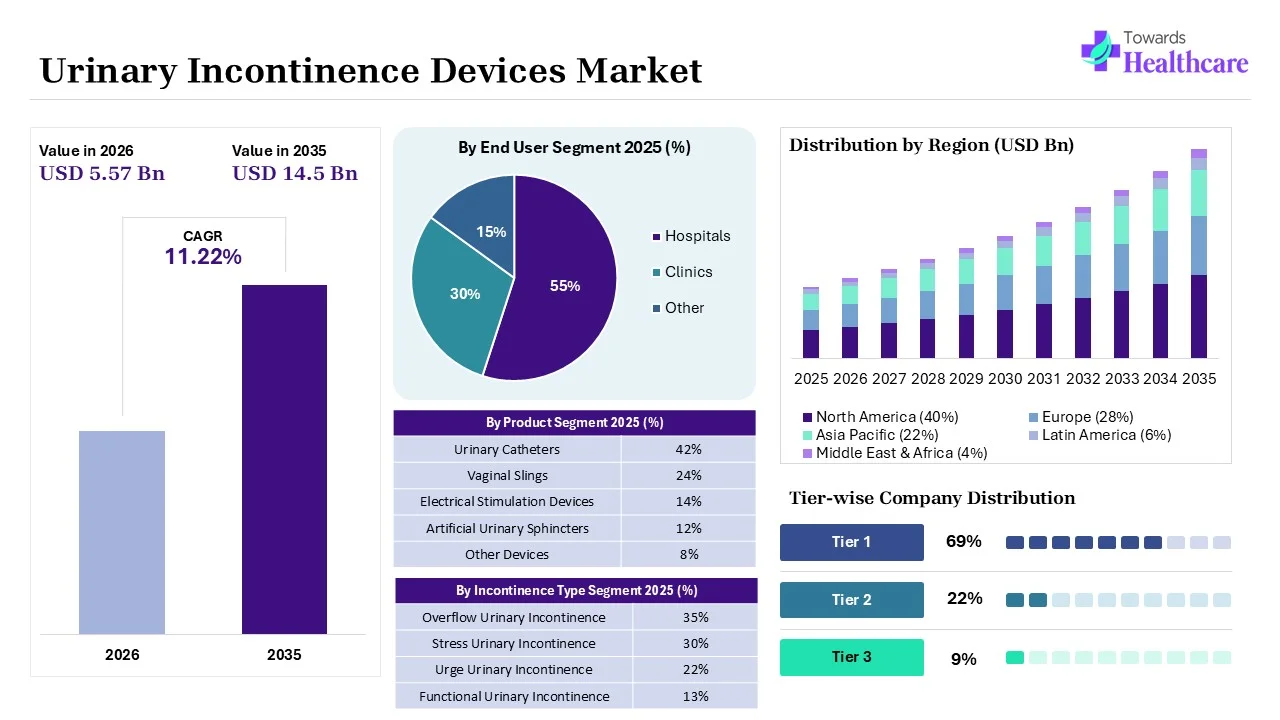

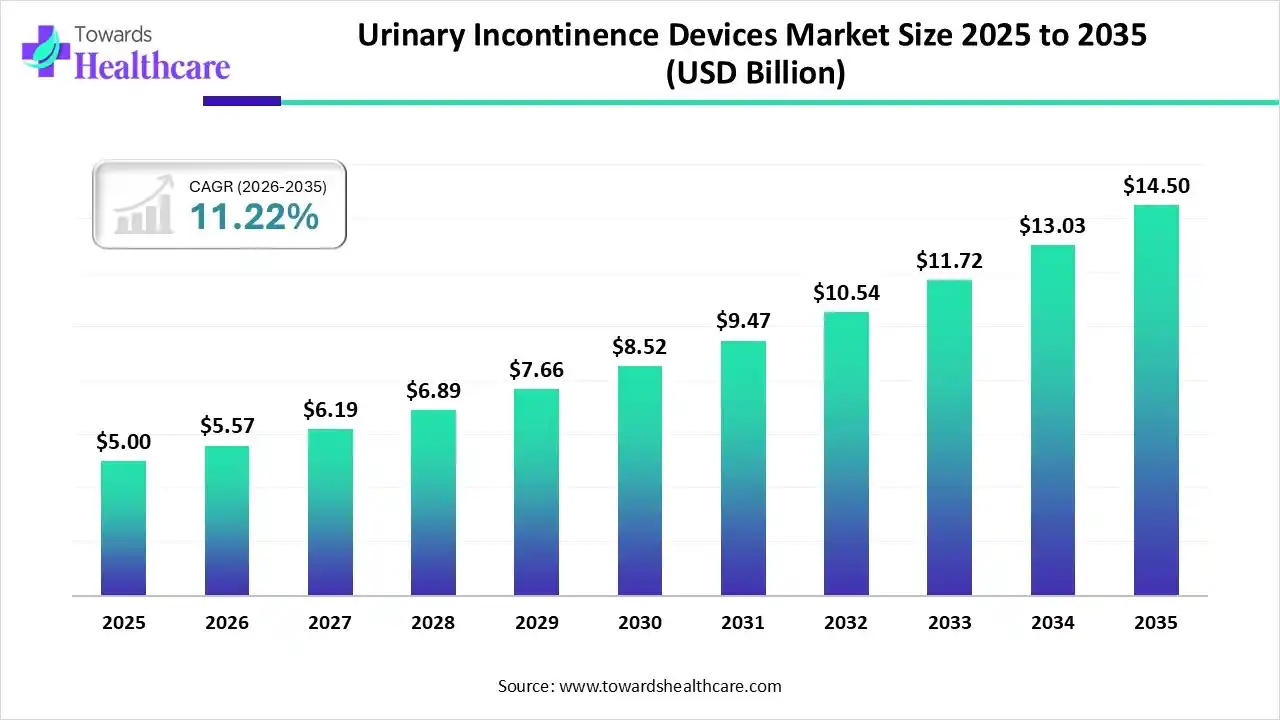

The global urinary incontinence devices market size was estimated at USD 5 billion in 2025 and is predicted to increase from USD 5.57 billion in 2026 to approximately USD 14.5 billion by 2035, expanding at a CAGR of 11.22% from 2026 to 2035.

The globe is facing a huge rise in an ageing population having diabetes and neurological disorders, which are leading to urinary dysfunction, and this further fosters the advancements in the market. However, the elders are spurring the use of AI algorithms in wearable devices and other substantial implants. The widespread adoption of smaller, rechargeable, and MRI-compatible implants assists targeted neuromodulation.

Mainly, the global urinary incontinence devices market is referred to as diverse absorbent pads, diapers, and waterproof underwear, coupled with more sophisticated external catheters, internal pessaries for women, and even implantable devices for critical instances. These varieties are propelled by a rising geriatric population, many chronic diseases, like diabetes, MS, stroke, prostate issues, with a raised demand for robust solutions. Recently, Medtronic received U.S. FDA approval for its Altaviva device, which is a minimally invasive, implantable tibial nerve stimulation (iTNM) device used to treat urge urinary incontinence (UUI) without the need for sedation or imaging for the procedure.

Primarily, for monitoring bladder filling and pressure, devices are utilizing non-invasive bioimpedance or optical sensors, and these solutions mainly use AI for further processing the sensor data, & sharing discreet notifications to the caregiver. Additionally, the wider adoption of AI models is involved in the analysis of urination sounds via a smartphone application to non-invasively detect flow rate, voided volume, and voiding time.

Urinary incontinence devices are medical devices designed to diagnose, manage, or treat involuntary urine leakage by improving bladder control, supporting the urethra, stimulating pelvic floor muscles, or collecting urine safely. These devices include urinary catheters, neuromodulation systems, artificial urinary sphincters, vaginal pessaries, urethral inserts, and external urinary collection devices used across hospitals, clinics, and home healthcare settings.

The urinary incontinence devices market is expanding due to the increasing prevalence of urinary incontinence, a growing geriatric population, rising obesity and neurological disorders, and greater awareness of available treatment options. Key trends include the adoption of wearable continence devices, smart bladder monitoring systems, and minimally invasive neuromodulation therapies. Technological advancements in AI-enabled monitoring, digital health integration, and biocompatible materials are improving patient outcomes. Future opportunities lie in personalized continence management, remote patient monitoring, and next-generation implantable devices, supported by continuous innovation and expanding home healthcare services.

Spurring Smart & Wearable Tech

Many leading companies are fostering the integration of sensors in absorbent products for alerts, like Medline's tech and wearable stimulators, such as INNOVO, Axonics' systems for pelvic floor nourishing.

Exploration of Sling Systems

The market is stepping into more sophisticated, lower-profile slings and mesh products for stress incontinence, a recent example is the Caldera Medical acquisition.

Immersive Electronic Artificial Urinary Sphincters (AUS)

In the coming era, the market will see major innovations in AI sphincters, including adaptive pressure regulation that automatically adjusts to a patient's movements and wireless control options via Bluetooth or an external remote.

Transforming Targeted Neuromodulation

Persistent breakthroughs in nerve stimulation, such as smaller, rechargeable, and MRI-compatible implants, will support targeting the sacral, tibial, and possibly pudendal nerves.

")

| Number of UTI Cases Globally each year | Approx. 400 million+ |

| Number of Health Service Visits Annually | Approx. 3 million |

| Women UTI % | 50-60% |

| Magcath | In April 2025, a company received an additional €535,000 (4 million Danish kroner) from its 36 existing Danish and Swiss business angel investors to assist in the prospective European launch of its female incontinence treatment device. |

| Uresta | In March 2025, it secured $3 million in funding to speed up the company’s U.S. launch and raise awareness of its innovative approach to bladder leakage. |

| Axena Health, Inc. | In February 2025, it collaborated with Mayo Clinic to unite the organization’s educational content on overactive bladder (OAB) into Axena Health’s clinically proven Leva Pelvic Health System. |

| Valencia Technologies | In February 2025, it secured a strategic investment of up to $35 million from Brooks Advisory Group to support the commercialization of its flagship eCoin system and establish minimally invasive treatments for urinary incontinence. |

| Key Elements | Scope |

| Market Size in 2026 | USD 5.57 Billion |

| Projected Market Size in 2035 | USD 14.5 Billion |

| CAGR (2026 - 2035) | 11.22% |

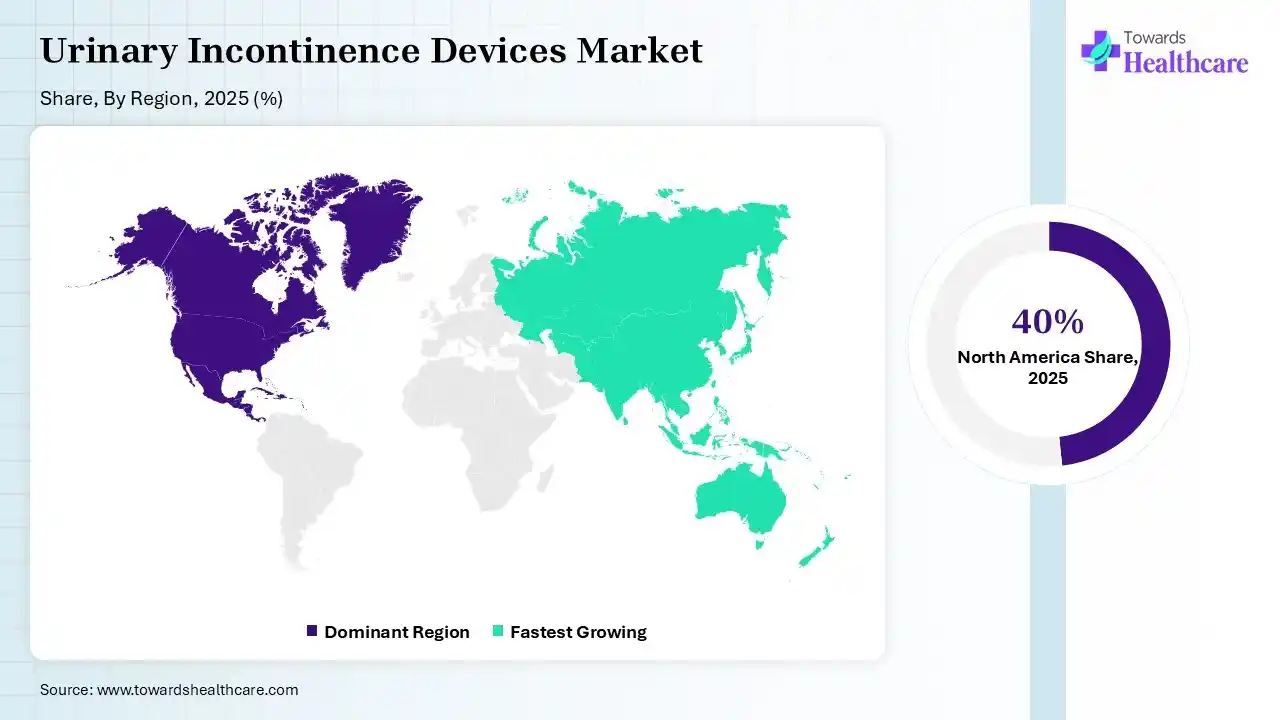

| Leading Region | North America by 40% |

| Key Applications | Stress urinary incontinence (SUI), urge incontinence, overflow incontinence, post-prostatectomy incontinence, neurogenic bladder management |

| Primary End Users | Hospitals, urology clinics, ambulatory surgical centers, long-term care facilities, home healthcare users |

| Key Growth Drivers | Aging population, rising prevalence of pelvic floor disorders, increased prostate surgeries, minimally invasive device innovation, awareness of female pelvic health |

| Market Segmentation | By Product, By Category, By Incontinence Type, By End User, By Region |

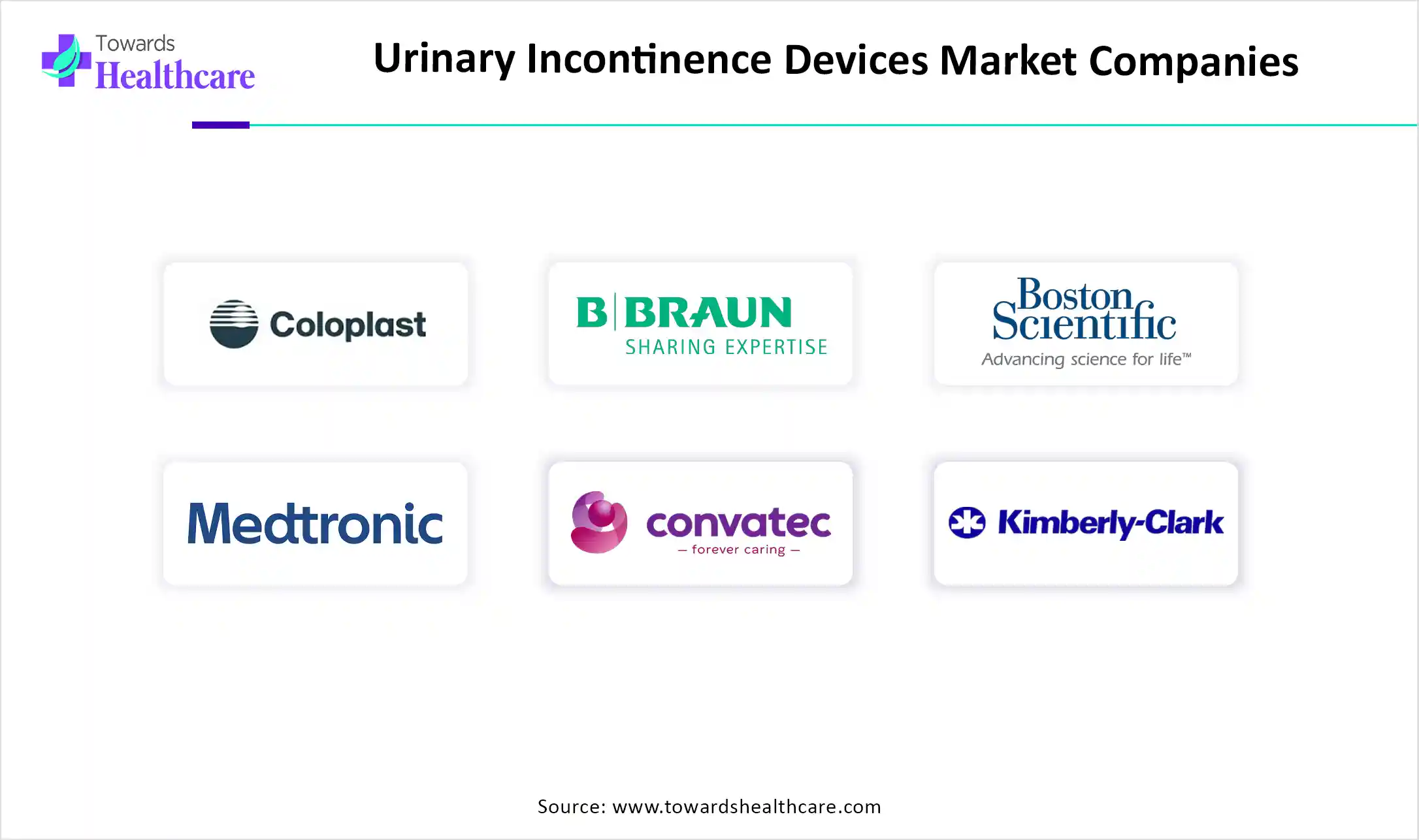

| Top Key Players | Coloplast, B. Braun, Boston Scientific, Medtronic, Convatec, Essity (TENA), Kimberly-Clark, Procter & Gamble, Teleflex Incorporated, Hollister Incorporated |

| Segments | Shares % |

| Urinary Catheters | 42% |

| Vaginal Slings | 24% |

| Electrical Stimulation Devices | 14% |

| Artificial Urinary Sphincters | 12% |

| Other Devices | 8% |

Which Product Dominated the Urinary Incontinence Devices Market in 2025?

With the largest share of 42%, the urinary catheters segment led the market in 2025. The increasing cases of diabetes, obesity, spinal cord injuries, and Benign Prostatic Hyperplasia (BPH) are resulting in urinary dysfunction and further demand for this product. The current era is focusing on groundbreaking research in silver-coated and antimicrobial-impregnated catheters as well as Female External Catheters (FECs), like the Coloplast Luja and C.R. Bard Purewick systems.

Artificial Urinary Sphincters

Moreover, the artificial urinary sphincters segment is anticipated to witness rapid expansion. They prominently provide a definitive solution for patients with severe stress incontinence, especially men with sphincter damage post-prostatectomy, after medications and other therapies fail. Researchers are leveraging electronic, remote-controlled, and adaptive devices for boosting functionality and lowering complications, such as urethral erosion. E.g., VICTO and VICTO+ are adjustable hydraulic AUS that can be fine-tuned post-operatively in a clinical setting via an injection port.

| Segments | Shares % |

| External Urinary Incontinence Devices | 58% |

| Internal Urinary Incontinence Devices | 42% |

Why did the External Urinary Incontinence Devices Segment Lead the Market in 2025?

In 2025, the external urinary incontinence devices segment captured a dominant share of 58% of the urinary incontinence devices market & estimated to sustain its dominance. A prominent catalyst is a rise in emphasis on comfort, with lowered infection risks (CAUTIs), optimised design with skin-friendly materials, and integration of digital health technologies. Specifically, the PureWick System (BD) employs gentle vacuum suction and a soft, wicking material placed externally at the vulva to draw urine away from the skin into a collection container.

Internal Urinary Incontinence Devices

In the coming era, the internal urinary incontinence devices segment will expand rapidly. They mainly encompass vaginal slings, artificial urinary sphincters (AUS), urethral inserts, and catheters. A growing effort into minimally invasive and technology integrations includes Bulkamid Urethral Bulking Agent, a water-based gel, delivered via minimally invasive injections into the urethral wall. It is also an easy, long-lasting treatment alternative for SUI in women.

| Segments | Shares % |

| Overflow Urinary Incontinence | 35% |

| Stress Urinary Incontinence | 30% |

| Urge Urinary Incontinence | 22% |

| Functional Urinary Incontinence | 13% |

Which Incontinence Type Led the Urinary Incontinence Devices Market in 2025?

The overflow urinary incontinence segment held the biggest share of 35% of the market in 2025. Mainly, aged people and those with diabetes or neurological conditions are more susceptible to overflow incontinence, which further needs advanced devices. Ongoing breakthroughs in neuromodulation devices, including Medtronic and Axonics, unveiled smaller, rechargeable, and full-body MRI-compatible implantable pulse generators (IPGs), like the AxonicsR15 and Medtronic InterStim Micro.

| Segments | Shares % |

| Hospitals | 55% |

| Clinics | 30% |

| Other | 15% |

How did the Hospitals Segment Dominate the Market in 2025?

The hospitals segment captured the largest share of the urinary incontinence devices market by 55% share in 2025. They primarily offer to maintain skin integrity, minimising the risk of incontinence-associated dermatitis (IAD) and pressure ulcers/injuries. By adopting these advanced devices, nurses and caregivers report satisfaction, with minimal workload connected with often pad changes and linen handling, clearing time for other vital care needs.

Clinics

In the upcoming years, the clinics segment is predicted to expand fastest. Substantial benefits of devices in clinics are immediate symptom relief, enhanced quality of life, and regained confidence for patients. Also, they provide tailored treatment, which enables fine-tuning of therapy. Top clinics like the Cleveland Clinic Glickman Urological & Kidney Institute and the Mayo Clinic, Rochester, are widely using these solutions.

")

In 2025, North America was dominant in the market by 40% share due to the presence of robust healthcare systems, specialized clinics, and supportive reimbursement policies. Also, they are accelerating new FDA approvals for implantable neuromodulation systems and the progression of smart, home-use devices.

For instance,

U.S. Market Trends

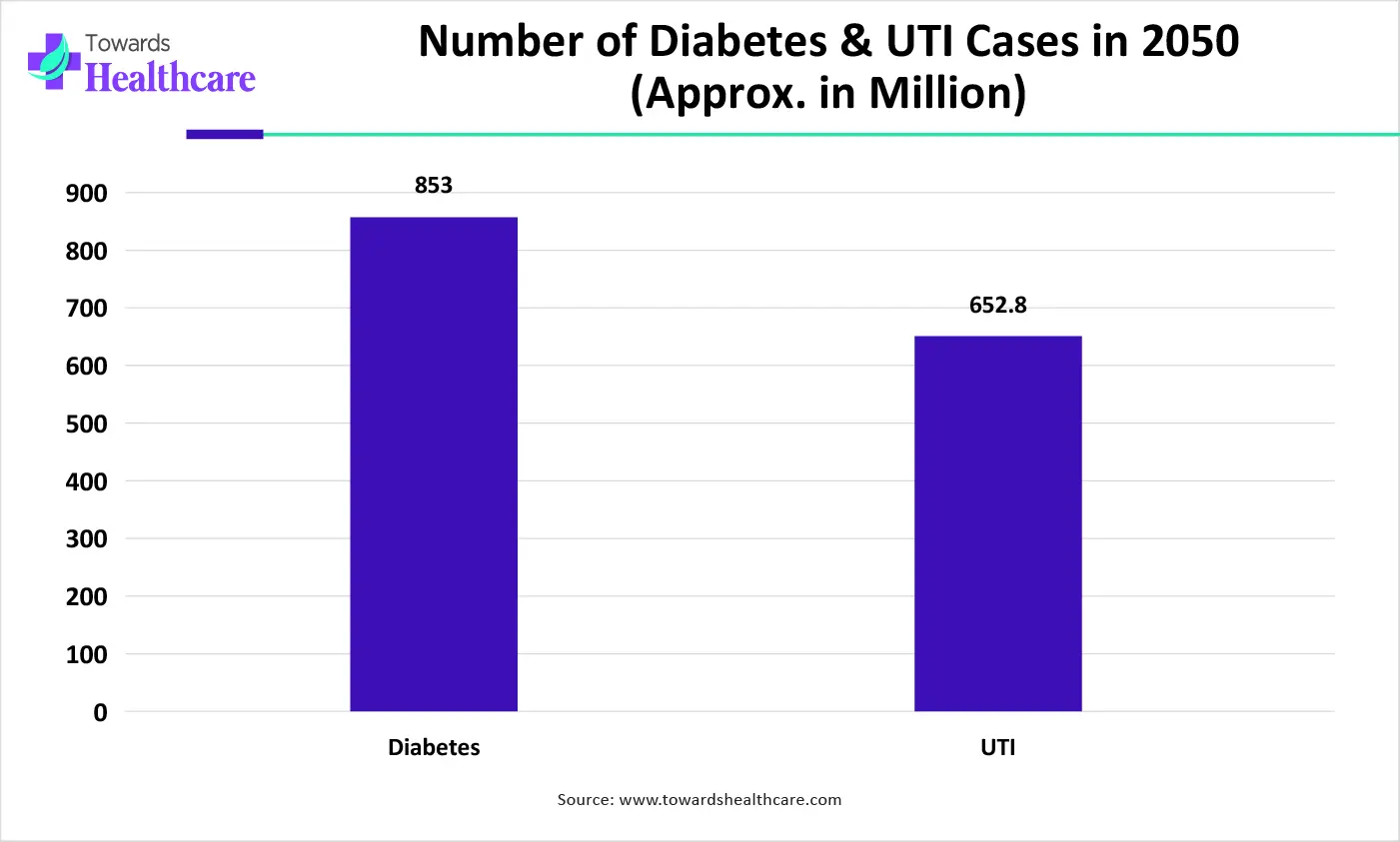

According to the ADA, in the U.S., there are 1.2 million new diabetes cases per year, and other neurological disorder instances are encouraging the development of urinary incontinence devices.

For instance,

Canada Advances Innovation in Urinary Incontinence Care

The Canada urinary incontinence devices market is growing due to the rising aging population, increasing prevalence of urinary incontinence, neurological disorders, and greater awareness of bladder health. Strong healthcare infrastructure, favorable reimbursement policies, and expanding adoption of minimally invasive therapies and neuromodulation devices are devices and driving demand. Continuous technological advancements, increasing home healthcare adoption, and growing investments in patient-centric continence care solutions are further supporting market expansion.

During 2026-2035, the Asia Pacific is predicted to expand fastest in the urinary incontinence devices market, with rising public understanding, due to 150 million UTI cases annually and minimal stigma, leveraging diagnosis and product adoption. However, they are pushing the development of more sustainable, reusable incontinence products, like washable pants with absorbent liners, to highlight environmental issues among consumers.

Whereas, China will expand at a rapid CAGR with increased study on evidence-based auriculotherapy (ear acupuncture points) as a complementary method for UI management in China, using techniques, especially ear plasters. China is a hub for developing a variety of smart wearables, apps for home rehab (WeChat), and advanced implants/stimulation.

")

In India urinary incontinence devices market is growing due to the increasing prevalence of urinary incontinence, a rapidly aging population, and rising cases of diabetes, obesity, and neurological disorders. Growing awareness of bladder health, improving infrastructure, expanding availability of advanced continence care devices are increasing adoption of home healthcare solutions, driving demand. Additionally, rising healthcare expenditure and domestic medical device manufacturing are supporting sustained market growth.

With notable growth, Europe is exploring various advances in the urinary incontinence devices market. This covers the recently published amending Regulation (EU 2025/1234), which enables electronic Instructions For Use (eIFUs) for all professional-use medical devices, including specific types of incontinence devices.

For instance,

Germany is focusing on progressing eco-friendly, sustainable, and washable incontinence products. Like, inContAlert, a Bayern, Germany-based startup is contributing to designing a wearable device by using a patented sensor and AI technology to measure bladder filling levels.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Medtronic, Boston Scientific | Develop neuromodulation, implantable stimulation, and surgical systems |

| Product Manufacturers | Coloplast, Convatec, BD, B. Braun | Produce catheters, slings, intermittent catheter systems, drainage solutions |

| Service Providers | Hospital networks, urology clinics | Deliver surgical implantation and long-term patient management |

| Platform Providers | Medtronic, Boston Scientific | Provide integrated neuromodulation ecosystems and digital monitoring platforms |

| CROs/CDMOs | Limited relevance | Minimal direct role in device manufacturing ecosystem |

| Software Vendors | Laborie | Urodynamic testing systems and diagnostic software for bladder function |

| Research Institutions | Academic urology centers | Clinical validation of pelvic floor therapies and neuromodulation |

| End-User Industries | Healthcare providers, home care | Use devices for chronic management and surgical intervention |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 69% | 22% | 9% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Coloplast | Humlebæk | Denmark | Global leader in continence care and urology devices with strong catheter and pelvic health portfolio | Intermittent catheters, male external catheters, pelvic floor solutions |

| Boston Scientific | Marlborough, Massachusetts | USA | Major player in sacral neuromodulation and minimally invasive incontinence therapies | InterStim neuromodulation system, urinary incontinence surgical devices |

| Medtronic | Dublin | Ireland | Pioneer in neuromodulation for bladder control disorders | InterStim therapy systems for urge incontinence and overactive bladder |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Hollister Incorporated | Libertyville, Illinois | USA | Strong continence care specialist with focus on long-term catheter users | Intermittent catheters, external urinary collection systems |

| Teleflex | Wayne, Pennsylvania | USA | Provides urology-focused catheter systems and hospital-based urinary care devices | Rüsch catheters, urinary drainage solutions |

| B. Braun Melsungen | Melsungen, Hesse | Germany | Broad medical device company with strong urology catheter portfolio | Urinary catheters, drainage systems, infection prevention devices |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| UroMems | Grenoble | France | Innovator in smart implantable artificial urinary sphincter technology | UroActive implantable continence control system |

| Atlantic Therapeutics | Galway | Ireland | Developer of non-invasive electrical stimulation for pelvic floor strengthening | INNOVO pelvic floor electrical stimulation device |

Strength

Weakness

Opportunity

Threats

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

By Product

By Category

By Incontinence Type

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar