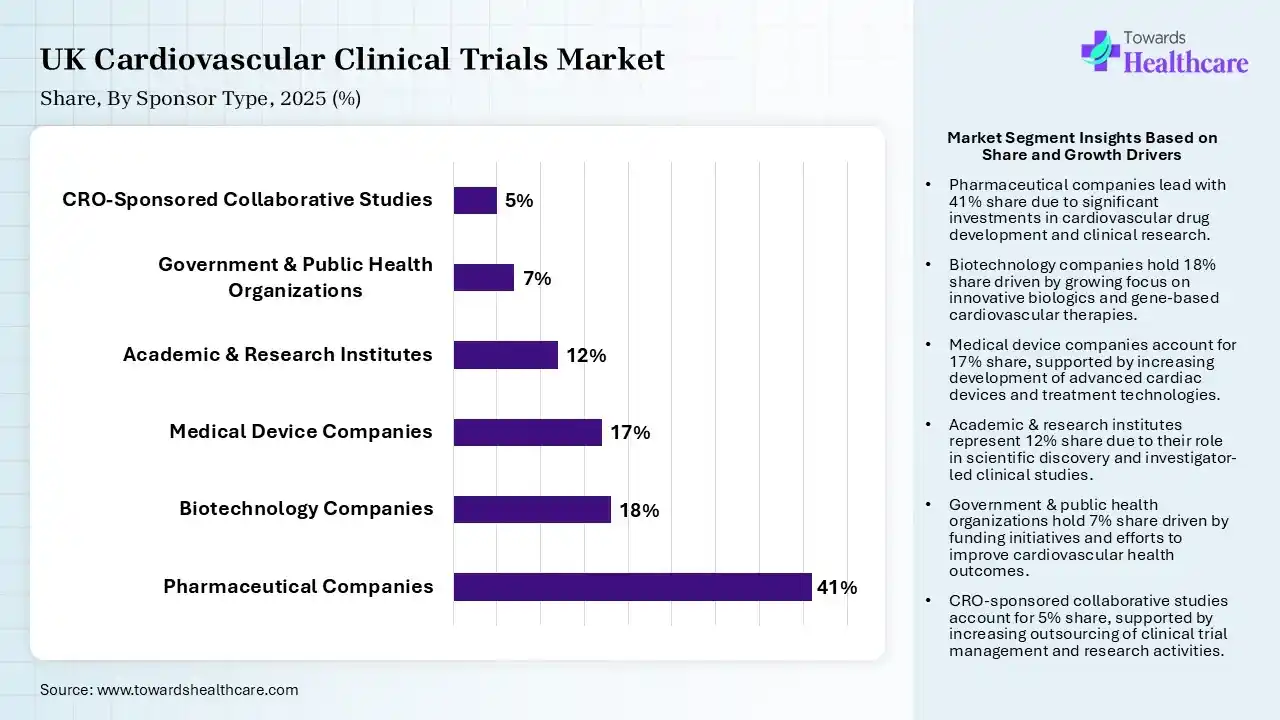

| Segment | Share 2025 (%) |

| Pharmaceutical Companies | 41% |

| Biotechnology Companies | 18% |

| Medical Device Companies | 17% |

| Academic & Research Institutes | 12% |

| Government & Public Health Organizations | 7% |

| CRO-Sponsored Collaborative Studies | 5% |

The Pharmaceutical Companies Segment Dominated the UK Cardiovascular Clinical Trials Market in 2025

The pharmaceutical companies segment dominated the market with a share of 41% in 2025 due to substantial investments in the development of innovative cardiovascular drugs and therapies. These companies sponsor a large number of clinical studies to evaluate safety, efficacy, and regulatory compliance. Their strong financial resources, extensive research pipelines, and collaborations with research institutions and healthcare providers further reinforced their leading position in the market.

The biotechnology companies segment held the second-largest share of 18% in 2025 and is expected to grow at the fastest CAGR of 8.03% in the market during the forecast period due to its strong focus on developing innovative biologics, gene therapies, and precision medicine solutions for cardiovascular diseases. Increasing investments in advanced therapeutic research and a growing pipeline of targeted treatments are driving clinical trial activity. Collaborations with academic institutions and healthcare organizations further support the segment’s significant market presence.

The medical device companies segment held a 17% share of the UK cardiovascular clinical trials market due to increasing innovation in cardiac implants, monitoring systems, and minimally invasive treatment technologies. Rising demand for advanced devices to improve patient outcomes and manage cardiovascular diseases is driving clinical evaluation activities. Additionally, continuous technological investment in device development is contributing to the segment’s expansion.

The academic & research institutes segment held a 12% market share due to growing involvement in investigator-led studies, translational research, and collaborative clinical programs. Increased funding for cardiovascular research, strong partnerships with healthcare organizations, and access to extensive patient data are supporting the trial's role in advancing scientific knowledge and evaluating innovative treatment approaches for cardiovascular diseases.

")

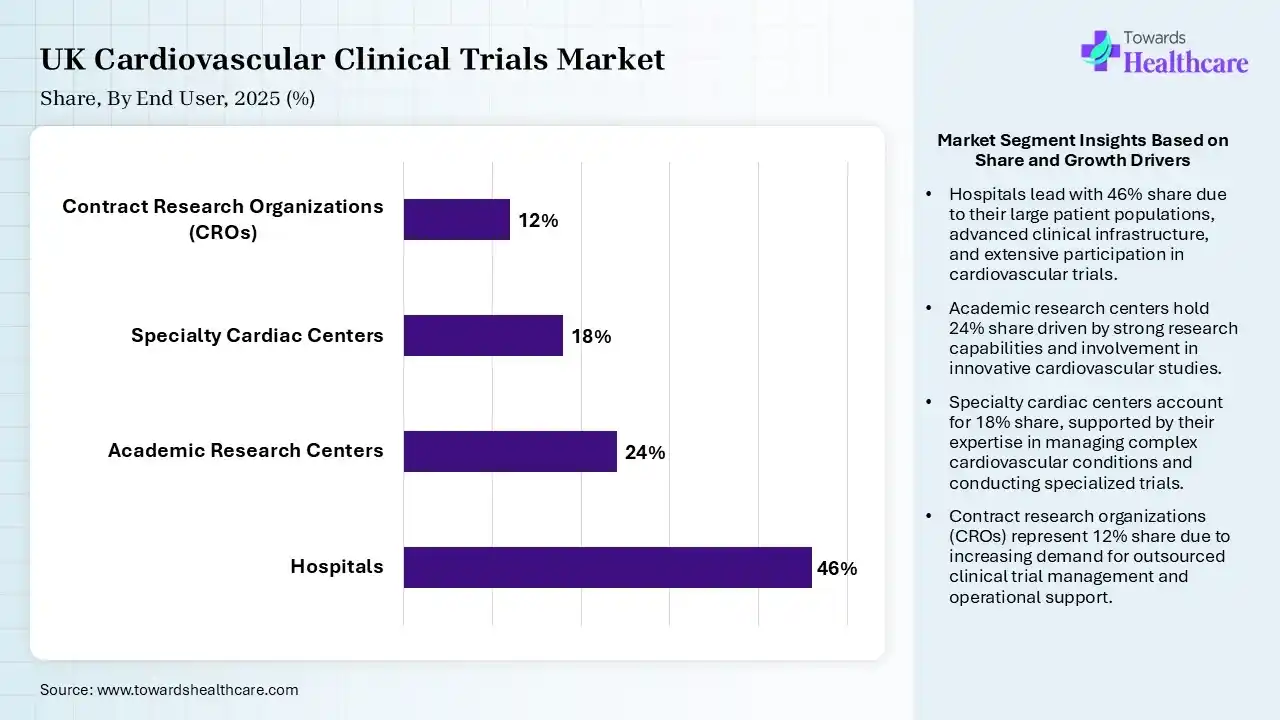

| Segment | Share 2025 (%) |

| Hospitals | 46% |

| Academic Research Centers | 24% |

| Specialty Cardiac Centers | 18% |

| Contract Research Organizations (CROs) | 12% |

The Hospitals Segment Dominated the UK Cardiovascular Clinical Trials Market in 2025

The hospitals segment held a dominant share of 46% in 2025 because hospitals serve as the primary sites for patient recruitment, treatment administration, and clinical monitoring. Their access to large cardiovascular patient populations, specialized medical expertise, and advanced diagnostic facilities enables efficient trial execution. Additionally, strong collaborations with pharmaceutical companies, research institutions, and healthcare networks further strengthened the leading position of hospitals in cardiovascular clinical research.

The academic research centers segment held the second-largest share of 24% in 2025 due to its strong involvement in investigator-led studies, early-stage research, and clinical innovation. These centers benefit from access to skilled researchers, advanced research infrastructure, and collaborations with hospitals, pharmaceutical companies, and government organizations. Increasing research funding and a growing focus on developing novel cardiovascular therapies continue to support the segment’s significant market position.

The specialty cardiac centers segment held 18% share in 2025 and is expected to grow at the fastest CAGR of 7.51% in the UK cardiovascular clinical trials market during the forecast period due to increasing demand for specialized cardiovascular treatment and research services. These centers offer dedicated expertise, advanced diagnostic capabilities, and access to targeted patient populations, making them attractive sites for clinical studies. The growing prevalence of complex heart condition and rising adoption of innovative cardiac therapies are further and rising adoption of innovative cardiac therapies are further driving clinical trials activity in specialty cardiac centers.

The contract research organizations (CROs) segment held a 12% market share as pharmaceutical, biotechnology, and medical device companies increasingly outsourced clinical research activities to improve efficiency and reduce costs. CROs provide expertise in trial management, regulatory compliance, patient recruitment, and data analysis. Growing clinical trial complexity, rising research investments, and the need for faster study execution are further driving demand for CRO services.

The UK cardiovascular clinical trials market is expanding due to rising cardiovascular disease prevalence, advanced research infrastructure, and increasing adoption of decentralized and data-driven trial models. Nearly 7 million people in England live with cardiovascular disease, creating strong demand for innovative therapies targeting heart failure, arrhythmias, coronary artery disease, and stroke. The National Health Service (NHS) provides researchers access to approximately 67 million patient records, accelerating patient recruitment, real-world evidence generation, and long-term outcomes assessment.

R&D

Regulatory Approvals

Patient Support and Services

| Companies | Headquarters | Offerings |

| hVIVO | London, UK | Early-phase clinical trials, patient recruitment, clinical pharmacology studies, and research support services. |

| Simbec-Orion | Merthyr Tydfil, UK | Phase I–IV clinical trial management, laboratory services, regulatory support, and data management. |

| MAC Clinical Research | Merseyside, UK | Clinical trial execution, patient recruitment, site management, and cardiovascular research services. |

| Richmond Pharmacology | London, UK | Early-stage clinical development, cardiovascular safety studies, and translational research services. |

| LGC Clinical Diagnostics | Teddington, UK | Biomarker testing, laboratory solutions, diagnostic support, and clinical trial services |

In April 2026, "I am honored to join Caristo at such a transformative moment, as coronary inflammation, an underlying driver of heart attacks, moves to the forefront of cardiovascular disease prevention," said Stephen M. Deitsch, CEO of Caristo Diagnostics. "At Caristo, we have pioneered the first AI technology capable of detecting coronary inflammation and stratifying cardiovascular risk. In the hands of skilled clinicians worldwide, this innovation has the potential to shift care from a reactive to a truly preventive model, ultimately improving patient outcomes. I look forward to working with our talented team to expand the global reach of our technology and create meaningful value for patients, physicians, payers, and our shareholders."

By Study Phase

By Study Design

By Indication

By Intervention Type

By Sponsor Type

By End User

By Patient Demographics

By Technology Integration

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar